GCC Construction Machinery Rental Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

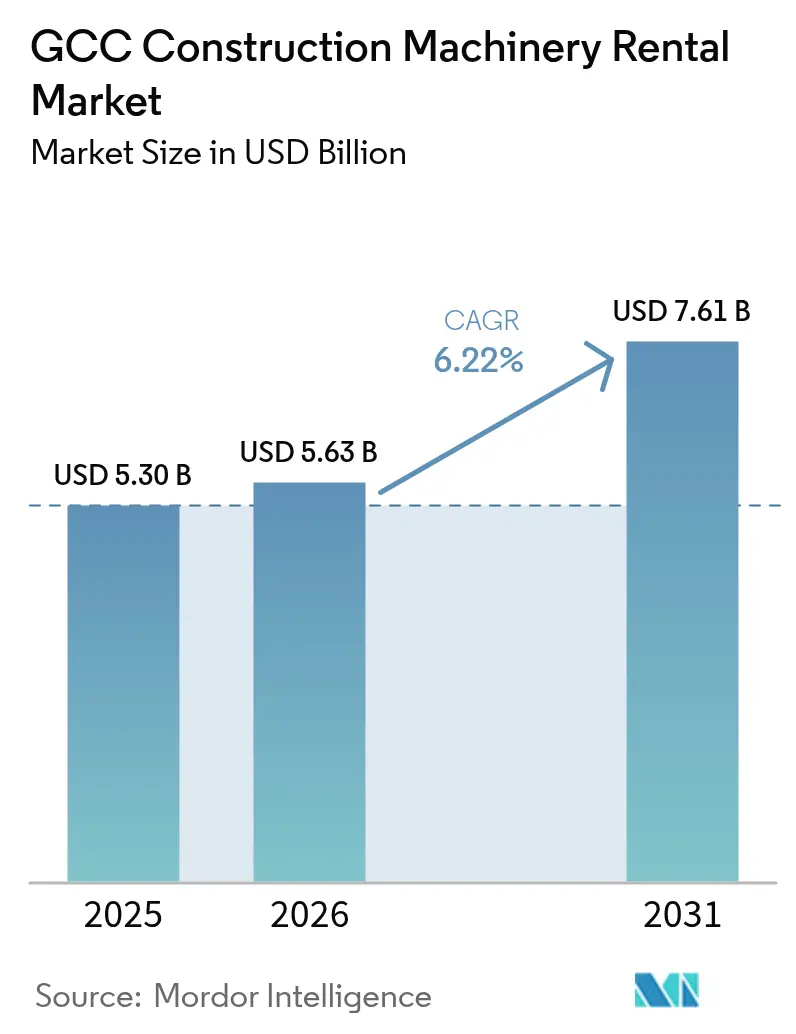

| Base Year Market Size (2025) | USD 5.30 Billion |

| Market Size (2026) | USD 5.63 Billion |

| Market Size (2031) | USD 7.61 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

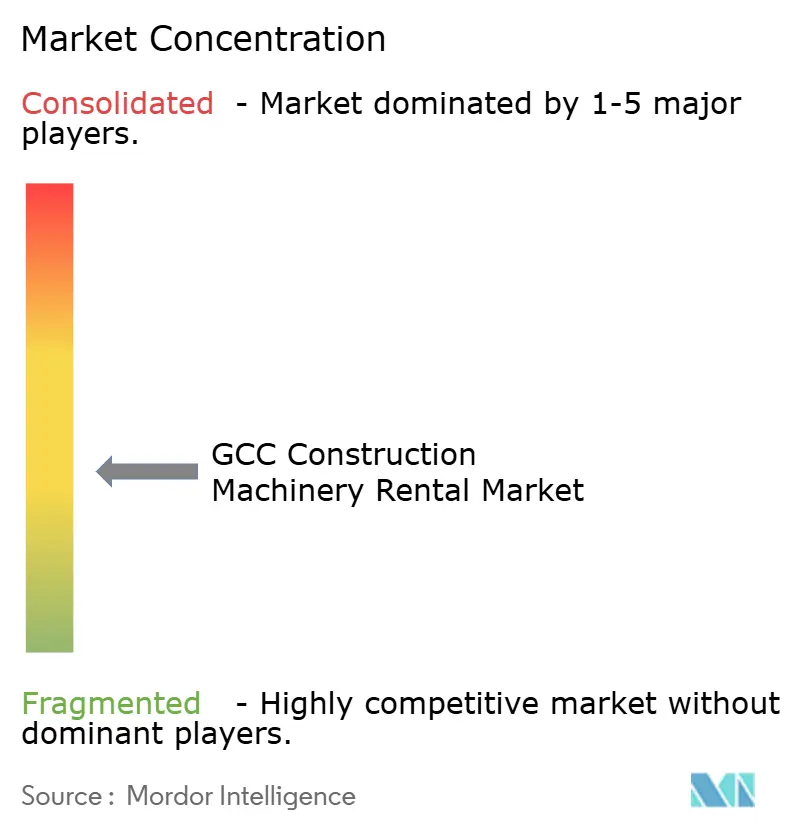

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Construction Machinery Rental Market Analysis by Mordor Intelligence

The GCC construction machinery rental market size was valued at USD 5.30 billion in 2025 and estimated to grow from USD 5.63 billion in 2026 to reach USD 7.61 billion by 2031, at a CAGR of 6.22% during the forecast period (2026-2031). This growth reflects contractors’ pivot toward asset-light models as Vision-led megaprojects compress procurement cycles, while tightening margins elevate the appeal of pay-per-use equipment access. Digital fleet optimization now underpins guaranteed uptime commitments, and mandatory Tier-4-Final / EU Stage V import rules accelerate fleet refreshes toward lower-emission assets. Saudi Arabia’s NEOM, UAE’s data-center boom, and Qatar’s LNG expansion anchor multi-year demand, while harsh desert conditions heighten the value of professionally maintained rental fleets. Moving forward, stricter green procurement criteria and COP28-aligned incentives position hybrid and fully electric equipment as the next performance frontier of the GCC construction machinery rental market.

Key Report Takeaways

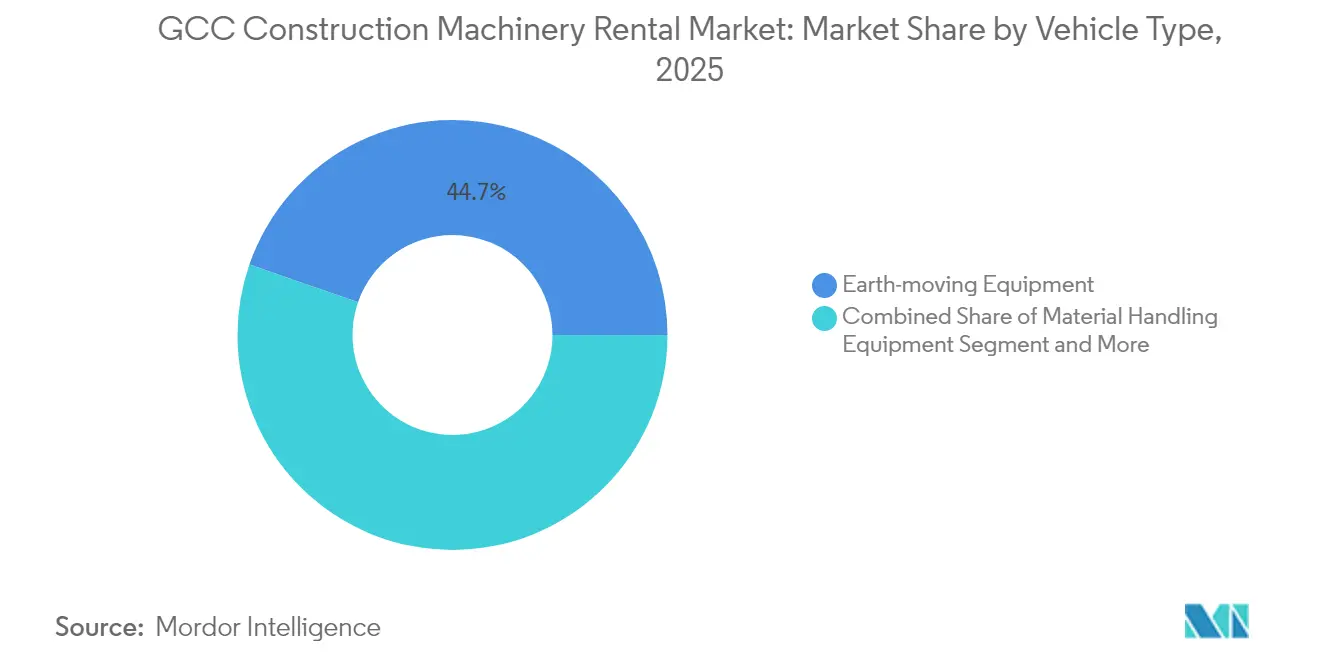

- By vehicle type, earth-moving equipment represented 44.68% of the GCC construction machinery rental market size in 2025; concrete and hoisting equipment is advancing at a 6.88% CAGR through 2031.

- By propulsion type, IC-engine machines held 87.65% of the GCC construction machinery rental market size in 2025, whereas full-electric and battery-powered units are growing at a 10.18% CAGR.

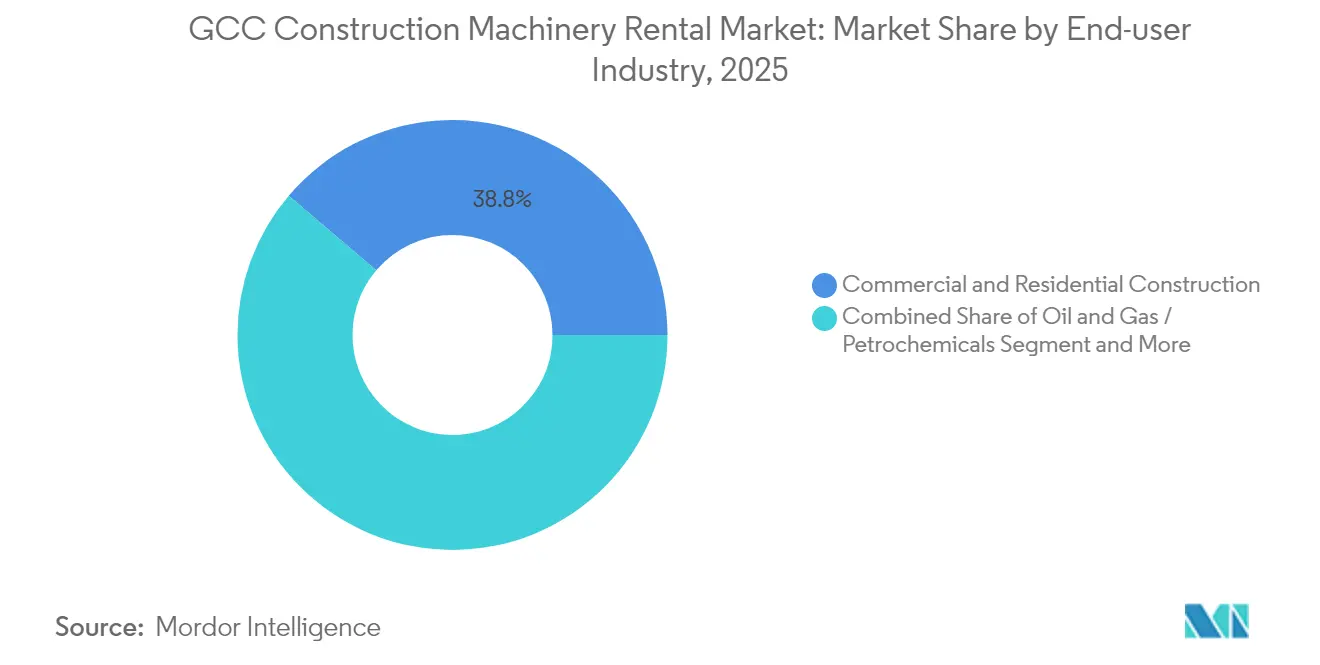

- By end-user industry, commercial and residential construction captured 38.78% of the GCC construction machinery rental market size in 2025; power and renewables is anticipated to expand at a 6.76% CAGR between 2026-2031.

- By country, Saudi Arabia commanded 54.52% of the GCC construction machinery rental market share in 2025; Qatar is projected to record the fastest 7.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Construction Machinery Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Boom Under GCC Vision | +1.8% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Data-Center and Renewable-Energy Build-Outs | +1.2% | UAE, Saudi Arabia, Oman | Medium term (2-4 years) |

| Shift to OPEX-Light Models | +0.9% | GCC | Short term (≤ 2 years) |

| Mandatory Tier-4-Final / EU Stage V Standards | +0.7% | UAE, Saudi Arabia | Medium term (2-4 years) |

| Digital Fleet-Management and Telematics | +0.5% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| COP28-Linked Green Procurement Incentives | +0.4% | GCC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Boom Under GCC Vision Programs

Megaprojects such as NEOM, the Red Sea Global tourism corridors, and Dubai 2040 drive unprecedented equipment demand, compressing traditional purchase cycles into rental-first decisions. Saudi Arabia’s Public Investment Fund into NEOM, while a new Wolffkran–Zamil joint venture is building a 150-unit-per-year tower-crane plant to serve regional projects [1]“Middle East Tower Crane Factory Announced,” Wolffkran, WOLFFKRAN.COM. UAE real-estate transactions growth in 2024, reinforcing steady vertical construction pipelines that rely on readily available cranes and concrete pumps. Qatar’s Third National Development Strategy outlines investment in PPP schemes through 2030, further stretching contractor capital. Long project lists across Oman’s Duqm SEZ and Bahrain’s metro program underscore how Vision agendas escalate the need for flexible fleets. Consequently, the GCC construction machinery rental market gains a structural boost from megaproject scheduling volatility and capex discipline requirements.

Rapid Growth Of Data-Center And Renewable-Energy Build-Outs

Hyperscale data-center clusters in Dubai South and Saudi Arabia’s King Salman Energy Park require precision foundation work, heavy lifts for prefabricated modules, and continuous onsite power generation. Concurrently, utility-scale photovoltaic plants such as UAE’s 2 GW Al Dhafra project and Oman’s green-hydrogen concessions demand specialty piling rigs, tracked cranes, and high-capacity telehandlers over multi-year periods [2]“Clean-Energy Capacity Targets,” Mubadala, MUBADALA.COM . Rental providers tailor equipment packages with thermal-stress kits and dust-protection features suited to desert conditions, lowering upfront costs for developers. As renewables accelerate toward the region’s clean-power target by 2050, specialist rental fleets become indispensable for meeting tight commissioning deadlines.

Contractor Shift To OPEX-Light Models Amid Tightening Project Margins

Public-sector payment cycles in Saudi Arabia and sporadic variation-order approvals tighten working capital, steering contractors away from outright purchases. Elevated interest rates and Basel III lending limits raise the hurdle rate on equipment ownership, prompting firms such as ALEC Engineering to prioritize liquidity preservation. Renting shifts depreciation, maintenance, and resale risk to fleet owners, while guaranteed uptime clauses safeguard project schedules. The monetization of telematics data—ranging from idle-time reporting to productivity dashboards—supports performance-based billing structures that align equipment costs with project cash inflows, reinforcing rental appeal.

Mandatory Tier-4-Final / EU Stage V Import Standards (UAE And KSA)

From 2024, customs authorities in Dubai require diesel machines to carry certified after-treatment systems, driving replacement of Tier 3 fleets ill-suited to particulate-matter thresholds [3]“Tier 4 Final Solutions,” Caterpillar, CATERPILLAR.COM. Compliance upgrades raise purchase costs, whereas rental providers amortize the premium over large fleets and embed operator-training packages that prevent costly mismanagement of DPF regeneration. Consequently, contractors adopt rental to secure compliant assets without a balance-sheet hit, and regional distributors accelerate trade-in programs feeding secondary markets in Africa.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Price Competition From Chinese Lessors | −1.1% | GCC | Short term (≤ 2 years) |

| Project Delays in Public Megaprojects | −0.8% | Saudi Arabia, Qatar, Kuwait | Medium term (2-4 years) |

| Scarcity of Certified Operators | −0.6% | GCC | Long term (≥ 4 years) |

| Climatic Stress Accelerates Depreciation | −0.4% | GCC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Price Competition From Chinese OEM-Affiliated Lessors

Shandong-based crane makers bundle zero-interest financing with rental offers, undercutting regional incumbents while accelerating regional parts-storage hubs in Dammam and Jebel Ali. Their integrated model leverages scale procurement from domestic factories, squeezing margins for operators reliant on European-sourced fleets. Although stringent Saudi localization rules favor established players, price-sensitive second-tier contractors gravitate toward Chinese alternatives, prompting incumbents to emphasize telematics-backed uptime guarantees and value-added training.

Project Delays And Payment Backlogs In Public-Sector Megaprojects

Riyadh Metro extension revisions and Kuwait’s airport terminal renegotiations push completion schedules beyond contractual horizons, leaving equipment idle on partially mobilized sites. Rental firms must extend credit while absorbing fleet under-utilization, eroding returns. Qatar’s post-World-Cup project reprioritization similarly defers capital-intensive phases, creating gaps in demand across hoisting categories. Effective receivables management and diversified deployment across multiple countries emerge as defensive tactics but carry added logistics complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Earth-Moving Leads Infrastructure Surge

Earth-moving assets captured 44.68% of the GCC construction machinery rental market size in 2025 on the back of expansive earthworks for NEOM corridors, UAE freight rail extensions, and Qatar’s gas-processing platforms. Digital blade-control on dozers and 3D-GPS guided graders underpin higher productivity against tight project timelines, reinforcing rental adoption as contractors seek the latest firmware without ownership risk. Material-handling cranes gain momentum in Oman’s Duqm port expansion, while concrete pumps and placing booms post a 6.88% CAGR as high-rise clusters multiply along Riyadh Boulevard and Dubai Creek.

Rental firms integrate OEM telematics into dashboards that allocate equipment across multiple sites, improving utilization and supporting dynamic pricing models. The GCC construction machinery rental market benefits from bundled service packages that include certified operators, maintenance call-outs within four hours, and on-site parts storage. Contractors increasingly benchmark total project cost per cubic meter moved rather than hourly equipment rates, anchoring the shift toward rental contracts that embed performance metrics.

By Propulsion Type: Electric Transition Accelerates

IC-engine machines retained 87.65% dominance in 2025, yet electric skid steers, mini-excavators, and rough-terrain forklifts register a 10.18% CAGR as municipalities impose emissions and noise caps around residential zones. Rental companies deploy mobile charging trailers powered by hybrid gensets, ensuring flexible job-site power while mitigating range anxiety. The GCC construction machinery rental market share of battery-electric models is set to grow by 2030 as battery energy density surpasses 300 Wh/kg, enabling eight-hour duty cycles in 30-ton excavators.

Hybrid-drive variants emerge as transitional solutions, especially for telehandlers and knuckle-boom lifts operating across dispersed logistics parks. Predictive analytics compare fuel burn between hybrid and diesel variants, guiding contractors toward optimal sustainability-cost trade-offs. Leasing terms incorporate carbon-reduction targets, with rental rates declining once verified telemetry demonstrates emissions savings against baseline Tier 3 fleets.

By End-User Industry: Renewable Power Spurs Specialized Demand

Commercial and residential building stayed the largest renter at 38.78% share in 2025, backed by Dubai’s significant real-estate transactions and Saudi giga-projects that include over several new hotel keys. Nonetheless, power and renewables is the fastest-rising segment at 6.76% CAGR as the region adds 15 GW of solar capacity and accelerates green-hydrogen pilots.

Pipeline infrastructure for North Field LNG, Oman’s Duqm refinery, and UAE’s ADNOC ammonia export terminals rely on specialized pipe-layers, vacuum-lift trailers, and modular transporter systems typically available only through rental pools. The GCC construction machinery rental industry therefore tailors fleet mix to sector-specific cycles, balancing housing booms with the multi-year cadence of power-plant builds.

Geography Analysis

Saudi Arabia anchors the GCC construction machinery rental market with a 54.52% share in 2025, buoyed by significant project pipeline spanning NEOM, Qiddiya, and The Line districts. The kingdom’s localization mandate, which requires minimum 25% Saudi-built components on government contracts, favors rental firms with domestic assembly partners, exemplified by the Wolffkran-Zamil tower-crane plant targeting 150 units per year.

The United Arab Emirates holds a significant position, leveraging its role as a regional commerce hub, with real-estate deals and robust logistics infrastructure that supports rapid cross-emirate equipment redeployment. UAE’s Net Zero charter incentivizes adoption of battery-electric compact machinery through fast-track environmental approvals, propelling the nation’s share of hybrid-ready fleets. Qatar represents the fastest-growing market at a 7.44% CAGR to 2031, tied to several planned projects and the North Field Production Sustainability Phase 2 that extends LNG dominance. Oman, Kuwait, and Bahrain together contribute a steady share of regional revenue, with Oman’s Duqm SEZ alone drawing investment in transport and petrochemical works, necessitating long-reach excavators and heavy haulage rigs. Policy-driven monetary easing since late 2024 lowers borrowing costs, indirectly supporting construction starts and rental penetration across all six GCC states.

Competitive Landscape

The GCC construction machinery rental market exhibits moderate fragmentation. Regional champions such as Al Faris Group leverage crane specialization and vertically integrated heavy-haul logistics, while Wolffkran Arabia focuses on tower-crane turnkey services for high-rise contractors. Chinese OEM-affiliated lessors—Zoomlion, XCMG Leasing—enter via joint-venture depots in Dammam and Dubai, offering bundled finance that compresses daily rates.

Digital differentiation defines the next competitive battleground. Al Faris introduced a telematics-backed “95% Uptime Assurance” program in 2025 that offsets liquidated damages for late equipment replacement, exploiting 4G/5G connectivity across NEOM clusters. Wolffkran Arabia equipped its luffing-jib fleet with anti-collision technology integrated into BIM models, reducing tower-crane downtime on Riyadh’s King Salman Park. Chinese entrants counter with AI-based load-moment indicators and multi-year warranties, banking on shorter payback periods due to lower acquisition costs.

Electric-equipment capability emerges as a strategic moat. Regional distributors of Volvo and JCB partner with rental firms to establish rapid-charging hubs at Dubai Logistics City and Riyadh Industrial Valley. Operators able to guarantee emissions-compliant fleets win preferred-supplier status on public tenders, while smaller independents confront capex hurdles tied to electric machines and charger procurement. Intensifying data-center developments further tilt the scale toward players offering combined rental and power-generation solutions.

GCC Construction Machinery Rental Industry Leaders

Al Faris Group

Bin Quraya

Byrne Equipment Rental LLC

Zahid Tractor & Heavy Machinery Co.

Johnson Arabia LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: AJI Rentals, the heavy-equipment rental division of ALEC Group, launched operations in Saudi Arabia, signaling aggressive regional expansion.

- January 2024: WOLFFKRAN for Equipment established a Riyadh-based venture to deliver end-to-end rental and service offerings across the kingdom.

- July 2022: The Red Sea Development Company (TRSDC), the Saudi developer behind the world's most ambitious regenerative tourism project, is teaming up with Dayim Equipment Rental, the region's full-service plant, machinery and vehicle provider.

GCC Construction Machinery Rental Market Report Scope

Construction equipment rental means a site for the retrieval and storage of large vehicles or large pieces of machinery usually related to construction available for the public’s use, which may include complementary and additional retail activities.

The GCC Construction Equipment/Machinery Rental Market is segmented by vehicle type, propulsion type, and country.

By vehicle type, the market is segmented into earthmoving equipment and material handling. By propulsion type, the market is segmented into IC engines and hybrid drives. By country, the market is segmented into Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates.

The report offers the size and forecast for the GCC Construction Equipment/Machinery Rental Market in value USD for all the above segments.

| Earth-moving Equipment |

| Material Handling Equipment |

| Road-building and Compaction Equipment |

| Concrete and Hoisting Equipment |

| Power and Utility Generators |

| IC Engine |

| Hybrid Drive |

| Full Electric / Battery-Powered |

| Commercial and Residential Construction |

| Oil and Gas / Petrochemicals |

| Infrastructure and Transport (roads, metros, ports, airports) |

| Power and Renewables |

| Industrial and Manufacturing |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Vehicle Type | Earth-moving Equipment |

| Material Handling Equipment | |

| Road-building and Compaction Equipment | |

| Concrete and Hoisting Equipment | |

| Power and Utility Generators | |

| By Propulsion Type | IC Engine |

| Hybrid Drive | |

| Full Electric / Battery-Powered | |

| By End-user Industry | Commercial and Residential Construction |

| Oil and Gas / Petrochemicals | |

| Infrastructure and Transport (roads, metros, ports, airports) | |

| Power and Renewables | |

| Industrial and Manufacturing | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

How large is the GCC construction machinery rental market in 2026?

The market is valued at USD 5.63 billion in 2026, with a forecast to reach USD 7.61 billion by 2031.

Which country leads demand for rented construction machinery across the GCC?

Saudi Arabia accounts for 54.52% of regional revenue, driven by its USD 680 billion project pipeline.

Which equipment type holds the largest rental share today?

Earth-moving machinery leads with 44.68% share due to extensive grading, excavation, and site preparation works.

What CAGR is expected for the overall market through 2031?

The GCC construction machinery rental market is projected to grow at a 6.22% CAGR over 2026-2031.

Page last updated on: