Advanced Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

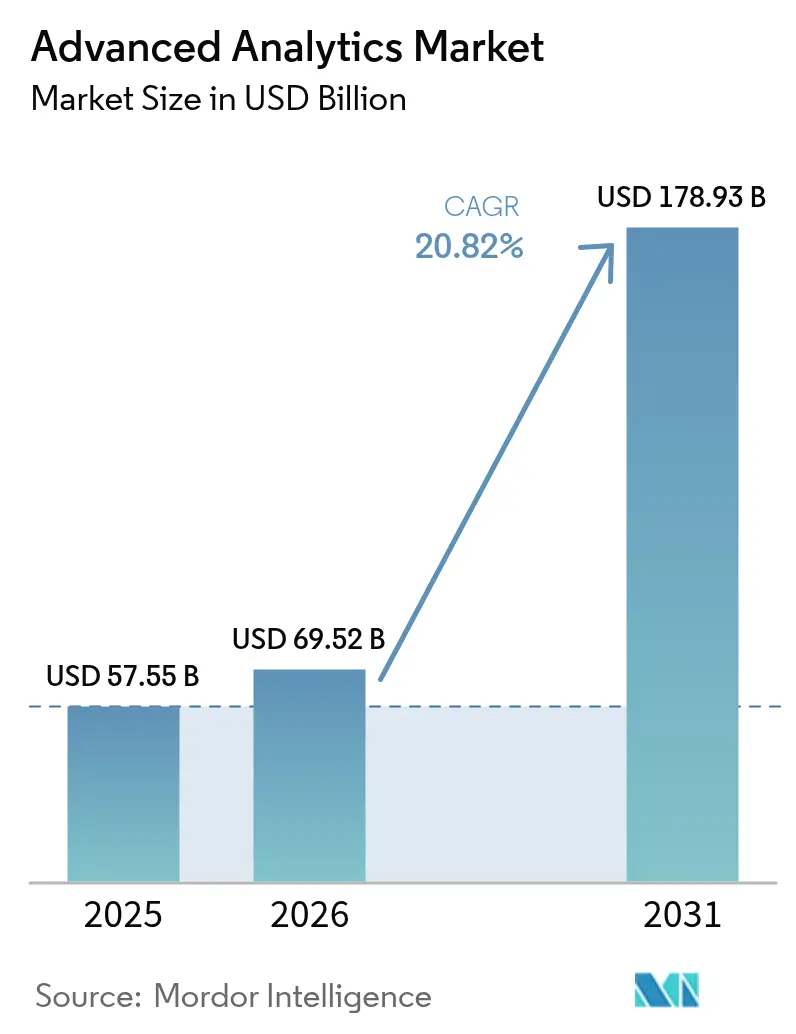

| Market Size (2026) | USD 69.52 Billion |

| Market Size (2031) | USD 178.93 Billion |

| Growth Rate (2026 - 2031) | 20.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Analytics Market Analysis by Mordor Intelligence

The advanced analytics market size in 2026 is estimated at USD 69.52 billion, growing from 2025 value of USD 57.55 billion with 2031 projections showing USD 178.93 billion, growing at 20.82% CAGR over 2026-2031. Surging data volumes, falling AI infrastructure costs, and urgent requirements for real-time decision support continue to expand adoption across industries. Rising fraud sophistication is accelerating demand for predictive, risk, and graph analytics, while platform consolidation is reducing customer switching costs and encouraging multi-function deployments. Edge processing is now critical for latency-sensitive use cases such as autonomous systems and industrial automation, lifting edge-analytics growth ahead of other segments. Simultaneously, explainable AI regulation in the EU is redirecting investment toward transparent, auditable models, granting compliant vendors an early-mover advantage. [1]Mesh Flinders, Ian Smalley, and Josh Schneider, “AI Fraud Detection in Banking,” IBM, ibm.com

Key Report Takeaways

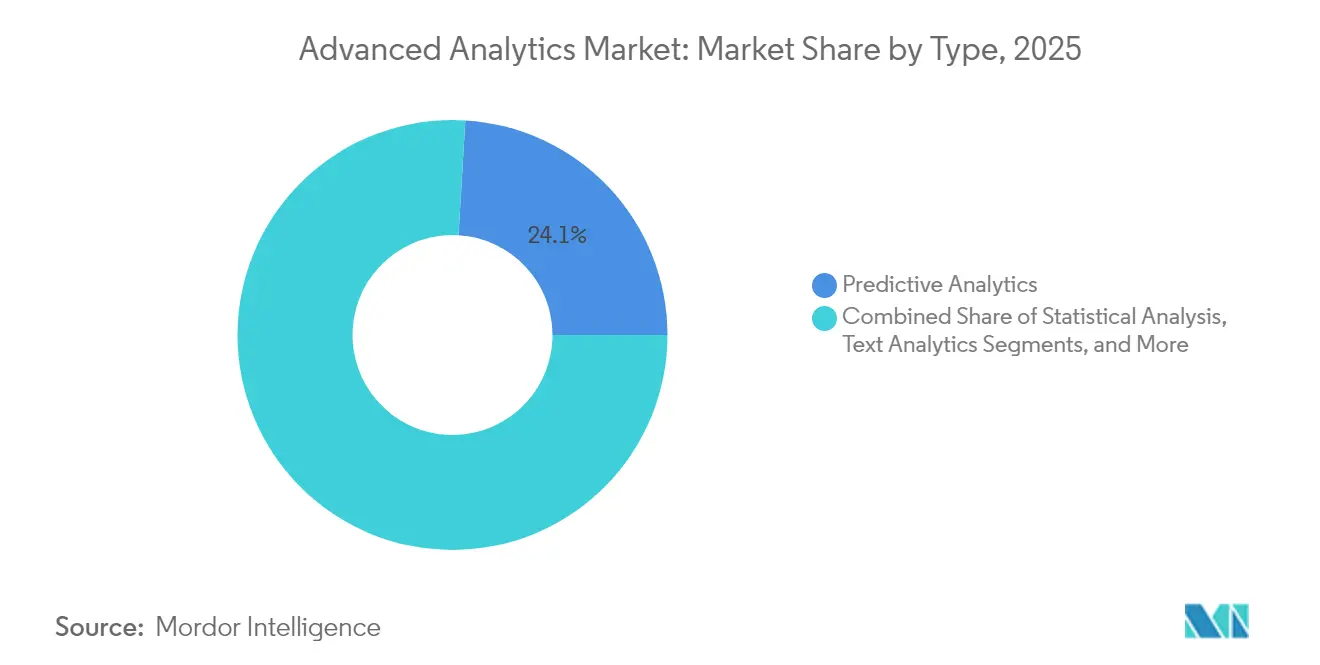

- By type, Predictive Analytics led with 24.05% of advanced analytics market share in 2025, whereas Edge Analytics is advancing at a 27.35% CAGR through 2031.

- By deployment mode, On-Premises captured 53.40% revenue share in 2025, while Cloud is projected to expand at 23.95% CAGR to 2031.

- By component, Solutions commanded 61.25% of the advanced analytics market size in 2025; Services are rising at a 22.90% CAGR through 2031.

- By business function, Sales & Marketing held 28.55% of the advanced analytics market size in 2025, but Operations & Supply-Chain will grow fastest at 22.85% CAGR.

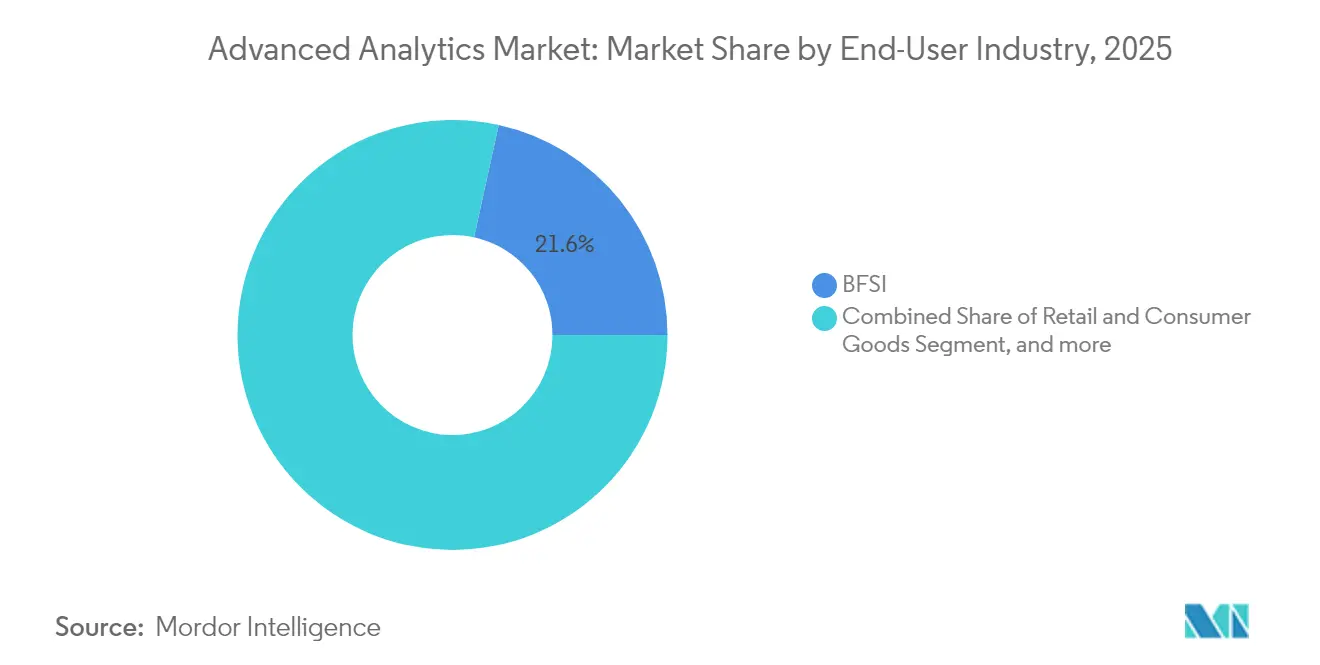

- By end-user industry, BFSI accounted for 21.55% of advanced analytics market share in 2025, whereas Healthcare & Life Sciences is growing at 23.70% CAGR.

- By organization size, Large Enterprises generated 65.10% revenue in 2025, yet SMEs are scaling at a 24.10% CAGR through 2031.

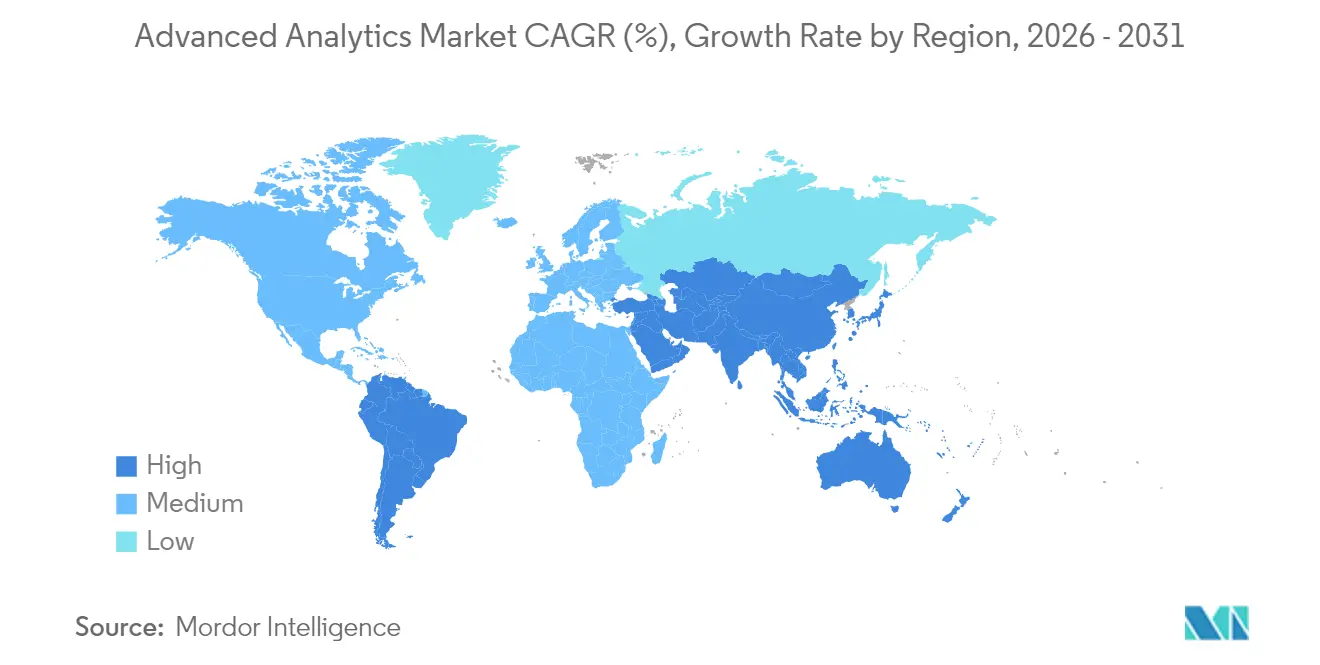

- By geography, North America retained 40.65% revenue share in 2025; APAC is forecast to climb at a 22.40% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Advanced Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating fraud-detection needs | +4.2% | Global, with concentration in North America and EU | Short term (≤ 2 years) |

| Big-data volume and complexity explosion | +5.8% | Global | Medium term (2-4 years) |

| Enterprise digital-transformation wave | +6.1% | North America, Europe, APAC core | Medium term (2-4 years) |

| Rapid AI/ML and cloud cost declines | +3.9% | Global | Short term (≤ 2 years) |

| Edge analytics for real-time decisions | +4.7% | APAC, North America | Long term (≥ 4 years) |

| Regulatory push for explainable AI | +2.8% | EU, with spillover to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Fraud-Detection Needs

Financial institutions face highly sophisticated fraud threats that outpace rule-based systems. U.S. regulators urge AI-driven monitoring, and machine-learning models already lift detection accuracy by 40% while halving false positives. IBM research shows 95% classification accuracy when large-scale transaction data is analysed in near real time. Hybrid cloud-edge architectures satisfy sub-second latency requirements and create opportunities for providers bundling fraud analytics, compliance dashboards, and model governance into unified platforms.

Big-Data Volume & Complexity Explosion

Enterprises generated 328.77 million TB daily in 2024, overwhelming traditional BI tooling. Nearly half now employ hybrid storage and data-fabric approaches to integrate siloed sources for advanced analytics market deployments. By 2025, more than 50% of critical processing is expected outside conventional data centers, reinforcing the need for automated data preparation and augmented analytics that expose insights to non-technical business users.

Enterprise Digital-Transformation Wave

AI-first strategies are replacing incremental digitization. While 92% of companies intend to raise AI spending, only 1% deem themselves mature, elevating demand for expert implementation partners and low-code development features that speed time-to-value. Hyperautomation—where analytics, RPA, and decision models converge—further magnifies platform requirements and underpins the 23.60% services CAGR.

Regulatory Push for Explainable AI

The EU AI Act enforces algorithmic transparency, costing enterprises EUR 52,227 per high-risk AI model annually. Vendors embedding explainability and audit trails directly into analytics pipelines gain a foothold, especially within finance and critical-infrastructure domains. Extraterritorial provisions extend these obligations to global providers, elevating transparent platforms from optional to essential. [3]European Commission, “AI Act | Shaping Europe’s Digital Future,” European Union, digital-strategy.ec.europa.eu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data integration and connectivity gaps | -3.4% | Global, particularly in legacy-heavy industries | Medium term (2-4 years) |

| Shortage of data-science talent | -2.8% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Sustainability limits on compute energy | -1.9% | EU, California, with global implications | Long term (≥ 4 years) |

| Vendor lock-in to hyperscale clouds | -2.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Integration & Connectivity Gaps

Fragmented architectures often trap data across aging on-premises, cloud, and operational-technology systems. Organizations allocate 64% of engineering time to integration rather than analysis, delaying returns and dampening enthusiasm for large-scale projects. Industrial firms battle proprietary protocols that complicate analytics linkages, reinforcing the premium placed on data-fabric and no-code integration solutions.

Shortage of Data-Science Talent

Universities do not graduate enough professionals skilled in statistics, coding, and domain knowledge. Smaller firms struggle to attract scarce experts, so they adopt automated ML and managed-service models, fuelling the services CAGR. Remote hiring alleviates location constraints yet introduces coordination overhead that prolongs deployment cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Edge Analytics Drives Highest CAGR

Edge Analytics owns a 27.35% CAGR to 2031, reflecting its role in latency-critical IoT scenarios. In contrast, Predictive Analytics retained 24.05% advanced analytics market share in 2025 as the mainstream choice for forecasting. Edge devices perform localized inference, cutting network costs and ensuring data sovereignty, which is vital for regulated verticals. Automotive, energy, and manufacturing players are embedding compact inference chips to enable anomaly detection and autonomous control loops. Vendors differentiate through federated-learning capabilities that train global models without raw-data egress. Text and Visual Analytics hold steady adoption as unstructured data volumes balloon, while Prescriptive and Risk Analytics are spurred by demand for optimization and scenario modelling.

The advanced analytics market size for Edge Analytics is poised to expand rapidly as 5G coverage broadens. Critical infrastructure owners shift from centralized clouds to distributed mesh fabrics that push decision logic to turbines, substations, and vehicles. Meanwhile, established predictive platforms are integrating real-time data streams to avoid obsolescence, illustrating the market’s pivot toward hybrid cloud-edge designs

By Deployment Mode: Cloud Growth Outpaces On-Premises

On-Premises architectures, favored by banks and public agencies, accounted for 53.40% revenue in 2025 largely due to data-sovereignty mandates. Still, Cloud deployment is rising at 23.95% CAGR as enterprises pursue elastic scaling and pay-as-you-go economics. Hyperscalers prioritize GPU fleet expansion, though intermittent capacity shortfalls create openings for specialized analytics clouds and colocation-edge hybrids.

Security improvements and confidential-compute services steadily erode customer objections. The advanced analytics market size for cloud workloads gains further lift from managed model-ops suites that automate drift detection, versioning, and governance. Hybrid scenarios blend sensitive on-premises data processing with burst-to-cloud training cycles, ensuring compliance without capping innovation. Regional data-residency laws now shape provider buildouts, particularly in the EU and APAC, where in-country zones address privacy statutes.

By Component: Services Reflect Complexity

Solutions platforms generated 61.25% of revenue in 2025 by bundling visualization, data prep, and model-building features. Yet the services segment accelerates at 22.90% CAGR because enterprises need road-mapping, change management, and industry-specific model tuning. Consulting teams specialize in regulated sectors, delivering explainability, bias testing, and scenario analysis for auditors. As customer churn shifts toward outcome-based engagements, managed-service contracts secure multi-year recurring fees.

The advanced analytics market size for professional services grows alongside platform spending as firms outsource continuous model refinement and integration. Hyperscalers now embed partner ecosystems to co-deliver vertical templates, compressing deployment timelines. Meanwhile, open-source frameworks push software margins lower, intensifying competition on advisory and managed offerings.

By Business Function: Operations Analytics Gains Momentum

Sales & Marketing led revenue in 2025 by targeting personalization and campaign optimization use cases. Operations & Supply-Chain analytics, however, is projected to record a 22.85% CAGR, as inflationary pressure compels real-time cost control. Predictive maintenance and dynamic inventory balance algorithms drive manufacturing savings of 10%-20%. Finance & Risk teams continue to expand model-driven compliance reporting, while HR analytics grows via retention pattern mining and DEI metrics.

The advanced analytics market responds with cross-functional platforms unifying data definitions and metrics libraries. Integrated suites allow frontline staff to embed visual insights within workflow apps, amplifying adoption beyond analytics centers of excellence. Citizen-developer features further reduce IT bottlenecks and accelerate experimentation cycles.

By End-User Industry: Healthcare Accelerates

BFSI dominated in 2025 with 21.55% revenue share due to fraud, AML, and credit-risk workloads. Healthcare & Life Sciences, backed by FDA clearance for 223 AI-enabled devices, leads growth at 23.70% CAGR. Clinical decision support, imaging analysis, and personalized medicine all require transparent, high-accuracy models compliant with health regulations.

Manufacturers leverage digital twins and predictive yield analytics to trim waste, while Retailers deploy recommendation engines and price-optimization tools. Telecom providers rely on network anomaly detection, and Energy utilities use grid-state prediction to balance renewables. Defence agencies pursue intelligence fusion and autonomous systems, though procurement complexity slows volume scaling.

By Organization Size: SMEs Scale Rapidly

Large Enterprises captured 65.10% revenue in 2025 by funding multi-function deployments and maintaining skilled data-science teams. Small and Mid-Sized Enterprises lift adoption at 24.10% CAGR due to SaaS subscription pricing and automated ML that hides complexity. Citizen-data-scientist features accelerate ROI for resource-constrained firms, broadening the advanced analytics market footprint.

Vendor roadmaps increasingly target SMEs with industry-specific starter kits and usage-based billing. Services partners bundle quick-start packages combining data integration, template dashboards, and continuous tuning, shortening sales cycles. Talent shortages hit SMEs hardest, boosting demand for managed analytics that supply both technology and expertise.

Geography Analysis

North America continued to command 40.65% of advanced analytics market revenue in 2025. Venture capital channelled USD 109.1 billion into AI, including USD 33.9 billion for generative models, expanding startup ecosystems and enterprise experimentation. U.S. hyperscalers address prior capacity constraints by injecting new GPU clusters, with Amazon’s USD 20 billion Pennsylvania build-out illustrating the scale of investment. Regulatory initiatives, though numerous, remain fragmented, prompting demand for governance add-ons that interpret divergent federal and state requirements.

APAC posts the highest 22.40% CAGR, propelled by manufacturing automation, 5G rollouts, and government smart-city grants. Chinese AI-model enhancements create competitive domestic alternatives, while India’s IT-services exports deliver implementation talent to regional manufacturers. Japan and South Korea push deep into edge-analytics applications for industrial robotics and autonomous mobility. Lower total-cost-of-ownership and public-sector digitalization policies expand the advanced analytics market across Southeast Asian nations integrating ecommerce, fintech, and logistics platforms.

Europe grows steadily under rigorously evolving policy. The EU AI Act accelerates purchases of explainable platforms to satisfy transparency rules, especially in critical sectors. Germany’s automotive and machinery firms adopt predictive and prescriptive analytics for Industry 4.0, while Nordic utilities embed sustainability analytics to optimize renewables. United Kingdom financial institutions invest in risk-model governance post-Brexit. The advanced analytics market size in Europe benefits from cross-border data-space initiatives that harmonize sharing standards among member states, yet compliance workloads elongate deployment cycles.

Competitive Landscape

The advanced analytics market features moderate fragmentation. Incumbent platform providers IBM, Microsoft, SAS, and Oracle exploit broad portfolios and entrenched enterprise relationships. Hyperscalers AWS, Google Cloud, and Microsoft Azure add pressure by offering integrated compute, storage, and managed model services, eroding traditional licensing models. Disruptors focus on automated machine learning, domain-specific cloud analytics, and real-time edge-processing stacks.

Platform consolidation shapes strategy: vendors acquire adjacent capabilities such as data-fabric layers, MLOps orchestration, and embedded BI to lock in customers. FICO’s awards program spotlights ecosystem partners Fujitsu, TSYS, and TCS that extend its platform into regional niches. USPTO’s AI strategy underlines government interest in protecting domestic AI innovations, indirectly bolstering R&D commitments. Competition revolves around feature completeness, cloud portability, and regulatory compliance assurances.

Price competition intensifies as open-source frameworks reach enterprise maturity, shifting differentiation toward service level guarantees and domain expertise. Edge-analytics specialists pitch ultra-low latency and ruggedized form factors, winning pilots in manufacturing and energy. Meanwhile, consultancies team with software vendors to deliver turnkey outcomes, capturing services revenue that traditional license sellers risk losing.

Advanced Analytics Industry Leaders

IBM Corporation

SAS Institute Inc.

SAP SE

Oracle Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amazon invested USD 20 billion in Pennsylvania to scale AI infrastructure and create 1,250 skilled jobs, alleviating GPU shortages and supporting advanced analytics workloads.

- June 2025: Snowflake launched next-generation compute and AI-driven data governance to speed hybrid analytics.

- June 2025: NTT DATA introduced AI-powered Software Defined Infrastructure for Cisco, enabling real-time insights across enterprise networks.

- May 2025: FICO honored Fujitsu, TSYS, and TCS for advanced analytics excellence within its partner ecosystem.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the advanced analytics market as all software platforms and associated services that apply predictive, prescriptive, and cognitive techniques to structured or unstructured data so enterprises can anticipate outcomes and automate decisions. Revenues from licenses, subscriptions, maintenance, and managed analytic services sold to organizations of every size and sector are included.

Scope exclusion: We exclude basic descriptive business intelligence dashboards or standalone visualization tools.

Segmentation Overview

- By Type

- Statistical Analysis

- Text Analytics

- Risk Analytics

- Predictive Analytics

- Prescriptive Analytics

- Visual Analytics

- Network Analytics

- Geospatial Analytics

- Social Media Analytics

- Edge Analytics

- Other Types

- By Deployment Mode

- On-Premise

- Cloud

- Hybrid

- By Component

- Solutions

- Services

- Consulting

- Managed Services

- By Business Function

- Sales and Marketing

- Finance and Risk

- Operations and Supply-Chain

- Human Resources

- Customer Support

- By End-User Industry

- BFSI

- Retail and Consumer Goods

- Healthcare and Life Sciences

- IT and Telecommunication

- Transportation and Logistics

- Government and Defense

- Manufacturing

- Energy and Utilities

- Media and Entertainment

- Other Industries

- By Organization Size

- Large Enterprises

- Small and Mid-Sized Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with analytics software architects, hyperscale cloud engineers, and enterprise data leaders across North America, Europe, and Asia Pacific. These discussions clarified average selling prices, deployment mixes, and budget trajectories, which we used to verify secondary findings and close information gaps.

Desk Research

We gathered baseline volumes and prices from tier-one public sources such as the OECD cloud adoption tables, Eurostat digital economy indicators, International Telecommunication Union traffic datasets, and the U.S. Bureau of Labor Statistics data science employment series. We also drew on customs statistics for analytics accelerators, peer-reviewed journals that track algorithm uptake, and corporate filings that break out analytics revenue. Proprietary feeds from D&B Hoovers and Dow Jones Factiva enriched company splits and deal flow, and many additional sources helped us refine context and validate signals.

Market-Sizing & Forecasting

We start with a top-down rebuild of global enterprise spending on data platforms, apportion it to advanced analytics using market share signals, and then filter the pool through deployment and industry penetration rates. Only after collating usage metrics, cloud workload hours, and vendor shipment data do we arrive at the preliminary revenue baseline, which is sharpened through supplier roll-ups and sampled ASP × user counts. Key model drivers include hyperscale GPU capacity, data scientist headcount, average price per predictive license, privacy regulation milestones, and macro GDP paths. A multivariate regression blended with scenario analysis projects these variables through 2030 and adjusts results for currency shifts.

Data Validation & Update Cycle

Every model output is compared by our team with venture funding rounds, quarterly vendor surprises, and contract announcements. Variances trigger re-checks and expert callbacks. Reports refresh annually, with interim updates for material events, and a final review happens just before client delivery.

Why Mordor's Advanced Analytics Baseline Commands Reliability

Published estimates often diverge, and we want buyers to understand why.

Differences arise from varied scopes, driver sets, and refresh cadences.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 57.55 B (2025) | Mordor Intelligence | |

| USD 75.89 B (2024) | Global Consultancy A | Includes BI add-ons and adjacent point solutions |

| USD 47.33 B (2024) | Industry Association B | Excludes implementation and support services |

| USD 26.9 B (2024) | Trade Journal C | Counts only pure-play vendor software revenue, assumes slow cloud shift |

These comparisons show that Mordor Intelligence, through disciplined scope alignment, balanced revenue mixes, and an annual refresh cycle, delivers a dependable baseline that decision makers can trust.

Key Questions Answered in the Report

What is the current value of the advanced analytics market?

The market is valued at USD 69.52 billion in 2026 and is projected to reach USD 178.93 billion by 2031, growing at a 20.82% CAGR.

Which analytics type is growing fastest?

Edge Analytics shows the highest growth, advancing at a 27.35% CAGR due to rising demand for sub-millisecond, on-device decision-making.

Why are services growing faster than software sales?

Complex deployments, talent shortages, and regulatory requirements push enterprises to seek consulting and managed services, driving a 22.90% CAGR for services revenue.

How does the EU AI Act influence vendor selection?

Mandatory transparency rules favour platforms with built-in explainability and audit trails, shifting European buying criteria toward compliant solutions.

Which region will expand most rapidly?

APAC leads with a forecast 22.40% CAGR, propelled by manufacturing automation, smart-city initiatives, and supportive government policies.

What is the biggest barrier to wider analytics adoption?

Data integration challenges remain the primary restraint, accounting for a 3.4-percentage-point drag on the global CAGR due to fragmented legacy systems and governance complexity.

Page last updated on: