Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

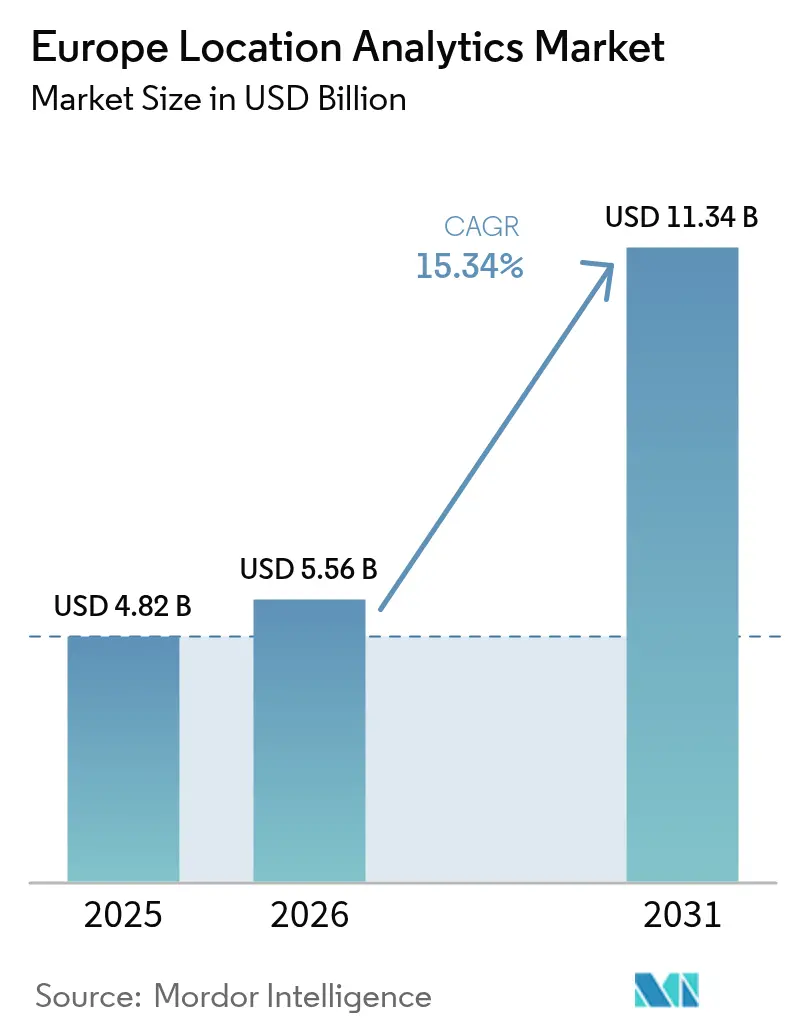

| Base Year Market Size (2025) | USD 4.82 Billion |

| Market Size (2026) | USD 5.56 Billion |

| Market Size (2031) | USD 11.34 Billion |

| Growth Rate (2026 - 2031) | 15.34% CAGR |

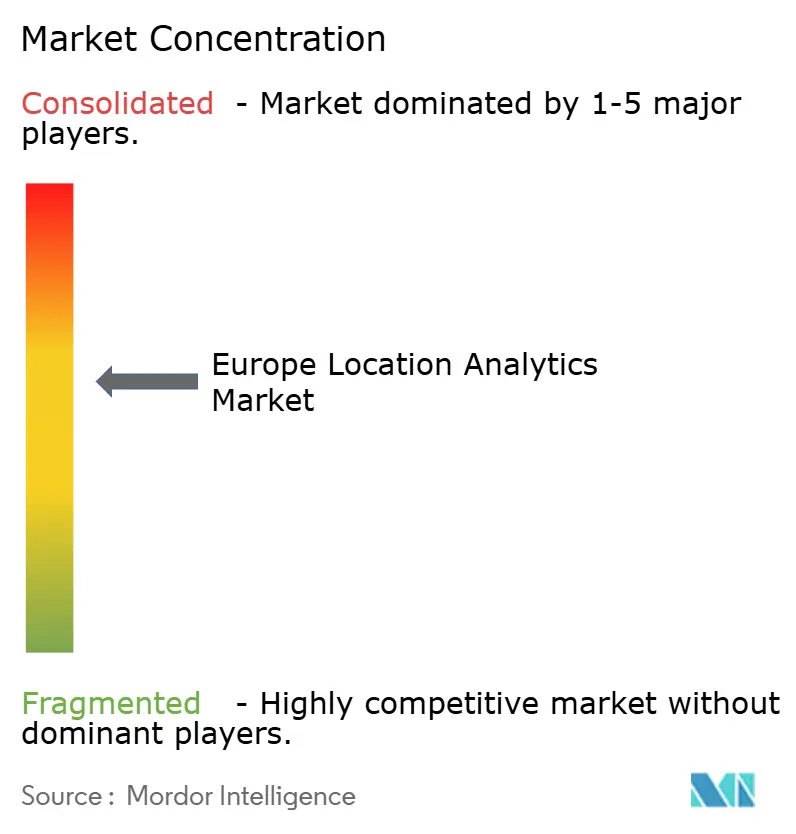

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Location Analytics Market Analysis by Mordor Intelligence

The Europe location analytics market size was valued at USD 4.82 billion in 2025 and estimated to grow from USD 5.56 billion in 2026 to reach USD 11.34 billion by 2031, at a CAGR of 15.34% during the forecast period (2026-2031). Fundamental momentum springs from nationwide 5G standalone roll-outs that cut wireless latency below 10 milliseconds, tighter GDPR enforcement that favors on-premise geospatial stacks for data sovereignty, and more than 100 digital-twin city projects supported by the Citiverse initiative. Intensifying cloud adoption, widening retail sensor fusion, and a rising wave of hospital digitalization funds continue to expand the Europe location analytics market footprint. Meanwhile, API-driven consumption models from hyperscalers compress time-to-value for newcomers, while privacy-first edge analytics opens new revenue lanes across logistics, healthcare, and public safety. Consolidation is underway as incumbents acquire niche indoor-positioning vendors, responding to enterprise preference for integrated hybrid-indoor–outdoor offerings.

Key Report Takeaways

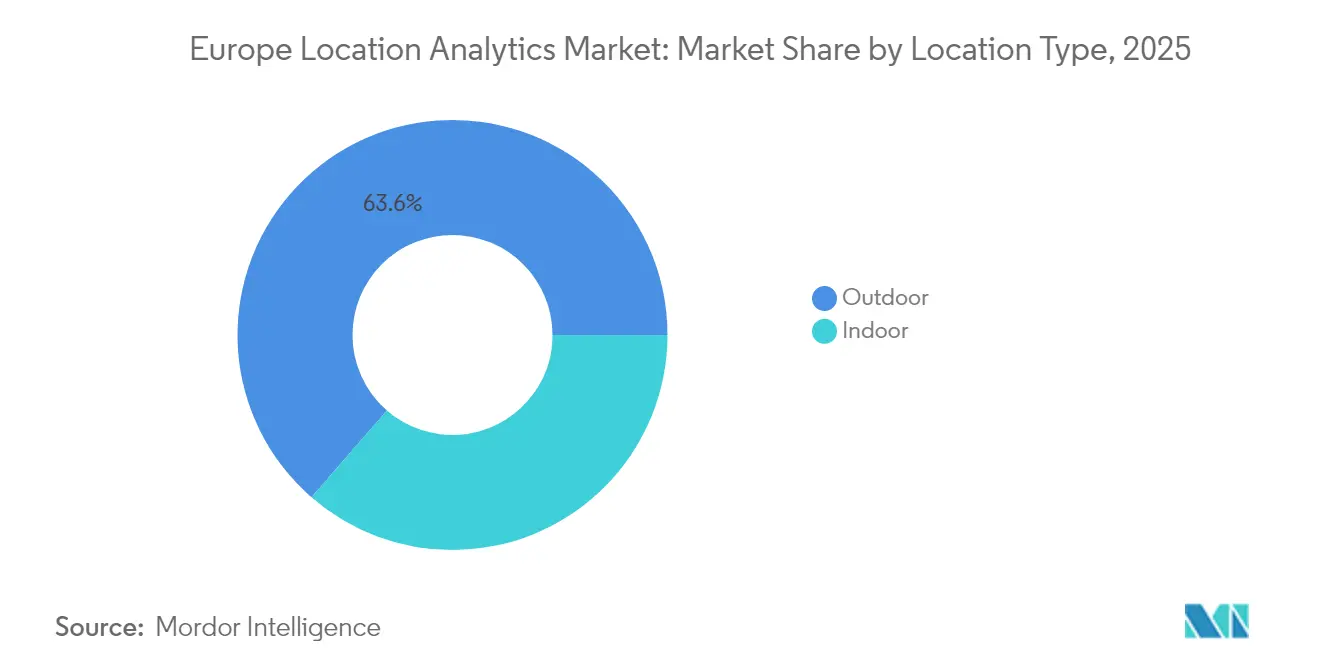

- By location type, outdoor analytics controlled 63.61% of the Europe location analytics market share in 2025, while indoor systems are forecast to post a 15.52% CAGR to 2031.

- By deployment, cloud platforms accounted for 57.12% of the Europe location analytics market share in 2025 and are set to grow at a 16.1% CAGR through 2031.

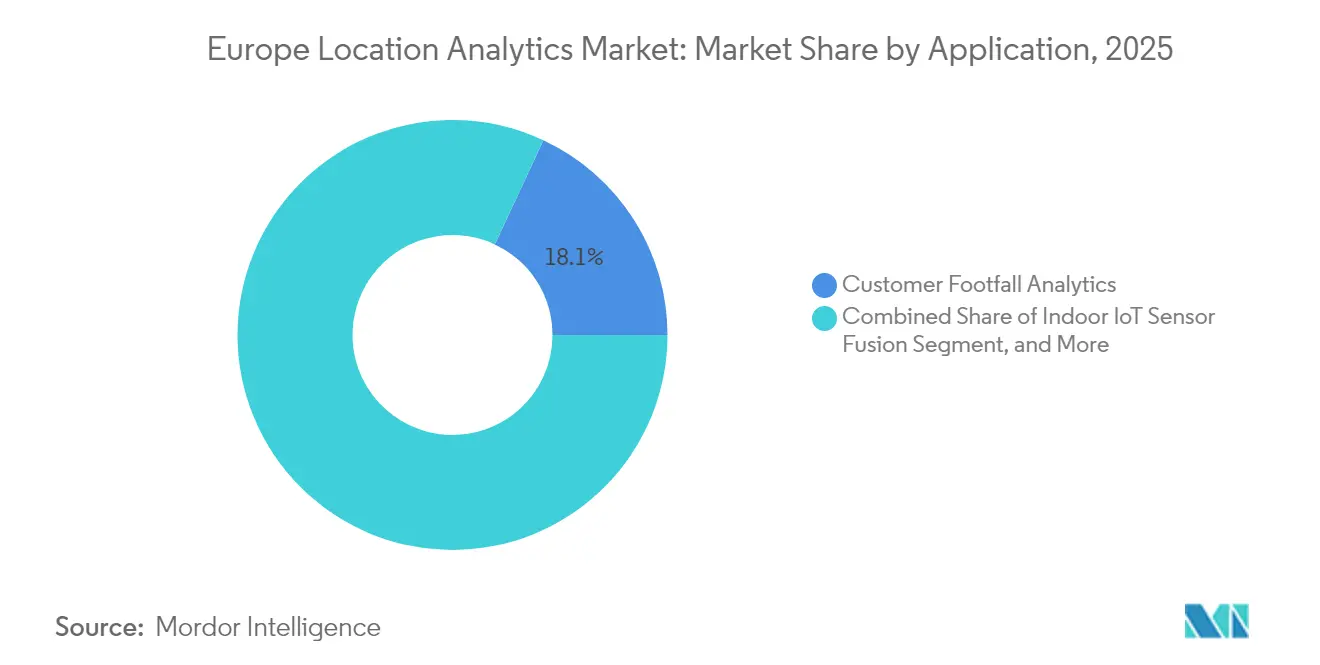

- By application, customer footfall analytics captured 18.05% of the revenue in 2025, whereas indoor IoT sensor fusion is projected to expand at a 15.6% CAGR through 2031.

- By end user, retail accounted for 23.20% of spending in 2025, and healthcare is projected to achieve a 16.85% CAGR during 2026-2031.

- By country, Germany represented 14.25% of regional revenue in 2025, but the United Kingdom is expected to advance the fastest, at a 15.95% CAGR, to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Location Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Real-Time Fleet Management Solutions | +2.8% | Germany, France, Netherlands, Nordic hubs | Medium term (2-4 years) |

| Accelerated 5G Roll-Out Enabling Hyper-Local Analytics | +3.2% | Germany, United Kingdom, France urban cores | Short term (≤ 2 years) |

| Integration of Geospatial AI in Public-Safety Operations | +2.1% | United Kingdom, France, Spain | Medium term (2-4 years) |

| Mandates for Smart-City Open Data Portals | +1.9% | Germany, Netherlands, Nordic zone | Long term (≥ 4 years) |

| Growth of Digital-Twin Infrastructure Projects | +2.4% | Spain, France, Belgium, Germany | Medium term (2-4 years) |

| Surge in Indoor IoT Sensor Fusion for Retail | +2.3% | United Kingdom, Germany, France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Real-Time Fleet Management Solutions

Logistics carriers are embedding geospatial analytics into their telematics stacks to reduce empty-mile kilometers and meet the scope 3 requirements of the Corporate Sustainability Reporting Directive. DHL earmarked EUR 2 billion (USD 2.33 billion) for European EV fleets in 2024, pairing edge gateways with traffic, weather, and volume density feeds to reduce route variance by 12%. Maersk’s predictive ETA engine cut hub dwell time 12% in H1 2024 by applying location AI to rail–port handoffs. DB Cargo has adopted automated geofencing, which reduces border crossings by 18 minutes per shipment, thereby accelerating customs clearance. Fleet software now bundles location analytics with predictive maintenance, tying elevation profiles and road quality to part-wear forecasts that pre-empt breakdowns.

Accelerated 5G Roll-Out Enabling Hyper-Local Analytics

Standalone 5G with network slicing guarantees sub-10 ms latency, unlocking augmented-reality navigation and autonomous warehouse forklifts. Vodafone Germany reached 90% population coverage by mid-2024, enabling private 5G networks employing centimeter-accurate indoor positioning. Orange France extended 5G to 75% of citizens by late-2024 to fuel real-time crowd-density heatmaps for retailers. EU Digital Decade aims for 75% 5G coverage by 2030, supporting millimeter-wave beamforming in airports and arenas. Deutsche Telekom and TRUMPF reached 30 cm accuracy in UWB-enabled factories, illustrating how 5G edge compute can localize work-in-progress inventory without relying on cloud cores.

Integration of Geospatial AI in Public-Safety Operations

European emergency agencies now couple advanced mobile-location feeds with geospatial AI. NHS England embedded spatial routing in its 111 helpline in 2024, cutting average caller wait times 14% by sending patients to the nearest site with open beds. Copernicus issued wildfire damage maps for Portugal within six hours of satellite pass, guiding aircraft dispatch.[1]Copernicus Emergency Management Service, “Portugal Wildfires 2024 Rapid Mapping,” emergency.copernicus.eu France piloted crime-pattern AI that aligns street geometry and lighting with patrol deployment, while new EU AI Act rules require human oversight for live biometric ID, tempering roll-out velocity. Dutch and Belgian flood agencies fused tide gauges, radar, and elevation layers to issue evacuation alerts 12 hours earlier than rule-based models.

Mandates for Smart-City Open Data Portals

More than 100 cities will launch interoperable twins under the EUR 80 million (USD 93.31 million) Citiverse scheme by 2026, standardizing GeoJSON and CityGML layers. Madrid’s 2024 twin models traffic, buildings, and energy to quantify carbon impact of zoning changes. Barcelona’s portal streams waste-truck GPS every 30 seconds, enabling third-party route apps that lower fuel use 8%. Brussels requires geospatial metadata with every new public-works file from 2025, ensuring continuous dataset freshness. Open standards reduce vendor lock-in, pushing suppliers to compete on analytics depth rather than data access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent GDPR Location-Consent Requirements | -2.6% | Pan-European, stricter in Germany, France, Belgium | Short term (≤ 2 years) |

| De-Fragmented Local Government Procurement Cycles | -1.4% | Southern and Eastern Europe | Long term (≥ 4 years) |

| Rising Cost of High-Resolution Satellite Imagery Licensing | -0.9% | United Kingdom, Germany, France | Medium term (2-4 years) |

| Limited Availability of Qualified Geo-AI Talent | -1.7% | Germany, United Kingdom, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent GDPR Location-Consent Requirements

The European Data Protection Board clarified in 2024 that Wi-Fi and BLE MAC tracking counts as personal data, forcing retailers to deploy consent banners that sink opt-in rates 30-40% below opt-out regions. Germany’s BSI urges on-device processing and differential privacy to curb cloud transfers. Belgium fined a beacon vendor EUR 250,000 (USD 291596.25) for lack of explicit consent, triggering sector-wide audits. Compliance costs hit SMEs hardest, steering contracts toward big-platform players with legal benches, yet also spur demand for on-premise deployments that avoid cross-border transfers flagged by the Schrems II ruling.

De-Fragmented Local Government Procurement Cycles

Vendors grapple with 27 procurement codes. Spain’s EUR 500,000 (USD 583192.50) environmental review threshold adds six months to large twin tenders. Italy reserves 30% of contract value for SMEs, splintering projects into multiple sub-awards that strain integration. Poland mandates national, not ISO, cyber audits, duplicating vendor effort. Planned Digital Services Act mutual certification remains years away, so near-term fragmentation continues to dampen sales velocity.[2]European Commission, “Digital Decade Targets,” digital-strategy.ec.europa.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location Type: Indoor Positioning Gains on Retail and Healthcare Mandates

Indoor analytics posted a 15.52% CAGR forecast from 2026 to 2031, eclipsing outdoor systems that still held 63.61% of 2025 spend. Sub-USD 1 ambient-IoT tags from Wiliot and 10-cm angle-of-arrival UWB from Quuppa shrink hardware barriers and push the Europe location analytics market deeper into theaters, terminals, and wards. Enterprise buyers prize the batteryless form factor that eliminates monthly maintenance rounds, while hospitals cut equipment loss 18%. The Galileo High Accuracy Service and ubiquitous GPS keep outdoor analytics indispensable for transit and precision agriculture. Still, indoor adoption surges as national health systems and retailers converge on hybrid BLE–UWB blueprints.

Edge gateways translate sub-second indoor feeds to cloud dashboards only when bandwidth permits, honoring GDPR minimization. Deutsche Telekom’s 30-cm UWB pilot inside metal-dense factories validates robustness where Wi-Fi multipath prevails. Ultra-wideband captures high-value industrial cases, while BLE dominates cost-sensitive retail. Collectively these factors multiply addressable use cases, reinforcing the Europe location analytics market as indoor accuracy climbs.

By Deployment: Cloud Platforms Capture API-Driven Consumption Models

Cloud held 57.12% of the 2025 spend and is projected to have a 16.1% CAGR, reflecting API bundling within Azure, AWS, and Fabric. Microsoft and TomTom extended Orbis Maps in Azure through 2030, simplifying licensing and encouraging developers to adopt consumption-based billing. HERE’s EUR 428 million(USD 499.21 million) Q3 2024 revenue, up 16%, underscores migration from on-premise estates. Microsoft Fabric has added spatial joins to OneLake, enabling SQL analysts to run geofencing queries without requiring GIS installations.

On-premise remains vital for defense, banking, and critical infrastructure. The European Banking Authority's outsourcing guide encourages financial institutions to maintain customer geolocation in private clouds. Esri’s January 2025 link-up with TomTom channels cloud routing into ArcGIS, while datasets remain local, demonstrating hybrid traction. As hyperscalers swallow routine spatial operations, vendors pivot to value-added twin simulations and AI-driven insight layers, sustaining differentiation inside the Europe location analytics market.

By Application: Footfall Analytics Lead, Sensor Fusion Accelerates

Footfall analytics secured 18.05% of 2025 revenue as chains chase conversion boosts and leaner labor rosters. However, sensor fusion is projected to achieve a 15.6% CAGR, combining BLE, Wi-Fi RTT, and inertial units to achieve 1 m precision without requiring new cabling. Wiliot’s tags track units from the dock to the shelf at the SKU level. Hospitals deploy BLE–UWB hybrids to locate infusion pumps, slicing search times. City emergency desks tap Copernicus rapid maps within six hours, demonstrating how real-time imagery augments risk response.

Asset tracking aligns with capital discipline by reducing redundant stock, while marketing geofences encounter opt-in friction under GDPR. Urban planners embrace twins to score zoning moves on emissions. These trends solidify new data streams and diversify subscription revenue, cementing application breadth inside the Europe location analytics market.

By End User: Healthcare Outpaces Retail on Digitalization Funds

Retail accounted for 23.20% of the 2025 spend for queue, dwell, and promotion analytics. The Europe location analytics market size for healthcare is primed for a 16.85% CAGR, buoyed by NHS England’s digital roadmap and Germany’s EUR 4 billion (USD 4.67 billion) hospital fund. Blyott’s 22% patient-flow gain and Quuppa’s 18% instrument loss reduction illustrate ROI.

Financial services pilot geo-fraud detection and branch optimization, with telematics motor policies hitting 17% penetration. Logistics leverages fleet analytics to cap empty miles, aligning with emissions disclosures. Tourism taps AI itinerary planners that adjust to live occupancy. Expanding sectoral use forms a diverse, resilient demand base for the Europe location analytics market.

Geography Analysis

Germany accounted for 14.25% of the Europe location analytics market in 2025, fueled by Vodafone’s 90% 5G standalone reach and Deutsche Telekom’s 30 cm UWB factory pilots that trim downtime. Federal funds of EUR 4 billion (USD 4.67 billion), through 2027, will bankroll smart-city, hospital, and automation projects, each embedding digital twins to model energy and traffic flows. Strong GDPR enforcement prompts enterprises to adopt on-premise deployments, thereby sustaining domestic demand for private geospatial stacks.

The United Kingdom is forecast to expand at a 15.95% CAGR as the GBP 2.5 billion (USD 3.33 billion) Connectivity Fund and GBP 800 million 5G Innovation Regions elevate rural coverage and industrial trials. Ordnance Survey’s twin requirement obliges councils to expose real-time datasets, sparking platform procurement. NHS England’s geospatial AI in the 111 helpline reduced wait times by 14%, spotlighting clinical ROI. London’s congestion-pricing expansion uses ANPR and GPS to enforce variable tolls, driving steady demand for high-accuracy location feeds.

France invested EUR 1.75 billion in digital infrastructure in 2024, achieving 75% 5G coverage and piloting digital twins in major metropolitan areas. Predictive-policing algorithms correlate crime hot spots with urban morphology but face civil-liberty scrutiny. Across Southern and Eastern Europe, EU-level programmes fund cross-border 5G corridors and twins, letting midsize cities leapfrog legacy gaps. Madrid’s twin tests zoning emissions, while Barcelona’s live waste-fleet portal trims route fuel 8%.

Competitive Landscape

The Europe location analytics market is moderately concentrated. Esri, HERE, and TomTom own deep API catalogs, yet hyperscalers blur boundaries by baking spatial services into cloud suites. Microsoft embedded SQL-native geospatial joins in Fabric OneLake in December 2024, eliminating the need for standalone GIS for many ETL use cases. TomTom renewed its Azure agreement through 2030, expanding the distribution of Orbis Maps. Hexagon bought Inpixon for over USD 50 million, folding BLE and UWB into its manufacturing and healthcare verticals.

Mapbox’s USD 280 million Series E signals robust venture appetite for developer-first tooling that monetizes via pay-as-you-go APIs. Wiliot’s sub-USD1 ambient tags undercut battery-based beacons, prompting incumbents to reassess device economics. HERE leans into automotive data exchanges, while Esri doubles on public-sector twins, weaving TomTom traffic into ArcGIS for hybrid deployments.

Skills scarcity shapes vendor playbooks. CARTO found that 70% of firms plan to adopt AI, yet only 56% invest in training; Cedefop reports that 44% offer none. Providers launch low-code templates and managed services to offset talent gaps. White-space prospects sit in seamless indoor-outdoor tracking for logistics hubs and GDPR-compliant privacy layers, arenas where agile startups can still carve share.

Europe Location Analytics Industry Leaders

Microsoft Corporation

Esri Global, Inc.

HERE Global B.V.

Google LLC

TomTom International B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Esri and TomTom partnered to feed cloud routing, traffic, and geocoding APIs into on-premise ArcGIS stacks, easing GDPR localization concerns.

- December 2024: Microsoft shipped Fabric OneLake geospatial analytics, enabling SQL-first spatial joins without separate GIS servers.

- November 2024: Google added Gemini AI to Maps Platform, delivering natural-language route optimization and real-time venue occupancy across Europe.

- October 2024: Mapbox raised USD 280 million in Series E to scale European real-time traffic services.

Europe Location Analytics Market Report Scope

The Europe Location Analytics Market study assesses the surging demand for data-driven spatial insights in Europe. These insights are pivotal for boosting operational efficiency, enhancing customer engagement, and informing strategic decisions across various industries. As businesses increasingly adopt both indoor and outdoor location-based solutions, this study examines the primary drivers of growth. These include the ongoing digital transformation, the broadening scope of IoT, and the escalating need for real-time data.

The Europe Location Analytics Market Report is Segmented by Location Type (Indoor, Outdoor), Deployment (Cloud, On-Premise), End User (Banking, Financial Services and Insurance, Retail, Transportation and Logistics, Tourism and Hospitality, Healthcare), Application (Customer Footfall Analytics, Asset Tracking, Risk and Incident Management, Marketing Campaign Optimization, Urban Planning and Zoning), and Geography (Germany, United Kingdom, France, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Location Type

| Indoor |

| Outdoor |

By Deployment

| Cloud |

| On-Premise |

By End User

| Banking, Financial Services and Insurance (BFSI) |

| Retail |

| Transportation and Logistics |

| Tourism and Hospitality |

| Healthcare |

By Application

| Customer Footfall Analytics |

| Asset Tracking |

| Risk and Incident Management |

| Marketing Campaign Optimization |

| Urban Planning and Zoning |

By Country

| Germany |

| United Kingdom |

| France |

| Rest of Europe |

| By Location Type | Indoor |

| Outdoor | |

| By Deployment | Cloud |

| On-Premise | |

| By End User | Banking, Financial Services and Insurance (BFSI) |

| Retail | |

| Transportation and Logistics | |

| Tourism and Hospitality | |

| Healthcare | |

| By Application | Customer Footfall Analytics |

| Asset Tracking | |

| Risk and Incident Management | |

| Marketing Campaign Optimization | |

| Urban Planning and Zoning | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe location analytics market in 2026?

The Europe location analytics market size reached USD 5.56 billion in 2026.

What is the forecast growth rate through 2031?

The market is projected to advance at a 15.34% CAGR between 2026 and 2031.

Which deployment model is expanding fastest?

Cloud platforms lead with a 16.1% CAGR, helped by API bundling from hyperscalers.

Why is healthcare spending on location analytics rising?

National digitalization funds and hospital flow efficiency targets are driving a 16.85% CAGR in healthcare deployments.

Which country shows the highest growth potential?

The United Kingdom is forecast to post the fastest growth at 15.95% CAGR through 2031.

What key technology trend will reshape indoor analytics?

Batteryless BLE and UWB sensor fusion enabling sub-meter accuracy without heavy infrastructure retrofits is accelerating adoption.

Page last updated on: