Europe Automotive Financing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

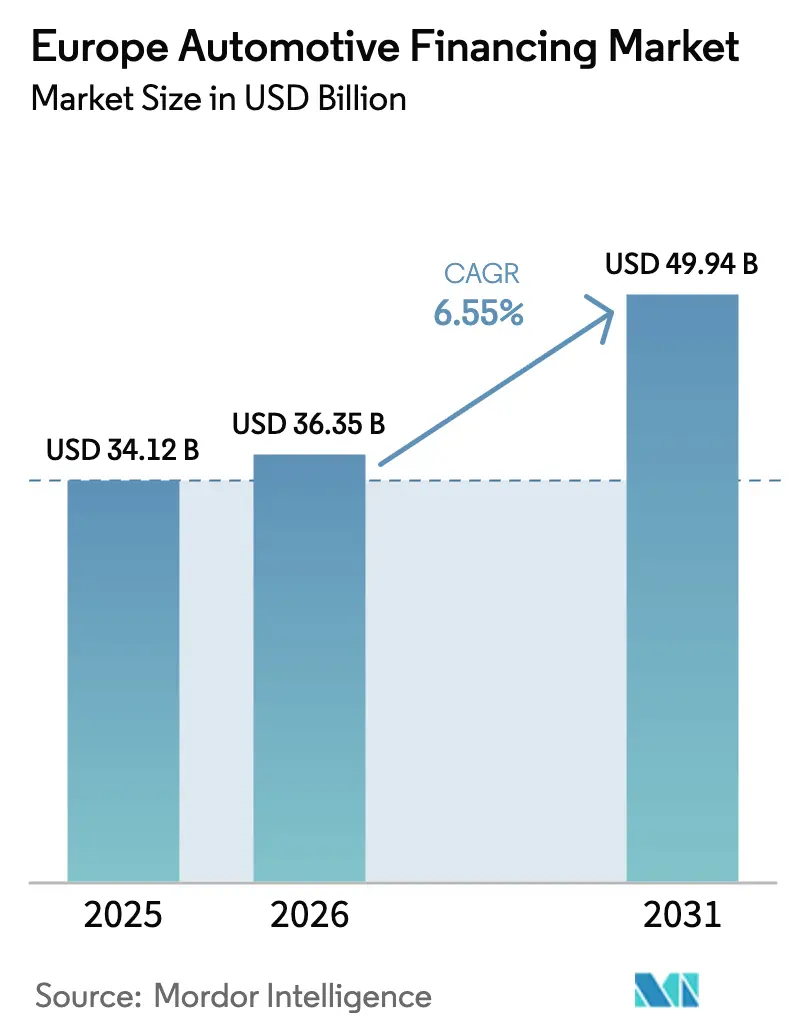

| Base Year Market Size (2025) | USD 34.12 Billion |

| Market Size (2026) | USD 36.35 Billion |

| Market Size (2031) | USD 49.94 Billion |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Financing Market Analysis by Mordor Intelligence

The European automotive financing market size was valued at USD 34.12 billion in 2025 and estimated to grow from USD 36.35 billion in 2026 to reach USD 49.94 billion by 2031, at a CAGR of 6.55% during the forecast period (2026-2031). Digital lending platforms, subscription-based ownership models, and targeted electric-vehicle incentives form the structural pillars that accelerate demand. OEM captive finance arms strengthen customer retention with telematics-driven risk pricing, while green-bond issuances trim funding costs and expand lenders’ balance-sheet capacity. Rapid adoption of salary-sacrifice EV schemes in the United Kingdom and residual-value guarantees in Germany reinforce market confidence. Simultaneously, used-car financing volumes are climbing as consumers prioritize value and sustainability in an inflationary environment[1]European Central Bank, “Statistical Data Warehouse: Interest Rate Series,” ecb.europa.eu.

Key Report Takeaways

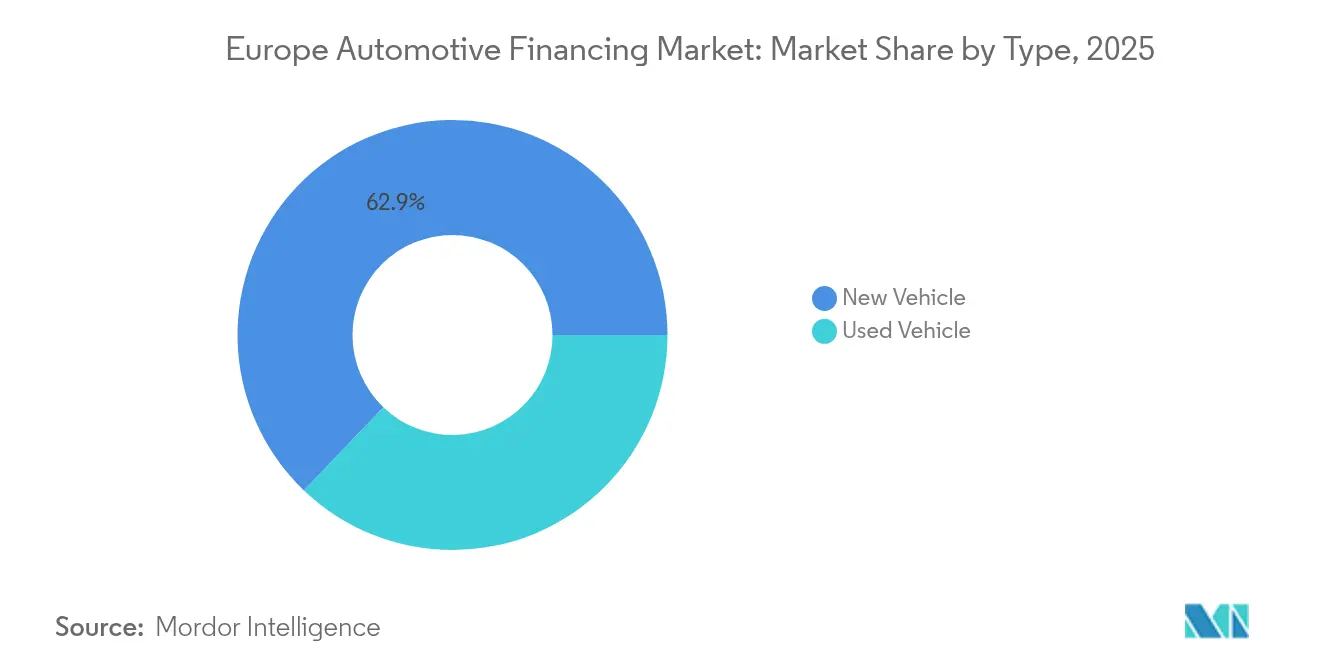

- By type, new vehicle financing retained 62.86% of the European automotive financing market share in 2025, whereas used vehicle financing is expected to advance at a 7.05% CAGR through 2031.

- By source type, OEM captive finance arms experienced the highest growth, expanding at an 7.82% CAGR, while traditional banks controlled 44.70% of the European automotive financing market size in 2025.

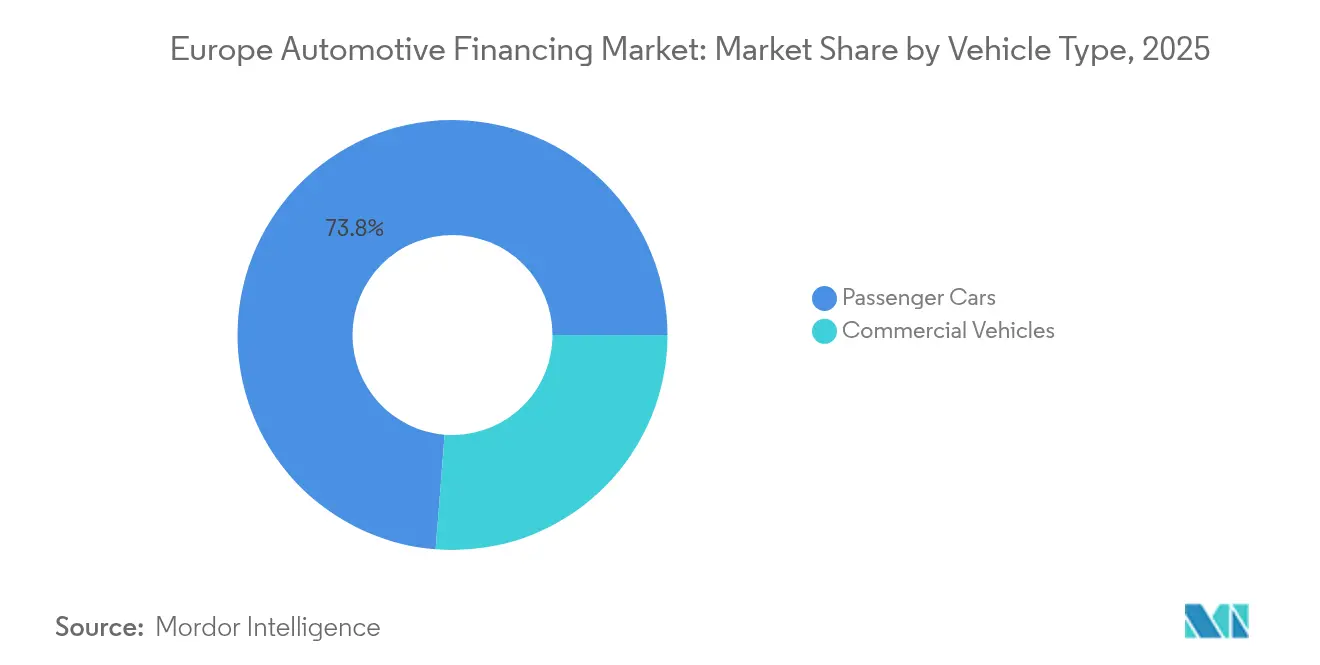

- By vehicle type, commercial vehicle financing accounted for 26.25% of the European automotive financing market size in 2025 and is projected to grow at the fastest rate, with a 7.02% CAGR, through 2031.

- By financing product, subscription models represented 3.26% of the European automotive financing market share in 2025, yet they are projected to post the highest 7.95% CAGR forecast to 2031.

- By country, the United Kingdom posted the fastest regional expansion at a 7.21% CAGR, while Germany held a 31.55% share of the European automotive financing market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Automotive Financing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Leasing and Subscription Shift | +1.2% | Germany, United Kingdom | Medium term (2-4 years) |

| OEM Digital Finance | +1.1% | Germany, France, United Kingdom | Medium term (2-4 years) |

| EV Leasing Subsidies | +0.9% | Nordic states, Germany | Long term (≥ 4 years) |

| Used-Car Finance Surge | +0.8% | Western Europe | Short term (≤ 2 years) |

| Salary-Sacrifice EV Plans | +0.7% | United Kingdom, Belgium, Netherlands | Medium term (2-4 years) |

| Green-Bond Cost Edge | +0.6% | EU-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Leasing and Subscription Models

Urban drivers are increasingly turning to car-subscription services, valuing flexibility and convenience over the traditional model of vehicle ownership. These services, often bundled with maintenance and flexible contract terms, cater to consumers desiring a seamless mobility experience. The growing consumer interest in subscription models suggests a promising future for products centered on recurring revenue. Automotive lenders, closely tied to manufacturers, are capitalizing on these shorter ownership cycles. They're not only managing financial risks more adeptly but also harnessing the wealth of data from connected vehicles. This data paves the way for tailored marketing strategies and enhanced service offerings. Countries such as Germany and the UK are piloting multi-brand subscription initiatives, particularly for new energy vehicles, offering month-to-month access that aligns with shifting consumer demands. While stringent data privacy regulations, such as GDPR, dictate the handling of customer information, they also establish clear standards for data sharing. This clarity is pivotal for developing pricing models that reflect actual vehicle usage.

OEM Captive Finance Digital Penetration

Captive lenders are now processing a significant portion of credit applications online—outpacing many universal banks. A leading example highlights that adopting a cloud-based decision engine has significantly accelerated underwriting cycles, resulting in quicker approvals and faster vehicle deliveries. In vehicle configurator portals, buyers can view real-time finance offers for each trim and option, enabling them to secure funding right at checkout. Integrated telematics enhances underwriting by providing driving-behavior insights that inform proprietary risk models, resulting in greater accuracy than traditional bureau-only scoring. Collectively, these advancements bolster the competitive advantage of captive finance arms, which merge digital origination, immediate pricing, and data-centric risk evaluation, setting them up for continued growth in the years ahead.

EV-Linked Leasing Subsidies by Governments

National incentive programs lower lease rates and accelerate the adoption of electric vehicles. Germany’s Umweltbonus reimburses up to EUR 6,000 (USD 6,950) per lease on qualifying zero-emission cars, materially reducing monthly payments. The Netherlands offers a tax rebate that exempts cars with a CO₂ fleet of 8 g/km or lower from registration levies, making leases structurally cheaper than loans. Because subsidies are disbursed to lessors rather than buyers, they reinforce leasing over traditional hire-purchase contracts. Nordic fleets feel the tailwind most, as dense public-charging grids align with subsidy frameworks that extend beyond 2028 [2]German Federal Office for Economic Affairs and Export Control, “Environmental Bonus 2024,” bafa.de.

Rapid Growth in Used-Car Financing

Macroeconomic uncertainty and longer vehicle lifespans prompt budget-conscious households to opt for certified pre-owned cars. The 7.41% CAGR logged for used-car loans outpaces all other product lines in the European automotive financing market. Blockchain-anchored vehicle history ledgers speed up underwriting, cutting fraud losses and trimming loan approval times. AI-driven damage-detection apps enable lenders to scan hundreds of images per vehicle, building more accurate residual-value curves. These technological gains enable banks to expand their loan books without incurring proportional staffing costs, while sustainability-linked criteria increase the appeal of late-model hybrid vehicles. Western Europe remains the epicenter, where regulatory inspection regimes support secondary-market transparency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Interest Rates | –0.9% | EU-wide | Short term (≤ 2 years) |

| BEV Residual Value Drop | –0.7% | Germany, United Kingdom, Netherlands | Medium term (2-4 years) |

| EU Withdrawal Tightening | –0.4% | EU-wide | Long term (≥ 4 years) |

| Debt-to-Income Caps | –0.3% | France, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Interest Rates Elevate Payments

Auto-loan interest rates have surged since the European Central Bank tightened its monetary policy. This uptick has resulted in heftier monthly payments for borrowers, prompting many to opt for extended loan durations, which in turn amplifies the total interest paid over the loan's lifespan. With financial certainty becoming paramount for consumers, there's a marked preference for fixed-rate contracts over their variable-rate counterparts. In light of this trend, lenders are proactively managing the risks associated with fixed-rate lending, frequently employing hedging strategies to protect their profit margins. While the ascent in rates has curtailed loan origination volumes, it has simultaneously bolstered profitability for well-capitalized banks by widening the gap between borrowing costs and lending rates. These shifts are particularly impactful in Southern Europe, where households already face elevated debt burdens, making them more sensitive to fluctuations in borrowing costs[3]European Central Bank, “Economic Bulletin Issue 5/2024,” ecb.europa.eu.

Declining BEV Residual Values

Rapid model turnover has pressured residual values for battery-electric vehicles, causing them to fall short of expectations and undermining price stability. In response, leasing companies have downgraded their value forecasts for popular compact models. This adjustment has resulted in higher lease payments upon contract renewals. Such downward revisions elevate the financial risk on balance sheets, straining capital adequacy metrics. Concurrently, insurers are witnessing a surge in total-loss claims, predominantly due to the steep costs associated with battery replacements. As a result, lenders are shifting towards more conservative loan-to-value ratios to reduce their exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Used-Car Loans Outpace New-Car Growth

Used-vehicle financing accounted for 37.14% of the European automotive financing market share in 2025 and is projected to expand at a 7.05% CAGR through 2031. Demand accelerates as the EU average vehicle age reaches 11.8 years, strengthening secondary-market liquidity. Certified pre-owned programs reduce information asymmetry, raising lender confidence. AI-scored inspection apps document exterior and mechanical condition, compressing approval time to under one hour for top-tier lenders.

In contrast, the new-car segment maintains 62.86% dominance, yet its growth trails at 5.55% CAGR. Sustainability metrics embedded in credit policy steer funds toward Euro 6-compliant used fleets, striking a balance between environmental compliance and affordability. Banks exploit higher margin spreads on used-car deals, while captives capture loyalty by financing their own off-lease vehicles. Consequently, used-car loans anchor portfolio yield even as macro headwinds persist across the European automotive financing market.

By Source Type: Captive Lenders Narrow the Gap

Banks held 44.70% of the European automotive financing market share in 2025, but captives are growing at an 7.82% CAGR and are on track to erode that lead. The disparity stems from embedded-data advantages that enable real-time credit scoring on the showroom floor.

Credit unions and fintech non-bank lenders complement the ecosystem by targeting underserved demographics with alternative scores, expanding financial inclusion. Captive arms fund over half of manufacturer incentives, creating blended offers that universal banks struggle to match. Regulatory capital benefits under the EU’s Simple, Transparent, and Standardised securitization rules further enhance captive funding efficiency, cementing their momentum in the European automotive financing market.

By Vehicle Type: Commercial Fleets Accelerate

Passenger-car loans claimed a 73.75% share in 2025; however, commercial-vehicle financing is the growth engine, forecasted to log a 7.02% CAGR through 2031. Electrified vans anchor last-mile delivery commitments signed by logistics majors.

Fleet managers are embracing battery leasing structures that separate residual risk, thereby moderating upfront capital requirements. Telematics-based predictive maintenance reduces downtime, making the total cost of ownership more transparent and predictable. As low-emission zones proliferate across European cities, commercial operators are upgrading to compliant vehicles, thereby sustaining a pipeline of asset-backed lending across the European automotive financing market.

By Financing Product: Subscriptions Gain Traction

Traditional fixed-rate loans still dominated, with a 67.95% share in 2025; however, subscription products displayed an 7.95% CAGR, the highest of any category. All-inclusive monthly pricing resonates with urban professionals who prefer to avoid multi-year commitments.

Lease contracts shorten to 24-month averages, mirroring digital-age expectations. Bundled insurance and service streamline budgeting, and lenders monetize ancillary services such as over-the-air software updates. This convergence positions subscription offerings as a durable growth pocket within the European automotive financing market.

Geography Analysis

In 2025, Germany secured a dominant 31.55% share, underscoring the nation's deep-rooted ties between its manufacturing and financial sectors. Captive lenders in Germany utilize residual-value guarantees, effectively curbing borrower risks and promoting wider adoption. Germany's preeminence is bolstered by a robust integration of OEMs and finance, advanced securitization avenues, and a proactive BaFin framework that facilitates instantaneous digital onboarding. With a high per capita income, there's a sustained demand for premium brand lending. Furthermore, the introduction of multi-brand leasing packages not only diversifies risk portfolios but also fortifies the overall financial stability.

The United Kingdom is on a growth trajectory, boasting the swiftest 7.21% CAGR, a trend projected to continue until 2031. This surge is driven mainly by the adoption of salary-sacrifice schemes for electric vehicles (EVs). The Financial Conduct Authority's regulatory sandboxes expedite fintech testing, positioning the U.K. as a nurturing ground for pioneering lending solutions in the European automotive finance arena. The U.K.'s ascent can be attributed to forward-thinking policies, notably tax-advantaged salary-sacrifice initiatives and exemptions from congestion charges for EVs. Collaborations with fintech entities are refining alternative scoring methods, broadening borrower access, even in the face of stringent macroprudential regulations.

France, Italy, and Spain present a tapestry of varied dynamics. France prioritizes balance-sheet health, imposing a 35% debt-to-income cap, while Italy's diverse banking landscape welcomes non-bank players, broadening product offerings but intensifying competition. Meanwhile, Spain reaps the rewards of domestic OEM investments, spurring demand for financing, especially in export-bound semi-autonomous driving fleets. These varied trends collectively bolster the depth and risk distribution of the European automotive financing landscape.

Competitive Landscape

The market exhibits moderate concentration, with top players leveraging their scale to absorb digital transformation spending and regulatory overhead. Volkswagen Financial Services, Santander Consumer Finance, and BNP Paribas Personal Finance maintain dominant loan books through cross-border platforms that optimize funding arbitrage.

Consolidation shapes the strategic backdrop. The ALD–LeasePlan merger, approved in 2024, created Ayvens, a fleet-leasing giant with 3.3 million vehicles under management. Such combinations unlock cost synergies in IT and procurement while broadening geographic reach.

Fintech challengers target niche segments such as subprime used-car lending or gig-economy van leasing, deploying API-first architectures that integrate price discovery and underwriting in under five minutes. Incumbents respond with venture investments and open-banking partnerships, ensuring that innovation diffuses broadly across the European automotive financing market.

Europe Automotive Financing Industry Leaders

Volkswagen Financial Services

Santander Consumer Finance, S.A.

BNP Paribas Personal Finance

CA Auto Bank

BMW AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: CA Auto Finance, the UK arm of CA Auto Bank, has secured an exclusive partnership with Geely Auto UK, a prominent automobile manufacturer, coinciding with the UK debut of the Geely EX5. This collaboration allows Geely to leverage CA Auto Finance's regional insights to bolster its brand introduction in the UK market. The partnership aims to provide tailored financial solutions to support Geely's entry and growth in the competitive UK automotive market, ensuring a seamless experience for customers and dealers alike.

- March 2025: Ayvens has secured a new financing deal with the EIB, aiming to expand its lineup of electric light commercial vehicles (eLCVs). This agreement, rooted in an EIB-supported climate initiative, empowers Ayvens to enhance its eLCV fleet throughout the European Union. The primary focus will be on key markets, including Germany, France, Italy, and the Netherlands, within the next three years.

- January 2024: Bumper, a fintech platform specializing in flexible payment solutions for car repairs, secured USD 48 million in its Series B funding round, spearheaded by Autotech Ventures. Bumper's unique offering provides drivers with interest-free payment options, easing the financial burden of sudden repair expenses.

Europe Automotive Financing Market Report Scope

Automotive financing, commonly referred to as car finance, encompasses a range of financial products that facilitate the purchase of vehicles, whether new or used, through methods other than a one-time, full-cash payment.

The Europe Automotive Financing Market Report is Segmented by Type (New Vehicle, and Used Vehicle), Source Type (OEM Captive Finance, Banks, Credit Unions, and Non-Bank Financial Institutions), Vehicle Type (Passenger Cars, and Commercial Vehicles), Financing Product (Loan, Lease, Balloon Payment, and Subscription), and Geography (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

The report provides market size and forecasts for automotive financing in terms of value (USD) for all the aforementioned segments.

| New Vehicle |

| Used Vehicle |

| OEM Captive Finance |

| Banks |

| Credit Unions |

| Non-Bank Financial Institutions |

| Passenger Cars |

| Commercial Vehicles |

| Loan |

| Lease |

| Balloon Payment |

| Subscription |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Type | New Vehicle |

| Used Vehicle | |

| By Source Type | OEM Captive Finance |

| Banks | |

| Credit Unions | |

| Non-Bank Financial Institutions | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Financing Product | Loan |

| Lease | |

| Balloon Payment | |

| Subscription | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the 2026 value of Europe automotive financing?

The Europe automotive financing market size equals USD 36.35 billion in 2026 with a 6.55% CAGR outlook to 2031.

Which country grows fastest in automotive financing through 2031?

The United Kingdom leads growth, advancing at a 7.21% CAGR as tax-advantaged EV programs stimulate loan and lease demand.

Why are subscription models gaining traction?

Bundled insurance, maintenance, and flexible terms attract urban consumers, making subscriptions the quickest-rising product at an 7.95% CAGR.

What risk does BEV residual-value decline pose?

Faster-than-expected depreciation forces lessors to hike lease factors and adopt conservative LTV caps to protect against end-of-term losses.

Page last updated on: