Europe LCV Rental Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.93 Billion |

| Market Size (2026) | USD 8.36 Billion |

| Market Size (2031) | USD 10.91 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

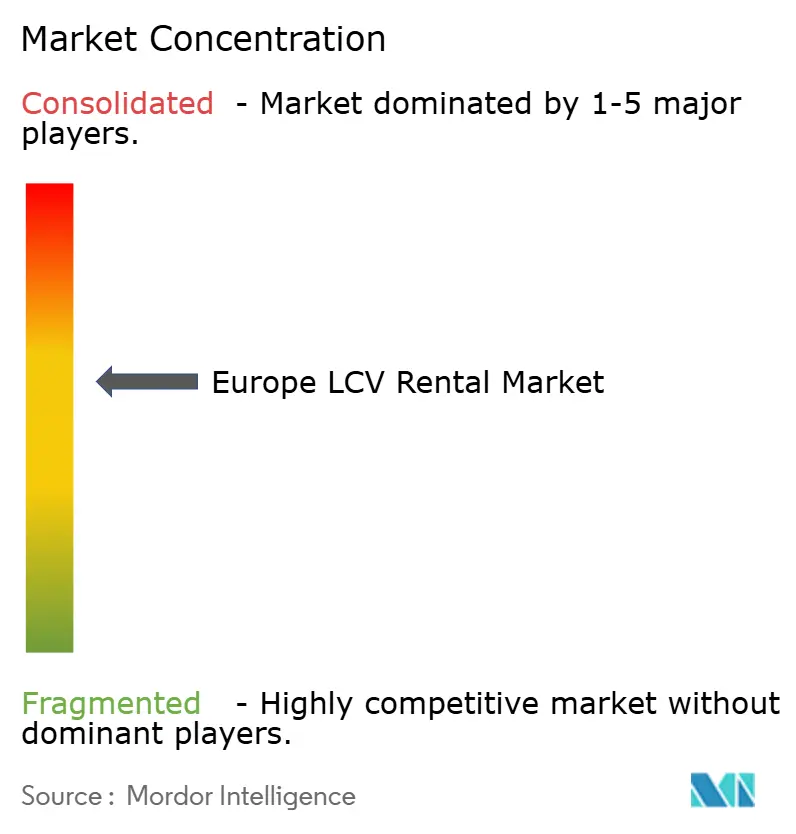

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe LCV Rental Market Analysis by Mordor Intelligence

The Europe LCV Rental Market size was valued at USD 7.93 billion in 2025 and estimated to grow from USD 8.36 billion in 2026 to reach USD 10.91 billion by 2031, at a CAGR of 5.45% during the forecast period (2026-2031). Strong parcel growth tied to e-commerce, widening adoption of asset-light logistics models, and accelerating electrification agendas are the core forces shaping the competitive trajectory. Operators with dense depot networks and digital booking capabilities are best positioned to capture geographically fragmented demand. At the same time, supply-side constraints linked to semiconductor shortages and WLTP compliance costs continue to tighten fleet renewal cycles. Germany anchors growth on the back of its dominant manufacturing and logistics ecosystem. In contrast, the United Kingdom outperforms on a percentage basis as post-Brexit distribution patterns favor cross-border flexibility. Meanwhile, rising corporate ESG commitments are nudging procurement teams toward battery-electric models, prompting rental companies to refine charging partnerships and telematics integration.

Key Report Takeaways

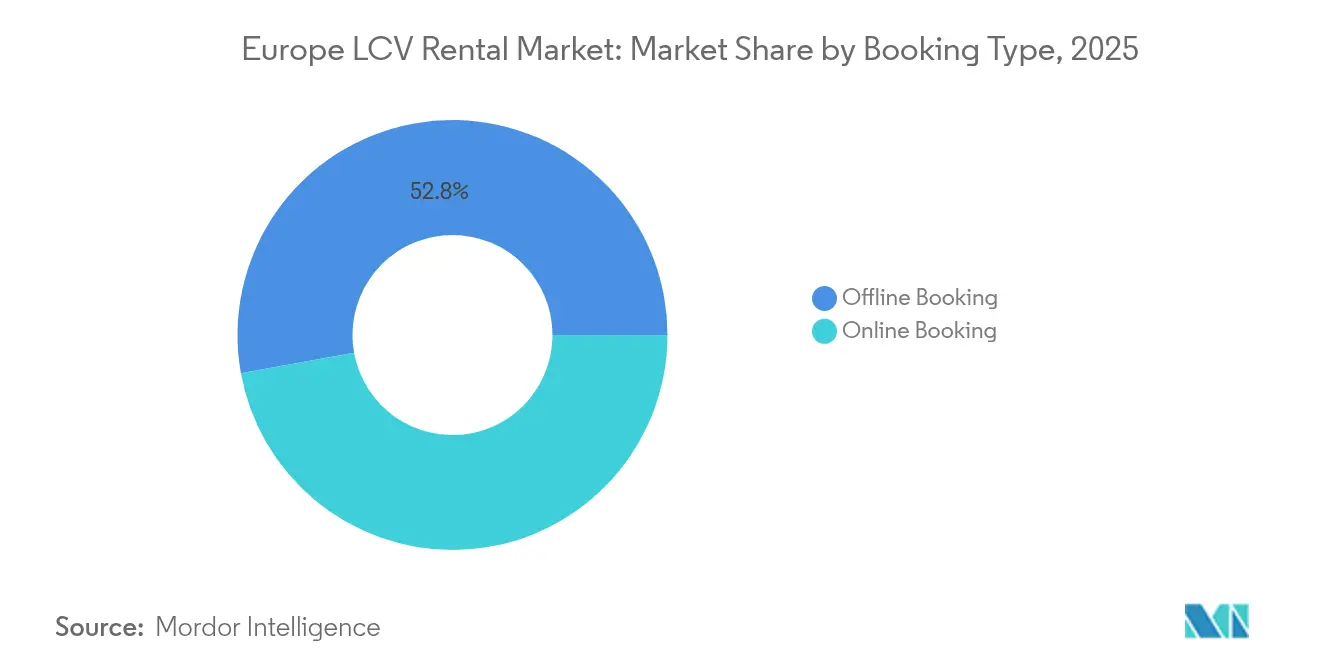

- By booking type, offline reservations held 52.84% of the European LCV rental market size in 2025; online bookings are advancing at a 5.49% CAGR during the forecast period (2026-2031).

- By rental type, long-term contracts commanded a 63.05% share of the European LCV rental market size in 2025, while short-term rentals are expanding at a 5.52% CAGR during the forecast period (2026-2031).

- By vehicle type, large vans accounted for 40.95% of the European LCV rental market share in 2025; compact vans posted the highest projected CAGR of 5.55% during the forecast period (2026-2031).

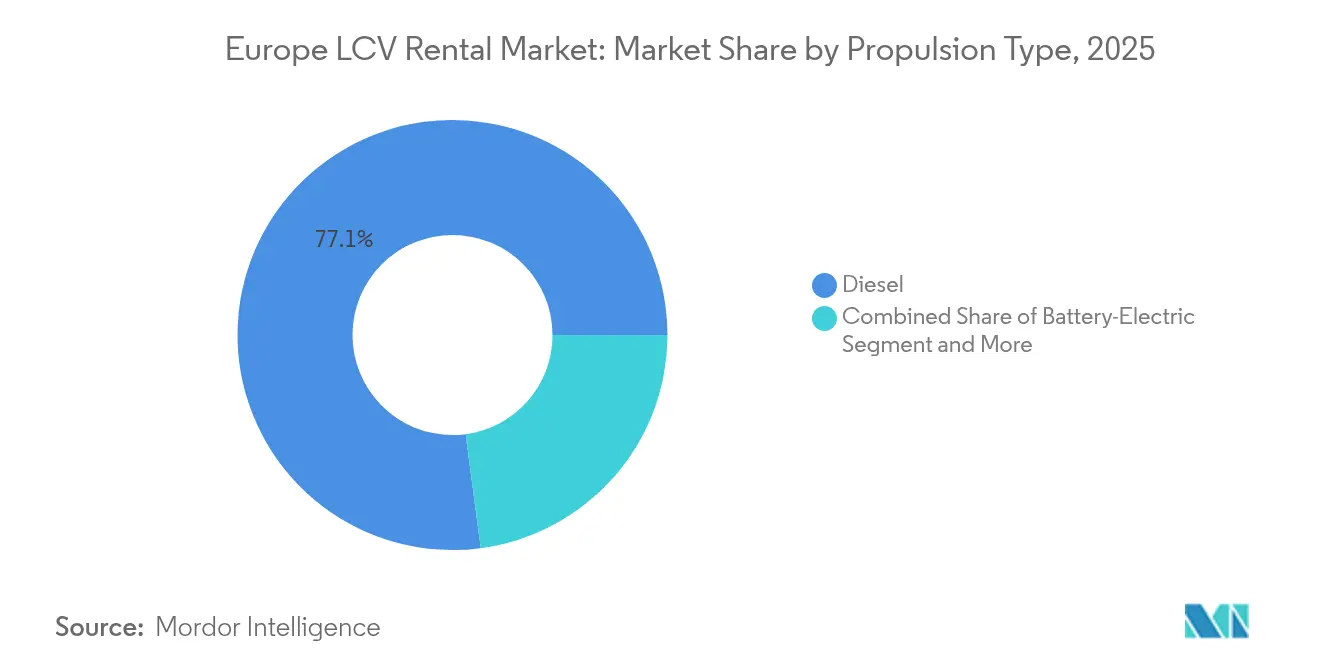

- By propulsion, diesel units retained 77.10% of the European LCV rental market size in 2025, whereas battery-electric vehicles are growing at a 5.53% CAGR during the forecast period (2026-2031).

- By end-user, CEP & e-commerce logistics captured 36.42% of the European LCV rental market size in 2025, leading growth at a 5.58% CAGR during the forecast period (2026-2031).

- By country, Germany held the top position with 38.40% share of the European LCV rental market in 2025, whereas the United Kingdom is forecast to record the fastest expansion at a 5.56% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe LCV Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated E-Commerce Parcel Volumes | +1.2% | Global, strongest in Germany, UK, France | Short term (≤ 2 years) |

| Shift To Asset-Light Gig-Economy Delivery Fleets | +0.8% | Urban centers across EU-27, Nordic expansion | Medium term (2-4 years) |

| Corporate ESG Targets | +0.7% | Germany, Netherlands, Nordics lead adoption | Long term (≥ 4 years) |

| Post-Brexit Cross-Border Rental Synergies | +0.6% | UK-EU corridor, Ireland-UK routes | Medium term (2-4 years) |

| Adoption Of Real-Time Telematics | +0.5% | Germany, France, UK leading implementation | Medium term (2-4 years) |

| OEM-Captive Subscription Pilots | +0.4% | Germany, France focus with EU-wide expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated E-Commerce Parcel Volumes

Explosive online retail activity lifts daily parcel counts, making flexible van access indispensable for peak-season coverage [1]“Cross-Border E-Commerce Report 2025,” DHL eCommerce, dhl.com. Same-day and next-day delivery promises to intensify the call for distributed depots that only large European LCV rental market networks can satisfy. Short-term peaks tied to Black Friday and holiday surges now account for an increasingly large slice of annual parcel flows, sharpening demand for daily and weekly hires. Rental fleets also help couriers avoid the idle-asset burden during off-peak months, a key cost distinction versus ownership. Compact van formats become even more vital as warehouse footprints migrate closer to dense city cores. Operators combining a nationwide footprint with real-time booking APIs outperform peers on utilization and yield.

Shift to Asset-Light Gig-Economy Delivery Fleets

Platform-based couriers such as Uber Eats and Gorillas push drivers to furnish their own vehicles, yet many lack the capital for outright purchases. The European LCV rental market offers a scalable workaround with flexible terms and usage-based pricing. TIMOCOM reported a high year-on-year jump in freight requests in 2024, underlining the strain on traditional fleet planning at [2]“Transport Market Barometer 2024,” TIMOCOM, timocom.com . Rental providers now craft gig-focused packages that blend short-duration contracts, lower deposits, and app-enabled onboarding. Such offerings help independent drivers comply with insurance and emission rules while minimizing working-capital exposure. In response, mainstream rental firms are rolling out weekend-only or evening-only rates aligned with peak food-delivery slots.

Corporate ESG Targets Boosting Electric LCV Leasing

Multinationals with science-based carbon targets are pivoting to battery-electric vans but remain wary of technology obsolescence risk. Renting allows pilot deployment without residual-value exposure, so demand for electric units within the European LCV rental market is accelerating. Europcar has pledged significant electric fleet additions, mirroring Avis Budget and Sixt commitments. Early movers lock in green-fleet availability contracts, often coupled with charging-as-a-service bundles that guarantee route-specific uptime. Regulators add impetus: the EU’s 2030 zero-emission fleet mandate effectively caps future diesel acquisitions, tilting corporate procurement toward electric rental agreements. Over time, higher residual values and falling battery costs will compress the total cost of operation gaps, widening the addressable customer base.

Post-Brexit Cross-Border Rental Synergies

Logistics firms straddling the UK-EU corridor must meet divergent registration and road-user charges. Instead of owning two parallel fleets, many book-compliant vehicles are in-country via rental partners. This reality has boosted cross-channel asset pools and fostered alliances among leading European LCV rental market operators. Rental agreements now often include customs documentation services, vehicle telematics pre-configured for EU roaming, and insurance endorsements that satisfy both jurisdictions. Reciprocal fleet-swap programs are emerging, especially on Ireland-UK routes, ensuring consistent vehicle standards across depots. These synergies create incremental revenue streams and raise fleet utilization, offsetting post-Brexit administrative overhead.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight EU-27 WLTP Emission Caps | -0.4% | EU-27 wide, Germany and France leading implementation | Short term (≤ 2 years) |

| Chip-Shortage-Induced Delivery Lags | -0.3% | Global supply chain impact, strongest in Germany manufacturing | Medium term (2-4 years) |

| Rising Insurance Premiums | -0.2% | Urban centers across EU-27, UK particularly affected | Short term (≤ 2 years) |

| Municipal Access Charges For Diesel Vans | -0.2% | London, Paris, Amsterdam, Berlin expanding to other cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tight EU-27 WLTP Emission Caps Raising Fleet Costs

Successive WLTP stages oblige rental firms to purchase pricier Euro 6e and electric models. Germany’s 2025 updates expand reporting obligations, adding administrative costs and pre-delivery retrofit work for telematics tracking [3]“WLTP Phase-In Guidelines 2025,” BMW Group, bmwgroup.com . France complements EU rules with weight-based penalties that further elevate diesel van acquisition prices. These costs squeeze EBITDA margins unless passed through as surcharges, which can temper demand from price-sensitive SME clients. Many operators respond by front-loading electric orders to secure subsidies before expiry, temporarily inflating capital outlays. Over the long term, stricter standards indirectly accelerate fleet modernization, lifting residual values and lowering maintenance events per rental day.

Chip-Shortage-Induced Delivery Lags

Semiconductor bottlenecks have extended order lead times for new vans over the past 12 months, forcing operators to retain older assets longer. German OEMs report intermittent assembly pauses, narrowing the supply funnel for high-spec telematics-ready vehicles. Aged fleets carry higher maintenance spend and risk SLA breaches when breakdowns occur during peak season. Rental companies counter with proactive refurbishment programs, but workshop downtime still trims available fleet days. This capacity pinch limits the European LCV rental market’s ability to fully monetize current demand upswings, especially during Q4 parcel peaks. Until chip fabs reach planned European expansion volumes, delivery reliability will remain a headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Transformation Accelerates

Offline contracts controlled the most significant slice of the European LCV rental market share in 2025 at 52.84%, underscoring entrenched relationship-based procurement for multi-year logistics agreements. Online portals, however, posted a 5.49% CAGR and are forecast to keep outpacing overall market growth through 2031.

Growth in digital reservations reflects rising smartphone penetration among depot managers and gig-economy drivers. SIXT’s 2024 roll-out of in-app charging integration showcased how application programming interfaces streamline ancillary services, driving repeat bookings. Online platforms offer dynamic pricing and real-time availability that offline channels cannot replicate, lifting fleet utilization. As artificial intelligence-based demand forecasting matures, digital channels will underpin margin expansion by aligning day-to-day pricing with parcel activity fluctuations across postal codes. Therefore, the European LCV rental market will see hybrid models where account managers handle framework contracts while tactical peaks flow through apps.

By Rental Type: Long-Term Contracts Sustain Fleet Planning

Long-term leases contributed 63.05% to the Europe LCV rental market size in 2025, giving operators predictable cash flows that support multi-year fleet financing. Short-term hires are growing faster at 5.52% CAGR, a trend fueled by volatile parcel volumes and on-demand food delivery startups.

Extended leases allow logistics majors to lock in emission-compliant vans at fixed rates, shielding budgets from residual-value swings. Rental firms can align depreciation schedules with WLTP phase-ins, keeping utilization high. Short-term expansion, meanwhile, is underpinned by weekend flash sales and festival peaks where courier demand multiplies for a few days. Telematics dashboards let operators shift idle inventory across depots overnight, minimizing repositioning costs. As subscription economics spread from passenger cars to light commercials, mid-length contracts of 3-12 months may blur the conventional long-versus short-term divide within the European LCV rental market.

By Vehicle Type: Compact Vans Win Urban Efficiency Battle

Large vans held 40.95% of the European LCV rental market size in 2025, due to their versatile payload-to-footprint ratio. Compact vans are rising fastest, projected at 5.55% CAGR through 2031, as low-emission zones reward smaller formats with easier access.

City freight consolidation centers push parcels into micro-hubs from which compact vans complete the final leg. Reduced turning radius and tighter curb clearances help drivers meet stringent delivery windows in congested downtown zones. Rental operators allocate more capex toward small-wheelbase models to ensure compliance with municipal ULEZ restrictions. Box trucks remain the workhorses for specialized goods but face stagnation given license hurdles and scarce urban loading bays. Looking ahead, modular cargo pod systems may further elevate compact van appeal by enabling quick switchover between refrigerated and parcel configurations.

By Propulsion Type: Electric Adoption Gains Speed

Diesel engines still represented 77.10% of the European LCV rental market in 2025, reflecting unparalleled refueling convenience on long-haul lanes. Battery-electric units boast the highest CAGR at 5.53% and are central to meeting Scope 3 emission targets.

Public charging points across 17 European nations reached a record number in 2024, including multiple high-power sites suitable for commercial van duty cycles. Rental companies partner with charging-network operators to bundle power costs into daily rates, simplifying client accounting. Hybrid and gas-powered alternatives offer transitional compliance for duty cycles beyond current battery ranges, yet technological leapfrogging may compress their relevance window. By 2030, WLTP tailpipe thresholds will effectively force new fleet purchases toward zero-emission platforms, accelerating the shift within the European LCV rental market.

By End-User Industry: CEP & E-Commerce Leads Demand Curve

Courier, express, and parcel services captured 36.42% of the European LCV rental market in 2025 while expanding at a 5.58% CAGR to 2031. The sector’s outsized share mirrors the structural transition of consumption toward online channels.

Omnichannel retail strategies require micro-fulfillment nodes that push more shipments through suburban depots, elevating van demand. FMCG retailers follow closely, leveraging rental flexibility to cope with promotional spikes and cold-chain compliance. Construction utilities tap the European LCV rental market for crew-cab vans that shuttle teams and equipment between dispersed sites, but growth is steadier. Passenger shuttle initiatives, including ride-pool pilots, remain niche yet gain traction where municipal congestion charges incentivize shared mobility.

Geography Analysis

Germany anchored 38.40% of the European LCV rental market share in 2025, reflecting its central transport corridors and dense supplier base. High outbound manufacturing flows ensure stable backhaul loads, so rental firms achieve superior utilization. Stricter LEZ rules in Berlin, Munich, and Hamburg motivate corporates to shift from aging owned fleets to newer rental units. WLTP compliance timelines are therefore shortening replacement cycles and boosting fleet renewal.

The United Kingdom delivered the fastest growth at 5.56% CAGR, powered by e-commerce penetration exceeding 26% of total retail sales and by Brexit-driven reconfiguration of cross-border distribution . Rental demand spikes around customs bottlenecks as freight forwarders buffer inventory in inland depots. Gig-economy couriers, an estimated 500,000 drivers, rely heavily on daily van rentals to navigate dynamic earnings patterns. UK operators also experiment with subscription bundles combining van access, insurance, and fuel cards under one weekly fee.

France, Spain, and Italy compose a sizable secondary bloc. France’s weight-based malus taxes push legacy diesel van owners toward rental, particularly among SMEs facing liquidity constraints. Spain’s Madrid and Barcelona zero-emission corridors are early sandboxes for electric van pilots. Italy’s north-south logistics split makes cross-dock efficiency paramount, and rental pools help operators adapt fleet types to mountain versus city routes without tying up capex. The Rest of Europe cluster, the Netherlands, Nordics, and Central and Eastern Europe, presents mixed maturity. Dutch policymakers subsidize fast chargers, enabling early majority electric adoption among parcel couriers. Nordic corporations embed carbon accounting in procurement scorecards; rental firms with green fleets capture premium rates. Central and Eastern Europe’s GDP growth and nearshoring trends stimulate industrial output, pushing demand for affordable large vans.

Competitive Landscape

Four incumbent groups—Enterprise Holdings, Europcar Mobility Group, Sixt SE, and Avis Budget Group—accounted for roughly three-fifths of the European LCV rental market in 2024. Scale confers purchasing leverage with OEMs, which is vital during semiconductor shortages. These leaders run integrated telematics suites that monitor mileage, driver behavior, and battery health across borders, supporting predictive maintenance that sustains high uptime.

Strategic focus is shifting from fleet volume to service ecosystem depth. Enterprise is expanding depots near micro-fulfillment warehouses to guarantee 15-minute collection windows. Europcar bundles CO₂ reporting dashboards into corporate contracts, aiding ESG audits. Sixt’s dedicated Van & Truck division targets Germany, France, and the United Kingdom with digital-first booking and delivery options. Avis Budget invests in AI-driven pricing engines that adjust rates according to parcel demand heat maps.

Competitive pressure also arises from OEM-backed subscription offers such as Stellantis Free2Move and Daimler’s electric eVan-rental pilots. These programs leverage captive finance arms to undercut independent lessors on the total cost of access. Regional specialists respond by carving niches: temperature-controlled vans for pharma, crew-cab 4x4s for Nordic utility repairs, and compliant fleets for Adriatic ferry operations. Technological differentiation and regulatory expertise will determine margin resilience over the next cycle of the European LCV rental market.

Europe LCV Rental Industry Leaders

Avis Budget Group

The Hertz Corporation

Enterprise Holdings, Inc.

FRAIKIN SAS

Europcar Mobility Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Volvo Group and Renault Group formed Flexis SAS to build electric light commercial vehicles, committing USD 600 million for 2026 production.

- February 2024: SIXT integrated public charging access and automated billing into its mobile app for electric van rentals.

- January 2024: SIXT inked a multi-year procurement agreement with Stellantis covering 250,000 vehicles across European markets.

Europe LCV Rental Market Report Scope

The Europe Light Commercial Vehicle Rental Market report offers the market dynamics, latest trends, size, share, and industry overview. The Europe Light Commercial Vehicle Rental Market is segmented by Booking Type ( Online booking and Offline Booking), By Rental Type (Short Term and Long Term), and By Country ( Germany, United Kingdom, France, Spain, Italy, and Rest of Europe)

Based on booking type, the market is segmented as Online booking and Offline Booking.

By Rental Type, the market is segmented as Short Term and Long Term,

and By Country, the market is segmented as Germany, United Kingdom, France, Spain, Italy, and the Rest of Europe.

| Online Booking |

| Offline Booking |

| Short-Term |

| Long-Term |

| Compact Vans (<3.0 t GVW) |

| Large Vans (3.0-3.5 t GVW) |

| Pick-ups & Crew-cabs |

| Box Trucks (3.5-7.5 t) |

| Diesel |

| Battery-Electric |

| Hybrid & Alternative Fuels (CNG/LNG/H2) |

| CEP & E-commerce Logistics |

| FMCG & Retail |

| Construction & Utilities |

| Passenger Shuttle & Ride-pool |

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Rest of Europe |

| By Booking Type | Online Booking |

| Offline Booking | |

| By Rental Type | Short-Term |

| Long-Term | |

| By Vehicle Type | Compact Vans (<3.0 t GVW) |

| Large Vans (3.0-3.5 t GVW) | |

| Pick-ups & Crew-cabs | |

| Box Trucks (3.5-7.5 t) | |

| By Propulsion Type | Diesel |

| Battery-Electric | |

| Hybrid & Alternative Fuels (CNG/LNG/H2) | |

| By End-User Industry | CEP & E-commerce Logistics |

| FMCG & Retail | |

| Construction & Utilities | |

| Passenger Shuttle & Ride-pool | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the European LCV rental market in 2026?

The market is valued at USD 8.36 billion in 2026 and is projected to climb to USD 10.91 billion by 2031.

Which country holds the most significant share of van rentals in Europe?

Germany has a 38.40% share in 2025 due to its strong manufacturing and logistics infrastructure.

What fuels the fastest growth in European van rentals?

Rising e-commerce parcel volumes and shifting toward asset-light gig-economy delivery fleets drive the highest demand upticks.

How are electric vans impacting rental fleets?

Battery-electric models are expanding at a 5.53% CAGR as companies use rentals to meet ESG targets without ownership risk.

Who are the leading players in European LCV rentals?

Enterprise Holdings, Europcar Mobility Group, Sixt SE, and Avis Budget Group control about 65% of the market, giving it a moderate concentration.

Page last updated on: