Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

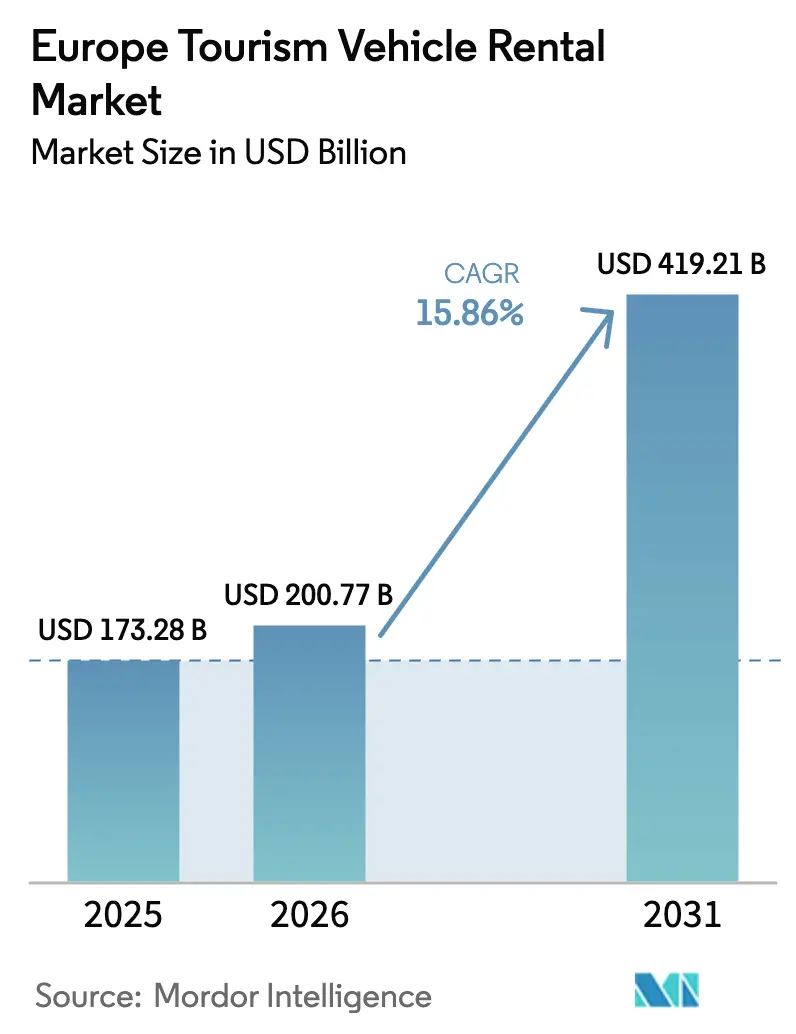

| Base Year Market Size (2025) | USD 173.28 Billion |

| Market Size (2026) | USD 200.77 Billion |

| Market Size (2031) | USD 419.21 Billion |

| Growth Rate (2026 - 2031) | 15.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Tourism Vehicle Rental Market Analysis by Mordor Intelligence

The Europe Tourism Vehicle Rental Market size is expected to grow from USD 173.28 billion in 2025 to USD 200.77 billion in 2026 and is forecast to reach USD 419.21 billion by 2031 at 15.86% CAGR over 2026-2031. Pent-up leisure demand, widening Gen Z adoption of access-over-ownership mobility models, and continued constraints on air-rail capacity all reinforce the positive trajectory of the European tourism vehicle rental market. Operators benefit from dynamic-pricing algorithms that lift average daily rates, while EU incentive schemes for electric-vehicle (EV) fleets underpin long-term margin resilience. Technology integration represents both opportunity and operational complexity, with SIXT pioneering app-integrated charging solutions across hundreds of thousands of European charge points, while fleet optimization through 5G and telematics enables real-time demand matching. The sector's growth trajectory faces headwinds from ultra-low-cost public transport expansion in Central and Eastern European markets, alongside proposed surge pricing regulations in Italy and Spain that could constrain revenue optimization strategies during peak tourism periods.

Key Report Takeaways

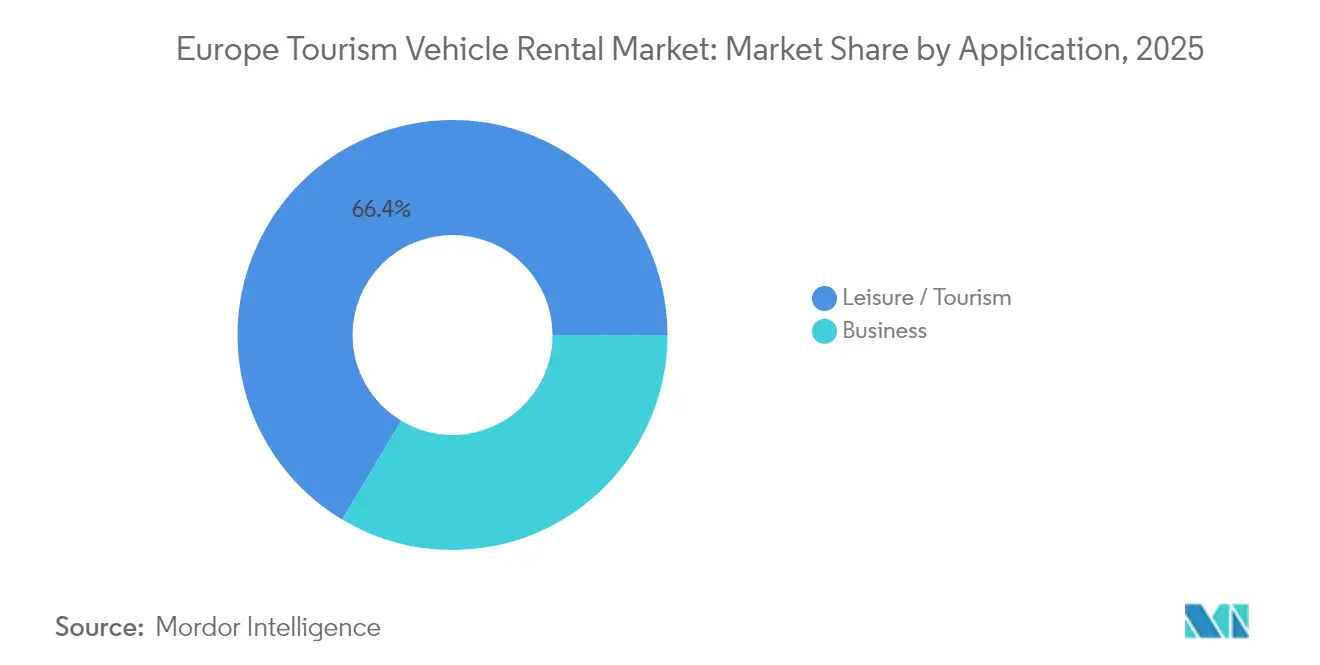

- By application, leisure tourism held 66.42% of the European tourism vehicle rental market share in 2025 and is projected to expand at a 16.12% CAGR through 2031.

- By booking channel, online platforms captured 72.84% revenue share of the European tourism vehicle rental market size in 2025, while the channel is set to post the fastest 16.05% CAGR.

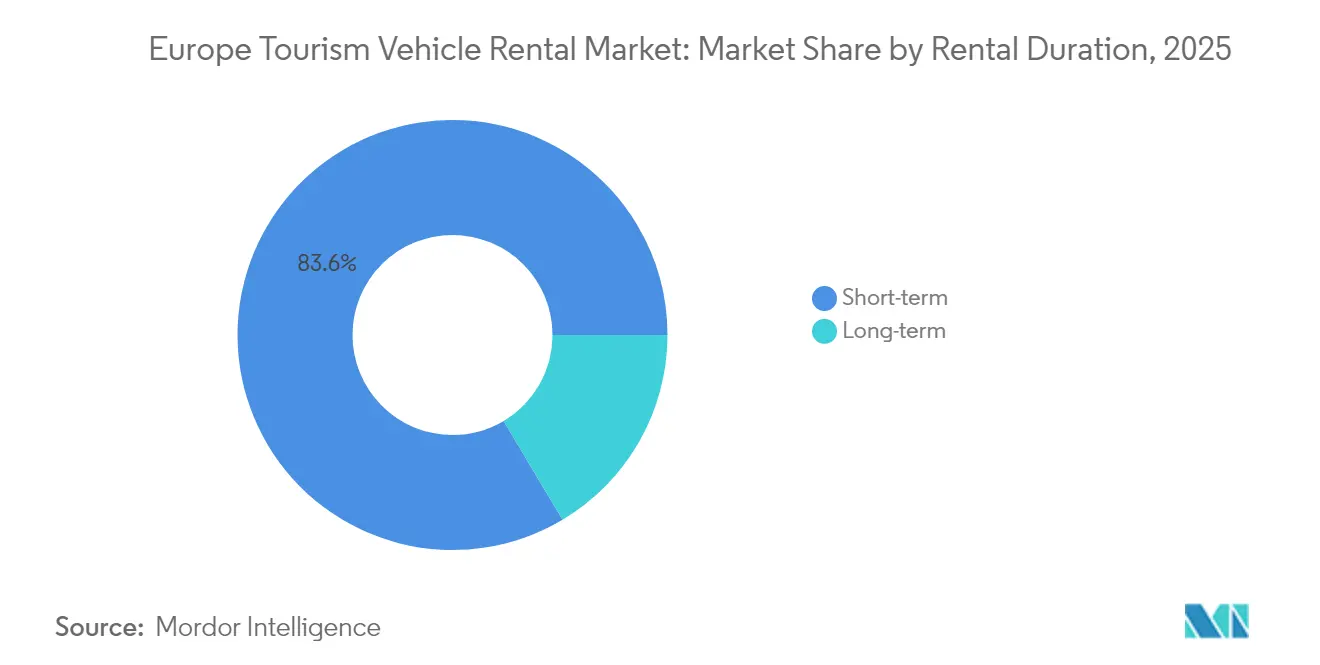

- By rental duration, short-term bookings commanded 83.55% of the European tourism vehicle rental market size in 2025; long-term rentals are poised for the strongest 15.92% CAGR.

- By vehicle type, economy and compact cars led with 36.22% revenue share in 2025, whereas electric and hybrid vehicles are forecast to grow the fastest at 16.34% CAGR.

- By country, Germany contributed 31.74% of 2025 revenue, while the United Kingdom is expected to see the highest 16.18% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Tourism Vehicle Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic intra-Europe leisure | +3.2% | Western Europe, Southern Europe | Medium term (2-4 years) |

| Shift from ownership to usership | +2.8% | UK, Germany, Netherlands | Long term (≥ 4 years) |

| Air-rail capacity pinch pushes tourists to road trips | +2.1% | Southern Europe, Mediterranean destinations | Short term (≤ 2 years) |

| Electric-vehicle subsidy schemes favour rental fleet renewals | +1.9% | EU core markets, Nordic countries | Medium term (2-4 years) |

| Dynamic-pricing algorithms | +1.7% | Early adoption in UK, Germany | Short term (≤ 2 years) |

| 5G/telematics integration | +1.4% | Western Europe, expanding to CEE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic intra-Europe leisure boom sustains rental demand

Demand has tilted toward flexible road trips as airport slot shortages and rail bottlenecks persist, making the Europe tourism vehicle rental market integral to itinerary planning. EU tourist establishments logged more than 3 billion guest-nights in 2024, a record that directly converted into higher fleet utilisation. Spain, Italy, and France captured the bulk of incremental visitors, rewarding operators located at gateway airports and downtown depots. Rental companies also lengthened average contract days because travelers explored multiple secondary cities per trip.

Shift from ownership to usership among Gen Z travellers

Digital-native Gen Z consumers perceive vehicles as on-demand mobility solutions rather than depreciating assets, dovetailing with car-sharing and subscription offers. Survey data show 57% of non-EV drivers across 12 EU states are open to battery-electric usage in the next vehicle decision cycle.[1]“Attitudes toward electric mobility in Europe,” European Environment Agency, eea.europa.eu. Netherlands-based car-share platforms logged around one fifth of the rise in corporate memberships, signalling wider crossover from business mobility budgets to leisure extensions.

Air-rail capacity pinch pushes tourists to road trips in Southern Europe

Summer 2024 highlighted structural congestion at key Mediterranean airports, while high-speed rail operators capped frequencies due to maintenance cycles. Ticket prices spiked, prompting visitors to pivot toward road travel. Secondary airports in Andalusia and Sicily reported double-digit expansion in rental pick-ups, underscoring the elasticity between transport modes. Operators benefited from longer booking windows that allowed them to optimise fleet allocation across regional stations. The margin uplift is most visible in one-way rentals that cater to multi-country itineraries, a format uniquely suited to the Europe tourism vehicle rental market.

Electric-vehicle subsidy schemes favour rental fleet renewals (2025-2028)

EU member states collected a decent amount for EV purchase incentives through 2028, covering up to EUR 7,000 per unit for fleet buyers. SIXT committed to buying as many as 250,000 vehicles from Stellantis, heavily weighted to battery models, demonstrating how subsidies offset higher acquisition cost. Planned installation of 3.5 million public chargers by 2030—up from roughly 900,000 now—reduces utilisation risk. Subsidy timelines align with typical fleet-rotation cycles, thereby smoothing residual-value volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-low-cost public transport in CEE markets | -1.8% | Central and Eastern Europe | Medium term (2-4 years) |

| EV charging-infrastructure latency | -1.5% | Rural areas across Europe, particularly Nordic and Alpine regions | Long term (≥ 4 years) |

| EU Digital Markets Act | -1.2% | EU-wide, with concentration in major tourism markets | Short term (≤ 2 years) |

| Surge-pricing caps | -0.9% | Italy and Spain, potential spillover to other Southern European markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ultra-low-cost public transport in CEE markets hampers conversion

Governments in Poland, Hungary, and Romania subsidise bus and rail fares that undercut daily rental rates by up to 70%. The price gap discourages tourists from booking cars, especially for point-to-point city breaks. Additionally, CEE cities have expanded multimodal ticketing that integrates trams, metro, and inter-city coaches, lowering friction for riders. Rental operators face utilisation dips during shoulder seasons when discretionary spend tightens. Some have responded by repositioning idle vehicles to Western markets, but logistics costs trim margins.

EV charging-infrastructure latency at rural tourist hot-spots

EU regulation mandates charging stations every 60 km along core corridors by 2025, yet mountain and coastal districts lag implementation, leaving coverage gaps. Alpine resorts in Austria and northern Sweden remain prone to queue-induced range anxiety. Rental companies must therefore maintain dual-fuel fleets, raising capital intensity. Seasonal peaks amplify the infrastructure crunch, pushing some operators to impose kilometre caps on EV bookings. Customer surveys cite charging concerns as the top barrier to selecting electric rentals for nature-based trips.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Leisure Tourism Drives Growth Despite Business Recovery

The leisure segment accounted for 66.42% of the Europe tourism vehicle rental market in 2025, and it is projected to outpace the overall market with a 16.12% CAGR to 2031, underscoring its dual role as both volume and growth engine. Leisure bookings surged as EU guest-night totals hit 3 billion in 2024, reflecting travelers’ preference for flexible road itineraries over group tours, a 2.2% increase compared to 2023. Intraregional trips represented 70% of cross-border flows, extending average rental durations and enhancing yield per contract. Multi-city journeys also increased one-way drop-off revenue.

Leisure growth also benefits from EU push for seamless Schengen travel, allowing tourists to drive across multiple countries without border controls. Promotional campaigns such as Spain’s “Travel Safe” initiative strengthened destination confidence, supporting longer stays that align with extended vehicle bookings. Digital influencers amplify road-trip itineraries, inspiring younger segments to replicate similar experiences, further widening the rental funnel.

By Booking Channel: Digital Transformation Accelerates Online Dominance

Online channels captured 72.84% of 2025 rental transactions and are forecast to log a 16.05% CAGR through 2031, cementing their primacy in customer acquisition. Algorithmic meta-search visibility, instant confirmation, and transparent pricing underpin customer trust. The EU Digital Markets Act labelled Booking Holdings a gatekeeper in 2024, raising the likelihood of higher commission structures. Operators mitigate dependence on intermediaries by refining direct-to-consumer apps that bundle rewards and seamless check-in.

Dynamic-pricing engines embedded in operator web portals sharpen revenue capture by tailoring rates to search-history signals. Free2move’s all-in-one mobility app offers access to more than 500,000 vehicles worldwide, integrating short-term rental, car-sharing, and subscription plans. Such super-apps reframe bookings as part of broader mobility ecosystems, reinforcing customer lifetime value.

By Rental Duration: Long-term Segment Emerges as Growth Driver

Short-term rentals—defined as contracts under 30 days—held 83.55% of revenue in 2025, yet the long-term category (1-3 months) is projected to expand at a 15.92% CAGR between 2026 and 2031. Subscription-style offers answer consumer needs for flexible yet commitment-light vehicle access, mirroring trends in streaming media and gym memberships. Millennials, facing urban parking constraints, prefer monthly mobility passes over ownership, turning to long-term rentals during work-from-anywhere stints.

Corporate demand fuels the segment as firms outsource fleet management to avoid residual-value risk. Enterprise Mobility’s Flex-E-Rent platform grew double digits in 2024, tapping small-business appetite for on-demand vans. Telematics enable usage-based billing, aligning cost with employee mileage. Long-term contracts also mitigate seasonality, redeploying idle assets from leisure-heavy Mediterranean stations to urban hubs during winter. Cross-selling insurance and maintenance bundles lifts average contract value. The segment’s momentum reinforces the strategic imperative for Europe tourism vehicle rental market participants to integrate subscription architecture within core systems.

By Vehicle Type: Electric Vehicles Lead Growth Despite Operational Challenges

Economy and compact models retained 36.22% share in 2025 owing to cost-efficient fleet economics, but electric and hybrid vehicles are forecast to record the fastest 16.34% CAGR. Government decarbonisation targets and low-emission zone expansion compel operators to electrify. SIXT’s in-app charging integration grants renters access to 500,000+ European charge points, addressing range anxiety. The Europe tourism vehicle rental market size for EVs is projected to triple by 2030 as battery costs fall and charging networks densify. Nonetheless, Hertz’s 2024 liquidation of 20,000 EVs underscores the residual-value and maintenance risks tied to high-utilisation environments.

SUVs and crossovers continue to attract families seeking cargo space, while luxury vehicles carve out experience-driven niches such as vineyard tours. Operators use tiered fleet structures to hedge demand volatility: high-utilisation economy units drive volume, premium EVs burnish brand image, and specialty off-roaders diversify yield. Telematics data informs future model mixes by correlating utilisation with customer-rating metrics. As charging infrastructure in rural regions lags, dual-fuel fleets persist, yet investment in mobile rapid chargers signals operator intent to accelerate the transition. Altogether, vehicle-mix optimisation remains a competitive fulcrum within the Europe tourism vehicle rental market.

Geography Analysis

Germany maintained 31.74% of 2025 revenue, benefitting from its central location, strong highway system, and a deeply ingrained corporate-travel culture. The country’s convention calendar and automotive exhibitions secure year-round demand, balancing seasonal leisure peaks. Car-hire stations cluster around Frankfurt, Munich, and Berlin airports, ensuring high fleet rotation rates. However, market maturity and assertive domestic competitors temper forward-growth prospects, yielding a solid yet moderating trajectory compared with peripheral markets.

The United Kingdom is set to post a vigorous 16.18% CAGR to 2031, regaining momentum following Brexit-related uncertainty. Island geography necessitates vehicle rentals for inbound tourists lacking personal cars, while congestion charges in London and other cities propel demand for short-duration hires on the city outskirts. Enterprise Mobility operates more than 480 branches nationwide, underscoring network scale. The UK government’s decision to defer EV duty surcharges on fleets until 2028 further sweetens the operating landscape, spurring accelerated electrification adoption.

Southern Europe—France, Italy, and Spain—leverages Mediterranean allure and favourable climate to anchor summer demand spikes. France saw double-digit rental revenue growth in 2024 as Parisian and Côte d’Azur attractions reclaimed pre-pandemic visitor volumes. Italy’s tax credit on tourism-related CAPEX enables operators to modernise branches and electrify fleets, while Spanish regional airports report record incoming charter flights. Rest-of-Europe markets, including Poland, Greece, and Portugal, displayed mixed performance: geopolitical tension slowed CEE recovery, whereas Portugal benefited from a surge in North American tourists. Overall, geographic spread offers portfolio insulation for Europe tourism vehicle rental market leaders.

Competitive Landscape

The Europe tourism vehicle rental market exhibits moderate consolidation, with the three largest global brands—Enterprise Mobility, Avis Budget Group, and Hertz—anchoring supply across major gateways. Enterprise Mobility, crediting European operations for outsized growth. Fleet scale allows bulk procurement discounts and multi-airport network coverage, forming high entry barriers. Regional champions such as Europcar and SIXT protect domestic strongholds through loyalty programmes and premium service tiers.

Technology is the primary battleground for differentiation. SIXT’s API-rich application layers loyalty, mobile check-in, and EV-charging payments, reducing friction across the customer journey. Avis deployed machine-learning algorithms that fine-tune rate fences in sub-5-minute increments, maximising asset yield. Meanwhile, Free2move and Virtuo Technologies blur category lines by combining car-sharing and short-term rental in a single interface, appealing to younger, app-centric audiences. Their asset-light models rely on predictive demand pools rather than expansive branch footprints, pressuring incumbents to streamline legacy overhead.

Strategic alliances expand reach: SIXT’s Stellantis order secures priority vehicle allocation, while Avis partners with IONITY to guarantee fast-charger access along trans-European routes. Cross-industry convergence accelerates, as evidenced by Lyft’s USD 197 million acquisition of FREENOW in April 2025, which imported EUR 1 billion in annualised gross bookings into its multi-modal network.[3]“Lyft to acquire FREENOW,” Lyft Inc., investor.lyft.com. Competitive intensity remains balanced by high capital requirements and the complexity of pan-European regulatory compliance, yet digital disruptors continue to chip away at commoditised pricing segments.

Europe Tourism Vehicle Rental Industry Leaders

Sixt SE

Avis Budget Group, Inc

Hertz Corporation

Enterprise Holdings Inc.

Auto Europe

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Free2move partnered with Ample to introduce modular battery-swapping for Fiat 500e units in Madrid, cutting recharge pauses below five minutes and scaling fleet from 40 to 100 vehicles.

- April 2025: Lyft acquired European mobility app FREENOW for around USD 197 million, broadening coverage to 11 countries and adding EUR 1 billion in annualised gross bookings.

- June 2024: Europcar entered the United States with airport locations in Atlanta and Dallas/Fort Worth, marking its first operational footprint beyond Europe.

Europe Tourism Vehicle Rental Market Report Scope

A tourist vehicle is a self-propelled vehicle capable of being used for the temporary living, sleeping, or eating accommodation of persons. Tourism vehicle rental services, in general, means rental agencies primarily serving people who require a temporary vehicle.

The Europe tourism vehicle rental market is segmented by application type (leisure/tourism and business), booking type (online and offline), rental duration type (short-term rental and long-term rental), and geography (United Kingdom, Germany, Italy, France, Sapin, and Rest of Europe).

The report offers market size and forecasts for the European tourism vehicle rental market in value (USD) for all the above segments.

By Application

| Leisure / Tourism |

| Business |

By Booking Channel

| Online |

| Offline |

By Rental Duration

| Short-term |

| Long-term |

By Vehicle Type

| Economy/Compact |

| SUV and Crossover |

| Luxury and Premium |

| Electric and Hybrid |

By Country

| United Kingdom |

| Germany |

| Italy |

| France |

| Spain |

| Rest of Europe |

| By Application | Leisure / Tourism |

| Business | |

| By Booking Channel | Online |

| Offline | |

| By Rental Duration | Short-term |

| Long-term | |

| By Vehicle Type | Economy/Compact |

| SUV and Crossover | |

| Luxury and Premium | |

| Electric and Hybrid | |

| By Country | United Kingdom |

| Germany | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe tourism vehicle rental market?

The sector is worth USD 200.77 billion in 2026 and is projected to more than double by 2031.

Which country holds the largest share in the Europe tourism vehicle rental market?

Germany leads with 31.74% of 2025 revenue due to its central location and strong corporate travel base.

How fast is the United Kingdom segment growing?

The UK is forecast to register a 16.18% CAGR from 2026-2031, the highest rate among major European markets.

Which booking channel is expanding the quickest?

Online platforms are projected to grow at 16.05% CAGR, driven by mobile app adoption and dynamic pricing.

Why are electric vehicles important for rental companies?

Government subsidies and low-emission regulations are nudging fleets toward electrification, with electric and hybrid rentals expected to grow at 16.34% CAGR through 2031.

What is the biggest restraint facing the market?

Ultra-low-cost public-transport policies in parts of Central and Eastern Europe reduce rental uptake, curbing overall market growth.

Page last updated on: