North America Automotive LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

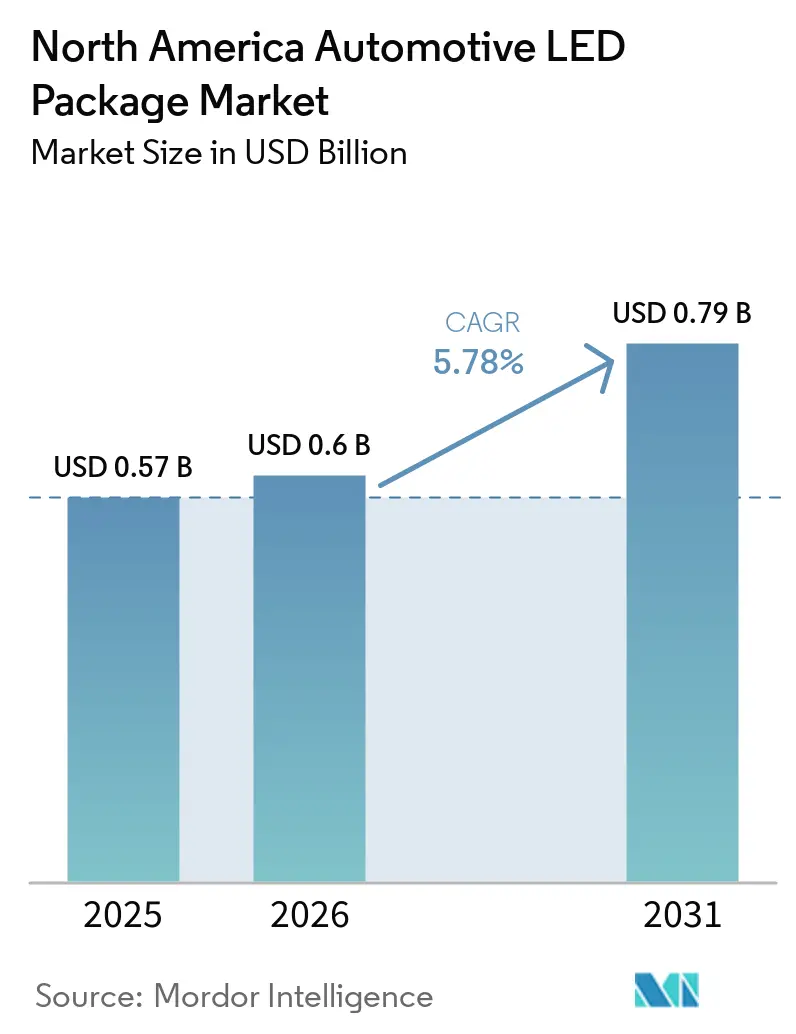

| Base Year Market Size (2025) | USD 0.57 Billion |

| Market Size (2026) | USD 0.6 Billion |

| Market Size (2031) | USD 0.79 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automotive LED Package Market Analysis by Mordor Intelligence

The North America automotive LED package market size is projected to expand from USD 0.57 billion in 2025 and USD 0.60 billion in 2026 to USD 0.79 billion by 2031, registering a CAGR of 5.78% between 2026 to 2031. Regulatory alignment on adaptive lighting, accelerating electric-vehicle (EV) launches, and miniaturization breakthroughs in chip-scale packages are sustaining demand even as overall vehicle output grows modestly. Automakers now treat forward-lighting modules as software-defined safety assets, which is steering procurement toward suppliers that bundle LEDs with driver integrated circuits and thermal-simulation services. Nearshoring incentives in Mexico have begun to diversify the supply chain, while United States buyers continue to dominate volume purchases. At the same time, tightening patent enforcement is reshaping supplier rosters, prompting tier-ones to seek broader cross-licensing coverage before finalizing bill-of-materials decisions.

Key Report Takeaways

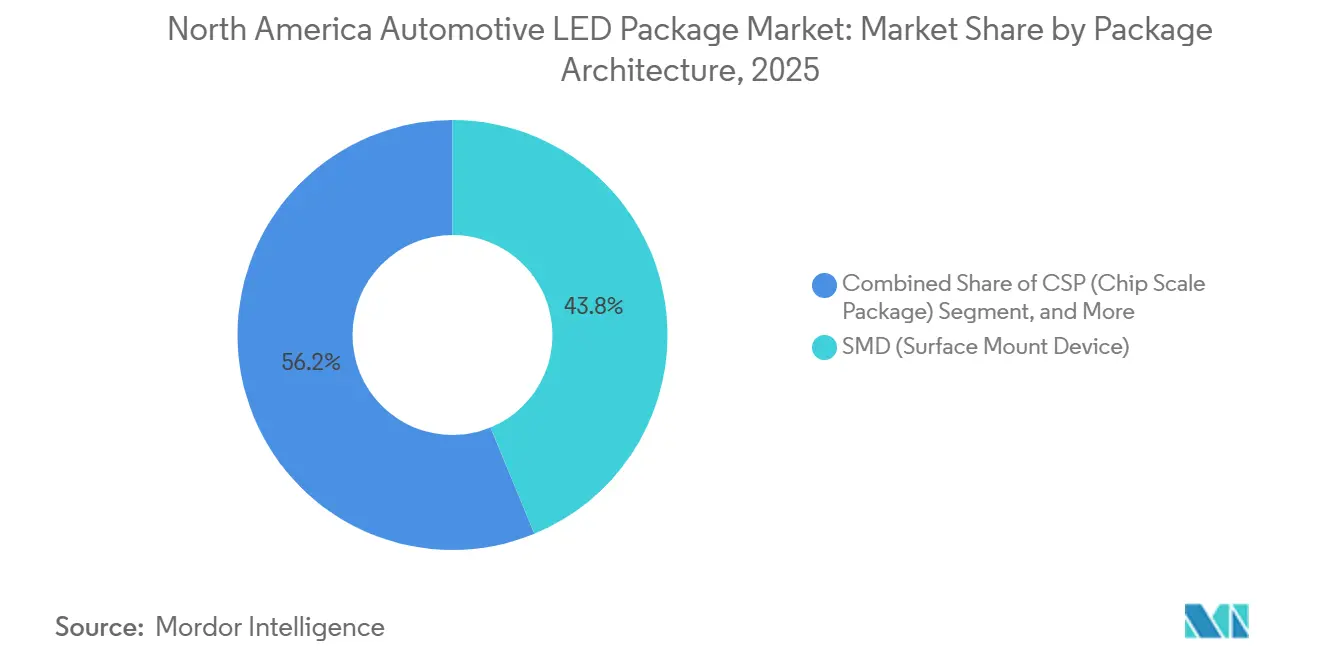

- By package architecture, surface-mount devices led with 43.78% of the North America automotive LED package market share in 2025, whereas chip-scale packages are advancing at a 6.42% CAGR through 2031.

- By power class, high-power LEDs above 1 watt captured 57.31% of the North America automotive LED package market size in 2025 and are forecast to grow at 6.55% between 2026-2031.

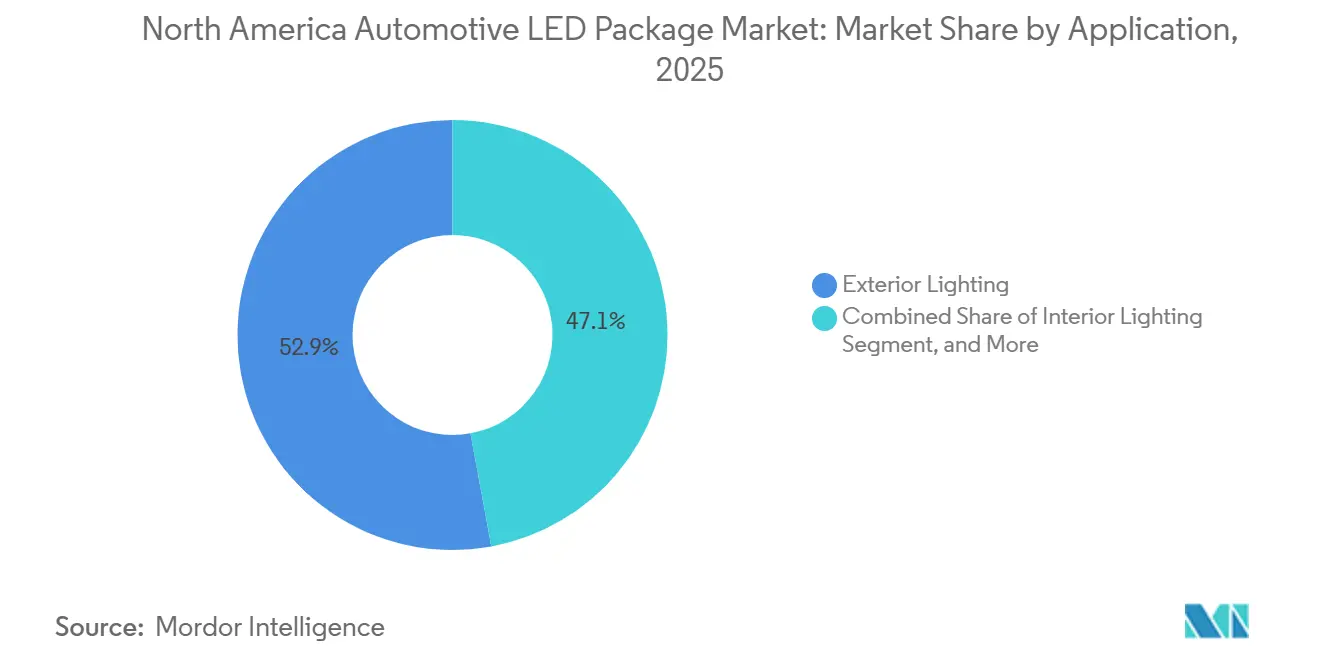

- By application, exterior lighting retained 52.89% revenue share in 2025, while interior lighting is expanding at a 6.39% CAGR to 2031.

- By vehicle type, passenger vehicles accounted for 73.58% of 2025 volume and will continue as the fastest-growing category with a 6.59% CAGR through 2031.

- By geography, the United States commanded 86.58% share in 2025; Canada is the fastest-growing national market at 6.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Automotive LED Package Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EV Headlamp Adoption for Adaptive Driving Beams | +1.8% | United States and Canada, spillover to Mexico EV assembly | Medium term (2-4 years) |

| Integration of µLED Arrays for Advanced ADAS Sensors | +1.4% | United States (ADAS mandates), Canada (regulatory alignment) | Long term (≥ 4 years) |

| OEM Shift Toward Dynamic Exterior Styling Elements | +1.2% | North America, concentrated in premium segments | Short term (≤ 2 years) |

| Light-on-Demand Features Enabling New In-Cabin HMI | +0.9% | United States and Canada luxury and mid-tier platforms | Medium term (2-4 years) |

| U.S. Regulatory Push for Daytime Running Lights Standardization | +0.3% | United States (FMVSS 108 compliance), Canada (TSD 108 Rev 8) | Short term (≤ 2 years) |

| Mexico's Near-Shore LED Packaging Incentives Post-USMCA | +0.2% | Mexico manufacturing zones, indirect benefit to U.S. and Canada OEMs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in EV Headlamp Adoption for Adaptive Driving Beams

Adaptive driving-beam headlamps are proliferating as EV platforms migrate to 48-volt architectures that simplify high-current LED driver design. Tesla activated glare-free high beams across its North American fleet in April 2025, following amendments to FMVSS 108 that cleared the last regulatory hurdle.[1]National Highway Traffic Safety Administration, “FMVSS 108 Final Rule,” nhtsa.gov ams OSRAM’s EVIYOS HD25 entered series production on NIO’s ET9 with 25,600 addressable pixels, demonstrating that automakers are willing to pay a 30-40% price premium for safety-driven differentiation. Rivian brought 480-pixel arrays to volume production in the R1T and R1S, signaling the convergence of commercial-grade lighting standards with passenger-car expectations. Because pixel density demands sub-2 mm package pitch, many tier-ones are now specifying flip-chip CSPs that slash thermal resistance while enabling thinner optics. As a result, the North America automotive LED package market is capturing incremental value from both upgraded hardware and the software licenses that orchestrate beam patterns.

Integration of µLED Arrays for Advanced ADAS Sensors

Micro-LED arrays provide uniform infrared illumination for driver-monitoring cameras and high-resolution visible light for road-scene projection. Nichia’s µPLS platform, with 16,384 micro-LEDs on a 256 × 64 matrix, entered mass production for occupant-detection modules in 2025.[2]Nichia Corporation, “µPLS Mass Production Announcement,” nichia.com Sony’s AEC-Q100-qualified IMX775 pairs with compact 940 nm LED arrays to deliver privacy-friendly cabin monitoring beginning in spring 2026. VueReal and Flex-N-Gate are co-developing brake-light modules that embed vehicle-to-vehicle messages directly in dynamic LED pixels, blurring lines between lighting and data connectivity. These sensor-integrated packages push the North America automotive LED package market toward co-fabricated emitter-detector stacks on common substrates, an architecture that incumbents and start-ups alike are racing to patent.

OEM Shift Toward Dynamic Exterior Styling Elements

Animated daytime running lights, segmented taillamps, and back-lit grilles are shaping brand identity in crowded EV segments. FORVIA HELLA and Audi integrated 61 switchable segments into the Q6 e-tron’s forward lighting, enabling welcome signatures and sweeping turn indicators.[3]FORVIA HELLA, “Q6 e-tron Lighting Collaboration,” hella.com Mercedes-Benz plans to embed over 50,000 LEDs in the 2026 S-Class headlamp cluster, a design achievable only with sub-200 µm chip-on-board packages. Flexible micro-LED deposition platforms such as VueReal’s MicroSolid Printing now support pixel densities above 1,000 per square inch, turning exterior lighting into a secondary display surface. With over-the-air updates controlling these arrays, lifetime revenue shifts from hardware alone to recurring software features, expanding the addressable slice of the North America automotive LED package market.

Light-on-Demand Features Enabling New In-Cabin HMI

Interior illumination is transforming into an interactive interface that synchronizes with drive modes, voice commands, and safety alerts. Polestar 4 offers tunable ambient schemes from 2,700-6,500 K, and Acura’s MDX IconicDrive delivers 27 color themes across 24 zones, linking lighting to infotainment and climate settings. LG Innotek’s Ultra Thin Pixel Lighting Module, only 0.12 inch thick, won a CES 2026 Innovation Award and boosts luminous efficiency by 30%, enabling slim roof liners and headrests to host LED clusters. Hyundai Mobis integrates 32 light patterns with ADAS alerts, underscoring a new safety role for cabin lighting. Collectively, these features are pushing the North America automotive LED package market beyond aesthetics toward functional human-machine communication.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal Management Limits for High-Power CSP Packages | -0.8% | North America, acute in high-ambient-temperature regions (southern U.S., northern Mexico) | Short term (≤ 2 years) |

| Supply Chain Exposure to Sapphire Substrate Shortages | -0.6% | Global, with acute impact on U.S. and Canadian tier-one suppliers dependent on Asian substrate producers | Medium term (2-4 years) |

| IP Litigation Risk in Flip-Chip Wafer-Level Packaging | -0.3% | United States (federal district courts), spillover to Canada via supply-chain disruption | Long term (≥ 4 years) |

| Passenger Vehicle LED Penetration Plateau in Canada | -0.1% | Canada, limited spillover to U.S. border states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Thermal Management Limits for High-Power CSP Packages

High-power chip-scale packages dissipate up to 80% of input energy as heat, and junction temperatures can climb beyond 125 °C during prolonged high-beam use. At that threshold, luminous flux can drop by 15-20% within 5,000 hours, jeopardizing the 10,000-hour warranty many automakers promise. Lumileds’ LUXEON Altilon SMD-A reduces thermal resistance to 2.5 °C/W with a copper lead frame, but often still requires active cooling, which adds module mass. Flip-chip configurations improve heat paths yet require costly wafer-level underfill; early production runs have reported yield losses that raise per-die costs. These constraints limit how aggressively the North America automotive LED package market can pivot to ultra-dense headlamp arrays without parallel advances in heat-sink design or phosphor stability.

Supply-Chain Exposure to Sapphire Substrate Shortages

Four suppliers control the bulk of automotive-grade sapphire wafers, and spot prices for 4-inch material swung 18% during 2025 as EV rollouts squeezed capacity. Sapphire’s modest thermal conductivity (≈ 35 W/m·K) caps power density, yet its lattice match to gallium nitride keeps it dominant for blue and white LEDs. While copper and silicon-carbide substrates promise triple the heat flux, they require new epitaxial recipes and longer qualification timelines. Building one 6-inch crystal-growth line costs upward of USD 50 million, so capacity lags demand. North American tier-ones therefore face longer lead times and must dual-source packages, adding procurement complexity and tempering near-term growth in the North America automotive LED package market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Package Architecture: Chip-Scale Momentum on Thermal Gains

Chip-scale packages increased their slice of the North America automotive LED package market to 6.42% CAGR, while surface-mount devices retained a 43.78% lead in 2025. CSPs eliminate wire bonds and shrink the footprint to within 20% of the die size, carving direct thermal paths that cut junction-to-board resistance by 30-40%. Flip-chip CSPs also support pixel pitches below 2 mm, critical for ≥400-pixel headlamp modules. However, intellectual-property disputes-Everlight sued Lumileds and Seoul Semiconductor in February 2026 over flip-chip patent US 7,554,126-inject adoption risk. SMD architectures remain preferred for cost-sensitive commercial vehicles, especially after ams OSRAM’s Oslon Compact PL reached 395 lumens at 1 A, showing that incremental efficiency gains can extend the life of conventional packages.

Bridgelux’s CSP line now delivers 209 lm/W at 350 mA, allowing automakers to meet brightness targets with 20-30% fewer LEDs, which trims driver-circuit and optics costs. Chip-on-board solutions achieve peak lumen density but require replacing the entire module if one die fails, limiting uptake to premium headlamps where design flexibility outweighs serviceability. Across 2026-2031, CSP shipments are forecast to close half the unit-share gap with SMDs, reinforcing their status as the fastest-advancing category in the North America automotive LED package market.

By Power Class: High-Power LEDs Secure Headlamp Leadership

High-power LEDs above 1 W delivered 57.31% revenue in 2025 and will post a 6.55% CAGR to 2031 as adaptive-beam systems target per-package outputs beyond 400 lumens. Seoul Semiconductor’s WICOP architecture in the 2024 Genesis GV80 doubled luminance compared with legacy packages and reduced heat-sink bulk by 40%, demonstrating the thermal headroom created by removing substrates. Mid-power devices occupy ambient lighting and secondary exterior signals, while low-power LEDs remain relegated to switch backlights and small indicators.

Yet micro-LED arrays blur these classes by aggregating tens of thousands of sub-0.1 W pixels into modules that draw more than 5 W. Managing heat across such dense layouts will shape power-class definitions in the North America automotive LED package market over the decade. Suppliers that integrate thermal vias and on-substrate heat spreaders are poised to capture incremental share as luminance ceilings rise.

By Application: Interior Lighting Climbs on HMI Integration

Interior lighting’s 6.39% CAGR through 2031 will erode exterior lighting’s share of revenue. Automakers now embed RGB-infrared LEDs in dashboards, door panels, and headliners, turning light into a feedback layer for driver alerts and entertainment cues. Toyoda Gosei’s moving-light door panels on the Lexus RZ animate welcome graphics and security warnings. Meanwhile, KEPO Technology’s networked LED drivers cut wiring mass while enabling over-the-air color updates. Exterior applications still command 52.89% of 2025 spend, but rising module counts in adaptive-beam headlamps mean that even small interior gains can move the North America automotive LED package market needle materially.

Sensing sub-segments also expand as cabin-monitoring mandates loom. ams OSRAM’s ALIYOS flexible foils merge RGBi emitters with driver ICs for curved surfaces, reducing assembly steps and opening new placement zones. Over the forecast window, packages that combine ambient and sensing wavelengths will enjoy premium pricing, cushioning margins even as commoditization pressures grow elsewhere.

By Vehicle Type: Passenger Cars Drive Volume Upswing

Passenger cars held 73.58% share in 2025 and will grow 6.59% annually, propelled by mass-market EV launches such as GM’s Equinox EV and Ford’s Mustang Mach-E, whose 2025 production rose 24.4% and 10.9% respectively. Stellantis’ Wagoneer S, debuting with full-LED interiors and exteriors, underscores how premium lighting packages have become table stakes even in mid-size SUVs. Commercial vehicles are slower to adopt adaptive lighting, but appear poised for an upswing as insurers reward fleets that integrate enhanced visibility features.

The shift to 48-volt electrical systems simplifies LED driver design, trims copper weight, and aligns with ADAS sensor voltage rails, further cementing passenger vehicles as the primary growth engine for the North America automotive LED package market. Light-duty vans used for last-mile delivery are expected to adopt passenger-car lighting standards as pedestrian safety rules tighten in dense urban centers.

Geography Analysis

The United States dominated the North America automotive LED package market with 86.58% share in 2025, due to its 3.95 million-unit vehicle output and rapid EV adoption. Harmonized FMVSS 108 updates, effective since 2022, now permit adaptive driving beams that enhance driver-assistance functions, accelerating domestic demand for high-pixel-count headlamps. OEMs leverage this regulatory clarity to scale matrix modules across multiple nameplates, diluting per-vehicle LED costs and boosting overall module shipments.

Canada, although smaller, is the fastest-growing national segment, with a 6.49% CAGR through 2031. Transport Canada’s TSD 108 Revision 8, in force April 2025, mirrors U.S. standards and eliminates bespoke Canadian tuning for photometric cut-offs. This alignment eliminates engineering redundancy and allows tier-ones to manufacture a single LED module for both markets, raising factory utilization rates. Provincial incentives for EV purchases further catalyze lighting-feature penetration, especially in provinces with aggressive carbon targets.

Mexico captures the remaining demand but wields outsized strategic weight because of nearshoring. Plan México, decreed January 2025, grants 91% accelerated depreciation on automotive assets, trimming effective tax burdens and lifting internal rates of return on new plants. MLS México’s USD 261.7 million LED campus in Durango, slated for first shipments in February 2026, exemplifies how suppliers are repositioning capacity to satisfy USMCA content rules while tapping cost advantages. As more lighting modules originate south of the border, shipping lead times into U.S. assembly plants drop from weeks to days, reinforcing regional supply resilience and sustaining momentum in the North America automotive LED package market.

Competitive Landscape

Five suppliers-ams OSRAM, Nichia, Lumileds, Seoul Semiconductor, and Samsung Electronics-hold an estimated combined share of more than half, indicating moderate concentration. Ams OSRAM and Nichia settled long-running patent rows with an October 2025 cross-license that now streamlines sourcing for tier-ones worried about infringement exposure. Meanwhile, San’an Optoelectronics’ USD 239 million deal to acquire Lumileds, expected to close in early 2026, places the third-largest vendor under Chinese ownership and raises export-control scrutiny among U.S. and Canadian automakers.

Litigation shapes strategy as much as pricing or specs. Seoul Semiconductor secured Unified Patent Court injunctions in October 2024 and April 2025, forcing European recalls of package-free LEDs and signaling that U.S. distributors must more thoroughly assess freedom-to-operate risk. Everlight’s twin U.S. lawsuits filed in February 2026 against Lumileds and Seoul extend that tension into North America. To hedge, tier-ones increasingly favor suppliers offering indemnification and design-in support, a value-add that raises switching costs and partially offsets component commoditization in the North America automotive LED package market.

Technical roadmaps now spotlight micro-LED integration, package-free architectures, and on-substrate driver ICs. LG Innotek’s Ultra Thin Pixel Lighting Module slashes thickness by 71% while lifting efficiency 30%, giving it a head start in premium cabins scheduled for 2027 launches. Start-ups such as VueReal target brake-light communication use-cases, demonstrating how niche functionalities can open lanes into entrenched supply chains. As patent barriers rise, cross-licensing webs and regional manufacturing footprints will determine who captures the next tranche of the North America automotive LED package market.

North America Automotive LED Package Industry Leaders

Nichia Corporation

ams OSRAM AG

Lumileds Holding B.V.

Seoul Semiconductor Co., Ltd.

Cree LED, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Excellence Optoelectronics accelerated its Durango, Mexico ramp, targeting 88 automotive LED modules in volume production by July with 80% utilization by year-end.

- February 2026: Everlight sued Seoul Semiconductor and Lumileds in U.S. federal courts, alleging infringement of flip-chip patent US 7,554,126.

- February 2026: Cree Lighting signed a long-term contract manufacturing agreement to secure LED component capacity for automotive and commercial customers.

- January 2026: LG Innotek won a CES 2026 Innovation Award for its 0.12-inch Ultra Thin Pixel Lighting Module, with mass production slated for 2H 2027.

North America Automotive LED Package Market Report Scope

The Electronic Manufacturing Services for Communication Equipment Market refers to the industry that provides design, manufacturing, testing, and assembly services for communication equipment.

The North America Automotive LED Package Market Report is Segmented by Package Architecture (SMD, CSP, Flip-Chip LED Packages, and COB), Power Class (Low Power, Mid Power, and High Power), Application (Exterior Lighting, Interior Lighting, Sensing/IR Applications, and Other Applications), Vehicle Type (Passenger Vehicles and Commercial Vehicles), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| SMD (Surface Mount Device) |

| CSP (Chip Scale Package) |

| Flip-Chip LED Packages |

| COB (Chip-on-Board) |

| Low Power (Less than 0.5 W) |

| Mid Power (0.5-1 W) |

| High Power (More than 1 W) |

| Exterior Lighting |

| Interior Lighting |

| Sensing / IR Applications |

| Other Applications |

| Passenger Vehicles |

| Commercial Vehicles |

| United States |

| Canada |

| Mexico |

| By Package Architecture | SMD (Surface Mount Device) |

| CSP (Chip Scale Package) | |

| Flip-Chip LED Packages | |

| COB (Chip-on-Board) | |

| By Power Class | Low Power (Less than 0.5 W) |

| Mid Power (0.5-1 W) | |

| High Power (More than 1 W) | |

| By Application | Exterior Lighting |

| Interior Lighting | |

| Sensing / IR Applications | |

| Other Applications | |

| By Vehicle Type | Passenger Vehicles |

| Commercial Vehicles | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the forecast value of the North America automotive LED package market by 2031?

It is expected to reach USD 0.79 billion by 2031 based on current growth projections.

Which LED power class leads shipments in North America?

High-power LEDs above 1 W dominate, holding 57.31% revenue share in 2025 and growing at 6.55% CAGR.

Why are chip-scale packages gaining traction with automakers?

They eliminate wire bonds, cut thermal resistance 30-40%, and enable sub-2 mm pixel pitch required for adaptive-beam headlamps.

How will Mexico’s nearshoring policies influence regional supply?

Plan México’s 91% depreciation incentive is attracting new LED factories, shortening lead times into U.S. assembly plants and diversifying supply.

Which country is the fastest-growing national market within North America?

Canada, expanding at a 6.49% CAGR through 2031 after aligning its lighting standards with U.S. regulations.

Page last updated on: