North America Insect Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

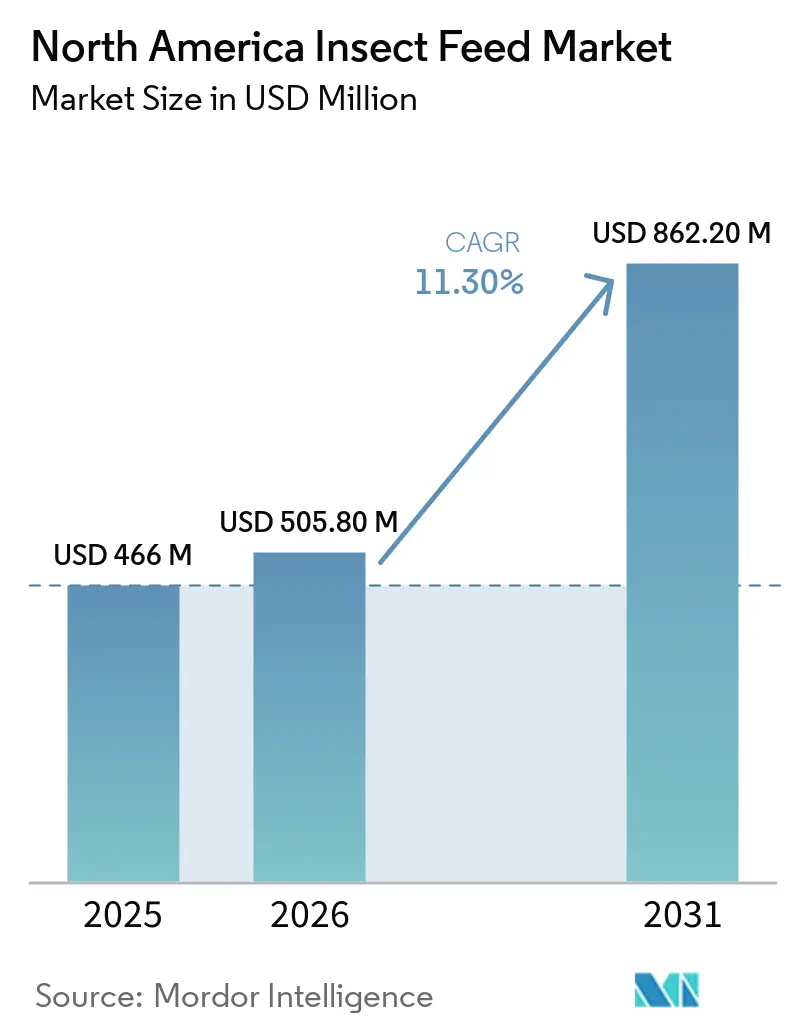

| Base Year Market Size (2025) | USD 466 Million |

| Market Size (2026) | USD 505.80 Million |

| Market Size (2031) | USD 862.20 Million |

| Growth Rate (2026 - 2031) | 11.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Insect Feed Market Analysis by Mordor Intelligence

The North America insect feed market size reached USD 466.0 million in 2025 and is projected to expand from USD 505.8 million in 2026 to USD 862.2 million by 2031, registering a CAGR of 11.3% during the forecast period (2026 - 2031). Regulatory progress in the United States and Canada has moved the North America insect feed market beyond a niche ingredient position and into a more defined commercial protein category with clearer end-use boundaries. Demand in the North America insect feed market is now supported by measurable off-take drivers rather than early-stage sustainability positioning alone, which has improved the case for repeat procurement by feed formulators. Commercial opportunity is strongest where regulatory approvals, premium protein demand, and traceable supply needs now overlap, especially in aquaculture and companion animal nutrition. At the same time, paused projects, restructuring activity, and the high cost of automated plant buildouts show that supply-side economics remain the main factor shaping how quickly the market can move toward its 2031 potential.

Key Report Takeaways

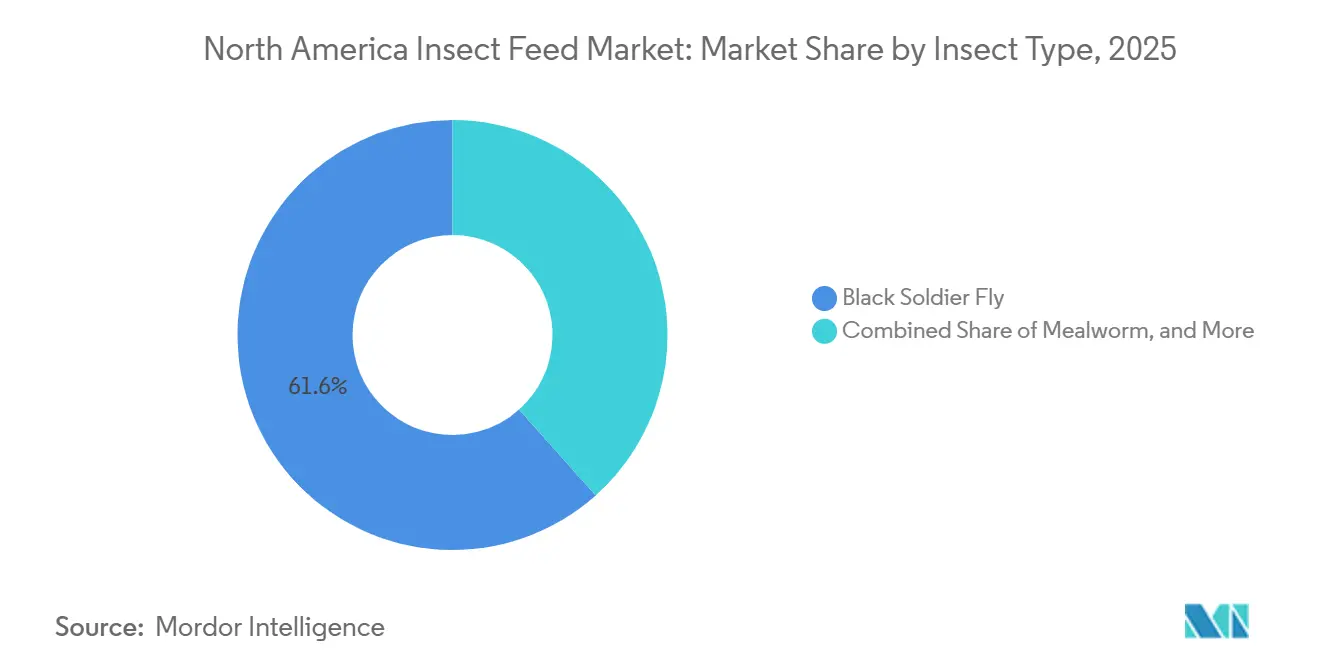

- By insect type, black soldier fly larvae led with 61.6% of the North America insect feed market size, while mealworms are forecast to expand at a 17.0% CAGR through 2031.

- By product form, insect meal accounted for 57.6% North America insect feed market share in 2025, while insect oil is advancing at a 16.9% CAGR through 2031.

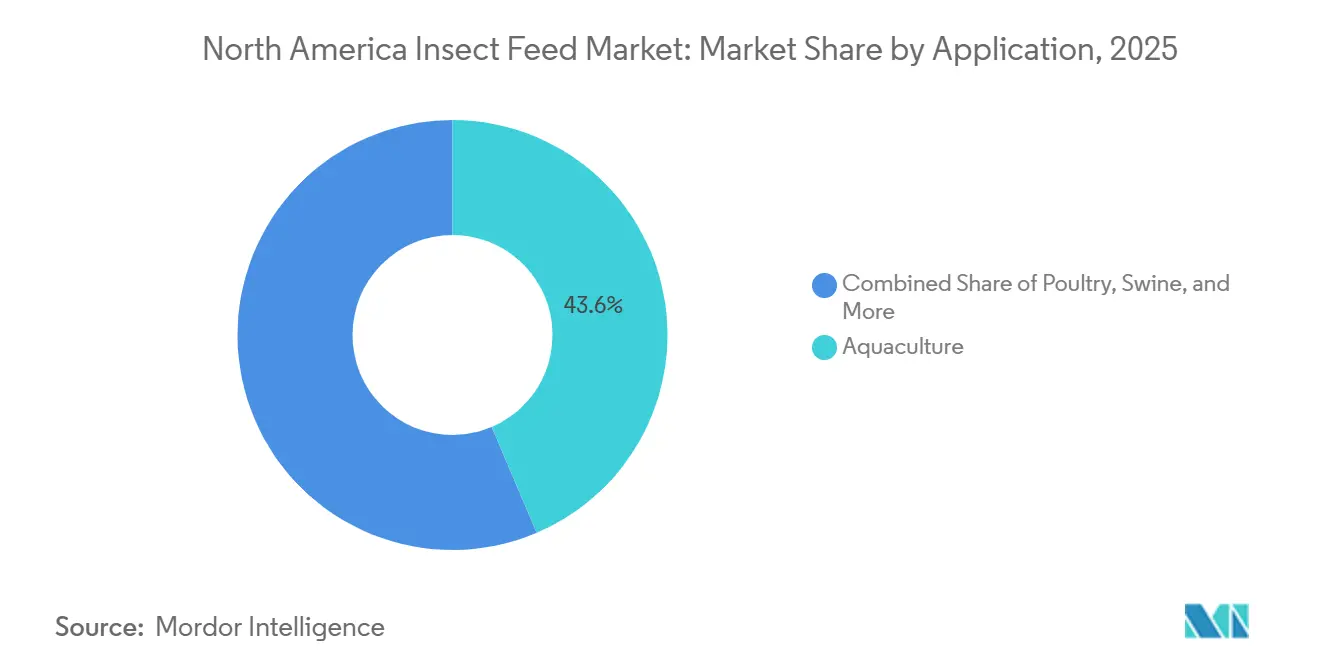

- By application, aquaculture held 43.6% of 2025 demand, while pet food is projected to grow above 16.0% annually through 2031.

- By end user, commercial feed mills represented 47.8% of 2025 demand, while integrated livestock producers are projected to grow at a 13.0% CAGR through 2031.

- By geography, the United States remained the largest market in 2025 with a share of 76%, while Canada recorded the highest projected CAGR at 12.9% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Insect Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AAFCO and CFIA approvals expanding permitted feed use | +2.5% | US and Canada | Short term (≤ 2 years) |

| Fishmeal and soybean meal volatility supporting substitution | +2.0% | Global, strongest pull in US and Canada aquaculture | Medium term (2-4 years) |

| Aquaculture feed formulators seeking domestic fishmeal alternatives | +1.8% | US and Canada | Medium term (2-4 years) |

| Premium pet food demand for hypoallergenic proteins | +2.2% | US and Canada | Short term (≤ 2 years) |

| Co-location with food and corn-processing side streams improving unit economics | +1.0% | US Midwest and Canada | Long term (≥ 4 years) |

| Frass monetization improving full-plant returns | +0.8% | US and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AAFCO and CFIA Approvals Expanding Permitted Feed Use

The pace of regulatory approvals remains the most operationally important growth driver in the North America insect feed market. Association of American Feed Control Officials (AAFCO) approved Black Soldier Fly Larvae (BSFL) tentative definition T60.117 in February 2024, which permitted use in salmonid, poultry, swine, and adult companion-animal food, and it also approved dried mealworm meal for adult dog food in January 2024 as the first mealworm-specific feed definition. Canada then introduced the Feeds Regulations 2024 in July 2024, which updated the national framework and simplified parts of the registration process for insect ingredient submissions. Each approval creates a new round of formulation work at commercial feed mills, so adoption tends to happen through repeat procurement cycles rather than a single purchasing decision. That pattern supports steady demand building in the North America insect feed market because each species and application approval opens another defined commercial lane. Canada’s Bill C-273, introduced in April 2026, adds another layer to this theme because provisional registration within 90 days for ingredients already approved in 2 or more jurisdictions could shorten commercialization timelines and strengthen Canada’s regulatory position.

Fishmeal and Soybean Meal Volatility Supporting Substitution

Price volatility in conventional feed proteins is giving the North America insect feed market a stronger economic footing than it had in earlier years. Global fishmeal prices reached USD 1,992 per metric ton in March 2026, up 40.9% year on year, while soybean meal stood at USD 312 per metric ton at the same point. This gap matters because it makes insect meal more relevant as a hedge for buyers exposed to fishmeal swings, even if insect meal still carries a premium to soy in many rations. FAO documented how El Niño-related anchovy quota reductions in Peru cut catches by 28% in 2023, which showed how quickly marine protein supply can tighten under climate stress. USDA market data from May 2026 also showed soybean meal at 46.5-48% protein trading at USD 315-360 per metric ton in U.S. corn-belt markets, so the soy benchmark remains difficult for insect meal to match on price alone[1]Source: USDA Agricultural Marketing Service, “Grain and Oilseed Market News – Soybean Meal 46.5-48%,” USDA AMS, ams.usda.gov. As a result, larger feed buyers are increasingly treating insect meal allocations as part of supply-chain risk management, which supports broader adoption in the North America insect feed market where fishmeal exposure is high.

Aquaculture Feed Formulators Seeking Domestic Fishmeal Alternatives

Aquaculture remains one of the clearest demand anchors for the North America insect feed market because it combines regulatory headroom with strong species-level feeding evidence. Studies published in Sustainable Food Systems and Frontiers in Aquaculture indicate that by 2025, Black Soldier Fly Larvae (BSFL) can replace up to 40% of fishmeal in rainbow trout diets and 25% in red drum diets without negatively impacting growth performance or feed conversion. Research by the United States Department of Agriculture - Agricultural Research Service (USDA-ARS) is also ongoing for species such as catfish and tilapia. In addition, the United States Department of Agriculture (USDA) draft National Aquaculture Development Plan (NADP) recognizes insect meal as an approved alternative to fishmeal for carnivorous fish, providing federal-level regulatory support[2]Source: USDA Agricultural Research Service, “Black Soldier Fly Larvae Evaluation for Catfish and Tilapia; Mealworm Trials for Salmonid,” USDA ARS Annual Research Report, ars.usda.gov. This combination of validated performance, domestic sourcing potential, and regulatory backing continues to strengthen the North America insect feed market, particularly in aquaculture feed formulations.

Premium Pet Food Demand for Hypoallergenic Proteins

Premium companion-animal nutrition is giving the North America insect feed market one of its fastest value-growth channels. The United States had 86.9 million pet-owning households in 2024, equal to 66% of all households, which gives premium pet nutrition a large underlying customer base. In this channel, buyers increasingly look for ingredient transparency, single-protein formats, and novel protein claims, which creates a better fit for insect meal than in commodity livestock rations. AAFCO’s August 2024 approval of BSFL oil for adult cat food widened the approved ingredient list for companion-animal applications and lowered formulation risk for new launches. ADM and Innovafeed have been commercializing the Hilucia ingredient brand in North America since 2023, and ADM also developed the Buzz Bar pet treat concept to show how BSFL protein can work in consumer-facing formats[3]Source: ADM, “Innovafeed Expands to US: French Agtech Firm Opens Insect Innovation Center in Decatur,” ADM News, adm.com. Contracts in this segment are likely to favor producers that can deliver consistent purity and traceability standards, which means premium pet food demand can lift the North America insect feed market while also concentrating supply with verified operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Insect meal pricing premium versus conventional proteins | -3.5% | Global, most acute in US commodity feed | Short term (≤ 2 years) |

| Species and life-stage approval limits capping addressable demand | -2.8% | US and Canada | Medium term (2-4 years) |

| Preconsumer substrate restrictions and depackaging bottlenecks | -1.2% | US and Canada | Medium term (2-4 years) |

| Capital scarcity for large automated facilities | -1.5% | North America-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Insect Meal Pricing Premium Versus Conventional Proteins

The largest commercial restraint in the North America insect feed market is still the pricing premium of insect meal against conventional proteins. USDA data from May 2026 showed soybean meal at USD 315-360 per metric ton, which stayed well below the cost of commercially produced insect meal. Fishmeal inflation has improved the substitution case in aquaculture, but swine and poultry buyers usually do not face a comparable price shock that would justify broad insect meal inclusion on economics alone. The cost curve for insect production is improving through scale, breeding advances, automation, and substrate integration, but recent setbacks show that this transition remains expensive and uneven. Darling Ingredients reported USD 58.0 million in restructuring and impairment charges in February 2026 related primarily to EnviroFlight and CTH natural casing businesses, which highlighted the pressure on current economics. Until more producers lock in multi-year contracts during favorable pricing windows, the North America insect feed market will continue to face limited penetration in commodity-grade rations.

Capital Scarcity for Large Automated Facilities

Capital availability is a structural limit on how quickly the North America insect feed market can add industrial capacity. Fully automated insect protein plants require large upfront investment, and payback depends on stable substrate access, reliable output quality, and signed offtake. The recent operating pauses and project changes across the region show that demand alone is not enough to guarantee project execution. Darling’s EnviroFlight-related restructuring charges and Protix’s April 2026 halt of the planned Tyson Foods joint venture facility both underscored the financing and return hurdles tied to scale-up. Even where the commercial case is attractive, lenders and equity partners still need proof that plants can run consistently and profitably over time. This means capacity growth in the North America insect feed market is likely to stay selective, with capital favoring operators that can show multi-stream revenue, strong partners, and lower-cost production models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insect Type: BSFL Dominates, Mealworms Gain in Premium Applications

Black soldier fly larvae held 61.6% of North America insect feed market share in 2025, which kept BSFL clearly ahead of all other insect types in the North America insect feed market. Its position is supported by broad substrate versatility, the widest regulatory coverage, and stronger fit with automated production systems than most competing species. AAFCO’s T60.117 approval gave BSFL access to salmonid, poultry, swine, and adult companion-animal uses, which widened its commercial reach in both the United States and Canada. Mealworms are forecast to grow at a 17.0% CAGR from 2026 to 2031, helped by AAFCO’s January 2024 approval for adult dog food, which opened a premium companion-animal route for a new insect species.

BSFL also benefits from a more mature production profile in the North America insect feed industry, which gives buyers greater confidence in continuity of supply. Texas A&M AgriLife introduced the patented BSF Billet technology in January 2026, and the system points to 20-30% productivity gains along with room-temperature larval storage for weeks to months. Mealworms still have a meaningful opening because their value proposition is different from BSFL and more closely tied to premium pet nutrition than to bulk aquaculture volume. Crickets and houseflies remain smaller in scale, but they retain relevance where familiarity, palatability, or species-specific use cases support trial activity in the North America insect feed market.

By Product Form: Insect Meal Leads, Oil Adds a Faster Growth Layer

Insect meal accounted for 57.6% of the North America insect feed market size in 2025, which kept protein concentrate as the largest product form in the North America insect feed market. This lead reflects its clearer regulatory standing, easier fit with existing feed formulation systems, and stronger evidence base across aquaculture and livestock uses. Buyers also value insect meal because its amino acid profile can work well in species-specific formulas where methionine and lysine balance matter. Insect oil is the fastest-growing product form with a 16.9% CAGR through 2031, supported by interest in BSFL lipids that are rich in lauric acid and are now being used for more than simple caloric substitution.

Whole dried insects still serve smaller but visible retail and specialty channels where visual simplicity and direct feeding matter, especially in backyard poultry and some companion-animal formats. The others category includes frass and puree, and both are becoming more commercially relevant as facilities move toward multi-output operating models. Entosystem’s Drummondville site and Innovafeed’s Decatur design both show that producers are structuring plants around protein, oil, and soil amendment rather than one output alone. That shift matters because the North America insect feed industry is increasingly rewarding product-form diversification, not just meal volume, as the basis for plant-level profitability.

By Application: Aquaculture Holds Volume, Pet Food Lifts Value Growth

Aquaculture represented 43.6% of the North America insect feed market size in 2025, making it the largest application in the North America insect feed market. Its leadership comes from a mix of regulatory support, documented fishmeal replacement results, and exposure to volatile marine protein costs. A 2025 study in Aquaculture International showed that BSFL could replace up to 50% of fishmeal in totoaba without compromising growth performance, which added to the broader body of work already in rainbow trout and red drum. Pet food is projected to grow above 16.0% annually through 2031, and that makes it the fastest-growing application because North American buyers continue to favor hypoallergenic, single-protein, and traceable formulations.

Poultry feed demand is expanding, but broad inclusion rates still depend on better economics versus soybean meal. Swine remains even more price sensitive because soy is deeply embedded in North American pig rations, though partial use in premium or organic systems continues to develop. The difference between aquaculture volume and pet food value growth suggests the North America insect feed market is shifting toward applications that pay for traceability and ingredient differentiation. Producers with stronger food-safety systems and closer brand relationships are therefore better positioned than those selling only into bulk ingredient channels.

By End User: Feed Mills Hold Scale, Integrated Producers Accelerate Faster

Commercial feed mills accounted for 47.8% of 2025 demand, which made them the largest end-user group in the North America insect feed market. Their importance comes from scale because they offer producers the clearest route to large and repeat offtake. At the same time, integrated livestock producers are forecast to expand at a 13.0% CAGR through 2031 as poultry and swine operators look for ways to reduce exposure to conventional protein price swings. This shift is important because integrated buyers often evaluate insect inputs not only on formulation cost, but also on supply risk, sourcing control, and long-term procurement flexibility.

Aquaculture farms and hatcheries follow a different pattern because their average order size is lower, but their willingness to pay can be higher when trial data is strong. Pet food manufacturers are also moving from occasional ingredient buying to deeper strategic partnerships, especially where exclusivity can support premium product positioning. NRGene Canada’s MaxBSF announcement in November 2025, which pointed to 50-150% faster growth and production cycles compressed from 14 days to 7-8 days, shows how genetics can improve supply responsiveness for these buyers. Smaller users such as specialty aquaculture operators and backyard poultry buyers remain limited in scale, but they can still provide high-margin outlets that matter within the North America insect feed industry.

Geography Analysis

The United States was the largest country with a market share of 76% in 2025 within the North America insect feed market. Its lead comes from the size of domestic aquaculture and premium pet food demand, and also from the fact that AAFCO remains central to the approval pathway that shapes ingredient commercialization. U.S. aquaculture feed consumption increased significantly, which gives insect ingredient suppliers a meaningful domestic base for fishmeal substitution. U.S. production investment has also been visible in projects such as Chapul Farms’ Jamestown, North Dakota facility and EnviroFlight’s Kentucky base, even though the region has also seen execution pressure in 2025 and 2026.

Cross-border trade still limits how far U.S. producers can extend their scale advantages across the region. USDA APHIS stated in July 2025 that BSFL insect meal shipped from the United States into Canada requires CFIA registration and is approved only for poultry and salmonid use. That requirement acts as a practical trade barrier and protects some room for local Canadian production to develop. Canada is the fastest-growing geography, with a 12.9% CAGR projected through 2031, and the North America insect feed market is increasingly benefiting from Canada’s policy support and production investment.

Canada’s growth is also supported by newer capacity and a more circular-economy policy framing. Oberland Agriscience opened a 108,000 sq-ft commercial BSFL facility near Halifax in November 2024, and CFIA approved its BSFL frass pellets as fertilizer and soil amendment in October 2025. Bill C-273, introduced in April 2026, could further reduce time to market by allowing provisional registration in 90 days for products already approved in 2 or more jurisdictions. Mexico and the Rest of North America are smaller today, but they are projected to grow steadily through 2031, supported by early private investment, mealworm and BSFL projects, and a need for alternatives where fishmeal imports remain expensive.

Competitive Landscape

The North America insect feed market remained fragmented in 2025, with EnviroFlight, Enterra Feed Corporation , Innovafeed SAS, Protix B.V., and Entosystem Inc. together holding significant combined share. No single producer had enough supply depth to serve North American aquaculture or mainstream commercial feed mills as a primary protein vendor across the full region. That fragmentation reflects both the youth of the sector and the difficulty of building reliable automated capacity at scale. It also means the North America insect feed market still has room for regional specialists and niche operators that can win business on substrate access, quality, or premium positioning rather than on scale alone.

Recent events have shown how exposed the competitive set is to plant economics and capital discipline. Darling Ingredients reported USD 58.0 million in restructuring and impairment charges in February 2026 related primarily to EnviroFlight and CTH natural casing businesses. Protix also halted its planned Tyson Foods joint venture facility in April 2026, which removed a major expected source of future BSFL capacity from the U.S. pipeline. Innovafeed suspended its Decatur pilot operations in August 2025, although the company later stated that the pause was strategic rather than a closure and that a full-scale facility with ADM remained planned. These developments show that supply growth has not kept pace with demand potential, which is why smaller operators with lower capital intensity are still able to compete in the North America insect feed market.

The strongest operators are converging around the same competitive model. They seek lower-cost feedstock through co-location, build plants around protein, oil, and frass rather than one output, and use technology to improve yield and handling. Entosystem’s USD 42 million funding round in October 2024 supported expansion and a second commercial BSFL facility, while Innovafeed and ADM opened the North American Insect Innovation Center in Decatur in April 2024 to deepen research and commercialization work. Technology examples also matter because they shape future cost curves, including Entocycle’s optical-dosing trials at EnviroFlight with above 95% dosing accuracy and Texas A&M’s BSF Billet system with 20-30% productivity gains. Together, these moves show that the North America insect feed market is not being defined only by current sales share, but also by which companies can combine process control, multi-stream revenue, and secured substrate supply into a durable operating model.

North America Insect Feed Industry Leaders

EnviroFlight (Darling Ingredients Inc.)

Enterra Feed Corporation

Innovafeed SAS

Protix B.V.

Entosystem Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Canada introduced Bill C-273, proposing provisional feed-product registration within 90 days for insect ingredients already approved in 2 or more jurisdictions, a measure that could materially accelerate commercial market entry for established producers.

- January 2026: Texas A&M AgriLife Research introduced the patented BSF Billet technology, offering 20-30% productivity gains and room-temperature larval storage for weeks to months, with commercial licensing underway for BSFL facilities across North America.

- April 2024: Innovafeed opened its North American Insect Innovation Center in Decatur, Illinois in partnership with ADM, establishing the leading US insect-ingredient research platform at the time.

North America Insect Feed Market Report Scope

Insect feed consists of animal nutrition products made from farmed insects, serving as sustainable substitutes for traditional feed ingredients like fishmeal and soybean meal. These products are produced by rearing insects on organic byproducts and processing them into nutrient-dense outputs for use in livestock and aquaculture.

The North America Insect Feed Market Report is Segmented by Insect Type (Black Soldier Fly, Mealworm, and More), by Product Form (Insect Meal, Insect Oil, and More), by Application (Aquaculture, Poultry, and More), by End User (Commercial Feed Mills, and More), and by Geography (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Black Soldier Fly |

| Mealworms |

| Houseflies |

| Crickets |

| Others |

| Insect Meal |

| Insect Oil |

| Whole Dried Insects |

| Others |

| Aquaculture |

| Poultry |

| Swine |

| Pet Food |

| Other Animal Feed |

| Commercial Feed Mills |

| Integrated Livestock Producers |

| Aquaculture Farms and Hatcheries |

| Pet Food Manufacturers and Others |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Insect Type | Black Soldier Fly |

| Mealworms | |

| Houseflies | |

| Crickets | |

| Others | |

| By Product Form | Insect Meal |

| Insect Oil | |

| Whole Dried Insects | |

| Others | |

| By Application | Aquaculture |

| Poultry | |

| Swine | |

| Pet Food | |

| Other Animal Feed | |

| By End User | Commercial Feed Mills |

| Integrated Livestock Producers | |

| Aquaculture Farms and Hatcheries | |

| Pet Food Manufacturers and Others | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is driving growth in North America insect feed demand through 2031?

Growth is being supported by regulatory approvals in the United States and Canada, fishmeal price inflation, stronger aquaculture use cases, and premium pet food demand. The market is projected to grow at an 11.3% CAGR.

Which insect type leads sales in North America?

Black soldier fly larvae leads the region with 61.6% of 2025 value because it has broader regulatory approval, better substrate flexibility, and stronger industrial-scale production readiness.

Why is pet food growing faster than some livestock feed uses?

Pet food is growing above 16.0% annually because premium buyers are looking for hypoallergenic and single-protein formulas, and regulatory approvals for insect ingredients in adult companion-animal food have expanded.

Why does aquaculture remain the largest application?

Aquaculture held 43.6% of the 2025 demand because fishmeal price volatility is high, and peer-reviewed studies support partial fishmeal replacement without harming growth performance in several farmed species.

What is holding back wider use in poultry and swine?

The biggest limits are the price premium of insect meal versus soybean meal, unresolved approval gaps across species and life stages, and the difficulty of scaling automated production at lower cost.

Which country offers the strongest near-term growth outlook in the region?

Canada has the highest projected CAGR at 12.9% through 2031, helped by regulatory momentum, operating capacity additions, and stronger support for circular feed models.

Page last updated on: