Rosacea Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

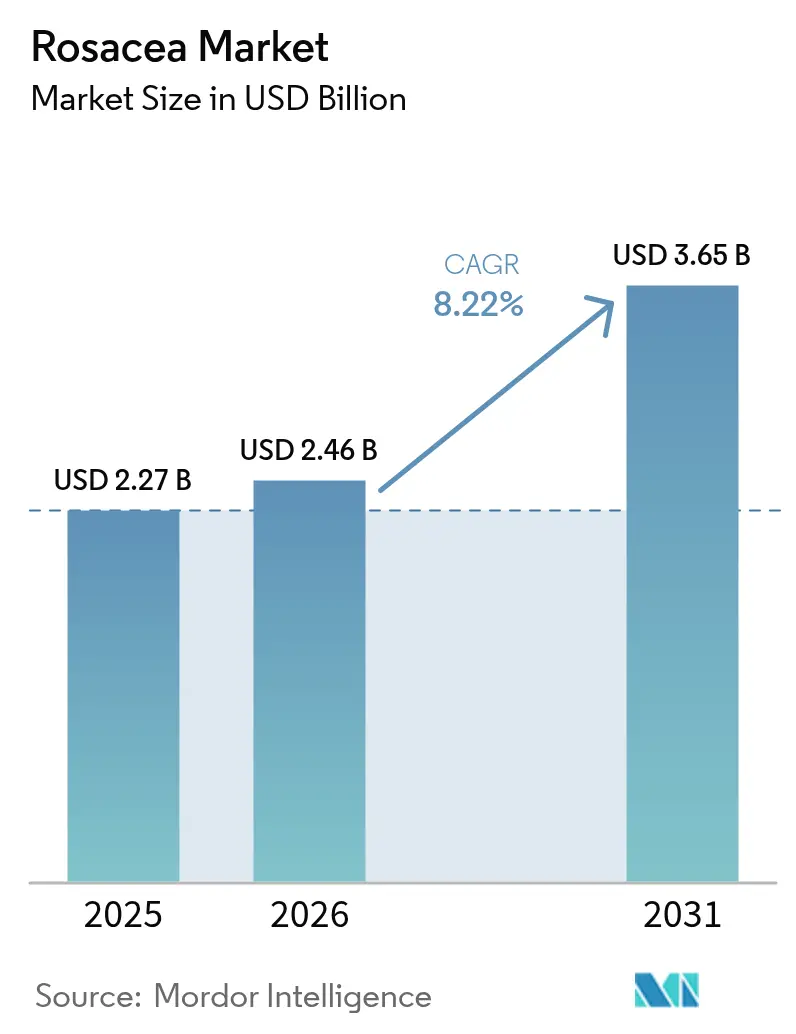

| Market Size (2026) | USD 2.46 Billion |

| Market Size (2031) | USD 3.65 Billion |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

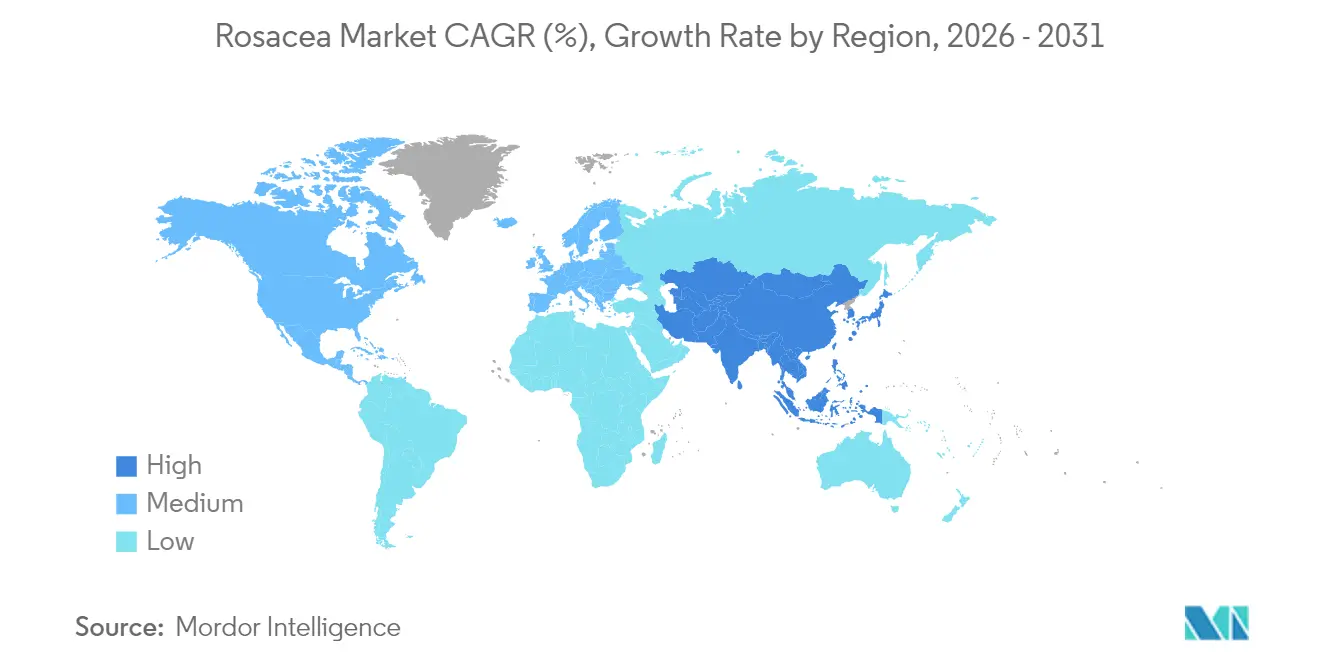

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

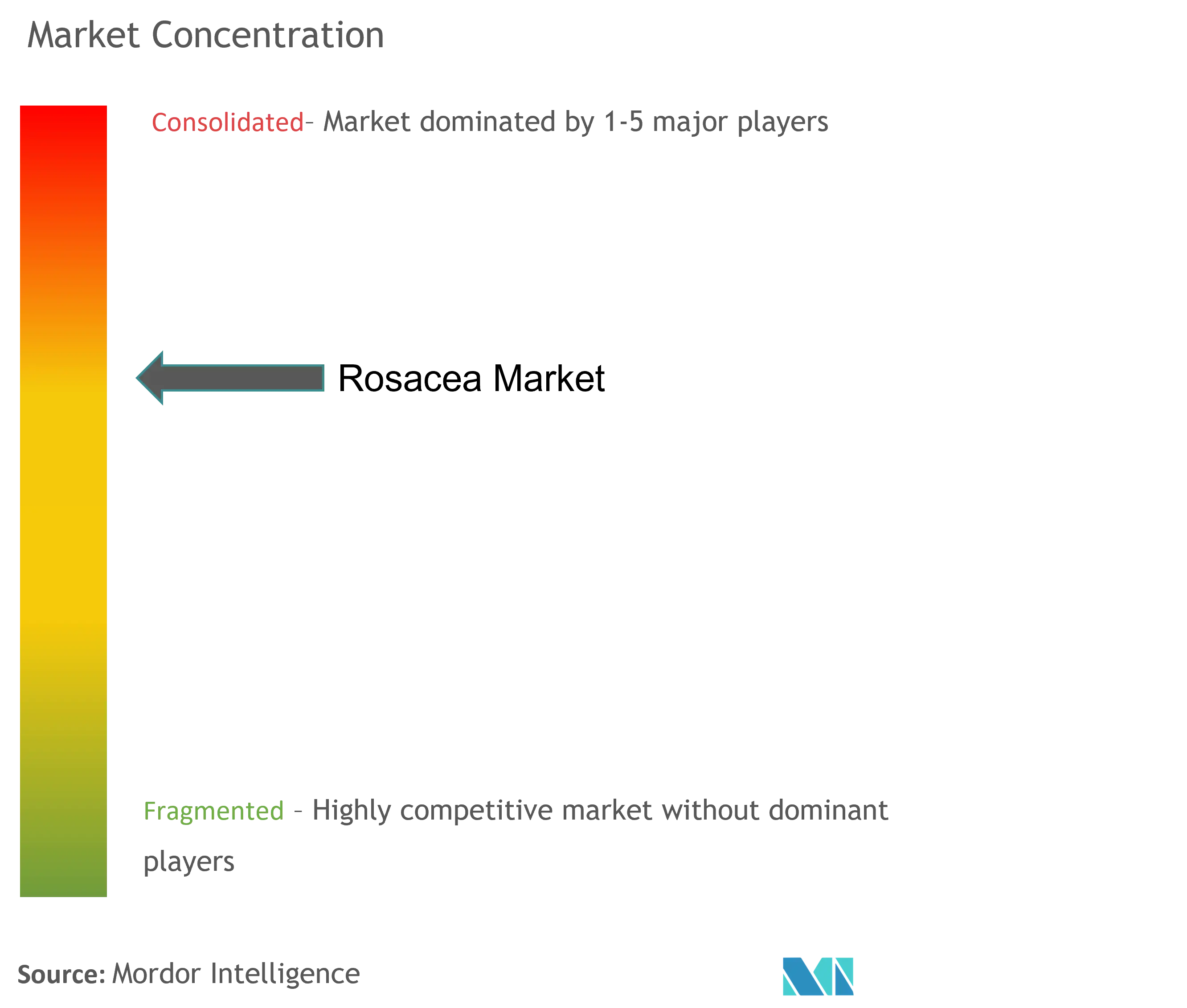

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rosacea Market Analysis by Mordor Intelligence

The rosacea market size was valued at USD 2.27 billion in 2025 and estimated to grow from USD 2.46 billion in 2026 to reach USD 3.65 billion by 2031, at a CAGR of 8.22% during the forecast period (2026-2031). The steady expansion is propelled by breakthrough regulatory approvals, refinements in drug-delivery science, and telehealth-enabled care pathways that emphasize early intervention and long-term adherence. Alpha-adrenergic agonists safeguard their leadership position, while JAK inhibitors gather momentum as precision immunomodulators. Topical therapies still dominate dispensing volumes, yet the first-in-class oral agent Emrosi is shifting prescribing behavior toward systemic convenience. North America anchors global revenue because of robust reimbursement and specialist density, whereas Asia-Pacific provides the fastest incremental growth as dermatology infrastructure and consumer purchasing power mature. Across all regions, digital diagnostics and e-pharmacy logistics compress the distance between diagnosis and therapy initiation, expanding the treated population and supporting sustainable market acceleration.

Key Report Takeaways

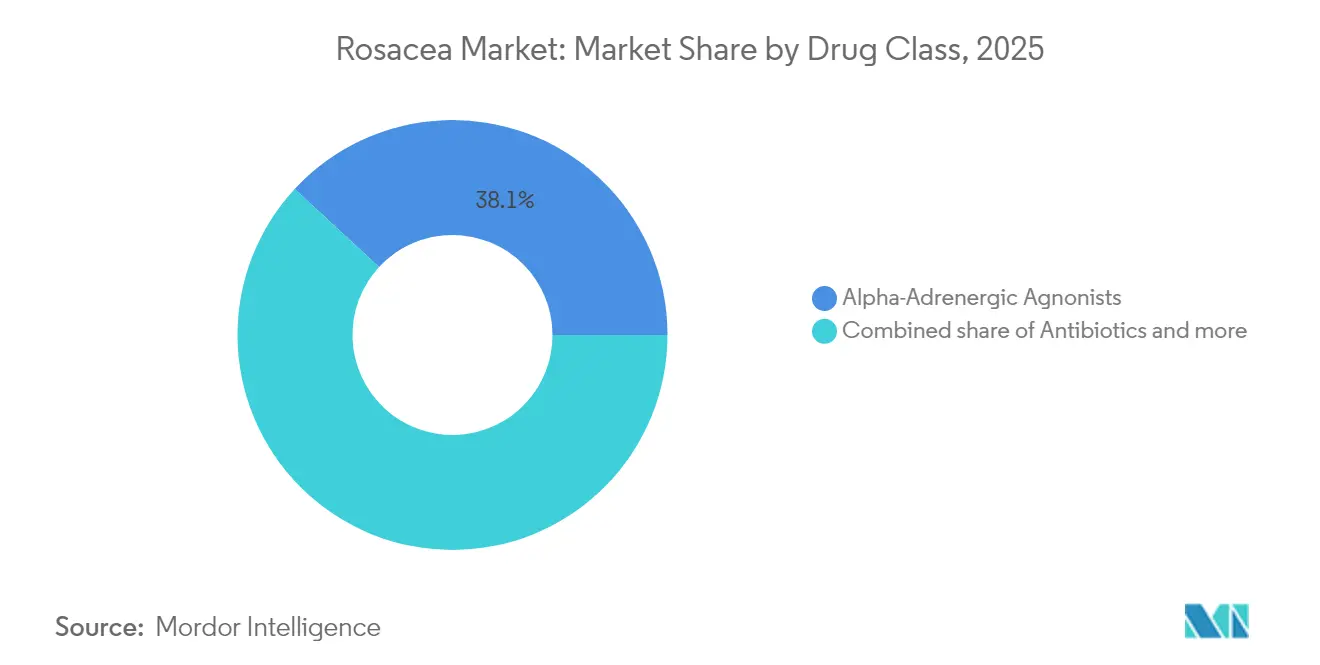

- By drug class, alpha-adrenergic agonists held 38.12% of the rosacea market share in 2025, while JAK inhibitors are projected to expand at a 9.05% CAGR through 2031.

- By route of administration, topical formulations captured 70.75% share of the rosacea market size in 2025, and oral products are advancing at a 9.55% CAGR through 2031.

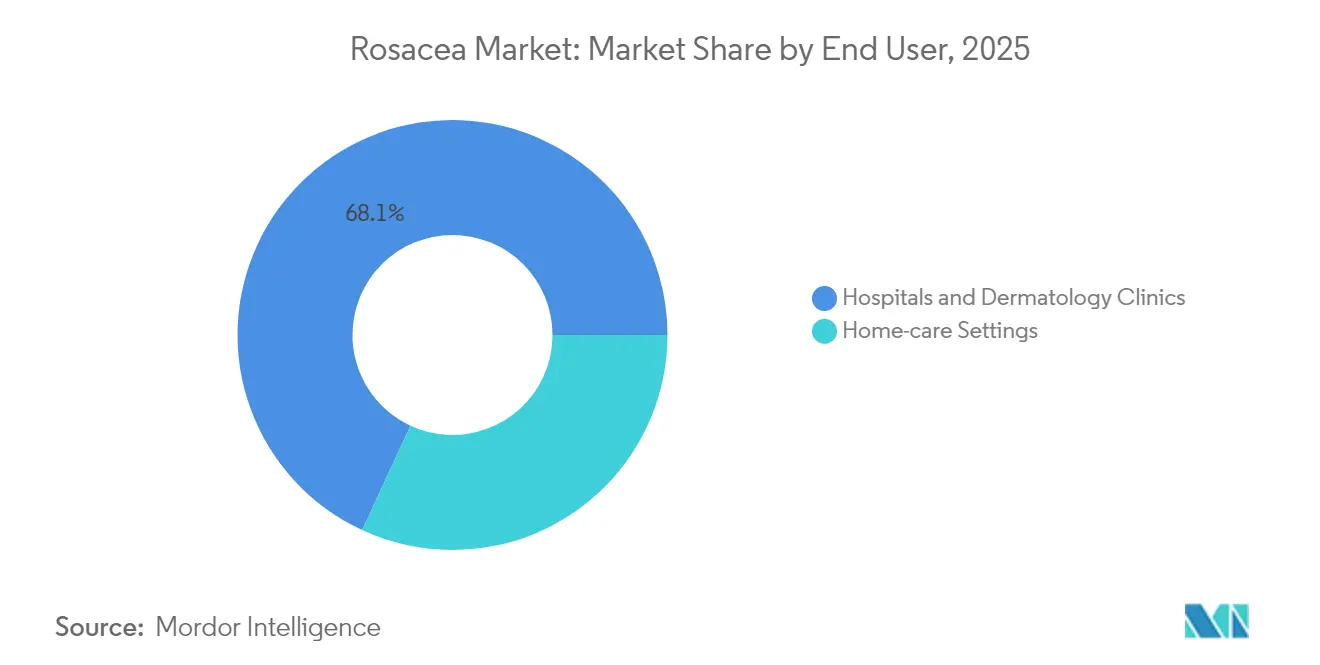

- By end-user facility, hospitals and dermatology clinics accounted for 68.10% of the rosacea market size in 2025; home-care settings are recording the strongest growth at 10.45% CAGR.

- By geography, North America led with 41.85% share of the rosacea market in 2025, whereas Asia-Pacific is forecast to log a 10.01% CAGR to 2031 .

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rosacea Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence among adults 30-60 years | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| FDA approvals of novel topical agents | +1.5% | North America, spillover to Europe & APAC | Short term (≤ 2 years) |

| Growing tele-dermatology & e-pharmacy uptake | +1.2% | Global, accelerated in APAC emerging markets | Medium term (2-4 years) |

| Advances in micro-encapsulated drug delivery | +0.9% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| JAK-inhibitor pipeline targeting immune pathways | +0.8% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| AI-powered diagnostic apps boosting early detection | +0.6% | Global, with rapid uptake in tech-forward regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Among Adults 30-60 Years Drives Demand

Incidence among people aged 30-60 years is climbing, aligning treatment need with peak earning capacity and autonomy in healthcare decision-making. Stress, diet, and environmental exposures in developed regions intensify symptom onset, boosting physician visits and prescription volumes. Patients increasingly recognize rosacea as a medical disorder rather than a cosmetic nuisance, bolstering willingness to pursue chronic pharmacotherapy. The demographic swell ensures a stable base of treatment candidates, underpinning long-range expansion of the rosacea treatment market .

FDA Approvals of Novel Topical Agents Accelerate Innovation

Recent regulatory momentum redefined therapeutic benchmarks. EPSOLAY’s micro-encapsulated benzoyl peroxide achieved near-70% lesion reduction in 12 weeks, validating sustained-release chemistry as a means to marry efficacy with tolerability . Emrosi became the first oral therapy approved for concurrent control of erythema and inflammatory lesions, demonstrating superiority to Oracea yet retaining safety parity. These clearances compress development timelines for next-wave agents and intensify pipeline investment, lifting the innovation baseline across the rosacea industry.

Growing Tele-Dermatology & E-Pharmacy Uptake Transforms Care

Overall telehealth adoption has stabilized at 4-6% of total medical visits in 2024, significantly higher than pre-pandemic levels but down from pandemic peaks. Remote triage suits rosacea’s chronic course by enabling iterative treatment tweaks without office visits. Parallel e-pharmacy expansion integrates prescription fulfillment into the same digital encounter, accelerating therapy start and supporting adherence through doorstep delivery. In Asia-Pacific, smartphone penetration and clinician scarcity amplify the value proposition, making virtual pathways a core growth lever for the rosacea market.

Advances in Micro-Encapsulated Drug Delivery Enhance Efficacy

Micro-encapsulation, lipid-core nanocapsules, and microsponge platforms elevate permeation and sustain dermal concentrations while minimizing irritation. EPSOLAY exemplifies how controlled release can rescue traditional actives—benzoyl peroxide—from tolerability limitations. Research into pH-responsive carriers aims to tailor dose release to facial micro-environments, promising individualized therapy regimens that reinforce adherence and widen the rosacea market’s reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of branded prescriptions | -1.4% | Global, particularly acute in price-sensitive markets | Short term (≤ 2 years) |

| Treatment-related irritation & poor adherence | -1.1% | Global, with variation by treatment type | Medium term (2-4 years) |

| EU micro-plastic rule risk to leave-on gels | -0.8% | Europe, potential spillover to other regions | Medium term (2-4 years) |

| API supply-chain concentration for ivermectin | -0.5% | Global, with regional variation in impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Branded Prescriptions Limits Access

Retail prices for premium branded gels can run between USD 60.90 and USD 152.25 per daily treatment success, burdening patients and insurers alike. Prior authorization hurdles and tiered formularies steer many users toward older generics, capping uptake of innovative agents despite clinical superiority. The financial barrier is most pronounced in emerging economies, dampening the rosacea market expansion potential until cost-containment or differential pricing models gain traction.

Treatment-Related Irritation & Poor Adherence Undermine Outcomes

More than one-third of patients report social stigma yet many abandon topicals due to initial irritation that precedes visible improvement. Chronic disease fatigue compounds the problem, as daily regimens become onerous. Inadequate counseling on managing transient side effects further erodes persistence. Discontinuation not only weakens clinical benefit but suppresses repeat purchasing, tempering the rosacea market growth curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Alpha-Adrenergic Agonists Hold Sway While JAK Inhibitors Rise

Alpha-adrenergic agonists retained 38.12% of rosacea market share in 2025 by rapidly shrinking facial erythema through vasoconstriction. JAK inhibitors, albeit from a smaller base, are logging a 9.05% CAGR as clinical evidence confirms their ability to curb both inflammatory lesions and redness in refractory patients. Antibiotics, especially doxycycline derivatives, preserve utility for papulopustular subtypes, whereas azelaic acid persists as a dual-action topical for mild cases. Ivermectin remains resilient but relies on a concentrated API supply chain that could expose the segment to volatility. Benzoyl peroxide re-enters clinician armamentaria under micro-encapsulated designs that override historical tolerability barriers. Competitive positioning therefore revolves around combining mechanistic complementarity with advanced carriers that secure patient comfort.

The rosacea market size for alpha-adrenergic agonists is forecast to advance steadily, yet their rosacea market share could cede ground if JAK inhibitors achieve broader label indications. Pipeline diversity favors combination products that harness rapid vasoconstriction with immunomodulation, promising step-down strategies that prolong remission. Branded incumbents counter this threat by investing in lifecycle extensions such as lower-concentration formulations and patient-friendly applicators. Collectively, drug-class competition illustrates a pivot toward precision targeting over blanket anti-inflammation, a trajectory that redefines therapy algorithms and invites new entrants.

By Route of Administration: Topicals Dominate, Orals Accelerate

Topicals delivered 70.75% of 2025 revenue owing to familiarity, minimal systemic exposure, and immediate perception of action. Nano-carrier and sustained-release science extends residence time, cutting application frequency and enhancing cosmetic elegance. However, the oral category is charting a 9.55% CAGR, the fastest among routes, after Emrosi showed that systemic convenience can coexist with dual-symptom efficacy. Patients juggling multiple skincare steps favor once-daily capsules that eliminate the guesswork of layered topicals.

Injectable modalities occupy niche use in severe telangiectatic subtypes but remain commercially marginal. Looking forward, the rosacea market size for oral therapies could widen if additional molecules clear safety and efficacy thresholds, eroding topical hegemony. Manufacturers attempt to preserve topical leadership through user-centric packaging, fragrance-free vehicles, and digital adherence reminders. Route diversification ultimately enlarges the overall rosacea market by aligning formulation style with individual lifestyle and disease burden.

By End-User Facility: Clinical Settings Rule, Home-Care Takes Off

Hospitals and dermatology clinics accounted for 68.10% of dispensing in 2025 because initial diagnosis and therapy customization demand expert oversight. Professional environments facilitate differential diagnosis between rosacea, acne, and seborrheic dermatitis, limiting mis-prescribing. Yet home-care settings are advancing at 10.45% CAGR as telemedicine follow-ups and e-pharmacy fulfillment empower patients to manage maintenance phases independently.

The rosacea market size linked to home-care is poised to rise as AI-guided smartphone checks flag flare-ups early and route patients back to specialists only when thresholds are breached. Device makers integrate UV, temperature, and humidity sensors into home mirrors to correlate triggers with symptom spikes, reinforcing self-management confidence. Clinics respond by bundling digital subscriptions with prescription refills, sustaining revenue while easing chair time pressure. The end-user mix therefore tilts toward decentralized models without undermining the pivotal diagnostic role of dermatologists.

Geography Analysis

North America held 41.85% rosacea market share in 2025 on the back of insurance coverage and physician density. FDA agility in green-lighting novel entities such as EPSOLAY and Emrosi further cements the region as the launchpad for global rollouts . Europe delivers steady gains amid stringent but harmonized regulation; the new EU micro-plastic directive may, however, nudge reformulation costs for certain leave-on gels. Asia-Pacific exhibits a 10.01% CAGR through 2031 as urban consumers adopt dermatology services and telehealth bridges rural access gaps. South America and the Middle East & Africa are earlier-stage but move in tandem with rising specialist training programs and public education drives.

The rosacea market size differential favors regions with reimbursement support, yet sheer population weight positions Asia-Pacific as the dominant long-run volume engine. Western companies court the region via strategic licensing that pairs novel molecules with local distribution prowess. Domestic generics producers, meanwhile, capture cost-sensitive segments, intensifying price competition. Exchange-rate trends, regulatory review pace, and digital infrastructure maturity will dictate regional trajectory interplay over the forecast window.

In Europe, national health technology assessments influence time-to-market, compelling manufacturers to compile robust real-world evidence beyond pivotal trials. This requirement could delay uptake but ultimately fortifies retention through proven cost-utility. Latin American markets lean on public–private partnerships to seed dermatology capacity, offering multinationals pilot grounds for subscription-based care models. The evolving geography matrix thus blends mature profitability in North America with emerging-market scale upside, collectively fueling a resilient rosacea market.

Regulatory Landscape

Rosacea therapeutics operate under mature drug-approval and manufacturing frameworks led by the US FDA (CDER) and the European regulatory system (European Commission/EMA). A key recent anchor is the FDA approval of Journey Medicals Emrosi (minocycline hydrochloride 40 mg extended-release capsules) in November 2024 for inflammatory lesions of rosacea in adults, which keeps the emphasis on robust pivotal evidence for clinically meaningful endpoints and on post-approval pharmacovigilance.

In Europe, access pathways combine EMA scientific standards with country-level market access processes, and lifecycle changes to established products increasingly flow through structured variation procedures. The EMA variations framework update that became applicable in January 2025 adds operational emphasis on compliant change-management for authorized products, which is relevant as manufacturers pursue formulation and label updates for topical and oral therapies across multiple markets. Health Canada continues to publish Summary Basis of Decision (SBD) documentation for approved therapies, reinforcing the role of transparent benefit-risk and quality requirements in market authorization.

Value Chain Analysis

The rosacea value chain spans discovery and clinical development, regulatory filing, API and excipient sourcing, drug product manufacturing (often via contract manufacturers for specialty players), and distribution through retail pharmacies, e-pharmacies, and clinic dispensing. The FDA DailyMed system provides a practical view of downstream execution: Emrosi labeling remained active in April 2025 and Oracea (doxycycline) received an FDA label update in April 2025, underscoring the ongoing compliance, labeling, and supply readiness work between approval and sustained commercialization.

On the supply side, the market relies on a mix of long-established actives (tetracyclines, azelaic acid, ivermectin) and newer delivery platforms such as micro-encapsulation, which require specialized formulation know-how and quality controls. Commercial scale-up and reach are reinforced by partnerships and rights-based models, with branded players and technology-focused developers (for example, Galderma, Sol-Gel, Journey Medical, AbbVie, and Bausch Health) using alliances and outsourced manufacturing to shorten the path from regulatory clearance to broad channel availability, including digitally enabled fulfillment.

Competitive Landscape

The rosacea industry remains moderately fragmented despite portfolio breadth among leaders Galderma, Bausch Health, and AbbVie. Collective share held by the top five players hovers near 45%, leaving room for nimble entrants exploiting delivery-tech niches. Partnerships dominate strategy: Galderma’s alliance with Sol-Gel secured exclusive U.S. rights to micro-encapsulated benzoyl peroxide, illustrating cooperative acceleration of formulation innovation. Journey Medical leveraged contract manufacturing to fast-track Emrosi from approval to commercial shelf in four months, demonstrating the value of agile supply networks.

Pipeline diversity intensifies rivalry. Tarsus Pharmaceuticals is carving an ocular rosacea niche with TP-04, widening category breadth and highlighting unmet need in peri-ocular inflammation. AbbVie showcases JAK inhibitor data at dermatology congresses to establish scientific mindshare ahead of possible label expansion. Digital differentiation emerges as a parallel battleground; firms integrate AI triage tools that funnel users into branded treatment pathways, embedding stickiness and capturing longitudinal data for post-marketing surveillance.

Price sensitivity and formulary negotiations pressure margins, prompting lifecycle management such as fixed-dose combinations or lower-concentration line extensions that ride existing brand equity while deterring generic substitution. White-space opportunity persists in sustainable packaging that satisfies emerging environmental norms without compromising product stability. Competitive intensity therefore balances classic pharmacological advancement with ecosystem thinking that fuses drug, device, and digital service into holistic solutions for rosacea sufferers.

Rosacea Industry Leaders

Aclaris Therapeutics

Bausch Health Companies

Sol-Gel Technologies Ltd.

Journey Medical Corporation (Fortress Biotech, Inc.)

Galderma

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity centers on therapies and care models that reduce friction between diagnosis, initiation, and long-term maintenance while addressing multiple rosacea manifestations. Tele-dermatology and e-pharmacy workflows support ongoing titration and refills, aligning with the shift toward home-care growth alongside clinic-led diagnosis. Differentiation that improves tolerability and adherence, including micro-encapsulated topical delivery and extended-release oral dosing, supports premium positioning in markets where branded costs and irritation-driven discontinuation constrain persistence.

Geographic whitespace also depends on how quickly regulatory clearances and commercialization partners extend access beyond the United States. Health Canadas September 2025 Notice of Compliance for EPSOLAY (micro-encapsulated benzoyl peroxide) for inflammatory lesions in adults, commercialized through partner Searchlight Pharma, shows how targeted approvals paired with local commercialization can widen treated populations. R&D focus is broadening beyond single-agent, symptom-specific approaches toward combination or sequential regimens, with attention on mechanisms that target vascular and neurogenic components, where persistent erythema and flushing remain less completely served than papulopustular disease.

Recent Industry Developments

- April 2026: Bausch Health Companies Inc. announced that Biafine Skin Recovery Emulsion became available via online ordering in the United States. While not a rosacea-specific approval, this expands direct-to-consumer access and e-commerce fulfillment capabilities, which can affect how dermatology-adjacent skin-care products are discovered and purchased.

- September 2025: Sol-Gel Technologies announced that Health Canada issued a Notice of Compliance for EPSOLAY for the treatment of inflammatory lesions of rosacea in adults, with commercialization through partner Searchlight Pharma. The approval expands access to micro-encapsulated benzoyl peroxide beyond the United States and reinforces controlled-release topical delivery as a differentiator in tolerability-sensitive facial dermatoses.

- July 2024: Sol-Gel Technologies signed six exclusive license agreements to commercialize TWYNEO and EPSOLAY across multiple European countries and South Africa. These agreements extend the international commercialization footprint for key dermatology assets and build distributor coverage that can accelerate uptake once country-level launch and reimbursement steps are completed.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the rosacea market is defined as the value of prescription and non-prescription pharmacologic treatments used to manage rosacea symptoms, across topical and oral routes, and tracked as revenues generated within the covered geographies.

Scope exclusions: cosmetic skin care positioned for general redness (without a rosacea treatment claim) and clinic-led procedures are excluded from this market sizing.

Segmentation Overview

- By Drug Class

- Alpha-adrenergic Agonists

- Antibiotics (Tetracyclines, Macrolides)

- Azelaic Acid & Derivatives

- Ivermectin

- Benzoyl Peroxide & Others

- By Route of Administration

- Topical

- Oral

- Others (Injectables, Device-assisted)

- By End-user Facility

- Hospitals & Dermatology Clinics

- Home-care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the clinical and commercial frame for rosacea treatment demand and to build starting assumptions that can be checked later in interviews. We referred to public health statistics and epidemiology sources such as CDC resources, NIH and NLM repositories, and WHO health databases to understand diagnosis trends and care access patterns that influence treated volumes.

We also reviewed regulator and guideline signals that shape product uptake, such as FDA drug labels and safety communications, along with clinical literature indexed in PubMed for treatment pathways and typical prescribing patterns. Additional context came from company filings and investor materials, dermatology association websites, and reputed press coverage around launches and approvals. Where needed, we used paid subscriptions for company financials and intelligence, patent lookups, and shipment-level import export context to sanity-check supply availability. The sources listed here are illustrative, and many other public references were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on converting desk assumptions into market-realistic ranges, especially for therapy mix, pricing progression, and how often patients stay on treatment. We spoke with dermatology clinicians, channel participants, and product or commercial leaders across major regions so regional diagnosis rates, access differences, and switching behavior could be reflected in our model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 45% |

| Mid tier: 46% | Functional/Unit leaders: 43% | EMEA: 30% |

| Smaller Players: 18% | Managers: 44% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build that links diagnosed and treated rosacea patients to therapy utilization over a year, and then applies an average price by route and product class to reach a revenue total. Since diagnosis is uneven across countries, we adjust the treated pool using access to dermatology care, prescription intensity, and typical persistence rates (patients often cycle through topical and oral options before settling).

To keep the total grounded, selective bottom-up checks are run using sampled product revenue disclosures, channel feedback on volume movement, and price points observed in major markets. Where product-level numbers are not visible, gaps are handled through proxy pricing and conservative utilization ranges. Key model inputs include prevalence and diagnosis rates, share of patients receiving prescription therapy, split of topical versus oral use, average duration of therapy, and price evolution tied to genericization and new launches. Forecasts are built using scenario analysis supported by expert feedback, with base, conservative, and growth-tilted cases mainly differing by diagnosis expansion, access, and net pricing changes over time.

Data Validation & Update Cycle

Validation is done through stepwise checks, starting with internal consistency tests on patient pools, therapy mix, and implied spend per treated patient by country and region. If outputs look out of line with known prescription behavior or regulatory and launch timelines, the assumptions are reopened and the relevant experts are re-contacted to explain the variance.

Before sign-off, the model is reviewed by another analyst to confirm formulas, currency handling, and year alignment. The final story is then checked against independent signals such as approval activity and treatment adoption commentary. Reports are refreshed annually, with interim updates when material events occur, such as major approvals, safety changes, or sudden pricing shifts. Right before delivery, we do a fresh pass so clients receive the most current view available.

Mordor Intelligence's Rosacea Market Size Compared Against Other Published Estimates

Published rosacea market values often vary because the counted product basket and the revenue point in the chain are not always the same. Timing differences in currency and inflation can further widen the spread, and the year used as the current estimate matters, since faster growth periods can make adjacent-year figures look inconsistent.

Cosmetic redness creams and clinic procedures are kept outside Mordor Intelligence's scope, which tends to narrow the total versus estimates that blend in adjacent aesthetic spending. Differences also come from whether market value is captured at manufacturer revenues versus end-market sales, plus how authors treat generic erosion, patient persistence on therapy, and regional diagnosis growth when moving from one year to the next.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.46 B (2026) | |

| Global Consultancy A | USD 2.08 B (2024) | Uses a different base year, and its value is anchored to a 2024 starting point with a separate forecast window, which can understate the 2026 level when growth is compounding. It can also apply a lower treated-patient conversion for the diagnosed pool, especially where dermatology access is uneven. |

| Trade Publisher B | USD 2.14 B (2025) | Defines value around factory gate revenues and includes related services, which can move totals away from therapy spend at the patient level depending on channel structure. The estimate also applies its own pricing progression assumptions through 2025, which can shift totals when generic erosion timing differs. |

Taken together, the spread is mainly explained by what gets counted as rosacea spending, the revenue lens used, and the year alignment of pricing and treated patient volumes. By keeping assumptions tied to diagnosis-to-treatment flow and then checking the implied spend against real-world pricing and utilization signals, our final number stays traceable and repeatable for planning.

Key Questions Answered in the Report

What is the current value of the rosacea market?

The market is valued at USD 2.46 billion in 2026 and is projected to reach USD 3.65 billion by 2031.

How fast is the industry expanding?

Revenue is forecast to rise at an 8.22% CAGR between 2026 and 2031, outpacing many other dermatology segments.

Which region generates the most revenue today?

North America leads with 41.85% share in 2025, supported by favorable reimbursement and specialist availability.

Where is the fastest growth expected?

Asia-Pacific is advancing at a 10.01% CAGR through 2031 as healthcare access and disposable incomes increase.

Which therapy class holds the highest market share?

Alpha-adrenergic agonists account for 38.12% of global revenue, driven by rapid erythema control.

Page last updated on: