Sensing Cable Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

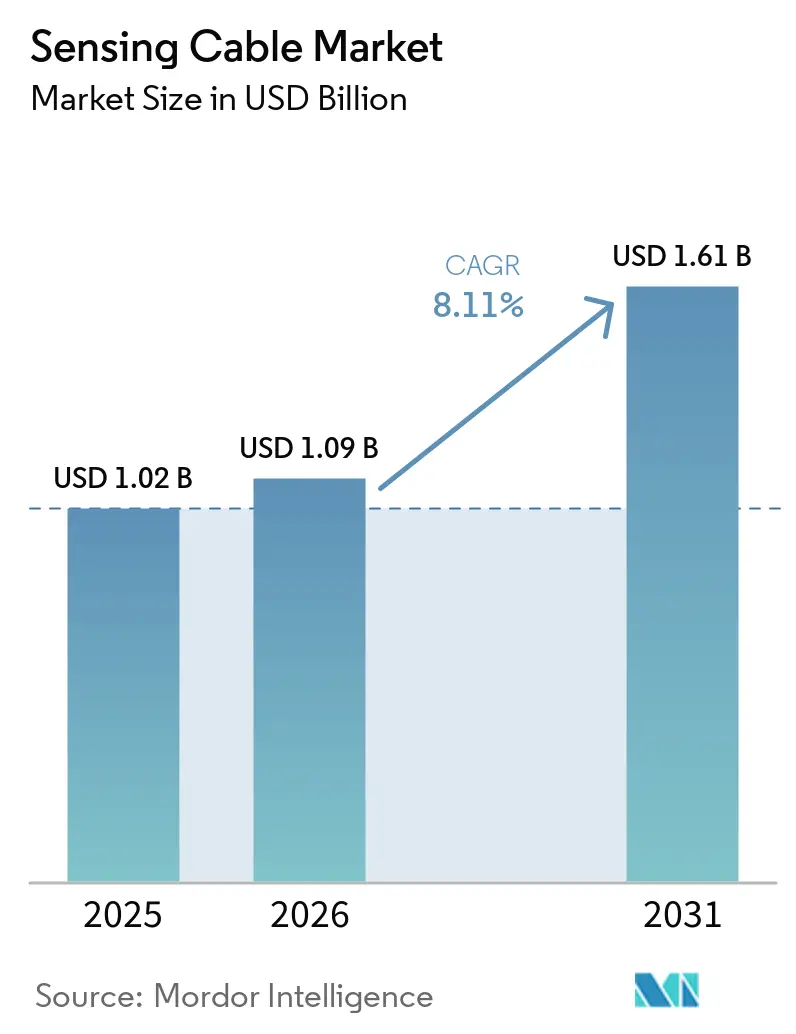

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.61 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sensing Cable Market Analysis by Mordor Intelligence

The sensing cable market size was valued at USD 1.02 billion in 2025 and estimated to grow from USD 1.09 billion in 2026 to reach USD 1.61 billion by 2031, at a CAGR of 8.11% during the forecast period (2026-2031). Continued enforcement of pipeline safety rules, large-scale data center construction, and the rise of dark-fiber monetization keep capital flowing into sensing deployments. Fiber-optic cables remain the workhorse for long-distance distributed temperature and acoustic sensing, while polymer optical fibers are gaining credibility in harsh industrial settings, thanks to new cladding materials that push survivability above 160 °C. Vendors differentiate through artificial intelligence analytics that reduce nuisance alarms and lower maintenance labor, an important consideration as trained technicians remain scarce. On the demand side, hyperscale and edge data centers treat continuous thermal monitoring as an insurance prerequisite, and national oil companies in the Middle East embed real-time integrity surveillance into every new pipeline, ensuring a resilient growth runway for the sensing cable market.

Key Report Takeaways

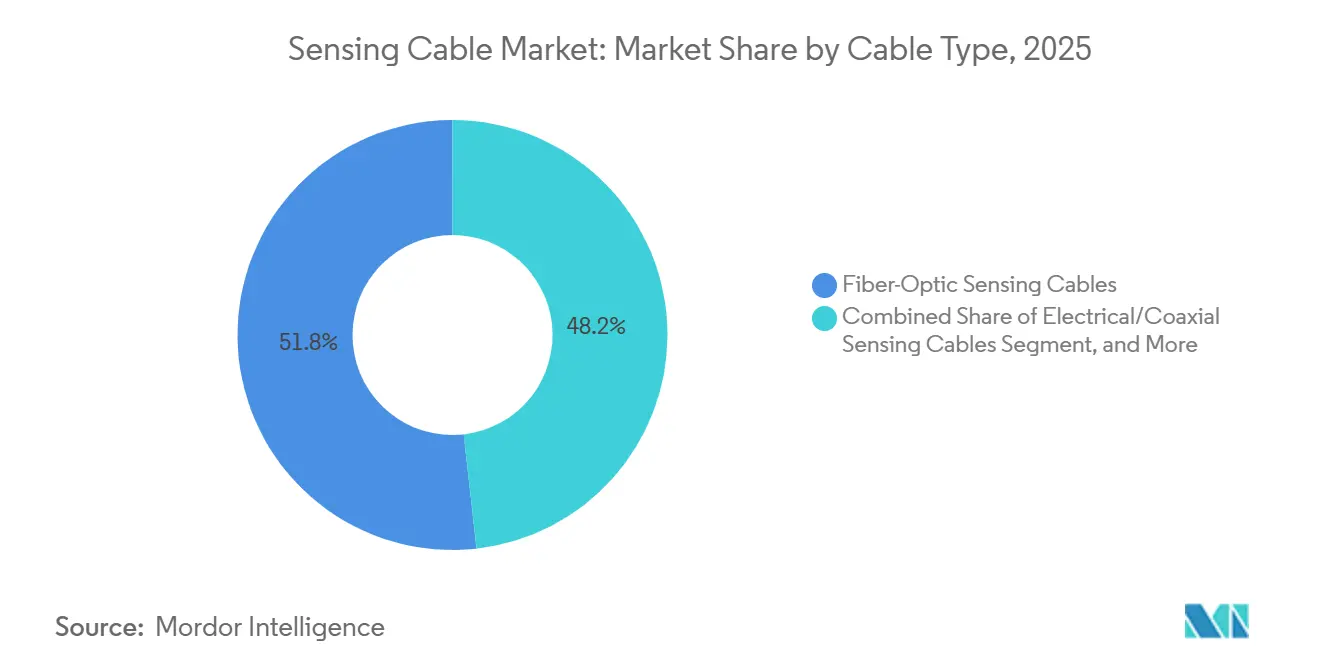

- By cable type, fiber-optic cables led with 51.78% of the sensing cable market share in 2025, while polymer optical fibers are projected to expand at a 9.06% CAGR between 2026 and 2031.

- By sensing technology, distributed temperature sensing accounted for 43.12% of revenue in 2025, whereas distributed acoustic sensing is poised to grow at a 9.09% CAGR through 2031.

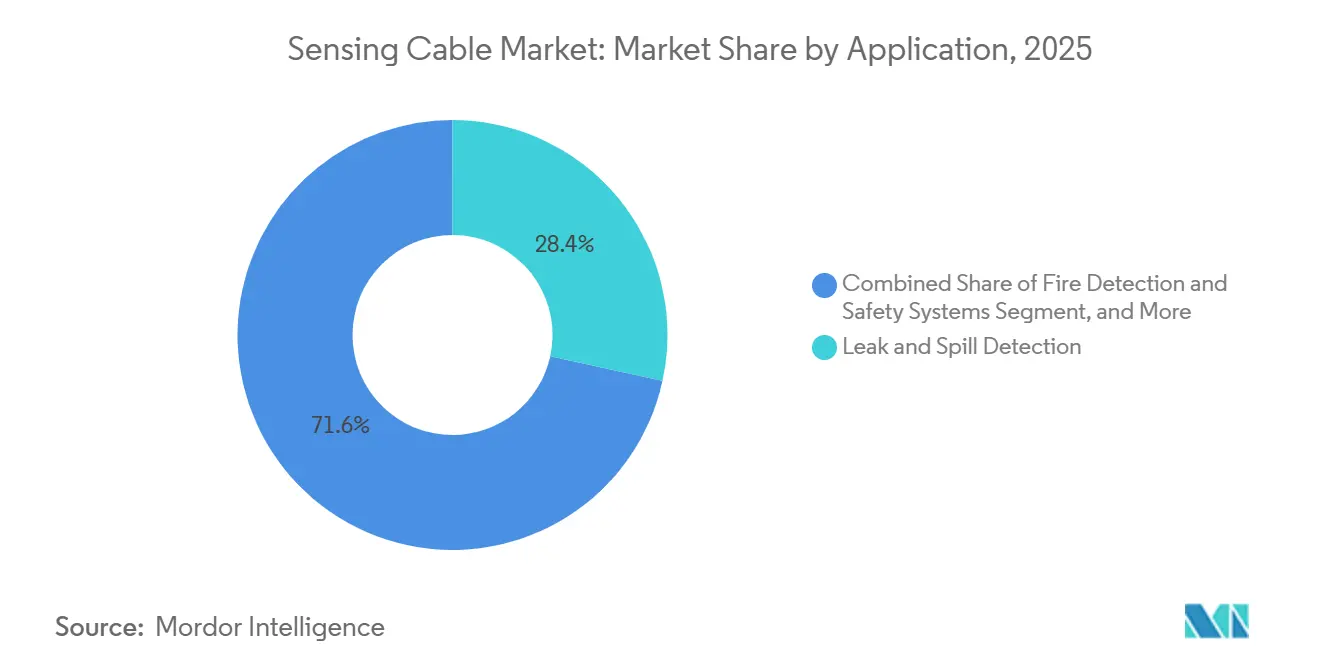

- By application, leak and spill detection generated 28.42% of 2025 revenue, yet fire detection and safety systems are forecast to register a 9.11% CAGR to 2031.

- By end-user industry, oil and gas users accounted for 35.99% of 2025 demand, but data centers and commercial buildings are set to grow at a 9.84% CAGR through 2031.

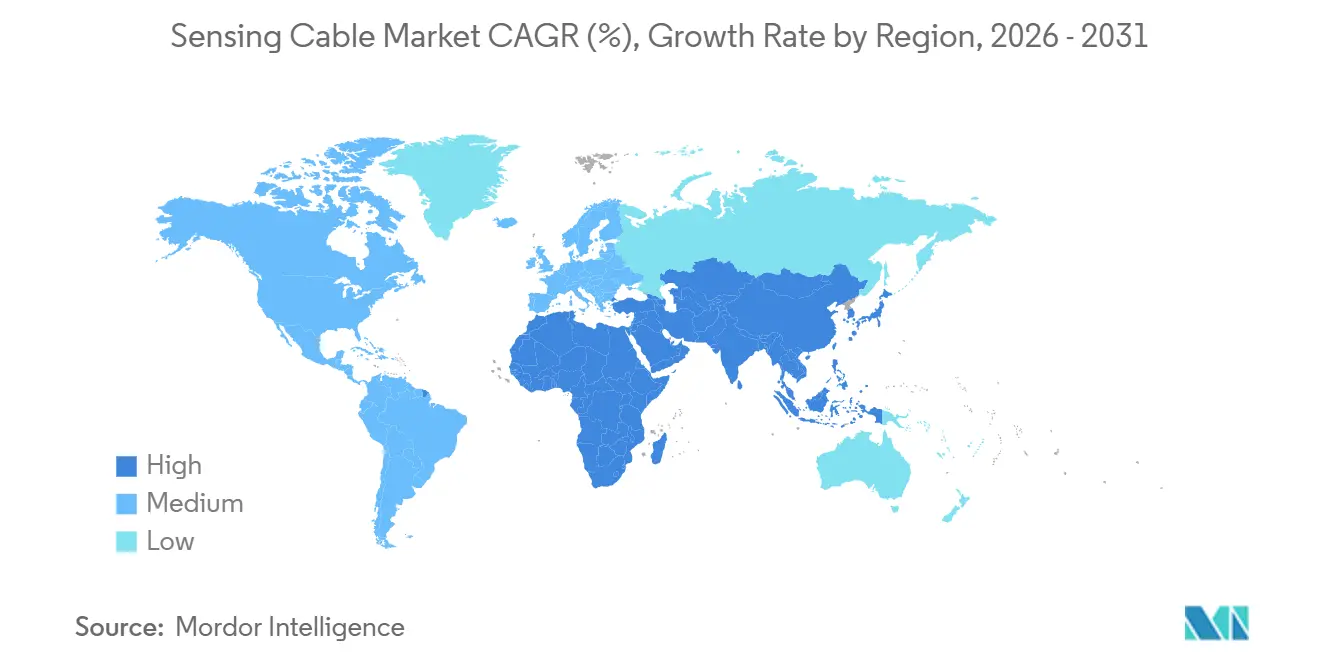

- By geography, Asia-Pacific captured 31.73% of the market share in 2025, while the Middle East is projected to advance at a 9.21% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sensing Cable Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Deployment of Distributed Fiber-Optic Sensing in Unconventionals | +2.1% | North America, Middle East, China shale basins | Medium term (2-4 years) |

| Mandatory Leak-Detection Regulations for Hazardous Pipelines | +1.8% | North America, Europe, spill-over to Middle East and South America | Short term (≤ 2 years) |

| Integration of AI Analytics Lowers OPEX and False Alarms | +1.5% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| Adoption of Passive Fire-Detection Cables in Hyperscale Data Centers | +1.3% | North America, Europe, Singapore, Tokyo, Sydney | Short term (≤ 2 years) |

| Monetization of Dark Fiber for Dual Telecom-Sensing Use | +0.9% | North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Sub-Sea HVDC Growth Demanding Continuous Thermal Monitoring | +0.7% | North Sea, Baltic, Japan-Taiwan, Australia, GCC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Deployment of Distributed Fiber-Optic Sensing in Unconventionals

Permanent fiber strings let shale drillers visualize frac-stage performance and reservoir flow in real time, trimming non-productive time and boosting recovery factors. Halliburton’s 2025 license for bare-fiber intervention technology demonstrated that operators could spool fibers during stimulation without halting pumping operations.[1]Halliburton Company, “WellSense FiberLine Intervention Technology,” halliburton.com Enhanced-scattering fibers that add periodic refractive-index modulation improve signal-to-noise by 15 dB, extend single-interrogator reach beyond 50 km, and reduce hardware count. National oil companies in the Middle East demand similar surveillance for extended-reach wells, where carbonate heterogeneity masks flow, locking in multi-year orders that expand the sensing cable market.

Mandatory Leak-Detection Regulations for Hazardous Pipelines

The U.S. Pipeline and Hazardous Materials Safety Administration now compels liquid-line operators to spot leaks within tight time and volume windows, and API RP 1130 names distributed fiber sensing as a compliant method. In Europe, the Seveso III Directive widens the net to chemical corridors, prodding retrofits of aging transmission lines. AP Sensing’s 1,300 km BRUA project in 2025 demonstrated sub-kilometer localization that meets regulatory requirements while providing forensic data for incident reporting. Because continuous fiber coverage removes blind spots, operators accelerate replacement of periodic flyovers, nudging the sensing cable market into routine budget cycles.

Integration of AI Analytics Lowers OPEX and False Alarms

False alarms sap crew productivity and strain maintenance budgets, so operators gravitate toward interrogators that embed machine-learning classifiers. VIAVI places edge inference on its test heads, slashing backhaul bandwidth and pushing event recognition latency below one second. Global pipeline and power-line operators report 40% fewer nuisance callouts, channeling labor toward genuine threats and freeing capacity for brown-field expansions. The cloud training loops absorb labeled data from multiple continents, growing model accuracy above 95% and building a self-reinforcing technology moat that sustains pricing power across the sensing cable market.

Adoption of Passive Fire-Detection Cables in Hyperscale Data Centers

The 2025 edition of NFPA 72 pushes pathway survivability and cybersecurity to the forefront, making continuous thermal monitoring non-negotiable for hyperscale facilities. Siemens’ Cerberus Nova platform, unveiled in April 2026, merges distributed temperature sensing with aspirating smoke detectors to catch incipient faults before servers throttle. Structure Research counts more than 24,000 edge sites that must match the uptime guarantees of flagship campuses, injecting fresh demand for passive linear heat cables. Because fiber sensing spans under-floor plenums and overhead trays that elude point detectors, operators standardize on it across greenfield and retrofit builds, enlarging the sensing cable market footprint beyond traditional industrial zones.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Interrogator-Unit Cost for Long-Reach Deployments | -1.4% | Global, acute in South America, Africa, Southeast Asia | Medium term (2-4 years) |

| Scarcity of Trained Fiber-Optic Installation Workforce | -1.1% | North America, Europe, India | Short term (≤ 2 years) |

| Cyber-Hardening Requirements Delaying Approvals | -0.6% | North America, Europe | Short term (≤ 2 years) |

| Polymer Sensing-Cable Degradation in High-Temperature Wells | -0.4% | North America, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Interrogator-Unit Cost for Long-Reach Deployments

Price tags between USD 50,000 and USD 200,000 per interrogator deter cash-strapped utilities and midstream firms from blanketing hundreds of kilometers. AP Sensing delivered 300 km submarine coverage in 2025, but the coherent Rayleigh lasers and low-noise detectors behind that feat inflate capital budgets. Managed service models aim to amortize costs across users but require dense asset corridors that few regions possess. Silicon-photonics prototypes hint at wafer-scale price breaks, though commercial launches remain two years away. Until then, high upfront costs temper emerging-market adoption and cap the global sensing cable market's trajectory.

Scarcity of Trained Fiber-Optic Installation Workforce

Fusion splicing, OTDR testing, and field hardening demand specialized talent that broadband rollouts already exhaust. India’s 2025 strategy paper flagged the workforce gap and triggered new training grants under the Ministry of Electronics and Information Technology.[2]CSIR-Central Glass and Ceramic Research Institute, “National Strategy Paper on Fiber Bragg Grating Sensors,” cgcri.res.in The Fiber Broadband Association’s OpTIC Path course supplies 144 hours of instruction, but its telecom focus leaves sensing skills underserved. Project delays of three to six months ripple through pipeline expansions and HVDC links, forcing owners to stockpile contractors or accept schedule slippage. Labor scarcity, therefore, restrains near-term scaling of the sensing cable market despite robust demand signals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cable Type: Polymer Fibers Carve Out High-Temperature Niches

Spending on fiber-optic formats accounted for 51.78% of the sensing cable market share in 2025, yet polymer optical fibers are forecast to grow at a 9.06% CAGR, driven by perfluorinated graded-index cores that remain transparent beyond 160 °C. The sensing cable market for polymer lines is poised to reach new heights as refiners and chemical plants seek solutions immune to electromagnetic interference. Silica-based cables still dominate long-haul assets because 0.2 dB/km attenuation enables single-interrogator spans over 100 km.

Hybrid power-plus-fiber constructions emerge for offshore wind farms where remote nodes lack grid feeds. Electrical and coaxial forms persist in legacy fire-loop retrofits, but shrinking cost differentials and the ban on halogenated jackets are pushing buyers toward fiber alternatives. Manufacturers experimenting with TOPAS and CYTOP cores drive incremental efficiency gains, while PFAS-free claddings address looming European chemical restrictions. As material science evolves, the sensing cable market welcomes a broader portfolio that aligns thermal, chemical, and mechanical resilience with application-specific needs.

By Sensing Technology: Acoustic Platforms Accelerate Beyond Temperature Leaders

Distributed temperature sensing accounted for 43.12% of 2025 revenue, underscoring its role in pipeline and power-cable health programs, yet distributed acoustic sensing is projected to outgrow all rivals at a 9.09% CAGR. Acoustic systems parse coherent Rayleigh backscatter to deliver kilohertz-rate vibration insights that spot intrusions, leaks, and seismic tremors in real time. The sensing cable market for acoustic platforms grows as edge AI reduces raw-data bandwidth, easing network integration costs.

Multi-parameter interrogators combine Raman, Brillouin, and Rayleigh channels, yielding holistic visibility for critical infrastructure but ringing in at price points above USD 300,000. Ocean observatories already harness acoustic spans longer than 900 km for subsea quake mapping. Over the forecast window, integrated temperature-vibration packages will filter down to mid-tier pipelines, tilting the sensing cable market share mix in favor of versatile acoustic-led bundles.

By Application: Fire Detection Systems Rally Past Traditional Leak Monitoring

Leak and spill detection accounted for 28.42% of 2025 revenue, thanks to strong regulatory backing, but fire safety systems are on track for a 9.11% CAGR as hyperscale campuses proliferate. Passive linear heat detectors meet NFPA 72 survivability clauses and integrate neatly with building-management systems, a decisive plus for insurance audits. The sensing cable market now intersects with smart-building initiatives as operators overlay thermal maps onto digital-twin dashboards.

Structural health monitoring matures, too, with instrumented geogrids bringing continuous strain data to geotechnical teams.[3]A2 Advanced Monitoring, “A2SensorGrid,” a2am.eu Grid operators experiment with real-time thermal ratings to defer capital upgrades, though adoption lags because retrofits under live-line conditions require meticulous planning. Security analytics convert acoustic channels into walk-detection perimeters along borders and rail corridors, adding incremental volume without cannibalizing leak or fire budgets. This diversified mix insulates the sensing cable market from commodity-price swings affecting oil pipelines.

By End-User Industry: Data Centers Leapfrog Traditional Oil and Gas Demand

Oil and gas users controlled 35.99% of spending in 2025, reflecting decades-long reliance on wellbore and pipeline sensing. However, data centers and commercial real estate are forecast to post a 9.84% CAGR as edge facilities mushroom. The sensing cable market share linked to hyperscale campuses is growing because uptime guarantees hinge on early thermal alarm capabilities that passive linear heat cables provide. Power utilities are integrating distributed temperature sensing on HVDC links to unlock dynamic ratings, with Luna Innovations winning a 300-mile U.S. project that highlights the convergence between the energy transition and sensing needs.

Defense agencies have started incorporating acoustic overlays into port security grids following the success of Silixa’s underwater detection trial, which gained recognition from the U.S. Navy in 2025. This development highlights the growing importance of advanced sensing technologies in enhancing maritime security. Meanwhile, industrial furnaces and refineries are increasingly adopting polymer optical fibers for localized hot-spot mapping, particularly when traditional thermocouples prove inadequate. This shift underscores the need for more precise and reliable temperature-monitoring solutions in high-temperature environments. Consequently, the sensing cable market is diversifying, moving away from its traditional dependence on oil price fluctuations. Instead, it is now benefiting from increased capital expenditure cycles in digital infrastructure, further driving its growth and adoption across various industries.

Geography Analysis

Asia-Pacific anchored 31.73% of 2025 revenue, underpinned by seismic monitoring in Japan, pipeline safety upgrades in China, and workforce acceleration programs in India. The sensing cable market in the region is growing as megacities bury more HV and telecom lines that require real-time thermal supervision. Japanese agencies mount interrogators on the Tsugaru and Nankai submarine cables, weaving a dense quake-alert net that validates fiber sensing for national disaster readiness.

North America held a roughly 28% share as PHMSA mandates made distributed sensing standard practice for liquids transmission lines. Hyperscale construction in Virginia and Texas is channeling orders toward fire-loop upgrades, while the Digital 395 project showcased the dual use of telecom fibers for seismic and network services. Canada’s oil sands continue thermal monitoring, but the pace slows with capital discipline. Mexico’s constrained budgets are attracting sensing-as-a-service providers that absorb capital risk, signaling a service-driven shift in the sensing cable market.

Europe represented about 24% of turnover, buoyed by subsea HVDC links that embed continuous temperature sensing. NKT’s EUR 2 billion (USD 2.16 billion) SSEN Transmission contract packages 525 kV cable with embedded fibers, underscoring the region’s push to electrify the North Sea. The Middle East is growing fastest at a 9.21% CAGR, with Ducab’s high-voltage fiber offerings and national oil company mandates driving adoption. Meanwhile, policy gaps and capital scarcity leave most of South America and Africa below 5% penwith penetration etrationot programs in Brazil’s offshore fields hint at latent potential once interrogator costs fall.

Competitive Landscape

The sensing cable market is moderately fragmented. Major oilfield players such as Schlumberger and Halliburton leverage their established presence by cross-selling temperature strings to safeguard drilling revenues. At the same time, specialized companies like AP Sensing, Silixa, and Fotech focus on enhancing algorithmic performance to secure greenfield project bids. Additionally, cable manufacturers such as NKT and Brugg Kabel are adopting vertical integration strategies by incorporating interrogation units into their offerings. This approach enables them to provide monitoring solutions as part of comprehensive turnkey HVDC projects, effectively blurring traditional supply chain boundaries and creating new competitive dynamics.

Competition within the market is also influenced by intellectual property clustering. For instance, Luna’s acquisition of Silixa has consolidated acoustic patents under one entity. However, this move introduces execution risks, as the reliance on oil-centric customer bases makes revenue streams vulnerable to fluctuations in commodity cycles. On the other hand, active participation in standards development, such as the IEC 61757 series, allows vendors to align their products with utility procurement requirements.[4]International Electrotechnical Commission, “IEC 61757 Series: Fibre Optic Sensors,” iec.ch This alignment not only strengthens their market position but also creates compliance barriers for new entrants, further shaping the competitive landscape.

Dark-fiber monetization is emerging as a significant opportunity, fostering innovative partnerships in the market. Telecom infrastructure owners, who possess the physical conduit but lack expertise in sensing technologies, are increasingly entering into managed service agreements. These collaborations enable revenue sharing without requiring utilities to adopt common-carrier roles. Furthermore, advancements in AI analytics are driving differentiation within the market. Companies like VIAVI and AP Sensing are integrating edge inference capabilities into their solutions, allowing them to command premium pricing while maintaining a competitive edge against low-cost entrants. Collectively, these factors contribute to a dynamic market environment, ensuring robust competition while enabling leading players to sustain double-digit gross margins across the sensing cable market.

Sensing Cable Industry Leaders

Silixa Ltd.

Luna Innovations Incorporated

Schlumberger Limited

Halliburton Company

Yokogawa Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: A2 Advanced Monitoring and Huesker debuted A2SensorGrid, embedding distributed strain sensing into geogrids for continuous ground-movement analytics in infrastructure projects.

- April 2026: Siemens launched the Cerberus Nova fire platform that marries distributed temperature sensing with aspirating smoke detection for hyperscale data centers.

- April 2026: In Australia, AFL has secured its role as the national fiber manufacturing partner for the Inligo Unite Cable System, strategically positioning its fibers for upcoming sensing layers.

- January 2026: NKT had clinched a contract worth EUR 2 billion (USD 2.16 billion) to deliver 525 kV HVDC subsea cables, complete with integrated distributed temperature sensing, for SSEN Transmission.

Global Sensing Cable Market Report Scope

The Sensing Cable Market refers to the global industry that develops, deploys, and commercializes specialized cables embedded with sensing capabilities to monitor physical and environmental parameters in real time. These cables function as continuous sensing systems, enabling the detection, measurement, and analysis of variables such as temperature, acoustic signals, strain, pressure, and intrusion over long distances and across critical assets.

The Sensing Cable Market Report is Segmented by Cable Type [Fiber-Optic Sensing Cables, Electrical/Coaxial Sensing Cables, Polymer Optical Fiber (POF) Sensing Cables, and Hybrid (Power + Fiber) Sensing Cables], Sensing Technology [Distributed Temperature Sensing (DTS), Distributed Acoustic Sensing (DAS), Distributed Strain/Pressure Sensing, and Hybrid Multi-Parameter Sensing], Application (Leak and Spill Detection, Structural Health and Geotechnical Monitoring, Power Cable and Grid Asset Monitoring, Perimeter and Security Intrusion Detection, and Fire Detection and Safety Systems), End-User Industry (Oil and Gas, Power and Utilities, Civil Infrastructure and Construction, Industrial Manufacturing and Process, Defense and Security, and Data Centers and Commercial Buildings), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Fiber-Optic Sensing Cables |

| Electrical/Coaxial Sensing Cables |

| Polymer Optical Fiber (POF) Sensing Cables |

| Hybrid (Power + Fiber) Sensing Cables |

| Distributed Temperature Sensing (DTS) |

| Distributed Acoustic Sensing (DAS) |

| Distributed Strain/Pressure Sensing |

| Hybrid Multi-Parameter Sensing |

| Leak and Spill Detection |

| Structural Health and Geotechnical Monitoring |

| Power Cable and Grid Asset Monitoring |

| Perimeter and Security Intrusion Detection |

| Fire Detection and Safety Systems |

| Oil and Gas |

| Power and Utilities |

| Civil Infrastructure and Construction |

| Industrial Manufacturing and Process |

| Defense and Security |

| Data Centers and Commercial Buildings |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Cable Type | Fiber-Optic Sensing Cables | ||

| Electrical/Coaxial Sensing Cables | |||

| Polymer Optical Fiber (POF) Sensing Cables | |||

| Hybrid (Power + Fiber) Sensing Cables | |||

| By Sensing Technology | Distributed Temperature Sensing (DTS) | ||

| Distributed Acoustic Sensing (DAS) | |||

| Distributed Strain/Pressure Sensing | |||

| Hybrid Multi-Parameter Sensing | |||

| By Application | Leak and Spill Detection | ||

| Structural Health and Geotechnical Monitoring | |||

| Power Cable and Grid Asset Monitoring | |||

| Perimeter and Security Intrusion Detection | |||

| Fire Detection and Safety Systems | |||

| By End-User Industry | Oil and Gas | ||

| Power and Utilities | |||

| Civil Infrastructure and Construction | |||

| Industrial Manufacturing and Process | |||

| Defense and Security | |||

| Data Centers and Commercial Buildings | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the sensing cable market in 2026?

The sensing cable market size stands at USD 1.09 billion in 2026, with growth momentum supported by pipeline safety rules and data center fire-safety mandates.

What CAGR is forecast for sensing cables between 2026 and 2031?

The market is projected to expand at an 8.11% CAGR during 2026-2031, reflecting steady adoption across energy, utilities, and digital-infrastructure sectors.

Which cable type dominates current revenue?

Silica-based fiber-optic sensing cables led with a 51.78% sensing cable market share in 2025, driven by their low attenuation and high thermal stability.

Which application segment is growing fastest?

Fire detection and safety systems for hyperscale and edge data centers are expected to post a 9.11% CAGR through 2031 as NFPA 72 standards tighten.

Which geography will outpace others through 2031?

The Middle East is forecast to record a 9.21% CAGR as national oil companies and utilities embed real-time integrity monitoring in pipelines and subsea HVDC links.

Why is AI integration important for sensing cables?

Embedded analytics cut false-alarm rates by up to 40%, reducing maintenance dispatches and accelerating fault localization, making AI a key value driver for future deployments.

Page last updated on: