Eye Infection Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.47 Billion |

| Market Size (2031) | USD 10.17 Billion |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

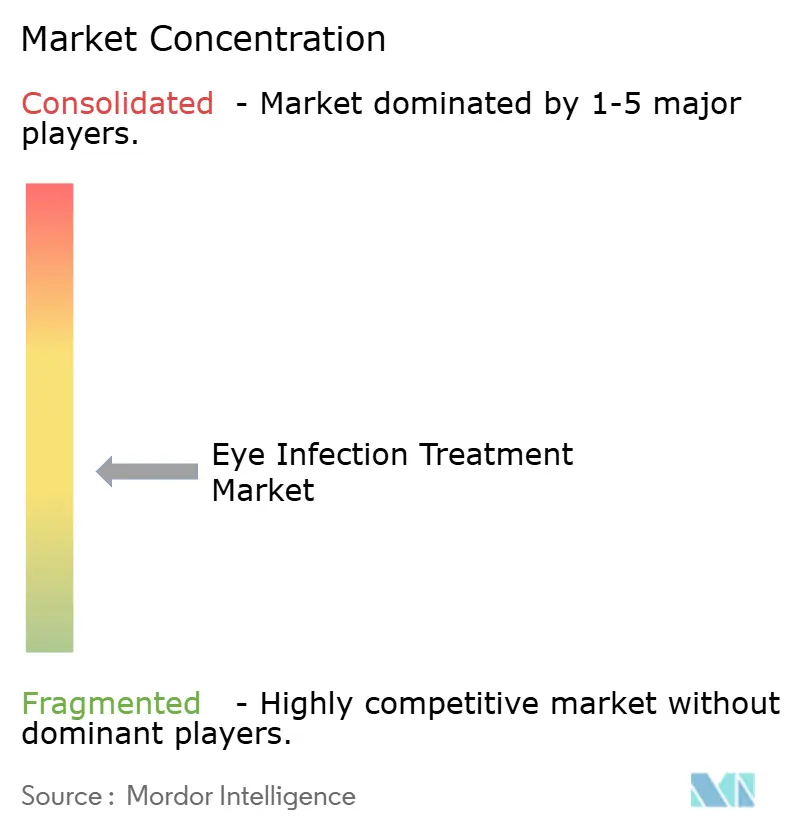

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Eye Infection Treatment Market Analysis by Mordor Intelligence

The Eye infection treatment market size is expected to increase from USD 8.47 billion in 2026 to USD 10.17 billion by 2031, growing at a 3.74% CAGR over 2026-2031. Population aging, expanding surgical prophylaxis volumes, and wider contact-lens use in emerging economies are lifting demand, yet generic erosion of legacy fluoroquinolones and mounting antimicrobial resistance are holding overall revenue growth to the low single digits. Antiviral therapies, especially ganciclovir gel for herpes simplex keratitis, are securing disproportionate gains as recurrent viral infections rise among immunosenescent cohorts. Sustained-release delivery platforms are also advancing, driven by dropless cataract protocols that appeal to payers focused on real-world adherence. Conversely, tariff-driven active-pharmaceutical-ingredient (API) cost spikes have inflated sterile-fill expenses, compressing margins for preservative-free brands.

Key Report Takeaways

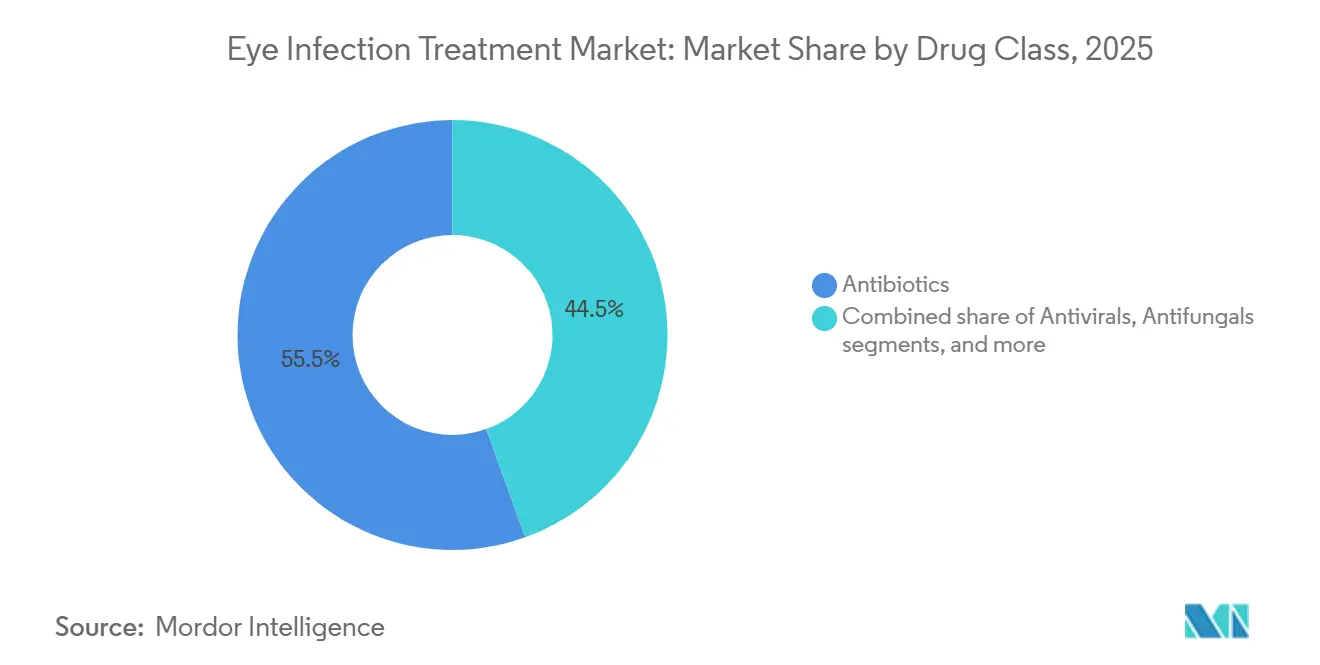

- By drug class, antibiotics led with 55.55% revenue share of the Eye infection treatment market in 2025, while antivirals are projected to expand at a 7.25% CAGR through 2031.

- By indication, conjunctivitis accounted for 34.53% of Eye infection treatment market share in 2025 and keratitis is advancing at an 8.75% CAGR to 2031.

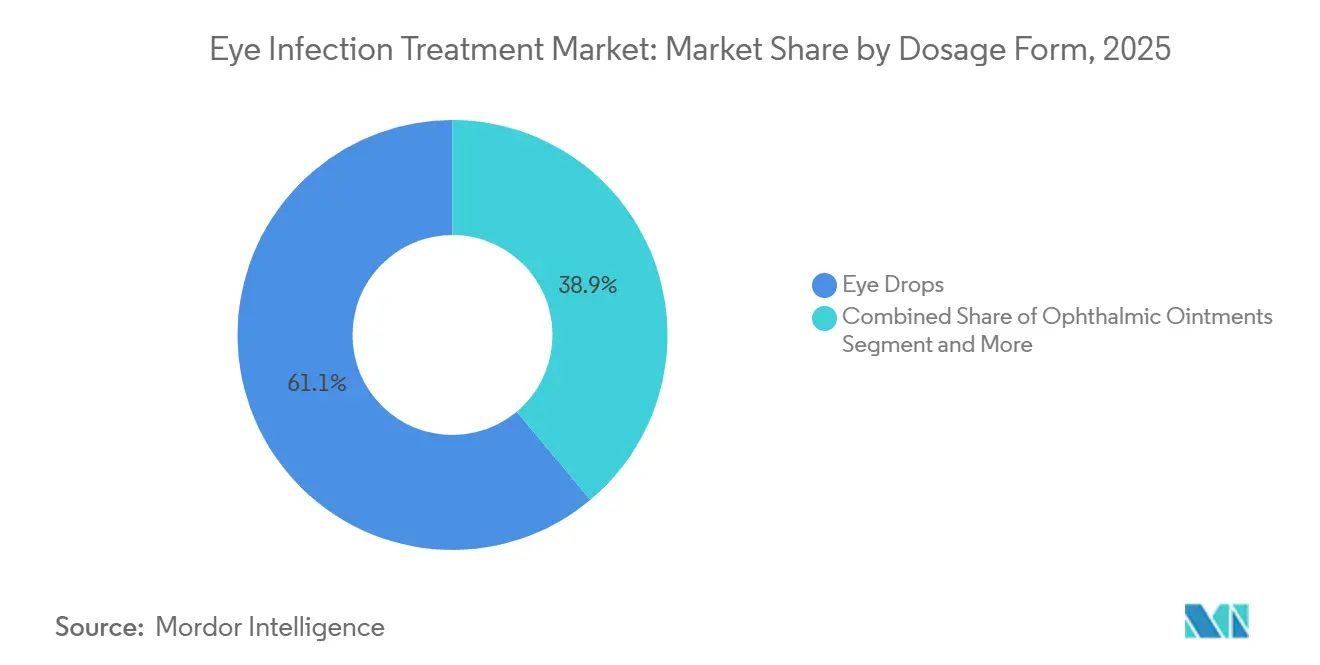

- By dosage form, eye drops controlled 61.15% of 2025 revenue, whereas sustained-release implants are forecast to grow at a 9.82% CAGR to 2031.

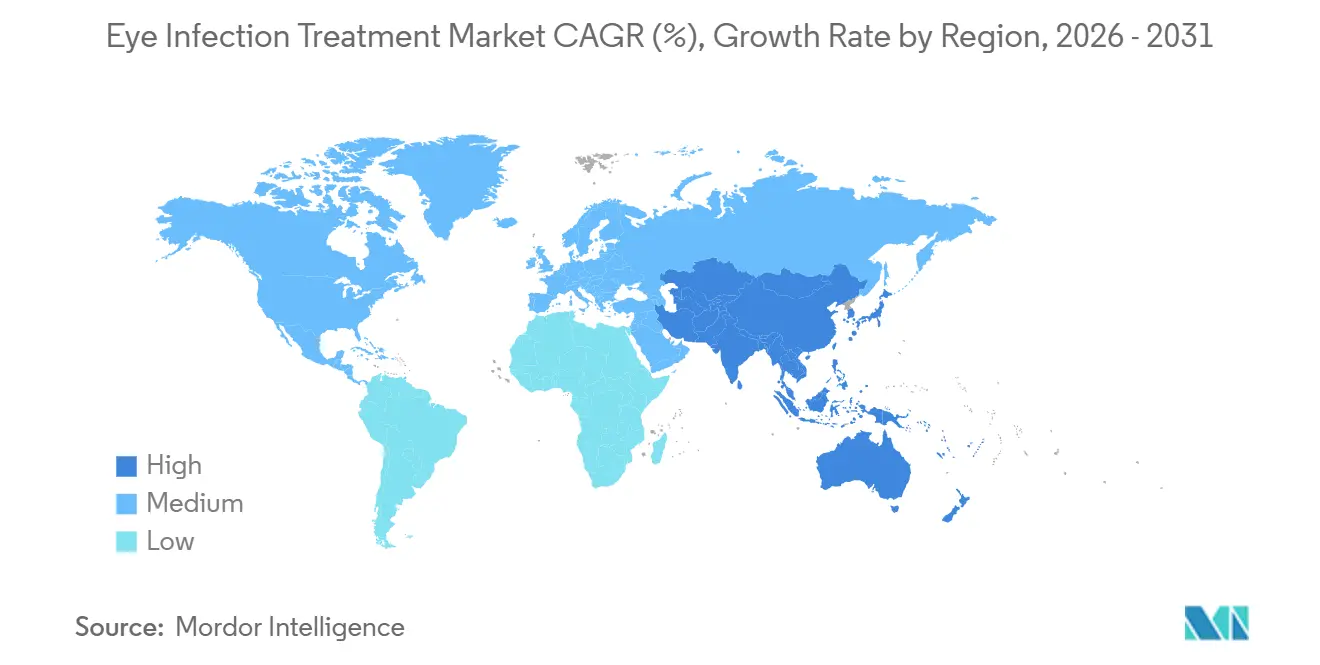

- By geography, North America captured 38.23% of 2025 revenue, while Asia-Pacific is on track for a 7.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Eye Infection Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-linked rise in bacterial and viral infections | +0.9% | Global, most acute in North America, Europe, Japan | Long term (≥ 4 years) |

| Growing contact-lens penetration in emerging economies | +0.7% | India, China, Southeast Asia, Latin America | Medium term (2-4 years) |

| Rapid uptake of preservative-free eye-drop formats | +0.5% | North America, Western Europe, Japan | Short term (≤ 2 years) |

| Post-operative prophylaxis from cataract and LASIK surgery | +0.8% | Global, with concentration in U.S., Europe, China, India | Medium term (2-4 years) |

| Hospital antibiotic-stewardship rules favoring topical agents | +0.4% | North America, European Union, Australia | Short term (≤ 2 years) |

| AI-enabled tele-ophthalmology for early detection | +0.3% | Rural India and China, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging-Linked Rise in Bacterial & Viral Ocular Infections

Geriatric immunosenescence is widening the susceptible pool for both bacterial conjunctivitis and herpes simplex keratitis. A Lancet Healthy Longevity study reported a doubling of Staphylococcus aureus ocular-surface colonization in adults aged 70-85 years compared with those aged 40-55 years. United Nations data indicate that the global ≥ 65 population will reach 1.6 billion by 2030, locking in a long-duration demand up-cycle for topical antibiotics and antivirals. Higher recurrence rates among older patients—28% within 12 months—are amplifying prescription volumes of ganciclovir and valacyclovir. Japan, Italy, and Germany already have ≥ 25% aging penetration, making them focal markets for advanced antiviral delivery.

Growing Contact-Lens Penetration in Emerging Economies

Contact-lens uptake in India, China, and Southeast Asia is outstripping hygiene education, with microbial keratitis cases up 18% in 2024-2025 according to the All India Ophthalmological Society[1]All India Ophthalmological Society, “Contact-Lens-Related Keratitis Surveillance 2024-2025,” aios.org. Retailer Lenskart performed 6 million eye tests in 2024, fueling first-time lens adoption but also greater exposure to Pseudomonas aeruginosa and Acanthamoeba. A Cornea journal study found overnight lens wear in 42% of Indian cases, accelerating demand for broad-spectrum fluoroquinolones. China’s e-commerce boom and lenient lens-solution standards have similarly spurred fungal keratitis spikes, shaping a robust consumption curve for fortified antibiotics and antifungals.

Rapid Uptake of Preservative-Free Eye-Drop Formats

Benzalkonium-chloride toxicity concerns have pulled ophthalmologists toward single-dose, preservative-free vials. U.S. FDA guidance in 2024 tightened biocompatibility testing, prompting reformulations across legacy brands[2]U.S. Food and Drug Administration, “Guidance for Ophthalmic Products 2024,” fda.gov . Early adopters include Bausch+Lomb’s preservative-free moxifloxacin, which reached 12% European share within six months of launch. Although the shift imposes a 25-30% price premium, surgeons in cataract and refractive centers accept higher costs to accelerate epithelial recovery, sustaining a premium segment within the Eye infection treatment market.

Post-Operative Prophylaxis Volumes From Rising Cataract & LASIK Surgeries

Global cataract procedures topped 20 million in 2024, with intracameral injections endorsed by the European Society of Cataract and Refractive Surgeons lowering endophthalmitis risk by 75%. Single-dose cefuroxime and moxifloxacin injections command higher per-procedure pricing, partly offsetting the decline in multi-day topical courses. LASIK and PRK surgeries, totaling 2.1 million in 2024, still depend on 3-7-day topical regimens, supporting baseline fluoroquinolone volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating antimicrobial resistance in ocular pathogens | -0.6% | Global hot spots in South Asia and Sub-Saharan Africa | Long term (≥ 4 years) |

| Patent cliffs and generic erosion of fluoroquinolones | -0.4% | North America, Europe, Japan | Short term (≤ 2 years) |

| Tariff-driven API supply-chain shocks | -0.3% | North America, Europe | Medium term (2-4 years) |

| Climate-linked fungal keratitis outbreaks | -0.2% | South Asia, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Antimicrobial Resistance in Ocular Pathogens

Methicillin-resistant Staphylococcus aureus now constitutes 30% of bacterial keratitis isolates, eroding first-line fluoroquinolone efficacy and forcing off-label fortified vancomycin use[3]World Health Organization, “Antimicrobial Resistance Surveillance Report 2024,” who.int. Pseudomonas aeruginosa resistance to ciprofloxacin climbed to 18% in 2025 among contact-lens wearers, more than doubling the 2020 figure. Absence of Phase III ophthalmic-specific antibiotics underscores a looming innovation vacuum.

Patent Cliffs & Generic Erosion for Legacy Fluoroquinolone Brands

Moxifloxacin ophthalmic solutions lost U.S. exclusivity in 2021, and by 2025 generics held 87% of unit share at 70-80% lower prices. Similar dynamics for gatifloxacin and levofloxacin cut branded promotional spending, redirecting multinational capital toward devices and dry-eye therapies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Antivirals Outpace Antibiotics Despite Smaller Base

Antibiotics held 55.55% of 2025 revenue, underscoring their frontline role, yet antivirals are projected to grow at 7.25% CAGR and are steadily closing the absolute-dollar gap as herpes simplex keratitis recurrence escalates among aging populations. The Eye infection treatment market size for antivirals is on track to surpass USD 2 billion by 2031, aided by once-daily ganciclovir gel adherence advantages. Antifungals remain niche, though climate-driven outbreaks provide a modest 4.2% CAGR tailwind.

Combination products blending antibiotics with corticosteroids add convenience in post-operative settings, while preservative-free repositioning of legacy fluoroquinolones is partially buffering price erosion. Portfolio bifurcation is evident: innovators chase premium antivirals and sustained-release classes, whereas generics concentrate on high-volume antibiotic staples.

By Indication: Keratitis Surges on Contact-Lens and Climate Pressures

Conjunctivitis retained 34.53% of Eye infection treatment market share in 2025, but keratitis’s 8.75% CAGR through 2031 makes it the expansion engine. Urban contact-lens wearers in India registered six-fold higher keratitis risk than non-wearers, with Pseudomonas and Acanthamoeba dominating cultures. Endophthalmitis, although rare, commands premium-priced intravitreal regimens that buoy revenue per patient.

Blepharitis and stye cases remain low-value because warm compresses suffice in most instances, whereas viral keratitis demands long-term antiviral maintenance, adding durable revenue streams. Climate-amplified fungal keratitis is surfacing as a high-severity niche, pointing to latent upside for next-generation azoles should pipeline activity resume.

By Dosage Form: Sustained-Release Platforms Disrupt Eye-Drop Dominance

Eye drops still accounted for 61.15% of 2025 revenue thanks to low production costs and ingrained prescriber habits, yet adherence studies show only 60% completion of multi-dose regimens. The surgically-placed Durysta implant validated biodegradable depots, catalyzing a 9.82% CAGR for sustained-release formats through 2031. Prices are higher, but payers appreciate reduced nursing time for post-operative instillation, reinforcing uptake among cataract clinics.

Ointments serve pediatric and night-time segments, though vision blurring limits daytime preference. Oral tablets cover orbital cellulitis and severe endophthalmitis but face displacement by intravitreal injections in tertiary centers. The dosage-form pivot toward depots aligns with payer priorities on adherence and with surgeon demand for dropless workflow efficiency.

Geography Analysis

Asia-Pacific leads volume growth with a 7.42% CAGR, driven by India’s large population, China’s aging burden, and rising contact-lens adoption across Southeast Asia. Low manufacturing costs let Indian producers supply 40% of global ophthalmic antibiotic volumes, though average realized prices are up to 75% below North American equivalents. China’s 2024-2025 domestic approvals accelerated import substitution and intensified price competition for multinationals.

North America retained 38.23% market share in 2025 because premium preservative-free products and high cataract-surgery rates sustain value per patient. The United States also adopted intracameral injections in select centers, redistributing revenue from topical drops to single-dose vials.

Europe recorded mid-single-digit growth, anchored by Germany, the U.K., and France. Strict EMA generic timelines slowed price erosion, but widespread intracameral prophylaxis underpinned demand for cefuroxime syringes. The Middle East and Africa, though smaller, are upgrading ophthalmic capacity, especially across Gulf Cooperation Council states. Latin America’s public procurement volatility tempers growth, yet localized producers in Mexico and Brazil are filling supply gaps.

Competitive Landscape

The sector remains moderately fragmented. Alcon, Bausch+Lomb, Novartis, Sun Pharmaceutical Industries, and Santen together command a meaningful but not dominant position, while a long tail of regional generics producers chips away at incumbent share. Multinationals are pivoting toward sustained-release implants, combination drops, and digital-diagnostic add-ons, abandoning low-margin commoditized antibiotics. Indian and Chinese firms leverage WHO-prequalified plants and export pricing to scale volume.

White-space opportunities persist in ophthalmic antifungals, pediatric dosage forms, and high-penetration antivirals. Santen’s 2024 purchase of Eyevance secured mucus-penetrating particle technology that boosts bioavailability 2.3-fold in preclinical models. Regulatory compliance costs under FDA 21 CFR Part 11 and EMA Annex 1 favor scale players, yet smaller contract manufacturers are closing gaps through quality-assurance partnerships.

Technology differentiation is emerging: AI-assisted diagnostics shorten time-to-treatment in underserved markets and may embed device-drug ecosystems. Pipeline innovation remains thin, however, as industry R&D spend runs at 8-10% of revenue, well below oncology benchmarks. Government pull incentives like the proposed U.S. PASTEUR Act could shift this calculus.

Eye Infection Treatment Industry Leaders

Alcon AG

Bausch + Lomb (Bausch Health)

Novartis AG

Sun Pharmaceutical Industries Ltd.

Santen Pharmaceutical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: L V Prasad Eye Institute and Bose Institute unveiled SA-XV, a 15-residue peptide with promising fungicidal activity in keratitis models.

- April 2025: Okogen submitted an Indian Phase IIb protocol for OKG-0303, a triple-active eyedrop targeting both viral and bacterial conjunctivitis.

Global Eye Infection Treatment Market Report Scope

Eye infections occur when harmful microorganisms affect any part of the eyeball or surrounding area. This includes the clear front surface of the eye (cornea) and the thin, moist membrane lining the outer eye and inner eyelids (conjunctiva). Various methods are used to treat eye infections.

The segmentation of the eye infection treatment market is categorized by drug class, indication, dosage form, and geography. By drug class, the market includes antibiotics, antivirals, antifungals, antihistamines, corticosteroids, glucocorticoids, and combination therapies. By indication, it covers conjunctivitis, keratitis, endophthalmitis, blepharitis, stye (hordeolum), uveitis, cellulitis, and ocular herpes. By dosage form, the segmentation includes eye drops, ophthalmic ointments, tablets/capsules, sustained-release implants and inserts, and other forms. Geographically, the market is divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the value (USD) for all the above segments.

| Antibiotics |

| Antivirals |

| Antifungals |

| Antihistamines |

| Corticosteroids |

| Glucocorticoids |

| Combination Therapies |

| Conjunctivitis |

| Keratitis |

| Endophthalmitis |

| Blepharitis |

| Stye (Hordeolum) |

| Uveitis |

| Cellulitis |

| Ocular Herpes |

| Eye Drops |

| Ophthalmic Ointments |

| Tablets / Capsules |

| Sustained-Release Implants & Inserts |

| Other Forms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Antibiotics | |

| Antivirals | ||

| Antifungals | ||

| Antihistamines | ||

| Corticosteroids | ||

| Glucocorticoids | ||

| Combination Therapies | ||

| By Indication | Conjunctivitis | |

| Keratitis | ||

| Endophthalmitis | ||

| Blepharitis | ||

| Stye (Hordeolum) | ||

| Uveitis | ||

| Cellulitis | ||

| Ocular Herpes | ||

| By Dosage Form | Eye Drops | |

| Ophthalmic Ointments | ||

| Tablets / Capsules | ||

| Sustained-Release Implants & Inserts | ||

| Other Forms | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which drug class is growing fastest in the Eye infection treatment market?

Antiviral therapies are projected to grow at about 7.25% CAGR through 2031, fueled by recurrent herpes simplex and adenoviral infections in aging populations.

Why is keratitis attracting higher growth than conjunctivitis?

Contact-lens expansion in India and China and rising climate-linked fungal cases are driving an 8.75% CAGR for keratitis, well above conjunctivitiss trajectory.

How are sustained-release platforms changing treatment patterns?

Depot implants and inserts cut post-surgical drop schedules, improving adherence, and are forecast to grow nearly 10% annually, challenging eye-drop dominance.

Which region offers the strongest volume upside?

Asia-Pacific delivers the fastest regional CAGR at 7.42% due to large populations, expanding surgery capacity, and accelerated generic approvals.

What is the key restraint threatening market growth?

Escalating antimicrobial resistance, with MRSA comprising 30% of keratitis isolates, is eroding the efficacy of established antibiotics and curbing market expansion.

Page last updated on: