Europe HR Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

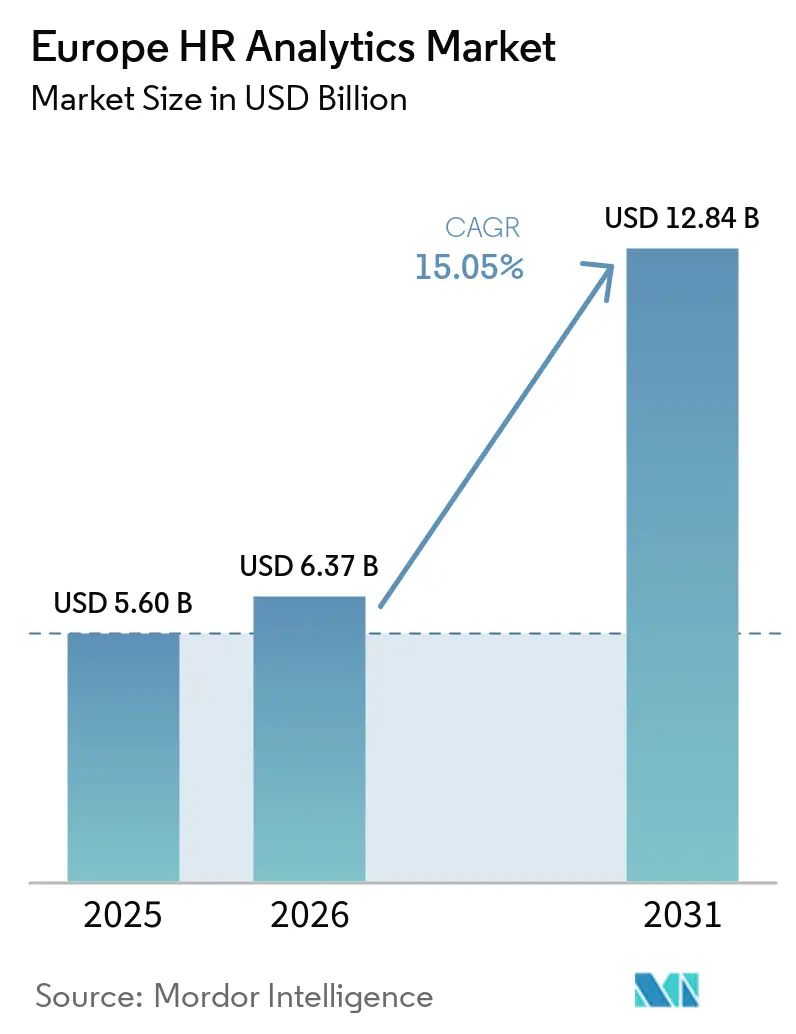

| Base Year Market Size (2025) | USD 5.60 Billion |

| Market Size (2026) | USD 6.37 Billion |

| Market Size (2031) | USD 12.84 Billion |

| Growth Rate (2026 - 2031) | 15.05% CAGR |

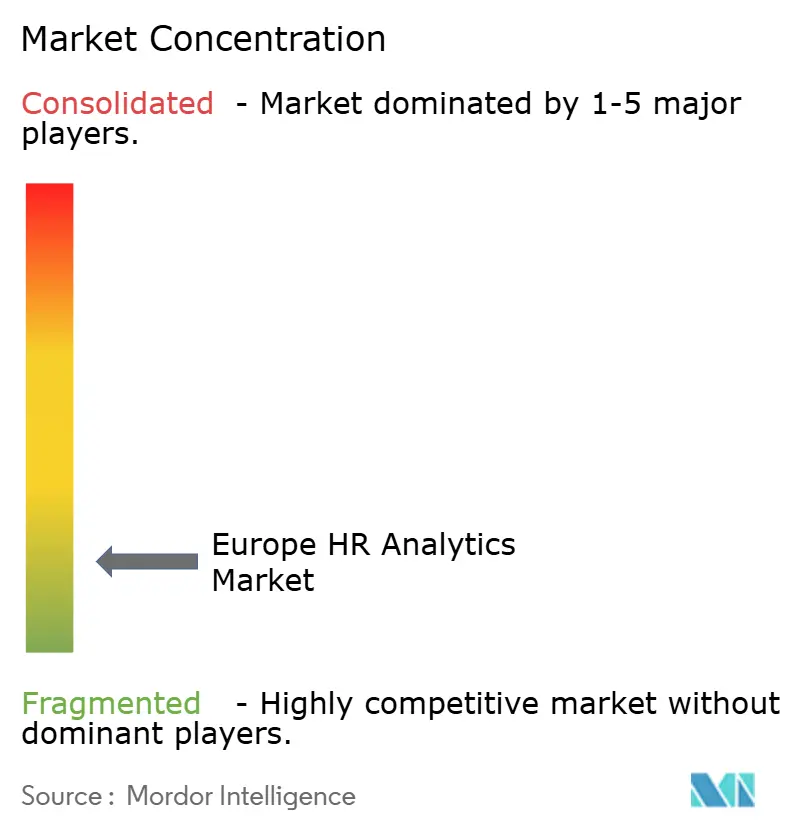

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe HR Analytics Market Analysis by Mordor Intelligence

The Europe HR Analytics market size is projected to be USD 5.60 billion in 2025, USD 6.37 billion in 2026, and reach USD 12.84 billion by 2031, growing at a CAGR of 15.05% from 2026 to 2031. The market is moving forward because labor regulations, cloud adoption, and AI-enabled workforce intelligence are changing how employers manage hiring, compensation, skills, and retention. The June 2026 deadline for transposing the EU Pay Transparency Directive, together with persistent skills shortages across occupations, has made analytics a practical requirement for many employers rather than a discretionary software upgrade. This shift is also changing spending patterns, as many organizations now need integration, advisory, and data governance support in addition to software licenses. Competition is tightening as European specialists build stronger AI layers and global platforms expand sovereign data hosting to meet regional compliance expectations. The European HR analytics market also has room to widen further as SMEs, public bodies, and regulated sectors move from manual reporting toward structured analytics platforms.

Key Report Takeaways

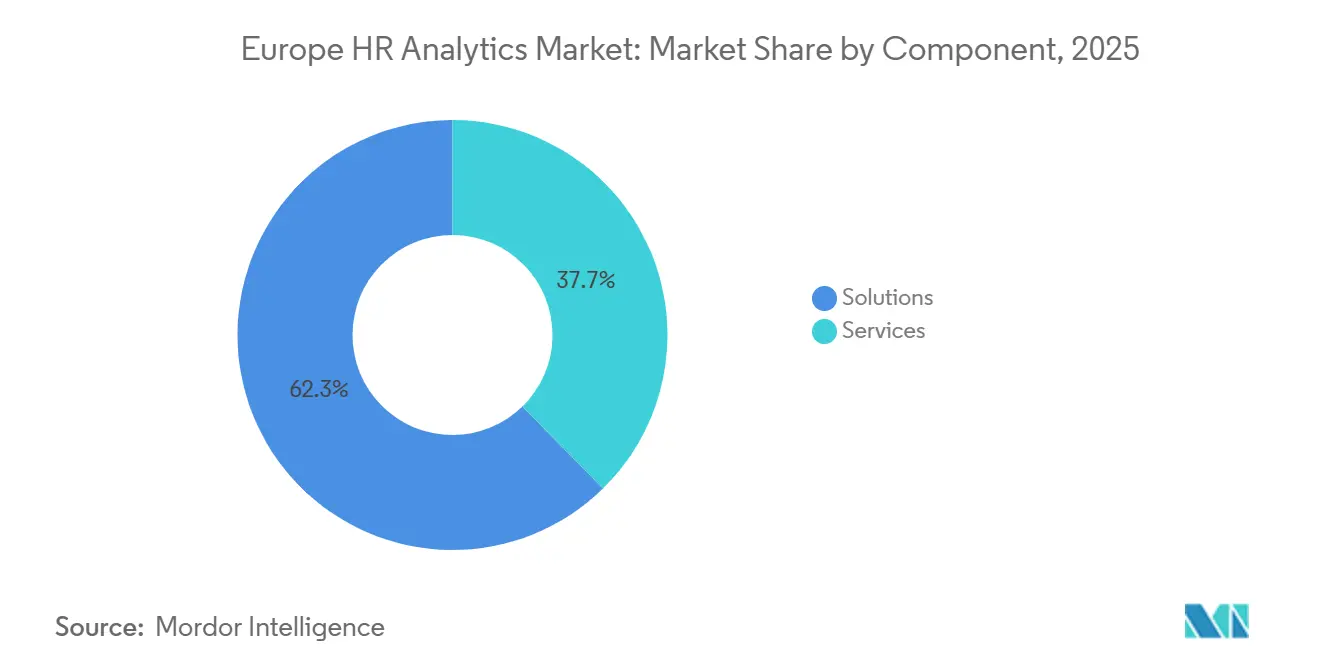

- By component, solutions held 62.37% share in 2025, while services are projected to expand at a 16.94% CAGR through 2031 in the Europe HR Analytics market.

- By deployment mode, cloud accounted for 68.41% of the market share of the European HR Analytics market in 2025, while hybrid is projected to grow at a 17.86% CAGR through 2031.

- By end-user enterprise size, large enterprises held 64.12% share in 2025, while SMEs are projected to advance at an 18.73% CAGR through 2031.

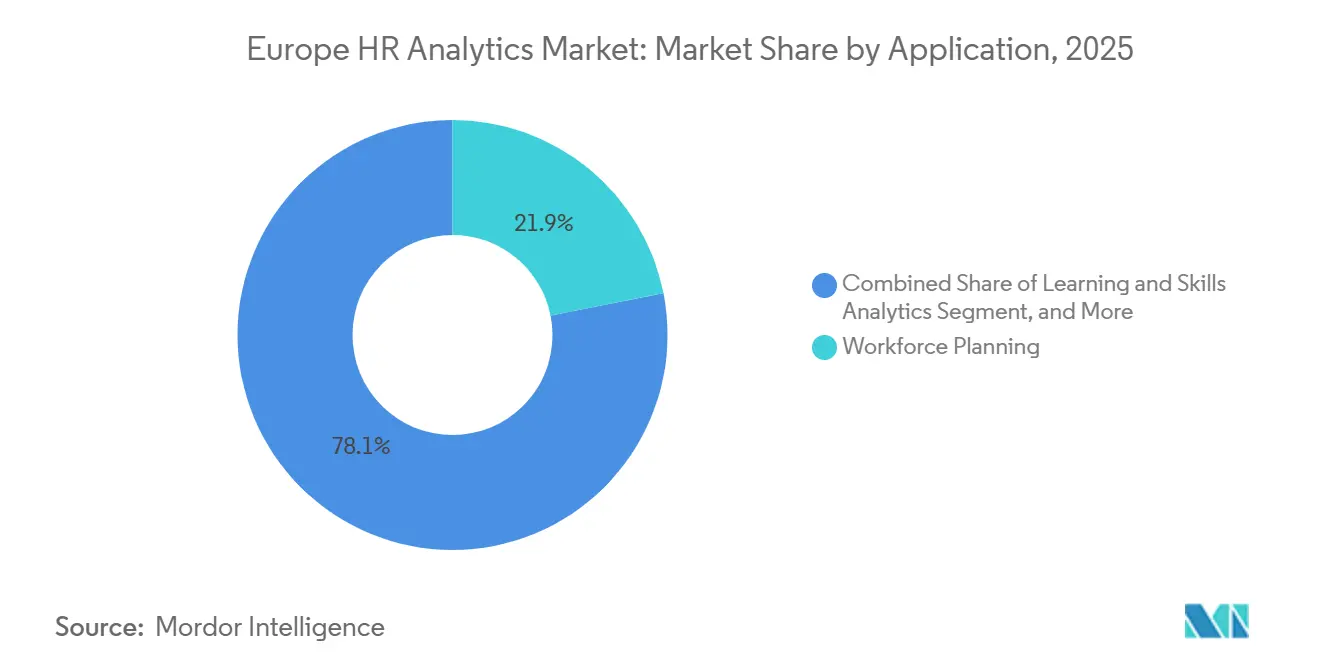

- By application, workforce planning accounted for 21.89% share of the European HR analytics market size in 2025, while learning and skills analytics is projected to expand at a 16.92% CAGR through 2031.

- By end-user industry, information technology and telecom held 24.73% share of the Europe HR Analytics market in 2025, while healthcare and life sciences are projected to record the fastest CAGR of 15.86% through 2031.

- By geography, Germany held 22.47% share of the Europe HR Analytics market in 2025, while the United Kingdom is projected to grow at an 18.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe HR Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-Native HR Analytics Adoption | +3.8% | Global, with concentrated effect in Western Europe, Germany, UK, and Benelux | Short term (= 2 years) |

| Data-Driven Recruitment and Retention Optimization | +2.9% | Global, strongest in IT and telecom and healthcare hubs across Germany, UK, and Netherlands | Short term (= 2 years) |

| Predictive Workforce Planning for Skills Shortages | +2.6% | EU-wide, high intensity in Germany, France, Italy, Spain, and Eastern EU states | Medium term (2-4 years) |

| Employee Experience and Engagement Analytics Expansion | +2.2% | Global, stronger in knowledge-intensive service economies such as the UK, Netherlands, and France | Medium term (2-4 years) |

| EU Pay Transparency Directive Compliance Readiness | +1.8% | EU-wide across all 27 member states, with initial intensity in France, Germany, and Netherlands | Short term (= 2 years) |

| CSRD and ESRS S1 Workforce Disclosure Requirements | +1.3% | EU-wide, with first-wave large enterprises already reporting and wave 2 from FY2027 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-Native HR Analytics Adoption Accelerates Platform Consolidation

Cloud migration has become the strongest structural force shaping software selection across the region. Employers are moving away from on-premises reporting environments because SaaS delivery provides faster updates, lower maintenance costs, and a simpler path to rolling out new analytics features. That shift is especially visible in Germany, where P and I’s valuation reached EUR 5.5 billion (USD 6.22 billion) in March 2025, and the company’s revenue moved past EUR 300 million (USD 339 million) with annual growth above 20%. Cloud migration is also exposing data-quality issues that had been hidden inside siloed HR and payroll systems for years. Once those issues surface, organizations need more support for integration, governance, and ongoing model tuning. In the Europe HR analytics market, that dynamic is extending vendor involvement after the initial deployment and raising the commercial importance of services.[1]HgCapital Trust, “HR Software Leader P&I Secures Further Backing from Hg in EUR 5.5 Billion Transaction,” HgCapital Trust, hgcapitaltrust.com

Data-Driven Recruitment and Retention Optimization Reshapes Talent Economics

Recruitment analytics is moving closer to core business planning because labor shortages remain broad and persistent across Europe. Cedefop’s Labor and Skills Shortage Index shows pressure across high-, medium-, and low-skilled occupations, indicating that employers can no longer rely solely on basic vacancy tracking.[2]Cedefop, “Cedefop Labour and Skills Shortage Index, Addressing Shortages to Boost Competitiveness,” Cedefop, cedefop.europa.eu Buyers are placing more value on platforms that can compare internal skills inventories with external labor signals and expected future demand. That is shifting commercial traction away from narrow applicant-tracking tools and toward broader talent-intelligence systems. Retention analytics is following the same path because employers need earlier warning signs as scarce talent becomes harder to retain. The European HR analytics market is therefore benefiting from a broader definition of recruiting return, encompassing skill gaps, hiring quality, and internal mobility within a single workflow.

Predictive Workforce Planning Addresses EU-Wide Skills Shortages

Workforce planning is no longer limited to annual headcount budgeting in large organizations. Employers increasingly need scenario-based planning that connects business demand, role availability, automation effects, and future skill supply. Cedefop’s shortage index supports that shift by showing simultaneous gaps across multiple parts of the labor market, not just in a few specialist occupations. SD Worx reported in May 2026 that 51% of European organizations now classify workforce planning as a high priority, yet only 32.9% have implemented a structured planning approach. That gap is creating demand for platforms that combine planning models with skills taxonomies and guided decision support. The Europe HR analytics market is capturing that demand because vendors can position planning tools as both a productivity asset and a response to widening labor constraints.

Employee Experience and Engagement Analytics Expansion Targets Continuous Listening

Employee experience analytics is expanding beyond annual surveys and into always-on listening models. Buyers want platforms that can combine performance, learning, compensation, and sentiment signals into a more complete view of workforce stability. In France, the Kelio and OpinionWay AI and HR Barometer 2026 found that 62% of companies remained uncertain about AI’s concrete impact on HR, even as 33% of HR managers actively deployed AI tools, up from 9% in 2024.[3]Kelio and OpinionWay, “L'IA Et Les RH En Entreprise En 2026, Résultats Du 3e Baromètre OpinionWay Pour Kelio,” Kelio, kelio.com That combination of uncertainty and rising use is creating demand for tools that shorten the path from raw HR data to practical action. Vendors are responding by embedding natural language analysis and guided insights inside performance and talent modules. In the European HR analytics market, this is driving wider adoption among organizations that lack dedicated analytics teams but still need clearer signals on engagement and attrition risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR and Sensitive Employee Data Governance Complexity | -1.5% | EU-wide, heightened in Germany, France, and Netherlands | Short term (= 2 years) |

| Fragmented Multicountry HRIS and Payroll Data Estates | -1.2% | Multinational employers across all EU geographies, most acute in Germany, France, and UK payroll environments | Medium term (2-4 years) |

| Works Council Consultation Requirements for Monitoring-Adjacent Analytics | -0.8% | Germany, France, Netherlands, and Austria, with wider influence through EU AI Act employment rules | Medium term (2-4 years) |

| EU AI Act Compliance Burden for High-Risk Employment AI | -0.6% | EU-wide, most acute for large enterprises deploying Annex III employment AI systems | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

GDPR and Sensitive Employee Data Governance Creates Analytics Friction

Data governance remains the most immediate operating constraint for many deployments across Europe. HR teams often hold the data they need in technical terms, but they cannot always reuse it across payroll, performance, recruiting, and attrition workflows without a fresh legal basis or stronger controls. The issue becomes more complex when employers move into profiling, special-category data, or cross-border processing, because those use cases can trigger deeper review and heavier documentation. National overlays also matter, especially in markets where employment privacy expectations are stricter and internal consultation requirements are more formal. That pushes vendors toward privacy-by-design architecture, narrower data access, and more granular permissions from the start of the project. In the Europe HR analytics market, these controls support long-term trust, but they also lengthen implementation cycles and raise near-term delivery costs.

Fragmented Multicountry Data Estates Constrain Cross-Border Workforce Intelligence

Multinational employers still struggle to create a unified employee record across countries, systems, and payroll vendors. Zalaris reported in December 2025 that around 74% of organizations use multiple payroll systems across geographies, which leads to inconsistent records and incompatible job frameworks. SD Worx also noted in April 2026 that payroll processing costs in multicountry environments can range from EUR 100 (USD 113) to nearly EUR 500 (USD 565) per employee, depending on legacy complexity and vendor sprawl. When those fragmented systems feed workforce models, the result is often partial analytics rather than full enterprise visibility. SD Worx further found that 28% of HR leaders in international organizations see limited analytics capability as a barrier to strategic influence. The European HR analytics market is addressing that problem through harmonization layers and managed integration, but the data-estate issue remains a real brake on speed and scale.[4]SD Worx, “How to Scale HR and Payroll Across Countries Without Losing Control,” SD Worx, international.sdworx.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Capture A Complexity Premium In A Faster-Moving Ecosystem

Solutions held 62.37% of the Europe HR analytics market share in 2025, while services are projected to expand at a 16.94% CAGR through 2031. That spread reflects a market structure in which software still anchors contract value, but services increasingly determine project success and renewal quality. As vendors add predictive attrition models, generative AI assistants, and skills graph capabilities, implementation demands are becoming more specialized. Buyers are now less likely to treat deployment as a one-time setup and more likely to view it as a continuous operating program.

Professional services are benefiting from that shift because employers need support for data migration, model calibration, change management, and governance. This is particularly true when organizations are moving from broad HCM reporting to dedicated workforce intelligence platforms that must connect with existing HRIS and payroll stacks. The European HR analytics market is rewarding vendors that can pair software with advisory depth, because value now depends on adoption and output quality as much as on license access. Software still accounts for the larger revenue pool, especially in multi-year SaaS contracts with large enterprises and public-sector clients. At the same time, Germany’s cloud-HR momentum, illustrated by P and I’s growth and valuation trajectory, shows why service intensity is rising alongside platform adoption

By Deployment Mode: Cloud Dominance Coexists With Persistent Hybrid Demand

Cloud deployment accounted for 68.41% of the market in 2025, which confirms that SaaS has become the default architecture for most new HR analytics buying decisions. Cloud systems are attractive because vendors can push product updates faster, support real-time data pipelines more easily, and handle compliance changes without large customer-side upgrade cycles. Hybrid deployment is the fastest-growing model, with a 17.86% CAGR from 2026 to 2031, because some employers still need part of the stack to remain under tighter internal control. That pattern is strongest in banking, healthcare, government, and other regulated settings where data residency, procurement rules, or sunk infrastructure costs still matter.

The on-premises segment is losing relative weight, but it is not disappearing from the region. Established public institutions and industrial organizations, especially in Germany, still maintain internal hosting for sensitive employee records and long-governed IT estates. Hybrid environments, therefore, act as a bridge, not simply as a temporary exception, because they let organizations modernize analytics without rewriting the full data architecture at once. The European HR analytics market is seeing a rise in cloud concentration, but the transition remains uneven across sectors and countries. Vendors with flexible deployment options, sovereign hosting arrangements, and strong integration layers are better placed to win regulated accounts and cross-border deals.

By End User Enterprise Size: SMEs Accelerate Adoption As Access Costs Fall

Large enterprises held 64.12% of the market in 2025, while SMEs are projected to grow at an 18.73% CAGR through 2031. The faster SME growth reflects a clear shift in affordability and usability, as modular platforms and prebuilt connectors have reduced the barriers that once kept advanced analytics within only the largest HR teams. Mid-sized employers that previously depended on spreadsheets and static reports can now access compensation, recruiting, and retention dashboards through lighter subscription models. This is widening the buyer base beyond organizations with in-house HR data specialists.

Large enterprises still account for most spending because they operate broader HR stacks, manage larger workforces, and sign higher-value contracts over longer periods. Their challenge is execution, since fragmented systems and multicountry payroll structures make deployment slower and more complex. SMEs usually have smaller budgets, but they often move faster because decision paths are shorter and product requirements are narrower. The Europe HR analytics market is therefore expanding from both ends, with enterprise clients contributing scale and mid-market buyers contributing growth velocity. That growth is also supported by compliance-driven use cases, especially where smaller employers need better pay reporting, workforce planning, and audit-ready employee data.

By Application: Workforce Planning Leads While Learning And Skills Analytics Gains Speed

Workforce planning accounted for 21.89% share of the European HR analytics market size in 2025, while learning and skills analytics is projected to expand at a 16.92% CAGR through 2031. Workforce planning holds the lead because employers need to model headcount, skill availability, and business scenarios against a volatile labor backdrop. Cedefop’s shortage data shows that pressure extends across healthcare, legal, scientific, services, sales, and personal care roles, which makes planning a cross-functional priority rather than a narrow HR exercise. SD Worx reinforced this in 2026 by showing that planning is widely recognized as important, even though formal execution remains incomplete in many organizations. That combination of broad demand and uneven maturity leaves significant room for platform expansion.

Learning and skills analytics is the fastest-growing application because employers need measurable ways to map capabilities, redeploy labor, and address internal shortages. This makes skills data more valuable, especially when organizations want to connect training, mobility, and succession planning in one system. The Europe HR analytics market also continues to see solid demand for talent acquisition, retention, DEI, and workforce compliance analytics, as data collection and disclosure obligations are becoming more formalized. EFRAG’s ESRS S1 framework supports that direction by setting out extensive own-workforce disclosure requirements that increase the need for structured data capture and reporting configuration. Compensation and pay equity analytics are also gaining relevance as employers prepare for more detailed transparency and reporting obligations across the region.

By End-User Industry: IT And Telecom Leads While Healthcare And Life Sciences Gains Ground

Information technology and telecom organizations held a 24.73% share in 2025, while healthcare and life sciences are projected to record the fastest CAGR of 15.86% through 2031. IT and telecom leads because employers in this sector already operate dense digital infrastructure and are more comfortable embedding analytics into hiring, performance, and skills decisions. They also face intense competition for software, cybersecurity, and data talent, which raises the value of predictive recruiting and internal mobility tools. Healthcare and life sciences are growing faster because staffing pressure remains structural, and employers need stronger forecasting and attrition modeling to stabilize shift-based workforces.

Cedefop’s shortage evidence supports the healthcare case because the region continues to report pressure across several high-skilled and service occupations tied to care delivery and support roles. BFSI demand is rising in compensation benchmarking, pay equity, and disclosure-related reporting, where cleaner workforce data has become more important. Manufacturing is focusing more on shift planning, labor allocation, and visibility into skills gaps across plants and technical roles. Government and public sector bodies are leaning toward workforce planning and compliance reporting, while retail is placing greater emphasis on frontline engagement and turnover monitoring. Across these user groups, the Europe HR analytics industry is becoming more application-led, with sector-specific use cases shaping product selection more than generic reporting breadth alone.

Geography Analysis

Germany held 22.47% of the European HR analytics market share in 2025, maintaining its leading position across the region. Its scale reflects a mature digital-HR buying environment, a strong system integrator base, and continued movement away from legacy software toward cloud-ready workforce platforms. The pace of vendor and investor interest is visible in P and I’s March 2025 valuation of EUR 5.5 billion (USD 6.22 billion), which was nearly 3 times its 2019 level. Germany still has more deployment friction than some peers because works council consultation and privacy expectations make implementation discipline essential. The Netherlands remains an active market for the European HR analytics market, as multinational employers' workforce disclosure needs support demand for structured reporting and analytics configuration.

The United Kingdom is the fastest-growing geography, with a projected CAGR of 18.38% from 2026 to 2031. Part of that momentum comes from its long-standing use of gender pay gap reporting, which has already pushed many large employers to build compensation analytics processes and cleaner employee data sets. The country also benefits from a strong HR technology investment environment and from buyer familiarity with software-led compliance tools. France remains one of the region’s more important markets by value because employers are facing both reporting requirements and active interest in AI-supported HR workflows. Kelio and OpinionWay showed in March 2026 that 33% of French HR managers were already using AI tools, even though 62% of companies still lacked clarity on AI’s practical impact on HR, suggesting a market that is engaged but still early in operational maturity.

Italy and Spain represent meaningful growth opportunities, although demand is developing through different channels. In both countries, labor-market mismatches and workforce modernization programs are driving interest in recruitment, planning, and skills analytics, especially where employers need better visibility into future roles and training needs. Russia remains more isolated from the wider regional software ecosystem, with local demand shaped less by EU compliance frameworks and more by domestic vendor activity. The rest of Europe, including the Nordics and several Central and Eastern European markets, adds further depth to the Europe HR analytics market as employers continue to invest in skills visibility, workforce planning, and cloud-based HR modernization.

Competitive Landscape

The European HR analytics market remains fragmented, with global enterprise platforms competing alongside EU-native specialists and focused vendors built around pay equity, skills intelligence, and engagement analytics. No single company holds a dominant position, and competition is shaped more by depth in a specific use case than by complete platform control across the region. Global vendors typically compete on scale, AI investment, and enterprise integration, while regional specialists compete on sovereign hosting, local compliance alignment, and a closer fit with European HR processes. This leaves buyers with a broad choice set, but it also means product comparison is becoming more detailed and less dependent on brand scale alone. In practice, vendors that can show clean integration, explainable AI, and strong governance are improving their position in larger deals.

Strategic moves in 2025 and 2026 show how quickly the field is evolving. Visier reported in February 2025 that nearly half of its 65,000-plus customers had adopted its Vee AI agent, and the company simultaneously expanded its Microsoft 365 Copilot integration and its enterprise AI agent platform. Eightfold AI added AI Interviewer 360, AI Interview Companion, Workforce Readiness intelligence, and TalentForge in May 2026, which signaled a stronger push toward agentic workflow building and European expansion. Crunchr strengthened its position in March 2026 when Finch Capital invested to support European expansion and the development of next-generation agentic analytics. These moves show that AI depth and deployment fit are now central to how vendors defend or build share in the Europe HR analytics market.

EU-native providers are using regional credibility as a practical differentiator. 365Talents confirmed in April 2026 that it plans to launch a Workforce Analyst AI Agent in H2 2026, aimed at helping HR teams model critical skills gaps and talent decisions more directly. Leapsome also expanded beyond performance and engagement with its People-Centric HRIS product in 2025, strengthening its position in German mid-market accounts seeking core HR and analytics in a more unified environment. The European HR analytics market still has white space in workforce disclosure automation and SME-ready skills intelligence, especially for buyers seeking quick implementation without high consulting overhead. That combination of fragmentation, active product development, and unmet niche demand supports a market structure in which competition remains open, and consolidation pressure is likely to remain selective rather than sweeping.

Europe HR Analytics Industry Leaders

Visier, Inc.

One Model Inc.

Concentra Analytics Limited

Crunchr B.V.

Syndio Solutions, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eightfold AI unveiled AI Interviewer 360, AI Interview Companion, Workforce Readiness intelligence layer, and TalentForge application builder at Cultivate 2026, alongside an Oracle Fusion Cloud Recruiting integration. The company also announced Cultivate Europe 2026 in London on June 11, reflecting a strategic commitment to European market expansion.

- April 2026: 365Talents SAS published its 2026 product roadmap, confirming the planned launch of a Workforce Analyst AI Agent in H2 2026 for HR admins to model critical skills gaps and talent decisions. The company, now part of Docebo following a merger, also won the 2026 AI HR Trophy with Alstom for dynamic skills management at scale.

- March 2026: Crunchr B.V. received a strategic investment from Finch Capital to accelerate European market expansion and fund the development of a next-generation agentic analytics architecture. Finch Capital described Crunchr as the only European end-to-end workforce insights solution with built-in security and authorization controls.

- February 2026: Visier, Inc. released its Winter 2026 platform update, including a Snowflake connector in beta, general availability of Studio Assistant and Vee Usage-Based Tuning, and Model Context Protocol enhancements for the Vee AI agent.

Europe HR Analytics Market Report Scope

The Europe HR analytics market refers to technology platforms and services that enable organizations across the region to collect, analyze, and interpret workforce data for strategic human resource management. These solutions cover applications such as talent acquisition, onboarding, retention, workforce planning, performance management, compensation and pay equity, employee engagement, learning and skills analytics, and DEI compliance.

The Europe HR analytics market report is segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Application (Talent Acquisition and Onboarding, Retention and Attrition Management, Workforce Planning, Performance and Productivity Management, Compensation and Pay Equity, Employee Engagement and Experience, Learning and Skills Analytics, DEI and Workforce Compliance Analytics, and Other Applications), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, and Government and Public Sector), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, Netherlands, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Talent Acquisition and Onboarding |

| Retention and Attrition Management |

| Workforce Planning |

| Performance and Productivity Management |

| Compensation and Pay Equity |

| Employee Engagement and Experience |

| Learning and Skills Analytics |

| DEI and Workforce Compliance Analytics |

| Other Applications |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Rest of Europe |

| By Component | Solutions |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By End User Enterprise Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Application | Talent Acquisition and Onboarding |

| Retention and Attrition Management | |

| Workforce Planning | |

| Performance and Productivity Management | |

| Compensation and Pay Equity | |

| Employee Engagement and Experience | |

| Learning and Skills Analytics | |

| DEI and Workforce Compliance Analytics | |

| Other Applications | |

| By End User Industry | BFSI |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Retail and E-commerce | |

| Industrial Manufacturing | |

| Government and Public Sector | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

What is the size of the Europe HR analytics market?

The Europe HR analytics market was valued at USD 5.60 billion in 2025, stands at USD 6.37 billion in 2026, and is projected to reach USD 12.84 billion by 2031 at a 15.05% CAGR.

Which segment leads by component in Europe?

Solutions led by component with a 62.37% share in 2025, while services is the faster-growing part of demand with a 16.94% CAGR through 2031.

Why is workforce planning such a large application area?

Workforce planning held 21.89% share in 2025 because employers need better visibility on headcount, skills supply, and business scenarios in a tight labor environment.

Which countries are driving regional growth the most?

Germany was the largest country market in 2025 with a 22.47% share, while the United Kingdom is projected to grow the fastest at an 18.38% CAGR through 2031.

Why are SMEs adopting HR analytics faster now?

SMEs are projected to grow at an 18.73% CAGR because modular platforms, lower entry costs, and easier integrations have made advanced analytics more accessible to mid-sized employers.

Which end-user sectors are most active in adoption?

IT and telecom led with a 24.73% share in 2025 due to stronger data maturity, while healthcare and life sciences is growing fastest at a 15.86% CAGR because workforce shortages are more acute.

Page last updated on: