Skin Tears Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

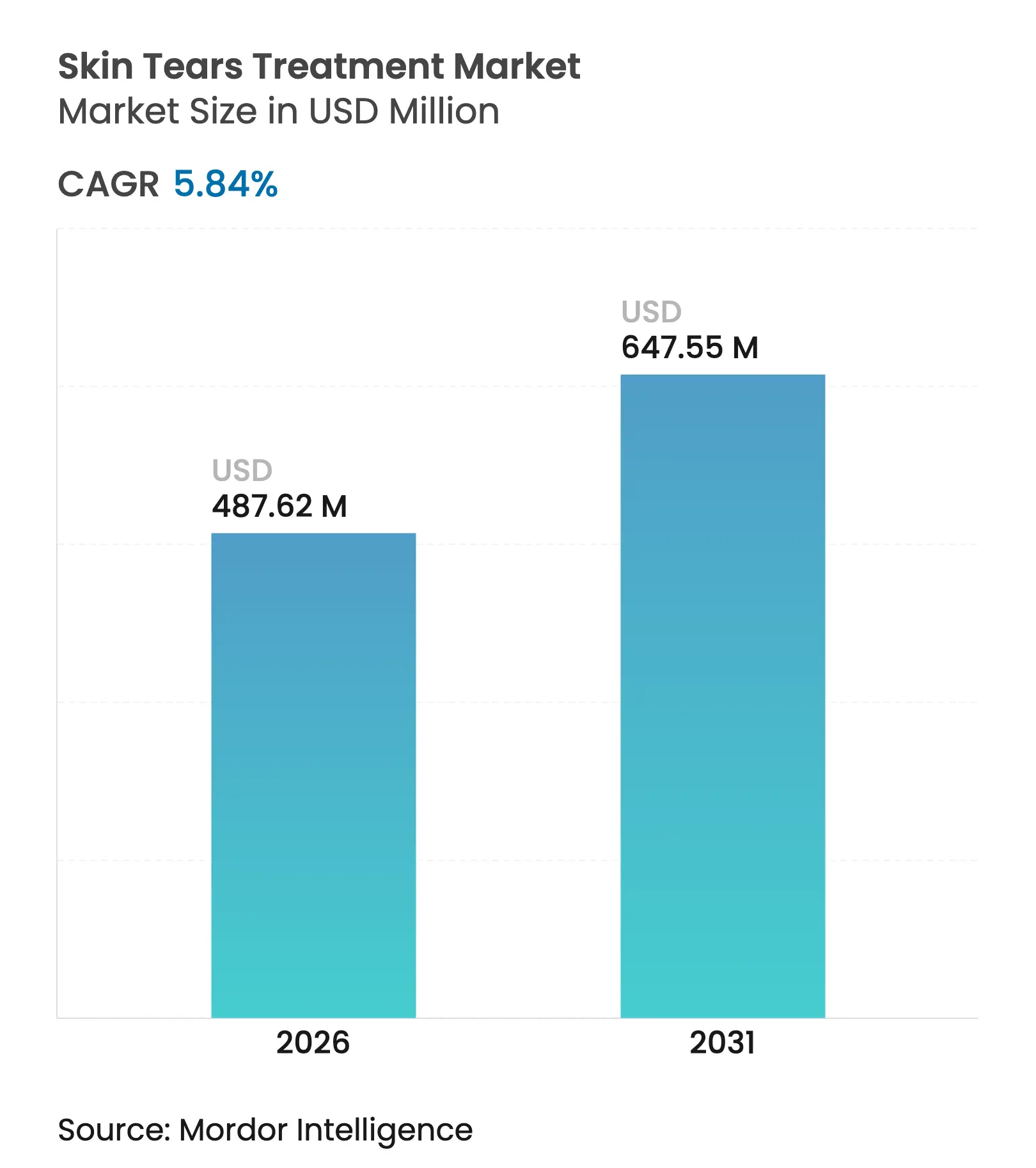

| Market Size (2026) | USD 487.62 Million |

| Market Size (2031) | USD 647.55 Million |

| Growth Rate (2026 - 2031) | 5.84 % CAGR |

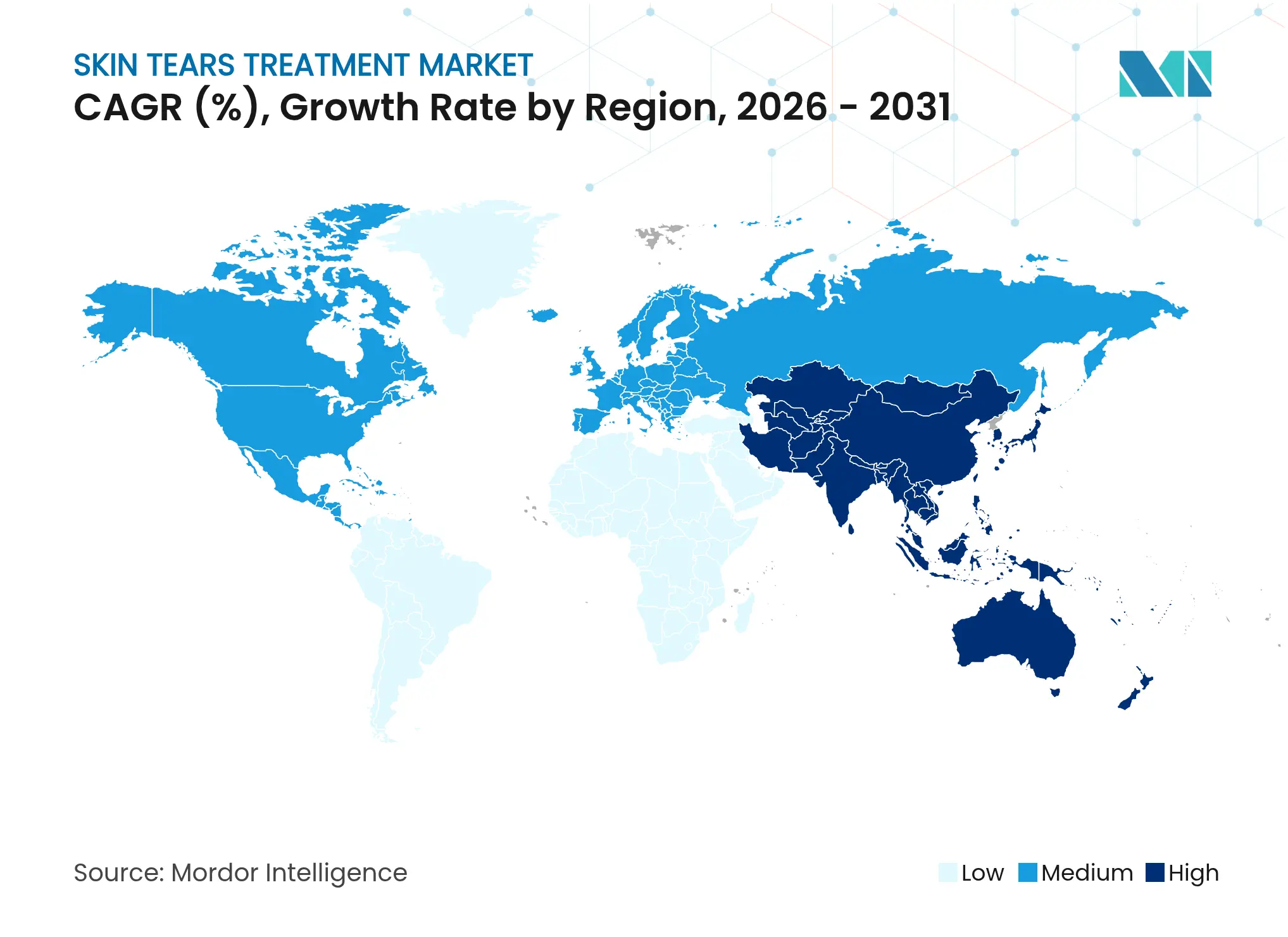

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Skin Tears Treatment Market Analysis by Mordor Intelligence

The skin tears treatment market size is expected to grow from USD 460.71 million in 2025 to USD 487.62 million in 2026 and is forecast to reach USD 647.55 million by 2031 at 5.84% CAGR over 2026-2031. Growth rests on the rapid expansion of the ≥65-year population, wider reimbursement for advanced dressings, and the adoption of AI-enabled wound assessment tools. Rising diabetes prevalence increases the complexity and frequency of wounds, pushing demand for bioactive dressings that moderate inflammation and speed closure. The shift from gauze to silicone-adhesive dressings limits trauma during changes and cuts healing time, while single-use negative-pressure wound therapy (NPWT) kits extend sophisticated care into home settings. Supply chain risks for medical-grade silicone and hyaluronic acid components persist, yet manufacturers are mitigating disruption through dual-sourcing and localized production.

Key Report Takeaways

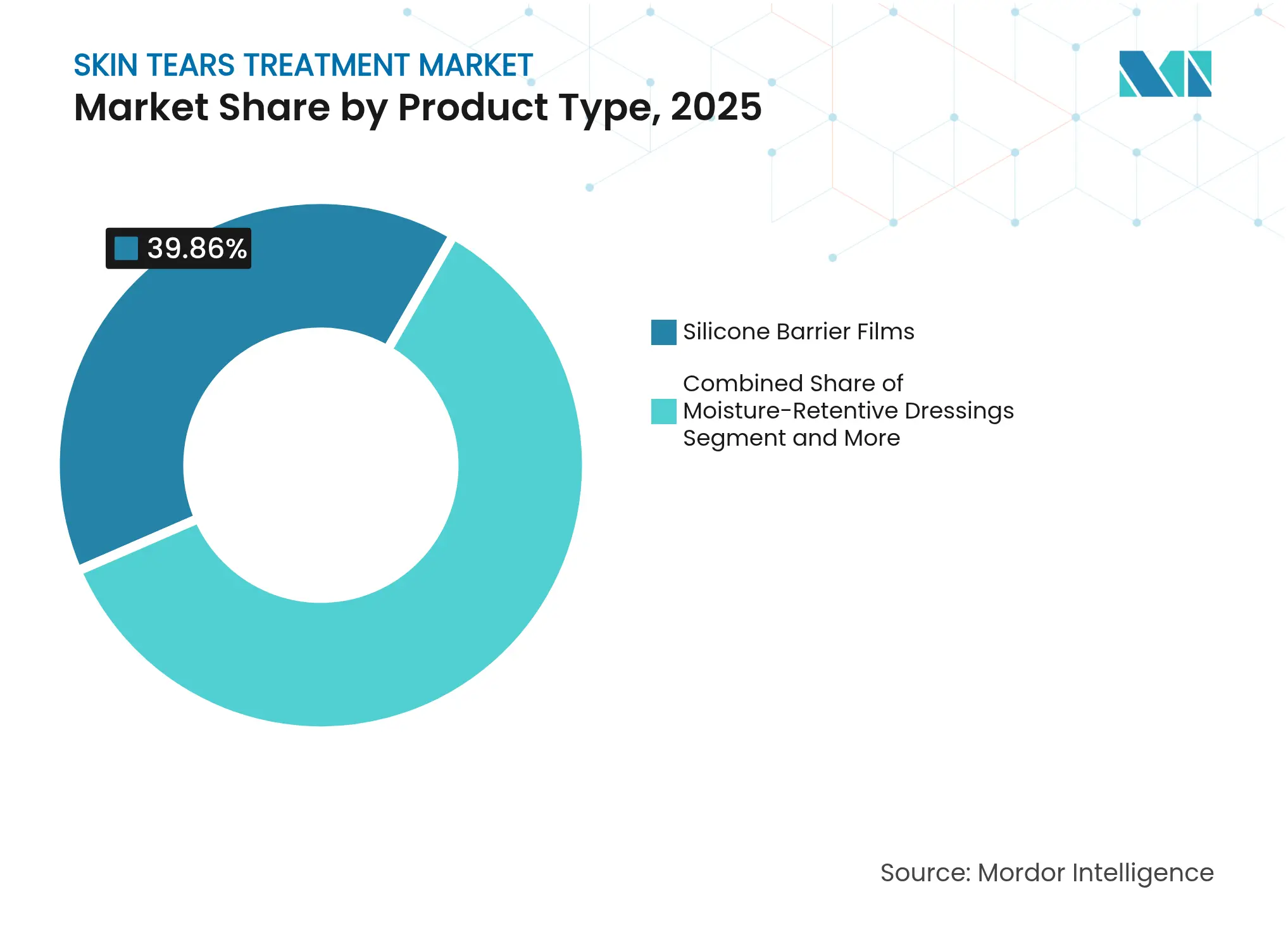

- By product type, silicone barrier films led with a 39.86% revenue share in 2025; NPWT kits are forecast to post the fastest 10.49% CAGR through 2031.

- By end-user, hospitals and clinics held 57.74% share in 2025; home-care settings are projected to grow at 11.43% CAGR to 2031.

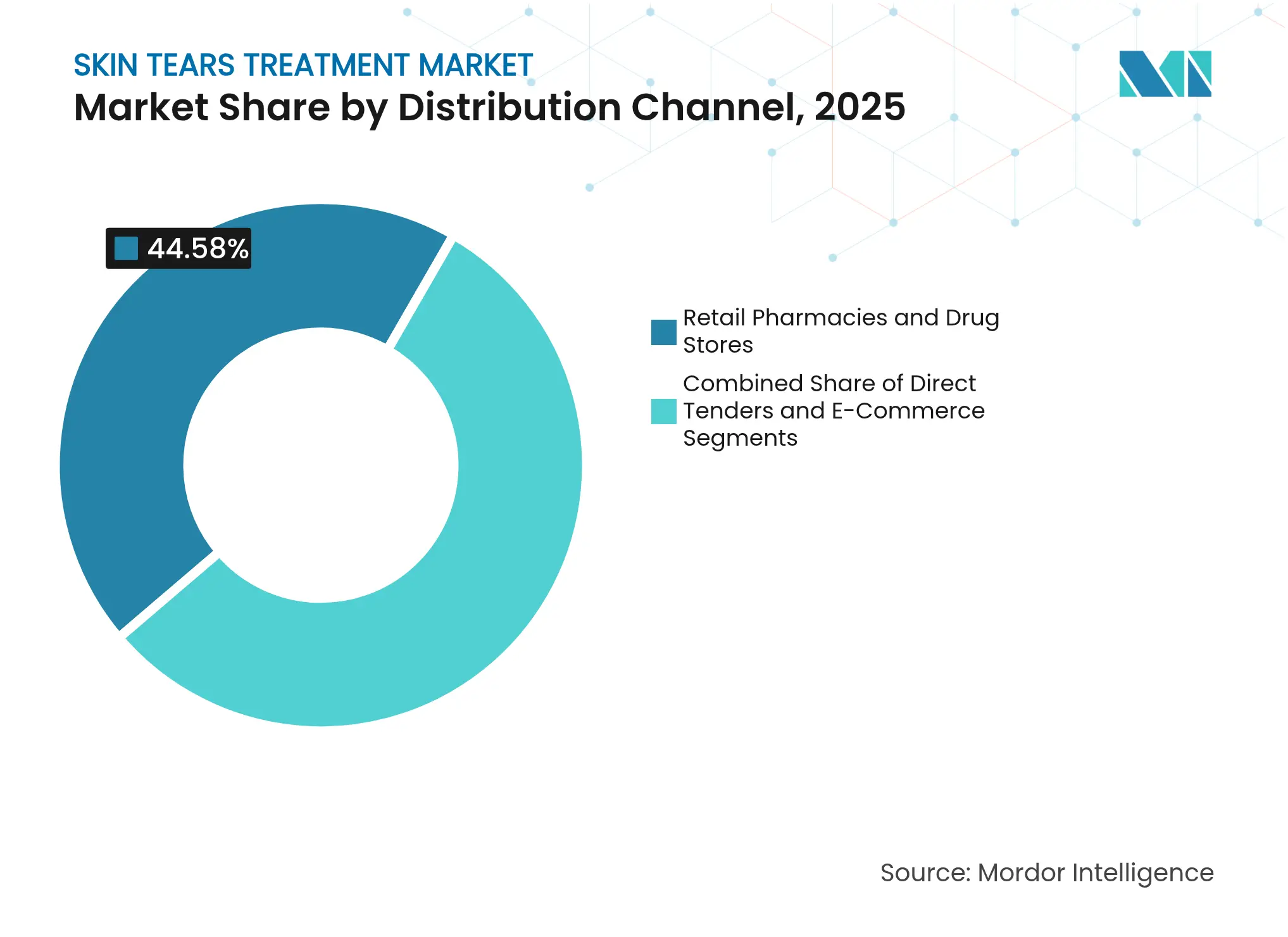

- By distribution channel, retail pharmacies & drug stores captured 44.58% of market size in 2025, whereas e-commerce is advancing at 10.55% CAGR through 2031.

- By geography, North America captured 41.95% share in 2025; Asia-Pacific is expected to expand at 10.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Skin Tears Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid increase in ≥65-year global population

Rapid increase in ≥65-year global population

| +1.8% | North America, Europe, Japan | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.8%

| Geographic Relevance:

North America, Europe, Japan

| Impact Timeline:

Long term (≥ 4 years)

|

Rising prevalence of diabetes-related tears

Rising prevalence of diabetes-related tears

| +1.2% | North America, emerging Asia-Pacific | Medium term (2-4 years) | |||

Shift from gauze to silicone dressings

Shift from gauze to silicone dressings

| +0.9% | North America, Europe, growing Asia-Pacific | Short term (≤ 2 years) | |||

Reimbursement expansion for advanced therapy

Reimbursement expansion for advanced therapy

| +0.7% | United States, selected EU markets | Medium term (2-4 years) | |||

Single-use NPWT adoption in home-care

Single-use NPWT adoption in home-care

| +0.6% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) | |||

AI-based image analytics for early detection

AI-based image analytics for early detection

| +0.4% | North America, Europe, Japan, urban China | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Increase in the ≥65-Year Global Population

Adults aged 65 and older experience dermal thinning and reduced collagen that heighten tear risk, making them core users of modern dressings[1]Pennsylvania Patient Safety Authority, “Skin Tears: The Clinical Challenge Advisory,” patientsafety.pa.gov. Eight in ten older adults take medications that further weaken skin, magnifying the vulnerability. Health systems are responding with tele-monitoring programs capable of flagging early skin compromise, reflecting recognition that clinic capacity cannot meet rising volume. AI smartphone apps that evaluate wound images help caregivers intervene before a tear reaches full thickness, reducing emergency admissions. With older adults already accounting for 2% of all inpatient skin tear reports in Pennsylvania, demographic aging guarantees persistent demand for specialized solutions through 2030.

Rising Prevalence of Diabetes-Related Skin Tears

Diabetes affects microcirculation and prolongs inflammation, causing wounds to heal 50% slower than normal and increasing tear severity. Innovative bioactive dressings now respond to high glucose or inflammatory markers, shifting care from passive coverage to active modulation. Microneedle arrays developed in Singapore deliver interleukin-4 or extract pro-inflammatory compounds, shrinking wound area and improving re-epithelialization in preclinical studies. Hospitals embed these tools in diabetic foot protocols to avert lower-limb amputations and trim the USD 33 billion annual U.S. burden of chronic wound care. Demand for such advanced modalities pushes the skin tears treatment market deeper into endocrinology and primary-care workflows.

Shift from Traditional Gauze to Silicone-Adhesive Dressings

Silicone dressings lower removal-pain scores by 60% and prevent secondary trauma, aligning with patient-centered care targets. Clinician surveys in 2024 found 97% rated silicone foam performance as equal or better than legacy products. Cost-effectiveness studies revealed 29% total savings once shorter healing times and fewer nurse visits were considered, countering the perception that silicone films are expensive. Medical-grade silicones also facilitate sterilization and enable drug-eluted formats, broadening therapeutic options. Health systems are codifying silicone use for high-risk cohorts to avoid medical adhesive-related skin injuries.

Reimbursement Expansion for Advanced Wound Therapies

The 2025 U.S. Medicare Physician Fee Schedule created new codes for caregiver training delivered via telehealth, boosting remote wound support[2]“CY 2025 Medicare PFS Final Rule: Essential Updates for Wound Care Professionals,” WoundReference, woundreference.com. Local Coverage Determinations now permit up to eight applications of skin substitutes within 16 weeks if standard care fails to halve wound area in four weeks. National pricing for blood-derived products and updated physician payment for complex procedures reduce financial barriers, spurring adoption of cellular matrices and collagen scaffolds. Europe is following with pilot tariffs that reward documented healing outcomes, making evidence generation a strategic imperative.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shortage of certified wound-care nurses

Shortage of certified wound-care nurses

| -0.8% | Rural North America, EU periphery, developing APAC | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-0.8%

| Geographic Relevance:

Rural North America, EU periphery, developing APAC

| Impact Timeline:

Medium term (2-4 years)

|

High unit cost of advanced barrier films

High unit cost of advanced barrier films

| -0.6% | Price-sensitive markets worldwide | Short term (≤ 2 years) | |||

Low clinician awareness in SE Asia & Africa

Low clinician awareness in SE Asia & Africa

| -0.5% | SE Asia, Sub-Saharan Africa, rural Latin America | Long term (≥ 4 years) | |||

Supply-chain fragility for silicone & HA

Supply-chain fragility for silicone & HA

| -0.4% | Global | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Shortage of Certified Wound-Care Nurses in Rural Settings

Specialists migrate toward urban centers, leaving rural facilities dependent on generalist staff for complex wounds[3]Center for Devices and Radiological Health, “Medical Device Supply Chain Vulnerabilities,” fda.gov. Tele-supervision fills some gaps yet cannot fully replicate hands-on expertise that NPWT systems demand. The International League of Dermatological Societies drafted six wound management principles for low-resource clinics to provide structured guidance when expert staff are absent. AI decision support offers promise but raises concerns about over-reliance on algorithms and erosion of relational care.

High Unit Cost of Advanced Barrier Films Versus Conventional Dressings

Silicone barrier films cost three to five times more per unit than gauze, tightening procurement budgets in capitated payment systems. Total-cost studies document 29% savings via faster healing, yet purchasing teams frequently prioritize sticker price. In emerging economies, reimbursement frameworks seldom cover premium dressings, forcing clinicians to compromise on product choice.

Segment Analysis

By Product Type: NPWT Innovation Drives Market Evolution

Silicone barrier films retained 39.86% of the skin tears treatment market share in 2025 because clinicians value low-trauma removal and reliable adherence. Portable NPWT kits are the fastest advancing segment at 10.49% CAGR, reflecting design improvements that permit home initiation without specialist oversight.

Growth of NPWT stems from embedded sensors that adjust negative pressure to exudate volumes, optimizing granulation while conserving battery life. Antimicrobial-impregnated foams address infection risk, and hyaluronic acid devices extend into tissue engineering, widening clinical indications. Collagen and cellular matrices benefit from expanded Medicare coverage that allows eight applications per course, encouraging hospital formularies to stock them. Gels and creams persist as adjuncts, though uptake slows as multifunctional dressings with sustained release gain ground. Continuous innovation keeps the skin tears treatment market dynamic and prevents rapid commoditization.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Home-Care Transformation Reshapes Delivery Models

Hospitals and clinics accounted for 57.74% of overall revenue in 2025, yet home-care settings are forecast to expand at 11.43% CAGR, narrowing the gap by 2031. The skin tears treatment market size for home use benefits from insurance coverage of remote nurse visits combined with patient preference to avoid institutional stays.

Solventum’s eight-layer extended-wear dressing reduces application time 61% and remains intact for seven days, lessening caregiver burden and readmissions. Ambulatory surgical centers leverage same-day discharge protocols, shifting complex wounds into community follow-up. Long-term care facilities adopt standardized protocols to balance cost and quality, while humanitarian medical posts need shelf-stable products tolerating temperature swings. Tele-consultation platforms support dispersed caregivers with AI-scored wound images, underpinning safe decentralization of advanced therapy.

By Distribution Channel: E-Commerce Disrupts Traditional Models

Retail pharmacies held 44.58% channel revenue in 2025 thanks to walk-in convenience and pharmacist counseling. However, e-commerce is projected to register a 10.55% CAGR, the highest among channels, as patients favor doorstep delivery of bulky dressings.

Online platforms improve product education through video tutorials and peer reviews, boosting correct self-application. Hybrid models marry central warehousing with local pharmacy pickup, ensuring same-day access when urgent. Direct tenders remain crucial for public hospitals, where group purchasing organizations secure volume discounts and quality standards. Regulatory scrutiny focuses on prescription validation and counterfeit avoidance, shaping platform governance.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America accounted for 41.95% of 2025 revenue, driven by comprehensive reimbursement, interdisciplinary wound centers, and early adoption of AI-enabled assessment tools. Medicare coverage of skin substitutes and telehealth codes for caregiver education lowered economic barriers and spurred technology uptake.

Europe benefits from universal coverage and strict quality regulations that speed diffusion of evidence-based products. Germany and the United Kingdom expanded home-care NPWT reimbursements in 2025, reinforcing community-based protocols. Japan integrates Kampo herbal ointments with silicone dressings, blending tradition and technology for older patients seeking holistic care.

Asia-Pacific delivers the fastest 10.33% CAGR as aging and diabetes converge with expanding insurance coverage. China’s tiered hospital reforms earmark funds for wound management clinics, while India’s private sector scales tele-dermatology to rural areas. The Middle East and Africa show incremental growth limited by workforce shortages and budget constraints, yet targeted education campaigns boost clinician awareness in Gulf Cooperation Council states. Emerging economies collectively broaden the skin tears treatment market, shifting the revenue center of gravity toward the east.

Competitive Landscape

Market Concentration

The market remains moderately fragmented: the top five vendors hold significant global revenue, yielding intense product competition. Smith+Nephew, ConvaTec, and Solventum leverage broad portfolios and direct sales networks to defend share. Smith+Nephew reported 3.8% underlying growth in Advanced Wound Management in Q1 2025 on strong NPWT demand and new silicone foams.

Players pursue vertical integration, bundling dressings, pumps, and cloud analytics into service platforms that guarantee outcomes. ConvaTec delayed Start-ups target AI image analysis and bioengineered scaffolds, partnering with device majors for scale.

Supply chain resilience is a rising differentiator. The FDA’s Office of Supply Chain Resilience highlights raw material vulnerabilities, prompting manufacturers to on-shore critical components or add duplicate suppliers. As procurement teams scrutinize sustainability credentials, companies tout recyclable packaging and reduced carbon footprints to win hospital tenders. Competitive intensity thus spans technology, policy, and ESG arenas.

Skin Tears Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ConvaTec welcomed the postponement of U.S. Local Coverage Determinations on skin substitutes, allowing more stakeholder input.

- November 2024: Hyaluronic acid injectables branded Estyme/Evolysse secured EU Medical Device Regulation certification, expanding advanced biomaterial options.

Table of Contents for Skin Tears Treatment Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rapid Increase In The Greater Than or Equal to 65-Year Global Population

- 4.2.2Rising Prevalence Of Diabetes-Related Skin Tears

- 4.2.3Shift From Traditional Gauze To Silicone-Adhesive Dressings

- 4.2.4Reimbursement Expansion For Advanced Wound Therapies (CMS, NHIF, Etc.)

- 4.2.5Adoption Of Single-Use Negative-Pressure Devices In Home-Care

- 4.2.6Use Of AI-Based Image Analytics For Early Tear Detection

- 4.3Market Restraints

- 4.3.1Shortage Of Certified Wound-Care Nurses In Rural Settings

- 4.3.2High Unit-Cost Of Advanced Barrier Films Vs. Conventional Dressings

- 4.3.3Low Clinician Awareness In South-East Asia & Africa

- 4.3.4Supply-Chain Fragility For Medical-Grade Silicone & HA

- 4.4Porter's Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product Type

- 5.1.1Moisture-Retentive Dressings

- 5.1.2Silicone Barrier Films

- 5.1.3Hyaluronic Acid Wound Devices

- 5.1.4Gels & Creams

- 5.1.5Antimicrobial Impregnated Dressings

- 5.1.6Negative-Pressure Wound Therapy (NPWT) Kits

- 5.1.7Collagen & Cellular Matrix Products

- 5.1.8Others

- 5.2By End-User

- 5.2.1Hospitals & Clinics

- 5.2.2Ambulatory Surgical Centers

- 5.2.3Home-Care Settings

- 5.2.4Long-Term Care Facilities

- 5.2.5Military & Humanitarian Aid Posts

- 5.3By Distribution Channel

- 5.3.1Direct Tenders

- 5.3.2Retail Pharmacies & Drug Stores

- 5.3.3E-Commerce

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Solventum Corporation

- 6.3.2Smith & Nephew plc

- 6.3.3ConvaTec Group plc

- 6.3.4Cardinal Health Inc.

- 6.3.5Medline Industries LP

- 6.3.6Molnlycke Health Care

- 6.3.7Coloplast A/S

- 6.3.8Hollister Inc.

- 6.3.9DermaRite Industries

- 6.3.10Essity AB (BSN medical)

- 6.3.11Acelity (KCI)

- 6.3.12Covalon Technologies Ltd.

- 6.3.13Urgo Medical

- 6.3.14Integra LifeSciences

- 6.3.15Organogenesis Holdings Inc.

- 6.3.16Advanced Medical Solutions Group

- 6.3.17Medaxis AG

- 6.3.18PolyMem (Performance Health)

- 6.3.19Brightwake Ltd.

- 6.3.20Advancis Medical

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Skin Tears Treatment Market Report Scope

Skin tears are wounds that may look like large cuts or scrapes. They're considered acute wounds. This means they occur suddenly and typically heal in an expected fashion over time. However, for some people, skin tears can become complex, chronic wounds. The report covers various types of products associated with the treatment of such skin tears.