Germany Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

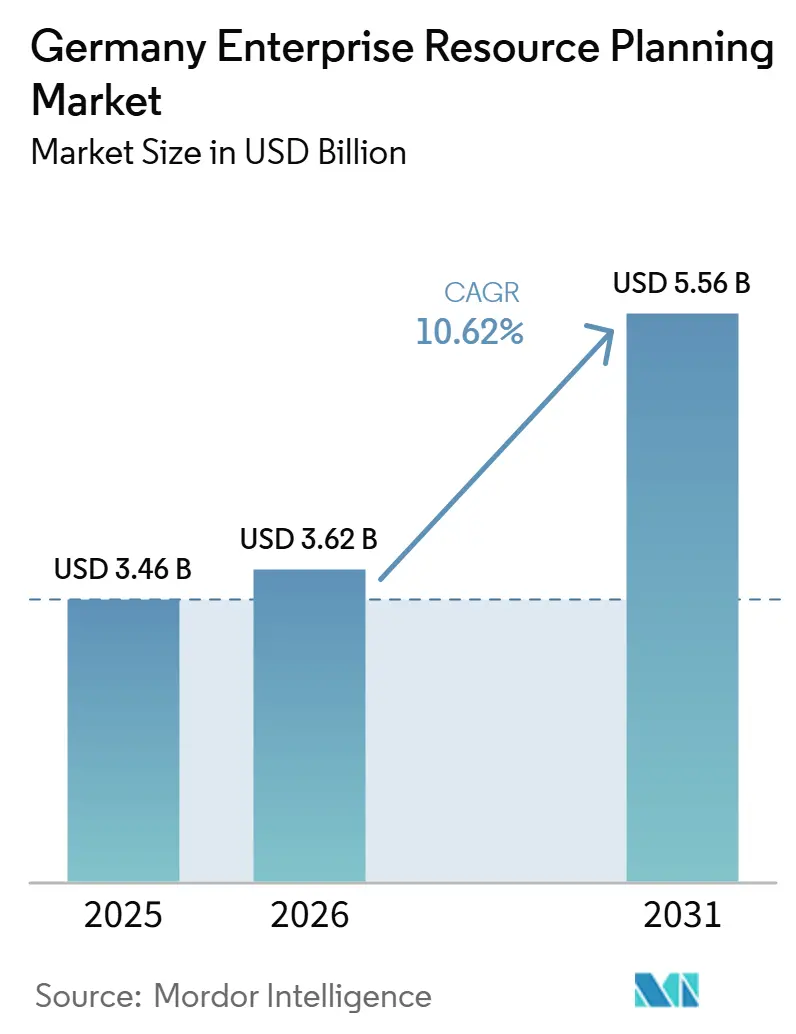

| Base Year Market Size (2025) | USD 3.46 Billion |

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 5.56 Billion |

| Growth Rate (2026 - 2031) | 10.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Germany enterprise resource planning market size is expected to increase from USD 3.46 billion in 2025 to USD 3.62 billion in 2026 and reach USD 5.56 billion by 2031, growing at a CAGR of 6.58% over 2026-2031. The measured pace reflects a mature landscape in which SAP’s 2027 mainstream-support deadline for ECC is driving latent replacement demand into active migration projects, especially across the Mittelstand. Hybrid-cloud strategies, regulatory mandates such as the Corporate Sustainability Reporting Directive, and mounting data-sovereignty concerns shape spending priorities as enterprises weigh private or sovereign cloud against hyperscale platforms. Large manufacturers are re-architecting shop-floor integration layers to align with Industry 4.0, while service sectors are accelerating human-capital and finance modernization to address talent shortages and meet e-invoicing obligations. Competitive intensity remains high: SAP dominates core systems, yet German specialists differentiate through vertical functionality, local support, and incremental hybrid deployment.

Key Report Takeaways

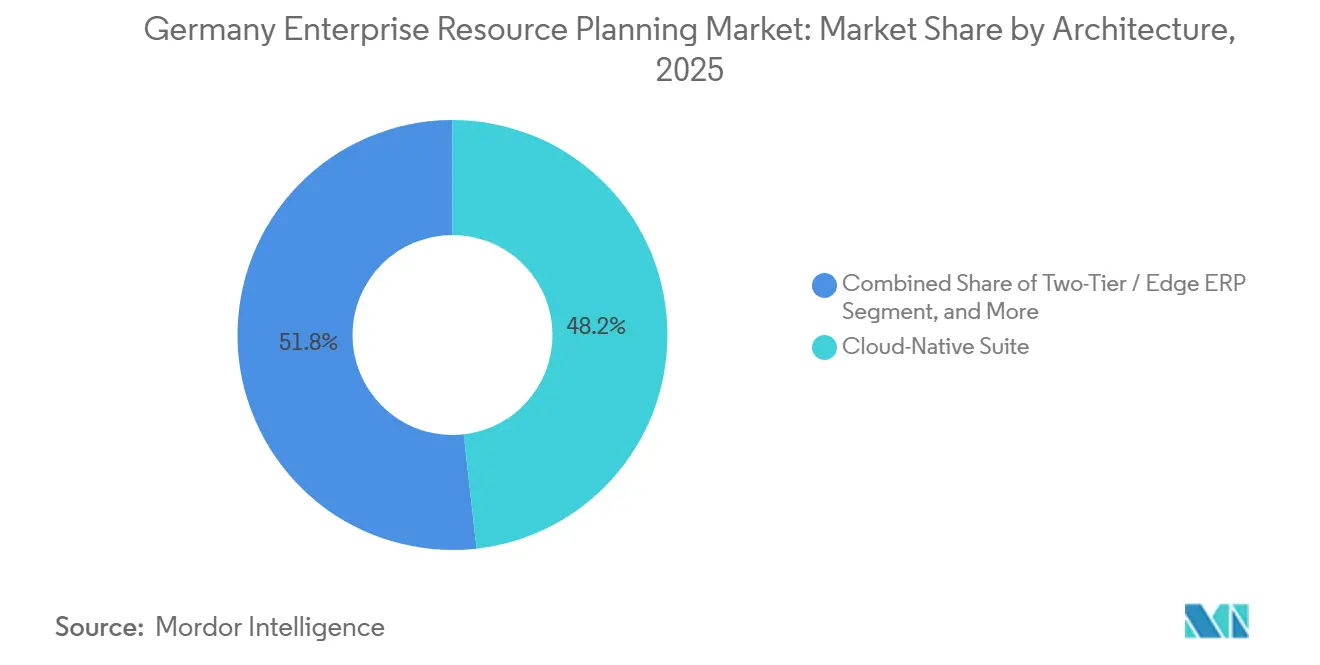

- By architecture, cloud-native suites led with 48.21% revenue share in 2025; two-tier configurations are projected to expand at a 15.12% CAGR through 2031.

- By business function, finance and accounting held 34.97% of the Germany enterprise resource planning market share in 2025, while human capital management is forecast to grow at 13.28% CAGR to 2031.

- By deployment model, cloud captured 63.44% of spending in 2025 and is advancing at a 16.43% CAGR through 2031.

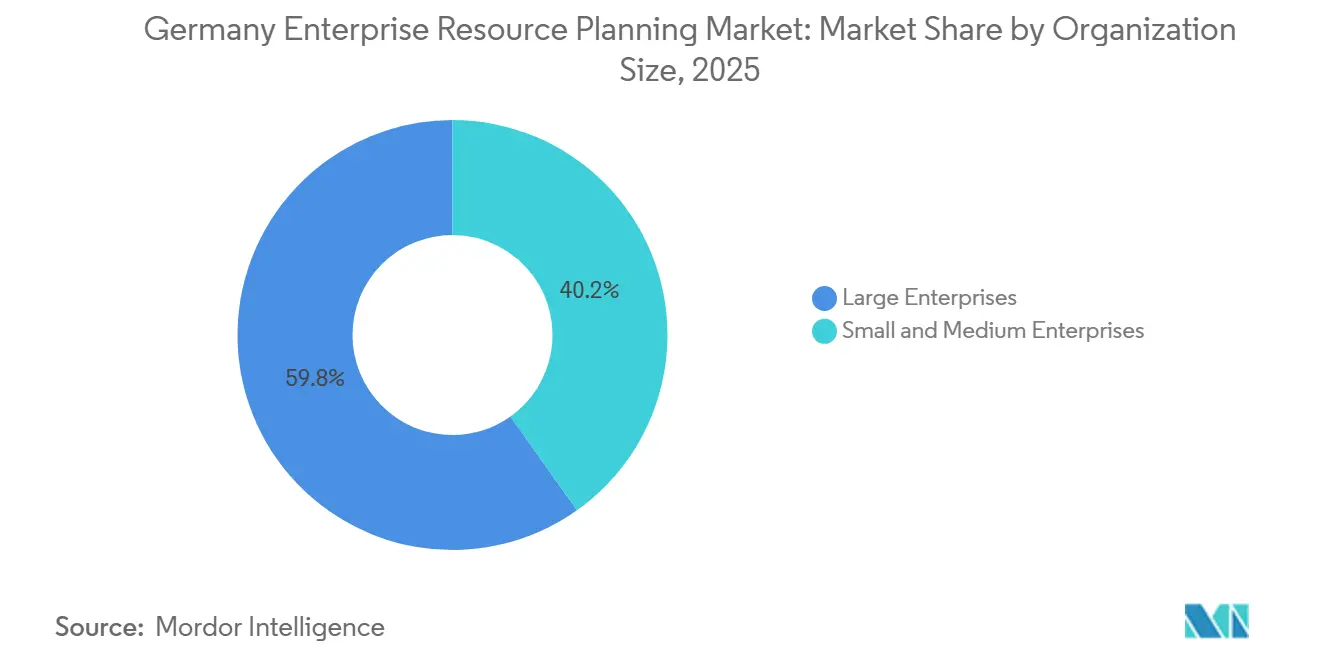

- By organization size, large enterprises commanded 59.83% of the Germany ERP market in 2025, yet SMEs are set to expand at a 14.72% CAGR between 2026-2031.

- By industry vertical, manufacturing accounted for 27.18% of the German enterprise resource planning market in 2025; healthcare and life sciences are projected to record the highest CAGR of 12.98% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Cloud Adoption Among German Mid-Market Firms | +1.8% | National, strong in Baden-Württemberg, Bavaria, North Rhine-Westphalia | Medium term (2-4 years) |

| Stringent Data Protection Regulations Driving Demand for Compliant ERP | +1.2% | National, aligned with GDPR and DSGVO | Long term (≥ 4 years) |

| Industry 4.0 Push Within German Manufacturing | +1.5% | Automotive and machinery hubs (Stuttgart, Munich, Wolfsburg) | Medium term (2-4 years) |

| Rising Need for Real-Time Supply Chain Visibility | +0.9% | National, with spillover to European subsidiaries of German multinationals | Short term (≤ 2 years) |

| De-carbonization Reporting Mandates Fueling ERP Sustainability Modules | +0.7% | National, driven by EU CSRD and Taxonomy Regulation | Medium term (2-4 years) |

| Shortage of Skilled SAP ABAP Developers Pushing Low-Code ERP Adoption | +0.5% | National, affecting enterprises with large SAP estates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Cloud Adoption Among German Mid-Market Firms

Mittelstand companies have replaced two-thirds of their core systems within two years, favoring cloud-native and hybrid models that align with vendor roadmaps and support remote work. A 2025 BITMi survey showed 82% of firms planning higher IT budgets for 2026, with 53% earmarked for cloud infrastructure.[1]BITMI.DE – German IT Budget Survey 2026 The SAP-Microsoft 99.95% SLA for Cloud ERP Private on Azure exemplifies offerings that de-risk uptime and integrate with Copilot and Teams. Yet many buyers still prefer private or sovereign clouds to avoid extraterritorial data-access laws, prompting vendors such as proALPHA to release hybrid options that keep MES on-premise while moving CRM to SaaS.

Stringent Data Protection Regulations Driving Demand for Compliant ERP

The General Data Protection Regulation, the German Federal Data Protection Act, and the EU Data Act mandate open interfaces, standardized export formats, and the abolition of switching fees by 2027. 42% of enterprises cite data protection as a barrier to public cloud adoption. SAP and Microsoft responded by partnering with Delos Cloud GmbH, which hosts workloads in German-controlled data centers to mitigate CLOUD Act concerns. For banks, the Digital Operational Resilience Act extends compliance to third-party risk management, forcing rigorous audits of ERP providers.

Industry 4.0 Push Within German Manufacturing

71% of manufacturers run Industry 4.0 applications, and 42% deploy AI in at least one business area, according to VDMA’s 2025 survey.[2]VDMA.ORG – Industry 4.0 and AI Adoption in German Manufacturing Siemens is investing EUR 200 million (USD 226 million) to transform its Amberg electronics plant into an AI-driven factory by 2030. ERP vendors now embed MES and quality analytics, turning back-office software into real-time orchestration layers; proALPHA’s 9.5 release synchronizes machine data with production orders to flag cycle-time deviations.

Rising Need for Real-Time Supply Chain Visibility

Control-tower architectures connect sensors, logistics partners, and suppliers to an event-driven ERP backbone. Continental’s 7,000-sensor deployment in Regensburg feeds cloud-based analytics that forecast disruptions and dynamically allocate parts. SAP’s Business Network for Supply Chain Collaboration delivers bi-directional updates on orders in transit, with documented ROI for German automotive tiers. Firms unable to provide live data risk being bypassed as buyers integrate directly with logistics APIs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy System Complexity and High Migration Costs | -0.9% | Enterprises with 20+ years of SAP customizations | Medium term (2-4 years) |

| Stringent Data Residency Concerns Limiting Public Cloud Uptake | -0.6% | Defense, BFSI, and public-sector verticals | Long term (≥ 4 years) |

| Economic Uncertainty Curbing IT Budgets Among SMEs | -0.4% | SMEs in cyclical industries | Short term (≤ 2 years) |

| Rising Energy Prices Increasing On-Premise TCO and Hindering Upgrades | -0.3% | Regions with high industrial electricity tariffs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy System Complexity and High Migration Costs

Currently, 71% of SAP customers continue to operate on ECC HCM, even as the May 2026 migration deadline approaches. This trend highlights the challenges posed by payroll customizations, which often make rapid re-implementation difficult. For instance, a mid-sized manufacturer is facing migration costs exceeding EUR 10 million (USD 11.3 million) and project timelines extending up to 36 months. While third-party maintenance services can provide a temporary solution by deferring upgrades, they also hinder innovation. This approach often results in organizations becoming reliant on outdated systems, which in turn locks valuable technical talent into managing legacy technical debt rather than focusing on forward-looking initiatives.

Stringent Data Residency Concerns Limiting Public Cloud Uptake

The CLOUD Act conflicts with GDPR, prompting 42% of German firms to prefer sovereign clouds or on-premise models to ensure compliance with data protection regulations. These sovereign offerings, while addressing regulatory concerns, come with a 10-20% cost premium compared to hyperscale cloud solutions. This increase in total cost of ownership (TCO) can potentially slow the adoption of new features and innovations. Delos Cloud, a notable player in this space, strives to strike a balance between sovereignty and scalability. However, customers still face the challenge of aligning their performance requirements with regulatory compliance, creating a complex decision-making process for enterprises navigating this landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Two-Tier Models Unlock Subsidiary Agility

Two-tier deployments are forecast to grow at 15.12% annually through 2031, while the Cloud-Native Suite segment captured the largest share of 48.21%. As multinational Mittelstand firms overlay lightweight regional instances atop core S/4HANA or Oracle ledgers. The Germany enterprise resource planning market size for two-tier architecture is projected to expand faster than any other segment, reflecting statutory reporting demands and cost discipline. ProALPHA’s hybrid-ready 9.5 release lets manufacturers keep latency-sensitive MES on-premises while syncing CRM to the cloud, preserving works council requirements without forfeiting global visibility. Vendors able to automate data replication and identity management across tiers will outpace competitors.

Second-order impacts include growing interface complexity and rising demand for unified admin consoles. Vendors such as proALPHA now bundle single sign-on (SSO) and multi-factor authentication (MFA) to address fragmentation and improve the user experience. As the EU Data Act enforces the use of open APIs, customers are increasingly expecting a seamless transition between edge instances and the core systems. This shift is driving the accelerated adoption of advanced integration patterns, such as message-queue systems and event-streaming architectures, which enable real-time data exchange and improved operational efficiency.

By Business Function: HCM Migrations Accelerate Under Deadline Pressure

Human capital management is projected to log a 13.28% CAGR; however, finance and accounting generated 34.97% over the forecast period. As organizations accelerate efforts to meet SAP’s H4S4 deadline. The Germany enterprise resource planning market share for HCM is expected to grow significantly, as cloud payroll adoption remains low due to the complexities of collective-bargaining rules. While finance remains the core function, the growing integration of embedded analytics and the enforcement of e-invoicing legislation are driving functional upgrades across enterprises. To stand out in the competitive landscape, vendors are incorporating advanced features such as AI-driven candidate scoring, predictive attrition analysis, and sentiment analysis into their offerings.

The persistent shortage of approximately 100,000 SAP specialists across Europe further amplifies the demand for low-code workflow builders. Enterprises are now placing greater emphasis on solutions that empower HR and finance teams to modify rules independently, without requiring ABAP coding expertise. This shift not only shortens release cycles but also reduces dependency on the limited pool of specialized consultants, enabling organizations to adapt more quickly to evolving business needs.

By Deployment Model: Hybrid Architectures Bridge Sovereignty and Scale

Cloud captured 63.44% of the Germany enterprise resource planning market in 2025 and is forecast to grow at a compound annual growth rate (CAGR) of 16.43% through 2031. However, challenges such as 30% cost overruns and the April 2025 Azure price hikes are prompting businesses to reassess their cloud strategies. Private and sovereign clouds have emerged as dominant players in regulated sectors, where compliance and data sovereignty are critical. Meanwhile, on-premises solutions remain a viable option for organizations with stable workloads and predictable utilization patterns, offering greater control over infrastructure and costs.

The EU Data Act, which became effective in 2024, has introduced significant changes to the market by reducing switching fees and mandating standardized data-export protocols. These measures have lowered the barriers for organizations to repatriate data or switch between providers, fostering a more competitive environment. Vendors that can provide unified billing and monitoring solutions across on-premise, private, and public cloud estates are expected to gain a competitive edge. This is because customers are increasingly prioritizing workload placement based on factors such as compliance requirements, latency needs, and cost efficiency, rather than being constrained by vendor-imposed limitations.

By Organization Size: SME Growth Outpaces Enterprise

SMEs are projected to grow at a compound annual growth rate (CAGR) of 14.72% through 2031, driven by the adoption of subscription-based pricing models, industry-specific templates, and zero-client browser interfaces such as proALPHA ray.[3]PROALPHA.COM – proALPHA ray browser-based interface Large enterprises captured 59.83% of the market share over the forecast period. These factors make enterprise resource planning (ERP) solutions more accessible and cost-effective for small and medium-sized enterprises. Additionally, SAP’s mid-market acceleration program and Scopevisio’s German-data-center model are gaining traction among cost-conscious buyers. These buyers prioritize localized support and seek solutions that enable rapid value realization, aligning with their operational and financial constraints.

Enterprises, while continuing to account for the majority of ERP spending, are increasingly focusing on optimizing their multi-instance estates and integrating advanced analytics capabilities. This shift reflects a broader trend toward leveraging ERP systems for strategic decision-making and operational efficiency. Vendors that position migrations as comprehensive business-transformation initiatives, emphasizing measurable outcomes and tangible benefits, are more likely to gain the support of C-suite executives. By framing these migrations as opportunities to drive innovation and achieve organizational goals, vendors can better align with enterprise leaders' priorities.

By Industry Vertical: Healthcare Digitization Outpaces Manufacturing’s Mature Base

Manufacturing accounted for 27.18% of the Germany enterprise resource planning market size in 2025, driven by the integration of ERP systems with Manufacturing Execution Systems (MES) and quality management tools to support Industry 4.0 initiatives. The sector continues to adopt advanced ERP solutions to streamline operations, enhance production efficiency, and enable real-time monitoring and decision-making. Healthcare and life sciences, benefiting from KHZG funding of EUR 4.3 billion (USD 4.9 billion), are projected to grow at a 12.98% CAGR. Hospitals are increasingly focusing on implementing patient-centric workflows that unify clinical and financial data, while serialization and traceability regulations are driving the integration of ERP systems with laboratory and pharmacy systems to ensure compliance and operational efficiency.

Retail and e-commerce vendors are accelerating their omnichannel transformation projects to meet evolving consumer demands and enhance customer experiences. Meanwhile, the BFSI sector is upgrading core ledger systems to comply with the Digital Operational Resilience Act, thereby ensuring robust, secure operations. Across all verticals, the growing emphasis on carbon-footprint tracking and sustainability is driving demand for ERP solutions with integrated ESG (Environmental, Social, and Governance) analytics. This trend is creating opportunities for vendors offering advanced sustainability modules, enabling businesses to meet regulatory requirements and achieve their environmental goals.

Geography Analysis

Germany’s ERP spend clusters in Baden-Württemberg, Bavaria, and North Rhine-Westphalia, regions known for their strong industrial base, including automotive OEMs and machinery manufacturers. These areas are experiencing intense S/4HANA migration activity, though progress is constrained by a shortage of consulting capacity. Siemens’ investment in its Amberg facility highlights the integration of ERP systems with digital twins and AI technologies, demonstrating that these leading regions are at the forefront of piloting next-generation ERP architectures to enhance operational efficiency and drive innovation.

Eastern states such as Saxony and Thuringia are emerging as significant growth areas for ERP adoption, driven by government-backed digitization incentives and the expansion of supplier networks. These regions are leveraging these initiatives to modernize their industrial and business processes. Additionally, public-sector modernization efforts are gaining momentum, guided by the OZG-RE and ZRE consolidation frameworks.[4]BUNDESREGIERUNG.DE – OZG-RE and ZRE consolidation details The mandates for XRechnung e-invoicing are being implemented across federal, state, and municipal levels, further accelerating the adoption of ERP solutions in the public sector.

Cross-border ERP deployment is also on the rise as German companies implement two-tier ERP systems in their Central and Eastern European subsidiaries. These deployments require robust multi-language and multi-GAAP support to address the complexities of operating in diverse regulatory environments. Vendors that can enable real-time financial consolidation and ensure statutory compliance across these cross-border operations are well-positioned to capitalize on this growing demand, as businesses increasingly seek seamless integration and operational transparency across their international operations.

Competitive Landscape

The Germany enterprise resource planning (ERP) market is concentrated at the enterprise level, with SAP maintaining a dominant position. SAP's partnership with Microsoft has strengthened its foothold by offering a 99.95% service-level agreement (SLA) and deep integration with Microsoft's Copilot. This collaboration enhances SAP's value proposition, particularly among risk-averse enterprises. Meanwhile, the mid-market and small-to-medium enterprise (SME) tiers remain fragmented, presenting opportunities for other players to establish a presence. ProALPHA's acquisition of Insiders Technologies highlights a strategic move to incorporate AI-driven document automation, signaling its intent to enhance cognitive capabilities through a roll-up strategy. Similarly, Abas has introduced its 2024 Q3.1 service pack, which includes Prodaso AI analytics and CO₂ tracking features, aiming to attract manufacturers under compliance pressure from the Corporate Sustainability Reporting Directive (CSRD).

Emerging disruptors such as Fabular and Metasfresh are leveraging open-source and modular cloud architectures to challenge established players. These disruptors focus on delivering faster and more cost-effective solutions, appealing to businesses seeking flexibility and efficiency. The competitive landscape is further influenced by the European Union's Data Act, which promotes open interfaces. This regulatory push reduces vendor lock-in, compelling ERP providers to differentiate themselves through the breadth of their ecosystems and the quality of their managed services. As a result, traditional players are under pressure to innovate and adapt to the evolving market dynamics.

The Germany enterprise resource planning market is undergoing significant transformation as established players and new entrants compete to address the diverse needs of enterprises, mid-market companies, and SMEs. While SAP continues to dominate the enterprise segment, its competitors are focusing on niche areas and leveraging advanced technologies to gain a competitive edge. The integration of AI, analytics, and sustainability features is becoming a key differentiator, particularly as regulatory requirements like the CSRD and the EU Data Act reshape the market. This evolving landscape underscores the importance of innovation, adaptability, and strategic partnerships in maintaining relevance and driving growth in the forecast period.

Germany Enterprise Resource Planning Industry Leaders

SAP SE

Microsoft Corporation

Oracle Corporation

Sage Group Plc

proALPHA Business Solutions GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: SAP and Microsoft launched SAP Business Data Cloud Connect for Microsoft Fabric, enabling zero-copy data exchange for real-time analytics.

- October 2025: Abas released Service Pack 2024.Q3.1, featuring advanced APS, the Prodaso AI Connector, and EU-compliant e-invoicing.

- September 2025: ProALPHA acquired Insiders Technologies to embed cognitive automation into its ERP suite.

- September 2025: The German federal government completed OZG-RE and ZRE consolidation, standardizing e-invoicing frameworks across all public administrations.

Germany Enterprise Resource Planning Market Report Scope

The Germany Enterprise Resource Planning (ERP) market comprises advanced software solutions that enable organizations to integrate and manage core business functions such as finance, supply chain, human resources, customer management, and manufacturing processes. The market reflects the growing adoption of digital, scalable, and industry-specific ERP systems across Germany.

The Germany Enterprise Resource Planning Market Report is Segmented by Architecture (Cloud-Native Suite, Mobile-First ERP, Social/Collaborative ERP, and Two-Tier/Edge ERP), Business Function (Finance and Accounting, Supply-Chain and Operations, Human Capital Management, Customer Relationship and Commerce, and Manufacturing Execution and Quality), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Industry Vertical (Manufacturing, Retail and E-commerce, BFSI, Government and Public Sector, IT and Telecom, Healthcare and Life Sciences, and Other Industry Verticals). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Native Suite |

| Mobile-First ERP |

| Social / Collaborative ERP |

| Two-Tier / Edge ERP |

| Finance and Accounting |

| Supply-Chain and Operations |

| Human Capital Management |

| Customer Relationship and Commerce |

| Manufacturing Execution and Quality |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Retail and E-commerce |

| BFSI |

| Government and Public Sector |

| IT and Telecom |

| Healthcare and Life Sciences |

| Others Industry Verticals |

| By Architecture | Cloud-Native Suite |

| Mobile-First ERP | |

| Social / Collaborative ERP | |

| Two-Tier / Edge ERP | |

| By Business Function | Finance and Accounting |

| Supply-Chain and Operations | |

| Human Capital Management | |

| Customer Relationship and Commerce | |

| Manufacturing Execution and Quality | |

| By Deployment Model | On-Premise |

| Cloud | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Industry Vertical | Manufacturing |

| Retail and E-commerce | |

| BFSI | |

| Government and Public Sector | |

| IT and Telecom | |

| Healthcare and Life Sciences | |

| Others Industry Verticals |

Key Questions Answered in the Report

What is the forecast value of the Germany enterprise resource planning market by 2031?

The market is projected to reach USD 5.56 billion by 2031.

Why are German SMEs accelerating ERP adoption?

Subscription pricing, industry templates, and browser-based interfaces reduce upfront costs and technical complexity, enabling 14.72% CAGR growth through 2031.

How will the EU Data Act influence ERP strategies?

By mandating open APIs and abolishing switching fees by 2027, the Act lowers vendor lock-in, encouraging hybrid and multi-cloud architectures.

Which business function shows the fastest growth?

Human capital management leads with a projected 13.28% CAGR, driven by the May 2026 H4S4 deadline and talent-management needs.

What sectors drive ERP spending in Germany?

Manufacturing holds the largest share at 27.18%, while healthcare and life sciences record the fastest expansion at 12.98% CAGR.

How concentrated is vendor competition?

The top five vendors account for roughly 70% of spending, indicating a market concentration score of 7.

Page last updated on: