South America Insect Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

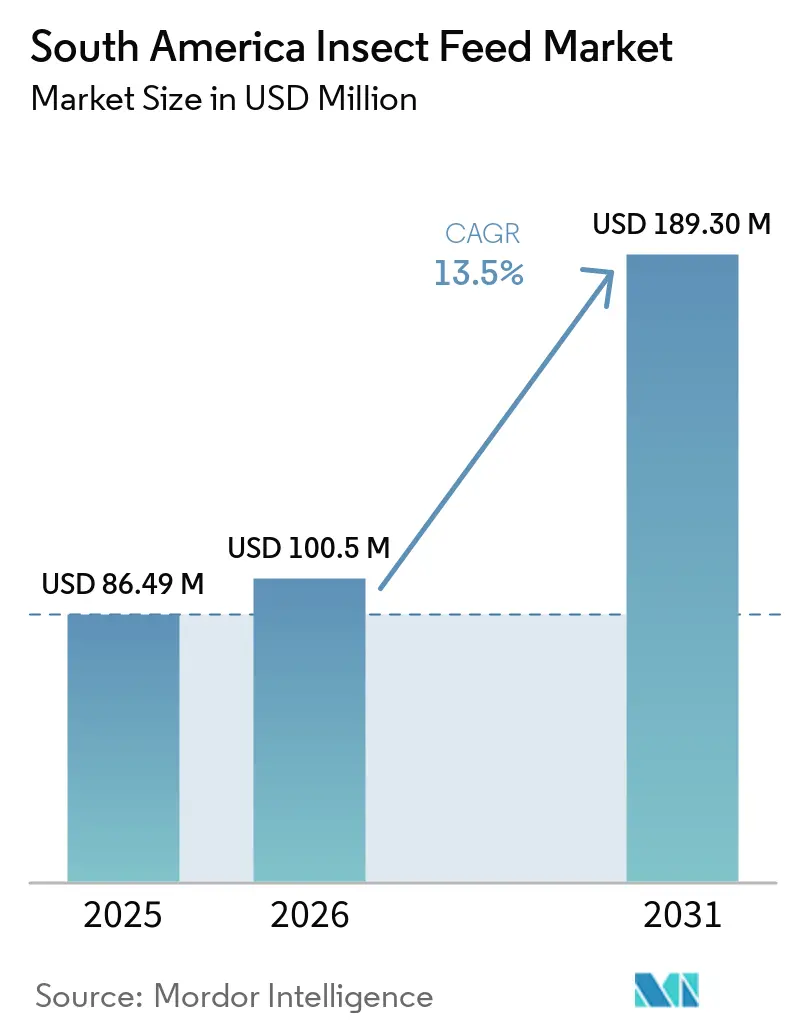

| Base Year Market Size (2025) | USD 86.49 Million |

| Market Size (2026) | USD 100.5 Million |

| Market Size (2031) | USD 189.30 Million |

| Growth Rate (2026 - 2031) | 13.50% CAGR |

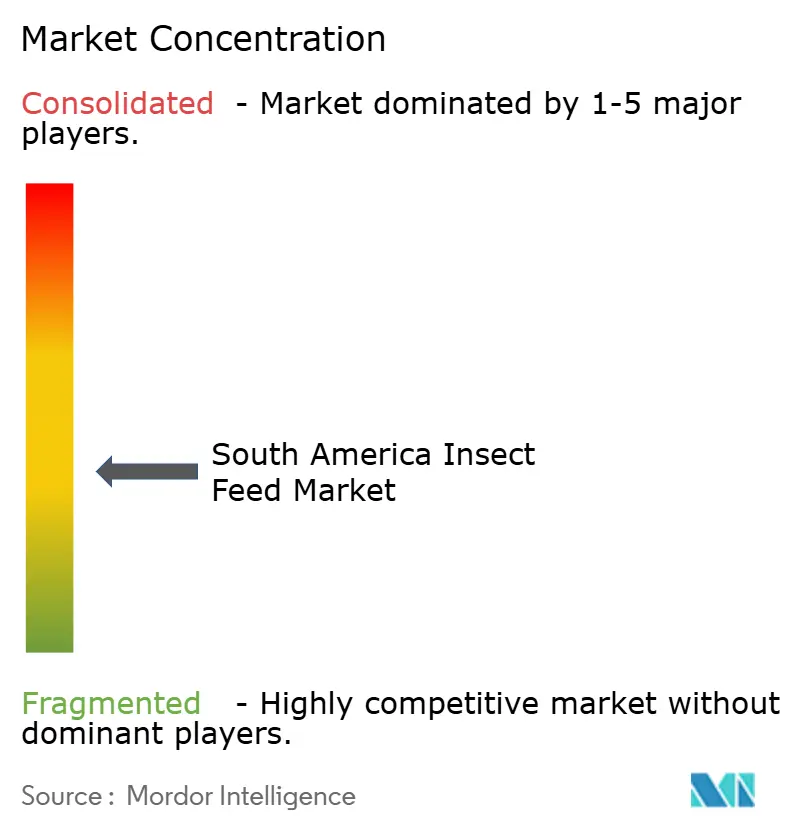

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Insect Feed Market Analysis by Mordor Intelligence

The South America insect feed market size was valued at USD 86.49 million in 2025 and is estimated to grow from USD 100.50 million in 2026 to reach USD 189.30 million by 2031, at a CAGR of 13.50% during the forecast period (2026–2031). Demand for insect feed is increasing due to the volatility of fishmeal costs, which are influenced by fluctuations in anchoveta catches off Peru, and the growing pressure on export-oriented animal protein chains to adopt lower-impact feed sources. In 2024, Brazil produced 86.6 million metric tons of commercial feed, with aquaculture feed growing by 8.6%. South America's total feed output reached 198.4 million metric tons, indicating a substantial and expanding regional base for alternative protein inputs[1]Source: Alltech, “2025 Agri-Food Outlook, 14th Annual Global Feed Production Survey,” Alltech, aquafeed.com. The South America insect feed market is benefiting from the abundant availability of agro-industrial byproducts, particularly in Brazil, Argentina, and Chile, which can be used as substrates. This advantage enables local producers to manage input costs more effectively compared to many international competitors. Regulatory advancements in Brazil and Argentina are facilitating the commercialization of approved insect-based ingredients. However, approval processes and regulatory frameworks differ across South American countries, creating an uneven competitive environment within the region [2]Source: Servicio Nacional de Sanidad y Calidad Agroalimentaria, “Se Incorporan en el Reglamento de Inspección Plantas que Elaboran Derivados de Insectos Para Alimentación Animal,” Argentina.gob.ar, argentina.gob.ar . Despite the market's fragmented nature, which presents opportunities for new capacity, the price disparity between insect-based feed and traditional options such as soymeal and fishmeal continues to hinder adoption in cost-sensitive feed formulations.

Key Report Takeaways

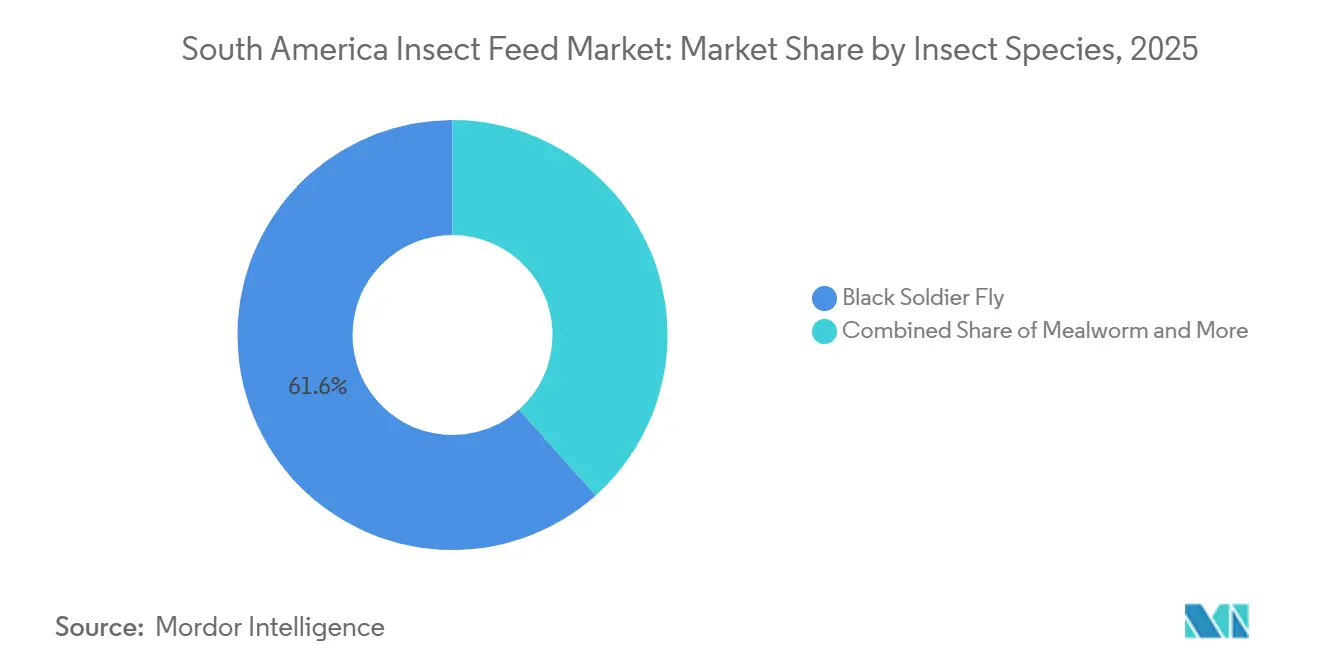

- By insect species, Black Soldier Fly held 61.6% of the South America insect feed market share in 2025, while Mealworm is projected to record the fastest growth at a 12.9% CAGR through 2031.

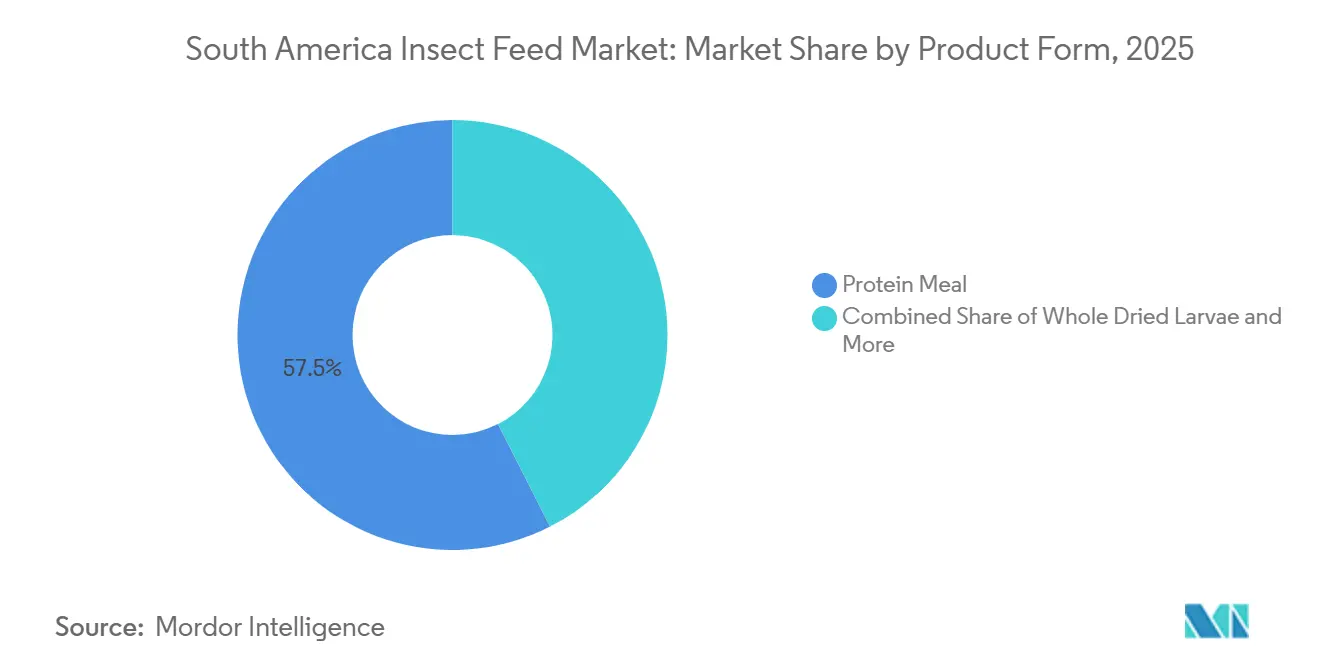

- By product form, protein meal accounted for 57.5% of the South America insect feed market size in 2025, while insect oil is forecast to grow the fastest at a 11.8% CAGR through 2031.

- By application, Aquaculture accounted for 43.5% of the market in 2025, while Poultry Feed is projected to grow at the highest CAGR of 13.7% through 2031.

- By geography, Brazil led regional demand with 47.3% market share in 2025, while Argentina is the fastest-growing country market at a 11.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Insect Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aquaculture feed formulators seeking fishmeal replacement | +5.2% | Chile, Ecuador, Brazil, with spillover to Colombia and Peru | Short term (≤ 2 years) |

| Pet food premiumization and hypoallergenic protein demand | +3.3% | Brazil and Chile, with early-stage adoption in Argentina and Colombia | Medium term (2-4 years) |

| Circular use of agro-industrial byproducts for larvae substrate | +3.8% | Brazil, Argentina, Chile, with spillover to Colombia | Short term (≤ 2 years) to Medium term (2-4 years) |

| Poultry and swine feed diversification away from soy dependence | +4.2% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Export decarbonization audits favoring low-footprint feed inputs | +2.8% | Chile, Brazil, Ecuador | Medium term (2-4 years) to Long term (≥ 4 years) |

| Frass monetization improving insect plant unit economics | +2.2% | Brazil and Chile, with early gains in São Paulo and Valparaíso | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aquaculture Feed Formulators Seeking Fishmeal Replacement

The South America insect feed market is getting one of its strongest boosts from aquaculture, as salmon, shrimp, and tilapia producers all face periodic pressure on fishmeal prices. Peru’s anchoveta catch variability continues to affect feed economics across the region, keeping alternative proteins in active evaluation by formulators. Production growth matters for the South America insect feed market because each step up in shrimp, salmon, and tilapia output increases the need for reliable protein inputs less exposed to marine raw material swings. BioMar, InnovaFeed, and Auchan moved this issue closer to commercial scale in September 2025 through a partnership with Ecuador’s shrimp feed chain, demonstrating that insect meal is being positioned as a practical ingredient rather than a trial concept. The South America insect feed market also benefits when insect meal delivers both protein and functional value, as this reduces the effective gap with conventional ingredients in aquafeed formulas.

Pet Food Premiumization and Hypoallergenic Protein Demand

Pet food is driving a different type of demand in the South America insect feed market, as buyers in this channel are less sensitive to commodity protein pricing. Insect protein fits well into elimination diets and sensitive-digestion formulas because it is a novel protein for many pets and can support premium positioning. Hill’s Pet Nutrition launched its Sensitive Stomach and Skin line in Brazil in February 2025, and the launch showed that insect protein had moved into a mainstream retail setting instead of remaining a niche experiment. Special Dog followed in August 2025 with Bionatural Sensitive, and Circular Pet launched a hypoallergenic insect-protein dog food in Chile in October 2025, confirming that the demand pattern was spreading across multiple countries. This matters for the South America insect feed market because premium pet food can absorb higher ingredient costs more easily than poultry or swine feed, making it an important early revenue stream for regional producers. The pace is still linked to regulatory progress, but the commercial signal from these launches is already clear.

Circular Use of Agro-Industrial Byproducts for Larvae Substrate

The South America insect feed market has a basic cost advantage, as agro-industrial byproducts are available in large volumes and close to processing clusters. The November 2025 Frontiers in Sustainable Food Systems analysis noted that the absence of a harmonized regional substrate framework continues to create uneven access to permitted waste streams across countries. That unevenness currently favors Brazil, where the South America insect feed market can draw on a broader, more industrialized feedstock base than some neighboring countries. Over time, if regional rules converge, producers in Argentina, Chile, and Colombia may be able to narrow this cost gap.

Poultry and Swine Feed Diversification Away from Soy Dependence

The South America insect feed market is also supported by the need to reduce heavy reliance on soy-based feed formulas. Brazil raised its biodiesel blend mandate to B15 from August 1, 2025, which increased demand for soybean oil and tightened the broader soybean processing balance. That shift does not remove soybean meal from feed, but it increases the appeal of having additional protein options in poultry and swine diets, especially when buyers want to diversify ingredient risk. Colombia's regional dependence is clear, as poultry accounted for the majority of the country’s corn imports, and feed formulas typically include large amounts of soybean meal [3]Source: USDA Foreign Agricultural Service, “Grain and Feed Annual, Colombia,” USDA Foreign Agricultural Service, apps.fas.usda.gov. For the South America insect feed market, this creates room for low-inclusion use cases where performance can be tested without forcing a full reformulation. That is why poultry and swine adoption is moving through practical trial phases before broad replacement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price gap versus soybean meal and fishmeal | -4.2% | Regional, especially Brazil, Argentina, and Colombia | Short term (≤ 2 years) to Medium term (2-4 years) |

| Regulatory inconsistency across feed and organic waste rules | -2.3% | Brazil, Argentina, Chile, and Colombia | Medium term (2-4 years) |

| Seasonal inconsistency in compliant pre-consumer feedstock streams | -1.4% | Brazil, Argentina, Chile | Short term (≤ 2 years) |

| Limited drying and oil-stabilization infrastructure for scale | -1.8% | Ecuador, Argentina, Colombia, and parts of Brazil outside core clusters | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Gap Versus Soybean Meal and Fishmeal

The biggest commercial restraint on the South America insect feed market is still price. Soybean meal remains deeply embedded in regional feed formulas, and it is supported by large domestic production systems that insect producers have not yet matched in scale. The gap narrows when fishmeal markets tighten, but it widens again when conventional protein markets stabilize, making demand more cyclical than steady in some applications. Production systems have improved between 2020 and 2025, but many South American plants are still operating at a scale where automated rearing and processing cannot drive a major cost reset. That keeps the South America insect feed market strongest in premium applications and controlled inclusion rates rather than broad commodity adoption.

Regulatory Inconsistency Across Feed and Organic Waste Rules

The South America insect feed market is also slowed by an advancing regulatory landscape that is not advancing at the same pace across countries. Argentina created its first formal framework for insect-derived feed products through National Service for Agrifood Health and Quality (SENASA) Resolution 1039/2024, which provided the country with a clearer starting point from September 2024. Brazil’s system is more developed in some use cases, but approval of novel feed ingredients can still take 18 to 36 months, which increases time, costs, and planning risks for producers. Colombia has not yet published a dedicated insect feed framework, while Chile uses its own approval process, leaving companies serving several countries with separate compliance paths. Until these rules are better aligned, the South America insect feed market will continue to see uneven commercialization across borders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insect Species: Black Soldier Fly Leads on Scale, Mealworm Gains on Specialization

Black Soldier Fly held 61.6% of the South America insect feed market share in 2025, reflecting its lead in scale, feed conversion, and adaptability to local organic side streams. Mealworm is the fastest-growing species segment, with a 12.9% CAGR through 2031, and its momentum is mainly driven by premium pet food and other higher-value nutrition applications. The South America insect feed market has favored black soldier fly so far because it fits the region’s main applications in aquaculture, poultry, and swine more directly than other species. That lead is also supported by the fact that regional producers such as Cyns and Bioconversión have built their commercial positioning around black soldier fly-based ingredients.

Mealworm is expanding its presence by targeting demand areas that do not directly compete with the primary volume applications of black soldier fly. Insecta Brasil has positioned mealworm-based products for use in fish, bird, swine, and pet nutrition, indicating that this species is carving out a niche in specialized nutrition rather than attempting to replace black soldier fly in bulk feed markets. Crickets continue to occupy a niche role in the South America insect feed market, with greater relevance in pet and novelty products compared to mainstream feed formulations. Houseflies and other insect species remain in the early stages of commercialization, with most advancements limited to pilot projects and selective product development rather than widespread market supply. Consequently, the South America insect feed market is projected to remain focused on black soldier fly for high-volume applications, while mealworm continues to grow in segments where premium buyers can sustain its pricing.

By Product Form: Protein Meal Anchors Revenue, Insect Oil Accelerates

Protein Meal accounted for 57.5% of the South America insect feed market in 2025, confirming that it remains the core commercial format across aquaculture, livestock, and pet food. Whole Dried Larvae serve smaller but relevant channels such as reptiles, ornamental birds, ornamental fish, and specialty pet products, where whole-form presentation still carries value. Insect oil is the fastest-growing product form, with a 11.8% CAGR through 2031, and demand is coming from aquafeed and pet food buyers seeking functional fats with a lower environmental burden than some conventional alternatives. Food for the Future’s March 2025 announcement on insect larvae oil in Chilean salmon diets gave the South America insect feed market its clearest commercial example of oil moving beyond the concept stage[4]Source: Food for the Future, “Nuevo Hito, El Salmón Chileno Incorpora Aceite de Larvas de Insectos en Su Dieta,” Food for the Future, f4f.cl.

Frass fertilizer currently generates less revenue compared to feed ingredients. However, its strategic importance surpasses its current sales contribution. In May 2025, Food for the Future and Anasac introduced a frass-based bio-stimulant in Chile, while Insect Protein launched a Class A Tenebrio molitor frass fertilizer in Brazil in September 2024. These developments highlight the trend of producers adopting multi-output business models. For the South America insect feed market, this indicates that product-form competition extends beyond meal and oil, as frass continues to enhance the economic viability of integrated insect production facilities.

By Animal Type: Aquaculture Drives Volume, Poultry Drives Growth Rate

Aquaculture accounted for 43.5% of the South America insect feed market in 2025, making it the largest application by revenue. Chilean salmon and Ecuadorian shrimp offer a natural entry point for the South America insect feed market, as both sectors are export-oriented, technically advanced, and under pressure to strengthen feed sourcing standards. The Food and Agriculture Organization (FAO) reported substantial export values for Chilean and Ecuadorian aquatic products, underscoring the regional importance of ingredient shifts across these value chains. In 2025, the partnership between InnovaFeed, BioMar, and Auchan in Ecuador further highlights that aquaculture remains the most immediate commercial pathway for insect meal adoption, particularly when buyers can align performance, sustainability, and export positioning.

The poultry segment is the fastest-growing application, with a 13.7% CAGR through 2031, driven by soy diversification needs in Brazil, Argentina, and Colombia. The swine segment is moving more gradually because integrators are still testing inclusion rates and performance before committing larger procurement volumes. Pet food remains smaller in volume, but it gives the South America insect feed market some of its highest-value opportunities because premium formulas can absorb ingredient costs that commodity feed cannot. Launches in 2025 by Hill’s in Brazil, Special Dog in Brazil, and Circular Pet in Chile showed that commercial pet food demand has already moved beyond early-stage trials. Other animal feed remains small, but it gives regional producers a steady outlet during capacity ramp-up and helps them balance volumes before larger contracts build.

Geography Analysis

Brazil is the largest geography in the South America insect feed market, accounting for 47.3% of the market share in 2025. The country produced 86.6 million metric tons of commercial feed in 2024, making it the world’s third-largest feed producer and providing the South America insect feed market with its broadest downstream demand base. Brazil’s fish farming output exceeded 1,011,540 metric tons in 2025, and tilapia accounted for 70.0% of that total, or 707,495 metric tons, which explains why aquaculture is such a strong demand center for insect ingredients[5]Source: Alltech, “2025 Agri-Food Outlook, 14th Annual Global Feed Production Survey,” Alltech, aquafeed.com. Regulatory approval for the use of black soldier flies in poultry, swine, and aquaculture has also given Brazil a more practical path to commercialization than some neighboring markets.

Argentina is the fastest-growing market in the South America insect feed market, with a 11.5% CAGR through 2031, and its biggest recent step was National Service for Agrifood Health and Quality (SENASA) Resolution 1039/2024, which created the first national framework for insect-derived feed products from approved species. Chile follows closely, with its position strengthened by the commercialization of insect oil in salmon feed and frass-based bio-stimulants, making it one of the region’s most integrated operating markets. Colombia is also anticipated to witness strong growth, driven by an expanding aquaculture base and continued reliance on conventional feed inputs such as grains and soy. The Rest of the South America region is projected to grow steadily, with Ecuador standing out for its strong presence in shrimp feed and for the development of black soldier fly meal production capacity.

The regional pattern shows that the South America insect feed market is not developing evenly, and country readiness still depends on the mix of regulation, local substrate availability, and nearby high-value animal protein chains. Brazil has the strongest combination of feed scale, aquaculture growth, and investor activity, while Chile has moved fastest in linking insect protein, insect oil, and frass into commercial channels. Argentina now has a stronger legal foundation for expansion, but it still needs greater operational depth before it can narrow the gap with Brazil and Chile. Colombia and the rest of the region offer meaningful upside, but they are still earlier in the commercialization path, leaving the South America insect feed market concentrated in a small number of national demand centers.

Competitive Landscape

The South America insect feed market remains fragmented in 2025, with a few prominent regional players and numerous smaller producers operating at a non-industrial scale. Food for the Future, Cyns, Insecta Brasil, and Protin Biotech are among the most visible names because they represent different species choices, different product mixes, and different commercialization routes. Food for the Future has taken one of the broadest approaches by working across protein meal, insect oil, and frass-based products, which gives it exposure to aquafeed, agricultural inputs, and related specialty channels. Cyns and Bioconversión have stayed closer to black soldier fly-based scale-up opportunities, while Insecta Brasil and Protin Biotech show how specialized nutrition and smaller commercial niches can still find a place in the South America insect feed market.

The South America insect feed market also feels the influence of global benchmark companies, but mostly through partnerships, product examples, and technology references rather than direct large-scale production assets in the region. InnovaFeed’s September 2025 partnership with BioMar and Auchan for Ecuadorian shrimp feed is the clearest case, because it linked a European producer to a South American aquaculture chain through a commercial feed program. Such developments are significant because the South America insect feed market remains at an early stage of development, allowing international benchmarks to influence customer expectations regarding product quality, sustainability standards, certification, and production scalability.

White-space opportunities remain clear in the South America insect feed market. Frass commercialization is still underdeveloped outside a few visible cases, and oil extraction and stabilization capacity are even more limited, despite insect oil being the fastest-growing product form. Colombia and several smaller South American countries still lack a regionally headquartered producer with clear operating scale, leaving room for Brazil- or Chile-based firms to expand first. At the same time, the restructuring seen in benchmark names such as EnviroFlight within Darling Ingredients’ 2025 results is a reminder that scale economics remain difficult, so competitive progress in the South America insect feed market is likely to come through staged expansion and targeted applications rather than large speculative buildouts.

South America Insect Feed Industry Leaders

Food for the Future

Cyns

!nsect Protein

Insecta Brasil

Protin Biotech

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: InnovaFeed SAS, BioMar, and Auchan announced a tripartite commercial partnership to integrate black soldier fly insect protein meal into commercial shrimp feed in Ecuador at scale, the first end-to-end insect meal supply chain in South American aquaculture, connecting InnovaFeed's Nesle production in France to BioMar's Ecuadorian feed mill and through to Auchan's European retail responsible sourcing program.

- May 2025: Food for the Future and Anasac launched a commercial frass-based bio-stimulant product incorporated into Anasac Jardín substrates, available through Easy and Sodimac retail chains in Chile, the first insect frass product to reach national mass-market retail distribution in South America.

- March 2025: Food for the Future confirmed the incorporation of insect larvae oil into Chilean salmon diets at a commercial scale, marking the first documented commercial insect oil deployment in South American salmon aquafeed.

South America Insect Feed Market Report Scope

Insect feed consists of animal nutrition products made from farmed insects, serving as sustainable substitutes for traditional feed ingredients such as fishmeal and soybean meal. These products are produced by rearing insects on organic byproducts and processing them into nutrient-dense outputs for use in livestock and aquaculture.

The South America Insect Feed Market is Segmented by Insect Species (Black Soldier Fly, Mealworm, Housefly, and Others), by Product Form (Protein Meal, Whole Dried Larvae, Insect Oil, and Frass Fertilizer), by Animal Type (Aquaculture, Poultry, Swine, Ruminants, and Pets), and by Geography (Brazil, Argentina, Chile, Colombia, and Rest of South America). The Report Offers the Market Size and Forecasts in Terms of Value (USD).

| Black Soldier Fly |

| Mealworm |

| Housefly |

| Others |

| Protein Meal |

| Whole Dried Larvae |

| Insect Oil |

| Frass Fertilizer |

| Aquaculture |

| Poultry |

| Swine |

| Ruminants |

| Pets |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Rest of South America |

| By Insect Species | Black Soldier Fly |

| Mealworm | |

| Housefly | |

| Others | |

| By Product Form | Protein Meal |

| Whole Dried Larvae | |

| Insect Oil | |

| Frass Fertilizer | |

| By Animal Type | Aquaculture |

| Poultry | |

| Swine | |

| Ruminants | |

| Pets | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the 2031 outlook for insect feed in South America?

The South America insect feed market is forecast to reach USD 189.30 million by 2031 from USD 100.50 million in 2026, growing at a 13.50% CAGR.

Which application generates the most demand in this space?

Aquaculture leads with 43.5% of 2025 regional value, supported by Chilean salmon, Ecuadorian shrimp, and Brazilian tilapia demand.

Which insect species is most widely used in feed products?

Black Soldier Fly is the leading species, with 61.6% of market value in 2025, because it fits aquaculture, poultry, and swine applications well.

Which country is leading adoption across South America?

Brazil is the largest country market which accounted for 47.3% share in 2025, supported by feed scale, aquaculture growth, and regulatory progress.

Why is poultry feed projected to grow faster than other animal types?

Poultry Feed is forecast to expand at 13.7% CAGR through 2031 because integrators are looking to diversify protein sources and reduce reliance on soy-heavy formulas.

What is the biggest barrier to wider commercial use?

The largest constraint remains the price gap versus soybean meal and fishmeal, which keeps insect ingredients most competitive in premium and selective inclusion use cases.

Page last updated on: