Insect-Based Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.72 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 10.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

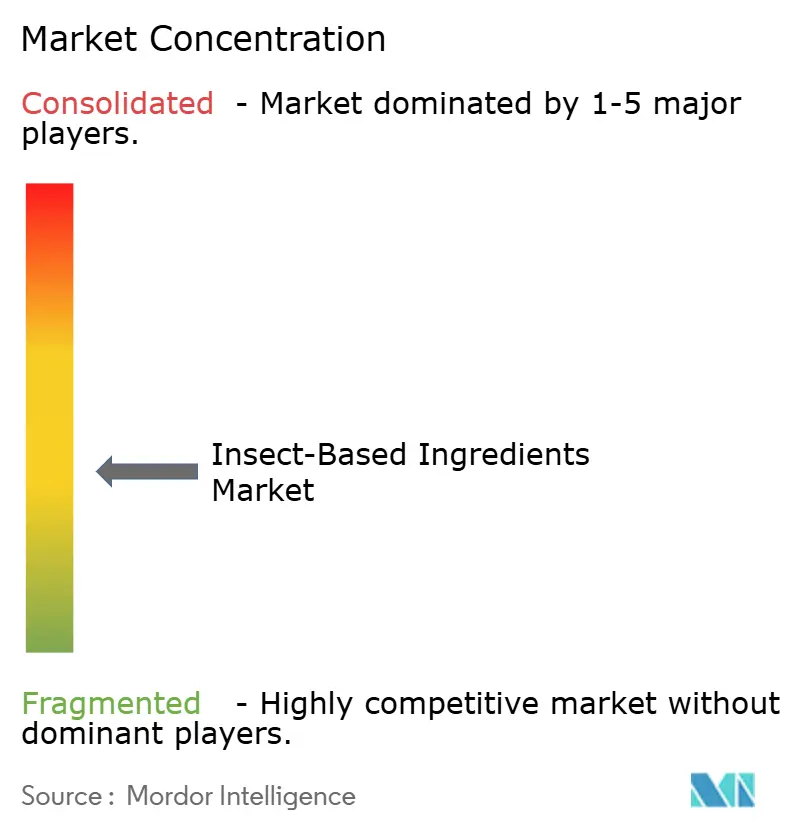

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insect-Based Ingredients Market Analysis by Mordor Intelligence

The insect-based ingredients market reached a market size of USD 0.72 billion in 2026 and is projected to reach USD 1.21 billion by 2031, advancing at a 10.9% CAGR over the forecast period. Accelerated regulatory approvals in Europe, the United States, and Canada have reduced time-to-market for novel insect feed ingredients, opening aquaculture and poultry channels and lifting demand for Black Soldier Fly protein [1]Source: European Food Safety Authority, “Novel Food Approvals,” EFSA.europa.eu. Investors are funneling capital into large-scale, vertically integrated plants that co-locate with grain and food-processing facilities, thereby tapping low-cost residues and lowering feedstock risk. Rising fishmeal price volatility, fishery quota cuts, and sustained pressure to decarbonize animal protein supply chains continue to position insect proteins and functional lipids as cost-competitive, low-carbon alternatives. The insect-based ingredients market is also benefiting from precision livestock farming, where lauric-acid-rich insect oils reduce gut pathogens and limit antibiotic reliance in poultry and swine.

Key Report Takeaways

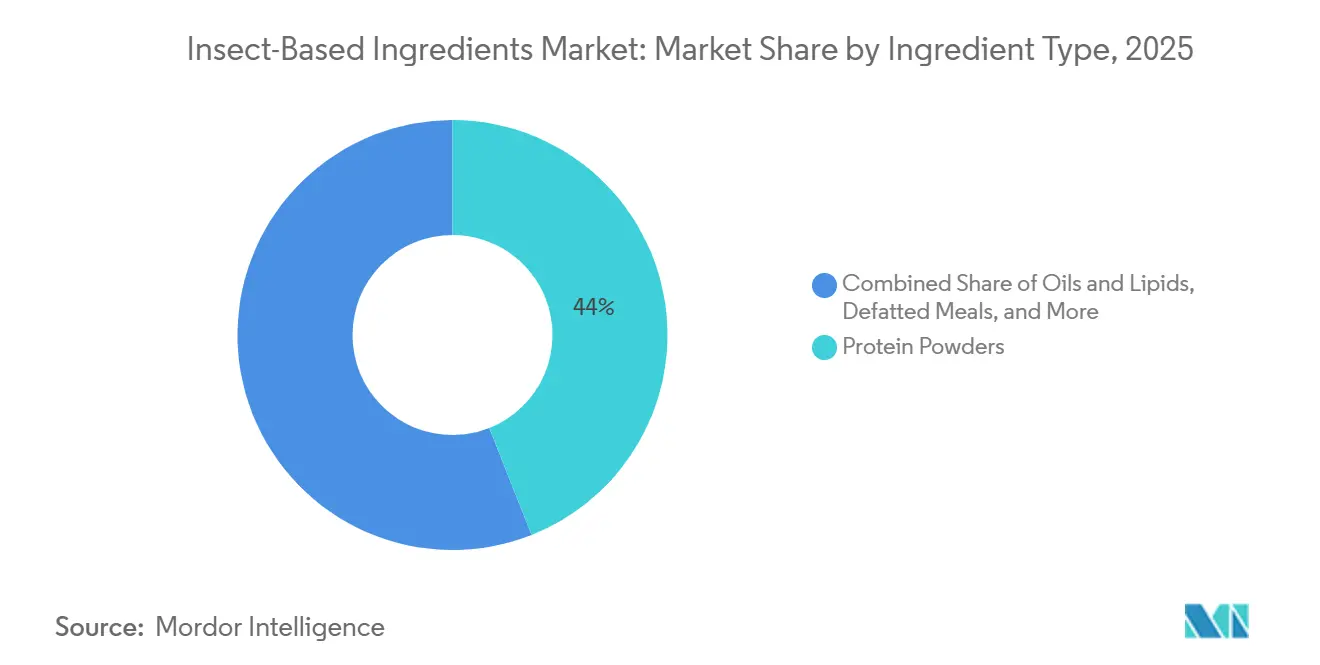

- By ingredient type, protein powders led with 44% share in 2025, while oils and lipids are projected to post the fastest 11.5% CAGR through 2031.

- By application, animal feed captured 47% of insect-based ingredients market share in 2025 and aquaculture feed is forecast to grow at 11.8% CAGR to 2031.

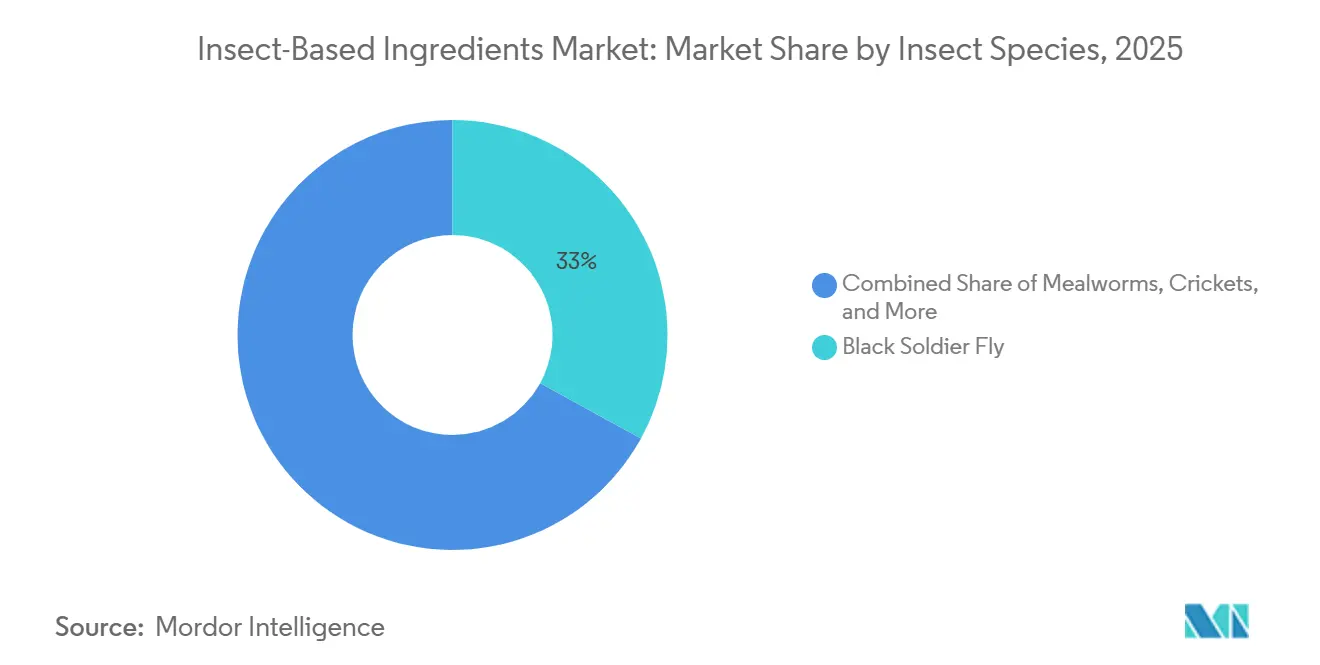

- By insect species, Black Soldier Fly larvae commanded 33% revenue share of insect-based ingredients market size in 2025 and are projected to advance at an 11.7% CAGR through 2031.

- By form, dry formats held 56% revenue share in 2025, whereas liquid concentrates are set to register a 10.1% CAGR during the forecast horizon.

- By geography, Europe led with 32% revenue share in 2025, while Asia-Pacific is projected to expand at the fastest 11.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Insect-Based Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising regulatory acceptance of insect protein in aquaculture and livestock feed | +2.8% | Europe, North America, Asia-Pacific core | Medium term (2–4 years) |

| Cost-competitive alternative to fishmeal and soy protein | +2.5% | Global, higher impact in Asia-Pacific aquaculture belts | Short term (≤ 2 years) |

| Sustainability commitments by global feed producers | +1.9% | Europe, North America, spillover to Asia-Pacific | Medium term (2–4 years) |

| Valorization of insect frass as certified organic fertilizer | +1.2% | Europe, North America, emerging in South America | Long term (≥ 4 years) |

| Growth of precision livestock farming needing functional lipids for gut health | +1.5% | North America, Europe, early adoption in Asia-Pacific | Medium term (2–4 years) |

| Circular-economy partnerships with agri-food by-product generators | +1.3% | Europe core, North America and Asia-Pacific expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Regulatory Acceptance of Insect Protein in Aquaculture and Livestock Feed

Positive scientific opinions from the European Food Safety Authority in 2024 approved Black Soldier Fly protein for salmonids and poultry, broadening earlier aquaculture-only authorizations. In parallel, the United States Food and Drug Administration streamlined data requirements, cutting the review cycle for well-documented dossiers to 18 months, while the Canadian Food Inspection Agency aligned inclusion thresholds for insect meal in aquafeed with European norms [2]Source: United States Food and Drug Administration, “Feed Ingredient Review Process,” FDA.gov. These harmonized rules have triggered multi-year offtake contracts between major feed blenders and insect producers, reducing commercial risk. Clearer guidelines also enable producers to develop multi-species product portfolios instead of pursuing case-by-case exemptions. The regulatory certainty lowers compliance costs, supports facility financing, and accelerates geographic scaling. Consequently, the insect-based ingredients market is moving quickly from pilot to industrial deployment across continents.

Cost-Competitive Alternative to Fishmeal and Soy Protein

Black Soldier Fly meal averaged USD 1.30 per kilogram in European spot trade during 2025, undercutting fishmeal, which fluctuated between USD 1.50 and USD 2.20 per kilogram on Peru anchovy quota swings. Although soybean meal costs less per kilogram, its lower protein content forces higher inclusion rates, eroding cost parity. Peer-reviewed tilapia trials replacing 30% fishmeal with insect meal maintained growth rates and trimmed total feed costs by 12%. Aquaculture clusters in Vietnam and Thailand lifted insect meal use by double-digit percentages in 2025 as operators sought price stability and closer supply chains. Growing economies of scale at plants larger than 10,000-metric-ton capacity are further narrowing unit costs. Taken together, insect protein is transitioning from niche supplement to structural component in commercial feed recipes.

Sustainability Commitments by Global Feed Producers

Feed majors, under pressure to decarbonize supply chains, are hard-wiring insect inputs into procurement plans. Cargill co-located with Innovafeed in Nesle, France, diverting 250,000 metric tons of corn residues annually and lowering Scope 3 emissions by 40,000 metric tons of carbon dioxide equivalent. Archer Daniels Midland plans a 60,000-metric-ton insect plant in Illinois targeting salmon and pet food channels with a cradle-to-gate carbon footprint 75% below fishmeal. Downstream, the Global Salmon Initiative mandates members source at least 10% low-carbon protein by 2030 [3]Source: Global Salmon Initiative, “Low-Carbon Protein Commitment,” GlobalSalmonInitiative.org . Such binding goals translate into predictable, long-term demand that strengthens investor confidence and catalyzes plant financing.

Valorization of Insect Frass as Certified Organic Fertilizer

Insect frass, rich in nitrogen, phosphorus, potassium, and chitin, qualifies as certified organic fertilizer when larvae are fed organic substrates under European Union Regulation 2018/848, allowing premium pricing of USD 1.73 to USD 3.46 per kilogram. Beta Hatch monetizes mealworm frass for greenhouse tomato and cucumber growers willing to pay 25% above compost. Hexafly’s HexaFrass secured distribution through Irish horticultural co-ops in 2024. Because frass can represent up to 30% of total biomass, fertilizer sales meaningfully lift revenue per kilogram of substrate processed and improve overall project payback, strengthening the economic case for large plants.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited industrial-scale capacity below 300,000 metric tons | -1.8% | Global, highest in Asia-Pacific and North America | Short term (≤ 2 years) |

| High capital expenditure per metric ton for automated vertical farms | -1.5% | Global, most binding in high-cost labor markets | Medium term (2–4 years) |

| Regulatory harmonization lag outside Europe and North America | -1.0% | Asia-Pacific, Middle East, Africa, South America | Long term (≥ 4 years) |

| Risk of allergen cross-reactivity with crustaceans | -0.6% | Global, stronger scrutiny in Europe and North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Limited Industrial-Scale Capacity Below 300,000 Metric Tons

Worldwide nameplate capacity reached only 250,000 metric tons in 2025, a fraction of the 1.5 million metric tons of fishmeal consumed annually by aquaculture. Innovafeed’s flagship plant yields 15,000 metric tons of protein meal, and Protix’s Dutch site adds another 15,000 metric tons, leaving formulators supply-constrained. Most aquafeed mills cap insect inclusion at 5% to secure continuity, muting volume growth. New plants take 24 to 36 months from ground-breaking to steady-state output. Capacity scarcity is most acute in Asia-Pacific, where aquaculture exceeds 70 million metric tons but local insect facilities supply less than 50,000 metric tons, forcing reliance on pricier imports.

High Capital Expenditure Per Metric Ton for Automated Vertical Farms

Automated Black Soldier Fly installations demand roughly USD 3,500 per metric ton of annual larvae capacity, three to four times the capital intensity of fishmeal factories. Protix required USD 138 million (EUR 120 million) to triple capacity in Bergen op Zoom, while nextProtein’s Tunisia line consumed USD 20.7 million (EUR 18 million) for just 12,000 metric tons. Payback stretches to eight years in Western Europe because labor, construction, and energy costs run high. These economics deter smaller entrants and slow geographic diversification into markets without abundant venture capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Protein Powders Maintain Scale, Oils Accelerate On Functional Edge

The insect-based ingredients market size for protein powders accounted for 44.0% of total value in 2025, underlining their role as direct fishmeal substitutes. Oils and lipids, although smaller, are forecast to be the fastest-growing slice at an 11.5% CAGR, outpacing defatted meals and frass. Platform producers are optimizing larvae to raise lauric acid content and bundling oil with data on gut health gains to justify premium list prices. Frass emerged as a credible organic fertilizer, particularly in high-value horticulture, raising blended revenue per ton of larvae processed.

Functional differentiation is steering buyers toward insect oils that deliver measurable feed conversion and pathogen control benefits. A broiler trial showing a 5% improvement in feed efficiency catalyzed new demand from European integrators. The insect-based ingredients market share for oils is anticipated to climb as precision livestock farming scales. In contrast, defatted meal finds niche demand in organic poultry operations needing lower fat to curb storage rancidity.

By Application: Aquaculture Feed Dominates Volumes, Pet Food Commands Price Premiums

Aquaculture absorbed 47% of 2025 demand, driven by shrimp, tilapia, and salmon producers replacing volatile fishmeal supplies. This channel is set to expand at an 11.8% CAGR, the strongest within applications, as inclusion caps ease. Poultry feed adoption grows in Europe and Canada, where regulators allow up to 15% Black Soldier Fly meal in broiler rations. Pet food occupies a smaller tonnage yet commands two to three times the price of aquafeed.

The insect-based ingredients market size for aquaculture protein is projected to exceed USD 0.60 billion by 2031, while pet food’s premium positioning supports high margins. Organic certified frass fertilizers sell for 25% above compost, widening producer revenue streams and improving project bankability. Sustainability labeling and consumer preference for novel proteins underpin price resilience in companion animal channels.

By Insect Species: Black Soldier Fly Leads, Mealworms And Crickets Face Scale Bottlenecks

Black Soldier Fly larvae generated 33% of 2025 revenue, reflecting a short 14-day growth cycle, tolerance for diverse substrates, and broad regulatory approval. It is also the fastest-growing species, projected to advance at an 11.7% CAGR through 2031. The insect-based ingredients market share for this species is set to rise further as plants above 30,000-metric-ton capacity come online. Mealworms deliver higher protein percentages but require 10-week cycles and strict climate control, inflating energy costs. Crickets remain a niche for specialty pet food owing to elevated rearing expenses and limited feed approvals.

Execution missteps underscore scaling risk as Ynsect entered restructuring in 2024, and cricket producer Aspire Food Group sought a rescue deal in 2025. By contrast, Innovafeed’s 55,000-square-meter facility processes 250,000 metric tons of by-products and demonstrates Black Soldier Fly scalability.

By Form: Dry Meals Dominate, Liquids Gain Ground Through Automation

Dry protein meals held 56% of 2025 value as they integrate seamlessly into pelleting lines and store up to 18 months. Liquid concentrates, though smaller, are forecast to post a 10.1% CAGR because automated spray systems reduce labor and dosing errors. Paste formats appeal to premium wet-pet-food makers, who seek novel textures and sustainability narratives.

The insect-based ingredients market size for dry formats will keep pace with overall demand, yet liquids will command higher margins per ton due to functional positioning. Protix’s launch of a pumpable oil compatible with broiler spray lines cut labor by 15% and set a benchmark for automation-friendly form factors. Dry defatted meals continue to serve organic broiler producers looking to minimize storage spoilage.

Geography Analysis

Europe led with 32% revenue share in 2025, anchored by clear feed regulations and density of co-located facilities in France and the Netherlands. Positive European Food Safety Authority opinions in 2024 expanded species approvals for salmonids and poultry, locking in steady demand. France hosts both Innovafeed’s 55,000-square-meter Black Soldier Fly site and Ynsect’s mealworm plant, while Dutch incentives have fostered research and commercialization clusters. Regulatory maturity supports growth through 2031, slower than emerging regions but off a higher base.

The Asia-Pacific region is forecast to record the fastest growth at 11.0% CAGR, driven by Vietnam, Thailand, and Indonesia, where shrimp and tilapia producers are integrating insect meal to meet eco-label requirements for exports to Europe and North America. Thailand’s growing production and rapidly scaling Entobel plant underscore regional momentum. China and India lag due to the absence of comprehensive guidelines, although local research pilots are underway. A capacity shortfall means that Asia-Pacific countries still import from Europe, adding freight premiums of USD 0.15 to USD 0.20 per kilogram.

North America, though smaller today, is set to grow on the back of the planned Innovafeed and Archer Daniels Midland facility in Illinois and EnviroFlight’s operational Kentucky plant. Canada aligned feed rules with Europe in 2024, facilitating cross-border trade. Mexico and Brazil are consulting on approvals, and South American growth is anticipated as poultry exporters pilot insect meal to hedge soybean price swings. Middle East and African uptake hinges on faster regulatory clarity and financing for local plants.

Regulatory Landscape

Insect-derived processed animal proteins (PAPs) are regulated most explicitly in Europe, where Regulation (EU) 2017/893 established the legal pathway for using farmed-insect PAP in aquaculture. Subsequent authorizations expanded use beyond aquaculture into poultry and pigs, while feed-ban rules maintain a prohibition for ruminants. Across the EU and the United Kingdom, permitted species for feed applications commonly include Hermetia illucens (Black Soldier Fly), Tenebrio molitor (yellow mealworm), Alphitobius diaperinus (lesser mealworm), and several cricket species, which supports multi-species portfolios for ingredient suppliers.

Compliance is anchored in hygiene and traceability requirements under the EU Animal By-Products framework (EC) No 1069/2009, along with tight substrate restrictions that prohibit inputs such as manure, catering waste, and meat-and-bone meal. This directly shapes feedstock sourcing and facility design. In April 2026, the International Platform of Insects for Food and Feed (IPIFF) published a policy paper advocating clearer treatment of insect frass within the EU Fertilising Products Regulation (including the CMC 10 pathway) and a more formal protein-diversification route within EU livestock strategy, signaling continued regulatory engagement around both feed ingredients and frass commercialization.

Competitive Landscape

The top five companies held a significant share of 2025 revenue, indicating moderate concentration. Innovafeed, Ynsect, and Protix leverage vertically integrated designs that monetize protein, oil, and frass, while regional specialists such as Entobel and Beta Hatch focus on localized supply chains. Investors favor proven operators with contracted offtake, such as Innovafeed’s partnership with Cargill, which brings sustainable and innovative feed options. Protix’s proprietary automation reduces labor by 40% and boosts feed conversion by 15%, supporting expansion into North America.

Strategic blueprints center on low-cost substrate sourcing, automation to reduce operating expenses, and partnerships with major feed brands to secure demand. Patent filings between 2023 and 2025 increased by 35%, covering applications such as machine vision for larval density, odor control, and waste heat recovery. New entrants are piloting modular container systems that slash capital intensity and enable distributed capacity near feedstock sources. Execution stumbles, such as Ynsect’s restructuring and Aspire Food Group’s production cutbacks, highlight scale-up risk and reinforce investor bias toward firms with demonstrated commercial output.

White-space growth lies in functional lipids for antibiotic-free animal production and certified organic fertilizers for greenhouse and horticulture segments. Market dynamics favor firms that can capture dual revenue streams and prove carbon-footprint reductions to corporate buyers.

Insect-Based Ingredients Industry Leaders

Innovafeed

Protix

EnviroFlight (Darling Ingredients)

Sentara Group

Ynsect

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial whitespace is emerging in scaling models that reduce the capital burden of fully integrated sites and improve supply reliability for feed formulators. In March 2026, REPLOID Group AG opened its first Steinberger ReFarmUnit in Burghausen, Germany, highlighting a decentralized approach to larvae rearing using local organic residues. Then in July 2026, Nasekomo opened an automated Black Soldier Fly reproduction facility in Bulgaria designed to supply neonate larvae to industrial producers, separating breeding from grow-out to strengthen upstream capacity and genetics control.

Large-scale capacity additions and commercialization milestones also support broader adoption in aquafeed and pet food channels, where buyers seek contracted volume and consistent specifications. Innovafeed reported in June 2026 that it completed the industrialization phase at Nesle, France, alongside securing EUR 51 million to move into commercial deployment. NextProtein raised EUR 18 million (Series B) in June 2026 tied to building a 12,000-ton-per-year facility in Tunisia. On the mealworm side, Tebrio commenced production at its oFarm facility in October 2025, reinforcing the shift toward commodity-scale output. Regulatory clarity in Europe underpins ingredient approvals for aquaculture and monogastrics, and it keeps frass monetization in scope where organic and EU fertilizer frameworks provide a route to market.

Recent Industry Developments

- May 2026: EnviroFlight highlighted published poultry research showing broiler diets with 2.5% and 5.0% Black Soldier Fly larvae inclusion improved feed conversion. The results reinforce the functional-performance case for insect ingredients in poultry rations and support broader formulation trials beyond aquaculture.

- September 2025: Innovafeed, BioMar, and Auchan Retail announced collaboration to integrate insect protein into commercial shrimp feed in Ecuador. Pairing an insect ingredient supplier with an aquafeed major and a retail partner advances end-to-end commercialization and helps translate sustainability claims into marketable shrimp value chains.

- January 2024: The European Investment Bank signed a EUR 37 million loan agreement with Protix under InvestEU to support scaling sustainable protein production capacity. This type of institutional financing improves bankability for capital-intensive insect facilities and can accelerate industrial capacity build-out where regulatory pathways are established.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers insect-derived ingredients produced, processed, and sold as inputs, mainly for animal nutrition and crop production. The sizing tracks the value of ingredient sales across major regions, with values counted at the ingredient level and not at the final product level.

Scope exclusions: We do not include finished consumer foods where insects are only a minor recipe component, or unrelated sustainable proteins that are not insect-derived.

Segmentation Overview

- By Ingredient Type

- Protein Powders

- Oils and Lipids

- Defatted Meals

- Frass (Organic Fertilizer)

- By Application

- Animal Feed

- Aquaculture Feed

- Poultry Feed

- Pet Food

- Agriculture Fertilizers

- Animal Feed

- By Insect Species

- Black Soldier Fly

- Mealworms

- Crickets

- Others

- By Form

- Dry

- Liquid

- Paste

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping the supply chain for insect proteins, oils, and frass, then aligning it with how animal feed and fertilizer demand is reported publicly. We referenced public sources such as FAO statistics, USDA data releases, Eurostat tables, and European Commission documentation on novel food and feed rules, since these help explain adoption timing by region and end use.

Next, we added repeatable market signals, including aquaculture output trends, poultry and pet food production indicators, and trade and customs reporting where relevant. Company annual reports, investor presentations, and reputable press were also used to understand capacity additions and shifts in product mix, and selected paid databases were used for company financials, patent activity, and shipment-level import and export validation. These sources are not exhaustive, and we reviewed other public references to compile the dataset, confirm assumptions, and identify gaps that needed follow-up.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with ingredient producers, feed formulators, distributors, and downstream users in livestock, aquaculture, and pet nutrition. We balanced coverage across major regions so adoption drivers, pricing logic, and regulatory timing could be cross-checked, then rechecked final assumptions when desk sources and field feedback did not align.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 16% | APAC: 43% |

| Mid tier: 46% | Functional/Unit leaders: 37% | EMEA: 31% |

| Smaller Players: 22% | Managers: 47% | Americas: 26% |

Market-Sizing & Forecasting

The core model uses a top-down approach where regional demand pools are reconstructed from animal production and feed-use patterns, and then filtered by realistic adoption rates for insect meal, insect oil, and frass-based inputs. After building the demand side totals, we corroborate them with selective bottom-up checks, including capacity and utilization roll ups for key producing regions and sampled pricing by ingredient form to confirm implied revenue levels.

Inputs used in the model include aquaculture and poultry output trends, fishmeal and soy meal price movements as reference substitutes, regulatory approval timing for insect use in feed and agriculture, announced capacity additions and ramp-up timelines, and average selling price progression by form (dry meal, oils, and paste). Forecasting is run using scenario analysis, where optimistic and conservative adoption paths are tested. The selected case is the one that best matches expert expectations and the observed pace of commercialization. Where bottom-up signals are incomplete, we use proxy utilization ranges and conservative yield assumptions, and then revisit these assumptions during primary validation.

Data Validation & Update Cycle

Outputs are checked against independent market signals such as reported production expansions, demand commentary from feed value chain participants, and observed pricing ranges, and then the main variances are investigated before sign-off. If a region shows an unusual jump in implied consumption or pricing, we revisit the adoption and mix assumptions and, when needed, re-contact a small set of respondents to confirm what changed.

Each report is refreshed annually, and interim updates are triggered when material events occur, such as a new approval, a major capacity start-up, or a sharp change in substitute ingredient prices. Before delivery, an analyst completes a fresh pass across the model and key assumptions so clients receive the most current view available.

Mordor Intelligence's Insect Based Ingredients Market Estimate Compared With Other Published Estimates

Published market sizes for insect-based ingredients do not always match because the counted products and end uses can shift between studies. Differences also come from the year used for pricing, the adoption curve assumed for feed and agriculture, and how aggressively capacity ramps are converted into sales.

Some sources appear to roll up a wider alternative protein theme or include more end uses like broader human food ingredients and nutraceutical inputs. In Mordor Intelligence sizing, the value is kept at the ingredient level for insect-derived inputs used in animal nutrition and crop production (including frass), and the assumptions are rechecked using adoption timing and pricing feedback gathered directly from the supply chain.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.72 B (2026) | |

| Global Consultancy A | USD 1.73 B (2024) | Uses an earlier base year with a higher starting value, and the scope is typically broader across insect ingredient uses, which can pull in adjacent human nutrition and other non-core revenue pools. |

| Market Analytics Group B | USD 1.90 B (2024) | Often reflects a broader definition that may count more insect-derived products and applications in the total, and the pricing and adoption assumptions can be less traceable to feed and fertilizer demand indicators. |

The table shows that most of the spread is explained by scope choices and base-year starting points, not small math differences. By keeping the included use cases clearly tied to feed and crop input demand, and then validating price and adoption assumptions through repeatable checks, our estimate is easier to reconcile with real commercialization activity.

Key Questions Answered in the Report

How large is the insect-based ingredients market in 2026?

The market reached USD 0.72 billion in 2026.

What compound annual growth rate is forecast through 2031?

A robust 10.9% CAGR is projected.

Which insect species generates the highest revenue?

Black Soldier Fly larvae produced 33% of 2025 revenue and remains the fastest-growing species.

Why are feed producers interested in insect oils?

Lauric-acid-rich oils improve gut health and feed conversion, aiding antibiotic-free production.

Which region is projected to expand the fastest?

Asia-Pacific is set to grow at an 11.0% CAGR, driven by shrimp and tilapia aquaculture.

How does insect frass contribute to revenue?

Certified organic frass sells at a 25% premium over compost and can represent up to 30% of plant output.

Page last updated on: