China LED Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

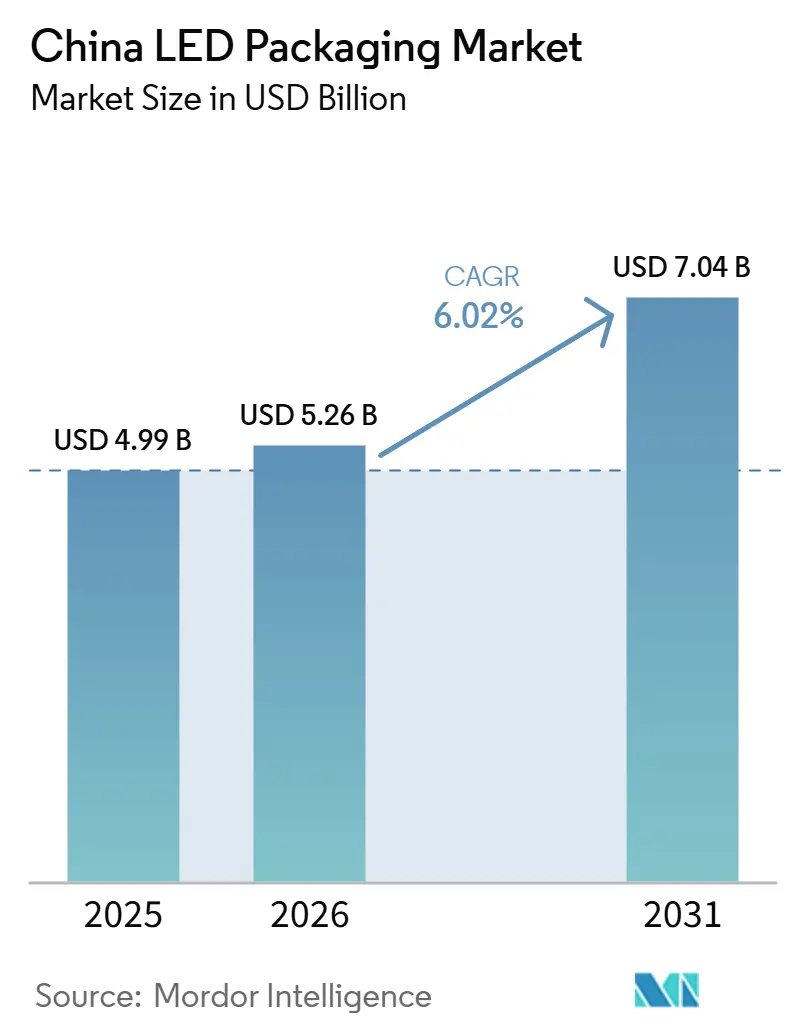

| Base Year Market Size (2025) | USD 4.99 Billion |

| Market Size (2026) | USD 5.26 Billion |

| Market Size (2031) | USD 7.04 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

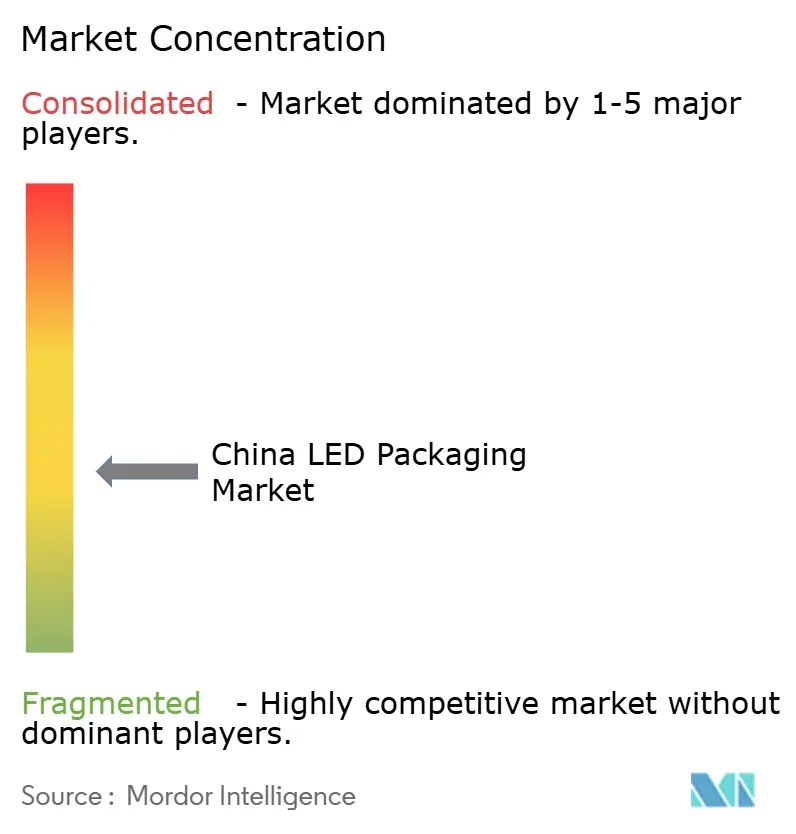

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China LED Packaging Market Analysis by Mordor Intelligence

The China LED packaging market size is projected to be USD 4.99 billion in 2025, USD 5.26 billion in 2026, and reach USD 7.04 billion by 2031, growing at a CAGR of 6.02% from 2026 to 2031. Pricing pressure in commodity mid-power surface-mount device formats continues to compress margins, encouraging manufacturers to pivot toward higher-value automotive, mini-LED television, and ultraviolet curing niches. Provincial data show that Guangdong’s tightly networked supply chain, combining epitaxy, driver ICs, substrates, and contract manufacturing, delivers cycle-time advantages that outweigh its rising labor costs. Vertically integrated champions are deepening control over epitaxy and phosphor synthesis, while smaller assemblers face recycling-cost burdens after the 2025 shift in e-waste policy. As a result, capital expenditure is concentrating in adaptive driving-beam modules, chip-scale mini-LED dies, and glass-substrate micro-LED packaging lines.

Key Report Takeaways

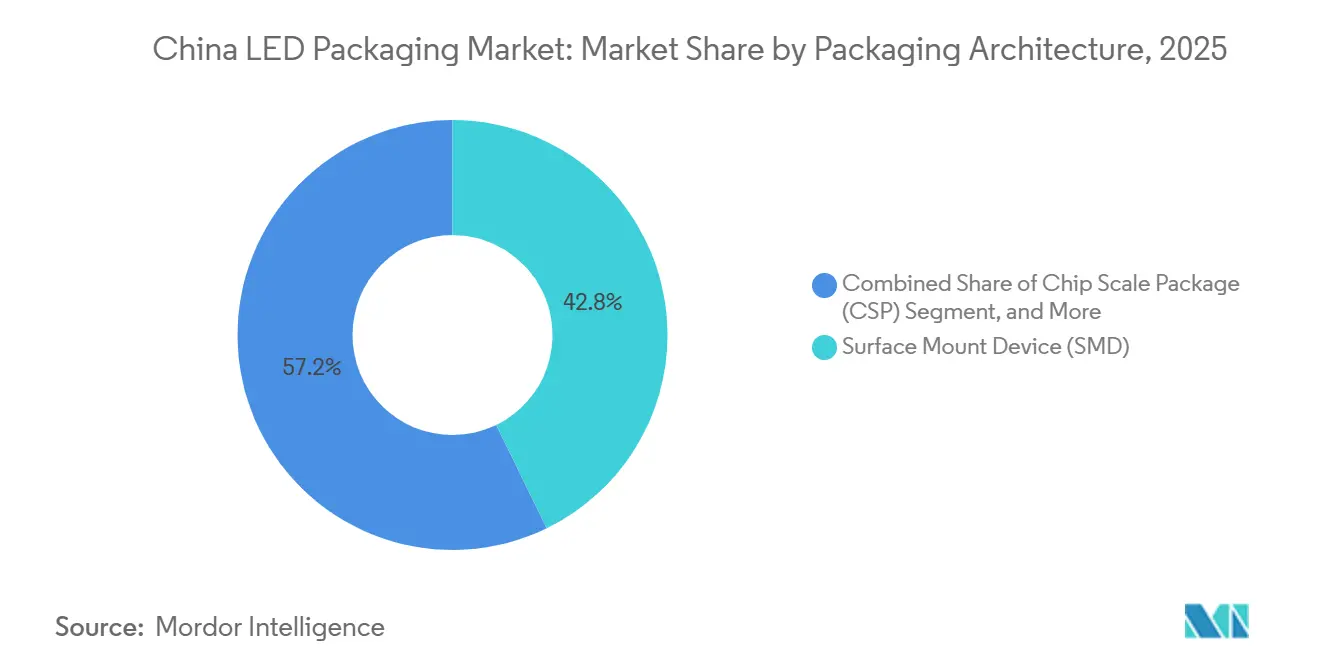

- By packaging architecture, surface-mount device formats held 42.78% of the China LED packaging market share in 2025, while chip-scale packages are forecast to expand at a 6.78% CAGR through 2031.

- By power class, mid-power devices accounted for 35.49% of the China LED packaging market size in 2025, whereas high-power packages are advancing at a 6.94% CAGR between 2026 and 2031.

- By emission type, visible-spectrum LEDs dominated with an 88.99% shipment share in 2025, yet ultraviolet packages are set to grow at a 6.74% CAGR to 2031.

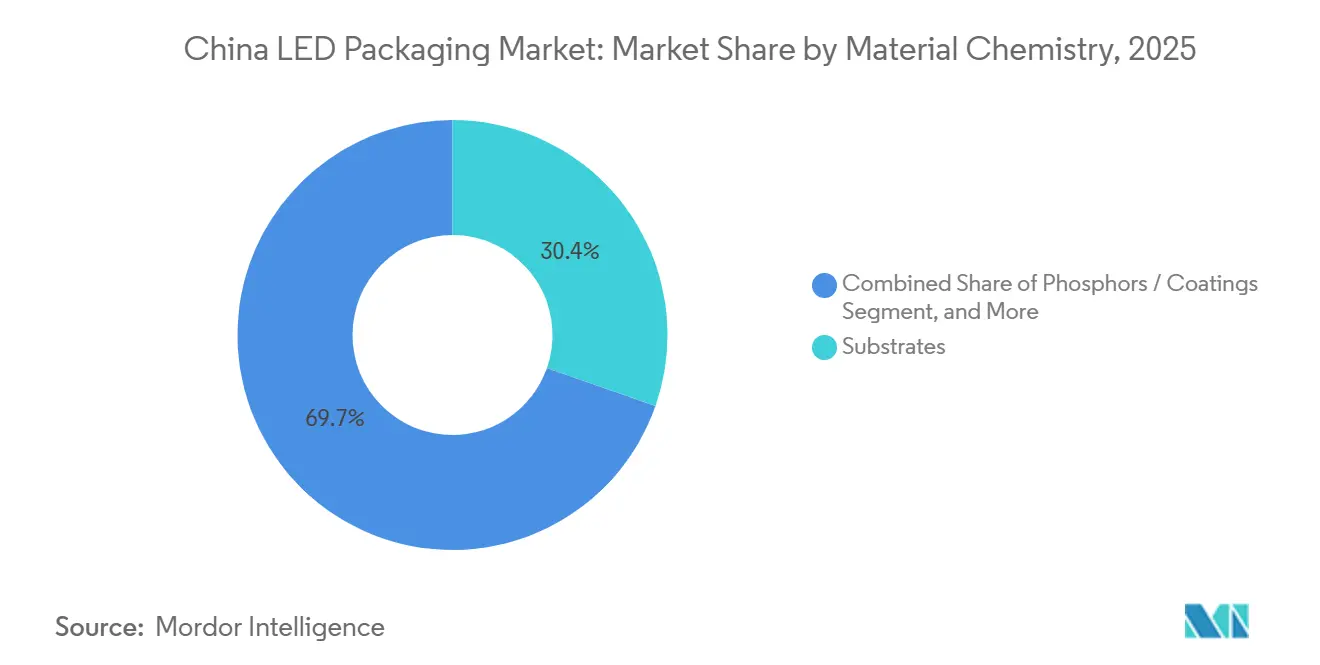

- By material chemistry, substrates accounted for 30.35% of 2025 revenues, while phosphors and coatings are progressing at a 6.91% CAGR through 2031.

- By application, general lighting led with a 40.48% revenue share in 2025, while automotive lighting is projected to grow at an 8.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China LED Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Backed Smart-City LED Retrofits | +1.2% | National, concentrated in Tier-1 and Tier-2 cities (Beijing, Tianjin, Shenzhen, Hangzhou) | Medium term (2-4 years) |

| Accelerating Mini/Micro-LED Backlighting Adoption | +1.5% | Global, with China as primary manufacturing and consumption hub; spillover to North America and Europe premium TV segments | Medium term (2-4 years) |

| Automotive LED Penetration in NEVs | +1.8% | National, with highest intensity in Guangdong, Jiangsu, Shanghai automotive clusters | Short term (≤ 2 years) |

| Export-Oriented EMS Demand for SMD Packages | +0.9% | Global, driven by Guangdong and Zhejiang exports to Europe (29.1%) and North America (31.6%) | Long term (≥ 4 years) |

| Vertical Integration by Chinese LED Champions | +0.7% | National, led by MLS, NationStar, San'an, Refond, Jufei in Guangdong and Fujian | Long term (≥ 4 years) |

| Mass-Transfer Glass Substrate Packaging Breakthroughs | +0.5% | National, with early adoption in Hubei (Tianmen) and Guangdong (Shenzhen) for micro-LED displays | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Backed Smart-City LED Retrofits

Municipal procurement programs are replacing legacy streetlights with networked LED luminaires that integrate dimming, sensors, and remote diagnostics. Projects such as the 79 000-unit retrofit completed in Tianjin’s Binhai New Area in 2024 cut energy use by 40%, proving the case for mid- to high-power chip-on-board modules.[1]Tianjin Municipal People’s Government, “Completion of Binhai New Area Smart-Streetlight Retrofit,” tj.gov.cn Tender documents increasingly require compliance with GB 7000.1-2024 safety rules and domestic-content thresholds, directing contract awards to Chinese packagers that can certify interoperability with national IoT standards. Because smart-streetlight controllers collect telemetry, suppliers with robust analytics platforms gain recurring service revenue. This shift toward performance-based contracts strengthens the grip of vertically integrated players that maintain in-house driver electronics and field-failure diagnostics.

Accelerating Mini/Micro-LED Backlighting Adoption

China shipped more than 8 million mini-LED televisions in 2025, and volumes are forecast to top 10 million units in 2026 as retail prices for 100-inch panels fall below CNY 10 000 (USD 1 385). Flagship sets such as Hisense’s 116-inch RGB mini-LED achieve 97% BT.2020 coverage and 10 000-nit peaks by tripling die counts per panel, massively expanding demand for chip-scale packages. Placement tolerances tighter than 50 µm and yield targets above 99.9% elevate the barrier to entry, prompting long-term supply tie-ups between BOE, China Star Optoelectronics, and domestic packagers. Korean and Japanese competitors now face a 50% price disadvantage on comparable specifications, spurring them to accelerate their own RGB micro-LED roadmaps.

Automotive LED Penetration in NEVs

LED adoption in China’s passenger-vehicle fleet surpassed 81.3% in 2024, and penetration in new-energy vehicles is already above 90%. Adaptive driving-beam modules demand high-power arrays that withstand −40 °C to +105 °C cycling and maintain sub-3-step MacAdam consistency, performance levels achievable only through automotive-grade process control. Domestic packagers with AEC-Q102 certification, notably Refond and Jufei, secured multi-year design wins with BYD, NIO, and Geely, commanding 15%-20% price premiums. The segment’s rigorous qualification cycles lock out commodity suppliers, concentrating revenue among quality-driven incumbents.

Export-Oriented EMS Demand for SMD Packages

Although U.S. tariffs add 15%-25% to Chinese exports, electronics manufacturing services firms in Shenzhen-Foshan maintain competitive landed costs by colocating package, substrate, and driver-IC supply in a single logistics radius. Lead times are typically 25%-35% shorter than in Vietnam or Malaysia, incentivizing multinational luminaire brands to keep sourcing SMD LEDs from Guangdong. To preserve margin while sidestepping tariffs, several Chinese packagers now ship semi-knocked-down kits to bonded hubs in Southeast Asia for final assembly.[2]Ministry of Commerce of the People’s Republic of China, “Circular on Rare-Earth Export Controls,” mofcom.gov.cn This hybrid model mitigates policy risk without offshoring core test-and-burn-in processes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Erosion from Excess Mid-Power Capacity | -0.8% | National, most acute in Zhejiang and Guangdong mid-tier packagers | Short term (≤ 2 years) |

| Dependence on Imported High-Performance Phosphors | -0.6% | National, affecting premium automotive and display packagers | Medium term (2-4 years) |

| Labor-Cost Inflation in Coastal Clusters | -0.4% | Guangdong (Shenzhen, Dongguan, Foshan), Zhejiang (Ningbo) | Long term (≥ 4 years) |

| Recycling and E-Waste Compliance Costs | -0.3% | National, with stricter enforcement in Guangdong, Jiangsu, Zhejiang | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Erosion from Excess Mid-Power Capacity

March 2026 list-price hikes of 3%-25% announced by leading packagers were quickly undercut in Zhejiang, where defect rates in budget lines still hover near 15% and equipment utilization lags the 85% break-even threshold. Combined industry revenue grew 8.9% in 2024, yet profit expansion was confined to firms with automotive or mini-LED focus, highlighting the fragility of commodity pricing. Revenue at MLS and NationStar declined in the first half of 2025, even as niche players Refond and Jufei posted double-digit growth, confirming the structural oversupply in mid-power formats. Until plant closures or demand growth absorb this overhang, margin compression will persist, discouraging fresh investment in SMD lines.

Dependence on Imported High-Performance Phosphors

China refines more than 80% of the global supply of rare-earth oxides, yet premium red and narrow-band green phosphors still rely on Japanese and German suppliers. The December 2025 expansion of export controls on lanthanum, cerium, yttrium, and europium raised spot prices 20%-30% for assemblers lacking long-term contracts. Automotive packages that must hold Δu'v' below 0.007 over life cycles cannot easily substitute domestic blends without requalification, creating a cost squeeze for tier-one packagers. R&D programs are accelerating to develop alternative host lattices with lower heavy-rare-earth content, but commercial deployment remains several years away, leaving a medium-term supply chain vulnerability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Architecture: CSP Expansion Underpins Mini-LED Growth

Chip-scale packages are projected to expand at a 6.78% CAGR through 2031 as television makers move from white backlights to RGB mini-LED engines that need higher die density and tighter placement tolerances. Surface-mount device formats still held 42.78% of the China LED packaging market share in 2025, as decades of automation have driven defect rates below 2% and pushed unit pricing to under USD 0.10 for 10 000-piece orders.

High-volume 2835, 3030, and 5050 footprints remain indispensable in residential lamps, yet flip-chip devices without wire bonds now dominate high-current automotive modules that need superior heat dissipation. Glass-substrate mass-transfer lines under construction in Tianmen aim for 99.995% transfer yields, a threshold that could unlock cost-effective micro-LED wearables and automotive displays.

By Power Class: High-Power Packages Capture Automotive Upside

In 2025, mid-power LEDs, rated between 0.5-1 W, accounted for 35.49% of total revenue. However, due to a persistent oversupply, these LEDs are grappling with single-digit gross margins. On the other hand, high-power packages, rated between 1-3 W, are witnessing a growth rate of 6.94% CAGR. This surge is largely attributed to their adoption in adaptive driving-beam headlights and industrial high-bay luminaires, both of which are known to reduce fixture counts and maintenance labor.

Indicator-class emitters with power levels below 0.5 W play a dominant role in the wearables and signage markets. However, the extremely narrow profit margins in these segments significantly constrain opportunities for reinvestment and further development. At the top end, copper-substrate emitters above 3 W now target horticultural grow lights and stadium floodlamps that absorb the 30%-50% price premium in exchange for higher lumen density and long L70 life.[3]Nichia Corporation, “NS2W806H-B2 Product Datasheet,” nichia.co.jp

By Emission Type: UV Momentum Builds Premium Niches

In 2025, visible-spectrum devices are projected to dominate shipments, accounting for 88.99% of the total. These devices play a crucial role in powering everyday lighting, displays, and automotive lamps. On the other hand, ultraviolet packages are experiencing significant growth, with a compound annual growth rate (CAGR) of 6.74%. This growth is primarily attributed to the increasing adoption of UV-A systems, which enhance the efficiency of industrial ink curing processes, and UV-C diodes, which are replacing mercury lamps in medical sterilizers. The shift toward UV-C diodes aligns with the regulatory requirements set forth by the Minamata Convention.

Sapphire or aluminum-nitride substrates, hermetic silicones, and narrow binning reduce UV bill-of-materials costs, enabling average selling prices 25% above those of mid-power white LEDs. Packagers that validate 10 000-hour L70 performance have begun locking multi-year design wins with equipment OEMs, creating an annuity-like revenue stream that cushions pricing pressure in commodity segments.

By Material Chemistry: Phosphor Innovation Drives Differentiation

Substrates contributed 30.35% of 2025 revenues, spanning ceramic, metal-core PCB, glass, and silicon bases that anchor thermal paths in high-power modules. Driven by narrow-band red blends and quantum-dot hybrids, which enhance color gamut and efficacy in premium televisions and adaptive headlights, the market for phosphors and optical coatings is witnessing a growth rate of 6.91% CAGR.

China’s December 2025 export-control expansion covering lanthanum, cerium, yttrium, and europium pushed spot prices 20%-30%, rewarding packagers with captive blending lines or long-term contracts. Domestic R&D is now focusing on alternative host lattices. These lattices reduce heavy-rare-earth content while maintaining Δu′v′ stability. The goal is to lessen dependence on overseas suppliers within three years.

By Application: Automotive Lighting Surges Past Commodity Segments

In 2025, general lighting contributed 40.48% of the total revenue. However, the demand for retrofitting in mature urban markets has reached a point of stagnation. On the other hand, automotive modules are experiencing significant growth, expanding at a compound annual growth rate (CAGR) of 8.85%. This growth is primarily driven by the increasing penetration of LED technology in new-energy vehicles, which has exceeded 90%. Additionally, adaptive driving-beam systems have achieved an installation rate of 38% in 2024, further supporting the expansion of this segment.

Mini-LED television backlights topped 8 million domestic units in 2025 and are expected to exceed 10 million in 2026, sustaining long-range pull for chip-scale packages. UV curing and horticultural systems remain niche in volume but deliver 15%-20% gross-margin premiums by demanding customized wavelengths and ruggedized encapsulants, balancing the overall profit mix of diversified packagers.

Geography Analysis

Guangdong province accounted for 52% of national output in 2025, giving it the largest share of the China LED packaging market among all regions. Shenzhen and Foshan ship more than 65% of the country’s LED exports to Europe and North America, helped by 60%-70% factory automation that cushions the monthly wages of USD 800-USD 850. The dense cluster of epitaxy, driver IC, and substrate vendors lets plants cut lead times by 25% compared with inland rivals. Rising municipal green-power surcharges and stricter waste-recycling audits are raising overhead, yet the province keeps its edge through scale and supply-chain speed. Provincial grants for adaptive driving-beam modules and mini-LED backlights are directing new capital toward high-spec lines.

The Yangtze River Delta, comprising Jiangsu and Zhejiang, accounts for 28% of the China LED packaging market through export-oriented surface-mount device lines. Hangzhou and Ningbo firms install bonded warehouses in Ho Chi Minh City and Bac Ninh, then finish lamp kits there to skirt 15%-25% U.S. tariffs while still relying on Guangdong-made packages. This hybrid logistics model reduces landed costs by 10% while preserving customer service levels for North American retail channels. Regional governments offer tax refunds on outbound shipments that meet ISO 14001 documentation rules, steering assembly houses to certify sustainable sourcing. Tight labor markets are starting to lift wages, yet process automation offsets most of the pressure.

Inland hubs such as Wuhan, Tianmen, and Chongqing are attracting new plants with land subsidies and discounted power. WG Tech’s glass-substrate micro-LED campus in Tianmen aims for 100 000 m² yearly capacity and promises 99.995% transfer yields, signaling that high-precision lines no longer need a coastal address. Logistics upgrades, including direct rail links to Shenzhen ports, cut transit time for finished modules by two days. Automotive OEMs in Hubei and Sichuan are seeking dual sourcing away from the coast, so packagers are adding pilot lines near vehicle assembly clusters. Lower land rent reduces fixed costs by 12% compared with Shenzhen, helping inland factories reach break-even at lower volumes. As regional diversification advances, supply-chain resilience improves, and inland sites capture a rising slice of future expansion.

Competitive Landscape

The industry remains fragmented, with the ten largest suppliers holding only 18.9% of 2024 revenue, well below levels that signal oligopoly. MLS and NationStar still lead unit volumes in general lighting, but weak mid-power pricing dragged each firm’s first-half 2025 sales lower. Refond and Jufei posted double-digit growth by focusing on automotive-qualified arrays and chip-scale mini-LED dies, demonstrating the payoff of quality certifications. Hongli Zhihui secured a five-year supply deal with BOE for RGB mini-LED backlights, locking in baseline capacity for its new Guangzhou plant.

Domestic leaders are doubling down on vertical integration. San’an now combines gallium nitride epitaxy, flip-chip die fabrication, and driver IC design within a single campus, shaving 3 weeks from product launch cycles. MLS merged a power-management-IC design house in January 2026, aiming to bundle control electronics with high-power packages for adaptive driving beams. Refond expanded in-house phosphor blending following the tightening of rare-earth export controls, ensuring color consistency for automotive headlamps. Jufei installed an Industry 4.0 execution system that pushes real-time yield data to its customer portal, a move that won repeat orders from television makers.

International incumbents, led by Nichia, Lumileds, and ams OSRAM, keep a firm hold on premium automotive and specialty niches where decades of reliability data give them an engineering moat. Lumileds released its HL2X series in 2025, targeting outdoor luminaires that need 191 lm/W at 700 mA, but the firm ended commodity 2835 production in China to stem margin bleed. Seoul Semiconductor opened a joint lab in Shanghai to co-develop UV-C sterilization modules with local equipment makers, signaling a shift toward cooperative innovation rather than pure component sales. Samsung LED is accelerating silicon-carbide photonics research, betting that laser-based lighting will leapfrog high-power LEDs in luxury vehicles by the next model cycle. Together, these moves show global players trimming low-end exposure while betting on differentiated technology to protect share.

China LED Packaging Industry Leaders

MLS Co. Ltd.

NationStar Optoelectronics Co. Ltd.

Hongli Zhihui Group Co. Ltd.

Refond Optoelectronics Co. Ltd.

Nichia Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Major suppliers, including MLS, Kinglight, and Syntec, implemented list-price increases of 3%-25% across LED lines, citing surging gold, silver, and copper costs; mid-power customers resisted most hikes.

- February 2026: Tongbao Optoelectronics debuted on the Beijing Stock Exchange, earmarking proceeds for new automotive lamp-module lines after booking CNY 717 million (USD 99 million) revenue in 2025.

- January 2026: TCL Huaxing bought an 80% stake in Zhaoguang Optoelectronics for CNY 490 million (USD 68 million) to secure in-house mini-LED backlight capacity.

- December 2025: China expanded rare-earth export controls to include lanthanum, cerium, yttrium, and europium, lifting high-performance phosphor costs for packagers that rely on spot markets.

China LED Packaging Market Report Scope

The China LED Packaging Market Report is Segmented by Packaging Architecture (Surface Mount Device (SMD), Chip-on-Board (COB), Chip Scale Package (CSP), Flip-Chip LED Packages, Dual In-line Package (DIP / Through-hole), Other Packaging Architectures), Power Class (Low Power (Below 0.5 W), Mid Power (0.5-1 W), High Power (1-3 W), Ultra-High Power (Above 3 W)), Emission Type (Visible LED Packages, Infrared (IR) LED Packages, Ultraviolet (UV) LED Packages), Material Chemistry (Substrates, Encapsulation, Bonding / Die-Attach, Phosphors / Coatings), Application (General Lighting, Automotive Lighting, Display And Backlighting, Consumer Electronics, Industrial and Specialty), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Surface Mount Device (SMD) |

| Chip-on-Board (COB) |

| Chip Scale Package (CSP) |

| Flip-Chip LED Packages |

| Dual In-line Package (DIP / Through-hole) |

| Other Packaging Architectures (IMD, GOB, Mini-LED Display Packaging) |

| Low Power (Below 0.5 W) |

| Mid Power (0.5-1 W) |

| High Power (1-3 W) |

| Ultra-High Power (Above 3 W) |

| Visible LED Packages |

| Infrared (IR) LED Packages |

| Ultraviolet (UV) LED Packages |

| Substrates |

| Encapsulation |

| Bonding / Die-Attach |

| Phosphors / Coatings |

| General Lighting |

| Automotive Lighting |

| Display And Backlighting |

| Consumer Electronics |

| Industrial and Specialty |

| By Packaging Architecture | Surface Mount Device (SMD) |

| Chip-on-Board (COB) | |

| Chip Scale Package (CSP) | |

| Flip-Chip LED Packages | |

| Dual In-line Package (DIP / Through-hole) | |

| Other Packaging Architectures (IMD, GOB, Mini-LED Display Packaging) | |

| By Power Class | Low Power (Below 0.5 W) |

| Mid Power (0.5-1 W) | |

| High Power (1-3 W) | |

| Ultra-High Power (Above 3 W) | |

| By Emission Type | Visible LED Packages |

| Infrared (IR) LED Packages | |

| Ultraviolet (UV) LED Packages | |

| By Material Chemistry | Substrates |

| Encapsulation | |

| Bonding / Die-Attach | |

| Phosphors / Coatings | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display And Backlighting | |

| Consumer Electronics | |

| Industrial and Specialty |

Key Questions Answered in the Report

How fast is automotive LED demand rising in China?

Automotive lighting revenue is expanding at an 8.85% CAGR through 2031 as adaptive driving-beam systems move toward mainstream adoption.

Which packaging architecture is gaining the most share?

Chip-scale packages show the highest growth, expanding at a 6.78% CAGR on the back of mini-LED television and automotive module uptake.

What threatens profitability in commodity LED lines?

Excess mid-power capacity keeps prices under pressure, and Zhejiang factories often run below optimal utilization, eroding margins.

How are rare-earth export controls influencing costs?

The December 2025 inclusion of lanthanum, cerium, yttrium, and europium in export quotas lifted specialty-phosphor prices by 20%-30% for non-integrated packagers.

Why are suppliers adding bonded hubs in Vietnam?

Bonded assembly in Southeast Asia helps Chinese firms bypass 15%-25% U.S. tariffs while maintaining core packaging and burn-in operations in Guangdong.

What is the outlook for UV LED niches?

UV packages, though small in volume, command premium pricing and are growing at 6.74% annually due to industrial curing and sterilization demand.

Page last updated on: