Europe Insect Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

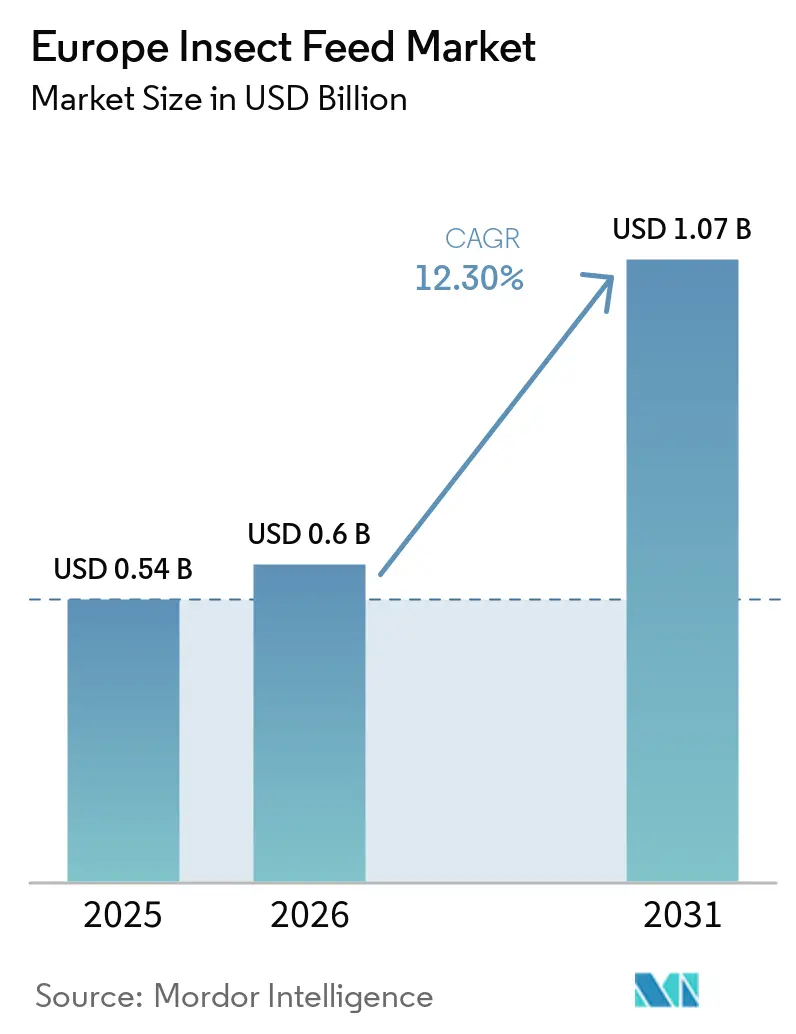

| Base Year Market Size (2025) | USD 0.54 Billion |

| Market Size (2026) | USD 0.6 Billion |

| Market Size (2031) | USD 1.07 Billion |

| Growth Rate (2026 - 2031) | 12.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Insect Feed Market Analysis by Mordor Intelligence

The Europe insect feed market was valued at USD 0.54 billion in 2025 and is projected to grow from USD 0.60 billion in 2026 to USD 1.07 billion by 2031, registering a CAGR of 12.3% during the forecast period (2026-2031). The market is transitioning from a niche alternative protein category to a more established component of the regional feed mix, driven by regulatory approvals, feed security concerns, and sustainability objectives. The European Union (EU) compound feed sector operates on a significant scale, with production reaching 274.1 million metric tons in 2025. Even small increases in the inclusion of insect ingredients create substantial opportunities for suppliers. Currently, insect ingredients account for less than 0.2% of total protein tonnage in European feed, highlighting the early stage of market penetration despite ongoing industrial expansion[1]Source: FEFAC, “Feed and Food 2024,” FEFAC, fefac.eu. This low base explains why producers are focusing on capacity building, refining operational models, and forming off-take partnerships, even as profitability challenges persist. Additionally, the market is benefiting from shifts in procurement practices, with feed buyers seeking ingredients that reduce reliance on imported proteins and support Scope 3 reporting goals across the value chain.

Key Report Takeaways

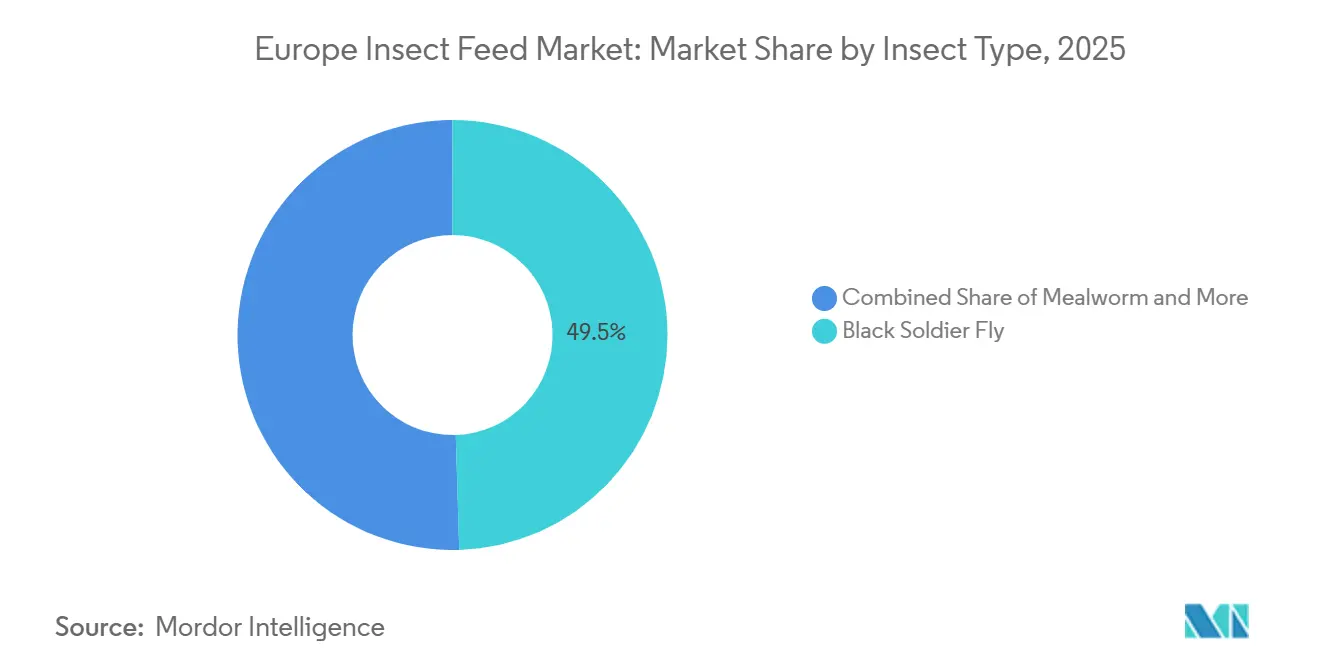

- By insect type, black soldier fly held 49.5% of the Europe insect feed market share in 2025, while mealworms are forecast to expand at a 13.6% CAGR through 2031.

- By product form, insect meal accounted for 58.0% of the Europe insect feed market size in 2025, while insect oil recorded the highest projected CAGR at 14.4% through 2031.

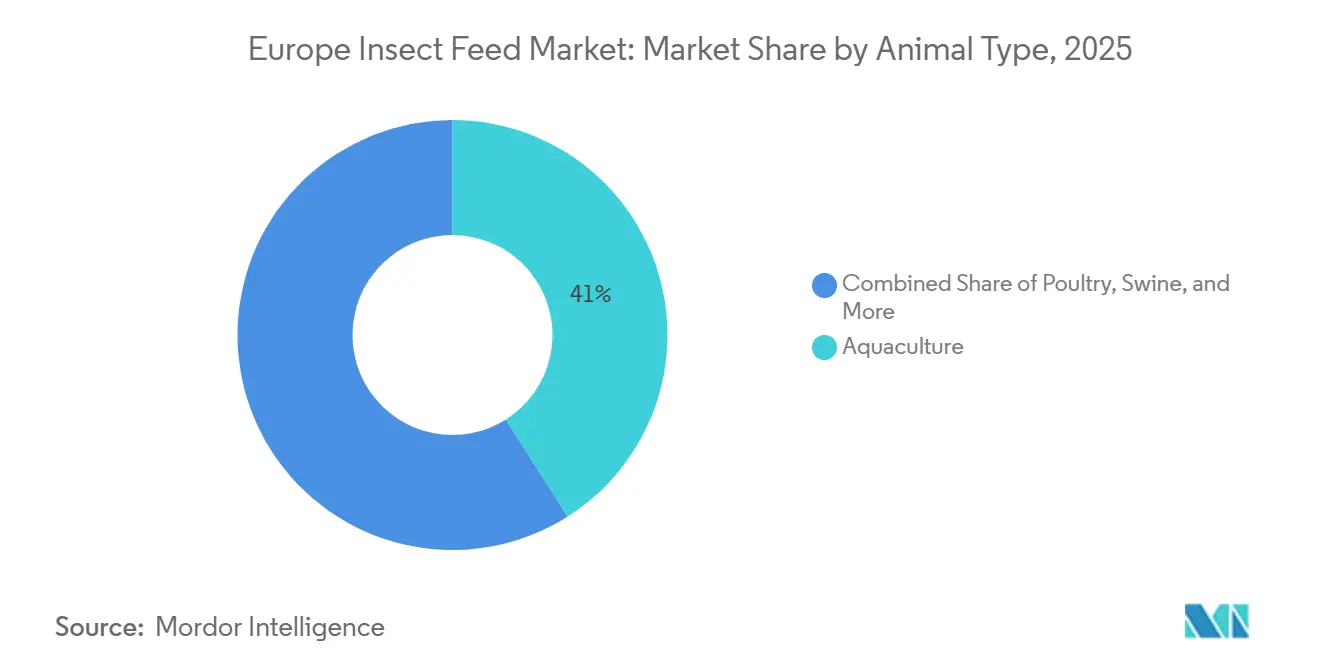

- By animal type, aquaculture accounted for 41.0% of the Europe insect feed market in 2025, while the pet segment is advancing at a 14.8% CAGR through 2031.

- By end user, commercial feed mills held 44.0% of the Europe insect feed market in 2025, while integrated livestock producers are forecast to grow at a 13.4% CAGR through 2031.

- By geography, France led with 24.0% of revenue in 2025, while Poland is projected to expand at a 14.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Insect Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU feed authorizations expand insect protein addressable demand | +2.2% | EU-wide, strongest in France, the Netherlands, and Germany | Short term (≤ 2 years) |

| Aquaculture feed seeks fishmeal and fish oil replacement | +2.0% | Norway, Denmark, the Netherlands, France, and the UK | Medium term (2-4 years) |

| Circular feed sourcing and Scope 3 reduction targets support adoption | +1.5% | EU-wide, led by France, Germany, and the Netherlands | Medium term (2-4 years) |

| Pet food premiumization lifts demand for novel insect ingredients | +1.2% | Germany, France, the UK, and the Netherlands | Short term (≤ 2 years) |

| Co-location with side streams and waste heat improves plant economics | +1.0% | France, the Netherlands, Finland, and Spain | Long term (≥ 4 years) |

| Functional lipids, chitin, and bioactive fractions broaden value capture | +0.7% | EU-wide, with early traction in Germany and the Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Feed Authorizations Expand Insect Protein Addressable Demand

The Europe insect feed market has benefited directly from the stepwise expansion of EU feed rules over the past several years. Regulation (EU) 2017/893 first allowed insect-processed animal proteins in aquaculture feed, and the 2021 amendment extended that permission to swine and poultry, which opened much larger livestock categories for commercial use. A 2024 regulatory clarification also confirmed that live insects can be used as feed materials for swine, poultry, and aquaculture, which gives smaller operators a lower processing route than full PAP production[2]Source: N. Meijer, R.A. Safitri, W. Tao, and E.F. Hoek-Van den Hil, “Review, European Union Legislation and Regulatory Framework for Edible Insect Production, Safety Issues,” Animal, doi.org. Each authorization has widened the customer base for producers across aquaculture, poultry, swine, and pet food, and this has made industrial scaling more commercially rational. The Europe insect feed market is also supported by the formal adoption of the International Platform of Insects for Food and Feed (IPIFF) good hygiene guidance in 2025, which improves traceability and reduces procurement concerns for feed mills entering the category for the first time. Growth is still limited by the continued exclusion of ruminants, but monogastric and aquaculture categories already represent the clearest short-term route for scale in the Europe insect feed market.

Aquaculture Feed Seeks Fishmeal and Fish Oil Replacement

Aquaculture remains one of the strongest demand anchors for the Europe insect feed market because fishmeal supply is constrained while aquaculture feed demand keeps increasing. EU aquatic food self-sufficiency fell to 38.1% in 2023, and the bloc imports a large share of the feed proteins it consumes, which raises both supply security and sustainability concerns[3]Source: International Platform of Insects for Food and Feed, “Positive and Strong Signs for the EU Insect Industry,” IPIFF, ipiff.org. Research in species such as rainbow trout, Atlantic salmon, European perch, and totoaba shows that insect meals can replace a meaningful share of fishmeal without damaging growth, digestibility, or product quality when inclusion is managed correctly. Norway is especially important because salmon farming has high feed-related emissions, which makes insect ingredients relevant not only as protein substitutes but also as carbon reduction tools inside existing feed systems. The Europe insect feed market is therefore drawing support from both performance validation and policy pressure in aquaculture. That combination becomes more important as industry groups push for formal inclusion targets in aquafeed over the next several years.

Pet Food Premiumization Lifts Demand for Novel Insect Ingredients

Pet food is giving the Europe insect feed market an important margin-support channel while larger livestock applications are still developing. European pet food brands have introduced insect proteins into hypoallergenic, monoprotein, and sustainability-led formulations, which have moved the category beyond experimental launches. European Pet Food Industry Federation (FEDIAF) reported that surveyed European pet owners showed a 70% acceptance rate in 2025 for insect-fed animals, and the same review indicated that more than half of European insect production was already directed toward pet food[4]Source: European Pet Food Industry Federation, “Insect-Based Ingredients in Pet Food,” FEDIAF, europeanpetfood.org. Research published in 2025 also showed that black soldier fly protein can achieve digestibility close to premium poultry meal in dogs and cats, which addresses one of the main technical barriers that had slowed wider use. The Europe insect feed market benefits here because premium pet food buyers are more able to accept novel ingredient pricing than commodity livestock feed buyers. That makes pet food an early revenue base that can help producers absorb fixed costs while they work toward the price points needed for broader feed mill adoption.

Functional Lipids, Chitin, and Bioactive Fractions Broaden Value Capture

The Europe insect feed market is no longer centered only on protein meal. Producers are increasingly building portfolios around insect oil, frass, hydrolysates, and other functional fractions because these products can carry higher value and improve overall plant economics. Black soldier fly oil is especially relevant because of its high lauric acid content, which has attracted attention in monogastric and pet food formulations. Companies are also looking at chitin and other bioactive components as part of a broader strategy to capture more revenue from each metric ton of biomass. The launch of branded ingredient platforms such as Hilucia in 2024 shows how suppliers are trying to move from bulk output into differentiated product families[5]Source: Innovafeed, “Hilucia by Innovafeed, A New Brand to Unlock the Power of Hermetia Illucens,” Innovafeed, innovafeed.com. Over time, this should make the Europe insect feed market less dependent on direct price competition with fishmeal and soybean meal alone. It also supports a more resilient business model in which protein is only one part of the value equation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Production costs remain above incumbent protein alternatives | -1.5% | EU-wide, with stronger pressure in Northern and Eastern Europe | Medium term (2-4 years) |

| EU-approved feedstock list constrains substrate flexibility | -1.2% | EU-wide, raised as a priority issue by several member states | Medium term (2-4 years) |

| Risk repricing after scale-up failures tightens financing access | -0.8% | France, Germany, and Benelux | Short term (≤ 2 years) |

| Demand remains concentrated in premium applications | -0.5% | EU-wide, easing first in aquaculture and premium pet food markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand Remains Concentrated in Premium Applications

Demand concentration is one of the major restraints shaping the Europe insect feed market. In practice, the strongest adoption still sits in aquaculture starter feeds, salmonid diets, premium pet food, and other higher-value channels rather than in broad poultry and swine formulations. Poultry and swine together make up most of the European compound feed tonnage, but those applications require much tighter price parity with soybean meal than the category can yet provide. Socio-economic research also suggests that mainstream economics remain tight even under significant scale increases, which means broad-based penetration is more likely to be gradual than sudden. This concentration matters because premium channels can be subject to reformulation cycles and brand positioning shifts. The Europe insect feed market, therefore, needs continued progress in cost reduction and industrial reliability before it can move from selective adoption into true mass-market inclusion.

EU-Approved Feedstock List Constrains Substrate Flexibility

Feedstock regulation poses a significant challenge to the Europe insect feed market. EU regulations classify insect production as a farmed animal activity, restricting the use of certain substrates and excluding several low-cost waste streams that could otherwise enhance economic viability. As a result, many producers are compelled to use certified plant-based substrates, which compete with conventional feed inputs in terms of cost. This issue has been raised in the European Parliament, where policymakers have discussed the possibility of more flexible substrate rules, at least for pet food chains or pilot projects. However, any changes would still require review and approval by the European Food Safety Authority (EFSA), leading to a lengthy rule-making process. This delay is critical, as the Europe insect feed market requires cost relief during its current scale-up phase, rather than after another full investment cycle. Until these regulations are revised, European producers will remain less adaptable compared to competitors operating under more flexible substrate policies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insect Type: Black Soldier Fly Lead Volume, Mealworms Gain Premium Ground

Black soldier fly accounted for 49.5% of the Europe insect feed market in 2025, driven by its scalability, nutritional benefits, and processing flexibility. These larvae are highly preferred due to their efficient feed conversion, production of usable protein and oil fractions, and compatibility with industrial side-stream sourcing models. Consequently, the Europe insect feed market has predominantly adopted black soldier fly larvae as the primary platform for large-scale commercialization. Research has further validated this trend, demonstrating that black soldier fly meal can effectively replace a significant portion of fishmeal in carnivorous species without negatively impacting growth performance.

Black soldier fly also aligns well with current European plant economics, as producers can extract meal, oil, and fertilizer from a single biomass stream. This enhances revenue potential and allows producers to adjust their product mix across feed and related markets. Meanwhile, mealworms are rapidly gaining traction, with a projected CAGR of 13.6% through 2031. Mealworms are particularly appealing in premium pet food and other specialized applications where digestibility and hypoallergenic properties are prioritized over large-scale production. The EU's authorization of UV-treated mealworm powder in January 2025 has further expanded processing opportunities and facilitated facility-sharing for mealworm production. Other insect types, such as houseflies and crickets, currently occupy smaller niches within the Europe insect feed market, catering to more specific feed applications rather than large-scale industrial use.

By Product Form: Insect Meal Dominates, Insect Oil Moves Fastest

Insect meal accounted for 58.0% of the Europe insect feed market in 2025, making it the core commercial product at this stage. Its prominence is attributed to its direct applicability in aquafeed and compound feed formulations, where protein concentration and digestibility are key purchasing factors. The market continues to rely on insect meal, as it is the most straightforward substitute for existing protein sources in established feed formulations. Technical data further supports its role, with insect meals demonstrating strong digestibility and amino acid profiles, making them increasingly suitable for specialized formulations. As a result, insect meal remains the most widely utilized product, even as the overall product portfolio diversifies.

Insect oil is the fastest-growing product form in the market, with a projected CAGR of 14.4% from 2026 to 2031. This growth is driven by rising demand for black soldier fly oil in pet food and monogastric feed, particularly for its lauric acid content and antimicrobial properties. Whole dried insects, while a smaller segment, are primarily used for treats, exotic animals, and niche specialty applications. Other product forms, such as puree and hydrolysates, are also gaining traction, especially in wet pet food and aquaculture starter feed applications, where functional formats are increasingly valued. The Europe insect feed industry is shifting toward higher-margin products like oils and specialty formats to mitigate the cost constraints associated with commodity protein sales. Companies such as HiProMine and Nasekomo illustrate that product strategy is becoming as critical as scale strategy in the Europe insect feed market.

By Animal Type: Aquaculture Leads, Pets Accelerates Fastest

Aquaculture accounted for 41.0% of the Europe insect feed market share in 2025, reflecting the history of regulatory approval and the strong nutritional evidence supporting its use in fish diets. It was the first major feed category approved under the European Union Insect Processed Animal Protein authorization and remains the most commercially validated application. The Europe insect feed market has established much of its initial revenue base around salmonids and other fish species, where fishmeal replacement has been extensively studied. Industry and scientific sources cite hundreds of studies supporting the inclusion of insects in fish diets under appropriate formulation conditions.

The pets segment is the fastest-growing application, with a projected CAGR of 14.8% through 2031. This growth is driven by an expanding range of insect-branded products, strong retailer support, and clinical evidence suggesting that black soldier fly protein can help manage adverse food reactions. While poultry and swine remain important medium-term targets, adoption in these segments is slower due to higher price sensitivity and conservative practices in feed mills. Other animal feed applications are gradually expanding from a smaller base as formulators gain confidence and more ingredient formats become available. Consequently, the Europe insect feed market is projected to rely on aquaculture for scale and pet food for growth momentum throughout the forecast period. This combination is likely to shape capacity planning, customer targeting, and product development strategies across the market.

By End User: Feed Mills Hold the Volume, Livestock Integrators Lead Growth

Commercial feed mills held 44.0% of the Europe insect feed market in 2025, which reflects where buying decisions are concentrated in the regional feed system. Large mills sit at the point where regulatory acceptance, ingredient testing, and downstream distribution come together, so their procurement behavior shapes the pace of wider adoption. European Feed Manufacturers' Federation (FEFAC) also noted that actual uptake in Dutch compound feed remained limited after authorization, which shows the difference between legal access and commercial incorporation. The Europe insect feed market still needs broader mill confidence in pricing, supply consistency, and certification before use can move much further into mainstream recipes. That is why partnerships with established feed companies matter so much to current expansion plans.

Integrated livestock producers are the fastest-growing end-user group, with a forecast CAGR of 13.4% through 2031. Their momentum comes from decentralized or franchise-style rearing models that allow insect biomass production closer to farms and side-stream sources. Companies such as FarmInsect and Nasekomo helped define this route by promoting modular and distributed production approaches before market conditions tightened. Aquaculture farms and hatcheries also form a distinct and growing end-user group, particularly where direct off-take relationships bypass traditional feed mill channels. Pet food manufacturers and specialty buyers complete the segment structure, and they remain important because they can absorb differentiated ingredient formats more quickly. Across these end users, the Europe insect feed market is showing that adoption will not follow one single route, but will vary by operating model, species focus, and ability to capture circular value.

Geography Analysis

France accounted for 24.0% of revenue in 2025, making it the largest market in the Europe insect feed market. That position is tied to France's early regulatory engagement, established production base, and the presence of large companies such as Innovafeed and Agronutris. The Europe insect feed market has developed faster in France because local production capacity, industrial partnerships, and policy visibility have all arrived earlier than in many other countries. Germany also remains an important market because of its large compound feed base and its role as a downstream demand center for neighboring suppliers. Poland is projected to grow at a 14.2% CAGR from 2026 to 2031, with adoption still led by aquaculture and premium pet food rather than commodity livestock feed.

Northern Europe is projected to witness strong growth, driven primarily by Norway, Denmark, and the broader salmon feed ecosystem. Norway plays a critical role due to its large-scale salmon aquaculture industry, which creates concentrated demand for both insect protein and insect oil. The region is seeing supply development aligned with this demand, supported by partnerships and new production facilities. Southern Europe is also projected to expand steadily, supported by increasing production capacity in Spain and a well-established aquaculture base in Italy. Spain is emerging as a key hub, with ongoing projects enhancing the region’s ability to supply both aquafeed and pet food markets.

Central and Eastern Europe represents the fastest-growing regional cluster, with Poland standing out as a leading market. Growth in this region is supported by relatively lower production costs, expanding industrial insect capacity, and proximity to major feed demand centers in Western Europe. Investments in production facilities and expansion plans are strengthening the region’s strategic importance in the European insect feed market. Other countries in the region are still at earlier stages of adoption, but improvements in distribution networks and support for the bioeconomy are enhancing market development. The rest of Europe contributes through niche demand, particularly in premium pet food segments and localized supply initiatives, with some markets gradually building integrated insect-based value chains.

Competitive Landscape

In 2025, the Europe insect feed market was moderately concentrated, with key players such as InnovaFeed SAS, Protix B.V., Agronutris, HiProMine S.A., and Tebrio collectively holding a significant share of the market's revenue. While these companies demonstrate leadership, the competitive landscape remains dynamic due to factors such as scaling operations, shifting financing conditions, and buyer preferences for operators with superior execution capabilities. The market is in an intermediate stage where both scale and operational discipline are critical. Larger companies leverage their scale to build customer confidence, but emerging players remain competitive by improving yields, reducing energy consumption, or focusing on higher-value product lines. This balance keeps the market open to change, even as the leading players maintain a measurable advantage.

One prominent strategy in the market has been industrial co-location. For example, in 2024, Innovafeed's model in France integrated insect production with nearby industrial inputs and waste heat. Similarly, nextProtein expanded its capacity in 2025 through a differentiated platform, supported by new funding for its Tunisia facility, which serves European value chains. Another approach involves direct downstream partnerships, as seen in Innovafeed's 2025 collaborations with BioMar and Auchan, and in Volare's off-take agreement with Skretting. These diverse approaches highlight how business model choices are influencing competition as much as installed production capacity.

Technological advancements and regulatory compliance are emerging as key competitive differentiators in the Europe insect feed market. Companies are increasingly investing in automation, artificial intelligence, advanced breeding technologies, and production optimization to improve efficiency, scalability, and product consistency, while also exploring technology-driven business models beyond ingredient production. At the same time, compliance with feed safety standards, quality certifications, and regulatory requirements is becoming increasingly important for securing access to large commercial buyers and expanding market reach. As a result, producers with strong technological capabilities, industrial-scale operations, and robust quality management systems are gaining a competitive advantage. Overall, the Europe insect feed market is projected to continue consolidating gradually. However, competition remains open, with opportunities for new entrants, capacity expansions, and further shifts in market positioning.

Europe Insect Feed Industry Leaders

InnovaFeed SAS

Protix B.V.

Agronutris

HiProMine S.A.

Tebrio (Tebrio Group S.L.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: InnovaFeed SAS, BioMar, and French retailer Auchan announced a three-party partnership to integrate Innovafeed's black soldier fly insect meal into BioMar Ecuador's commercial shrimp feed, with shrimp raised on this feed to appear in Auchan's responsible sourcing range, marking the first time insect-fed seafood reached European retail shelves at a commercial scale. This development strengthened downstream market validation and supported demand for insect-based feed ingredients in Europe.

- January 2025: Tebrio broke ground on a large-scale insect farm in Salamanca, Spain, with substantial capacity to produce protein, lipids, and biofertilizers. This significantly boosted regional production capacity and supported Europe’s position as a key supply hub.

- July 2024: InnovaFeed SAS completed a major expansion of its industrial site in Nesle, France, substantially increasing production capacity. This reinforced large-scale industrialization and improved supply reliability for European feed markets.

Europe Insect Feed Market Report Scope

Insect feed consists of animal nutrition products made from farmed insects, serving as sustainable substitutes for traditional feed ingredients such as fishmeal and soybean meal. These products are produced by rearing insects on organic byproducts and processing them into nutrient-dense outputs for use in livestock and aquaculture.

The Europe Insect Feed Market is segmented by Insect Species (Black Soldier Fly, Mealworm, Housefly, and Others), by Product Form (Protein Meal, Whole Dried Larvae, Insect Oil, and Frass Fertilizer), by Animal Type (Aquaculture, Poultry, Swine, Ruminants, and Pets), by End User (Commercial Feed Mills, Integrated Livestock Producers, and Smallholder/On-farm Systems), and by Geography (Germany, France, United Kingdom, Netherlands, Spain, Italy, Poland, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Black Soldier Fly |

| Mealworm |

| Housefly |

| Others |

| Protein Meal |

| Whole Dried Larvae |

| Insect Oil |

| Frass Fertilizer |

| Aquaculture |

| Poultry |

| Swine |

| Ruminants |

| Pets |

| Commercial Feed Mills |

| Integrated Livestock Producers |

| Smallholder/On-farm Systems |

| Germany |

| France |

| United Kingdom |

| Netherlands |

| Spain |

| Italy |

| Poland |

| Russia |

| Rest of Europe |

| By Insect Species | Black Soldier Fly |

| Mealworm | |

| Housefly | |

| Others | |

| By Product Form | Protein Meal |

| Whole Dried Larvae | |

| Insect Oil | |

| Frass Fertilizer | |

| By Animal Type | Aquaculture |

| Poultry | |

| Swine | |

| Ruminants | |

| Pets | |

| By End User | Commercial Feed Mills |

| Integrated Livestock Producers | |

| Smallholder/On-farm Systems | |

| By Geography | Germany |

| France | |

| United Kingdom | |

| Netherlands | |

| Spain | |

| Italy | |

| Poland | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is driving demand for insect-based feed ingredients in Europe?

Growth is being supported by EU feed authorizations, pressure to diversify protein sourcing, aquaculture demand for fishmeal alternatives, and premium pet food adoption.

How large will be the Europe insect feed market by 2031?

The Europe insect feed market is forecast to reach USD 1.07 billion by 2031, rising from USD 0.60 billion in 2026 at a 12.30% CAGR.

Which insect type leads commercial use in feed formulations?

Black soldier fly led with 49.5% of revenue in 2025 because they combine favorable feed conversion, scalable production, and a broad fit across meal and oil applications.

Why is aquaculture the biggest use case for insect feed in Europe?

Aquaculture held 41.0% of revenue in 2025 because EU approval came earlier for fish feed, and a large body of research already supports insect meal inclusion in aquafeed.

Which animal type is growing the fastest through 2031?

Pets segment is projected to grow at a 14.8% CAGR through 2031 as brands expand hypoallergenic and sustainability-led lines based on insect ingredients.

Page last updated on: