Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

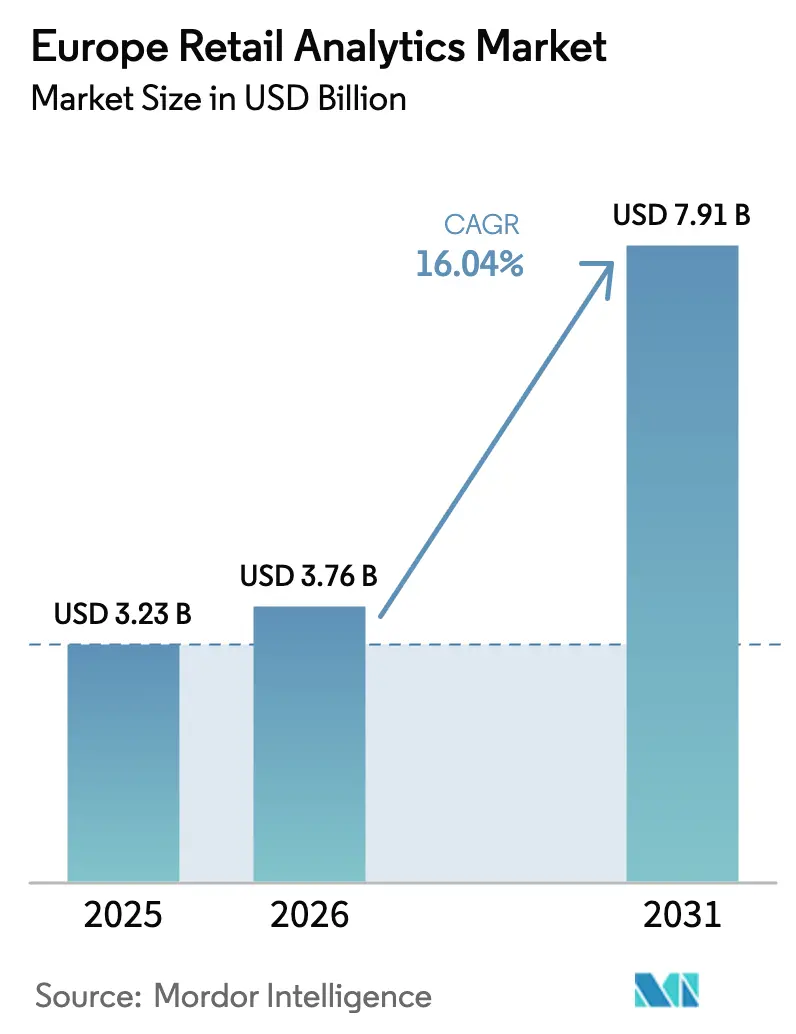

| Base Year Market Size (2025) | USD 3.23 Billion |

| Market Size (2026) | USD 3.76 Billion |

| Market Size (2031) | USD 7.91 Billion |

| Growth Rate (2025 - 2030) | 16.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Retail Analytics Market Analysis by Mordor Intelligence

The Europe retail analytics market size is projected to be USD 3.23 billion in 2025, USD 3.76 billion in 2026, and reach USD 7.91 billion by 2031, growing at a CAGR of 16.04% from 2026 to 2031. Surging investment in first-party data platforms, inflation-era margin pressure, and unified commerce mandates are accelerating platform renewals across the region. Cloud-native services that blend elastic compute with advanced AI are increasingly preferred as merchants deploy real-time pricing and computer-vision workloads. Growing reliance on privacy-enhancing technologies is steering spending toward vendors that embed consent management and explainability features by design. Competitive intensity, meanwhile, is rising as ERP incumbents embed analytics into core workflows and data-platform specialists differentiate on open architecture and EU data-residency options.

Key Report Takeaways

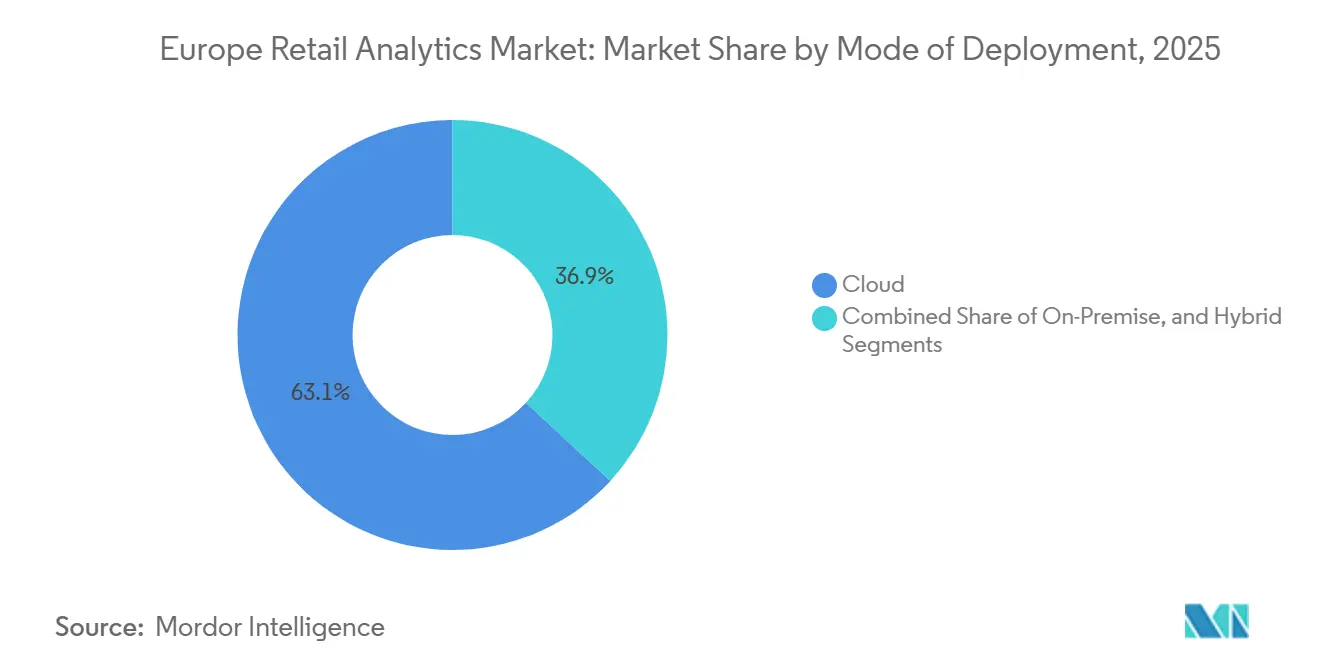

- By mode of deployment, the cloud segment led with 63.13% of Europe retail analytics market share in 2025, while the same segment is also projected to expand at a 17.83% CAGR through 2031.

- By module type, marketing and customer insights commanded 27.54% revenue share in 2025; supply-chain and fulfillment analytics is forecast to advance at an 18.02% CAGR to 2031.

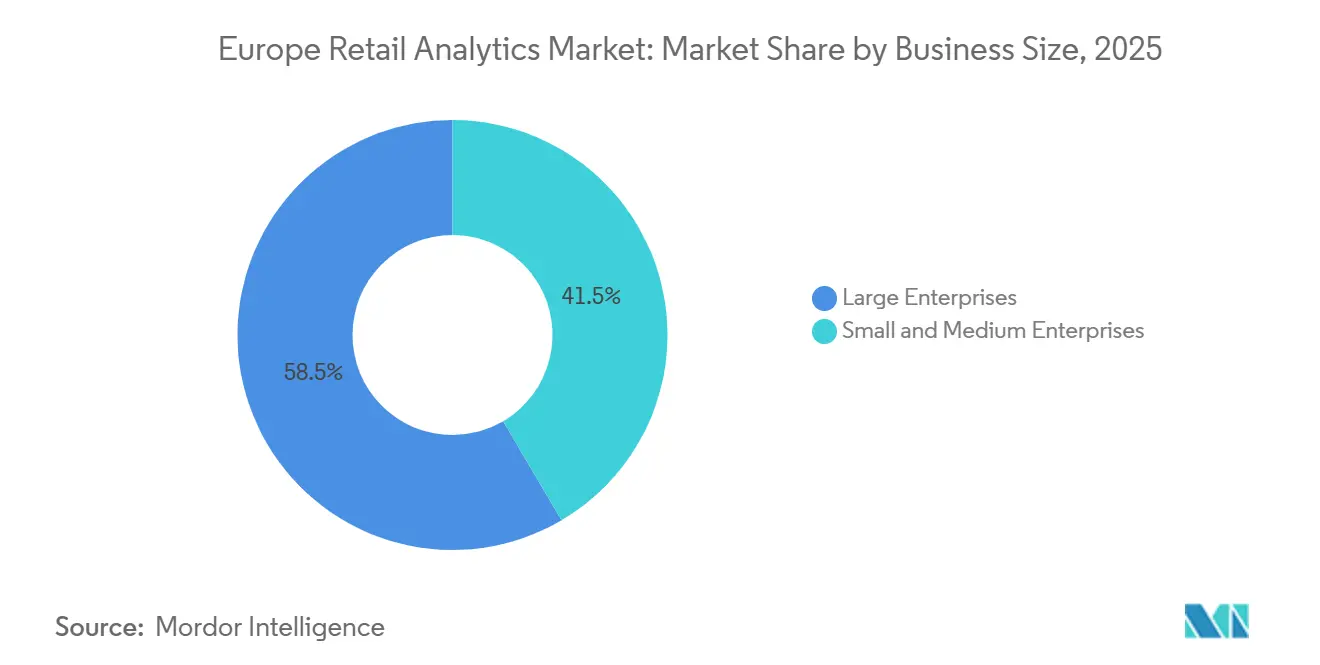

- By business size, large enterprises held 58.46% of spending in 2025, whereas small and medium enterprises are projected to grow at a 17.43% CAGR over 2026-2031.

- By retail format, omnichannel deployments captured 42.61% of implementations in 2025, and pure-play e-commerce analytics is expected to rise at a 16.93% CAGR up to 2031.

- By country, the United Kingdom accounted for 28.17% share in 2025, while Spain is anticipated to post the quickest expansion at a 16.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Retail Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Driven Personalization Lifts In-Store Conversion | +3.2% | Western Europe, Nordic region | Medium term (2-4 years) |

| AI-Powered Pricing Engines Optimize Margin in Inflationary Europe | +2.9% | Eurozone core, UK | Short term (≤ 2 years) |

| Unified Commerce Mandates Single View of Customer | +2.6% | UK, Benelux, Nordics | Medium term (2-4 years) |

| Proliferation of Edge Analytics for Real-Time Shelf Monitoring | +2.1% | Germany, France, UK | Medium term (2-4 years) |

| Retail Media Network Analytics Unlock Incremental Revenue Streams | +1.8% | UK, Germany, France | Long term (≥ 4 years) |

| ESG-Aligned Shrinkage Analytics Integrating Computer Vision | +1.5% | Western Europe, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Driven Personalization Lifts In-Store Conversion

European chains are embedding predictive models into kiosks, mobile apps, and point-of-sale terminals to surface individualized offers that lift basket size and drive repeat visits. Adobe’s 2024 benchmarking found that unified customer-data platforms improved fashion and grocery conversion rates by 20%-30%. GDPR’s value-exchange ethos makes such personalization a competitive necessity rather than a differentiator. KPMG reported that 68% of retailers plan to boost AI-led personalization budgets by 2026. Agentic commerce pilots, where AI agents negotiate bundles and payments on a shopper’s behalf, will further intensify real-time profile requirements. As data-sharing consent becomes harder to secure, merchants must showcase tangible benefits to retain first-party relationships.

AI-Powered Pricing Engines Optimize Margin in Inflationary Europe

Inflation volatility pushed grocers and fashion retailers to replace weekly price cycles with algorithms that recalibrate shelf prices several times per day. McKinsey’s 2025 grocery study documented 1-2 percentage-point gross-margin lifts among adopters during the 2024 cost-of-living squeeze. Modern engines ingest competitor feeds, weather updates, and local events, then optimize markdown calendars while guarding brand perception. BCG forecasts EUR 10 billion-EUR 15 billion (USD 11.3 billion-USD 16.9 billion) in incremental margin by 2027, provided transparency safeguards assuage regulator and consumer concerns. Vendors now bundle explainability dashboards to comply with EU AI-Act disclosure clauses.

Unified Commerce Mandates Single View of Customer

Omnichannel formats represented 42.61% of deployments in 2025, underscoring the pivot from channel-centric reporting to holistic customer views. Salesforce observed that 73% of merchants prioritized customer-data platforms to knit together e-commerce, store, and service-desk interactions.[1]Salesforce, “State of Commerce 2024,” SALESFORCE.COM Buy-online-pick-up-in-store, cross-channel attribution, and proactive retention journeys rely on this foundation. TCS measured a 15%-25% lift in customer lifetime value where a single identity graph replaced siloed data lakes. GDPR-compliant lineage tracking adds complexity, but cloud-native stacks with built-in consent auditing are easing adoption.

Proliferation of Edge Analytics for Real-Time Shelf Monitoring

Edge appliances relocate compute from distant data centers to in-store gateways, enabling sub-100-millisecond inference for object detection and planogram checks. STMicroelectronics introduced 5-watt chips purpose-built for retail vision in 2024. Sensormatic documented 20%-30% reductions in inventory loss where shrinkage alerts stream locally before summary data flows to the cloud. Processing video on-premise trims bandwidth bills and alleviates data-sovereignty worries. A secondary ESG use case is emerging as the same sensors quantify food waste, reusable packaging compliance, and fixture-level energy use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy Tightening Under GDPR and ePrivacy Regulation | -2.1% | EU27, UK, EEA countries | Short term (≤ 2 years) |

| Shortage of Retail Data-Science Talent Pool | -1.8% | Germany, UK, France, Nordics | Medium term (2-4 years) |

| Legacy POS Fragmentation Impedes Data Integration | -1.3% | Italy, Spain, Eastern Europe | Medium term (2-4 years) |

| Capital-Expenditure Freeze Among SME Retailers | -1.1% | Italy, Spain, France SME sector | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Tightening Under GDPR and ePrivacy Regulation

Proposed ePrivacy rules broaden explicit-consent demands for cookies, device fingerprinting, and location analytics, curtailing third-party identifiers that feed personalization and attribution models. The European Commission recorded a 62% refusal rate for tracking consent in 2025, shrinking campaign reach.[2]European Commission, “ePrivacy Regulation Draft 2025,” EUROPA.EU Article 22 of GDPR introduces human-in-the-loop mandates for automated decision-making, slowing dynamic pricing rollouts. Retailers are piloting differential privacy, federated learning, and synthetic datasets, but lack of mature tooling raises cost and complexity.

Shortage of Retail Data-Science Talent Pool

Competing sectors offer higher salaries, and retailers hesitate to fund multi-year upskilling. The EU’s Digital Decade program aims for 20 million ICT specialists by 2030, yet retail-specific curricula remain sparse in Southern and Eastern Europe. Vendors pitch low-code tooling to mitigate gaps, but complex use cases such as multi-echelon inventory forecasting still need Python-savvy practitioners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Deployment: Cloud Adoption Accelerates as Hybrid Matures

Cloud captured 63.13% of Europe retail analytics market share in 2025, reflecting merchants’ shift toward scalable infrastructure for real-time pricing and vision workloads. Public-cloud migration also unlocks managed AI, disaster recovery, and multi-region replication, reducing total cost of ownership for mid-cycle hardware refreshes. On-premise estates persist among grocers with legacy ERP and stringent data-residency contracts, notably in Germany and France. Hybrid architectures are emerging as a compliance hedge, allowing sensitive transactions to stay on-premise while heavy analytics batches run in the cloud. Microsoft’s 2025 hybrid SKU syncs point-of-sale data to Azure Synapse without full migration.[3]Microsoft, “Dynamics 365 Commerce Enhancements 2024-2025,” MICROSOFT.COM Snowflake’s 2024 residency controls let merchants query distributed warehouses through one interface, sidestepping Article 44 cross-border hurdles.

Greater elasticity means retailers can spin up GPU clusters during peak pricing or vision workloads, then shut them down, slashing idle costs. Vendors incentivize the transition to SAP and Oracle by discounting licenses for multi-year cloud terms, effectively funding migration projects. The Europe retail analytics market size attributable to cloud is thus forecast to widen its lead through 2031, while hybrid gains incremental traction among regulated sectors. As retailers embed edge-compute nodes inside stores, hybrid topologies will likely dominate workloads requiring both in-store latency and cloud-scale training cycles.

By Module Type: Supply-Chain Tools Outpace Customer Insight Suites

Marketing and customer insight suites held 27.54% revenue in 2025, underscoring continued appetite for personalization and retail-media measurement. Yet supply-chain and fulfillment tools are expanding fastest at an 18.02% CAGR, driven by autonomous replenishment and last-mile optimization engines that release working capital. Zalando cut overstock by 15% and achieved 98% in-stock accuracy after rolling out AI-based demand sensing. Accenture recorded 10%-20% safety-stock reductions among adopters, freeing cash for digital reinvestment. The Europe retail analytics market size attached to supply-chain modules is expected to outstrip legacy assortment-planning suites through 2031. Loss-prevention solutions fusing computer vision with shrinkage analytics are gaining ground as camera prices drop and ESG frameworks demand food-waste reporting.

Adoption trajectories differ by retailer maturity. Vertically integrated fashion houses focus on allocation and markdown optimization to preserve brand equity, while grocery chains prioritize demand forecasting to curb perishables. Category-management suites remain sticky because decades-old business rules are hard-wired, capping their growth relative to newer AI-first products. Meanwhile, financial-performance dashboards that blend P&L with operational metrics are consolidating multiple legacy BI stacks into single views, streamlining decision-maker workflows.

By Business Size: SaaS Consumption Models Democratize Analytics

Large enterprises accounted for 58.46% of spending in 2025, leveraging Europe retail analytics market capabilities to optimize vendor rebates, drive ESG reporting, and orchestrate multi-country rollouts. Growing security certifications and private-cloud options allow conglomerates to offload workloads once deemed too sensitive. SMEs, however, are the growth engine, with a 17.43% CAGR forecast as voucher programs under the EU Digital Decade subsidize first-year subscriptions up to 50%. Vendors now bundle software, integration, and support into pay-as-you-grow packages, lowering entry barriers.

Persistent obstacles remain. Independent grocers lack IT staff to align SKU hierarchies with cloud data models, and owner-operators worry about surrendering proprietary sales data. Turnkey connectors, drag-and-drop dashboards, and industry-specific templates are narrowing the gap. For large enterprises, investments are expanding into workforce analytics and supplier-risk scoring, signaling a move beyond core merchandising into holistic value-chain optimization within the Europe retail analytics industry.

By Retail Format: Omnichannel Dominates as E-Commerce Monetization Rises

Omnichannel deployments constituted 42.61% of projects in 2025, mirroring consumer demand for seamless cross-channel journeys. Unified inventory visibility, curbside pickup routing, and loyalty integration depend on Europe retail analytics market insights that reconcile online and store data in near real time. E-commerce analytics, while smaller today, is climbing at 16.93% as retail-media networks monetize on-site traffic. BCG values incremental advertising revenue between EUR 5 billion and EUR 8 billion (USD 5.6 billion-USD 9.0 billion) by 2027 for European grocers and fashion chains. Media measurement suites are therefore bundled with audience segmentation and bid-optimization algorithms, feeding a virtuous cycle in which ad dollars finance further analytical innovation.

Store-centric analytics remains crucial for foot-traffic heat-mapping, queue prediction, and staffing optimization, especially among grocery and department stores where experience drives basket size. Hybrid use cases, such as geofenced mobile promos triggered by proximity, depend on triangulating MAP data with loyalty and real-time inventory. Retailers that fuse these signals report higher redemption and attachment rates, reinforcing the strategic relevance of an integrated Europe retail analytics market strategy across formats.

Geography Analysis

The United Kingdom held 28.17% of 2025 spending, anchored by mature loyalty ecosystems, early cloud uptake, and continuous investment by grocers such as Tesco and Sainsbury’s. Tesco’s January 2025 expansion of Blue Yonder demand forecasting spans 4,000 stores, illustrating deployment scale. Sainsbury’s 2024 SAP S/4HANA Cloud migration unified ledgers with real-time analytics, trimming promotional waste. The Digital Markets Unit’s oversight imposes additional governance that smaller rivals find costly, giving incumbents compliance advantages. Brexit-related data-transfer friction persists, yet leading retailers circumvent it with EU-region data centers that preserve supply-chain visibility.

Spain is the growth pacesetter at a 16.57% CAGR to 2031, propelled by digital-first grocers like Mercadona and SME cloud vouchers. The European Commission documented 58% of Spanish SMEs targeting analytics adoption by 2026, double the 2023 level. Mercadona’s AI-driven markdown engine lifted turnover and freed cash for expansion. Italy shows heterogeneous uptake: independent retailers lag, but luxury fashion houses deploy clienteling apps that reinforce brand positioning. Germany’s market benefits from Industry 4.0 sensorization; EDEKA and REWE introduced edge-vision shrinkage systems in 2024 that processed video locally to honor data-residency clauses.

France demonstrates robust traction among hypermarkets. Carrefour’s September 2024 Blue Yonder rollout covered 12,000 stores, reducing safety stock and improving on-shelf availability. Galeries Lafayette shifted to Oracle Retail Cloud in December 2024, unifying inventory and customer records for individualized service. Across the Nordics, ESG-linked analytics is advanced as retailers track carbon and waste metrics in line with regional legislation, whereas Eastern Europe focuses on foundational inventory and POS integration. Cross-border players like Zalando showcase pan-European leverage of centralized data science to harmonize policies across diverging regulatory landscapes.

Competitive Landscape

Europe retail analytics market participants range from ERP behemoths embedding AI into transaction flows to cloud-native lakehouse innovators. SAP’s November 2025 link-up with Snowflake federates Datasphere assets into the Data Cloud, sidestepping replication while meeting GDPR minimization principles. Oracle Retail Cloud won Ocado, Peek and Cloppenburg, and WE Fashion in early 2025, highlighting appetite for unified dashboards that close attribution loops. Microsoft’s Dynamics 365 Commerce integrates Synapse Analytics for merchants like Currys, bringing in-house BI and machine learning under one subscription.

Blue Yonder, now owned by Panasonic, anchors replenishment and pricing modules for Tesco, Walmart, and METRO, marrying IoT sensors with Luminate Commerce algorithms. Snowflake’s Accelerate EMEA program subsidizes migration workshops and delivers templates tailored for demand forecasting, targeting mid-tier retailers seeking rapid ROI. Adobe, Databricks, and IBM integrate lakehouse or generative AI into commerce suites, aiming to compress data prep, modeling, and activation into unified workspaces.

Smaller disruptors carve niches. ThoughtSpot and Sisense provide natural-language query layers to democratize data consumption, though uptake remains concentrated among digital-first chains. Sensormatic and Fractal exploit computer vision for shrinkage and ESG compliance, differentiating through edge-compute deployment models. Competitive advantage increasingly pivots on AI-governance maturity, bias detection, explainability, and audit logs that align with draft EU AI-Act rules. As buyers gravitate toward multi-year suites, vendors bundle managed services to reduce integration friction, signaling a gradual consolidation phase within the Europe retail analytics industry.

Europe Retail Analytics Industry Leaders

SAP SE

Oracle Corporation

IBM Corporation

SAS Institute Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: SAP and Snowflake allied to interlink SAP Datasphere with Snowflake Data Cloud, simplifying EU-compliant data federation for retail customers.

- February 2025: METRO AG adopted Blue Yonder replenishment and markdown optimization to cut inventory costs by 10% and lift product availability by 15%.

- February 2025: Ocado Retail migrated to Oracle Retail Cloud, merging POS, inventory, and customer data for unified campaign ROI tracking.

- February 2025: Peek and Cloppenburg selected Oracle Retail Xstore and Customer Engagement to weave loyalty data into omnichannel journeys.

Europe Retail Analytics Market Report Scope

The Europe Retail Analytics Market is witnessing significant growth due to the increasing adoption of advanced analytics tools by retailers to enhance decision-making processes, optimize operations, and improve customer experiences. The integration of technologies such as artificial intelligence, machine learning, and big data analytics is driving the demand for retail analytics solutions across the region.

The Europe Retail Analytics Market Report is Segmented by Mode of Deployment (On-Premise, Cloud, Hybrid), Module Type (Strategy and Planning, Marketing and Customer Insights, Financial Management, Store Operations and Loss Prevention, Merchandising and Category Optimization, Supply-Chain and Fulfillment), Business Size (Small and Medium Enterprises, Large Enterprises), Retail Format (Brick-and-Mortar, E-Commerce, Omnichannel Retail), and Geography (United Kingdom, Germany, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Mode of Deployment

| On-Premise |

| Cloud |

| Hybrid |

By Module Type

| Strategy and Planning |

| Marketing and Customer Insights |

| Financial Management |

| Store Operations and Loss Prevention |

| Merchandising and Category Optimisation |

| Supply-Chain and Fulfilment |

By Business Size

| Small and Medium Enterprises |

| Large Enterprises |

By Retail Format

| Brick-and-Mortar |

| E-Commerce |

| Omnichannel Retail |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Mode of Deployment | On-Premise |

| Cloud | |

| Hybrid | |

| By Module Type | Strategy and Planning |

| Marketing and Customer Insights | |

| Financial Management | |

| Store Operations and Loss Prevention | |

| Merchandising and Category Optimisation | |

| Supply-Chain and Fulfilment | |

| By Business Size | Small and Medium Enterprises |

| Large Enterprises | |

| By Retail Format | Brick-and-Mortar |

| E-Commerce | |

| Omnichannel Retail | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the forecast value of the Europe retail analytics market by 2031?

It is projected to reach USD 7.91 billion by 2031.

Which deployment model leads adoption among European retailers?

Cloud deployment led with 63.13% share in 2025 and continues to grow fastest at a 17.83% CAGR.

Why are supply-chain analytics tools growing so quickly?

Autonomous replenishment and last-mile optimization engines deliver working-capital savings, driving an 18.02% CAGR for supply-chain modules.

Which country is expanding most rapidly in adopting retail analytics?

Spain is expected to post the highest growth, with a 16.57% CAGR through 2031.

What regulatory developments influence data strategy in European retail?

Stricter GDPR enforcement and the proposed ePrivacy Regulation tighten consent rules, pushing retailers toward first-party data and privacy-enhancing technologies.

How are retail media networks impacting analytics investment?

Retailers monetize on-site traffic through advertising, and the incremental revenue funds advanced measurement and bid-optimization analytics, accelerating e-commerce deployments.

Page last updated on: