Global Aloe Vera Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

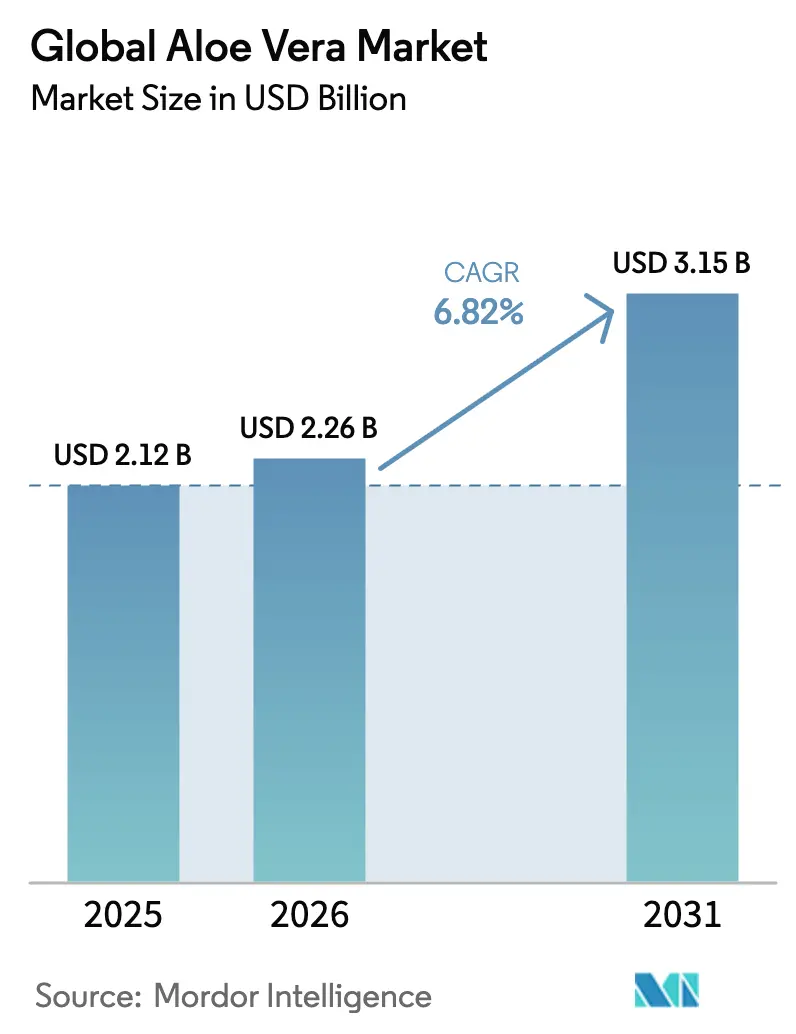

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 3.15 Billion |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Aloe Vera Market Analysis by Mordor Intelligence

The aloe vera market size in 2026 is estimated at USD 2.26 billion, growing from 2025 value of USD 2.12 billion with 2031 projections showing USD 3.15 billion, growing at 6.82% CAGR over 2026-2031. Growth stems from steady integration of aloe vera ingredients across cosmetics, food, and therapeutic products, aided by clear certification guidelines that require a minimum acemannan threshold for authentic labeling. Regulatory acceptance has broadened, as demonstrated by the United States Food and Drug Administration classifying certain aloe vera preparations as flavoring agents under Good Manufacturing Practices, thereby expanding formulation options in food and beverages. Advanced extraction techniques now retain higher levels of bioactive compounds while minimizing hydroxyanthracene derivatives, enabling premium formulations that meet strict European Food Safety Authority limits of 0.1 ppm in flavorings. Organic certified supply chains are also growing quickly after the United States Department of Agriculture (USDA) tightened enforcement in 2024, reinforcing consumer trust in certified organic botanicals. Finally, multi‐year initiatives by producers to vertically integrate farming, processing, and distribution are strengthening resilience to climate shocks and ensuring consistent raw material quality in the aloe vera market.

Key Report Takeaways

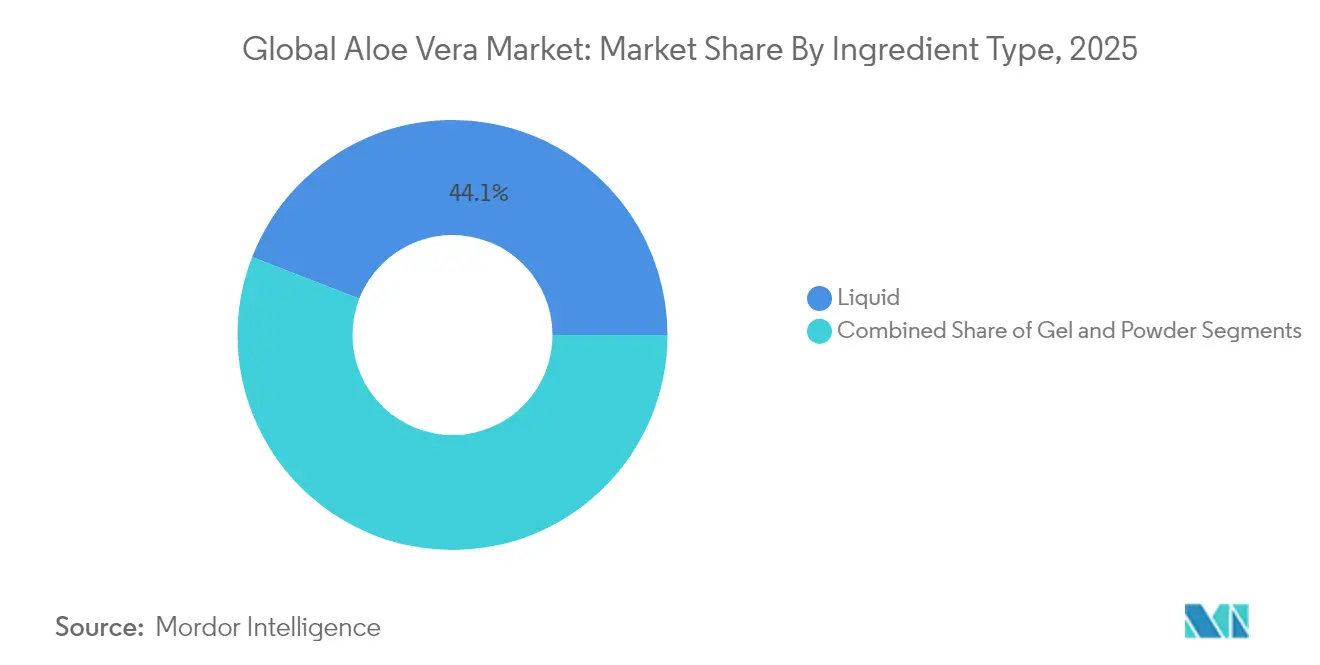

- By ingredient type, liquid formulations held 44.10% of aloe vera market share in 2025, while gel formulations are projected to expand at an 8.21% CAGR through 2031.

- By nature, conventional products accounted for 66.30% of the aloe vera market size in 2025, whereas the organic segment is forecast to rise at a 7.34% CAGR to 2031.

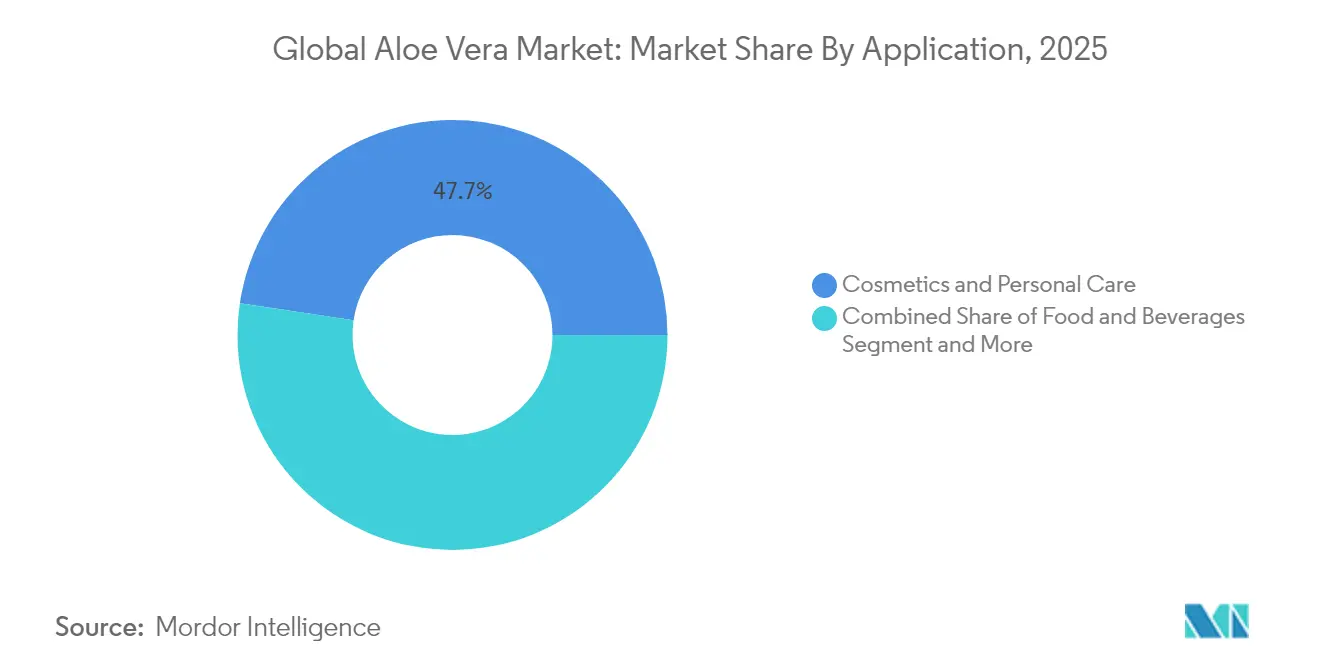

- By application, cosmetics and personal care led with 47.65% revenue share in 2025; food and beverages is the fastest‐growing application segment at a 7.22% CAGR to 2031.

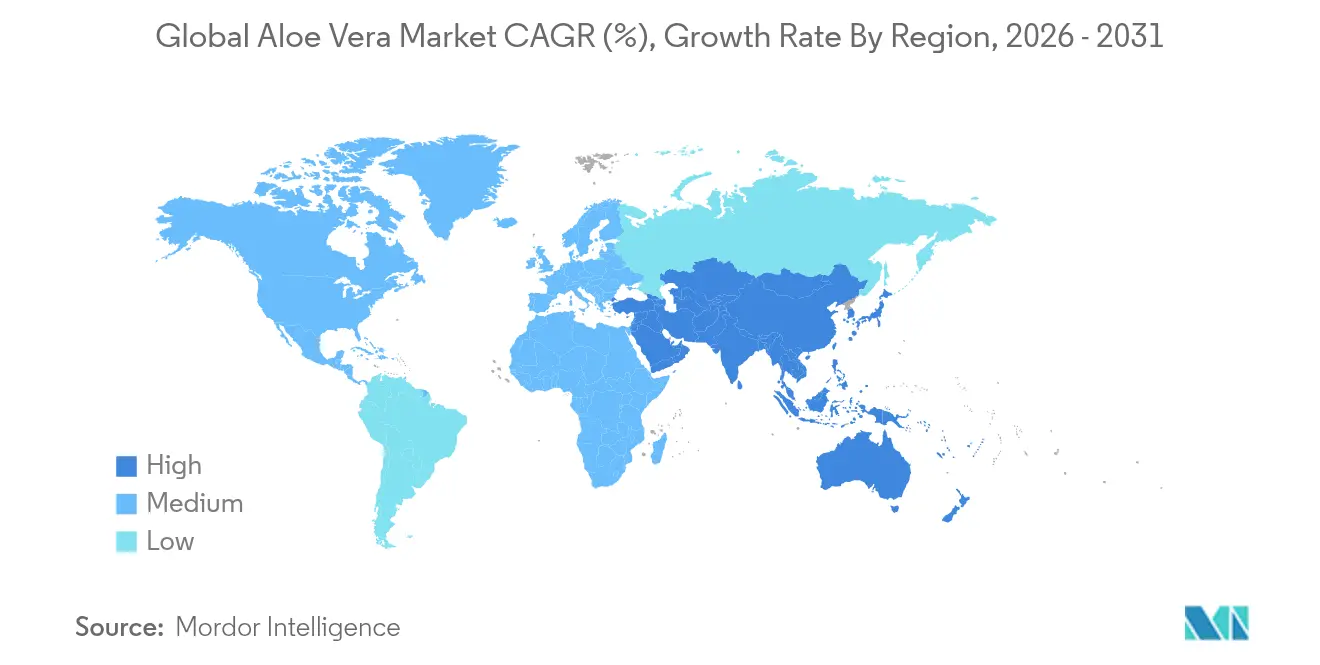

- By geography, Asia-Pacific commanded 39.10% of the 2025 aloe vera market share, and the region is expected to grow at 7.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aloe Vera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural skincare ingredients | +1.2% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| Increasing use in food & beverage formulations | +1.5% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Advancing extraction and processing technologies | +0.8% | Global, led by developed markets | Short term (≤ 2 years) |

| Rising preference for certified organic products | +1.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expanding cosmetic industry boosts aloe vera-based product demand | +0.9% | Global, strongest in Asia-Pacific and South America | Long term (≥ 4 years) |

| Aloe vera gaining popularity for therapeutic and medicinal use | +0.7% | North America and Europe, clinical focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural Skincare Ingredients

Consumer interest in plant-based skincare has intensified, favoring formulations that showcase aloe vera polysaccharides, flavonoids, and vitamins. Recent clinical work shows that aloe vera promotes keratinocyte repair via EGFR/PKC signaling, validating topical wound-healing claims. Manufacturers are launching premium gels with enriched acemannan levels, while European Medicines Agency monographs supporting “well-established medicinal use” bolster brand confidence. As ingredient lists become more transparent, product labels highlighting certified acemannan content differentiate offerings in the aloe vera market. Retail analytics indicate that aloe-infused serums and moisturizers priced 15–20% above conventional items maintain robust sell-through, suggesting that efficacy narratives translate into willingness to pay. Strategic partnerships between growers and multinational cosmetic brands further stimulate demand in North America and Europe.

Increasing Use in Food and Beverage Industry

Beyond traditional juice, processors are incorporating stabilized aloe vera gel particulates into yogurts, confectionery coatings, and functional shots targeting gut and immune health. Controlled studies on irritable bowel syndrome symptom reduction reinforce consumer confidence. FDA GRAS status for specified preparations reduces regulatory barriers, though compliance with aloin thresholds remains critical. Chinese and Indian beverage companies continue to trial aloe inclusion rates of 10–30 g/liter in mainstream drinks, reflecting cultural acceptance and middle-class appetite for functional ingredients. Producers also appreciate the ingredient’s natural antimicrobial activity, allowing fewer synthetic preservatives. The resulting product diversity underpins a long-term volume uplift for the aloe vera market.

Advancing Extraction Technologies

Innovation focuses on cryogenic, enzymatic, and membrane filtration techniques that preserve acemannan and remove hydroxyanthracene derivatives below IASC’s 10 ppm oral limit iasc.org. Newly commercialized cryo-spray drying yields 20% higher polysaccharide retention than conventional hot-air drying, improving bioactive density in concentrates. Pilot bioreactors using plant-cell culture deliver standardized polyacetylated mannans, and USDA’s Aloe 2.0 initiative illustrates the potential to decouple supply from climatic risk nifa.usda.gov. These advances permit precise formulation, reduce batch variability, and lower energy intensity, supporting premium positioning within the aloe vera market.

Rising Preference for Organic and Plant-Based Products

USDA’s Strengthening Organic Enforcement rule, effective March 2024, extended certification to more brokers and retailers, closing loopholes and elevating consumer trust [1]U.S. Department of Agriculture, “Strengthening Organic Enforcement Final Rule,” usda.gov. Market surveys in 2025 show 63% of U.S. millennials check for organic seals on botanical supplements, up from 44% in 2022. For farmers, organic aloe introduces favorable benefit–cost ratios (> 2:1) in emerging economies, encouraging acreage conversion. Digitalized trade facilitation, promoted by the Asian Development Bank, cuts export paperwork and accelerates customs clearance, raising competitiveness of certified organic exports [2]Asian Development Bank, “Trade Facilitation 2025 Update,” adb.org. These conditions accelerate the organic sub-segment’s rise within the aloe vera market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adulteration undermining consumer trust | -0.9% | Global import markets | Short term (≤ 2 years) |

| Supply chain disruptions tied to climate volatility | -0.7% | Major producing regions | Medium term (2–4 years) |

| Overconsumption health risks restrict aloe vera market appeal | -0.6% | Global | Medium term (2–4 years) |

| High research and development costs slow aloe vera product innovation | -0.4% | Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adulteration Issues Undermine Aloe Vera Market Trust

Investigations have revealed products without detectable acemannan sold under “100% aloe” labels, triggering class actions and eroding brand credibility. The FDA has issued warning letters over deficient raw-material identity testing, exposing supply chain gaps. AOAC official method 2018.14 now offers a validated approach for acemannan quantification, yet widespread adoption remains uneven. Retailers demand IASC or equivalent certification, creating a dual-tier market in which uncertified goods face shelf-space constraints. Blockchain traceability pilots aim to reassure buyers but add cost, pressuring price-competitive players in the aloe vera market.

Supply Chain Disruptions Limit Product Availability

Droughts in southern Mexico, a primary leaf source, cut yields by 30% in 2024, while storms in the Dominican Republic damaged processing facilities, reducing global supply elasticity. The crop’s 12- to 18-month maturation period restricts rapid acreage expansion, and specialized de-colorization equipment is capital intensive. Heightened phytosanitary inspections lengthen transit times into the European Union, elevating spoilage risk. Although larger firms pursue vertical integration, small and mid-scale processors lack capital for climate-resilient infrastructure, increasing their exposure. These factors curb near-term supply growth within the aloe vera market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Gel Formulations Drive Innovation

Gel formulations generated swift growth at an 8.21% CAGR through 2031, outpacing liquids that held 44.10% of the aloe vera market share in 2025. Bioactive retention is superior in gels because cold-chain processing sustains acemannan content that regulators and clinical researchers monitor for therapeutic efficacy. Liquid formulations still dominate beverages and cosmetics, leveraging existing mixing lines and consumer familiarity. Powders cater to nutraceutical manufacturers who require concentrated active levels and ease of shipping. Hospital procurement guidelines increasingly specify gel purity standards, creating a premium sub-segment within the aloe vera market size for clinical supplies.

Manufacturers embrace direct-ink-writing technology to 3-D print aloe-based scaffolds for regenerative medicine, broadening product scope well beyond topical creams. Strategic patents on cryo-derived gels create barriers to entry and secure licensing income. Meanwhile, powders offer a decade-long shelf life and ease of international distribution, securing relevance in regions where cold-chain logistics remain cost-prohibitive. Blenders frequently rehydrate powders into finished beverages on-site, lowering ocean freight weight and limiting spoilage. As formulation innovation continues, gels will capture emerging healthcare and high-performance cosmetic niches while liquids and powders preserve scale in mass products, keeping all three formats integral to the broader aloe vera market.

By Nature: Organic Segment Accelerates Despite Conventional Dominance

Conventional products retained 66.30% of the aloe vera market share in 2025 because legacy cultivation, established distribution, and lower certification costs support competitive pricing. However, the organic category is advancing at a 7.34% CAGR, markedly exceeding the aloe vera market average. Retailers allocate prime shelf space to USDA Organic or EU Organic logo items, citing higher average order values.

Gen Z shoppers rank “certified organic” as the top purchase driver for personal care botanicals, propelling product formulators to secure compliant supply lines. E-commerce platforms highlight QR-code traceability that links to digital certificates, reinforcing transparency in the aloe vera market size for organic goods. Conventional producers are therefore weighing partial acreage conversion or dual reporting systems to maintain credibility without eroding existing scale benefits.

By Application: Food and Beverages Emerge as Growth Leader

Cosmetics and personal care held 47.65% revenue in 2025, reflecting aloe’s longstanding role as a humectant and soothing agent in skin creams and sun care. Nevertheless, the food and beverage segment is projected to expand at a 7.22% CAGR, making it the most dynamic contributor to the aloe vera market. FDA confirmation that certain aloe preparations qualify as flavoring agents encourages wider inclusion in flavored waters, yogurts, and snack bars. Controlled trials on digestive benefits, coupled with a growing consumer preference for clean-label functionality, reinforce demand.

Product developers utilize low-temperature drum drying to create soluble aloe powders that disperse instantly in beverage bases, ensuring homogenous texture. In skin care, ongoing research demonstrates that aloe-derived mannans enhance epidermal barrier repair, sustaining legacy volume in creams and lotions. Pharmaceutical applications remain nascent but promising: Wake Forest University began Phase 1 trials on freeze-dried aloe capsules for interstitial cystitis in February 2025 . This clinical pathway could open new high-margin therapeutic niches, reshaping downstream demand patterns within the aloe vera market.

Geography Analysis

Asia-Pacific held 39.10% of the aloe vera market in 2025 and is forecast to grow at a 7.41% CAGR through 2031. Favorable climates in India and Thailand, plus national medicinal-plant subsidies, broaden cultivation bases. China’s integration of aloe into traditional medicine underscores robust domestic demand. The Asian Development Bank estimates that ongoing trade digitalization could cut procedural costs by 11%, enhancing regional supply chain fluidity. These dynamics reinforce Asia-Pacific’s status as a production and processing hub for the aloe vera market.

North America constitutes a mature yet lucrative arena marked by stringent FDA oversight and high consumer spending on clean-label wellness. The United States leads in technical innovation, housing numerous patent holders in cryogenic and enzymatic extraction. Widespread retail awareness of IASC certification supports premium price points. However, climatic limitations restrict domestic leaf output, leaving processors dependent on imports vulnerable to freight bottlenecks and phytosanitary delays. This exposure fuels investment in greenhouse cultivation trials in the Southwest and Puerto Rico to localize supply, a strategy expected to stabilize aloe vera market size contributions from the region.

Europe operates under the strictest botanical additive regulations worldwide. Consumer preference strongly tilts toward certified organic and sustainably sourced botanicals, aligning with EU Green Deal objectives. Germany, France, and the Nordic countries collectively account for over 60% of regional demand for aloe nutraceuticals. Ongoing Brexit adjustments have complicated logistics, but European producers mitigate risk by diversifying suppliers across Spain’s Canary Islands and Africa’s Cape Verde, stabilizing throughput in the aloe vera market.

Competitive Landscape

The aloe vera market remains moderately consolidated. Fewer than 20 multinational producers jointly account for just over half of global certified output, while hundreds of smaller firms operate regionally. IASC certification drives differentiation: compliant products achieve retail premiums of 15–25% relative to uncertified goods. Class-action suits prompted stricter raw-material testing and catalyzed blockchain pilots for end-to-end traceability. IASC now conducts facility re-audits every 3 years, exerting cost pressure on non-compliant processors.

Technological capability constitutes a key competitive lever. Companies adopting cryogenic processing report 20–30% higher bioactive yields, enabling entry into medical dressings and nutraceutical capsules that command elevated margins. Patents covering enzyme-assisted de-pulping and membrane filtration concentrate assets among early movers. In 2025, AVITA Medical introduced Cohealyx, a collagen matrix compatible with aloe gels, illustrating synergy between medical devices and botanical actives.

Strategic expansion includes vertical integration: top producers acquire farms in Mexico and the Dominican Republic, locking in supply while mitigating climate risk. Elsewhere, contract farming with guaranteed buy-back terms supports smallholder livelihoods, enhancing sustainability credentials. The aloe vera industry also witnesses nascent interest from synthetic biology firms aiming to bio-engineer acemannan; however, natural-origin preference restrains rapid penetration. Collectively, these moves underscore heightened competition for high-purity raw materials, quality certifications, and intellectual property within the aloe vera market.

Global Aloe Vera Industry Leaders

Aloecorp

Concentrated Aloe Corp

Aloe Jaumave SA de Cv

Aloe Queen Inc.

Green Earth Products Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AVITA Medical launched Cohealyx, a collagen dermal matrix designed to complement aloe vera wound-care protocols.

- December 2024: Aloecorp expanded its business operations by acquiring the Aloe Vera division of Pharmachem Innovations. This acquisition expanded Aloecorp's production capacity and added three advanced facilities in Mexico.

- April 2023: Concentrated Aloe Corporation (CAC) partnered with Eurosyn SpA, one of the suppliers of specialty chemicals in Italy. Through this collaboration, Eurosyn was delegated to distribute CAC's products, including aloe vera, in the Italian Eurosyn market to expand its market presence while providing CAC with a reliable presence in the territory.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the global aloe vera market as the total value of raw and minimally processed aloe vera gel, liquid concentrates, and powder sold into food, beverage, cosmetic, and nutraceutical manufacturing channels worldwide. The study values trade in bulk ingredients rather than finished retail products, thereby aligning volumes directly with industrial demand.

Scope exclusion: nursery plants, ornamental aloe sales, and finished over-the-counter cosmetics are outside this study's remit.

Segmentation Overview

- By Ingredient Type

- Gel

- Liquid

- Powder

- By Nature

- Conventional

- Organic

- By Application

- Cosmetics and Personal Care

- Food and Beverages

- Pharmaceuticals and Dietary Supplements

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed plantation owners in Mexico, processors in Thailand, contract manufacturers in Germany, and purchasing heads at two U.S. natural-cosmetic brands. These discussions validated extraction yields, regional price spreads, and typical inclusion rates per product line, which helped us reconcile secondary data gaps and test model sensitivities.

Desk Research

Our analysts began by mapping planted acreage, extraction output, and cross-border trade using publicly available datasets such as FAOSTAT crop area tables, UN Comtrade HS-121190 shipment codes, and ITC Trademap export values. Regulatory notes from the US FDA, the European Food Safety Authority, and India's FSSAI clarified allowable inclusion rates that influence industrial uptake. Industry association briefs from the International Aloe Science Council, scientific papers indexed on PubMed, and company 10-K filings enriched supply-demand signals. Select paid databases, including D&B Hoovers for processor financials and Dow Jones Factiva for deal tracking, offered further triangulation. The sources cited here are illustrative, not exhaustive; many additional datasets informed the desk review.

Market-Sizing & Forecasting

A top-down build started with global leaf output, which was converted to gel, liquid, and powder availability through region-specific extraction factors. Select bottom-up checks, processor capacity roll-ups, and sampled average selling price multiplied by contract volumes were then overlaid to refine totals. Key variables include cultivated acreage, average leaf yield per hectare, extraction recovery rate, industrial utilization ratio, and ingredient price trajectories. Forecasts use multivariate regression, linking those variables with macro drivers such as clean-label product launches and certified organic farmland expansion. Where primary sampling lagged, we applied price-volume elasticity bands agreed with experts to close estimation gaps.

Data Validation & Update Cycle

Before sign-off, Mordor analysts run variance tests against historical trade flows and prior-year company revenues; anomalies trigger re-contacts. Reports refresh annually, with mid-cycle updates issued when weather shocks, regulatory shifts, or material M&A alter supply fundamentals.

Why Mordor's Aloe Vera Market Baseline Inspires Confidence

Published numbers often diverge because each firm picks its own ingredient coverage, price points, and refresh cadence. As we see, aloe vera flows across both commodity and wellness value chains.

Key gap drivers include differing treatment of downstream finished goods, the use of straight-line growth assumptions, and varied currency bases, which are then compounded by infrequent primary validation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.12 billion (2025) | Mordor Intelligence | - |

| USD 3.09 billion (2025) | Global Consultancy A | Narrow ingredient coverage, higher ASP assumption, limited expert verification |

| USD 2.29 billion (2024) | Regional Consultancy B | Excludes derivatives beyond extracts, applies constant growth, biennial updates |

| USD 1.64 billion (2025) | Industry Journal C | Counts only finished OTC items, omits B2B bulk trade volumes |

The comparison shows that when scope boundaries shift or validation is light, totals swing widely. By aligning coverage with true industrial demand, refreshing models every year, and grounding inputs in both public statistics and firsthand operator insights, Mordor Intelligence delivers a balanced, transparent baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the global aloe vera market?

The aloe vera market stands at USD 2.26 billion in 2026 and is forecast to reach USD 3.15 billion by 2031 at a 6.82% CAGR.

Which region leads aloe vera production and demand growth?

Asia-Pacific holds 39.10% of global share and is projected to grow at 7.41% CAGR due to strong farming infrastructure and functional beverage uptake.

Why are gel formulations gaining share over liquids?

Gel processing preserves higher acemannan levels, meeting clinical and regulatory standards, and is expanding into wound-care and pharmaceutical niches at an 8.21% CAGR.

How is organic certification affecting the aloe vera industry?

USDA’s 2024 rule expanded mandatory certification, boosting consumer trust and helping the organic segment grow faster than conventional products.

Page last updated on: