Decabromodiphenyl Ether Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.20 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 3.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Decabromodiphenyl Ether Market Analysis by Mordor Intelligence

The Decabromodiphenyl Ether Market size is expected to increase from USD 1.16 billion in 2025 to USD 1.20 billion in 2026 and reach USD 1.45 billion by 2031, growing at a CAGR of 3.83% over 2026-2031. Asia-Pacific regulatory exemptions that allow recycled plastics to contain up to 1,000 mg/kg of decaBDE support significant volumes in electronics and automotive parts, even as the European Union enforces a stricter unintentional-trace limit of 10 mg/kg. Integrated Dead Sea producers maintain bromine production costs below USD 2.70 per kg, providing a 20-30% price advantage over phosphorus-based alternatives and preserving gross margins. Polyolefins dominate the decabromodiphenyl ether market due to their ability to achieve UL 94 V-0 ratings in wire-and-cable jacketing with only 10-12% loading. Polyurethane is the fastest-growing material, as spray-foam applications can meet ASTM E84 standards without requiring additional intumescent coatings. Electronics housings remain the primary application, but recycled automotive plastics are gaining market share as European circularity regulations mandate 25% recycled content, allowing legacy bromine additives to remain below threshold limits when diluted.

Key Report Takeaways

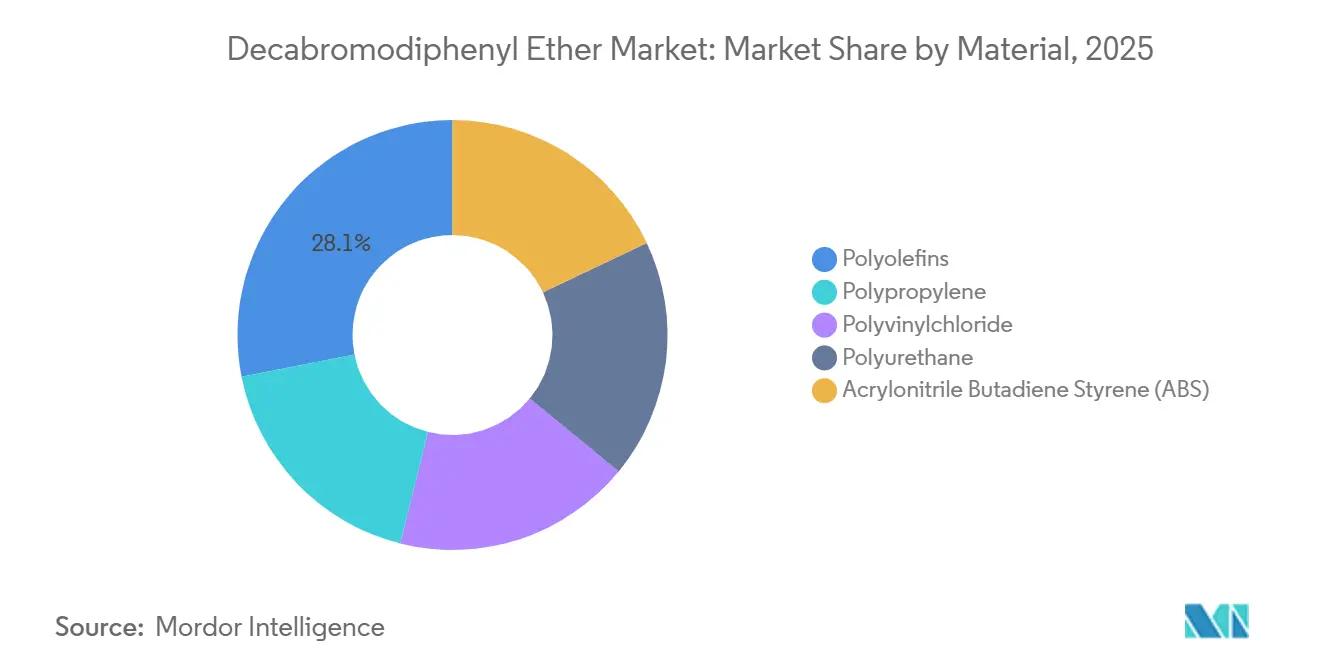

- By material, polyolefins led with 28.11% of decabromodiphenyl ether market share in 2025, while polyurethane is forecast to expand at a 4.33% CAGR through 2031.

- By application, electrical and electronic equipment housings accounted for a 33.39% decabromodiphenyl ether market share in 2025, while automotive components are advancing at a 4.22% CAGR through 2031.

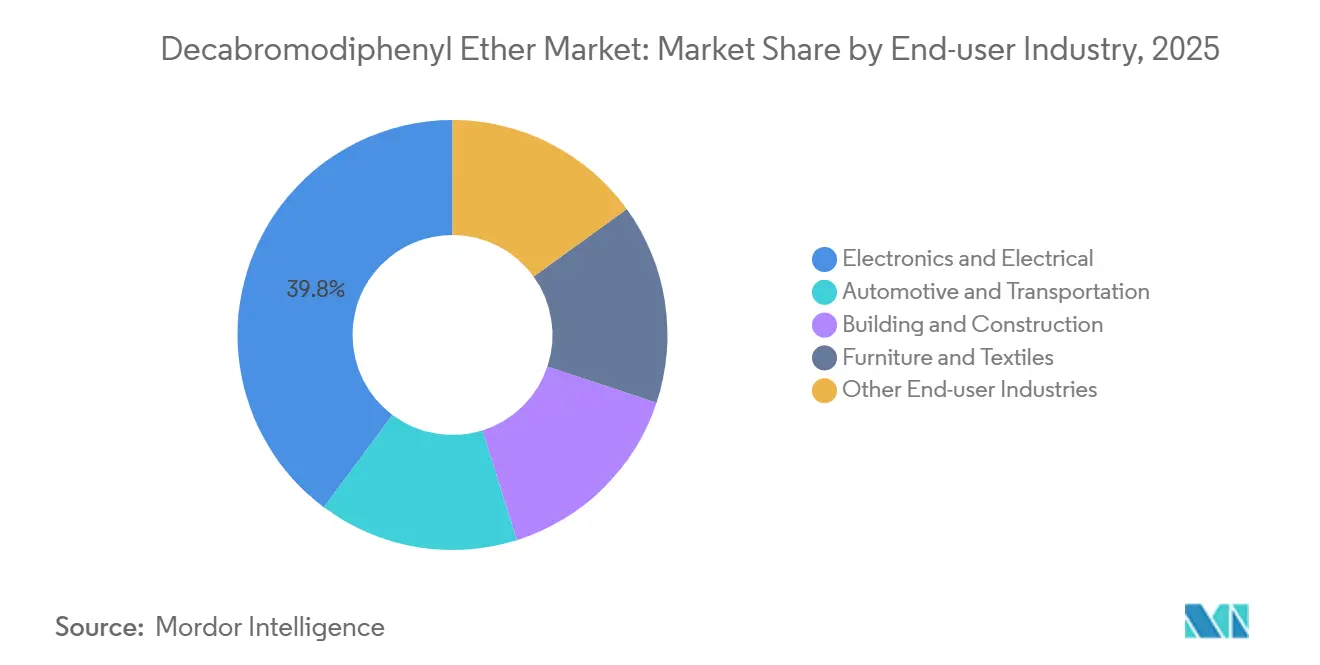

- By end-user industry, electronics and electrical accounted for a 39.78% decabromodiphenyl ether market share in 2025, while automotive and transportation is advancing at a 4.67% CAGR through 2031.

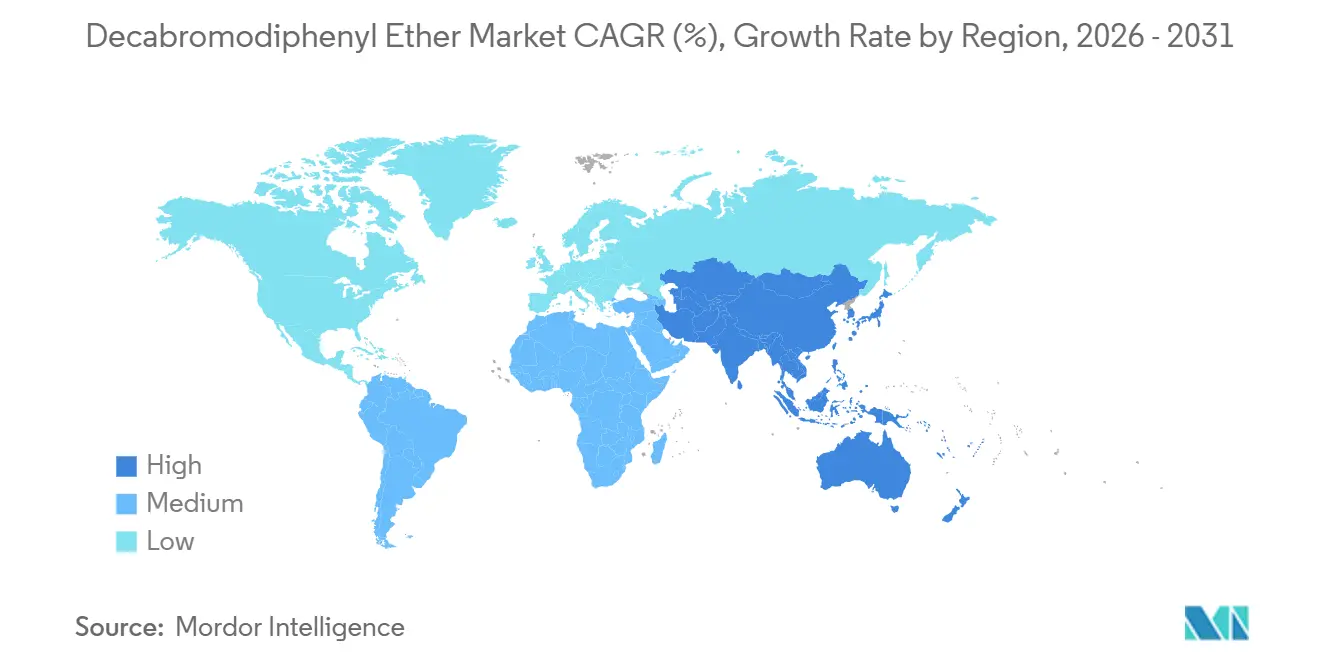

- By geography, Asia-Pacific held 50.44% decabromodiphenyl ether market share in 2025 and is projected to record the highest regional 4.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Decabromodiphenyl Ether Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust demand from Electronics and Electrical plastics sector | +1.2% | Global, concentrated in Asia-Pacific (China, South Korea, Vietnam) and North America | Medium term (2-4 years) |

| Growth of construction plastics in developing economies | +0.9% | Asia-Pacific (India, ASEAN), Middle-East and Africa, and South America | Long term (≥ 4 years) |

| Cost-competitiveness versus alternative brominated FRs | +0.7% | Global, particularly Asia-Pacific and Middle-East with low-cost bromine feedstock | Short term (≤ 2 years) |

| Asia-Pacific regulatory exemptions for recycled plastics containing decaBDE | +0.6% | Asia-Pacific (China, India, ASEAN countries) | Medium term (2-4 years) |

| Rising use in recycled automotive interior plastics | +0.5% | Europe, North America, Asia-Pacific (Japan, South Korea) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Demand from Electronics and Electrical Plastics Sector

Consumer electronics, data-center hardware, and EV charging equipment collectively accounted for 39.78% of projected 2025 usage. Miniaturized connectors and thin-wall housings require UL 94 V-0 compliance at thicknesses below 0.75 mm, achievable with 8-10% decaBDE in PC/ABS blends that also meet Lenovo’s 900 ppm total-halogen limit. Improved sales in LANXESS’s Electro and Electronics division during Q4 2025 highlight the demand for high-heat components in 5G and AI cards, which offset the broader shift toward halogen-free chemistries. The IEC 62368-1 standard, allowing components to operate at temperatures up to 150 °C, favors decaBDE over intumescent coatings that degrade near 120 °C. China, producing approximately 35% of global electronics, continues to specify decaBDE, as its draft GB/T recycled-plastics standard permits 1,000 mg/kg in non-food-contact applications.

Growth of Construction Plastics in Developing Economies

Rigid foam insulation used in metro, airport, and warehouse projects across India, Indonesia, and the Philippines must comply with ASTM E84 flame-spread indices of ≤75 and smoke indices of ≤450. Formulations containing 10-14% decaBDE meet these requirements while reducing installed costs by 18-22% compared to halogen-free systems[1]International Code Council, “IBC 2024 and Proposed 2027 Revisions,” iccsafe.org. The Asian Development Bank projects Southeast Asia will invest over USD 200 billion annually in infrastructure through 2030, driving demand for polyurethane and PIR boards incorporating brominated flame retardants. In the U.S., spray-foam contractors also favor decaBDE blends for simplifying compliance with ICC-ES AC377 compared to phosphorus systems, which require higher loadings.

Cost Competitiveness Versus Alternative Brominated FRs

Dead Sea brines, containing over 5,000 mg/L bromine, approximately 10 times the concentration found in Arkansas, keep energy costs near USD 0.40 per kg of elemental bromine. Spot prices for decaBDE in Asia ranged between USD 3.50 and USD 4.20 per kg in late 2025, remaining below TBBPA and DBDPE prices of USD 4.80–5.60 per kg. Phosphorus esters require 15-20% loading to achieve UL 94 V-0 compliance in PC/ABS, effectively doubling additive costs. The 8% decline in average U.S. bromine import values to approximately USD 2.70 per kg in 2024 further enhanced relative margins for decaBDE compounders.

Asia-Pacific Regulatory Exemptions for Recycled Plastics Containing DecaBDE

China’s draft GB/T standard permits recycled plastics for non-food applications to contain up to 1,000 mg/kg of decaBDE, significantly higher than the EU’s 10 mg/kg trace limit. European manufacturers must segregate low-halogen streams, while Asian OEMs blend 30-40% post-consumer ABS or polypropylene without additional testing. South Korea’s revised EPR law mandates 25% recycled content by 2027 but does not enforce substance checks, allowing companies like Samsung and LG to use recyclates containing 5-8% decaBDE. This regulatory disparity is expected to persist until the European Commission negotiates harmonized limits with trading partners after 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU REACH and Stockholm Convention restrictions | -0.8% | Europe, with spillover effects in North America and developed Asia-Pacific markets | Short term (≤ 2 years) |

| Commercial shift toward safer substitute chemistries | -0.5% | Global, led by North America and Europe; gradual adoption in Asia-Pacific | Medium term (2-4 years) |

| OEM sustainability procurement bans | -0.4% | Global, concentrated in automotive and electronics sectors in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU REACH and Stockholm Convention Restrictions

The EU reduced the unintentional-trace limit for PBDEs to 10 mg/kg in 2026, effectively eliminating most recycled ABS and polypropylene streams[2]European Parliament, “Regulation on End-of-Life Vehicles,” europa.eu. X-ray fluorescence testing adds USD 0.08-0.12 per kg to compounding costs and rejects up to 70% of recyclate. Canada’s outright ban on DBDPE and Australia’s 2027 deadline indicate that OECD markets for decaBDE could contract by 15-18% through 2031. Regulatory filings reveal that each new risk assessment under REACH or TSCA costs producers over USD 2 million per substance, prompting consolidation among smaller bromine manufacturers.

Commercial Shift Toward Safer Substitute Chemistries

Albemarle’s SAYTEX polymeric flame retardants, which claim a 70% lower carbon footprint compared to BPADP, are undergoing trials in European battery enclosures. LANXESS promotes polymeric brominated flame retardants that chemically bond to polymers, reducing migration. Halogen-free phosphates and aluminum phosphinates currently hold 12-15% of the European market despite a 25-30% price premium. Industry association PINFA continues to advocate for halogen-free standards, though higher loadings often reduce impact strength and elongation, slowing adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polyolefins Dominate While Polyurethane Accelerates

Polyolefins accounted for 28.11% of the decabromodiphenyl ether market share in 2025 because 10-12% decaBDE ensures UL 94 V-0 compliance in wire-and-cable jacketing and electrical housings. The segment's cost advantage over halogen-free compounds sustains demand, even with procurement bans from certain white-goods brands.

Polyurethane exhibited the highest growth rate, with a 4.33% CAGR through 2031, as spray-foam contractors increasingly use decaBDE blends to meet ASTM E84 standards without requiring gypsum-board thermal barriers. While changes in building-code smoke limits and the adoption of metal-faced PIR panels may reduce additive intensity, growing insulation demand in Asia continues to drive revenue growth.

By Application: Electrical and Electronic Equipment Housings Lead, While Automotive Components Gains Momentum

Electrical and electronic equipment housings represented 33.39% of 2025 demand, driven by ABS and PC/ABS parts requiring flame protection in thin-wall applications. The miniaturization of 5G and AI hardware, along with high halogen tolerance in the Asia-Pacific region, ensures a stable production base. Automotive components are projected to grow at the fastest rate, with a 4.22% CAGR through 2031, as EU regulations mandate the use of recycled plastics, many of which contain legacy decaBDE. This allows compounders to achieve UL 94 V-0 compliance at competitive costs. The market share tied to automotive interiors is expected to grow, particularly in dashboards and door-panel blends.

Wire and cable applications remain a consistent outlet, although the shift to fiber optic and low-voltage Ethernet systems is expected to limit long-term tonnage growth. In the construction sector, stricter smoke-developed limits from 2027 onward may require higher additive loads or a partial transition to intumescent coatings, potentially restraining revenue growth.

By End-user Industry: Electronics and Electrical Lead, While Automotive and Transportation Rise

The electronics and electrical industry accounted for 39.78% of 2025 consumption. Asia's significant share of global gadget manufacturing and relaxed recycled-plastic thresholds support the continued use of decaBDE in housings, connectors, and power supplies.

The automotive and transportation sector is expected to grow at the fastest rate, with a 4.67% CAGR through 2031, as recycled ABS and polypropylene streams containing 5-8% decaBDE provide OEMs with a cost-effective solution to meet 25% recycled-content mandates. However, the market share associated with building and construction insulation may decline as green-label programs penalize the use of persistent additives.

Geography Analysis

Asia-Pacific controlled 50.44% of the decabromodiphenyl ether market share in 2025 and is projected to grow at a 4.71% CAGR through 2031, supported by China's 1,000 mg/kg recycled-plastic allowance and the development of a 30,000 tpa seawater bromine plant in Caofeidian. India's infrastructure projects further drive demand for PIR boards and spray foam. Additionally, Japan and South Korea export decaBDE-containing scrap to Vietnam and China, effectively transferring environmental liabilities offshore.

In North America, Albemarle's Magnolia and LANXESS's El Dorado facilities provide supply security, with Tetra Technologies expected to increase Arkansas output by late 2027. However, EPA's TSCA risk evaluations and OEM procurement bans pose challenges to growth. Canada's DBDPE ban is pushing local electronics manufacturers toward halogen-free PC/ABS, reducing decabromodiphenyl ether market revenue.

Europe faces significant challenges, with the POPs Regulation's 10 mg/kg trace limit and the 2028 digital passport mandate reducing usable recyclate streams and accelerating substitution. Germany, France, and the United Kingdom have implemented halogen-free building-insulation regulations, while Russia and CIS nations continue to purchase brominated systems, providing a limited outlet for regional suppliers.

South America, the Middle-East, and Africa account for a smaller share of the market. Lax enforcement of brominated additive limits and rapid construction spending contribute to modest but stable consumption, often supplied by cost-competitive Chinese producers.

Competitive Landscape

The market is moderately concentrated. Dead Sea brines provide bromine at an energy cost below USD 0.40 per kg, enabling producers to supply decaBDE in Asia at USD 2.70 per kg, compared to USD 3.50-4.20 from Chinese seawater-extraction plants. ICL's Industrial Products unit reported USD 1.254 billion in revenue with a 22% margin in 2025, despite volume declines in North America and Europe. Albemarle's Specialties revenue reached USD 1.366 billion, though 2026 guidance is lower following a January 2026 flood at its Jordan Bromine Company joint venture. LANXESS's Specialty Additives sales totaled EUR 2.056 billion, with Q4 2025 electronics volumes showing positive growth.

Chinese competitors, such as Shandong Haiwang and Oceanchem, are expanding seawater-extraction facilities but lack downstream application labs to meet OEM flame-test requirements. USGS import data indicates that Israel supplied 87% of U.S. bromine volumes in 2024, highlighting geopolitical concentration. New entrants are introducing polymeric brominated systems that withstand pyrolysis recycling and reduce leaching, but their 30-40% price premium limits adoption to high-margin niches.

Decabromodiphenyl Ether Industry Leaders

Albemarle Corporation

LANXESS

ICL

Shandong Haiwang Chemical Co., Ltd

Unibrom Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: The US Environmental Protection Agency finalized stricter PBT rules under TSCA for decabromodiphenyl ether and PIP (3:1), setting a 0.1% concentration limit and mandatory PPE requirements, effective January 2025. These revisions resulted in higher compliance costs and stricter reporting standards for manufacturers in the electronics, automotive, and nuclear industries.

- July 2024: The European Commission's updated REACH Restrictions Roadmap, which paused restrictions on certain organophosphate flame retardants pending hazard evaluations, introduced regulatory uncertainty that extended the competitive position of legacy substances such as decabromodiphenyl ether. Although intended to support the gradual phase-out of harmful flame retardants, this adjustment impacted substitution trends and sustained demand for decabromodiphenyl ether in specific high-performance applications where alternatives had not yet been fully adopted.

Global Decabromodiphenyl Ether Market Report Scope

Decabromodiphenyl ether (decaBDE) is a highly brominated flame retardant that has been widely used in plastics, electronics, and textiles. In 2017, it was classified as a hazardous pollutant under the Stockholm Convention due to its persistence and bioaccumulative properties.

The Decabromodiphenyl Ether Market is segmented into material, application, end-user industry, and geography. By material, the market is segmented into polyolefins, polyvinylchloride, polyurethane, acrylonitrile butadiene styrene (ABS), and polypropylene. By application, the market is segmented into electrical and electronic equipment housings, wire and cable, textiles and upholstery, construction materials (insulation foams, panels), automotive components (dashboards, seating plastics), and other applications. By end-user industry, the market is segmented into electronics and electrical, automotive and transportation, building and construction, furniture and textiles, and other end-user industries. The report also covers the market size and forecasts for decabromodiphenyl ether in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Polyolefins |

| Polyvinylchloride |

| Polyurethane |

| Acrylonitrile Butadiene Styrene (ABS) |

| Polypropylene |

| Electrical and Electronic Equipment Housings |

| Wire and Cable |

| Textiles and Upholstery |

| Construction Materials (Insulation Foams, Panels) |

| Automotive Components (Dashboards, Seating Plastics) |

| Other Applications |

| Electronics and Electrical |

| Automotive and Transportation |

| Building and Construction |

| Furniture and Textiles |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material | Polyolefins | |

| Polyvinylchloride | ||

| Polyurethane | ||

| Acrylonitrile Butadiene Styrene (ABS) | ||

| Polypropylene | ||

| By Application | Electrical and Electronic Equipment Housings | |

| Wire and Cable | ||

| Textiles and Upholstery | ||

| Construction Materials (Insulation Foams, Panels) | ||

| Automotive Components (Dashboards, Seating Plastics) | ||

| Other Applications | ||

| By End-user Industry | Electronics and Electrical | |

| Automotive and Transportation | ||

| Building and Construction | ||

| Furniture and Textiles | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the decabromodiphenyl ether market?

The decabromodiphenyl ether market stands at USD 1.20 billion in 2026 and is forecast to reach USD 1.45 billion by 2031.

Which region contributes the most revenue?

Asia-Pacific supplied 50.44% of worldwide sales in 2025 and shows the highest regional growth at 4.71% CAGR through 2031.

What application will add demand the quickest through 2031?

Automotive components are projected to climb at a 4.22% CAGR through 2031 as OEMs blend recycled, decaBDE-containing resin to meet circularity rules.

Why do electronics manufacturers favor decaBDE?

The additive secures UL 94 V-0 at low loading, fits IEC 62368-1 high-temperature parts, and retains a 20-30% cost edge over phosphorus systems.

Page last updated on: