Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4 Billion |

| Market Size (2026) | USD 4.11 Billion |

| Market Size (2031) | USD 4.68 Billion |

| Growth Rate (2026 - 2031) | 2.64% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Alfalfa Market Analysis by Mordor Intelligence

The Europe alfalfa market size is projected to increase from USD 4.00 billion in 2025 to USD 4.11 billion in 2026 and reach USD 4.68 billion by 2031, registering a CAGR of 2.64% from 2026 to 2031. The Europe alfalfa market is on a steady growth path, supported by firm dairy demand, while it continues to face tighter environmental regulations and water management pressures. Common Agricultural Policy (CAP) 2023-2027 eco-scheme payments have supported the inclusion of forage legumes in crop rotations, helping keep alfalfa relevant in farm revenue planning across the region. The Carbon Removal and Carbon Farming Certification Regulation (CRCF) in 2024 also strengthens the commercial case for alfalfa rotations by creating a pathway for certified carbon farming activity in the European Union. At the same time, dehydration plant upgrades that improve drying efficiency and moisture control are helping established processors protect product quality and manage costs more effectively. As a result, the Europe alfalfa market remains supported by stable feed demand and improved processing economics, even as irrigation limits and logistics risks keep the growth rate measured rather than rapid.

Key Report Takeaways

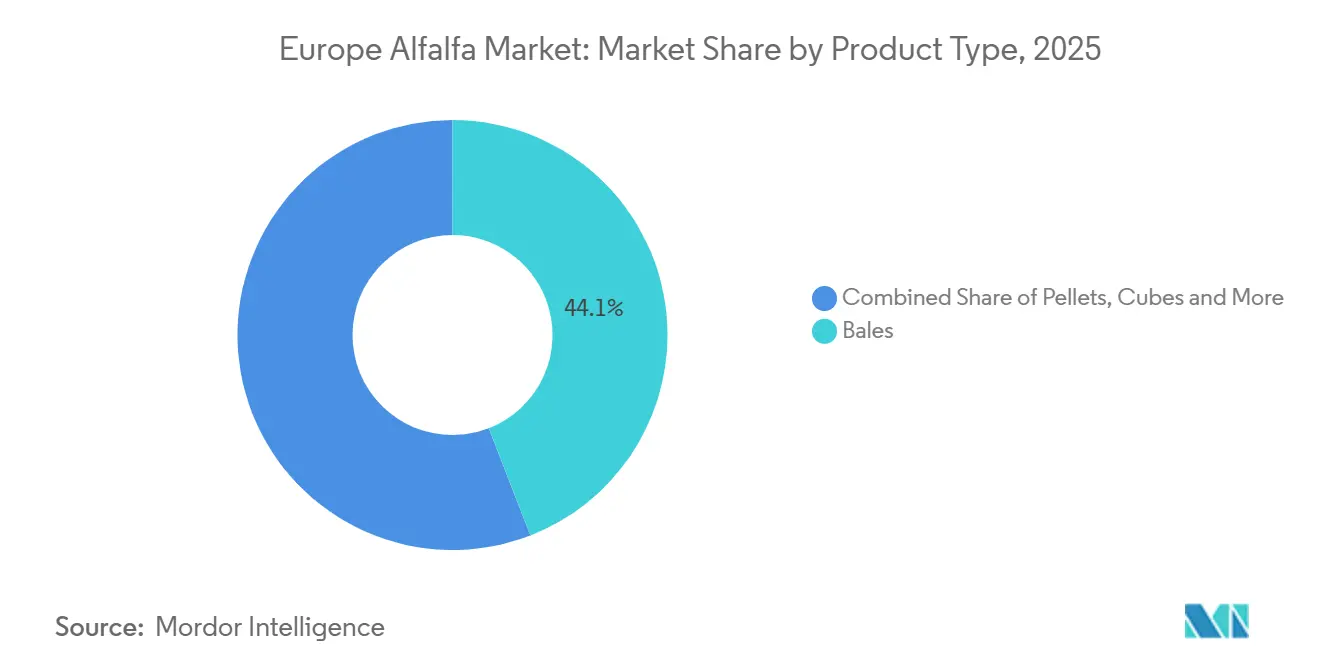

- By product type, bales held 44.10% of market share in 2025, while pellets are projected to expand at a 7.80% CAGR from 2026 to 2031.

- By application, dairy cattle feed accounted for 38.60% share of market size in 2025, while equine feed is forecast to grow at a 7.20% CAGR between 2026 and 2031.

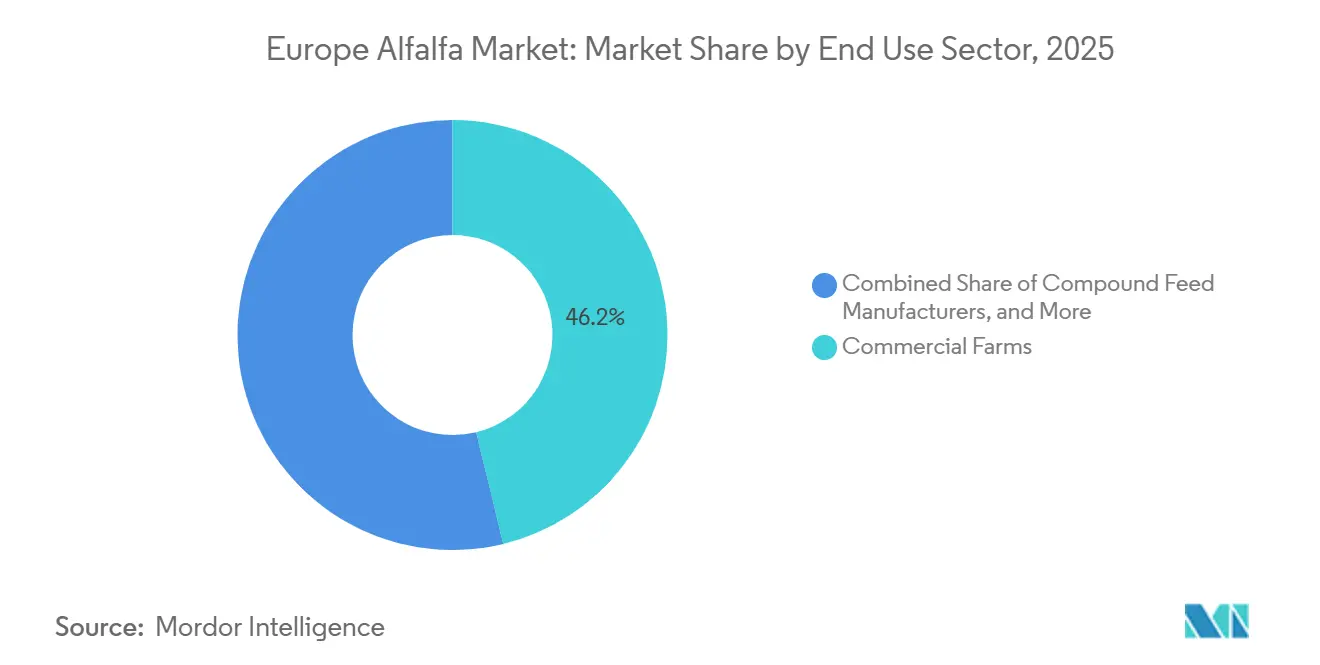

- By end-use sector, commercial farms captured 46.20% share in 2025, while pet food and specialty nutrition are forecasted to advance at a 7.60% CAGR from 2026 to 2031.

- By geography, Germany held 22.40% share in 2025, while the United Kingdom is identified as the fastest-growing country with 7.05% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Alfalfa Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of high-protein alfalfa in European dairy rations | +0.8% | European Union-wide, strongest in Germany, France, Ireland, and Denmark | Medium term (2-4 years) |

| Growth in export-driven alfalfa forage trade across key European corridors | +0.6% | Spain and France as primary exporters, Germany and the United Kingdom as import hubs | Medium term (2-4 years) |

| Rising demand for certified organic and non-GMO alfalfa forage | +0.5% | Germany, France, and the United Kingdom | Long term (≥ 4 years) |

| Carbon credit opportunities in alfalfa-inclusive crop rotations | +0.3% | European Union-wide, led by France, Germany, and Spain | Long term (≥ 4 years) |

| Advances in post-harvest precision drying and moisture management | +0.5% | Spain as primary, France and Italy as secondary | Medium term (2-4 years) |

| Rising alfalfa adoption in equine and specialty livestock nutrition | +0.4% | United Kingdom, Germany, and France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of High-Protein Alfalfa in European Dairy Rations

The Europe alfalfa market continues to benefit from dairy farms seeking dependable, protein-rich forage amid volatile feed costs. Teagasc in 2025 notes that intensive dairy feeding programs require a strong nutritional balance, and alfalfa fits well because it helps meet crude protein targets without relying solely on higher-cost concentrate inputs. The evidence also shows that dairy cooperatives in Castile and León and Galicia, Spain, have raised per-cow alfalfa inclusion rates by 9% since 2024, as protein-linked forward contracts have become more common. A 2025 study in Frontiers in Sustainable Food Systems found that fodder legumes can reduce greenhouse gas emissions in dairy systems when they replace rapeseed-extraction meal as a protein source. This combination of nutritional value, ration flexibility, and emissions-reduction benefits keeps dairy demand as the most stable volume base in the Europe alfalfa market.

Growth in Export-Driven Alfalfa Forage Trade Across Key European Corridors

The market also gains support from a stronger export position, particularly in Spain and France. Spanish Association of Dehydrated Alfalfa Manufacturers (AEFA) data indicate that Spanish dehydrated alfalfa exports reached 1,080,641 metric tons in 2025, a 43.5% increase from 2024, reflecting a strong recovery in overseas demand. The same source indicates that the United Arab Emirates received 133,622 metric tons of bale exports during the 2024-2025 campaign, while South Korea significantly increased its purchases from Spain, highlighting the expansion of trade relationships beyond a narrow buyer base. La Coopération Agricole states that France’s Luzerne de France network operates 24 dehydration plants, providing the French side of the Europe alfalfa market with a broad processing base and a stable platform for intra-European sales. The wider trade environment also remains supportive, as the European Commission reported a European Union agri-food trade surplus of EUR 49.9 billion in 2025, equivalent to USD 53.892 billion, confirming the structural strength of export-oriented agricultural supply chains[1]Source: Directorate-General for Agriculture, “EU Agri-food Trade Hits New Records in 2025," agriculture.ec.europa.eu.Collectively, this export momentum signals to buyers across Asia and the Gulf that European alfalfa supply chains are structurally reliable, reducing the procurement-risk premium that has historically pushed long-term contract buyers toward North American suppliers, and reinforcing Europe's position as a primary, rather than supplementary, source of high-quality dehydrated forage.

Rising Demand for Certified Organic and Non-GMO Alfalfa Forage

The market is moving toward a clearer split between bulk commodity forage and premium certified forage. Buyers in organic dairy, non-GMO livestock feed, and tightly specified supply programs increasingly require traceable products with stronger controls over production methods and residue exposure. The report notes that Germany’s organic dairy base in Bavaria and Lower Saxony continues to source certified supply from Spain and France, as domestic availability does not fully meet demand. European Union-FarmBook guidance, April 2026 highlights the value of high-legume forage varieties for organic systems, identifying early vigor, nitrogen efficiency, and resilience as priority traits. NAFOSA also states that its Peralta facility in Navarra, Spain, operates with 100% organic production capacity, underscoring how the Europe alfalfa market is developing dedicated infrastructure for this premium segment.

Carbon Credit Opportunities in Alfalfa-Inclusive Crop Rotations

The Europe alfalfa market is gaining additional support from carbon farming policy and stronger evidence on soil performance. A 2025 paper in the European Journal of Soil Science reviewed 39 paired treatment sites across Europe and reported an average soil organic carbon accrual factor of 1.08 for forage legume rotations, supporting the case that alfalfa-inclusive systems build soil carbon stocks rather than deplete them. The European Union formally adopted the Carbon Removal and Carbon Farming Certification Regulation (CRCF) in December 2025, creating a certification pathway for carbon removals and carbon farming activities, including legume rotations. La Coopération Agricole has aligned the French alfalfa sector’s strategy with sustainability, which supports the need for auditable records and verified farm practices under this framework. As a result, the Europe alfalfa market is likely to see carbon-related value emerge first among larger processing groups and organized cooperatives, which can manage certification costs more effectively.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited water availability and tightening irrigation policies | -0.6% | Spain in the Ebro and Guadalquivir basins, Southern France, and Italy in the Po Valley | Long term (≥ 4 years) |

| Shipping rate instability and export logistics uncertainty | -0.5% | Global, most acute for Spanish and French exporters shipping to the Middle East and Asia | Medium term (2-4 years) |

| Competitive pressure from grass hay and silage as feed substitutes | -0.4% | Germany, Ireland, the United Kingdom, and the Netherlands | Short term (≤ 2 years) |

| Compliance burden from phytosanitary and residue regulations | -0.3% | European Union-wide, most acute on Spain to Middle East and Spain to Asia export corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Water Availability and Tightening Irrigation Policies

Water access remains the most significant structural supply constraint in the Europe alfalfa market. Alfalfa can produce multiple cuttings per season, but this output requires reliable irrigation, especially in Mediterranean production zones where summer moisture stress is common. This factor is particularly important in Spain, as the country serves as the main production base for export-grade dehydrated alfalfa and supports a large share of the Europe alfalfa market’s tradable supply. When irrigation allocations tighten, the second and third cuttings become more vulnerable, and processors experience lower throughput and less consistent raw material quality. As a result, the market can continue to grow only if productivity gains and water-efficient agronomy offset the hard ceiling created by stricter water management.

Shipping Rate Instability and Export Logistics Uncertainty

Freight risk remains a major commercial restraint, as alfalfa has a low value-to-weight profile and cannot easily absorb sharp increases in shipping costs. Coordinating Body of Farmers' and Livestock Producers' Organizations (COAG) warned that conflict risks along Gulf routes threaten the Spanish alfalfa export corridor serving Arab markets, highlighting how quickly logistics disruptions can affect sales to key demand centers. AEFA data already show that Spanish exporters must maintain flexibility across destination markets, with growing shipments to Asia complementing traditional Middle Eastern demand. This trend increases the need for dependable container access, effective route planning, and contract structures that can manage freight volatility. As a result, the European alfalfa market remains exposed to logistics shocks, even when underlying feed demand is stable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pellets Accelerate as Logistics and Nutrition Demands Converge

Bales held 44.10% of the Europe alfalfa market share in 2025, maintaining their position as the leading product format across large dairy operations in Germany, France, and Spain. Bale handling supports automated feeding systems, requires less processing than pellets, and moves efficiently through established regional supply chains, which continues to strengthen their market position. Standard bale formats also meet the needs of buyers that prioritize volume, feed familiarity, and lower unit costs over premium presentation. Compressed bales serve a narrower but important role by improving container fill rates and reducing freight costs per metric ton in export programs.

Pellets represent the strongest growth format, with the Europe alfalfa market size for pellets projected to expand at a CAGR of 7.80% from 2026 to 2031. Pellets are gaining traction because they offer better moisture stability, more uniform density, and easier handling in precision feeding systems and dust-sensitive equine settings. The analysis also indicates that pellet capacity expansion remains concentrated among a limited number of vertically integrated Spanish operators, which means supply additions may occur in uneven phases rather than follow a smooth trajectory. Cubes remain a useful middle ground because they provide better density than loose bales while retaining appeal in specialist feeding programs that value palatability and leaf retention.

By Application: Dairy Anchors Volume While Equine Redefines Margin

Dairy cattle feed accounted for 38.60% of the Europe alfalfa market size in 2025, confirming that ruminant nutrition remains the primary demand base for the market. France and Germany reinforce this position through high-intensity dairy systems that rely on consistent roughage quality and a stronger protein balance in forage rations. Alfalfa’s role in dairy feed extends beyond herd size, as the analysis also indicates higher inclusion rates under contracts that reward protein performance.

Equine feed is the fastest-growing application, with a CAGR of 7.20% forecasted from 2026 to 2031, making it the key margin-led growth opportunity in the Europe alfalfa market. Dengie highlights alfalfa’s role in horse diets and its value in supporting fiber intake and ration quality, which drives demand for premium pellets, chops, and other processed formats. Beef cattle feed remains more stable and slower growing, as grass-based systems in the United Kingdom and Ireland reduce the need for purchased alfalfa in many cases. Poultry and small ruminant applications remain smaller, but they continue to contribute to demand by extending alfalfa use into yolk-color support, prebiotic fiber applications, and dairy sheep and goat systems that serve specialty cheese supply chains.

By End Use Sector: Commercial Farms Lead but Specialty Channels Lift Price Realization

Commercial farms held 46.20% share in 2025, making them the largest end-use base in the Europe alfalfa market. This share reflects strong demand from commercial dairy and equine operators, which purchase forage in larger volumes and depend on consistent quality through formal procurement channels. Compound feed manufacturers also support volume stability, as they incorporate alfalfa meal and pellet output into formulated feed programs across several livestock categories. Together, these two channels keep the Europe alfalfa market linked to stable industrial and farm-level demand, rather than relying only on niche retail purchases.

Pet food and specialty nutrition is forecasted to be the fastest-growing end-use sector, registering a 7.60% CAGR from 2026 to 2031, making it the clearest premium channel in the Europe alfalfa market. Household and hobby animal owners add further value by purchasing smaller packaged formats, which generate much higher price realization than bulk farm shipments. A 2025 study in the European Journal of Agronomy showed that forage legume integration can reduce off-farm nitrogen purchases and farm-level nitrogen surplus in intensive dairy systems, supporting the value proposition for commercial users under tighter nutrient management rules[2]Source: European Journal of Agronomy, “Integrated forage system reduces off-farm purchased nitrogen and limits surplus on intensive dairy farms in northern Italy,” sciencedirect.com. The channel mix, therefore, creates a split structure in which large farms drive volume, while specialty nutrition and branded retail products account for a disproportionate share of margin growth.

Geography Analysis

Germany held 22.40% of the Europe alfalfa market in 2025, making it the largest country market in the region. The country's leadership is supported by its large commercial dairy sector, high demand for premium forage, and widespread adoption of certified non-GMO and organic feed. Germany's advanced livestock production systems and strict feed-quality standards continue to drive consistent demand for processed alfalfa products, particularly high-quality bales and pellets used in intensive dairy operations.

The United Kingdom is anticipated to be the fastest-growing country market during the forecast period. Growth is being driven by increasing demand from the equine sector, rising adoption of premium processed forage products, and stricter feed hygiene and dust-control requirements. The expansion of high-value livestock production and growing preference for certified forage products are further supporting the uptake of dehydrated alfalfa, positioning the United Kingdom as one of Europe's fastest-expanding demand markets.

Spain, France, and Russia continue to play important but distinct roles within the Europe alfalfa market. Spain serves as the region's primary production and export hub, supported by extensive irrigated cultivation and a well-developed dehydration industry. According to AEFA, Spain exported 1,080,641 metric tons of dehydrated alfalfa in 2025, including 728,085 metric tons of bales and 351,556 metric tons of pellets, reinforcing its position as one of the world's leading alfalfa exporters[3]Source: AEFA, “Spanish exports of dehydrated fodder regain their strength in the 2024/2025 campaign," alfalfaspain.es. France remains a major production and processing center through its cooperative-based industry structure, with the Luzerne de France network operating 24 processing plants. Despite weather-related challenges, the country recorded 66,500 hectares under alfalfa cultivation and produced 725,000 metric tons in 2025, supporting both domestic consumption and regional trade. Russia, meanwhile, is a significant volume producer within the market, although its production is largely consumed domestically to support the country's extensive ruminant livestock sector rather than export markets. Together, these countries create a balanced regional market in which export-oriented production, value-added processing, and premium livestock feed demand collectively shape the competitive landscape.

Competitive Landscape

The Europe alfalfa market remains moderately fragmented at the company level. This structure creates substantial opportunities for regional cooperatives, local processors, and specialist exporters across Spain, France, and Italy. Scale alone does not define competitiveness in the Europe alfalfa market, as buyers increasingly favor suppliers that combine farm access, processing control, certification, and dependable export execution. As a result, vertically integrated operators and organized cooperatives are better positioned than purely transactional traders.

Al Dahra has strengthened its position by directly controlling upstream agricultural assets, including 56,000 hectares in Romania and several Spanish production units noted in the report . Its sustainability reporting also highlighted regenerative and reduced-disturbance farming across cultivated land in its Romanian Agricost operation, along with scope 1, 2, and 3 greenhouse gas inventory work across its European farming portfolio. NAFOSA has pursued differentiation through dedicated organic capacity and facility investment, with the company stating that its Peralta operation runs at 100% organic production capacity.

Desialis has taken a more research-led approach in December 2024, by launching the In-PULSA program to support product validation in equine nutrition, demonstrating how the Europe alfalfa market is moving beyond bulk forage toward evidence-backed specialty positioning. Policy and compliance now shape competition almost as much as acreage and plant capacity. The CRCF gives producers with auditable crop rotations and stronger documentation a new way to support revenue quality and commercial positioning. Premium organic, non-GMO, equine, and specialty nutrition channels also favor suppliers that offer consistent testing, branded formats, and stronger proof of origin. Therefore, competition in the Europe alfalfa market is likely to center on reliable certified supply, efficient processing, and closer alignment with higher-value feed programs rather than volume expansion alone.

Europe Alfalfa Industry Leaders

-

Al Dahra ACX Global Inc.

-

Anderson Hay and Grain Inc.

-

Alfalfa Monegros SL

-

Riverina Pty Ltd.

-

Grupo Osés Agroalimentaria S.L. (NAFOSA S.A.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: AEFA renewed its Board of Directors for the 2026–2030 term and strengthened its international engagement by representing Spain’s dehydrated alfalfa industry at the ILDEX Fair in Vietnam in May 2026. The association also plans to participate in the China Dairy Exhibition 2026, further expanding its presence across Asia-Pacific under the European Union-funded joint promotional program implemented by AIFA and AEFA.

- November 2025: AEFA sent one of the largest national delegations, with 59 participants, to the World Alfalfa Congress 2025 in Reims, France. The delegation presented Mediterranean irrigation management, energy-efficient dehydration, and soil-adaptive variety selection as key competitive differentiators for European-origin alfalfa.

- December 2025: Al Dahra's latest sustainability report shows that 76% of its Romanian Agricost land uses regenerative farming practices, and that it has a full Scope 1, 2, and 3 greenhouse gas inventory for its European operations. This raises environmental standards in the European alfalfa market and offers transparency for livestock buyers seeking to reduce supply chain emissions, providing a competitive advantage as demand for green-certified feed grows.

Europe Alfalfa Market Report Scope

Alfalfa, Medicago sativa, is an important forage crop cultivated for animal nutrition because of its high protein content, palatability, and value in hay and processed feed formats.

The Europe Alfalfa Market is Segmented by Product Type (Bales, Pellets, Cubes, and Compressed Bales), by Application (Dairy Cattle Feed, Beef Cattle Feed, Poultry Feed, Equine Feed, Small Ruminant Feed and Camelids and Other Livestock Feed), End Use Sector (Commercial Farms, Compound Feed Manufacturers, Household and Hobby Animal Owners, and Pet Food And Specialty Nutrition), and Geography (Spain, France, The United Kingdom, Germany, Russia and Rest of Europe). The Report Offers Market Estimation and Forecasts In Value (USD) and Volume (Metric Tons).

By Product Type

| Bales |

| Pellets |

| Cubes |

| Compressed Bales |

By Application

| Dairy Cattle Feed |

| Beef Cattle Feed |

| Poultry Feed |

| Equine Feed |

| Small Ruminant Feed |

| Camelids and Other Livestock Feed |

By End Use Sector

| Commercial Farms |

| Compound Feed Manufacturers |

| Household and Hobby Animal Owners |

| Pet Food and Specialty Nutrition |

By Geography

| Spain |

| France |

| United Kingdom |

| Germany |

| Russia |

| Rest of Europe |

| By Product Type | Bales |

| Pellets | |

| Cubes | |

| Compressed Bales | |

| By Application | Dairy Cattle Feed |

| Beef Cattle Feed | |

| Poultry Feed | |

| Equine Feed | |

| Small Ruminant Feed | |

| Camelids and Other Livestock Feed | |

| By End Use Sector | Commercial Farms |

| Compound Feed Manufacturers | |

| Household and Hobby Animal Owners | |

| Pet Food and Specialty Nutrition | |

| By Geography | Spain |

| France | |

| United Kingdom | |

| Germany | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of Europe alfalfa by 2031?

The Europe alfalfa market is forecast to reach USD 4.68 billion by 2031 from USD 4.11 billion in 2026, at a 2.64% CAGR.

Which product format is growing fastest in Europe alfalfa?

Pellets are the fastest-growing product type, with a projected 7.80% CAGR from 2026 to 2031, supported by moisture stability and precision feeding use.

Which country leads Europe alfalfa demand?

Germany leads with a 22.40% share in 2025 because of its large dairy sector and strong demand for certified non-GMO and organic forage.

What is the biggest supply-side risk for Europe alfalfa producers?

Water scarcity is the main structural risk because irrigated Mediterranean production zones, especially in Spain, are central to regional tradable supply.

Page last updated on: