Ethyl Tertiary Butyl Ether Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.79 Billion |

| Market Size (2031) | USD 12.21 Billion |

| Growth Rate (2026 - 2031) | 9.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethyl Tertiary Butyl Ether Market Analysis by Mordor Intelligence

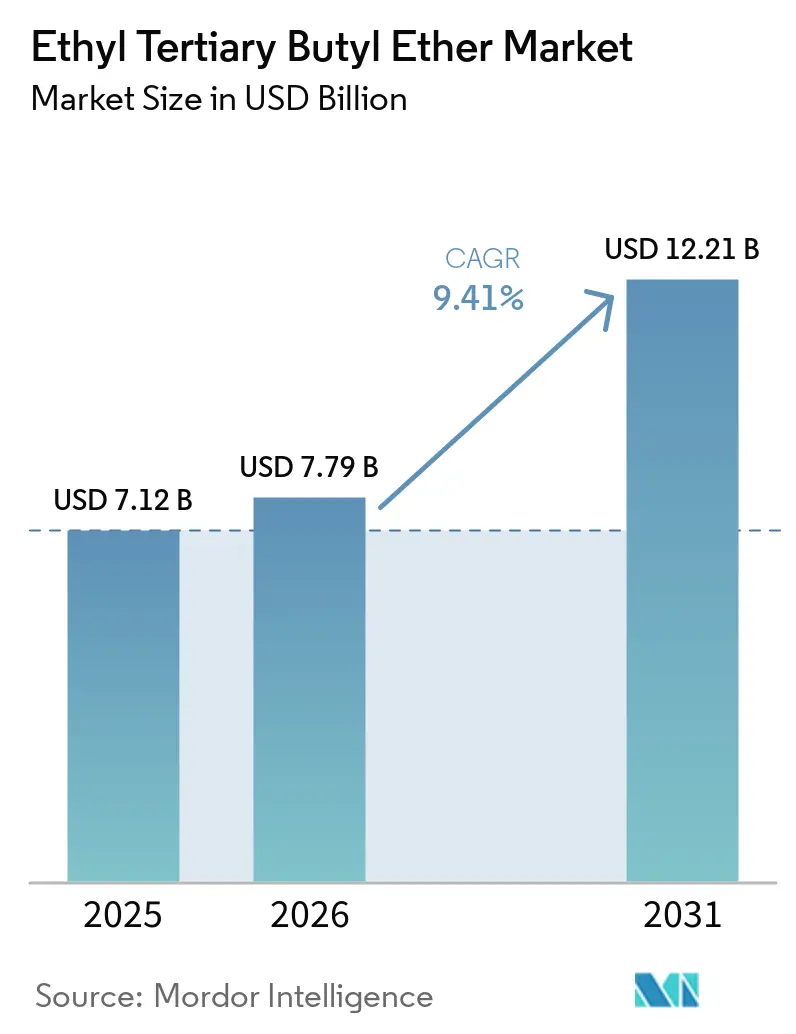

The Ethyl Tertiary Butyl Ether Market size is projected to be USD 7.12 billion in 2025, USD 7.79 billion in 2026, and reach USD 12.21 billion by 2031, growing at a CAGR of 9.41% from 2026 to 2031. Stronger biofuel mandates in Europe and Japan, the completed MTBE phase-out in North America, and rising premium-gasoline demand in China continue to redirect octane-enhancement spending toward ethyl tertiary butyl ether. Refiners value the additive’s low vapor pressure and high research octane number because it allows them to keep more light hydrocarbons in the gasoline pool without breaching evaporative-emissions limits. Production economics increasingly hinge on certified bioethanol availability, while pilot routes to renewable isobutylene promise lower carbon intensity after 2028. Growing interest in sustainable marine and aviation fuels offers an optional upside, although current fuel specifications still exclude ether additives.

Key Report Takeaways

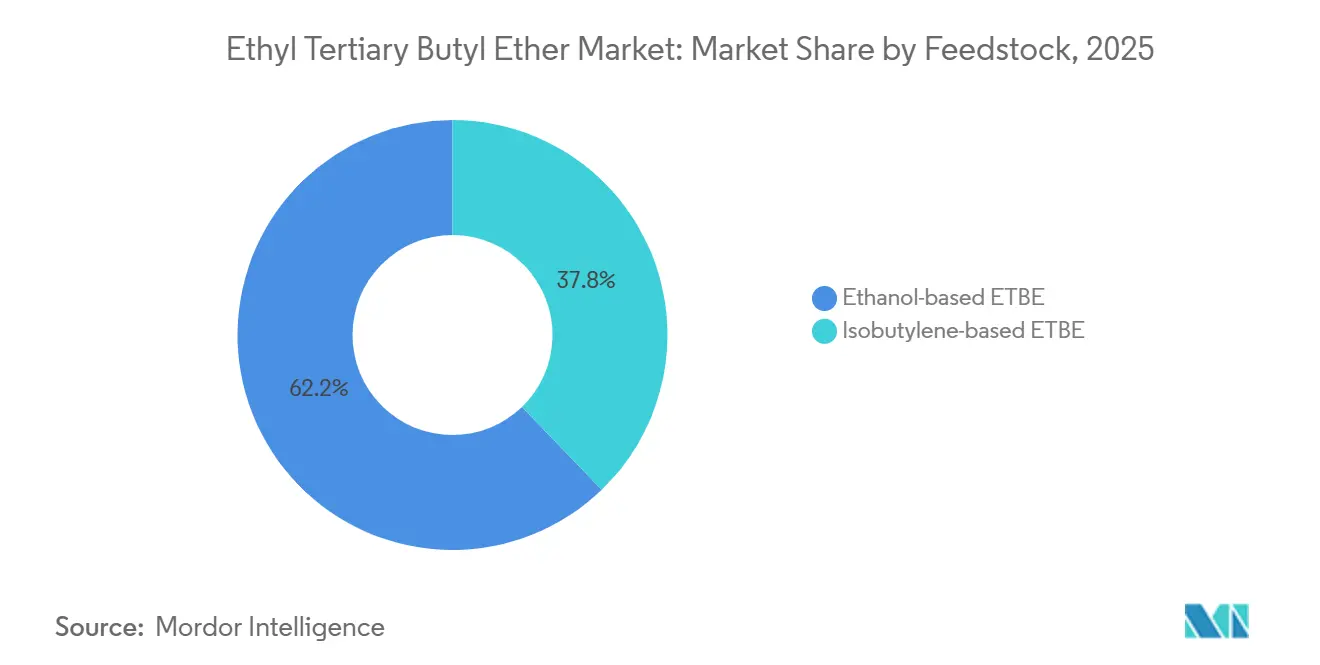

- By feedstock, ethanol-based ETBE captured 62.22% of the ethyl tertiary butyl ether market share in 2025 and is advancing at a 9.22% CAGR through 2031.

- By fuel type, unleaded gasoline had a share of 45.11% in 2025 of the market. E10 and other biofuel blends' market share is expected to grow at a CAGR of 9.78% during the forecast period (2026-2031).

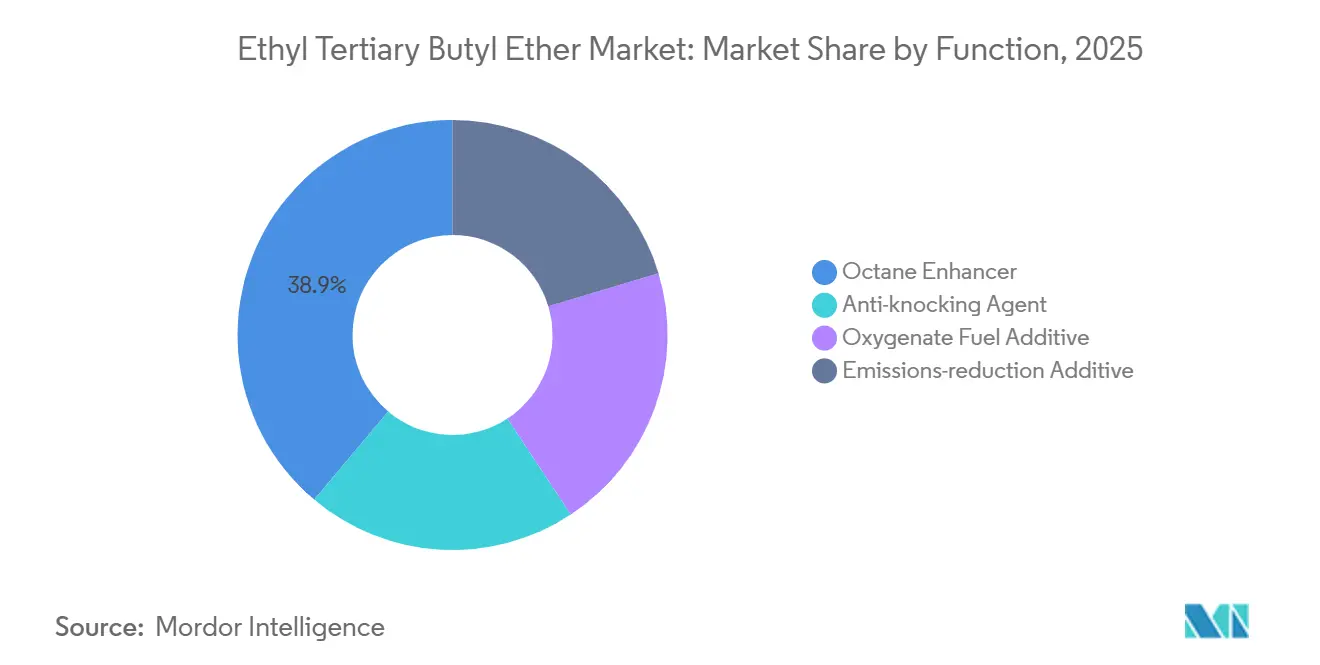

- By function, octane enhancer had the largest share of 38.88% in 2025 and emissions-reduction additive's share is expected to increase at the fastest CAGR of 9.11% during the forecast period (2026-2031).

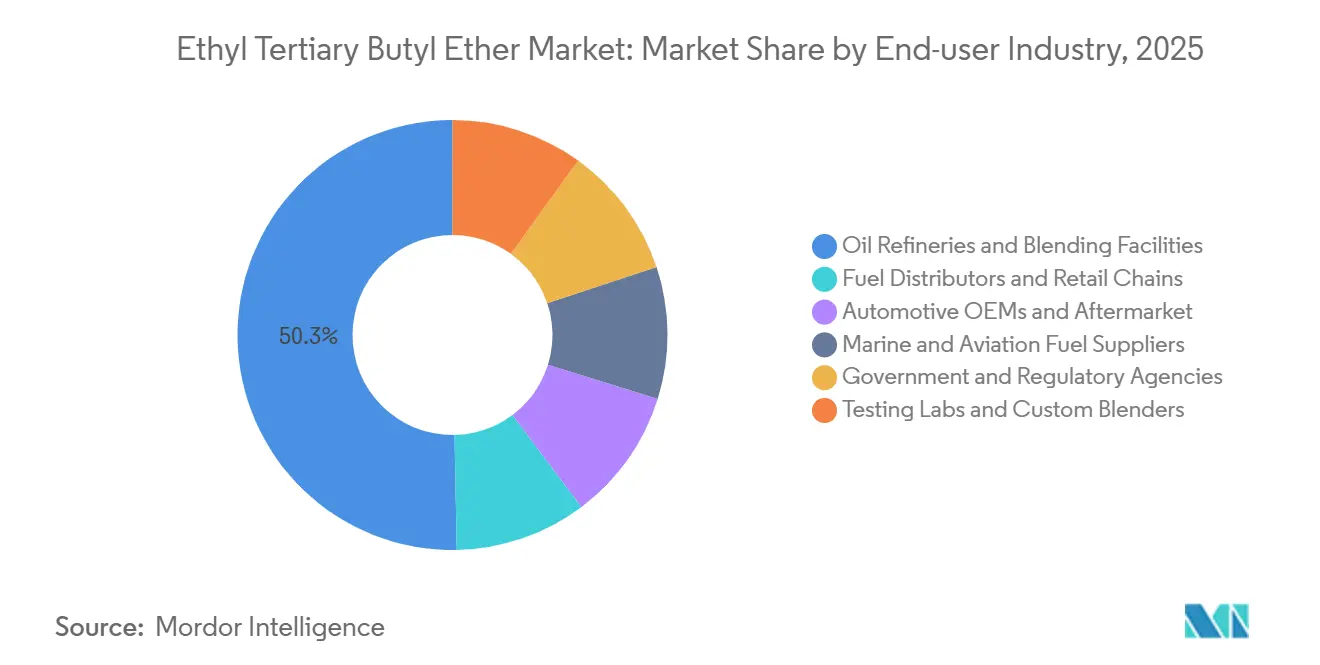

- By end-user industry, oil refineries and blending facilities held 50.31% of 2025 revenues, but marine and aviation suppliers show the highest projected CAGR at 9.03% to 2031.

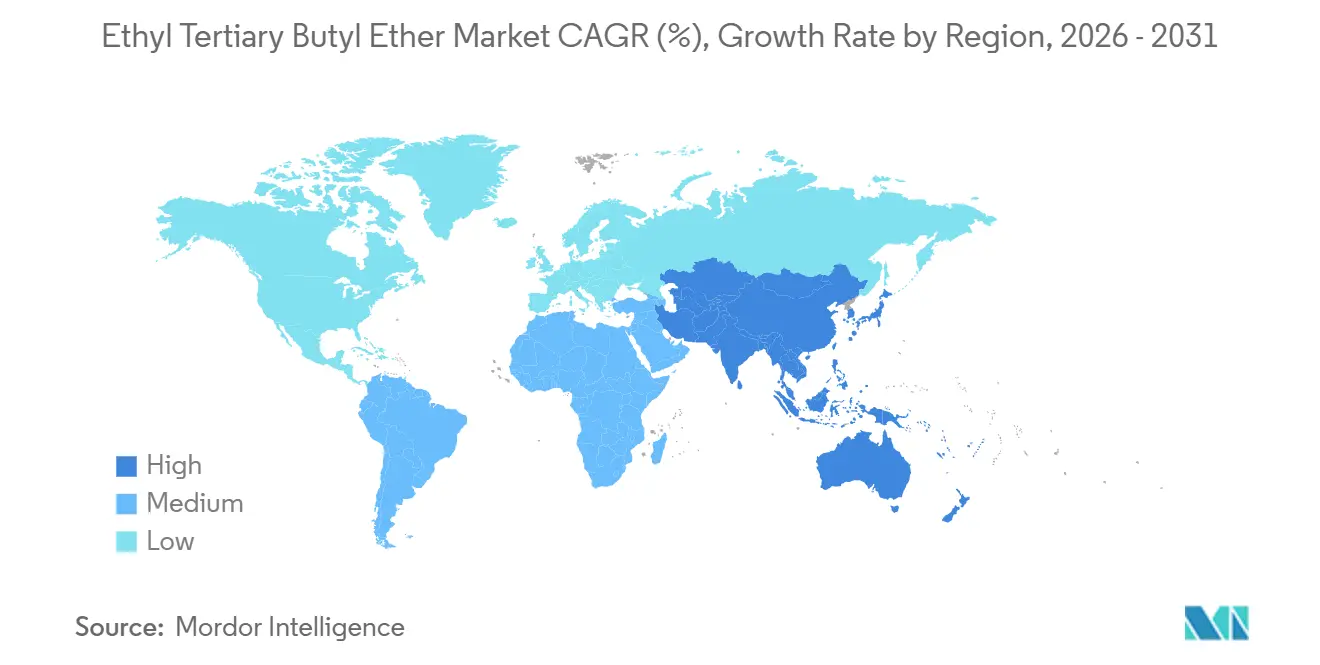

- By geography, Europe commanded 36.22% of 2025 global revenues, whereas Asia-Pacific is set to expand by 9.15% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ethyl Tertiary Butyl Ether Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution of MTBE with ETBE due to lower groundwater-contamination risk | +1.8% | Global, with legacy phase-outs in North America complete; ongoing in Asia-Pacific | Long term (≥ 4 years) |

| Stricter automotive-emission regulations | +2.1% | Europe (Euro 7), North America (EPA Tier 3), China (National VI), India (BS-VI) | Medium term (2-4 years) |

| European Union RED II advanced biofuel quotas unlocking premium demand | +2.4% | Europe, with spillover to markets exporting to EU | Medium term (2-4 years) |

| Integration of renewable isobutylene from industrial waste-gas fermentation | +1.3% | Europe (Global Bioenergies, Leuna plant), North America (Gevo) | Long term (≥ 4 years) |

| Emerging need for oxygenates in low-emission marine and sustainable-aviation fuels | +0.9% | Global, with early regulatory traction in Europe (FuelEU Maritime, ReFuelEU Aviation) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Substitution of MTBE With ETBE Due to Lower Groundwater-Contamination Risk

California banned MTBE in 2003, and the United States phased it out nationwide by 2006 after widespread groundwater contamination, opening durable demand for ETBE as a safer ether alternative. Japan followed in 2003, retrofitting Cosmo Oil’s Sakai unit to ETBE and blending 297,000 kiloliters of bio-ETBE in fiscal 2023. South Korea and Taiwan still review oxygenate options, suggesting incremental uptake as older MTBE capacity retires. ETBE’s faster biodegradation and lower water solubility reduce remediation liabilities for fuel distributors. The substitution effect will taper after 2030 because most legacy MTBE plants will already be converted or shut down.

Stricter Automotive-Emission Regulations

Euro 7, EPA Tier 3, China National VI, and India BS-VI standards tighten limits on NOx, particulates, and aromatics, prompting refiners to raise oxygen content for cleaner combustion. ETBE provides 15.66% oxygen by weight and a RON of 119, letting engines run leaner without calibration changes. China’s GB 18351-2025 caps oxygen at 2.7% for non-ethanol gasoline, carving a premium niche for ETBE in high-octane blends. Europe’s real-driving-emissions testing under cold conditions further rewards low-volatility oxygenates. Regulatory momentum keeps the additive relevant even as direct ethanol blending expands.

European Union RED II Advanced Biofuel Quotas Unlocking Premium Demand

RED II mandates 3.5% advanced biofuels in transport energy by 2030 and counts bio-ETBE produced from Annex IX feedstocks as double credit toward the target. Refiners, therefore, chase certified cellulosic ethanol and emerging bio-isobutylene to lower compliance costs. Double-counting raises the price premium they can pay for bio-ETBE relative to fossil ethers. Japan’s preferential fuel-tax framework had bolstered ETBE imports, but the provisional gasoline-tax cut expiring in 2025 will trim its fiscal edge. European premium-gasoline demand remains the largest guaranteed outlet for certified bio-ETBE volumes.

Emerging Need for Oxygenates in Low-Emission Marine and Sustainable-Aviation Fuels

FuelEU Maritime and ReFuelEU Aviation rules create carbon-intensity ceilings for ships and aircraft serving EU routes[1]International Maritime Organization, “FuelEU Maritime and CORSIA Guidelines,” imo.org. ETBE’s high energy density and drop-in properties make it a candidate co-blend, yet neither ISO 8217 nor ASTM D1655 currently lists it. Global Bioenergies demonstrated up to 50% blend with kerosene that meets key jet-fuel tests, suggesting formal approvals could unlock new demand by the next decade. Until then, the opportunity remains speculative and contributes a modest uplift to long-term growth expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from bioderived ethers and direct ethanol blending | -1.6% | Asia-Pacific (India, China E10 mandates), Europe (E10 adoption 40.3% of petrol sales) | Short term (≤ 2 years) |

| High CAPEX for retrofitting/refurbishing ETBE production units | -0.7% | Global, with acute pressure in Europe and North America where legacy MTBE units require conversion | Medium term (2-4 years) |

| Fragmented ethanol sustainability certification schemes raising compliance cost | -0.5% | Europe (ISCC, RSB, 2BSvs), with spillover to export markets supplying EU refiners | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition From Bioderived Ethers and Direct Ethanol Blending

India reached E20 nationwide in 2025 and now holds 19.9 billion liters of ethanol capacity, making direct blending cheaper than ETBE synthesis[2]Ministry of Petroleum and Natural Gas India, “Ethanol Blending Program Update 2025,” petroleum.nic.in. China’s E10 standard forbids extra oxygenates, so ETBE stays limited to premium non-ethanol grades. Europe’s E10 share of 40.3% in 2023 could grow if Germany scraps its residual E5 grade. Meanwhile, tertiary amyl ethyl ether and other C5-based ethers vie for the same premium-gasoline space. The headwind is strongest in cost-sensitive Asian markets during the next two years.

High CAPEX for Retrofitting ETBE Production Units

Upgrading old MTBE plants requires larger reactors, ethanol-drying membranes, and wastewater systems. Intratec estimates investment at 14% above a greenfield MTBE unit when integrated and 46% higher standalone. Refiners also face falling gasoline demand as electric-vehicle sales climb, raising stranded-asset risk. European sites now channel capital toward renewable diesel and SAF, pushing ETBE to the back of the queue for discretionary spending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Renewable Ethanol Widens Its Lead

Ethanol-based ETBE secured 62.22% of the ethyl tertiary butyl ether market share in 2025, buoyed by RED-compliant cellulosic streams and the U.S.-Brazil ethanol corridor fueling Japanese imports. The Ethyl tertiary butyl ether market size for Ethanol-based ETBE feedstock is projected to expand at a 9.22% CAGR to 2031. Cost sensitivity ties growth to corn and sugarcane price swings, yet double-counting incentives under RED III partially shelter margins. Isobutylene-based ETBE gains strategic relevance as renewable routes mature, especially once Global Bioenergies’ Leuna unit and Gevo’s Net-Zero 1 supply early commercial volumes.

In the medium term, certified-advanced status tilts European demand further toward cellulosic ethanol and waste-gas-derived isobutylene. Beyond 2028, maturing scale economics could let renewable isobutylene replace 15-20% of petrochemical supply, cementing a diversified feedstock base for the Ethyl tertiary butyl ether market.

By Fuel Type: Unleaded Gasoline Retains Largest Share Amid E10 Surge

Unleaded gasoline captured 45.11% of the ethyl tertiary butyl ether market revenue in 2025 and remains the backbone because many premium European and Japanese grades exclude ethanol to limit vapor-pressure spikes. Yet the Ethyl tertiary butyl ether market size associated with E10 and other biofuel blends is set to rise fastest at a CAGR of 9.78% during the forecast period (2026-2031), propelled by mandates that double-count ETBE’s bioethanol contribution and curb aromatics to meet toxic-air-pollutant limits. Germany and France illustrate this duality: E10 penetration rises, but premium E5 retains a profitable ETBE niche.

Going forward, vapor-pressure-limited summer gasoline and cold-start concerns in northern climates continue to justify ether blending. Even so, once vehicle fleets are fully E10-capable and retail networks reconfigured, direct ethanol could claim a larger share, trimming ETBE volumes in standard-grade petrol while preserving it in premium niches, a nuance critical to Ethyl tertiary butyl ether market participants.

By Function: Emissions-Reduction Additives Fastest-Growing Application

Octane enhancer represented 38.88% of the ethyl tertiary butyl ether market size in 2025, anchored in refinery economics, favoring light-hydrocarbon retention. Emissions-reduction additive will rise at a 9.11% CAGR during the forecast period (2026-2031) as Euro 7 and China National VI tighten real-world driving limits. Under these rules, every 1 wt% of oxygen in gasoline can shave unburned-hydrocarbon emissions by up to 15 mg/km, making ETBE attractive because it supplies oxygen without the volatility penalty of ethanol.

Over the forecast window, hybrid powertrains with smaller, turbo-charged gasoline engines favor high-RON oxygenates to mitigate knock at higher compression ratios. This technical synergy places the Ethyl tertiary butyl ether market on a growth pathway tied not just to volume but to premium-grade margin capture.

By End-user Industry: Refineries Dominate, Marine and Aviation Suppliers Emerge

Oil refineries and blending facilities accounted for 50.31% of the ethyl tertiary butyl ether market share in 2025. Their captive reactor, storage, and QC infrastructure minimizes incremental logistics cost, embedding ETBE as a turnkey octane-oxygenate. Independent fuel distributors add flexibility by re-optimizing blends post-terminal, yet their role largely mirrors upstream decisions.

Marine and aviation users, though just a single-digit share today, are expected to post the swiftest CAGR of 9.03% during the forecast period (2026-2031) as the IMO and ICAO layer carbon-intensity rules onto shipping and aviation. Should ASTM D1655 or ISO 8217 broaden oxygenate ceilings, bunker and jet-fuel suppliers may lift blend ratios, creating a new offtake vector for the Ethyl tertiary butyl ether market. Until then, research and development collaborations dominate activity, with pilot demonstrations scheduled at Rotterdam and Singapore test beds in 2026-2027.

Geography Analysis

Europe anchored 36.22% of the ethyl tertiary butyl ether market revenue in 2025, driven by RED III quotas and mature premium-gasoline demand. Germany, France, Italy, and Spain together make up most of the continental throughput because premium grades retain high ETBE loadings. Eastern European refiners such as Orlen Lietuva are also evaluating MTBE-to-ETBE conversions to comply with cross-border export standards.

Asia-Pacific is the fastest-growing region at a 9.15% CAGR through 2031. Japan alone imported 1.83 billion liters of ETBE in 2024 and maintains a hard 500 million-liter ethanol-equivalent mandate. China’s premium gasoline pool, shielded from E10 constraints, still specifies ether oxygenates for high-end brands, preserving upside for the Ethyl tertiary butyl ether market even as mass grades migrate to ethanol. In India, refinery planners assess whether ETBE can coexist with E20 in premium categories once flex-fuel vehicles enter volume after 2028.

North America is mature, operating in the shadow of a 15 billion-gallon-per-year corn-ethanol quota under RFS2. As a result, the Ethyl tertiary butyl ether market presence is confined to specialty racing fuels and limited aviation-gasoline pools. Canada and Mexico follow similar patterns, each favoring direct ethanol blending for cost and availability reasons. South America, led by Brazil, abstains from ETBE because of abundant sugarcane ethanol and entrenched E27.5 gasoline blends.

Middle East-and-Africa uptake remains nascent but strategically interesting. Saudi refiners examine ETBE as a route to meet domestic octane targets without major naphtha reformer expansions, while South Africa’s pending fuel-quality upgrade opens a small premium-grade opportunity. In both sub-regions, low pump prices temper near-term volumes yet leave room for high-margin premium niches.

Competitive Landscape

The ethyl tertiary butyl ether market is moderately concentrated. Process technology plateaued years ago; hence, competitive edge rests on audited sustainable feedstock, integration with refinery logistics, and the agility to pivot between gasoline additives and SAF precursors. These factors collectively set a medium competitive intensity for the Ethyl tertiary butyl ether market.

Ethyl Tertiary Butyl Ether Industry Leaders

LyondellBasell Industries Holdings B.V.

Eni

BP p.l.c.

JX Nippon Oil & Gas Exploration Corporation

Braskem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Researchers conducted an experimental and kinetic modeling study on the combustion of ethyl tert-butyl ether (ETBE) under engine-relevant conditions. Part I focused on high-temperature chemistry, while Part II examined low to intermediate temperature chemistry using ignition delay times for validation. Such research can help in propelling the market.

- November 2025: An assessment aimed to evaluate the potential human carcinogenic risks associated with ETBE by systematically reviewing existing human, animal, and mechanistic data was done. While no epidemiological studies were found, two standard cancer bioassays were conducted for each compound.

Global Ethyl Tertiary Butyl Ether Market Report Scope

Ethyl tert-butyl ether (ETBE) is a clear, colorless, and highly flammable liquid primarily used as a gasoline oxygenate to increase octane ratings and reduce engine emissions.

The ethyl tertiary butyl ether market is segmented by feedstock, fuel type, function, end-user industry, and geography. By feedstock, the market is segmented into ethanol-based ETBE and isobutylene-based ETBE. By fuel type, the market is segmented into unleaded gasoline, premium gasoline, E10 and other biofuel blends, and other fuel types. By function, the market is segmented into octane enhancer, anti-knocking agent, oxygenate fuel additive, and emissions-reduction additive. By end-user industry, the market is segmented into oil refineries and blending facilities, fuel distributors and retail chains, automotive OEMs and aftermarket, marine and aviation fuel suppliers, government and regulatory agencies, and testing labs and custom blenders. The report also covers the market size and forecasts for ethyl tertiary butyl ether in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Ethanol-based ETBE |

| Isobutylene-based ETBE |

| Unleaded Gasoline |

| Premium Gasoline |

| E10 and Other Biofuel Blends |

| Other Fuel Types |

| Octane Enhancer |

| Anti-knocking Agent |

| Oxygenate Fuel Additive |

| Emissions-reduction Additive |

| Oil Refineries and Blending Facilities |

| Fuel Distributors and Retail Chains |

| Automotive OEMs and Aftermarket |

| Marine and Aviation Fuel Suppliers |

| Government and Regulatory Agencies |

| Testing Labs and Custom Blenders |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Feedstock | Ethanol-based ETBE | |

| Isobutylene-based ETBE | ||

| By Fuel Type | Unleaded Gasoline | |

| Premium Gasoline | ||

| E10 and Other Biofuel Blends | ||

| Other Fuel Types | ||

| By Function | Octane Enhancer | |

| Anti-knocking Agent | ||

| Oxygenate Fuel Additive | ||

| Emissions-reduction Additive | ||

| By End-user Industry | Oil Refineries and Blending Facilities | |

| Fuel Distributors and Retail Chains | ||

| Automotive OEMs and Aftermarket | ||

| Marine and Aviation Fuel Suppliers | ||

| Government and Regulatory Agencies | ||

| Testing Labs and Custom Blenders | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for ethyl tertiary butyl ether be by 2031?

The Ethyl Tertiary Butyl Ether Market size is projected to be USD 7.12 billion in 2025, USD 7.79 billion in 2026, and reach USD 12.21 billion by 2031, growing at a CAGR of 9.41% from 2026 to 2031.

Which region shows the fastest growth pace?

Asia-Pacific is anticipated to post the highest 9.15% CAGR during the forecast period (2026-2031) owing to Japan’s import mandate and premium-gasoline demand in China.

What feedstock dominates current production?

Ethanol supplies 62.22% of 2025 volumes and remains the primary feedstock because it helps refiners meet RED II biofuel quotas.

Why do refiners prefer ETBE over direct ethanol in premium gasoline?

ETBE delivers higher octane with lower vapor pressure, allowing refiners to hit RON targets without breaching evaporative-emission limits.

Page last updated on: