Proliferative Diabetic Retinopathy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

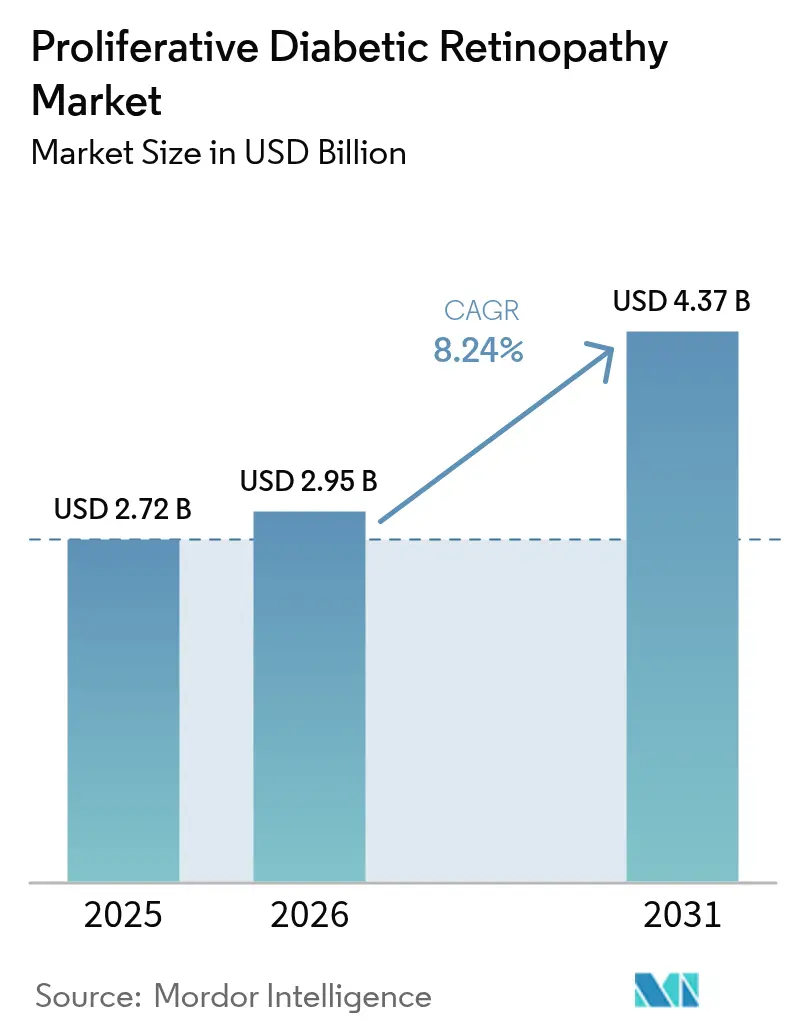

| Market Size (2026) | USD 2.95 Billion |

| Market Size (2031) | USD 4.37 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

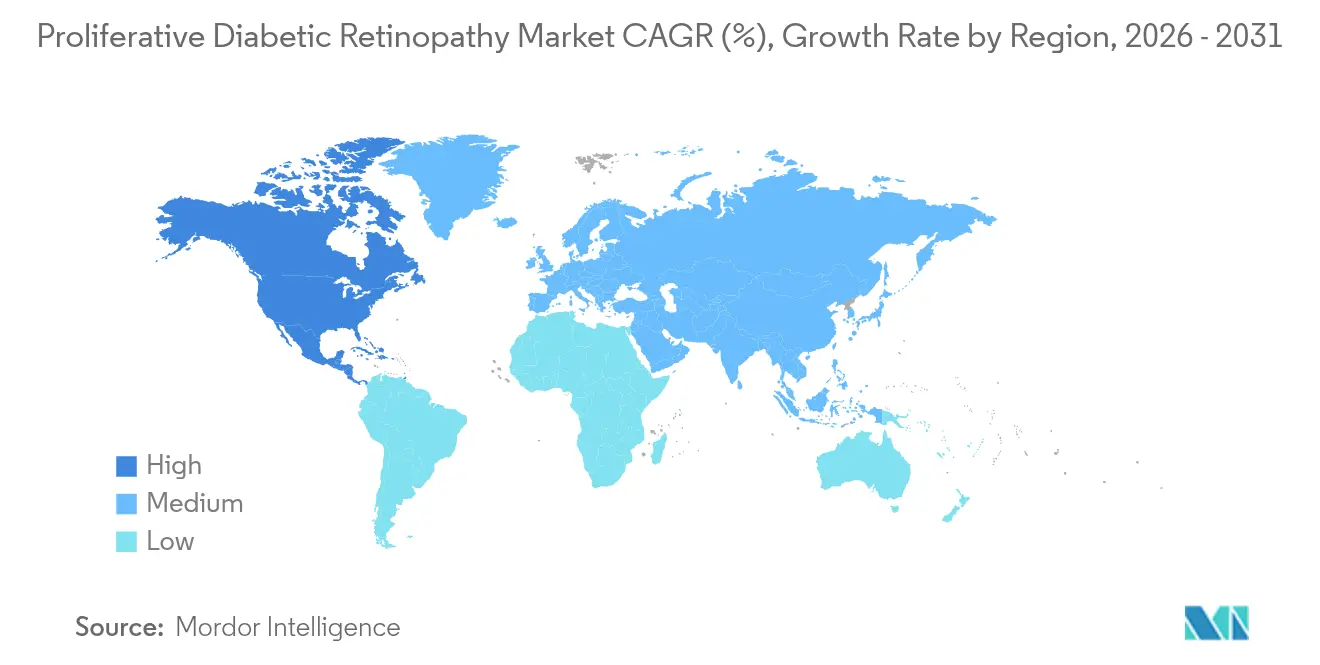

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

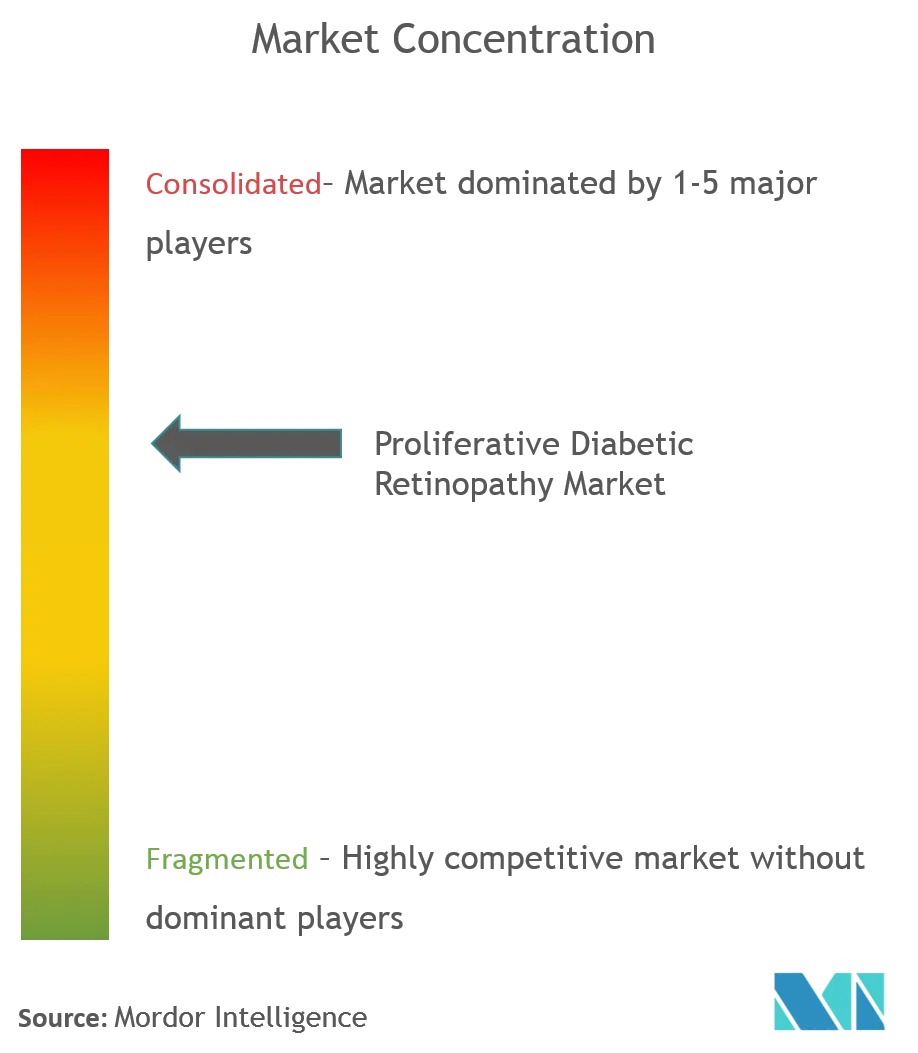

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Proliferative Diabetic Retinopathy Market Analysis by Mordor Intelligence

The proliferative diabetic retinopathy market size is expected to grow from USD 2.72 billion in 2025 to USD 2.95 billion in 2026 and is forecast to reach USD 4.37 billion by 2031 at 8.24% CAGR over 2026-2031. This growth aligns with the steady rise in global diabetes prevalence, which has more than quadrupled since 1990 and now affects over 800 million adults worldwide. Demand is reinforced by the Centers for Disease Control and Prevention estimate that diabetic retinopathy will affect 14.7 million Americans by 2050. Innovation in sustained-release implants and AI-enabled screening supports early detection, while biosimilar approvals temper pricing pressure in many markets. At the same time, technology-driven surgical advances such as subthreshold micropulse laser platforms reduce treatment burden, creating fresh adoption catalysts. A persistent shortage of retinal specialists poses a risk to care access, especially in emerging economies, yet teleophthalmology programs help bridge that gap. Taken together, these forces underpin a healthy outlook for the proliferative diabetic retinopathy market through the decade.

Key Report Takeaways

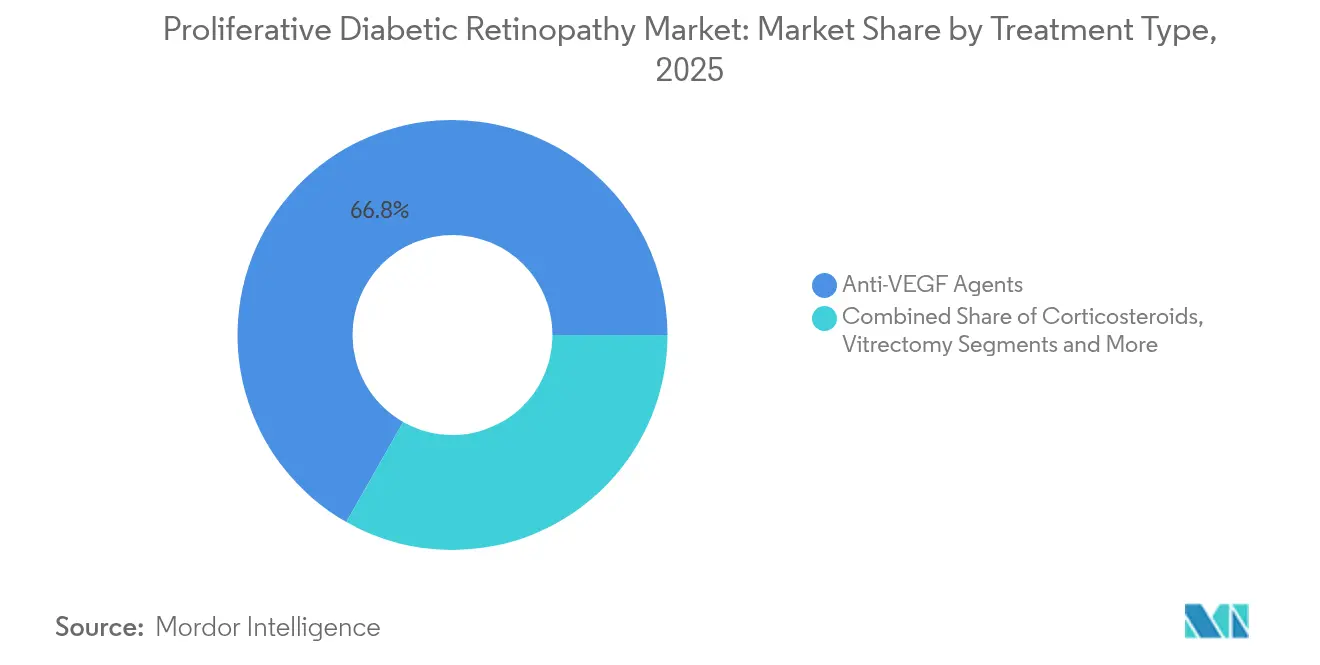

- By treatment type, anti-VEGF agents commanded 66.78% of the proliferative diabetic retinopathy market share in 2025, while laser surgery is forecast to grow at a 8.99% CAGR to 2031.

- By mode of administration, intravitreal delivery accounted for 46.92% share of the proliferative diabetic retinopathy market size in 2025, whereas topical and periocular routes are projected to expand at 9.22% CAGR through 2031.

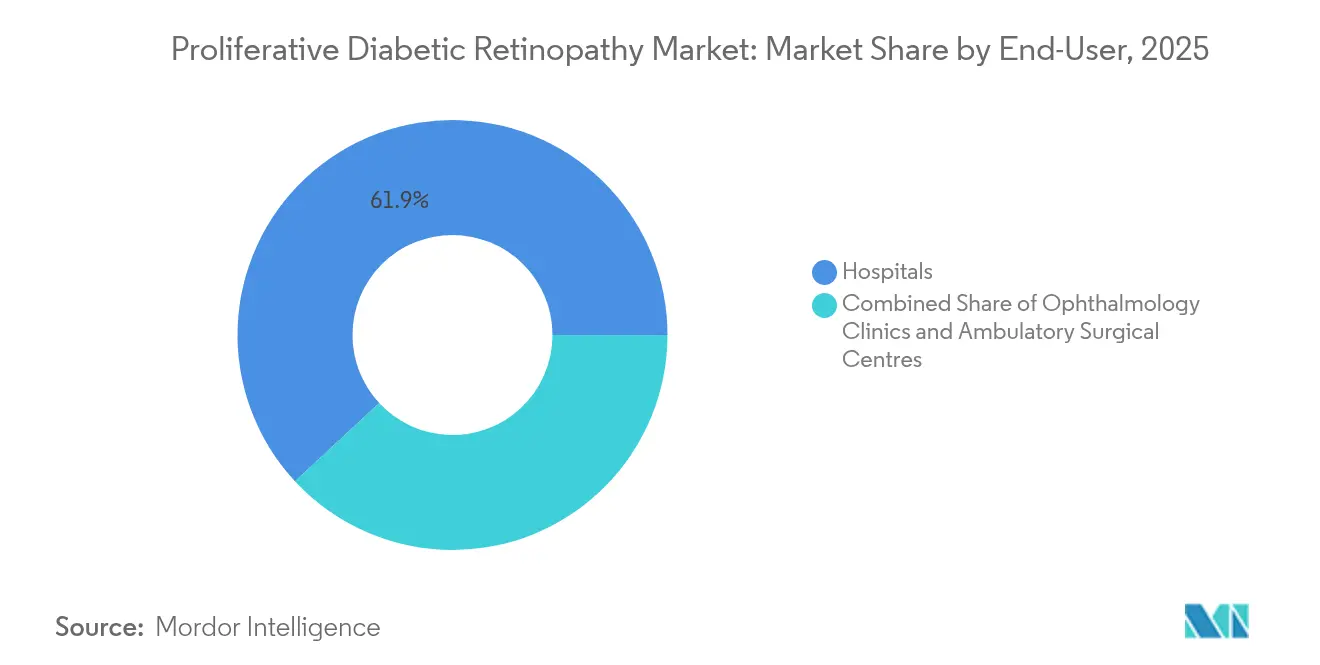

- By end-user, hospitals held 61.91% share of the proliferative diabetic retinopathy market size in 2025, and ophthalmology clinics are advancing at an 8.79% CAGR to 2031.

- By geography, North America led with 42.85% proliferative diabetic retinopathy market share in 2025, while Asia-Pacific is expected to rise at a 10.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Proliferative Diabetic Retinopathy Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of diabetes and longer life expectancy | +2.1% | Global – highest in Asia-Pacific and MENA | Long term (≥ 4 years) |

| Increasing adoption of intravitreal anti-VEGF biologics | +1.8% | North America & EU, expanding to emerging markets | Medium term (2-4 years) |

| Availability of minimally invasive retinal laser & vitrectomy platforms | +1.3% | Global – early use in developed markets | Medium term (2-4 years) |

| Growing healthcare expenditure boosting access to eye-care services | +1.5% | Asia-Pacific core, spill-over to Latin America | Long term (≥ 4 years) |

| AI-enabled screening programs enabling earlier PDR detection | +0.9% | North America & EU, pilot programs in APAC | Short term (≤ 2 years) |

| Long-acting ocular implants reducing treatment burden | +0.7% | North America & EU, limited emerging-market uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes and Longer Life Expectancy

Global diabetes prevalence doubled between 1990 and 2022, rising from 7% to 14% of the adult population. Longer lifespans mean patients live with the disease for decades, and epidemiologic studies show a 4.36-fold higher retinopathy risk after 10 years of diabetes [1]Soroush Seifi, “Real-World Outcomes of Anti-VEGF Biosimilars,” nature.com. The International Diabetes Federation projects 783.2 million cases by 2045, with middle-income economies facing the largest increases. Germany illustrates this path; analysts expect type 2 diabetes prevalence to reach 14.2 million by 2040. As prevalence climbs, the proliferative diabetic retinopathy market gains a stable patient base for both pharmacologic and surgical care.

Increasing Adoption of Intravitreal Anti-VEGF Biologics

Medicare claims show aflibercept injections rose 138% between 2014 and 2023, reflecting clinician confidence in anti-VEGF therapy. In May 2025 the FDA cleared Genentech’s Susvimo for diabetic retinopathy, enabling continuous delivery with biannual refills. Regional access remains uneven: physician density drives large differences in injection rates across U.S. states, while biosimilars such as Yesafili and Opuviz began easing price barriers in 2025. Comparable efficacy data from Iran’s ATRIA trial further validate the biosimilar pathway. Wider biologic uptake elevates the proliferative diabetic retinopathy market by expanding the treated population and encouraging longer therapy duration.

Availability of Minimally Invasive Retinal Laser & Vitrectomy Platforms

Subthreshold micropulse laser therapy treats pathology without visible retinal scarring, helping preserve vision while reducing adverse events [2]José-Luis Montero, “Micropulse Laser Therapy Review,” mdpi.com. Robotic systems developed at the University of Utah achieve sub-micrometer precision, supporting delicate sub-retinal procedures under local anesthesia. Hypersonic vitrectomy devices such as Vitesse reach cut rates equal to millions of cuts per minute, although early trials reported technical challenges in 46% of cases. As technology matures, surgeons can combine 23-gauge vitrectomy with cataract extraction for faster recovery. These advances improve outcomes and shorten operating times, reinforcing patient and payor adoption of surgical care.

Growing Healthcare Expenditure Boosting Access to Eye-Care Services

Emerging markets allocate larger budgets to diabetes care as incomes rise; Eastern Mediterranean countries record per-patient costs ranging from USD 1,707 in Iran to USD 555 in Pakistan. Brazil’s primary-care network reports only 44.8% of adults achieving glycemic control, reinforcing demand for specialist ophthalmic services. Reimbursed tele-ophthalmology programs in Latin America and Asia-Pacific offer cost-effective screening at scale. Higher health spending widens therapeutic reach and raises the ceiling for the proliferative diabetic retinopathy market.

AI-Enabled Screening Programs Enabling Earlier Detection

Real-world deployments of autonomous image-analysis software achieve 87.7% sensitivity and 90.6% specificity for vision-threatening retinopathy. U.S. primary-care clinics using these tools improved screening rates by 31 percentage points in 2024. Asia-Pacific pilots replicate this success; India’s SMART DROP protocol combines AI triage with community outreach, creating a template for low-cost coverage. Earlier detection shifts more patients into timely intervention and underpins revenue growth across therapeutic categories within the proliferative diabetic retinopathy market.

Long-Acting Ocular Implants Reducing Treatment Burden

Genentech’s Susvimo delivers ranibizumab for six months, cutting annual injection frequency by 83% compared with monthly therapy. Ocular Therapeutix’s axitinib insert and Kodiak Sciences’ tarcocimab sustained-delivery platform follow the same path, targeting ≥ 6-month dosing intervals. Lower visit frequency improves adherence, limits chair time, and may reduce indirect costs to patients and payors. The cumulative impact adds steady tailwinds to the proliferative diabetic retinopathy market.

Restraints Impact Analysis*

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended regulatory approval timelines for ophthalmic biologics | -1.2% | Global – regional complexity varies | Medium term (2-4 years) |

| High cost of anti-VEGF injections limiting adherence | -1.8% | Global – most severe in emerging markets | Long term (≥ 4 years) |

| Safety concerns with repeated intravitreal injections | -0.9% | Global – stronger in regions with active pharmacovigilance | Short term (≤ 2 years) |

| Shortage of retinal specialists in LMICs | -1.1% | Low- and middle-income countries, rural areas worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extended Regulatory Approval Timelines for Ophthalmic Biologics

New entrants face multiyear data requirements for biologic comparability, toxicology, and device-drug combinations. Regeneron’s Eylea HD secured priority review in April 2025 yet still waits for an August action date. Oculis needed more than three years to complete Phase 3 enrollment for a topical steroid therapy. Gene and cell therapies demand bespoke manufacturing audits that lengthen review cycles. Smaller firms often cede ground to incumbents that can finance lengthy development and navigate diverse regional rules, tempering overall market growth.

High Cost of Anti-VEGF Injections Limiting Adherence

U.S. payers impose step-therapy rules on up to 75% of commercial policies, pushing patients toward lower-cost off-label bevacizumab before accessing approved agents. Vision loss nonetheless generated USD 134.2 billion in secondary costs in 2024, dwarfing drug spending and illustrating the cost-of-non-treatment paradox. Administrative delays further extend initiation times; retina practices report that prior authorization adds an average of nine days to first injection. Emerging markets face steeper barriers: per-patient diabetes spending across Middle East and North Africa economies varies by more than 300%, placing branded biologics beyond reach. Biosimilars may ease the burden, but uptake is slowed by limited physician familiarity and institutional contracting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type – Anti-VEGF Lead Strengthens While Lasers Surge

In revenue terms, anti-VEGF biologics generated 66.78% of proliferative diabetic retinopathy market share in 2025, reflecting proven vision-saving efficacy. Laser surgery has become the fastest-advancing option, growing at 8.99% CAGR on the back of subthreshold micropulse platforms that avoid tissue damage. Corticosteroids remain relevant through implants such as Ozurdex that release medication over four to six months. Vitrectomy is adopting 23-gauge and 25-gauge tools, which shorten procedure time and recovery. Combination agents like faricimab target both VEGF-A and Ang-2, yielding superior durability in real-world studies.

Sustained-release implants position manufacturers for durable revenue streams. Genentech’s Susvimo expansion into diabetic retinopathy in 2025 underscores the trend, while gene therapy candidates such as ABBV-RGX-314 advance toward pivotal trials. Novel mechanisms, including plasma kallikrein inhibition, broaden the therapeutic playbook. Across modalities, a shift toward personalized regimens catering to disease severity and patient preferences widens addressable demand in the proliferative diabetic retinopathy market.

By Mode of Administration – Intravitreal Dominance Faces Non-invasive Rivals

Intravitreal injection retained 46.92% share of proliferative diabetic retinopathy market size in 2025 thanks to entrenched procedure workflows. Yet topical and periocular delivery grows at 9.22% CAGR, propelled by Phase 3 progress for eye-drop steroids and deep-penetration nanocarriers. Suprachoroidal platforms inject therapy between sclera and choroid, targeting the retina more directly while sparing vitreous manipulation. Sub-retinal gene therapy remains an option in select centers using precision robotics from academic innovators . As sustained-release reservoirs and biodegradable inserts mature, frequent office injections could shift to outpatient implant surgeries, realigning revenue mix within the proliferative diabetic retinopathy market.

Safety findings motivate investment in alternative routes. Reports of severe intraocular inflammation after high-dose aflibercept and faricimab underscore concerns. Continuous-delivery implants bypass repeated needle entries, while topical programs eliminate injection entirely. The race to replicate intravitreal efficacy through less invasive access will shape administration trends through 2031.

By End-User – Specialized Care Settings Accelerate

Hospitals carried 61.91% of proliferative diabetic retinopathy market size in 2025, but ophthalmology clinics are growing at 8.79% CAGR as payors favor lower-cost, high-throughput environments. A projected shortfall of 2,650 ophthalmologists in the United States by 2035 is encouraging multi-clinic chains to streamline specialist productivity. Ambulatory centers now handle an increasing share of vitrectomies, taking advantage of bundled payment incentives. Teleophthalmology and AI triage allow clinics to reach rural areas where only 29% of patients currently have adequate specialist access.

Consolidation continues: Cencora acquired Retina Consultants of America for USD 4.6 billion in January 2025, creating a nationwide retina super-group. Integrated hospital systems respond by establishing retina centers of excellence within tertiary facilities to retain procedure revenue. Hybrid models that mix large hospital infrastructure with clinic-level efficiency are likely to dominate end-user dynamics across the proliferative diabetic retinopathy market.

Geography Analysis

North America captured 42.85% proliferative diabetic retinopathy market share in 2025, supported by broad insurance coverage, fast regulatory cycles, and early adoption of sustained-release therapies. Yet workforce deficits present a strategic obstacle; a 12% decline in ophthalmologist supply against 24% growth in demand through 2035 has already triggered consolidation and tele-ophthalmology rollouts. AI-based screening initiatives now log sensitivities above 92%, reinforcing North America’s leadership in digital health integration.

Asia-Pacific is the fastest-growing region, expanding at a 10.15% CAGR as demographic shifts, urbanization, and rising incomes drive disease incidence and treatment access. Chinese studies indicate diabetic retinopathy prevalence between 24.7% and 43.1% among diagnosed diabetics. India’s SMART DROP protocol illustrates scalable public-health approaches that raise detection in rural districts. Japan and South Korea leverage established reimbursement systems to absorb premium implants and gene therapies, while Southeast Asia focuses on mobile screening units and subsidized biologic procurement. These layered strategies widen the addressable segment of the proliferative diabetic retinopathy market across diverse APAC economies.

Europe, the Middle East and Africa, and South America show varied trajectories. Germany may see diabetes cases climb to 14.2 million by 2040 because of post-pandemic incidence trends. Brazil’s Type 1 diabetes registry recorded a 35.7% retinopathy rate, showing room for expanded retina services. Tele-ophthalmology helps overcome geographic barriers across Pacific Island Countries and Territories, hinting at replication potential for other dispersed geographies.

Competitive Landscape

The proliferative diabetic retinopathy market is moderately concentrated, dominated by Regeneron, Roche/Genentech, and Novartis, each leveraging proprietary biologics, delivery devices, and global sales infrastructure. Genentech secured FDA approval in May 2025 for Susvimo in diabetic retinopathy, offering biannual refills that cut chair time by five-sixths. Regeneron’s high-dose aflibercept pursues longer dosing intervals, while Novartis pairs brolucizumab with customized monitoring programs. Competitive intensity rises as biosimilars obtain interchangeability status in major markets, prompting list-price reductions and bundled contracting.

Device and digital entrants reshape the field. Companies such as Carl Zeiss Meditec and Topcon supply AI-ready fundus cameras that integrate with cloud-based analytics. AbbVie and REGENXBIO advance a one-time sub-retinal gene therapy, potentially disrupting recurrent-injection business models. Technology providers like Alphabet’s Verily collaborate with health systems to embed automated screening into primary-care visits.

Vertical integration accelerates, exemplified by Cencora’s acquisition of Retina Consultants of America, creating purchasing leverage and unified clinical protocols. Pharmacies and insurers experiment with home-delivery biologic services, while big-box retailers open in-store vision centers. Competitive boundaries blur, rewarding firms that combine pharmacology, devices, and data analytics to deliver comprehensive retinal-care solutions.

Proliferative Diabetic Retinopathy Industry Leaders

Novartis AG

Regeneron Pharmaceuticals Inc

Allergan Plc

Hoffmann-La Roche (Genentech)

Oxurion NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Genentech received FDA approval for Susvimo (ranibizumab injection) in diabetic retinopathy, introducing the first continuous delivery therapy with biannual refills.

- April 2025: Oculis completed enrollment in both DIAMOND Phase 3 trials for OCS-01 dexamethasone eye drops targeting diabetic macular edema.

- March 2025: FDA approved revakinagene taroretcel-lwey (ENCELTO) for macular telangiectasia type 2, marking the first encapsulated cell therapy to deliver ciliary neurotrophic factor to the retina.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the proliferative diabetic retinopathy (PDR) market as the global revenue derived from drugs, laser photocoagulation systems, and vitreoretinal surgeries that directly treat retinal neovascularization and its sequelae in patients diagnosed with PDR, irrespective of diabetes type or care setting.

Scope exclusion: diagnostic-only cameras, OCT units, and population-wide screening AI solutions are kept outside this value pool.

Segmentation Overview

- By Treatment Type

- Anti-VEGF Agents

- Corticosteroids

- Laser Surgery

- Vitrectomy

- Sustained-release Implants

- Others

- By Mode of Administration

- Intravitreal

- Sub-retinal

- Topical & Periocular

- By End-User

- Hospitals

- Ophthalmology Clinics

- Ambulatory Surgical Centres

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Several semi-structured interviews with retina surgeons, payor pharmacists, and hospital buyers across North America, Europe, India, and Brazil helped us validate procedure splits, average selling prices, waiting times, and likely adoption of sustained-release implants. Surveys with diabetes educators refined our uptake assumptions for early-stage referral patterns.

Desk Research

We mapped the addressable pool through credible open sources such as the International Diabetes Federation, World Health Organization visual-impairment datasets, United States CDC diabetes statistics, peer-reviewed ophthalmology journals, and trade-association registries like the American Society of Retina Specialists. Company 10-Ks, investor decks, and clinical-trial registries supplied treatment-volume clues. Mordor analysts also leveraged D&B Hoovers for hospital procurement trends and Dow Jones Factiva for regional reimbursement moves. This desk work built the baseline incidence, prevalence, and treated-patient grids that feed our model.

Additional context on anti-VEGF pricing, vitrectomy throughput, and laser console shipments was distilled from Questel patent analytics, WSTS component reports (for laser diodes), and Bestsellingcarsblog vehicle data as a healthcare inflation proxy for Asia. The sources listed illustrate, and are not exhaustive, of the wider literature we interrogated.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort framework converts diagnosed diabetes numbers into eligible PDR cases, which are then adjusted by treatment penetration and retreatment frequency. Bottom-up roll-ups of anti-VEGF unit sales and sampled vitrectomy volumes provide a cross-check before totals are locked. Key variables include adult diabetes prevalence, annual PDR progression rate, anti-VEGF retreatment cycles, laser photocoagulation sessions per eye, and regional public-insurance coverage ceilings. Five-year forecasts employ multivariate regression blended with scenario analysis on biosimilar pricing shocks and AI-enabled early detection.

Data Validation & Update Cycle

Outputs pass variance checks against historical procedure counts, analyst peer review, and a senior-level sign-off. The model is refreshed annually, with interim updates triggered by drug approvals, reimbursement shifts, or sudden epidemiological events.

Why Our Proliferative Diabetic Retinopathy Baseline Commands Reliability

Published estimates diverge because firms pick different disease stages, bundle diagnostics, or apply uniform drug-pricing curves.

Key gap drivers include some studies folding non-proliferative disease revenues into totals, others applying aggressive ASP erosion without checking hospital purchase contracts, and many using biennial refreshes that miss biosimilar launches. Mordor's tighter scope, yearly update cadence, and dual-path validation minimize such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.72 bn (2025) | Mordor Intelligence | - |

| USD 2.70 bn (2025) | Regional Consultancy A | Limited geography weighting; assumes uniform retreatment frequency |

| USD 4.32 bn (2024) | Global Consultancy B | Bundles screening devices and postoperative care revenues |

| USD 10.08 bn (2025) | Industry Journal C | Reports whole diabetic retinopathy continuum, inflating base |

These comparisons show that when scope creep and infrequent updates are stripped away, Mordor Intelligence provides a balanced, transparent baseline aligned to real-world treatment flows and repeatable data points.

Key Questions Answered in the Report

What is the current Proliferative Diabetic Retinopathy Market size?

The proliferative diabetic retinopathy market is valued at USD 2.95 billion in 2026.

Who are the key players in Proliferative Diabetic Retinopathy Market?

Novartis AG, Regeneron Pharmaceuticals Inc, Allergan Plc, Hoffmann-La Roche (Genentech) and Oxurion NV are the major companies operating in the Proliferative Diabetic Retinopathy Market.

Which is the fastest growing region in Proliferative Diabetic Retinopathy Market?

Rapid diabetes incidence, aging populations, and rising healthcare spending push Asia-Pacific growth to a 10.15% CAGR.

Which treatment type leads revenue today?

Anti-VEGF biologics hold 66.78% of proliferative diabetic retinopathy market share.

Page last updated on: