Asia-Pacific Discrete GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

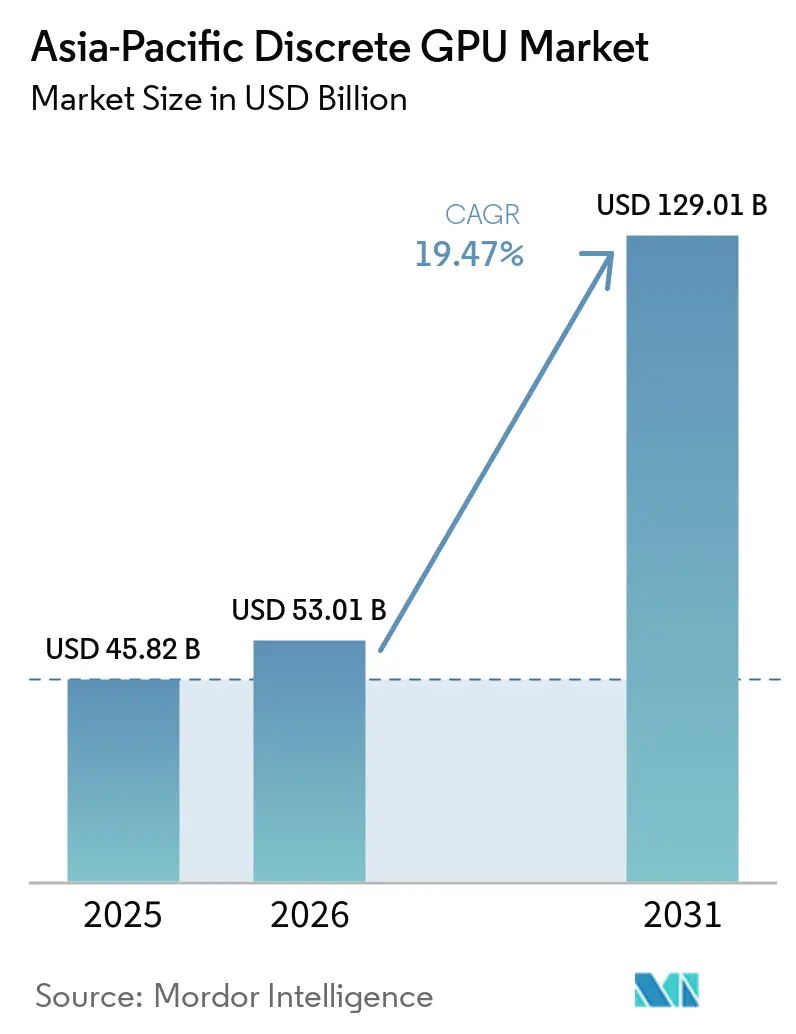

| Base Year Market Size (2025) | USD 45.82 Billion |

| Market Size (2026) | USD 53.01 Billion |

| Market Size (2031) | USD 129.01 Billion |

| Growth Rate (2026 - 2031) | 19.47% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Discrete GPU Market Analysis by Mordor Intelligence

The Asia-Pacific discrete GPU market size is expected to grow from USD 45.82 billion in 2025 to USD 53.01 billion in 2026 and is forecast to reach USD 129.01 billion by 2031 at a 19.47% CAGR over 2026-2031. Demand is shifting from consumer graphics cards toward infrastructure-grade accelerators as governments rush to establish sovereign AI capacity, hyperscalers compress upgrade cycles to support trillion-parameter models, and memory-bandwidth ceilings steer procurement toward high-bandwidth memory (HBM) architectures. Export-control restrictions on advanced U.S. chips accelerate localization in China, while India’s production-linked incentives catalyze fresh capacity in assembly and test. Energy tariffs, cooling limits, and advanced-packaging bottlenecks influence datacenter site selection, nudging new builds toward secondary cities with cheaper land and renewable energy. Competitive intensity remains high: NVIDIA enjoys a near-monopoly share of shipments, yet domestic challengers leverage policy tailwinds and pricing gaps to erode its position in entry-level inference nodes.

Key Report Takeaways

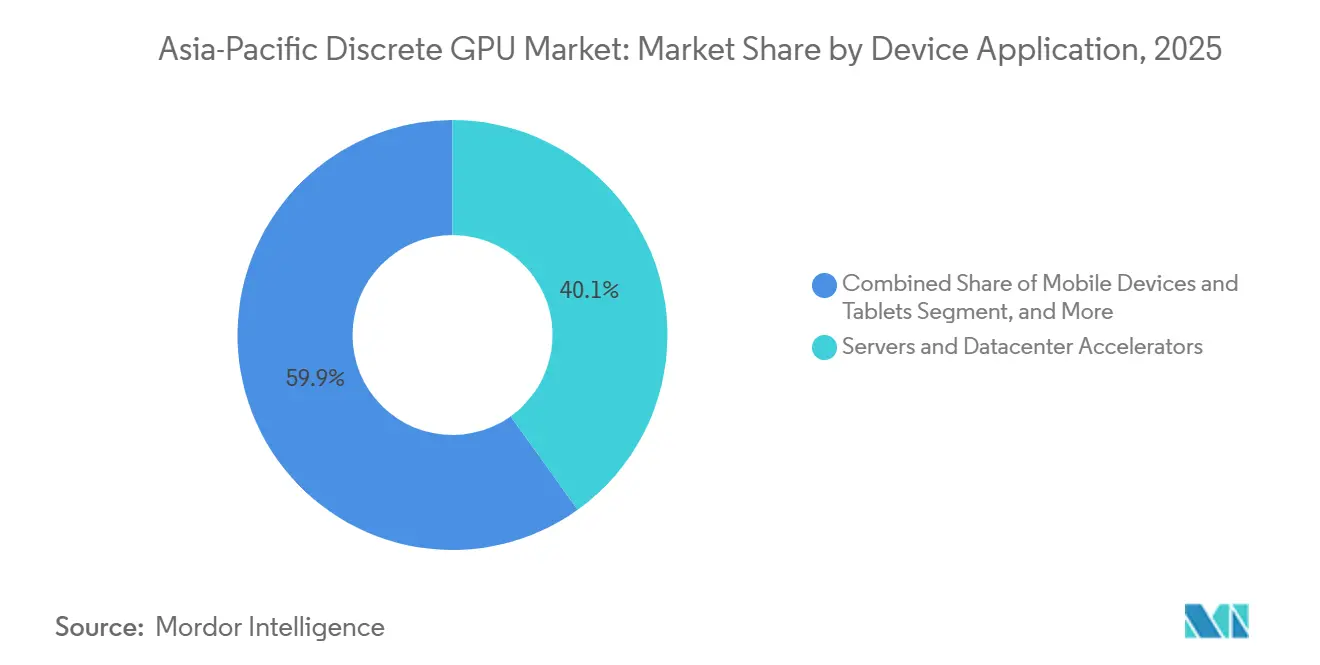

- By device application, servers and datacenter accelerators accounted for 40.10% of 2025 revenue and is expected to advance at a 19.73% CAGR through 2031.

- By memory type, GDDR-based GPUs led with 71.30% of the 2025 value, while HBM-based designs are expected to be the fastest-growing, growing by 19.88% to 2031.

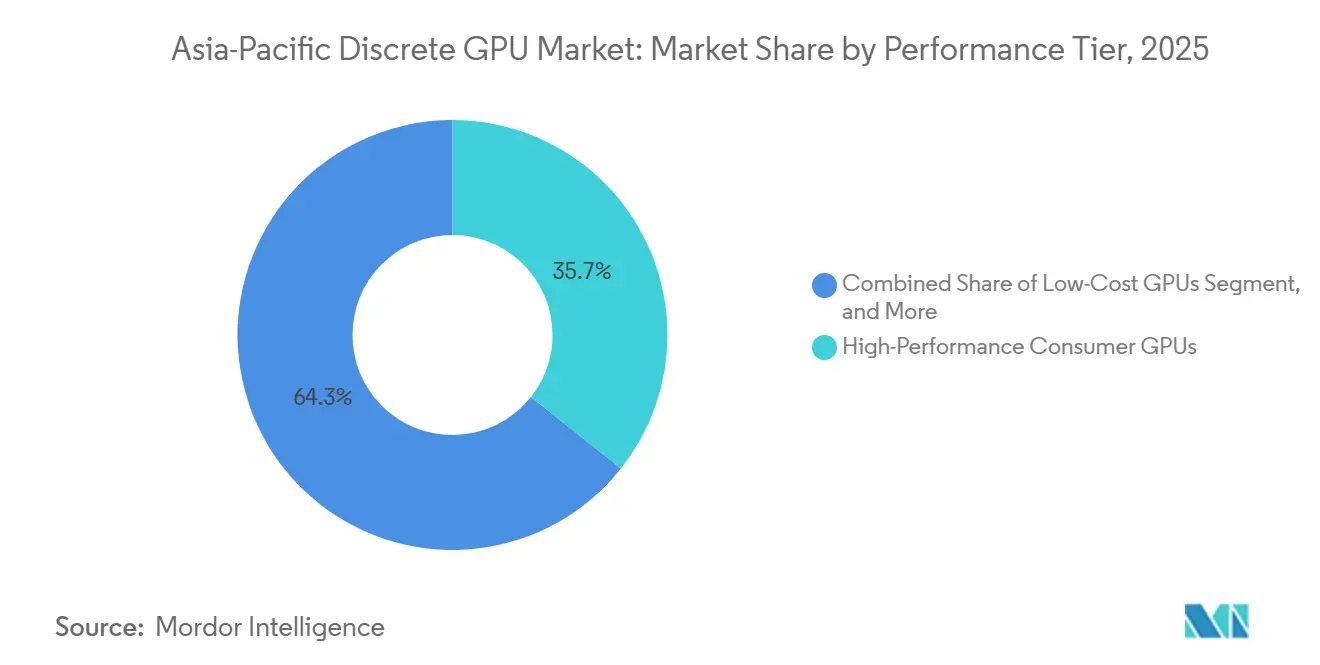

- By performance tier, high-performance consumer GPUs captured 35.66% Asia-Pacific discrete GPU market share in 2025, whereas datacenter and AI accelerators priced above USD 1,200 are projected to expand at a 19.91% CAGR.

- By country, China commanded 48.91% of regional revenue in 2025, while India is expected to be the fastest-growing geography, with a 19.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Discrete GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Exponential Growth in AI Training and Inference Workloads | +6.5% | China, India, Japan, South Korea | Medium term (2-4 years) |

| Rapid Expansion of Hyperscale Data Centers Across Asia-Pacific | +5.1% | China, India, Southeast Asia, Japan, Australia | Short term (≤ 2 years) |

| National Initiatives for Domestic GPU Manufacturing in China and India | +3.2% | China, India | Long term (≥ 4 years) |

| Rising Popularity of AAA PC and Mobile Gaming Titles | +2.8% | China, South Korea, Japan, Southeast Asia | Medium term (2-4 years) |

| Bundled GPU-as-a-Service Offerings by Regional Cloud Providers | +2.2% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Integration of Discrete GPUs into Next-Gen Augmented Reality Glasses | +1.4% | China, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exponential Growth in AI Training and Inference Workloads

Parameter counts on large language models crossed the 1-trillion threshold in 2025, pushing compute density well beyond integrated-graphics capabilities.[1]AMD Investor Relations, “AMD Secures 6-GW GPU Commitment From Meta,” ir.amd.com Meta contracted 6 gigawatts of AMD Instinct MI455X capacity in March 2026, while Oracle ordered 50,000 MI450 devices for its cloud estate. India earmarked USD 1.24 billion for 10,000 GPUs in 2025 and aims to reach 100,000 units by 2027 under its sovereign-compute agenda.[2]Government of India, “IndiaAI Mission Procurement Roadmap,” indiaai.gov.in Japan and South Korea have each budgeted roughly USD 4 billion to stand up exascale clusters, turning AI infrastructure into a strategic asset. These deployments shorten replacement cycles, front-load capital expenditure, and lift demand for top-tier accelerators featuring HBM3E memory and advanced packaging.

Rapid Expansion of Hyperscale Data Centers Across Asia-Pacific

AWS committed AUD 20 billion (USD 13 billion) to its Australian footprint, Microsoft reserved USD 2.9 billion for Japanese capacity, and Google pledged USD 3 billion for a Maharashtra facility delivering 200 megawatts by 2027. Singapore’s 2025 DataCenter-First Framework allocated 200 megawatts but mandates 50% renewable power and a sub-1.3 PUE, effectively requiring liquid-cooled GPU racks that add 15-20% to capex. Tencent Cloud and Alibaba Cloud now package NVIDIA A100 instances with elastic billing, shifting discrete GPU purchases from enterprises to hyperscalers. These investments underpin a dense procurement cycle for H100 and MI300X boards, sustain demand in the Asia-Pacific discrete GPU market, and intensify supply-chain pressure on CoWoS capacity.

National Initiatives for Domestic GPU Manufacturing in China and India

China’s “Made in China 2025” strategy accelerated Moore Threads and Biren Technology from 12 nm prototypes to 7 nm tape-outs within a year; Biren’s BR104 entered mass production in 2025 to serve inference tasks excluded from U.S. controls. Moore Threads unveiled the Huashan architecture in December 2025 and closed a CNY 660 million (USD 92 million) municipal-cloud deal in March 2026. India’s USD 10 billion semiconductor incentive lured Micron to a USD 2.75 billion assembly plant in Gujarat and prompted Tata Electronics to partner with NVIDIA on local module integration. These policies trim reliance on imported GPUs, compress vendor margins, and diversify the Asia-Pacific discrete GPU industry landscape.

Rising Popularity of AAA PC and Mobile Gaming Titles

China’s PC-gaming population climbed to 388 million in 2025 as titles such as “Black Myth: Wukong” raised the baseline GPU specs to 8 GB of VRAM with ray tracing. South Korea’s esports venues in Seoul and Busan sustain demand for 240-Hz displays that require discrete GPUs capable of 1440p play at high frame rates. Handheld PCs like ASUS ROG Ally pair integrated Radeon graphics for portable play but still rely on discrete cards for 4K docking scenarios, reinforcing mid-range update cycles. The region’s mobile-first demographic converts to PC play through value-priced GPUs under USD 400, buoying shipment volumes even as premium datacenter accelerators dominate revenue.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Ongoing Supply Chain Volatility for Advanced Process Nodes | -1.8% | Global, acute in China | Short term (≤ 2 years) |

| Intensifying Price Competition from Integrated GPUs in Entry-Level Devices | -1.5% | China, India, Southeast Asia | Medium term (2-4 years) |

| Escalating Regional Energy Tariffs Hitting Datacenter GPU TCO | -1.2% | Singapore, Japan, South Korea, Hong Kong | Short term (≤ 2 years) |

| Cooling Infrastructure Limits in Dense Urban Datacenters | -0.9% | Singapore, Hong Kong, Tokyo, Seoul | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ongoing Supply Chain Volatility for Advanced Process Nodes

By late 2026, TSMC's CoWoS line achieved a milestone of processing wafers monthly. However, NVIDIA secured a dominant share of that output, with AMD trailing, creating a tight squeeze for potential new entrants. H100 lead times stretched to 52 weeks in mid-2025, forcing customers into 18-24-month preorder windows that erode budgeting flexibility. Export-control ceilings of 4,800 H100 units per month for China diverted buyers to gray-market boards priced up to 60% above list or to lower-performance A800 variants requiring licenses.[3]Karen Hao, “Export Curbs Squeeze China’s AI Ambitions,” csis.org HBM supply remains tight as SK Hynix allocates 80% of HBM3E volume to NVIDIA, prompting a USD 13 billion expansion plan announced in March 2026, but relief arrives only after 2028. These bottlenecks weigh on the Asia-Pacific discrete GPU market by delaying deployments and inflating costs.

Intensifying Price Competition from Integrated GPUs in Entry-Level Devices

Intel’s 2025 Panther Lake mobile chips integrate Arc B390 graphics, delivering 122 GPU TOPS and enabling 1080p playback without discrete hardware in sub-USD 800 laptops. AMD’s Radeon 890M inside Ryzen AI MAX offers 60% higher performance than its predecessor, winning Lenovo and HP designs that previously used low-cost add-in boards. Qualcomm’s Snapdragon X Elite supplies 15-hour battery life that discrete GPUs cannot match, influencing enterprise procurement toward ultraportables. Price-sensitive customers in China and India are increasingly accepting integrated graphics for popular titles, dampening demand for entry-level discrete GPUs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Application: Datacenter Accelerators Anchor Revenue Growth

Servers and datacenter accelerators generated 40.10% of 2025 revenue, underscoring the outsized role of AI training clusters built by hyperscalers and sovereign clouds. The Asia-Pacific discrete GPU market is projected to expand at a 19.73% CAGR through 2031 as enterprises repatriate inference from public clouds to cost-optimized on-premises racks. NVIDIA H100 and AMD MI300X boards, priced near USD 30,000 per unit, dominate new capacity even though unit volumes trail those of consumer cards. Workstation GPUs remain important for creators using CUDA and ROCm pipelines, while console demand stays stable on the back of Nintendo’s expected late-2026 launch. Automotive adoption is nascent, yet Chinese EV makers such as BYD evaluate discrete modules for immersive cabin displays. Edge-industrial devices are a quiet growth pocket, pairing low-power boards with machine-vision workloads that CPUs cannot service.

Mainstream PC and notebook demand faces margin compression as integrated GPUs reach 80-90% of discrete performance at zero incremental bill-of-materials cost. Nevertheless, professional visualization rigs still prefer discrete cards for Adobe Premiere and Blender rendering. Gaming handhelds with hybrid architectures spur incremental volume, while research clusters in academia adopt surplus consumer cards when datacenter stockouts persist. The segment’s blend of price-elastic consumer sales and inelastic datacenter buys helps stabilize overall revenue, even as shipment mix shifts toward accelerators. As policy mandates tighten data sovereignty, regional system integrators bundle turnkey racks with 700-watt GPUs, liquid cooling, and renewable-energy sourcing agreements, reinforcing long-run growth.

By Memory Type: HBM Gains Share Despite GDDR’s Installed Base

GDDR-based boards owned 71.30% of 2025 revenue because desktop gaming and creator workstations still revolve around GDDR6X’s 21 Gbps lanes. The Asia-Pacific discrete GPU market share of HBM-based devices is smaller, yet this cohort is growing at 19.88%, as AI training requires up to 3 TB/s of bandwidth, which is unavailable on GDDR platforms. Samsung and SK Hynix inked HBM4 supply deals with AMD in March 2026, setting 13 Gbps-per-pin targets that lift MI455X throughput over 3 TB/s. Micron’s 2025 entry added a significant share to global capacity, but 40-week lead times persist because through-silicon-via stacking remains yield-constrained. GDDR7, due in late 2026, raises speed to 32 Gbps and could postpone HBM adoption for ultra-high-frame-rate gaming.

HBM’s premium cost positions it almost exclusively in datacenter accelerators, where cost-per-inference justifies the expense. Consumer graphics cards favor GDDR for better dollars-per-frame economics, yet prosumer workstations may begin adopting entry-level HBM parts once JEDEC finalizes pin-compatible packaging guidelines. Over the forecast window, the shipment mix continues to pivot toward HBM, even as revenue share lags due to higher average selling prices on accelerator boards. Memory vendors, meanwhile, front-load capex into new lines, betting that the Asia-Pacific discrete GPU market will require multiple exabytes of stacked-DRAM annually by 2031.

By Performance Tier: AI Accelerators Command Premium Pricing

High-performance consumer GPUs priced between USD 400 and USD 1,200 accounted for 35.66% of 2025 revenue, driven by enthusiasts chasing 4K-120 Hz gameplay and content creators rendering in 8K. Datacenter and AI accelerators above USD 1,200 expand fastest at 19.91% as hyperscalers prize performance-per-watt, PCIe Gen 5 bandwidth, and CUDA-core density. The Asia-Pacific discrete GPU market size for mainstream USD 100-400 boards is under pressure from integrated solutions that satisfy casual gaming needs. GPUs priced below USD 100 persist in emerging-market desktops but shrink annually as notebook penetration rises. GIGABYTE’s USD 2,499 AORUS RTX 5090 INFINITY typifies the premium niche: 600-watt thermal design, GDDR7 memory, and factory overclock for boutique render farms.[4]Gigabyte Press Office, “AORUS RTX 5090 INFINITY Launch,” gigabyte.com

Intel’s USD 949 Arc Pro B70 tries to woo CAD and medical-imaging users, yet faces inertia from CUDA-optimized software stacks. NVIDIA’s upcoming Blackwell architecture, rumored for 2027, could push flagship accelerator pricing past USD 40,000, widening the gulf between consumer and datacenter tiers. Meanwhile, China’s Moore Threads and Biren price-inference-optimized cards are 40-50% below NVIDIA A100 equivalents, carving share in municipal clouds constrained by export rules. This bifurcation ensures the Asia-Pacific discrete GPU market balances volume-driven consumer sales against value-heavy datacenter demand.

Geography Analysis

China contributed 48.91% of regional revenue in 2025, yet it confronts export-control ceilings that limit H100 inflows and elevate domestic substitutes. Moore Threads logged CNY 1.45 billion (USD 203 million) in 2025 sales and secured a CNY 660 million (USD 92 million) municipal-cloud contract in March 2026, evidence that local governments accept 30-40% performance discounts for supply sovereignty. Analysts at Bernstein expect NVIDIA’s China share to fall to 8% by late 2026 as domestic GPUs satisfy roughly 80% of incremental demand. Gaming demand is resilient, underpinned by 388 million PC players and AAA titles driving refreshes in the USD 200-600 band.

India is advancing at a 19.78% CAGR on the back of the IndiaAI Mission, which aims to deploy 100,000 GPUs by early 2027. NVIDIA and Yotta brought a 16,384-GPU H100 cluster online in mid-2025, while AMD teamed with Tata Consultancy Services on Helios rack-scale systems worth USD 250 million. Industrial power costs average 6.71 cents per kWh in 2025, one-third of Singapore’s 19.19 cents, attracting inference workloads from high-tariff hubs. Esports audiences surpassed 100 million, planting early seeds for consumer GPU upgrades.

Japan, South Korea, and Southeast Asia represent roughly one-third of regional turnover. Microsoft’s USD 2.9 billion Azure expansion delivered new GPU-ready zones across Tokyo and Osaka, while South Korea’s USD 4 billion exascale plan is stimulating demand for yield-simulation clusters at Samsung and SK Hynix fabs. Singapore allocated 200 megawatts under its DataCenter-First Framework with strict renewable-energy and PUE targets that necessitate liquid cooling.[5]GPU-NEX Research, “South Korea Exascale Cluster Plans,” gpunex.asia Malaysia and Indonesia attract hyperscalers by combining low land cost with hydroelectric power, although tropical humidity complicates heat-rejection engineering. Australia’s AWS-backed USD 13 billion expansion anchors demand for next-gen Blackwell GPUs across the rest of Asia-Pacific.

Competitive Landscape

NVIDIA controlled a significant share of discrete GPU shipments in Q4 2025, AMD captured a smaller portion, and Intel took a minimal share, giving NVIDIA pricing power but exposing it to monopsony risks as cloud buyers diversify. In March 2026, NVIDIA invested USD 5 billion in Intel for jointly developed NVLink-Fusion CPU-GPU architectures, signaling that ecosystem control now extends beyond silicon into coherent-interconnect IP. AMD countered with a USD 250 million Nutanix alliance that bundles MI455X accelerators into turnkey AI infrastructure, while its Samsung HBM4 deal ensures competitive memory bandwidth through 2028.

Chinese challengers leverage policy and price to chip away at datacenter inference. Moore Threads, Biren Technology, and Innosilicon shipped GPUs in 2025, priced below A100 while offering a portion of its performance, an attractive compromise for municipal clouds under export scrutiny. These firms increasingly differentiate through software stacks tuned for popular open-source frameworks such as PaddlePaddle and MindSpore, narrowing CUDA’s historic moat. At the edge, Intel’s Arc Pro B70 targets sub-75-watt inference nodes but faces an entrenched NVIDIA Jetson lineup and ARM-based ASICs from startups like Hailo.

Packaging and memory supply are the new choke points. TSMC allocates a significant portion of its CoWoS capacity to NVIDIA and a smaller portion to AMD, leaving little room for newcomers, while Intel’s Foveros and Samsung’s I-Cube remain behind in yield. HBM4 agreements grant AMD parity with NVIDIA H100 memory throughput, resetting competitive baselines for 2027 launches. Add-in-board makers ASUS, GIGABYTE, and MSI differentiate on thermals and factory overclocks rather than silicon, as exemplified by GIGABYTE’s AORUS RTX 5090 INFINITY, which bundles a custom PCB and GDDR7. Regulatory uncertainty over additional U.S. export rules keeps gray-market channels active, distorting official shipment counts and pressuring list pricing.

Asia-Pacific Discrete GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Samsung Electronics Co., Ltd.

Innosilicon Technology (Shanghai) Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AMD and Meta announced a 6-gigawatt GPU agreement featuring Instinct MI455X, with first-half deployment of 1 gigawatt.

- March 2026: Samsung Electronics and AMD signed a multi-year HBM4 supply memorandum targeting 3.3 TB/s bandwidth in late-2026 production.

- March 2026: NVIDIA completed a USD 5 billion strategic investment in Intel covering 215 million shares and joint NVLink-Fusion R&D.

- March 2026: Intel launched Arc Pro B70 and B65 professional cards starting at USD 949 for Asia-Pacific workstations.

Asia-Pacific Discrete GPU Market Report Scope

The Asia-Pacific Discrete GPU Market Report is Segmented by Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, and Other Embedded and Edge Devices), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs), and Country (China, Japan, South Korea, India, Southeast Asia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| GDDR-based GPUs |

| HBM-based GPUs |

| Low-Cost GPUs (Less than USD 100) |

| Mainstream GPUs (USD 100-USD 400) |

| High-Performance Consumer GPUs (USD 400-USD 1,200) |

| Data Center / AI Accelerator GPUs (Greater than USD 1,200) |

| China |

| Japan |

| South Korea |

| India |

| Southeast Asia |

| Rest of Asia-Pacific |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices | |

| By Memory Type | GDDR-based GPUs |

| HBM-based GPUs | |

| By Performance Tier | Low-Cost GPUs (Less than USD 100) |

| Mainstream GPUs (USD 100-USD 400) | |

| High-Performance Consumer GPUs (USD 400-USD 1,200) | |

| Data Center / AI Accelerator GPUs (Greater than USD 1,200) | |

| By Country | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How fast is GPU demand in Asia-Pacific data centers growing?

Servers and datacenter accelerators in the Asia-Pacific discrete GPU market are expanding at a 19.73% CAGR through 2031 as hyperscalers and sovereign clouds accelerate AI training deployments.

What memory technology is displacing GDDR in AI workloads?

HBM-based GPUs are the fastest-growing memory segment, advancing at 19.88% as large language models require bandwidth beyond GDDR6X capabilities.

Which country offers the strongest growth opportunity after China?

India is forecast to grow at a 19.78% CAGR, supported by the IndiaAI Mission’s target of 100,000 GPUs by early 2027 and low industrial power tariffs that reduce the total cost of ownership.

What factor most constrains near-term GPU supply?

Limited CoWoS advanced packaging capacity at TSMC and tight HBM allocation from SK Hynix stretch lead times to 52 weeks or more for flagship accelerators.

Are integrated GPUs threatening entry-level discrete cards?

Yes, Intel’s Arc-equipped mobile CPUs and AMD’s Radeon 890M deliver mid-range 1080p performance inside the processor package, eroding demand for sub-USD 400 discrete GPUs in price-sensitive markets.

Page last updated on: