Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

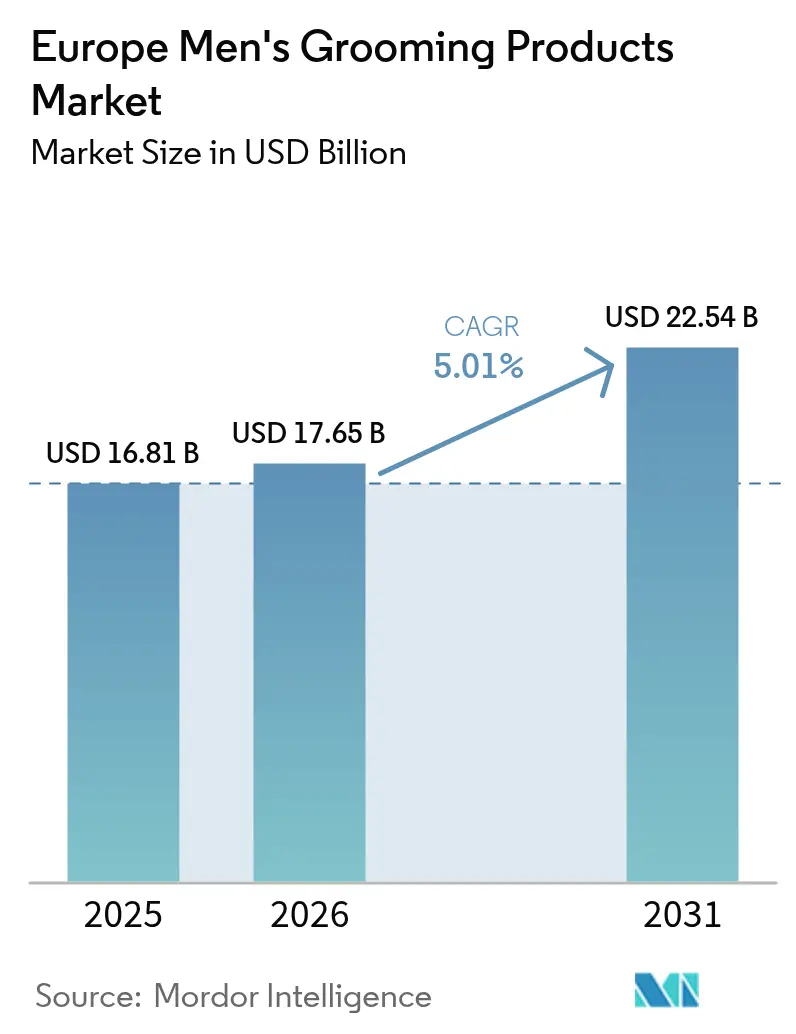

| Base Year Market Size (2025) | USD 16.81 Billion |

| Market Size (2026) | USD 17.65 Billion |

| Market Size (2031) | USD 22.54 Billion |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

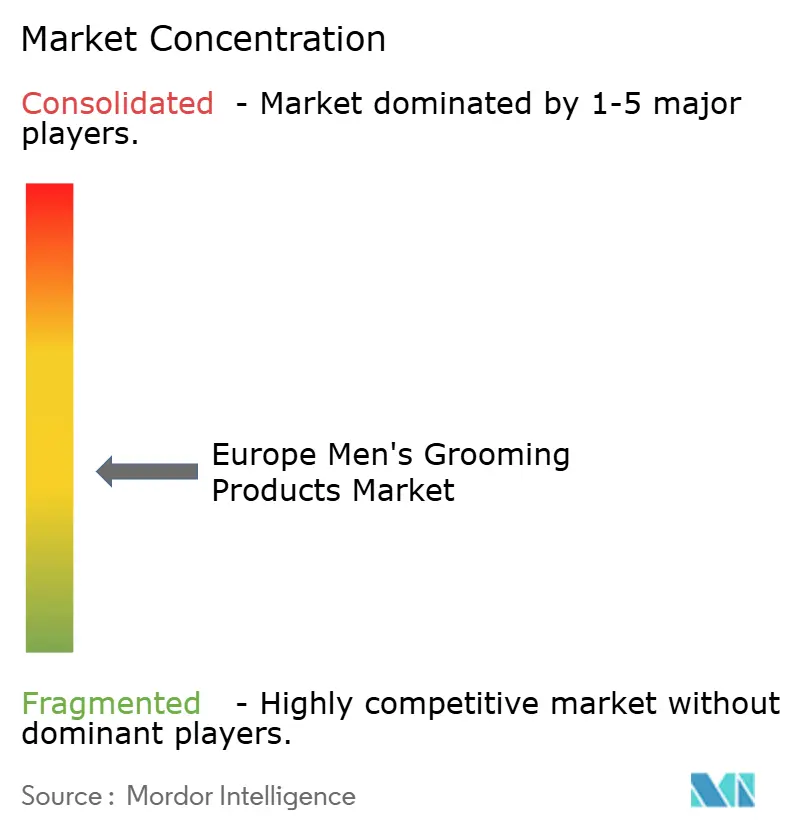

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Men's Grooming Products Market Analysis by Mordor Intelligence

The Europe men’s grooming products market size was valued at USD 16.81 billion in 2025 and estimated to grow from USD 17.65 billion in 2026 to reach USD 22.54 billion by 2031, at a CAGR of 5.01% during the forecast period (2026-2031). This growth is driven by changing cultural attitudes, increased male awareness of personal care, and an evolving definition of masculinity that incorporates grooming as part of self-expression and wellness. Men across Europe are transitioning from basic hygiene practices to more comprehensive grooming routines, boosting demand for a wider range of products. The market is experiencing significant premiumization, with consumers favoring high-quality, ingredient-rich formulations offering functional benefits such as anti-aging, hydration, and sensitivity relief. Additionally, the rising demand for natural and organic products highlights growing environmental awareness and a preference for sustainable, ethically sourced options.

Key Report Takeaways

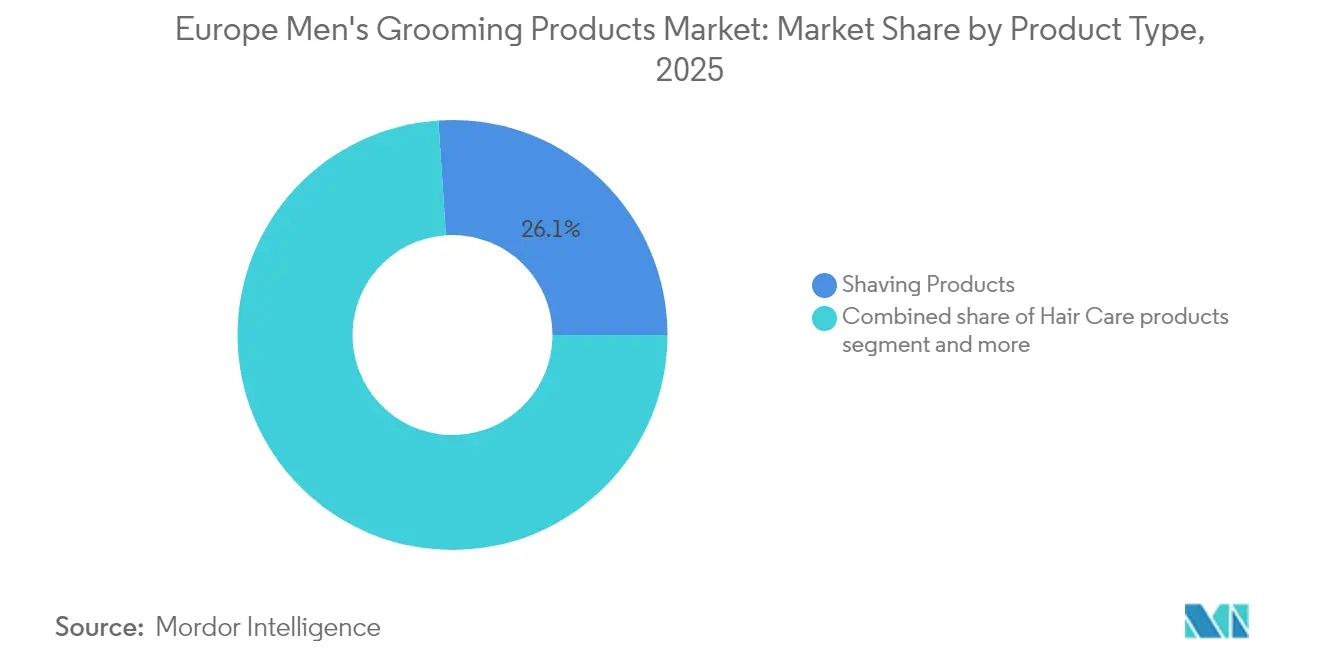

- By product type, shaving products led with 26.05% of Europe men's grooming products market share in 2025, while skincare is advancing at a 5.74% CAGR to 2031.

- By price range, mass lines held 68.10% of 2025 revenue, but premium offerings are on track for a 6.09% CAGR through 2031, the fastest in the segment.

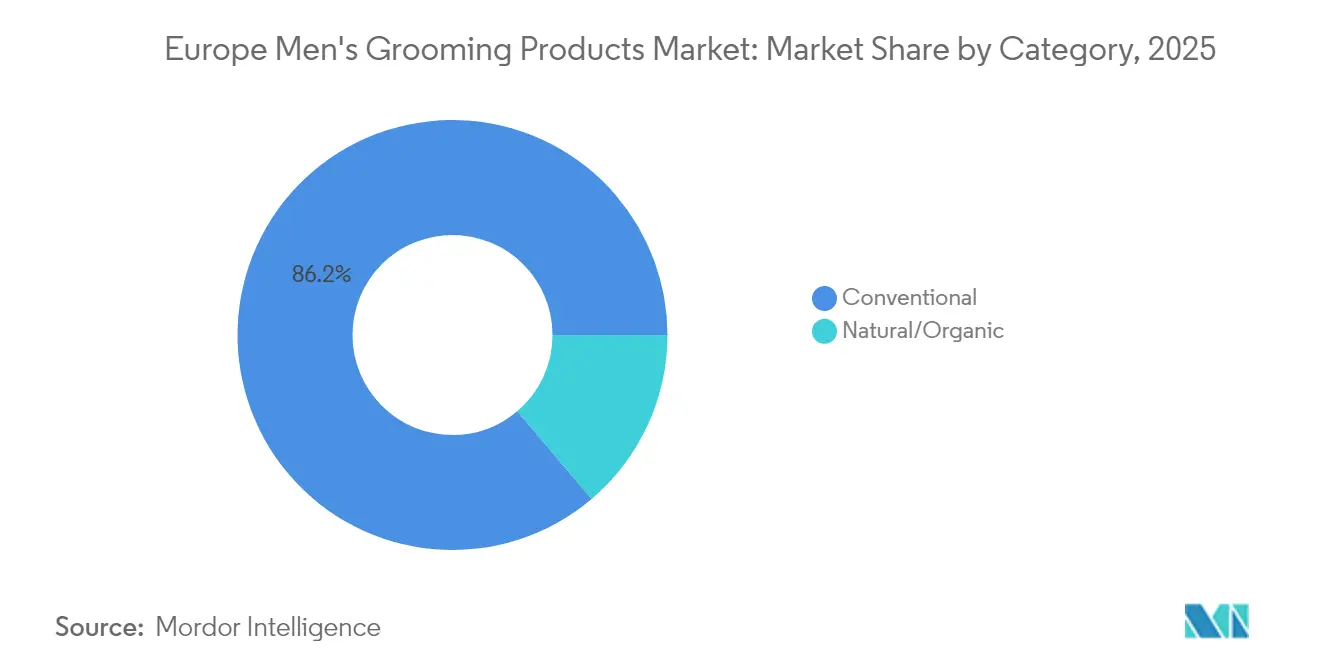

- By category, conventional formulas accounted for 86.20% of 2025 sales, yet natural and organic variants are rising at a 6.31% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets retained 38.60% share in 2025, whereas online retail stores are expanding at a 6.55% CAGR through 2031.

- By geography, Germany captured 20.70% of regional revenue in 2025; Poland is the fastest-growing market at a 6.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Men's Grooming Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Changing cultural attitudes and evolving masculinity norms | +0.8% | Regional, strongest in United Kingdom, Germany, Nordics | Medium term (2-4 years) |

| Workplace and social appearance expectations | +0.7% | Western Europe (United Kingdom, France, Germany, Benelux) | Short term (≤ 2 years) |

| Product innovation and diversification | +1.2% | Regional, led by Germany, France, United Kingdom | Long term (≥ 4 years) |

| Growing demand for beard care and styling | +0.6% | Western and Southern Europe, urban centers | Medium term (2-4 years) |

| Increased focus on premium and sustainable formulations | +1.1% | Western Europe, spill-over to Poland, Czechia | Long term (≥ 4 years) |

| Influence of social media, celebrities and influencers | +0.9% | Regional, particularly United Kingdom, France, Italy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Changing cultural attitudes and evolving masculinity norms

Changing cultural attitudes and evolving masculinity norms are driving growth in the Europe men’s grooming products market. Traditional perceptions of male self-care are shifting, with greater acceptance of grooming, skincare, and personal wellness. Modern European men increasingly view grooming not only as a hygienic practice but also as a means of expressing personal style, confidence, and individuality. This shift has reduced historical stigmas associated with the use of skincare, haircare, and cosmetic products. Social media, influencer culture, and targeted marketing campaigns have further accelerated this trend by normalizing discussions around skincare routines, facial hair styling, and premium grooming practices. These changing norms have also encouraged men to explore new product categories, including anti-aging treatments, natural and organic products, multifunctional skincare, and fragrances, which were previously considered niche or feminine. Consequently, the market is experiencing higher consumer engagement, increased adoption across various age groups, and a growing willingness to invest in premium and innovative grooming solutions, driving overall market expansion.

Workplace and social appearance expectations

Workplace and social appearance expectations are key factors driving the growth of the Europe men’s grooming products market. Professional environments and social settings increasingly emphasize well-groomed appearances as essential for personal branding and career advancement. According to the Office for National Statistics, the United Kingdom's employment rate reached 75.0% in 2024, reflecting greater participation in competitive job markets [1]Source: Office for National Statistics, "Employment in the UK: October 2024", ons.gov.uk. In such environments, polished appearances are often associated with professionalism, confidence, and social acceptance. This trend motivates men to adopt comprehensive grooming routines, including skincare, haircare, shaving, and styling products, to meet formal workplace standards and evolving social norms. The need to maintain a neat and fresh appearance throughout the workday and in social interactions further drives demand for multifunctional, long-lasting, and user-friendly grooming solutions. Moreover, increased workforce participation boosts the frequency of grooming product purchases and experimentation, as men seek products that enhance their personal image and align with contemporary expectations in both professional and casual settings.

Product innovation and diversification

Product innovation and diversification are key factors driving growth in the Europe men's grooming products market by expanding product offerings and addressing increasingly sophisticated consumer demands. Brands are moving beyond traditional categories to develop specialized products tailored to specific hair types, styling preferences, and skin concerns. This approach helps capture a broader audience and promotes more frequent purchases. For example, in July 2025, Robin James launched the premium male hair care brand Anforh, introducing products such as Texture Volume Spray and Texture Shampoo, which focus on enhancing hair texture and volume areas previously underserved in men's grooming. These innovations appeal to style-conscious consumers seeking personalized solutions and elevate the perception of male grooming from basic hygiene to a more refined personal care experience. Diversification into niche segments, including volumizing sprays, scalp treatments, and multi-benefit shampoos, reflects the growing preference among men for multifunctional, effective, and high-quality products.

Growing demand for beard care and styling

The increasing demand for beard care and styling products is a key driver in the Europe men’s grooming market, reflecting evolving trends where facial hair has become a prominent aspect of personal style and identity. Men are increasingly purchasing specialized products, including beard oils, balms, shampoos, and grooming tools, to maintain, style, and condition their beards. This shift has significantly expanded the traditional shaving category into a broader facial hair care segment, catering to diverse grooming preferences. According to Cosmetica Italia, in 2023, approximately EUR 58.4 million worth of soaps, shaving foams, and gels for men were sold in Italy alone, underscoring strong consumer interest in products that cater to both clean-shaven looks and well-maintained beards [2]Source: Cosmetica Italia, "Consumption of men's care products in Italy", cosmeticaitalia.it. This growth is further fueled by a rising number of men adopting beards as a fashion statement and seeking products that address specific facial hair care needs, such as moisturizing the skin beneath the beard, preventing irritation, and shaping it effectively to achieve a polished appearance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulations | -0.5% | Europe-wide, strictest in Germany, France | Long term (≥ 4 years) |

| Prevalence of fake grooming items | -0.3% | Southern and Eastern Europe, online channels | Medium term (2-4 years) |

| Intense competition and market saturation | -0.6% | Western Europe (Germany, United Kingdom, France) | Short term (≤ 2 years) |

| Private Label Alternatives | -0.4% | Germany, United Kingdom, Netherlands, discount chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations

Stringent regulations pose a significant challenge to the Europe men’s grooming products market, as manufacturers must comply with complex and frequently changing legal requirements related to product safety, ingredient usage, labeling, and environmental impact. European regulatory bodies enforce strict standards, such as the EU Cosmetics Regulation (EC) No 1223/2009, which mandates extensive testing, ingredient transparency, and adherence to restrictions on substances deemed harmful or controversial. These regulations can extend product development timelines, increase costs associated with formulation changes, safety evaluations, and documentation, and restrict the use of certain widely used ingredients, particularly in categories like fragrances, preservatives, and colorants. Smaller brands and new market entrants face heightened compliance challenges due to limited resources, which can hinder innovation and reduce market responsiveness.

Prevalence of fake grooming items

The prevalence of counterfeit grooming products presents a significant challenge to the Europe men’s grooming market by eroding brand trust, compromising product safety, and disrupting legitimate sales channels. These counterfeit products, often distributed through unauthorized retailers or online platforms, may contain harmful ingredients, lack quality control, and fail to comply with regulatory standards. This exposes consumers to risks such as skin irritation and allergic reactions, thereby undermining confidence in men’s grooming brands. Furthermore, counterfeit sales divert revenue from authentic manufacturers and authorized distributors, negatively impacting profitability and reducing resources available for innovation. The presence of fake products also increases the complexity of brand protection efforts, necessitating enhanced monitoring, legal actions, and consumer education, all of which contribute to higher operational costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skincare Gains as Anti-Aging Formulations Mature

Shaving products accounted for 26.05% of the Europe men’s grooming products market revenue in 2025, maintaining a dominant position due to the high-frequency nature of shaving among European men. This segment's strength lies in its essential role as a routine necessity for a broad demographic, spanning various age groups, professions, and cultural backgrounds. Its stability and recurring demand are unmatched by many other grooming categories. The segment's leadership is further bolstered by continuous product innovation. Modern razors and blades feature advanced ergonomics, precision steel, lubrication strips, and flexible heads to enhance comfort and minimize irritation. Additionally, pre-shave creams, oils, and soaps have evolved to provide improved moisturization, skin protection, and smoother application.

Skincare is projected to grow at a robust CAGR of 5.74% from 2026 to 2031, significantly influencing the dynamics of the Europe men’s grooming market. This growth is driven by a shift among male consumers from basic hygiene routines to more advanced, health-focused personal care habits. Increasing awareness of issues such as dryness, acne, sensitivity, pollution damage, and early signs of aging has led men to adopt products like cleansers, moisturizers, sunscreens, and targeted treatments, which were previously overlooked or used inconsistently. The segment's expansion is further supported by science-backed formulations and dermatology-inspired products tailored to men’s thicker, oilier, and more irritation-prone skin, offering a more personalized and functional skincare experience.

By Price Range: Premium Segment Captures Sustainability and Efficacy Premiums

Mass-market products accounted for a significant 68.10% of Europe men’s grooming sales in 2025, maintaining their position as the cornerstone of the market. These products offer accessibility, familiarity, and broad appeal, aligning with the everyday grooming needs of most male consumers. Their dominance is attributed to their role as essential, repeat-purchase items, encompassing key categories such as shaving essentials, basic skincare, body care, deodorants, and haircare. These products are integral to routine hygiene rather than discretionary self-care. Mass-market brands have sustained their relevance by consistently upgrading formulations, incorporating skin-friendly ingredients, and modernizing packaging while keeping prices affordable. This ensures they remain the preferred choice for value-conscious and habitual shoppers. Their extensive product range, from simple moisturizers to multi-functional grooming solutions, caters to men seeking straightforward routines with reliable performance.

Premium offerings, projected to grow at a 6.09% CAGR through 2031, are transforming Europe men’s grooming market by addressing a growing demand for high-quality, performance-oriented, and experience-driven grooming solutions. This segment’s growth reflects an increasing willingness among men to invest in their appearance, skin health, and personal identity. Moving beyond basic hygiene, premium products emphasize indulgence, refinement, and self-care as aspirational lifestyle elements. These products stand out through advanced formulations, dermatologist-approved ingredients, superior textures, refined fragrances, and targeted benefits such as anti-aging, hydration, sensitive-skin care, beard conditioning, scalp treatments, and specialized styling. These features appeal to consumers who are becoming more educated, ingredient-conscious, and focused on product efficacy.

By Category: Natural and Organic Formulations Ride Clean Beauty Wave

Conventional products accounted for a significant 86.20% of Europe’s men’s grooming revenue in 2025, maintaining their dominance due to their alignment with everyday grooming routines and long-standing consumer preferences. These products, which include traditional skincare, shaving essentials, and deodorants, benefit from decades of brand trust, established formulations, and widespread availability. They remain the default choice for the majority of male consumers who prioritize practicality, familiarity, and reliability over novelty. Conventional ranges are perceived as dependable and consistent in performance, appealing to men who prefer straightforward routines and are less inclined to experiment with new ingredients or niche formulations.

Natural and organic variants, projected to grow at a strong 6.31% CAGR from 2026 to 2031, are reshaping the future of the Europe men’s grooming market. This growth reflects a shift in consumer preferences toward cleaner, safer, and more environmentally responsible grooming choices. Men are increasingly ingredient-conscious, questioning the safety, sourcing, and environmental impact of the products they use on their skin, hair, and facial hair. According to the Center for the Promotion of Imports (CBI), European buyers are placing greater emphasis on sustainable resource management, driven by rising consumer demand for eco-friendly beauty and personal care products. This trend is particularly evident in markets like Germany, where nearly 60% of consumers express concerns about ingredient origin and transparency . As a result, men are increasingly opting for formulations that are plant-based, responsibly sourced, cruelty-free, and free from harsh chemicals such as parabens, sulfates, and synthetic fragrances.

By Distribution Channel: Online Retail Gains as DTC Brands and Omnichannel Players Converge

Supermarkets and hypermarkets, accounting for 38.60% of Europe men’s grooming distribution share in 2025, remain crucial in enhancing market accessibility and influencing consumer purchasing behavior. Their extensive reach, convenience, and ability to provide a wide range of products under one roof make them a preferred choice for male consumers. These retail formats cater to those who value one-stop shopping, routine replenishment, and easy access to essential grooming products such as shaving items, basic skincare, haircare, and deodorants. Their effectiveness is further supported by strategic shelf placement, in-store promotions, loyalty programs, and a broad representation of brands, which collectively boost visibility, encourage impulse purchases, and strengthen consumer familiarity with key brands.

Online retail stores, growing at a robust 6.55% CAGR through 2031, are reshaping Europe men’s grooming market by redefining how consumers discover, evaluate, and purchase products. This growth reflects a shift in consumer preferences toward convenience, personalization, and privacy, particularly in categories such as skincare, shaving, and premium grooming products. E-commerce enables consumers to access a broader assortment, including niche and premium items that may not be consistently available in traditional retail outlets. L’Oréal’s 2024 annual report highlights this trend, reporting e-commerce sales of EUR 12.3 billion, emphasizing the channel’s growing importance within the beauty and personal care industry. Online retail also supports direct-to-consumer engagement, allowing brands to foster loyalty through subscriptions, personalized recommendations, and targeted promotions. Furthermore, digital platforms provide brands with opportunities to strengthen consumer relationships and expand their reach.

Geography Analysis

Germany accounted for 20.70% of Europe men’s grooming market revenue in 2025, representing the largest country share on the continent. This dominance is attributed to the enduring success of Beiersdorf’s Nivea Men franchise and a robust network of drugstore chains, such as DM-Drogerie Markt, which operates over 4,000 stores nationwide. The market leadership is further supported by well-established consumer habits, high awareness of male grooming routines, and strong brand loyalty, particularly in the shaving, skincare, and haircare segments. German consumers’ trust in legacy brands and the availability of a diverse range of both mass-market and premium products position Germany as a key market in Europe, serving as a benchmark for product launches, innovation, and category growth.

Poland is emerging as the fastest-growing market in Europe, with a projected CAGR of 6.68% from 2026 to 2031. This growth is driven by increasing awareness of male grooming, rising disposable incomes, and the expansion of retail networks in urban and suburban areas. These factors are positioning Poland as a significant growth market within the region. The United Kingdom remains a key market despite economic challenges. The expansion of international retailers, such as Sephora, which plans to operate over 20 stores by 2027, is enhancing access to premium and niche grooming products. This continued retail growth supports the country's position as a significant player in the European men’s grooming market.

Spain is characterized by high price sensitivity and a preference for multifunctional grooming products that combine skincare and personal care benefits. This pragmatic consumer approach emphasizes value and efficiency, reflecting a market trend that prioritizes practicality over indulgence. The Netherlands, France, and Italy remain strategically important due to their large consumer bases, mature retail infrastructure, and openness to both premium and mass-market grooming innovations. These markets play a critical role in shaping the European men’s grooming landscape. Sweden and the broader Nordic region exhibit strong demand for natural and organic formulations.

Competitive Landscape

The Europe men’s grooming products market is moderately concentrated, with multinational corporations such as Procter & Gamble Company, Unilever PLC, Beiersdorf AG, L’Oréal S.A., and Edgewell Personal Care Company dominating the landscape. These companies maintain leadership across key categories, including shaving, skincare, haircare, and deodorants, by leveraging extensive product portfolios, strong brand equity, and broad distribution networks. Their market position is further strengthened by consistent investments in marketing, research and development, and the introduction of regionally tailored products that address diverse consumer preferences across Europe. Despite this concentration, the market remains competitive due to the presence of emerging niche players and shifting consumer demands.

White-space opportunities exist in specialized segments such as beard care, where established brands have been slower to develop targeted formulations for grooming, conditioning, and styling. This has created space for smaller companies and start-ups to introduce premium products, including oils, balms, and grooming kits tailored to facial hair management. These offerings appeal to a growing segment of younger, style-conscious male consumers. Additionally, categories such as natural and organic grooming products and multifunctional skincare are attracting new entrants. Consumers increasingly prioritize products that combine effectiveness with sustainability, ingredient transparency, and ethical sourcing. These trends present opportunities for innovation and differentiation, challenging established players to expand beyond traditional product lines.

The European market exhibits a bifurcated structure, with mass-market brands and premium specialists adopting distinct strategies. Volume-driven mass brands emphasize widespread distribution, competitive pricing, and fostering repeat-purchase loyalty. In contrast, premium players focus on differentiation through ingredient innovation, clean or organic formulations, sustainability credentials, and experiential retail partnerships. Premium brands increasingly utilize boutique stores, e-commerce platforms, and curated in-store experiences to engage consumers, enhance brand perception, and justify higher price points. This dual approach highlights the importance of balancing scale with differentiation to remain relevant, as companies address the growing demand for personalized, premium, and sustainable grooming solutions across Europe.

Europe Men's Grooming Products Industry Leaders

-

Procter & Gamble Company

-

Beiersdorf AG

-

L’Oréal S.A.

-

Unilever PLC

-

Edgewell Personal Care Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Unilever announced that it has signed an agreement to acquire the personal care brand Dr. Squatch from the growth equity firm Summit Partners. The brand provides a range of products, including natural soaps, body washes, deodorants, hair care, skin care, and other men's grooming items.

- May 2025: Manscaped announced its launch in Harrods, a renowned luxury department store in the United Kingdom, known for offering premium men's grooming products.

- March 2025: Slick Gorilla introduced their first Daily 2-in-1 Shampoo and Conditioner. It is formulated with Panthenol, a key ingredient that provides hydration and moisture. The product is vegan, cruelty-free, and manufactured entirely in the United Kingdom.

- September 2023: Gillette has introduced a new shaving range specifically designed for men's intimate areas. The product line includes a trimmer, razor with blades, and shower and shaving cream, all formulated to cater to the needs of more sensitive areas of the body.

Europe Men's Grooming Products Market Report Scope

Europe men's grooming products market is segmented by product type into shaving products and razors and blades. The shaving products segment is further classified into pre-shave and post-shave segments with the former comprising of shaving cream, pre-shave oil, shaving soap, and others. The post-shave sub-segment comprises of after-shave, balms, and others. The market is differentiated by distribution channels into specialty stores, supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. The market is also segmented by geography into the United Kingdom, France, Germany, Spain, Russia, Italy, and the rest of Europe.

By Product Type

| Skin Care products | Face Wash | |

| Moisturizers | ||

| Face Mask | ||

| Other Skin Care Products | ||

| Hair Care products | Shampoo and Conditioners | |

| Styling Products | ||

| Hair Colorants | ||

| Other Hair Care Products | ||

| Shaving Products | Pre-Shave | Shaving Cream |

| Pre-Shave Oil | ||

| Shaving Soap | ||

| Other Pre-Shave Products | ||

| Post-Shave | After-Shave | |

| Balms | ||

| Other Post-Shave Products | ||

| Razors and Blades | ||

| Other Product Types | ||

By Price Range

| Mass |

| Premium |

By Category

| Conventional |

| Natural/Organic |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Retail Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Skin Care products | Face Wash | |

| Moisturizers | |||

| Face Mask | |||

| Other Skin Care Products | |||

| Hair Care products | Shampoo and Conditioners | ||

| Styling Products | |||

| Hair Colorants | |||

| Other Hair Care Products | |||

| Shaving Products | Pre-Shave | Shaving Cream | |

| Pre-Shave Oil | |||

| Shaving Soap | |||

| Other Pre-Shave Products | |||

| Post-Shave | After-Shave | ||

| Balms | |||

| Other Post-Shave Products | |||

| Razors and Blades | |||

| Other Product Types | |||

| By Price Range | Mass | ||

| Premium | |||

| By Category | Conventional | ||

| Natural/Organic | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Convenience Stores | |||

| Specialty Stores | |||

| Online Retail Stores | |||

| Other Retail Channels | |||

| By Geography | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

Key Questions Answered in the Report

What is the projected value of the Europe men's grooming products market by 2031?

The market is forecast to reach USD 22.54 billion by 2031.

Which product type is expanding fastest across Europe?

Skincare lines tailored to men are advancing at a 5.74% CAGR.

Which country shows the highest growth rate in men’s grooming sales?

Poland leads with a 6.68% CAGR through 2031.

How significant is online retail for men’s grooming in Europe?

Online sales are rising at a 6.55% CAGR, outpacing all other channels.

Page last updated on: