Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

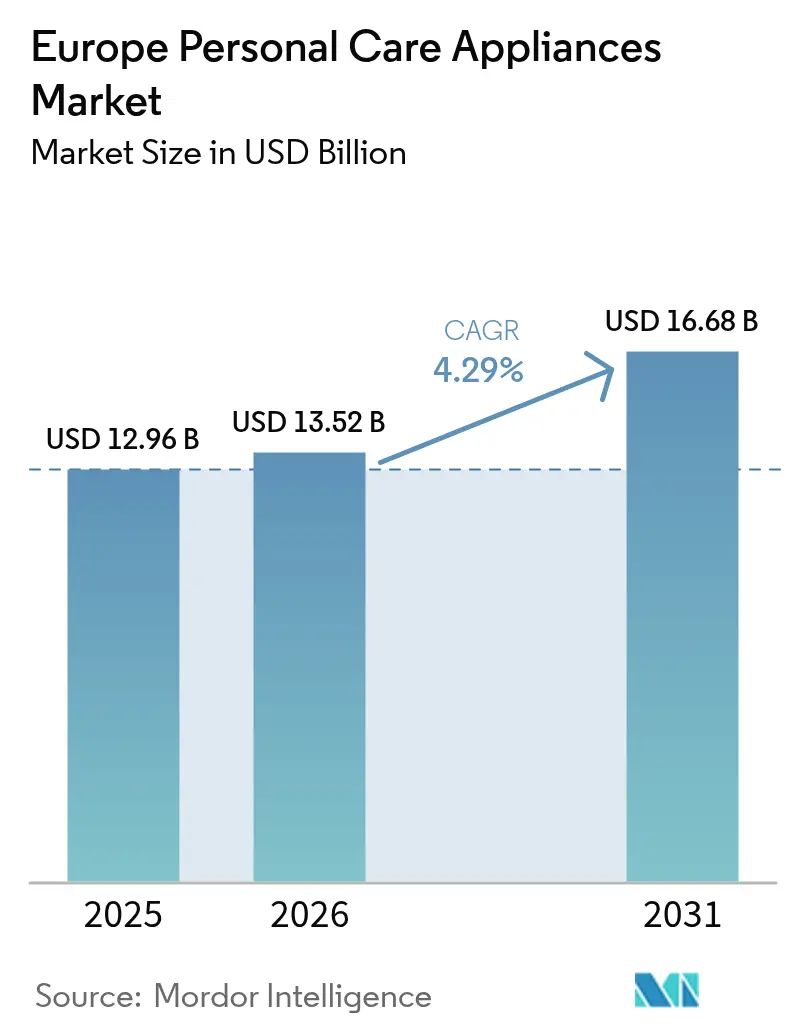

| Base Year Market Size (2025) | USD 12.96 Billion |

| Market Size (2026) | USD 13.52 Billion |

| Market Size (2031) | USD 16.68 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Personal Care Appliances Market Analysis by Mordor Intelligence

The Europe Personal Care Appliances Market size market is expected to grow from USD 12.96 billion in 2025 to USD 13.52 billion in 2026 and is forecast to reach USD 16.68 billion by 2031 at 4.29% CAGR over 2026-2031. This growth trajectory reflects the region's mature yet evolving consumer landscape, where traditional shaving and grooming routines are increasingly complemented by sophisticated styling technologies and smart connectivity features. The market's moderate expansion masks significant underlying shifts, particularly the accelerating adoption of cordless technologies and the premiumization strategies deployed by major players to offset regulatory cost pressures. Demand is shifting from basic grooming aids toward technology-rich, network-ready tools that promise precision, portability, and lower lifetime environmental impact. Premiumization helps leading brands absorb regulatory cost pressures while cordless formats gain ground thanks to fast-charging lithium-ion systems. Social-commerce engines amplify consumer experimentation, and sustainability benchmarks contained in impending EU directives guide product redesign across the entire value chain. Behind the market’s moderate headline growth, an accelerating cadence of M&A and R&D investment signals a long-term pivot toward high-value, data-driven ecosystems that blend beauty, wellness, and connected-home functionality.

Key Report Takeaways

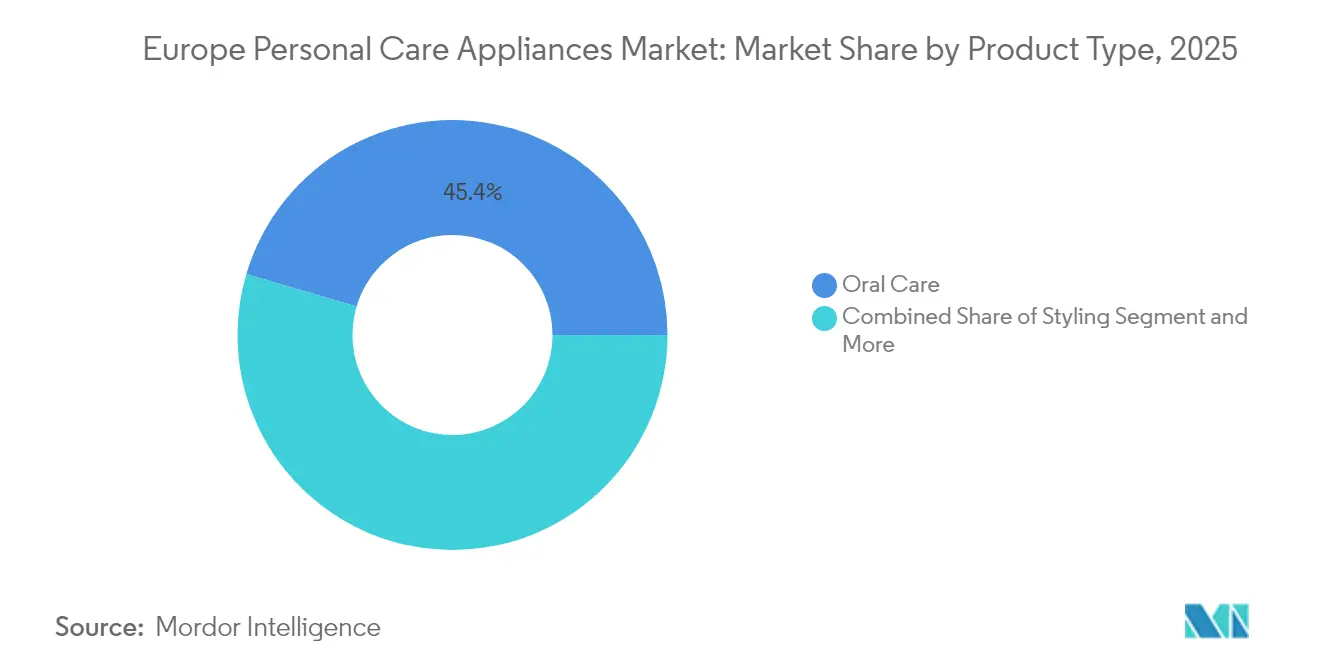

- By product type, oral care appliances led with 45.42% of Europe personal care appliances market share in 2025; styling appliances are expanding at a 4.72% CAGR to 2031.

- By gender, unisex designs captured 54.11% of the Europe personal care appliances market size in 2025, while men-focused devices are advancing at a 5.61% CAGR through 2031.

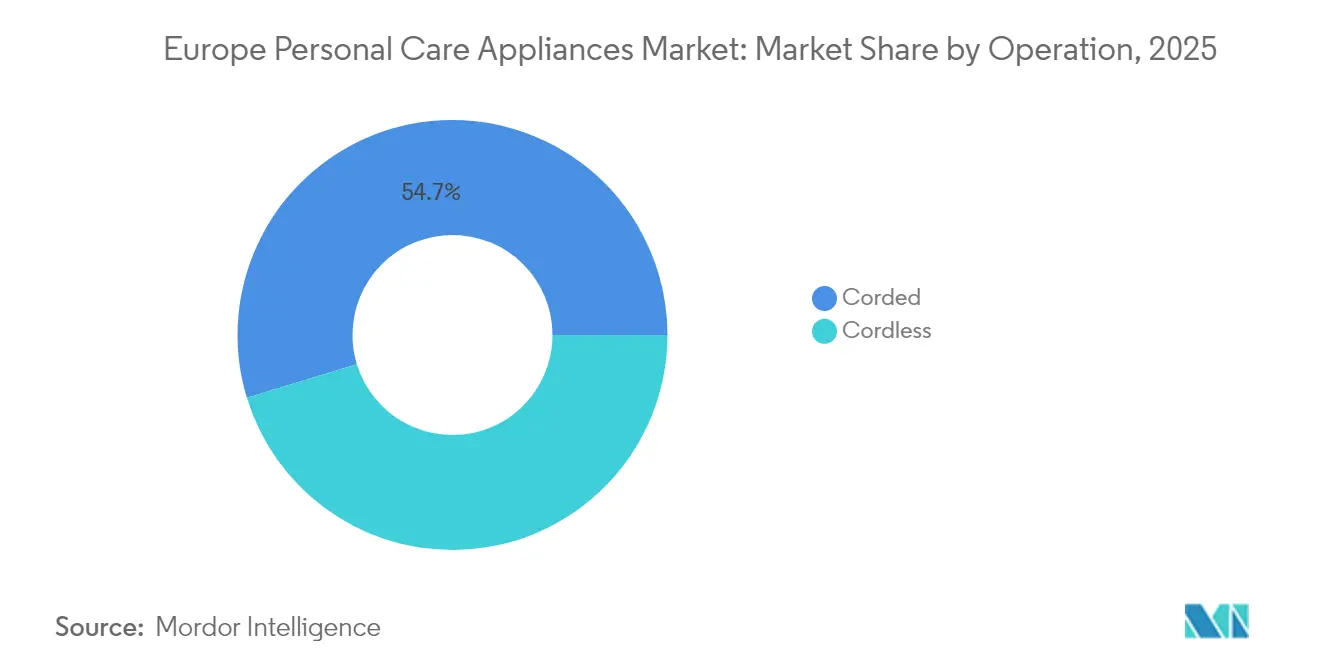

- By operation, corded formats held 54.71% of the Europe personal care appliances market size in 2025; cordless models record the fastest growth at 6.16% CAGR.

- By distribution channel, online retail accounted for 48.86% of the Europe personal care appliances market share in 2025 and is rising at a 4.76% CAGR.

- By geography, Germany contributed 19.12% of Europe personal care appliances market revenue in 2025, whereas the Netherlands posts the highest 6.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Personal Care Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Awareness of Personal Grooming and Hygiene | +0.8% | Global, with stronger influence in Germany, France, United Kingdom | Medium term (2-4 years) |

| Technological Advancements Including IoT, AI, and Smart Features | +1.2% | Northern Europe leading, expanding to Southern Europe | Long term (≥ 4 years) |

| Influence of Social Media and Celebrity Endorsements | +0.6% | Western Europe core, with TikTok-driven growth in younger demographics | Short term (≤ 2 years) |

| Adoption of Rechargeable and Cordless Appliances | +1.0% | Netherlands, Germany, United Kingdom leading adoption | Medium term (2-4 years) |

| Rising Demand for At-Home Grooming Solutions | +0.7% | Post-pandemic trend across all European markets | Medium term (2-4 years) |

| Trend Towards Unisex and Gender-Inclusive Products | +0.5% | Nordic countries leading, spreading to Central Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Awareness of Personal Grooming and Hygiene

Consumer consciousness around personal grooming has intensified beyond traditional hygiene maintenance toward comprehensive wellness routines that integrate skincare, oral care, and styling regimens. This shift drives premiumization across product categories, with manufacturers like Procter & Gamble introducing USD 380 electric toothbrushes to capture higher-value consumer segments while offsetting tariff-related cost pressures. The trend particularly benefits oral care appliances, which maintain the largest segment share at 46.05%, as consumers increasingly recognize the connection between oral health and overall wellness. German consumers exemplify this evolution, with 67% prioritizing sustainability in appliance purchases and 81% valuing durability and quality over price considerations. This awareness expansion creates opportunities for brands to justify premium pricing through enhanced functionality and health-focused marketing narratives.

Technological Advancements Including IoT, AI, and Smart Features

Smart connectivity and artificial intelligence integration are transforming personal care appliances from standalone tools into interconnected wellness ecosystems that provide personalized recommendations and usage optimization. The EU's ReCiPSS project demonstrated the commercial viability of IoT-enabled appliances through 333 sensor-equipped washing machines across Denmark, Netherlands, Slovenia, and Sweden, generating EUR 90,000-150,000 in annual revenues while enabling predictive maintenance and energy optimization [1]Source: European Commission, "How pay-per-use washing machines could clean up the manufacturing industry", projects.research-and-innovation.ec.europa.eu. This technology foundation supports the cordless segment's 6.25% CAGR growth, as manufacturers integrate smart charging algorithms, usage pattern recognition, and app-based control systems. Panasonic's latest product lineup exemplifies this trend with USB-C charging, beard sensors, and nanoe™ moisture technology that adapts to environmental conditions. The convergence of IoT capabilities with personal care creates data-driven value propositions that enhance customer retention and enable subscription-based service models.

Influence of Social Media and Celebrity Endorsements

Social media platforms are reshaping discovery and purchase patterns, with TikTok demonstrating 190% growth versus Meta's 10% expansion in European beauty commerce, fundamentally altering how consumers research and validate personal care appliance choices. This shift particularly benefits styling appliances, which achieve 4.83% CAGR growth as influencer-driven tutorials showcase advanced techniques requiring specialized tools. The trend accelerates unisex product adoption, with 54.72% market share in 2024, as gender-fluid beauty content normalizes shared grooming routines and cross-category usage. Celebrity partnerships and viral content creation drive impulse purchases and premium positioning, enabling brands to command higher margins for aesthetically designed appliances that photograph well for social sharing. The influence extends beyond awareness to actual purchasing behavior, with Gen Z consumers using TikTok for discovery before transitioning to Instagram, YouTube, and Facebook for validation and purchase decisions.

Adoption of Rechargeable and Cordless Appliances

Battery technology improvements and consumer mobility preferences are driving the cordless segment's superior 6.25% CAGR growth, outpacing the traditional corded segment despite its current 55.34% market share dominance. L'Oréal's Air Light Pro hairdryer exemplifies this evolution, combining infrared drying technology with high-speed motors to achieve 31% energy savings while maintaining performance parity with corded alternatives. The transition reflects broader consumer expectations for untethered convenience and travel-friendly designs, particularly among younger demographics who prioritize flexibility over maximum power output. Manufacturers are responding with rapid charging capabilities, extended battery life, and modular charging systems that support multiple devices. The trend creates competitive advantages for brands that can deliver corded-level performance in cordless formats while maintaining price competitiveness and durability standards.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition From Manual Grooming Alternatives | -0.4% | Southern Europe more affected, price-sensitive segments | Short term (≤ 2 years) |

| Limited Product Differentiation in Some Segments | -0.3% | Mature markets: Germany, United Kingdom, France | Medium term (2-4 years) |

| Proliferation of Counterfeit Products | -0.5% | Eastern Europe and online channels primarily affected | Medium term (2-4 years) |

| Consumer Resistance to Premium Pricing | -0.6% | Economic uncertainty regions: France, Germany, Southern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition From Manual Grooming Alternatives

Traditional manual grooming tools maintain competitive pressure on electric appliances through superior affordability, zero maintenance requirements, and established consumer habits that resist technological adoption. This constraint particularly affects price-sensitive segments and regions experiencing economic uncertainty, with France projecting only 0.4% consumer durables growth in 2025 and Germany facing continued market contraction after a 2.7% decline in 2023. The challenge intensifies in oral care, where manual toothbrushes cost significantly less than electric alternatives while delivering adequate cleaning results for many consumers. Manual alternatives also avoid the complexity of charging, replacement parts, and potential technical failures that can frustrate users. Manufacturers counter this restraint through value-focused positioning, extended warranties, and subscription models that reduce upfront costs while demonstrating long-term savings and superior health outcomes.

Limited Product Differentiation in Some Segments

Commoditization pressures in mature product categories constrain pricing power and growth potential as core functionalities converge across competing brands, particularly in basic shaving and trimming applications. The challenge reflects the market's moderate concentration level, where multiple players offer similar feature sets without clear technological advantages or compelling value propositions. This limitation forces manufacturers to compete primarily on price and distribution reach rather than innovation premiums, compressing margins and limiting investment capacity for breakthrough developments. The constraint particularly affects mid-tier brands that lack the R&D resources of premium players like Dyson, which commits GBP 500 million toward differentiated beauty technologies, or the scale advantages of mass-market leaders. Successful differentiation increasingly requires integration of smart features, sustainable materials, or specialized performance characteristics that address specific consumer pain points rather than general-purpose functionality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Oral Care Dominance Drives Market Foundation

Oral care appliances command 45.42% market share in 2025, establishing the segment's foundational role in European personal care routines, while styling appliances emerge as the fastest-growing category at 4.72% CAGR through 2031. The oral care segment's dominance reflects heightened health consciousness and professional dental care integration, with Philips leading sustainability initiatives through 70% bio-based brush head plastics and comprehensive recycling programs spanning 420 collection points across the UK. Styling appliances benefit from social media influence and professional-grade technology adoption, as consumers seek salon-quality results for home use. Shaving and grooming products maintain steady performance through premiumization strategies, while beauty appliances capture niche segments focused on skincare integration and LED therapy applications.

The segment dynamics reflect broader technological convergence, with manufacturers integrating smart sensors, app connectivity, and personalized algorithms across product categories. EU Medical Device Regulation compliance increasingly affects beauty appliances that incorporate optical radiation or invasive features, requiring enhanced safety documentation and clinical evidence. Other products, including foot massagers and nail care tools, contribute incremental growth through wellness trend alignment and aging population demographics. The product portfolio expansion strategy enables brands to capture larger wallet share while reducing dependence on single-category performance fluctuations.

By Gender: Unisex Products Lead Market Evolution

Unisex products dominate with 54.11% market share in 2025, yet men-specific appliances achieve superior 5.61% CAGR growth through 2031, reflecting evolving gender dynamics in personal care consumption patterns. The unisex leadership demonstrates successful product design that transcends traditional gender boundaries, enabling household sharing and reducing purchase complexity for couples and families. Men's segment acceleration reflects expanding grooming routines beyond basic shaving toward comprehensive skincare, hair styling, and wellness applications. Women's segment maintains steady performance through premium positioning and technology integration, particularly in hair care and beauty device categories.

This segmentation evolution aligns with broader social trends toward gender-inclusive marketing and product development, as brands recognize the limitations of binary categorization in contemporary consumer behavior. Regulatory compliance factors minimally impact gender segmentation, though product safety standards apply equally across all demographic targets. The trend toward unisex products creates economies of scale in manufacturing and marketing while enabling brands to address diverse household needs through streamlined product portfolios rather than duplicative gender-specific offerings.

By Operation: Cordless Revolution Transforms User Experience

Cordless appliances drive market transformation with 6.16% CAGR growth through 2031, challenging the current corded segment dominance of 54.71% market share in 2025 through superior convenience and technological advancement. The cordless acceleration reflects battery technology improvements, charging speed enhancements, and consumer preference for mobility and travel-friendly designs. Corded appliances maintain market leadership through superior power delivery, unlimited usage duration, and lower initial costs, particularly in high-performance categories like professional-grade hair dryers and styling tools. The operational divide creates distinct value propositions that serve different consumer priorities and usage patterns.

The operational segment demonstrates sustainability potential. These include modular cordless vacuum designs with replaceable batteries, color-coded maintenance components, and mechanical connections that eliminate adhesive-based assembly. The operational choice increasingly influences product lifecycle management, with cordless devices requiring battery replacement strategies and corded alternatives offering longer service lives. Manufacturers balance performance, convenience, and sustainability considerations while developing hybrid solutions that combine corded power with cordless flexibility through docking systems and rapid charging capabilities.

By Distribution Channel: Online Retail Reshapes Market Access

Online retail channels capture 48.86% market share in 2025 while maintaining 4.76% CAGR growth through 2031, establishing digital commerce as the dominant distribution model for European personal care appliances. The online leadership reflects consumer preference for product research, price comparison, and convenient delivery, particularly for replacement parts and consumables that support ongoing appliance usage. Supermarkets and hypermarkets maintain significant presence through impulse purchasing and immediate availability, while specialty stores provide expert consultation and demonstration opportunities that support premium product sales. Other distribution channels, including department stores and duty-free outlets, serve specific consumer segments and geographic markets with tailored product assortments.

The distribution evolution benefits from social commerce integration, with TikTok's 190% growth rate enabling direct purchase links from influencer content and product demonstrations. Specialized retailers like Boots, Nocibé, and Douglas maintain over one-third of European shopper traffic through brand partnerships and exclusive product launches. The channel dynamics create opportunities for manufacturers to optimize inventory management, reduce distribution costs, and gather direct consumer feedback while maintaining relationships with traditional retail partners who provide physical touchpoints and local market expertise.

Geography Analysis

Germany leads the European personal care appliances market with 19.12% share in 2025, leveraging its manufacturing heritage, premium brand positioning, and strong consumer purchasing power despite facing economic headwinds that constrain overall market growth. The German market exemplifies mature consumer behavior, with 81% of consumers prioritizing durability and quality over price considerations, creating opportunities for premium positioning and sustainable product development. German industry association IKW reported record-high EUR 33.4 billion sales in beauty and personal care products in 2023, though companies face deteriorating economic conditions that may constrain future growth . The market's emphasis on engineering excellence and environmental responsibility aligns with EU regulatory frameworks including the Ecodesign for Sustainable Products Regulation and Digital Product Passport requirements.

The Netherlands emerges as the fastest-growing European market at 6.21% CAGR through 2031, driven by progressive consumer adoption of sustainable technologies and early embrace of circular economy principles. Dutch consumers demonstrate high acceptance of refurbished appliances and recycled materials, with Miele's washing machine refurbishment program in the Netherlands serving as a model for circular business practices across Europe. The Netherlands' leadership in smart home adoption and IoT integration creates favorable conditions for connected personal care appliances that offer predictive maintenance and usage optimization. The market benefits from high disposable income, environmental consciousness, and willingness to pay premiums for innovative and sustainable products.

The United Kingdom, Italy, France, Spain, Poland, Belgium, and Sweden collectively represent substantial market opportunities with distinct consumer preferences and regulatory environments that influence product positioning and distribution strategies. The UK market demonstrates resilience despite economic challenges, with specialized retailers maintaining strong positions through brand partnerships and expert consultation services. France projects modest 0.4% growth in consumer durables for 2025, reflecting political uncertainty and cautious consumer spending that may favor value-oriented positioning over premium alternatives. Italy and Spain show stronger growth potential driven by lifestyle trends and social media influence, while Poland benefits from economic development and increasing disposable income. The Rest of Europe category encompasses emerging markets with significant long-term potential as economic development and consumer sophistication continue advancing.

Competitive Landscape

The European personal care appliances market exhibits moderate concentration, enabling competitive dynamics between established multinational corporations and emerging technology disruptors that leverage innovation and direct-to-consumer strategies. Market leaders including Procter & Gamble, Koninklijke Philips N.V., Spectrum Brands, and Dyson compete through differentiated technology platforms, premium positioning, and comprehensive distribution networks, while smaller players like Gtech challenge incumbents with specialized product offerings and competitive pricing.

Strategic patterns emphasize sustainability integration, smart connectivity, and circular economy principles as competitive differentiators, with companies investing heavily in R&D to maintain technological leadership and justify premium pricing in increasingly commoditized segments. Consolidation activity reshapes competitive dynamics through strategic acquisitions that combine complementary capabilities and expand market reach, exemplified by Bic's EUR 200 million acquisition of Tangle Teezer to accelerate hair care sector growth and L'Oréal's full buyout of water-saving technology firm Gjosa.

Opportunities emerge in connected appliances, sustainable materials integration, and personalized wellness solutions that address specific consumer pain points rather than general-purpose functionality. Regulatory compliance with IEC 60335-2-27:2024 safety standards for optical radiation appliances and EU Medical Device Regulation requirements creates barriers to entry while enabling differentiation through superior safety and performance documentation. Technology adoption focuses on IoT integration, artificial intelligence, and energy efficiency improvements that support both performance enhancement and regulatory compliance objectives.

Europe Personal Care Appliances Industry Leaders

-

Procter & Gamble

-

Koninklijke Philips N.V.

-

Conair LLC

-

Dyson

-

Panasonic Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Dyson launched new airwrap in United Kingdom – and it surpassed all other hair tools. The airwrap co-anda 2x featured Dyson's latest and most powerful motor, which offered twice as much air pressure and promised to bring faster drying and less heat damage. The all-new hair tool was said to dry hair “as fast as a full performance hair dryer”.

- September 2025: The lifestyle-tech brand Laifen, which specialized in high-performance personal care devices, expanded its product portfolio to include electric shavers. At IFA 2025 in Berlin, Laifen unveiled two models for the first time: the compact T1 Pro Electric Razor for precise shaving and the powerful P3 Pro Electric Razor for demanding beard care.

- August 2025: Revamp Professional introduced two new hair styling tools aimed at the Christmas gifting market. The Curl Air Style 7 in 1 Ionic Air Styler and the Effortless Curls extra-long 32mm ceramic tong were designed to offer a variety of styling options, focusing on both performance and hair care. Both products featured Revamp's ProglossTM Super Smooth Oils, which included Keratin, Argan, and Coconut oil.

- August 2025: Royal Philips, a health technology and grooming company, launched the Philips Norelco Head Shaver Pro Series — an electric shaver engineered to deliver enhanced precision and comfort. As a development from America's prominent electric shave and grooming brand, the Philips Norelco Head Shaver Pro Series was designed for a smooth, close and comfortable head shave that brought the confidence to raise standards.

Europe Personal Care Appliances Market Report Scope

Personal care appliances include electric devices used for grooming, beautification, and personal hygiene such as hair dryers, hair straighteners, hair stylers, trimmers, power shavers, epilators, and powered toothbrushes. The European personal care appliances market is segmented by gender, type, distribution channel, and geography. The market by gender is segmented into men, women, and unisex. The market by type is segmented into shaving and grooming, styling, beauty appliances, and oral care. Shaving and grooming are further segmented into shavers, trimmers, and epilators. Similarly, the styling segment is sub-segmented into hair straighteners, hair dryers, hair curlers, and other styling products. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels. The market by geography is segmented into Spain, the United Kingdom, Germany, France, Italy, Russia, and the Rest of Europe. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Shaving and Grooming | Shavers |

| Trimmers | |

| Epilator | |

| Styling | Hair Straightener |

| Hair Dryer | |

| Hair Curler/Rollers | |

| Others Styling Products | |

| Beauty Appliances | |

| Oral Care | |

| Others |

By Gender

| Men |

| Women |

| Unisex |

By Operation

| Corded |

| Cordless |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Shaving and Grooming | Shavers |

| Trimmers | ||

| Epilator | ||

| Styling | Hair Straightener | |

| Hair Dryer | ||

| Hair Curler/Rollers | ||

| Others Styling Products | ||

| Beauty Appliances | ||

| Oral Care | ||

| Others | ||

| By Gender | Men | |

| Women | ||

| Unisex | ||

| By Operation | Corded | |

| Cordless | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe personal care appliances market in 2026?

The Europe personal care appliances market size is USD 13.52 billion in 2026.

What is the expected growth rate for personal care appliances in Europe?

The market is projected to rise at a 4.29% CAGR from 2026 to 2031.

Which product segment leads European sales?

Oral care appliances command the largest 45.42% share of 2025 revenue.

Why are cordless designs gaining popularity?

Cordless tools post a 6.16% CAGR because faster-charging batteries and USB-C ports deliver portability without sacrificing performance.

Page last updated on: