Hyaluronidase Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

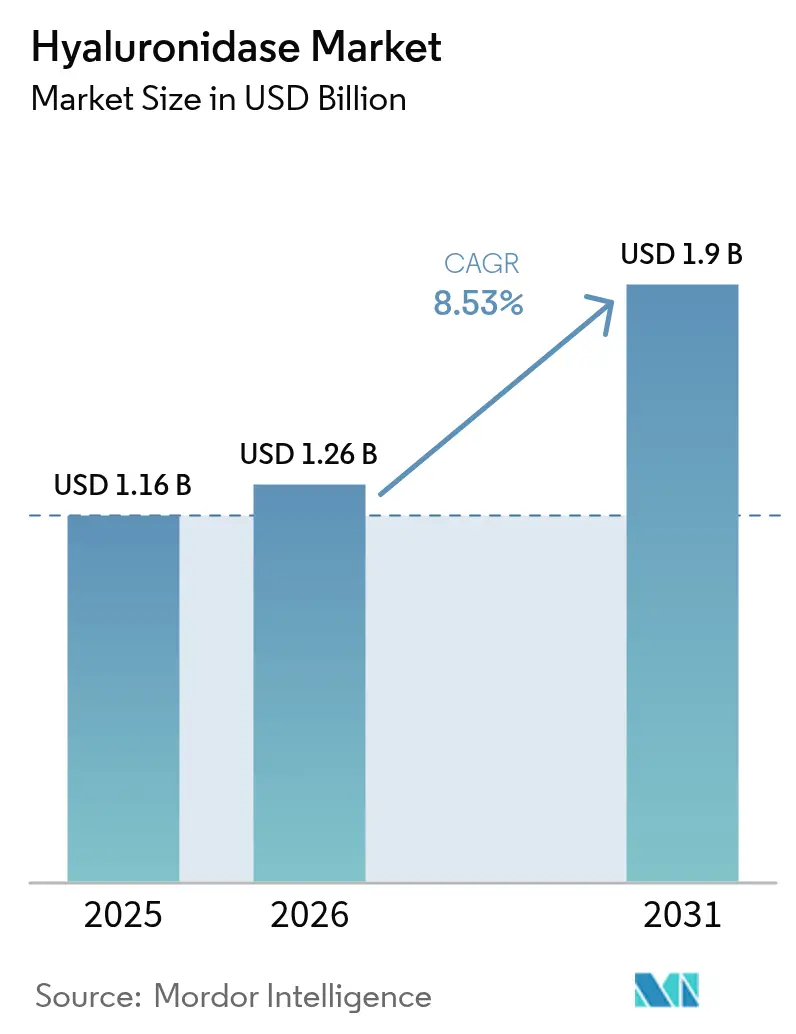

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 1.9 Billion |

| Growth Rate (2026 - 2031) | 8.53% CAGR |

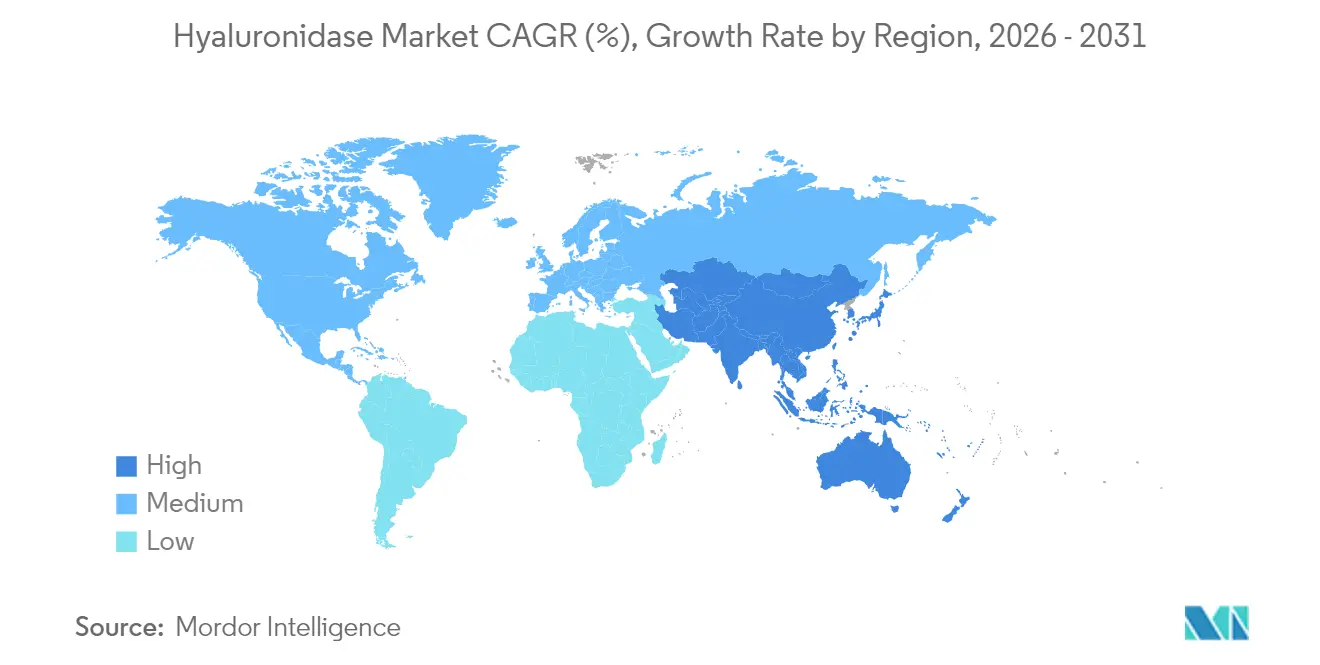

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

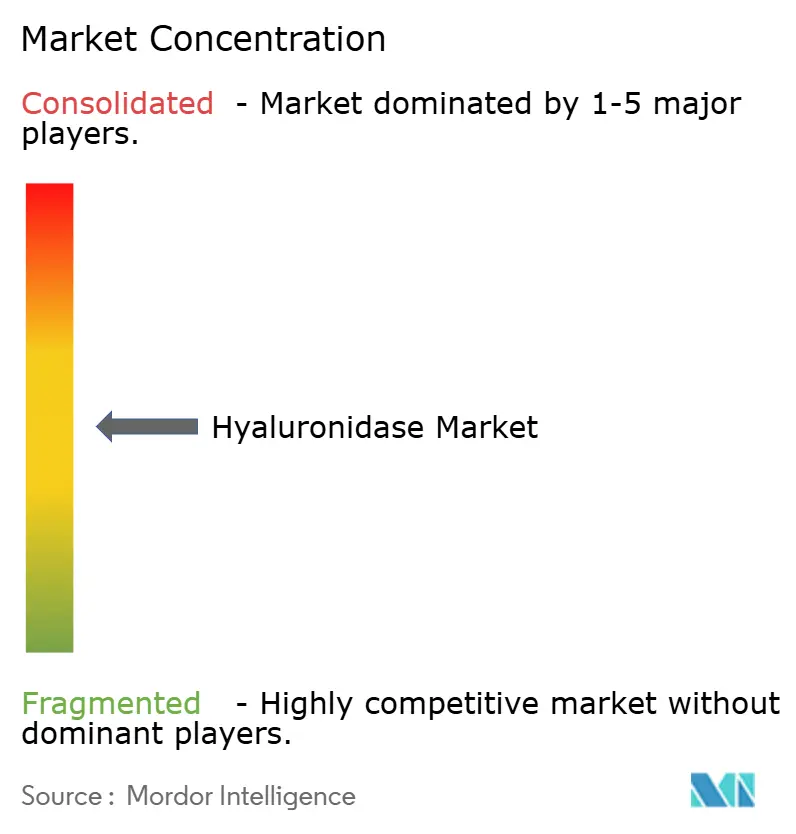

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hyaluronidase Market Analysis by Mordor Intelligence

The hyaluronidase market size was valued at USD 1.16 billion in 2025 and estimated to grow from USD 1.26 billion in 2026 to reach USD 1.9 billion by 2031, at a CAGR of 8.53% during the forecast period (2026-2031). Growing demand for subcutaneous biologics, the rapid expansion of aesthetic filler procedures that rely on safe filler reversal, and increasing adoption of patient-centric drug delivery models are the primary forces propelling the Hyaluronidase market. Regulatory momentum is strong; multiple FDA approvals of hyaluronidase-containing combination products between 2024 and 2025 have validated the enzyme’s clinical value and accelerated integration across oncology, immunology, and ophthalmology. Geographic dynamics are equally decisive: North America maintains leadership thanks to advanced healthcare infrastructure and early uptake of novel delivery systems, while Asia Pacific is advancing fastest on the back of expanding healthcare access, rising disposable incomes, and the presence of innovative domestic enzyme developers. Competitive intensity is moderate, with proprietary platform holders such as Halozyme Therapeutics licensing technology to large-cap partners looking to differentiate their biologic portfolios. Strategic collaborations, coupled with the push toward recombinant variants that offer consistency and lower immunogenicity, continue to unlock fresh growth corridors throughout the Hyaluronidase market.

Key Report Takeaways

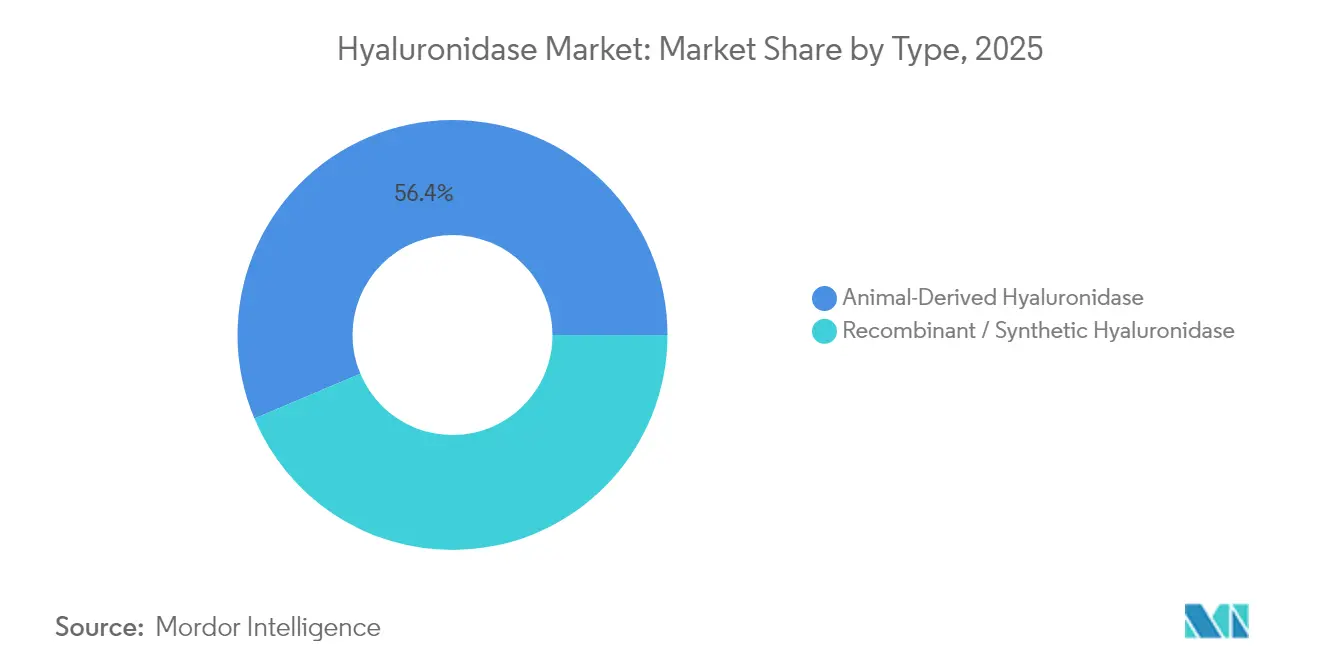

- By type, Animal-Derived Hyaluronidase led with 56.35% hyaluronidase market share in 2025, while Recombinant/Synthetic Hyaluronidase is projected to expand at a 9.55% CAGR through 2031.

- By formulation, Lyophilized Powder held 61.55% revenue share of the hyaluronidase market size in 2025, whereas Solution & Gel is forecast to grow at a 10.35% CAGR to 2031.

- By application, Dermatology (aesthetic filler reversal) accounted for 32.05% share of the hyaluronidase market in 2025; Ophthalmology is set to rise at an 10.95% CAGR over 2026-2031.

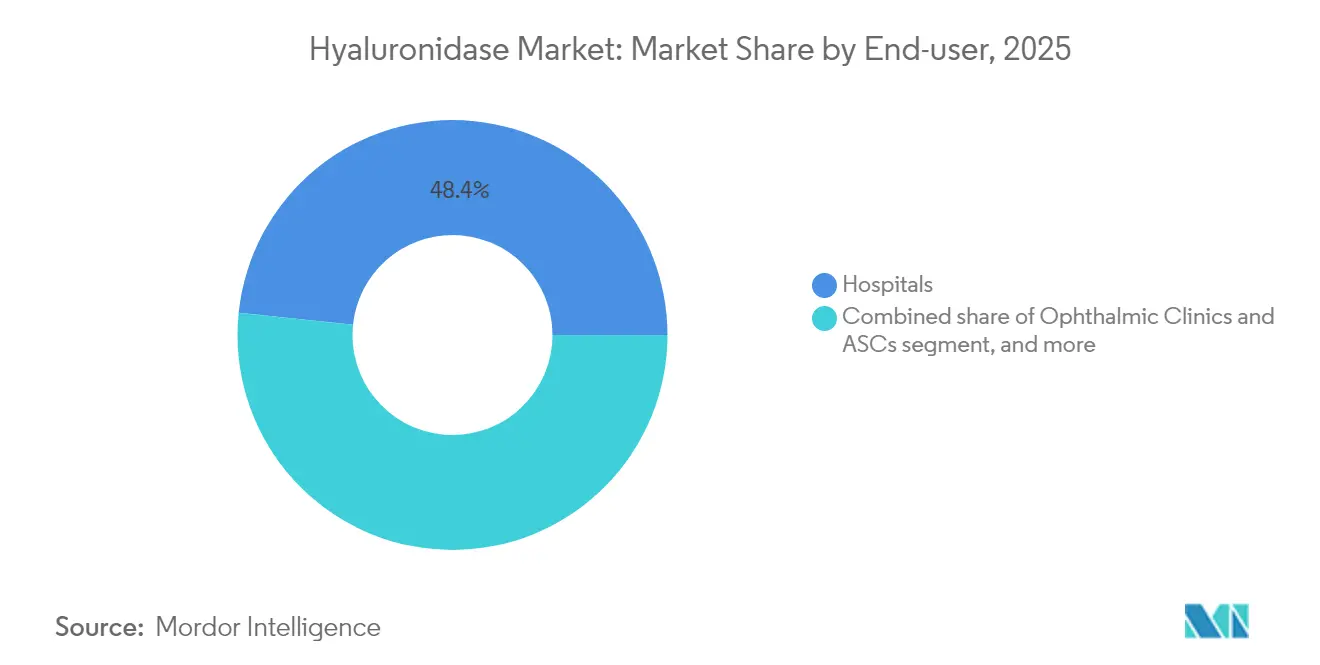

- By end-user, Hospitals captured 48.35% hyaluronidase market share in 2025, while Specialty Dermatology & Aesthetic Clinics are expected to advance at a 12.35% CAGR through 2031.

- By delivery mode, Injectable administration commanded 67.45% share of the hyaluronidase market size in 2025; Subcutaneous Infusion is projected to post a 13.1% CAGR up to 2031.

- By geography, North America dominated with 38.15% hyaluronidase market share in 2025, whereas Asia Pacific is anticipated to record a 9.05% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Hyaluronidase Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Aesthetic & Dermatology Procedures Requiring Filler Reversal | +2.3% | North America, Europe, Asia Pacific (urban centers) | Short term (≤ 2 years) |

| Growth in Subcutaneous Biologics Enabled by Hyaluronidase | +2.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rising Oncology Day-Care Chemotherapy Using Rapid-Infusion Protocols | +1.5% | North America, Europe, developed Asia Pacific | Medium term (2-4 years) |

| Increasing IVF Cycle Volumes Worldwide | +0.7% | Global, with emphasis on China, Japan, US, Europe | Long term (≥ 4 years) |

| Surge in Ophthalmic Surgeries Demanding Regional-Anesthesia Adjuncts | +0.9% | Global, with higher impact in aging populations | Medium term (2-4 years) |

| Manufacturing Scale-Up of Recombinant Enzymes Lowering Unit Costs | +0.2% | Global, with initial impact in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Aesthetic & Dermatology Procedures Requiring Filler Reversal

Worldwide uptake of hyaluronic-acid fillers has created an equally robust requirement for hyaluronidase as the only targeted antidote for vascular compromise, over-correction, and patient-requested dissolutions. Ultrasound-guided injections now enable precise enzyme placement, reducing the dose needed while improving outcomes, which has moved hyaluronidase from an emergency tool to a routine component of comprehensive filler services. Specialty clinics find that predictable dissolving protocols drive repeat visits and higher procedure confidence, supporting sustained Hyaluronidase market demand. Increasing social media visibility of “filler fatigue” reversals in 2024 and 2025 has further normalized elective enzyme use, expanding the addressable patient base. The trend aligns with the broader shift toward minimally invasive aesthetic solutions that promise quick recovery and customizable results. North American and European markets, where dermal filler penetration is highest, continue to shape clinical best practices adopted later in Asia Pacific and Latin America.

Growth in Subcutaneous Biologics Enabled by Hyaluronidase

Pharma pipelines are pivoting toward subcutaneous versions of blockbuster antibodies to cut chair time and broaden outpatient or at-home administration. Bristol Myers Squibb’s Phase 3 CHECKMATE-67T trial showed subcutaneous nivolumab plus hyaluronidase achieved non-inferior efficacy to intravenous dosing while shrinking infusion time from 30 minutes to 5 minutes, underscoring the operational value of enzyme-enabled delivery. ENHANZE technology has already been used in nearly 2 million patients, signaling clinical trust and scalability for future rollouts. Health-system payers recognize the economic upside of freeing infusion chairs, which accelerates formulary inclusion of these fixed-dose combinations. As more PD-1, PD-L1, and other monoclonal antibodies transition to subcutaneous formats through 2030, the Hyaluronidase market gains a long-term volume engine that transcends single-product cycles. Recombinant human variants stand to capture the lion’s share of this incremental demand by meeting stringent safety and consistency requirements.

Rising Oncology Day-Care Chemotherapy Using Rapid-Infusion Protocols

The FDA’s 2024 approval of atezolizumab and hyaluronidase-tqjs (Tecentriq Hybreza) established a 15-minute subcutaneous option compared with an hour-long intravenous regimen, demonstrating the paradigm shift toward ambulatory oncology care[1]FDA, “Tecentriq Hybreza Approval,” fda.gov. Such rapid-infusion protocols alleviate capacity constraints in infusion suites, enabling higher patient throughput without capital expansion. Patients report greater convenience and less time lost to treatment, factors that improve adherence and quality of life. Physicians view the shorter administration window as clinically equivalent but operationally superior, which drives rapid guideline incorporation. Similar approvals for daratumumab, ocrelizumab, and nivolumab combinations in late 2024 and 2025 have cemented hyaluronidase-enabled delivery as a competitive differentiator in the crowded oncology landscape. As additional agents in immuno-oncology and hematology adopt this route, cumulative demand reinforces the growth trajectory of the Hyaluronidase market.

Increasing IVF Cycle Volumes Worldwide

Global fertility treatments are expanding on demographic shifts and delayed parenthood trends, with oocyte denudation relying on hyaluronidase to remove cumulus cells ahead of ICSI. Peer-reviewed studies show recombinant cumulase yields higher euploid embryo rates than bovine-derived enzymes, prompting clinics to favor premium formulations despite higher costs[2]E-Palli Publishers, “Recombinant Cumulase in IVF Outcomes,” epalli.net. Success-rate differentials translate into strong willingness to pay, positioning recombinant variants as profit accretive for fertility centers. Emerging applications—such as HABSelect techniques assessing sperm chromatin integrity—extend enzyme demand beyond core denudation. Automated denudation modules embedding hyaluronidase further entrench the enzyme in laboratory workflows, making it a consumable essential rather than an optional reagent. Rising Asia Pacific IVF volumes, particularly in China and India, anchor long-term volumetric growth for the Hyaluronidase market and support regional manufacturing scale for recombinant supplies.

Restraints Impact Analysis of Hyaluronidase Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety & Immunogenicity Concerns Limiting Repeat Use | -0.6% | Global, with higher impact in regions with stringent pharmacovigilance | Short term (≤ 2 years) |

| Dependence on Animal-Derived API Supply Chains | -0.4% | Global, with higher impact in regions with strict regulatory oversight | Medium term (2-4 years) |

| Generic Pricing Pressure Post-Patent Expiry | -0.3% | North America, Europe | Medium term (2-4 years) |

| Cold-Chain Logistics Challenges in Low-Infrastructure Regions | -0.2% | Emerging markets, rural areas in developing countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety & Immunogenicity Concerns Limiting Repeat Use

Although adverse reactions remain infrequent, the immunogenic potential of animal-derived hyaluronidase still deters repeat dosing in chronic-therapy settings. A systematic review of hyaluronidase-facilitated subcutaneous immunoglobulin highlighted isolated allergic events that necessitate vigilant monitoring and pre-dose testing, particularly in immunocompromised cohorts. While recombinant formulations reduce risk, long-term safety evidence is still maturing across emerging indications such as neurology and regenerative medicine. Hospitals sometimes establish restrictive protocols that require hypersensitivity testing, elongating administration workflows and tempering volume growth. Negative social-media anecdotes, albeit anecdotal, can influence patient sentiment and amplify caution. Together these factors impose a moderate drag on the expansion tempo of the Hyaluronidase market until robust, longitudinal safety datasets accumulate.

Dependence on Animal-Derived API Supply Chains

Animal-sourced hyaluronidase accounts for 57% of 2024 volumes, leaving several application segments exposed to supply fluctuations tied to bovine and ovine raw material availability. Batch-to-batch variability in activity and purity introduces dosing uncertainty, complicating precision-medicine approaches and discouraging use in high-risk surgical procedures. Regulatory bodies are progressively favoring recombinant versions, and facilities relying on animal extraction face rising compliance costs for viral inactivation and endotoxin control. As recombinant capacity ramps up in Asia Pacific and Europe, legacy producers confront capex pressures to modernize or exit. Near-term volatility therefore persists, restraining full-scale deployment in sensitive indications and creating a headwind for Hyaluronidase market expansion until supply diversification matures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Hyaluronidase Market Segment Analysis

By Type:

Recombinant Variants Gain Clinical PreferenceAnimal-derived hyaluronidase maintained a 56.35% Hyaluronidase market share in 2025, leveraging cost advantages in price-sensitive settings. Yet recombinant and synthetic enzymes are accelerating at a 9.55% CAGR, supported by superior purity, batch consistency, and lower immunogenic risk. Oncology and immunology therapies increasingly mandate recombinant inputs to align with stringent biologics standards, propelling platform innovators such as HALOZYME and Alteogen. Patent filings focus on freeze-dried preparations that reduce cold-chain burden, underscoring formulation innovation as a differentiation lever in the Hyaluronidase market.

Recombinant variants also command a pricing premium that lifts revenue even at lower volume shares. Technology licensors typically secure milestone-linked payments and mid-single-digit royalties when partners incorporate the enzyme into pipeline antibodies, embedding annuity-like earnings into business models. As Asia Pacific regulators, led by South Korea’s MFDS, grant local approvals for recombinant products, regional adoption accelerates and further erodes the dominance of animal-derived supplies.

By Formulation:

Solution & Gel Gaining MomentumLyophilized powder remains the primary format, holding 61.55% volume share in 2025 thanks to superior shelf life without refrigeration. However, ready-to-use solution and gel formulations are set to grow at 10.35% CAGR as combination products and point-of-care convenience gain priority. Ophthalmology procedures prefer solution vials for controlled micro-dosing, while dermatology uses both gels and solutions depending on injection depth. Prefilled syringes and autoinjectors reduce preparation errors and downtime, resonating with outpatient centers that value workflow efficiency.

Product developers are experimenting with stabilizers such as trehalose and arginine to maintain activity in liquid state over six months at 2-8 °C, closing the historical stability gap with freeze-dry formats. Successful launches could shift formulary preference toward liquids in regions with reliable cold-chain logistics, redistributing Hyaluronidase market demand toward higher-margin SKUs.

By Application:

Ophthalmology Emerges as Growth LeaderDermatology accounted for 32.05% of the Hyaluronidase market size in 2025, anchored by the expanding global dermal-filler ecosystem and the enzyme’s role in managing complications. The specialty has normalized pre-stocking hyaluronidase for every filler procedure, ensuring continuous baseline demand. Conversely, Ophthalmology is anticipated to register the fastest 10.95% CAGR through 2031 as recombinant enzymes improve the reliability of peribulbar blocks and newer applications in vitreoretinal surgery gain clinical validation.

Chemotherapy is another priority segment as multiple monoclonal antibodies win subcutaneous labels, with each launch adding incremental multi-million-unit enzyme demand. In IVF, recombinant cumulase adoption supports embryo-quality gains, reinforcing steady double-digit growth within reproductive medicine.

By End-User:

Specialty Clinics Drive Premium Segment GrowthHospitals retained 48.35% share of the Hyaluronidase market in 2025, reflecting broad procedural diversity and centralized procurement. Yet Specialty Dermatology & Aesthetic Clinics are expanding at 12.35% CAGR because these facilities integrate ultrasound guidance and premium recombinant formulations as a standard of care, raising per-procedure value. Ophthalmic clinics and ambulatory surgical centers benefit from shorter patient stay metrics, encouraging the uptake of hyaluronidase-enhanced anesthesia.

Fertility centers constitute a smaller but strategically important niche given high willingness to pay for outcome-enhancing inputs. Oncology day-care infusion suites increasingly stock fixed-dose hyaluronidase antibody cocktails, elevating throughput without physical expansion.

By Delivery Mode:

Subcutaneous Infusion Revolutionizes AdministrationInjectable delivery, covering intradermal and localized subcutaneous injections, controlled 67.45% volume share in 2025. Subcutaneous infusion of fixed-dose combinations is, however, charting a 13.1% CAGR, reshaping administration norms across oncology, immunology, and neurology. The CheckMate-67T study confirmed bioequivalence between subcutaneous nivolumab plus hyaluronidase and its intravenous counterpart, while slashing chair time to under five minutes.

Ophthalmic solution delivery remains a niche but stable use, whereas topical formats continue in exploratory phases targeting transdermal permeation. Device innovation—prefilled pens and wearable pumps—adds convenience, encouraging self-administration and decentralizing care models, trends that reinforce upward momentum in the Hyaluronidase market.

Geography Analysis

North America Hyaluronidase Market

North America captured 38.15% of the hyaluronidase market in 2025 due to early adoption of innovative drug-delivery frameworks and a sizeable aesthetic medicine community. The presence of platform originators such as Halozyme and robust reimbursement for biologics accelerate clinical penetration across oncology and immunology. FDA approvals of Tecentriq Hybreza, Opdivo Qvantig, and DARZALEX FASPRO during 2024-2025 further entrenched subcutaneous infusion as a preferred modality, bolstering enzyme volume flow. Nonetheless, a 2024 survey indicated that 45.6% of emergency rooms lacked on-hand hyaluronidase supplies, exposing readiness gaps for filler complication management.

APAC Hyaluronidase Market

Asia Pacific is forecast to expand at 9.05% CAGR between 2026 and 2031, benefiting from rising disposable incomes, burgeoning cosmetic procedure volumes, and local recombinant manufacturing. South Korea’s 2024 approval of Tergase® positions Alteogen as a regional champion that can supply domestic and export markets, challenging Western incumbents on both cost and technology. China’s oncology pipeline is similarly keen on subcutaneous reformulations to accelerate hospital throughput. Rapid medical tourism growth in Thailand and Singapore intensifies adoption of advanced aesthetic protocols that mandate enzyme availability, widening the Hyaluronidase market’s regional footprint.

Europe Hyaluronidase Market

Europe remains a mature but significant contributor, with diverse national reimbursement frameworks shaping adoption velocity. While EMA does not centrally regulate hyaluronidase as a standalone enzyme, country-specific authorities have granted approvals that mirror U.S. indications, sustaining cross-border consistency. The proliferation of more than 100 hyaluronic-acid fillers across Germany, Italy, Spain, and the United Kingdom magnifies baseline enzyme demand. Patent cliffs for early ENHANZE registrations are creating a window for biosimilar entrants, pressuring incumbents to invest in next-generation formulations and robust post-marketing support to defend share within the hyaluronidase market.

Competitive Landscape

The hyaluronidase market features moderate fragmentation backed by a clear hierarchy of platform licensors, specialty API manufacturers, and formulation partners. Halozyme Therapeutics continues to monetize its recombinant PH20 enzyme through multi-asset deals, while Alteogen gains traction with ALT-B4, a structurally distinct recombinant variant licensed to AstraZeneca for several oncology antibodies in April 2025[3]AstraZeneca, “ALT-B4 License Agreement,” astrazeneca.com. Such agreements commonly involve upfront cash, milestone payments, and mid-single-digit royalties, establishing durable revenue streams for enzyme innovators.

Intellectual-property battles have migrated from core enzyme sequences to application-specific formulations. Recent patents describe highly concentrated anti-CD20 antibody mixtures stabilized with hyaluronidase for once-monthly subcutaneous dosing, a sign that delivery science rather than enzyme discovery now anchors differentiation. Manufacturing advances focus on thermostable liquid formulations requiring less stringent cold-chain, targeting emerging markets with infrastructure constraints.

Emerging disruptors—including biotechnology start-ups exploring chimeric or PEGylated hyaluronidases—seek to deliver higher catalytic efficiencies, longer in-tissue residence times, or tailored degradation profiles. Meanwhile, traditional API suppliers contemplate shifting from animal extraction to recombinant expression systems or risk obsolescence. Collectively, these dynamics sustain innovation velocity and competitive churn, shaping pricing and partnership structures across the hyaluronidase market.

Hyaluronidase Industry Leaders

PrimaPharma, Inc

Amphastar Pharmaceuticals, Inc

Bausch & Lomb Incorporated

Halozyme, Inc.

Sun Pharmaceutical Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Hyaluronidase Market Companies Covered in this Report

- Halozyme

- Bausch Health

- Amphastar Pharmaceuticals

- PrimaPharma, Inc.

- Sun Pharmaceuticals Industries

- Stem Cell Technologies

- The Cooper Companies

- Shreya Life Sciences Pvt Ltd.

- Fresenius

- Viatris

- Teva Pharmaceutical Industries

- Cipla

Recent Industry Developments in Hyaluronidase Market

- May 2025: Johnson & Johnson’s DARZALEX FASPRO received a positive ODAC vote for high-risk smoldering multiple myeloma, broadening hyaluronidase applications in oncology.

- May 2025: Argenx gained FDA approval for a prefilled syringe format of Vyvgart Hytrulo, enabling self-injection in generalized myasthenia gravis.

- April 2025: AstraZeneca licensed Alteogen’s ALT-B4 hyaluronidase to develop subcutaneous formulations of multiple oncology drugs.

- January 2025: Bristol Myers Squibb secured FDA approval for nivolumab and hyaluronidase-nvhy (Opdivo Qvantig) as the first subcutaneous PD-1 inhibitor.

- January 2025: Genmab reported DARZALEX sales, including the subcutaneous version with hyaluronidase, reached USD 3.24 billion in Q1 2025, marking a 20% year-over-year rise.

Global Hyaluronidase Market Report Scope

Based on what the report is about, hyaluronidase is an enzyme that breaks down hyaluronic acid and makes connective tissues more permeable. These enzymes are widely used in aesthetic procedures. The hyaluronidase market is divided into three sections: type (animal-derived hyaluronidase, synthetic hyaluronidase), application (chemotherapy, in vitro fertilization, ophthalmology, dermatology, and other applications), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

Segmentation Overview

| Animal-Derived Hyaluronidase |

| Recombinant / Synthetic Hyaluronidase |

| Lyophilized Powder |

| Solution & Gel |

| Dermatology |

| Chemotherapy |

| Ophthalmology |

| In-Vitro Fertilization |

| Others Applications |

| Hospitals |

| Specialty Dermatology & Aesthetic Clinics |

| Ophthalmic Clinics & ASCs |

| Other End-users |

| Injectable |

| Subcutaneous Infusion |

| Ophthalmic Solution |

| Topical |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Animal-Derived Hyaluronidase | |

| Recombinant / Synthetic Hyaluronidase | ||

| By Formulation | Lyophilized Powder | |

| Solution & Gel | ||

| By Application | Dermatology | |

| Chemotherapy | ||

| Ophthalmology | ||

| In-Vitro Fertilization | ||

| Others Applications | ||

| By End-user | Hospitals | |

| Specialty Dermatology & Aesthetic Clinics | ||

| Ophthalmic Clinics & ASCs | ||

| Other End-users | ||

| By Delivery Mode | Injectable | |

| Subcutaneous Infusion | ||

| Ophthalmic Solution | ||

| Topical | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the hyaluronidase market?

The global hyaluronidase market is valued at USD 1.26 billion in 2026.

What growth rate is forecast for the market through 2031?

Revenue is projected to rise at an 8.53% CAGR, reaching USD 1.9 billion by 2031.

Which region is expected to expand the fastest?

Asia Pacific is forecast to post the highest regional growth with a 9.05% CAGR from 2026 to 2031.

Why are recombinant hyaluronidase variants gaining clinical preference?

Recombinant enzymes offer consistent activity and lower immunogenic risk, supporting rapid uptake in oncology, immunology, and fertility applications.

How does hyaluronidase improve subcutaneous biologic delivery?

The enzyme temporarily degrades extracellular hyaluronic acid, enabling faster drug absorption and cutting infusion time—for example, subcutaneous nivolumab plus hyaluronidase administers in 5 minutes versus 30 minutes intravenously.

Which end-user segment shows the fastest demand growth?

Specialty dermatology and aesthetic clinics are advancing at a 12.35% CAGR as routine filler-reversal protocols drive higher procedure volumes.

Page last updated on: