Insect Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

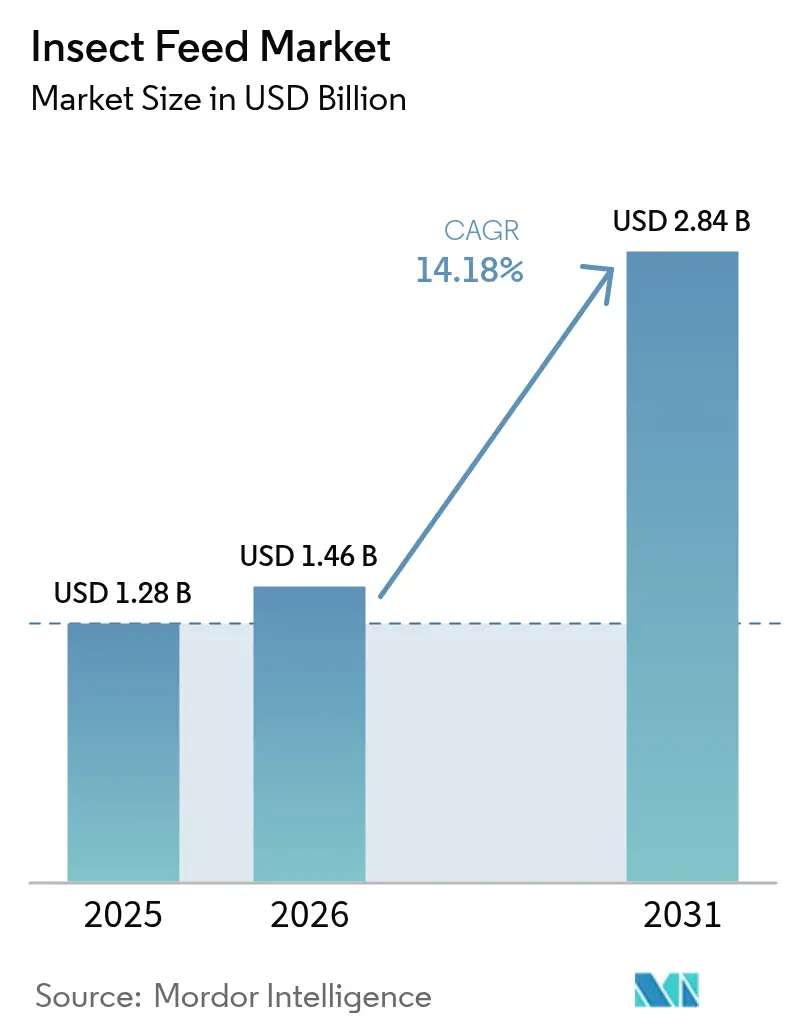

| Market Size (2026) | USD 1.46 Billion |

| Market Size (2031) | USD 2.84 Billion |

| Growth Rate (2026 - 2031) | 14.18% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insect Feed Market Analysis by Mordor Intelligence

The insect feed market size was valued at USD 1.28 billion in 2025 and estimated to grow from USD 1.46 billion in 2026 to reach USD 2.84 billion by 2031, at a CAGR of 14.18% during the forecast period (2026-2031). Increasing regulatory approvals, corporate sustainability requirements, and automated production efficiencies across aquaculture, livestock, and companion-animal nutrition sectors drive the market expansion. Insects demonstrate superior resource efficiency, with crickets offering 80% edible and digestible content compared to chicken and pigs at 55% and cattle at 40%. Insects require significantly less plant protein input to produce equivalent animal protein output compared to traditional livestock, which needs approximately 6 kg of plant protein to produce 1 kg of animal protein. The industry's growth is supported by government grants for capital investments and circular-economy models that minimize feedstock costs and greenhouse-gas emissions. While venture funding has become more selective, companies demonstrating effective automation and efficient waste stream utilization continue to attract investment capital. The market is becoming more competitive as rendering companies, established feed manufacturers, and new enterprises work to incorporate insect-based protein into standard feed products.

Key Report Takeaways

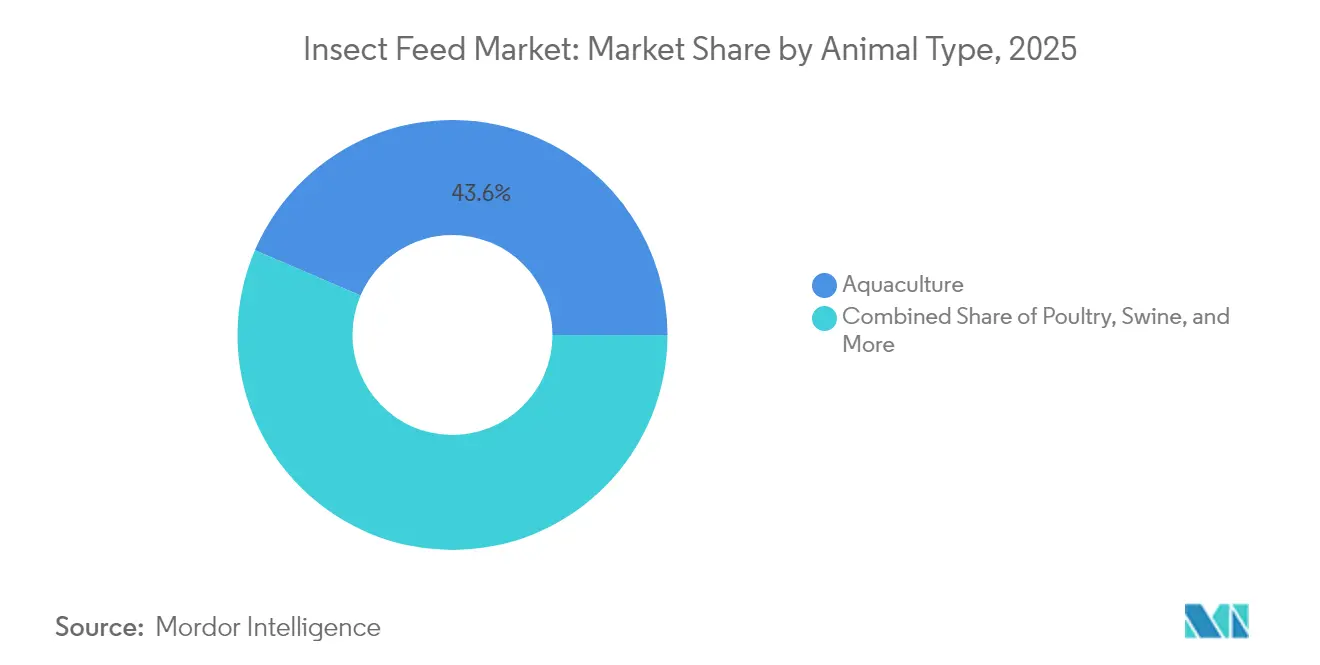

- By animal type, aquaculture led with a 43.55% market share of the insect feed market in 2025, while poultry applications are projected to advance at an 17.75% CAGR through 2031.

- By insect species, black soldier fly larvae captured 61.62% of the insect feed market size in 2025, and mealworm utilization is forecast to expand at a 16.98% CAGR to 2031.

- By product form, protein meal accounted for a 57.55% share of the market in 2025, and insect oil is projected to register the highest CAGR at 16.87% through 2031.

- By end user, commercial feed mills accounted for 47.75% of the revenue share in 2025, while integrated livestock producers demonstrated the fastest growth, at a 13.02% CAGR, over the same period.

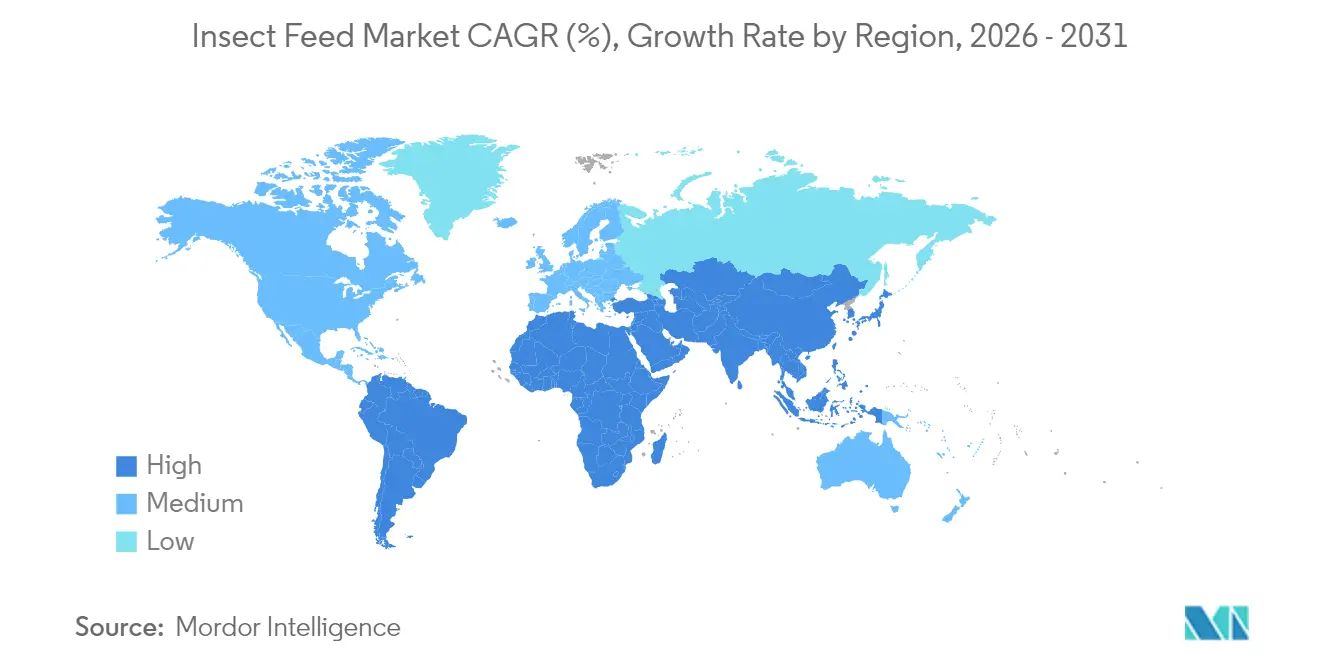

- By geography, North America secured a 33.85% share of the market in 2025, and the Middle East region is projected to grow at a 12.42% CAGR through 2031.

- Darling Ingredients Inc., Protix B.V., InnovaFeed SAS, Entobel Holding Pte. Ltd., and Entomo Farms Inc. (Next Millennium Farms Inc.) collectively hold a smaller share of the market in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insect Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High feed-conversion efficiency of insects | +2.8% | Global with concentrated adoption in Europe and North America | Medium term (2-4 years) |

| Corporate Environmental, Social, and Governance Mandates Accelerating Alternative-protein Adoption | +2.1% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Regulatory approvals for insect processed animal proteins in animal feeds | +2.5% | Europe leading, followed by North America and select Asia-Pacific markets | Short term (≤ 2 years) |

| Zero-waste co-location with agro-industrial facilities | +1.9% | Global with early implementations in Europe and North America | Medium term (2-4 years) |

| Carbon-credit monetization for waste-upcycling insect farms | +1.4% | Europe and North America, emerging in South America | Long term (≥ 4 years) |

| AI-driven genotype selection boosting larval yields | +1.7% | Technology-advanced markets in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Feed-conversion Efficiency of Insects

Insect larvae achieve feed conversion ratios of 1.5:1 to 2.0:1, significantly higher than conventional protein sources such as fishmeal (3.5:1) and soybean meal (4.2:1), providing economic benefits for feed manufacturers. Black soldier fly larvae transform organic waste into protein biomass containing 42% protein and essential amino acids similar to fishmeal, while consuming 75% less water and producing 80% fewer greenhouse gas emissions compared to traditional protein production methods. Research from the University of California shows that mealworm production needs 2,000 times less land than beef protein production, with larvae completing their development in 6-8 weeks compared to several months for conventional livestock. This efficiency is particularly important in aquaculture, where feed comprises 60-70% of total production costs, making insect-based proteins economically viable even at higher prices.

Corporate Environmental, Social, and Governance Mandates Accelerating Alternative-Protein Adoption

Net-zero commitments from global companies, including Nestlé and Elanco, influence feed procurement contracts that emphasize low-carbon proteins. The European Union taxonomy classifies insect farming as a sustainable activity, enabling access to green financing and reduced borrowing costs for facility construction. Major feed companies, including Cargill and ADM, have established alternative-protein divisions, generating significant purchase orders that provide revenue security for insect producers. This regulatory framework benefits companies using insect feed, as sustainability performance increasingly shapes procurement decisions throughout the animal protein supply chain.

Regulatory Approvals for Insect Processed Animal Proteins in Animal Feeds

The European Food Safety Authority's approval of processed animal proteins from insects for aquaculture feeds in 2024 removed a major regulatory barrier that had restricted commercial adoption across EU member states. The Association of American Feed Control Officials' (AAFCO) acceptance of black soldier fly larvae meal as a safe ingredient for dog and cat foods created access to the USD 50 billion North American pet food market[1]Source: Association of American Feed Control Officials, “AAFCO Approves Black Soldier Fly Larvae Meal for Pet Food,” aafco.org. The United Kingdom's Animal and Plant Health Agency optimized import procedures for processed insect proteins, decreasing regulatory compliance costs by 30% for commercial producers. These regulatory changes enable feed manufacturers to make capital investments in production facilities and establish long-term supply contracts. The improved regulatory environment strengthened investor confidence, resulting in venture capital funding of USD 500 million for insect protein companies in 2024, despite overall market downturns.

Carbon-Credit Monetization for Waste-Upcycling Insect Farms

Gold Standard certification recognizes insect facilities that divert organic waste, generating 2.5 metric tons of CO₂-equivalent savings per metric ton of input and carbon-credit revenues of USD 0.15-0.20 per kilogram of protein sold[2]Source: Gold Standard, “Methodology for Insect Farming Carbon Credits,” goldstandard.org. Life cycle assessments show that insect protein production generates 75% fewer greenhouse gas emissions compared to conventional fishmeal production, enabling carbon credit sales to offset production costs. The European carbon markets value waste diversion credits, with insect farming projects qualifying for the European Emissions Trading System credits when integrated with waste management operations. This carbon credit monetization improves project economics and attracts environmental, social, and governance-focused investors seeking environmental impact alongside financial returns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer perception and “yuck factor” for insect-fed proteins | –1.8% | Global with higher impact in Western markets | Long term (≥ 4 years) |

| High capital expenditures for climate-controlled vertical insect farms | –2.2% | Global particularly affecting emerging-market adoption | Medium term (2-4 years) |

| Supply-chain sensitivity to feedstock bio-security | –1.5% | Global with heightened concerns in regulated markets | Short term (≤ 2 years) |

| Tightening venture funding after early-stage insolvencies | –2.1% | Global with concentrated impact in venture-dependent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer Perception and “Yuck Factor” for Insect-Fed Proteins

Consumer acceptance remains a significant barrier, particularly in Western markets where cultural perceptions of insects limit the adoption of animal products from insect-fed livestock, despite indirect consumption. According to surveys, 65% of North American consumers are reluctant to purchase meat from animals raised on insect-based feed, reducing demand from retailers targeting environmentally conscious consumers. While consumer education about indirect consumption and environmental benefits is crucial, changes in consumer attitudes will likely progress more slowly than production capacity growth, limiting near-term price premiums. This consumer resistance affects premium pricing strategies and market penetration, especially for consumer-facing brands emphasizing sustainable feed practices.

Supply-Chain Sensitivity to Feedstock Bio-Security

Insect production facilities face significant risks from pathogen contamination in feedstock materials, as a single contamination incident can destroy entire production cycles and cause supply disruptions lasting 6-8 weeks. The United States Animal and Plant Health Inspection Service has documented an increase in border interceptions of contaminated organic materials intended for insect farming, indicating growing supply chain security risks[3]Source: Animal and Plant Health Inspection Service, “Biosecurity Guidelines for Insect Farming Operations,” aphis.usda.gov. The geographic concentration of feedstock suppliers creates additional vulnerabilities, as regional disease outbreaks or regulatory changes can affect multiple production facilities simultaneously. To mitigate these risks, commercial producers must maintain redundant supply chains and higher inventory levels, which increases their working capital requirements and operational complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Aquaculture Dominates While Poultry Surges

Aquaculture holds 43.55% of the insect feed market share in 2025, primarily due to black soldier fly meal's ability to match salmonid nutritional requirements. The meal's amino acid profile enables complete fishmeal replacement without compromising growth performance. Commercial trials in Europe and North America demonstrate equivalent or superior feed-conversion ratios, reduced phosphorus emissions, and enhanced disease resistance in shrimp and trout. The increasing fishmeal prices enhance the economic advantage, leading major aquafeed manufacturers to secure forward-purchase contracts for reliable supply and environmental compliance. The European Union and Canadian regulatory frameworks support market growth by establishing clear labeling and import guidelines.

The poultry segment projects the highest growth rate with an 17.75% CAGR through 2031. Broiler producers are incorporating insect protein at 5-15% levels to replace soybean meal, addressing commodity price fluctuations and enhancing gut health, particularly in antibiotic-free production systems. Initial programs in the United States and South Korea demonstrate that insect oil supplementation improves litter conditions and reduces mortality rates, attracting mid-sized feed manufacturers seeking both protein content and functional benefits. Select consumer brands have initiated marketing efforts highlighting improved animal welfare standards, though products command premium prices.

By Insect Species: Black Soldier Fly Leads, Mealworm Accelerates

Black soldier fly larvae accounted for 61.62% of the insect feed market size in 2025. This dominance stems from its ability to process various organic waste streams and adapt to different temperature conditions. The species benefits from clear regulatory frameworks in major markets and established patent protection for automated breeding and harvesting processes, which helps maintain profit margins. The consistent supply and stable amino-acid composition make it the preferred choice for large-scale aquafeed and poultry producers.

The mealworm segment is projected to grow at a 16.98% CAGR. This growth is driven by pet food manufacturers who value its palatability and aquaculture companies exploring it as a partial fishmeal substitute in specific species. The shorter production cycles and reduced odor allow facilities to be located nearer to urban waste sources, creating opportunities for brownfield site development. Research partnerships are investigating enzyme treatments to improve digestibility, which could enhance value in young-animal feed applications.

By Product Form: Protein Meal Prevails, Insect Oil Gains Pace

Protein meal held a 57.55% share of the insect feed market in 2025, due to its standardized nutrient composition and shelf-life stability required by industrial feed blenders. The maturation of batch-testing protocols and Hazard Analysis and Critical Control Points compliance enables mills to incorporate insect-derived protein up to 20% of total protein content without modifying vitamin and mineral premixes. Whole dried larvae maintain a niche market among ornamental fish and exotic pet owners who prioritize natural feeding behaviors.

Insect oil exhibits the highest growth rate at 16.87% CAGR, primarily due to its high lauric-acid content, which delivers antimicrobial benefits and enhances gut integrity in young pigs and poultry. The integration of extraction systems in new production facilities improves biomass utilization rates and creates additional revenue streams. Feed manufacturers are evaluating oil as an alternative energy and palatability source, often combining purchases with protein meal for efficient logistics.

By End User: Commercial Feed Mills Anchor Demand, Integrated Livestock Producers Accelerate

Commercial feed mills held 47.75% of the insect feed market share in 2025, supported by their established procurement systems, formulation expertise, and diverse multi-species customer base that stabilizes volume demands. Their substantial purchasing power enables them to secure long-term supply contracts, providing demand predictability that supports new production facility financing. These mills have expanded their quality control processes to include traceability of waste feedstock sources and are collaborating with suppliers to implement standardized certifications.

Integrated livestock producers represent the fastest-growing customer segment with a 13.02% CAGR. Their integrated control of feed, farming, and processing operations provides strong motivation to secure low-carbon inputs that support their sustainability commitments. Multiple poultry integrators in the United States and Asia have acquired minority positions in insect production companies, obtaining favorable pricing terms and creating joint research teams to optimize inclusion rates across different animal growth stages.

Geography Analysis

North America held 33.85% of the insect feed market share in 2025, maintaining its market leadership. This position stems from Association of American Feed Control Officials approvals and USD 30 million in United States Department of Agriculture funding for domestic plant expansion in 2024. The United States market saw growth through expansions by InnovaFeed and Darling Ingredients, backed by agricultural technology venture capital. In Canada, Entosystem secured CAD 58 million (USD 43 million) in funding in 2024, benefiting from provincial grants and waste management incentives that support regional production centers. Mexico's shrimp industry has begun testing insect meal as an alternative to fishmeal, indicating regional collaboration.

The Middle East demonstrates the highest growth rate at 12.42% CAGR, driven by food security initiatives to reduce feed import dependence. Saudi Arabia is advancing this strategy through build-operate contracts for insect production facilities using municipal waste. Europe maintains strong growth following European Food Safety Authority approvals for insect Processed Animal Proteins across livestock categories. Germany and the Netherlands lead in production capacity, with academic partnerships enhancing operational efficiency. France incorporated insect farming into its circular economy strategy, offering tax incentives for facilities near food processing centers. The United Kingdom reduced compliance costs by approximately one-third for black soldier fly meal imports after Brexit.

Asia-Pacific markets show varying development levels. Thailand and Singapore have implemented expedited licensing processes to establish themselves as trade centers. China is investing in insect genetics and automation research, preparing for increased domestic demand pending standardization. South America and Africa emerge as new market frontiers, combining agricultural waste availability with protein demand. This potential is demonstrated by the International Finance Corporation's USD 15 million investment in ProNuvo's Kenya operations in 2024.

Regulatory Landscape

Regulation for insect-derived ingredients continues to develop across major consuming regions, with approvals and ingredient definitions expanding addressable feed applications while tightening traceability and biosecurity requirements. In the European Union, Regulation (EU) 2021/1372 sets the framework for using insect processed animal proteins (PAPs) in aquaculture, as well as poultry and pig feed, with controls that prevent intra-species recycling. In February 2024, the EU Standing Committee on Plants, Animals, Food and Feed (SCoPAFF) clarified the legal status of live insects as feed materials in the EU (excluding ruminants), which supports additional use cases beyond rendered meals and oils.

In the United States, adoption remains closely tied to AAFCO ingredient definitions and state implementation. FDA CVM Guidance for Industry (GFI) #293 (October 2024) clarified the enforcement policy around AAFCO-defined animal feed ingredients, helping companies plan compliance pathways without pursuing separate food additive approvals for established definitions. In November 2024, AAFCO adopted definitions that broadened eligible species and end uses, including dried black soldier fly larvae for finfish, poultry, swine feed and adult dog food, and dried mealworm meal for adult dog food. This reinforced commercialization momentum in aquaculture and pet nutrition, where label claims, allergen warnings, and guaranteed analysis specifications face closer scrutiny.

Competitive Landscape

The insect feed market is moderately fragmented, with the top five companies, Darling Ingredients Inc., Protix B.V., InnovaFeed SAS, Entobel Holding Pte. Ltd., and Entomo Farms Inc. (Next Millennium Farms Inc.) holding a smaller market share in 2024. Darling Ingredients utilizes its rendering logistics to expand Black Soldier Fly operations across the United States and Europe while benefiting from cross-selling to existing feed clients. Protix has established market differentiation through its proprietary automation and joint ventures, including its recent expansion into Japan and Southeast Asia with Sumitomo, securing first-mover advantage in high-value aquafeed markets.

Strategic partnerships serve as the primary growth mechanism. InnovaFeed and ADM are co-locating facilities alongside corn-processing complexes, combining capital expenditure and waste streams to reduce return on investment periods. Tyson Foods maintains a minority stake in Protix to ensure an alternative protein supply for its European poultry brands. Intellectual property portfolios focused on automated larval harvesters, AI breeding, and odor-mitigation systems create competitive advantages. Companies with efficient regulatory approval processes gain faster market access, as demonstrated by Darling's ability to secure multi-state permits within six months due to its established compliance history.

Post-2024 funding limitations have reduced speculative investments, but well-funded major companies are utilizing the market downturn to acquire distressed assets and proprietary technology, accelerating consolidation. Early-stage companies with AI and sensor-driven platforms, such as Nasekomo, remain valuable acquisition targets as they address operational cost and consistency challenges. The emerging competitive focus involves the commercialization of co-products, including chitin and frass fertilizer, where extraction and formulation patents will influence margin diversification.

Insect Feed Industry Leaders

Darling Ingredients Inc.

Protix B.V.

InnovaFeed SAS

Entobel Holding Pte. Ltd.

Entomo Farms Inc. (Next Millennium Farms Inc.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial aquafeed and pet food remain the clearest near-term pull-through channels for insect ingredients, supported by partnerships that move inclusion from pilots into purchasing programs. In January 2026, Innovafeed and NaturAlleva announced a commercial partnership to integrate black soldier fly ingredients into aquafeed for sea bass, sea bream, sturgeon, and trout, creating additional industrial-scale adoption pathways for high-value species. Demand is also supported by corporate sustainability procurement requirements from multinational food and animal-health companies, and by the ability of insect systems to monetize co-products such as frass fertilizer and chitin alongside protein meals and oils.

On the supply side, opportunities center on lowering unit costs and reducing scale risk through automation, new financing, and distributed production architectures. In June 2026, Innovafeed announced a EUR 51 million funding round and shifted toward commercial deployment and optimization around its Nesle site, reflecting a move from R&D-heavy scale-up toward operational efficiency and more consistent volumes for aquaculture and pet food customers. New infrastructure concepts also create space for specialized breeding and genetics platforms, such as AI-enabled reproduction hubs supplying neonate larvae to multiple grow-out facilities, which can reduce biological variability and shorten ramp-up times for capacity expansions in regions building circular-economy supply chains around agro-industrial and municipal waste streams.

Recent Industry Developments

- June 2026: Innovafeed announced a EUR 51 million funding round and reported completion of its industrialization phase, reorganizing activities around its Nesle site to accelerate commercial deployment of its Hilucia ingredient ranges. The update points to a shift from scale-up execution toward cost optimization and repeatable volumes for aquaculture and pet food supply agreements.

- November 2025: Skretting Vietnam partnered with Entobel to deliver shrimp feeds containing insect meal, signaling a step toward larger-volume use of insect protein in Asian shrimp aquaculture. The collaboration links an established aquafeed formulator with an insect ingredient supplier, supporting broader customer acceptance through feed performance and quality assurance routines.

- November 2024: Innovafeed received an USD 11 million grant from the U.S. Department of Agriculture to support an insect ingredient production facility in Decatur, Illinois, focused on insect frass for fertilizer and animal nutrition applications. The award strengthens North American capacity build-out by adding non-dilutive capital and reinforces circular-economy positioning through co-product commercialization.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of insect-derived ingredients sold into animal feed, including insect meal and insect oil used in feed formulations for aquaculture and other livestock, across major producing and consuming regions.

Scope exclusions: We exclude sales of insects meant for direct human consumption and we do not count on-farm waste disposal services that do not result in a commercial feed ingredient sale.

Segmentation Overview

- By Animal Type

- Aquaculture

- Poultry

- Swine

- Ruminants

- Pets

- By Insect Species

- Black Soldier Fly

- Mealworm

- Housefly

- Others

- By Product Form

- Protein Meal

- Whole Dried Larvae

- Insect Oil

- Frass Fertilizer

- By End User

- Commercial Feed Mills

- Integrated Livestock Producers

- Smallholder / On-farm Systems

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- Egypt

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market frame and build realistic input ranges before any modeling started. We referenced public statistics and technical context from sources such as FAO datasets for feed and aquaculture indicators, USDA and EU Commission agriculture publications, and feed-ingredient trade flows from UN Comtrade.

To keep assumptions grounded, we also reviewed patent databases for insect-rearing and processing activity, environmental and food-safety guidance published by regulators, and public materials from feed associations and insect-sector groups. Company filings, investor presentations, and reputable press were used to confirm capacity announcements, plant ramp timelines, and price movement narratives, and a paid subscription for company financials plus an import-export shipment-level database was used selectively to sanity check a few inputs. These sources are illustrative only, and many other public documents and datasets were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work centered on interviews and structured surveys with insect producers, feed blenders, aquafeed formulators, distributors, and procurement teams at end users, so pricing and adoption assumptions could be tested against buying behavior. Because this is a global market, we aimed for coverage across APAC, EMEA, and the Americas, and we re-contacted selected experts when model outputs moved outside the ranges indicated by commercial quotes and capacity discussions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 42% |

| Mid tier: 45% | Functional/Unit leaders: 40% | EMEA: 31% |

| Smaller Players: 18% | Managers: 47% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable feed-ingredient demand pool by tracking aquaculture and livestock feed output trends, then applying realistic inclusion rates for insect meal and insect oil. Those penetration assumptions were anchored using interview feedback on formulation trials, regulatory acceptance, and supply availability, and then adjusted by region to reflect different adoption speeds.

After that, we corroborated totals using selective bottom-up approximations, including sampling producer capacity additions, likely utilization during ramp-up, and a price-per-ton range for key insect ingredients. We then check those assumptions against the implied revenue totals. Key model inputs included aquafeed production growth, substitution pressure versus fishmeal and soy, approved-use timelines by region, expected yields from processing, and average selling price progression as plants scale. Forecasts were built using scenario analysis, where adoption and pricing paths were stress-tested under conservative and faster-scale cases. Where bottom-up checks were incomplete, we handled the gap by applying utilization bands rather than assuming full nameplate capacity converts to sales.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the final number stays consistent with real-world signals. We compared modeled consumption with independent indicators such as feed output direction, announced capacity versus realistic ramp curves, and typical price corridors shared by buyers and sellers, then investigated outliers before sign-off.

Before publication, a second analyst review was completed to ensure definitions were applied consistently across regions and years, and that year-on-year movements could be explained by clear drivers. Reports refresh annually, with interim updates triggered when a material event occurs, such as a major plant commissioning, a regulatory change, or a sharp shift in feed ingredient pricing. Right before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Insect Feed Market Sizing Compared With Other Published Estimates

Published market sizes for insect feed do not always match, because groups often count different product buckets, choose different base years, and apply different adoption speeds for aquafeed versus other livestock. Differences also show up when one estimate treats early-stage capacity as full sales, or when currency conversion timing and price-per-ton assumptions are not refreshed often.

The main gap comes from whether frass fertilizer, pet food ingredients, and broader insect protein categories are mixed into the feed-only total. In that scope, Mordor Intelligence counts insect meal and insect oil sold into animal feed formulations and keeps frass outside the market value even if it is produced at the same facilities.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.28 B (2025) | |

| Global Publisher A | USD 0.32 B (2024) | Uses an earlier base year and appears to reflect a narrower realized-sales view, which can understate 2025 value if ramp-up and ASP progression are not updated as capacity comes online. |

| Industry Publisher B | USD 1.39 B (2025) | Casts a wider net by referencing insect co-products for animal nutrition, which can push the total higher when adjacent outputs are blended with feed-ingredient revenue. |

The spread in the table is mostly explained by scope choices and how quickly adoption and pricing are assumed to mature. By keeping the counted revenue tied to feed-ingredient sales, then cross-checking it with capacity ramp reality and buyer-side formulation behavior, the final value stays traceable to inputs that can be reviewed and repeated.

Key Questions Answered in the Report

How large is the insect feed market in 2026?

It stands at USD 1.46 billion and is projected to double to USD 2.84 billion by 2031.

Which animal segment uses the most insect protein?

Aquaculture leads, capturing 43.55% of global demand in 2025 due to fishmeal cost pressures.

What is the leading insect species in commercial feed?

Black soldier fly larvae dominate with 61.62% market share because of their waste-conversion efficiency.

Which region is growing fastest for insect-based feed?

The Middle East shows the highest CAGR at 12.42% through 2031 as governments pursue feed self-sufficiency.

What are the biggest hurdles to wider adoption?

High capex for vertical farms, consumer perception challenges, and venture-funding constraints top the list.

How do insect farms monetize environmental benefits?

Verified carbon credits worth USD 0.15-0.20 per kilogram of protein are sold for waste diversion and emissions savings.

Page last updated on: