2-Ethyl Hexanol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.88 Billion |

| Market Size (2031) | USD 8.36 Billion |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

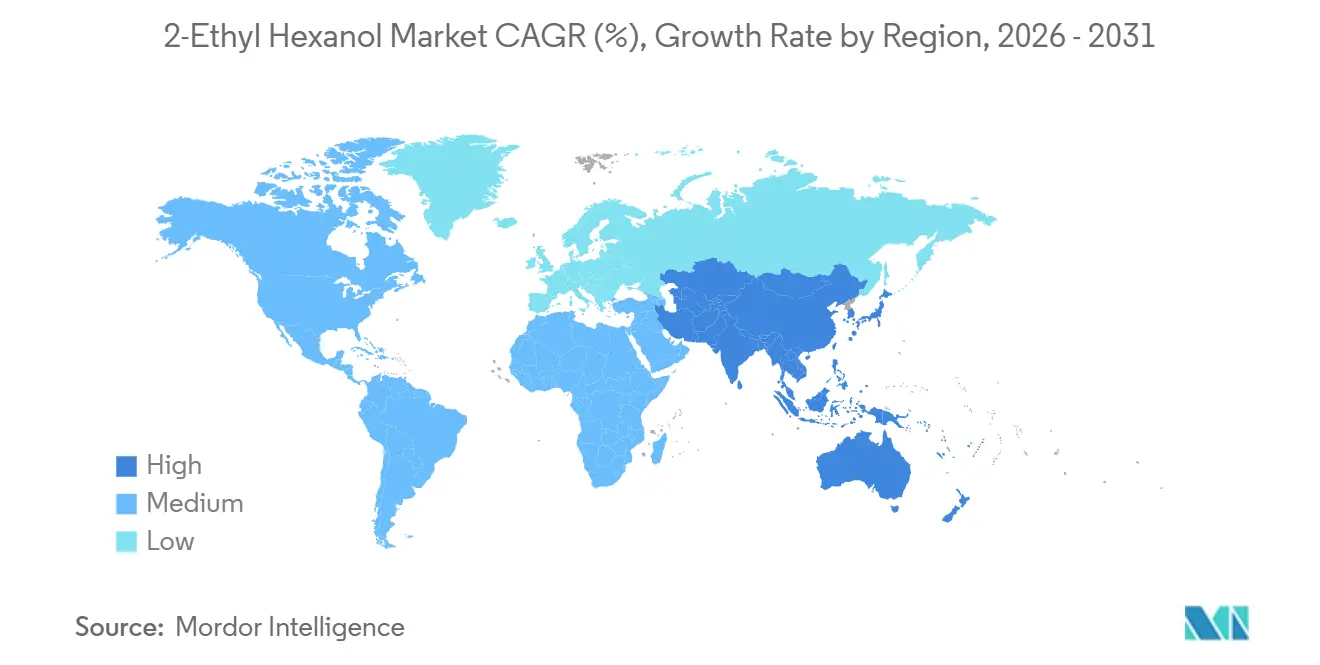

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

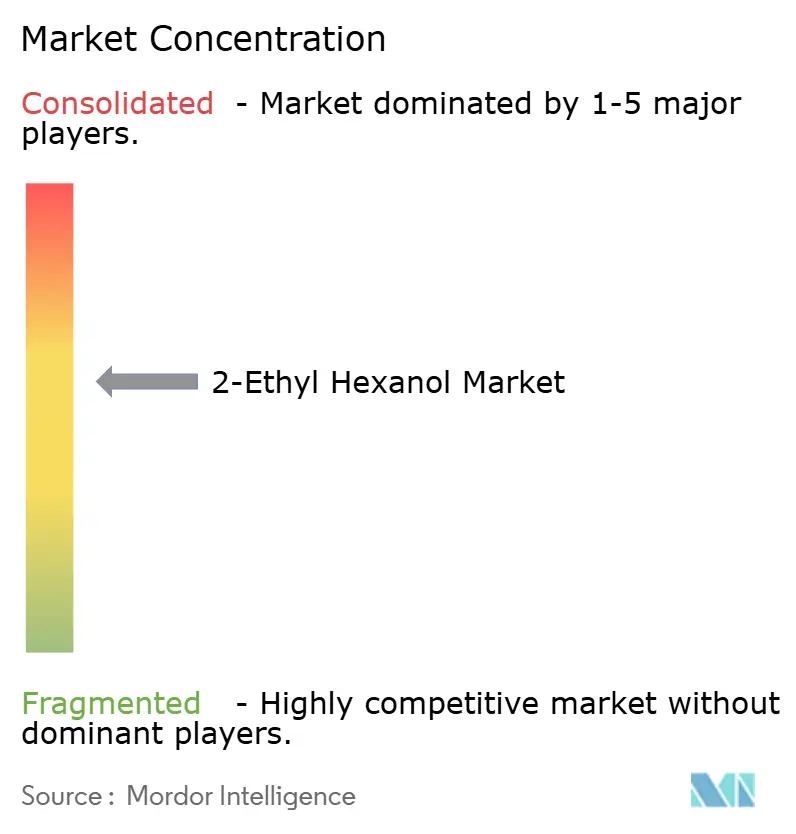

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

2-Ethyl Hexanol Market Analysis by Mordor Intelligence

The 2-Ethyl Hexanol Market size is expected to grow from USD 6.62 billion in 2025 to USD 6.88 billion in 2026 and is forecast to reach USD 8.36 billion by 2031 at 3.98% CAGR over 2026-2031. Demand remains anchored to plasticizers for flexible PVC (polyvinyl chloride), yet rising use of 2-ethylhexyl acrylate in low-VOC coatings and 2-ethylhexyl nitrate in fuel additives is steadily diversifying consumption patterns. Asia-Pacific keeps its leading revenue position because India and China continue to scale downstream petrochemicals, while Europe is steering demand toward non-phthalate and bio-based grades as REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) deadlines approach. Feedstock volatility persists as negative propane-dehydrogenation (PDH) margins and outages at Northeast Asian crackers lift propylene costs, squeezing oxo-alcohol producers and encouraging vertical integration. Producers are responding with capacity additions in Malaysia and Germany, and by certifying renewable 2-EH grades for medical devices and food-contact applications.

Key Report Takeaways

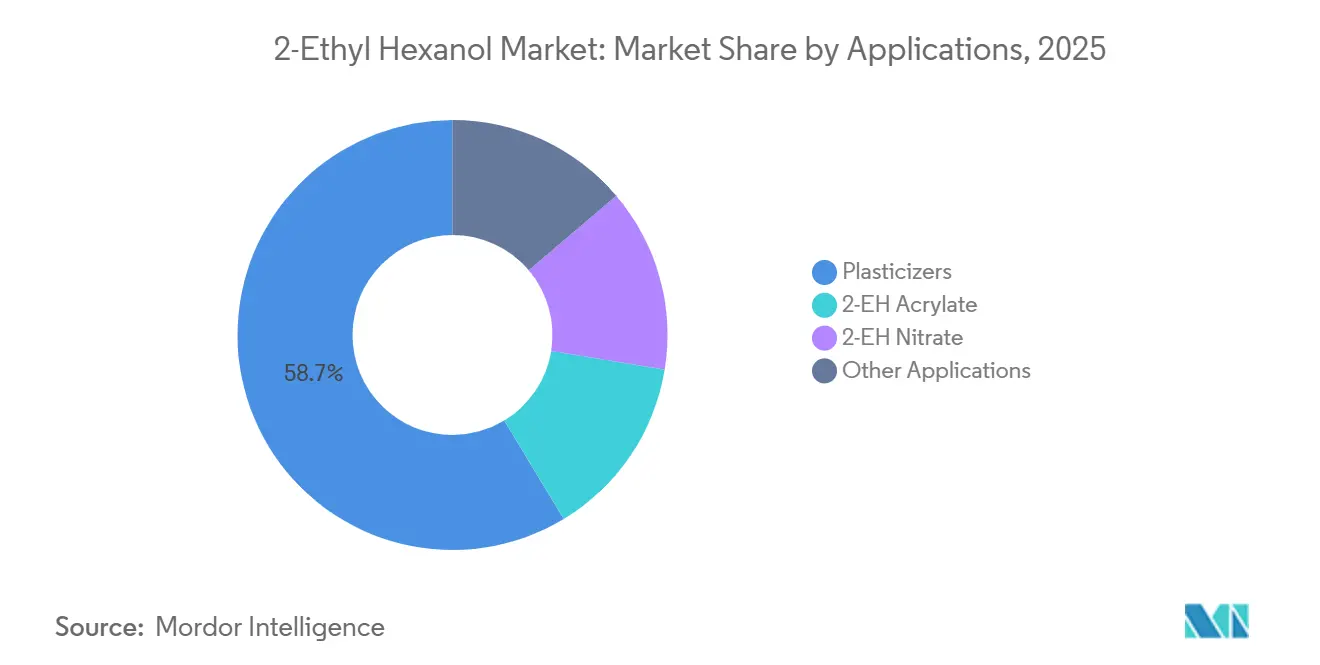

- By application, plasticizers had a share of 58.65% in 2025, and the share of 2-EH Acrylate is expected to increase at a CAGR of 6.31% during the forecast period (2026-2031).

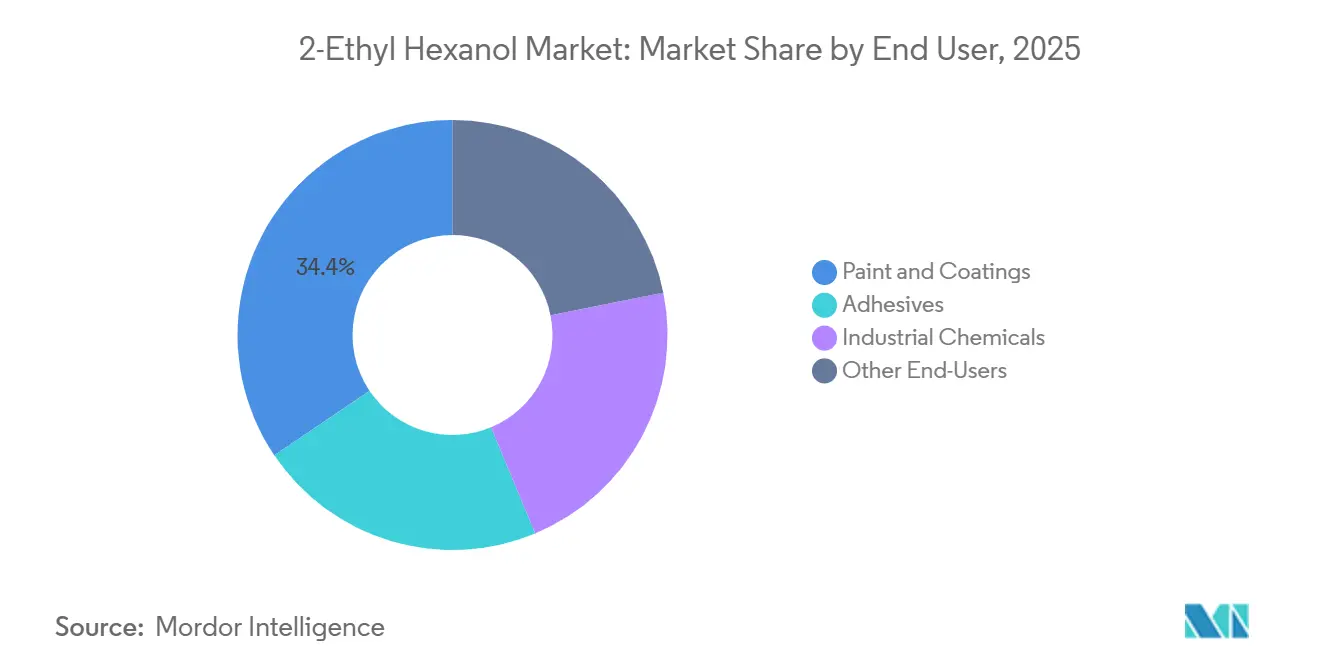

- By end-user, paints and coatings had a share of 34.44% in 2025, and the share of adhesives is poised to grow with a CAGR of 6.22% during the forecast period (2026-2031).

- By geography, the Asia Pacific had a share of 53.12% in 2025, and the region's share is expected to grow with a CAGR of 5.98% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 2-Ethyl Hexanol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plasticizers demand growth in flexible PVC (construction and automotive) | +1.8% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2–4 years) |

| Rising adoption of high-solids/low-VOC coatings driving 2-EH acrylate usage | +1.2% | Global, with early gains in Europe and North America | Short term (≤ 2 years) |

| Diesel performance additives (2-EH nitrate) demand in emerging markets | +0.6% | Asia-Pacific, Middle East & Africa | Long term (≥ 4 years) |

| Capacity expansions in Asia-Pacific improving price competitiveness | +0.9% | Asia-Pacific, export flows to North America and Europe | Medium term (2–4 years) |

| Bio-based 2-EH pilot plants gaining regulatory incentives | +0.4% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plasticizers Demand Growth in Flexible PVC (Construction and Automotive)

Plasticized PVC remains essential for wire-and-cable, flooring, films, and interior trim, and flexible PVC plasticizers captured 38.6% of global plasticizer use in 2024. India’s USD 37 billion petrochemical build-out is reinforcing domestic demand for both DEHP (Di(2-ethylhexyl)phthalate) and newer terephthalate esters, while automotive lightweighting is steering OEMs (original equipment manufacturers) toward non-phthalate alternatives such as DOTP (dioctyl terephthalate) that can satisfy Proposition 65 and REACH migration limits. Battery-electric vehicles further amplify the need for flame-retardant, low-migration plasticizers in harnesses and pack enclosures, fostering interest in premium trimellitate and cyclohexanoate esters. Producers, therefore, continue to rely on 2-ethylhexanol as an alcohol component even as they reformulate away from legacy phthalates[1]Bastone, “Non-phthalate Plasticizers Gain Traction in Medical and Auto Uses,” bastone.com.

Rising Adoption of High-Solids / Low-VOC Coatings Driving 2-EH Acrylate Usage

Architectural and industrial formulators are shifting to high-solids resins that cut VOC emissions 30-50% to meet EU Directive 2004/42/EC and U.S. EPA (Environmental Protection Agency) air-toxics rules. 2-Ethylhexyl acrylate replaces butyl acrylate because its longer alkyl chain improves film flexibility and wet-edge time without sacrificing scrub resistance. BASF raised 2-EHA prices by as much as USD 100 per tonne across Asia-Pacific in March 2026 to offset rising energy and compliance costs, underscoring tight supply-demand balances. Offshore wind towers and marine assets are adopting 2-EHA-based resins to satisfy ISO 12944 corrosion standards, while e-commerce packaging fuels demand for fast-curing, low-odor pressure-sensitive adhesives that depend on 2-EHA copolymers[2]BASF, “BASF Adjusts Prices for 2-Ethylhexyl Acrylate in Asia-Pacific,” basf.com.

Diesel Performance Additives (2-EH Nitrate) Demand in Emerging Markets

Global 2-ethylhexyl nitrate consumption reached 221,000 tonnes in 2024 and is forecast to climb to 302,000 tonnes by 2035. Asia-Pacific and Sub-Saharan Africa lead growth as diesel generators backstop intermittent renewables and on-road fleets strive to meet Euro VI and Bharat Stage VI norms. 2-EH nitrate decomposes near 150°C to improve cetane and cut ignition delay, enabling refiners to comply without expensive engine recalibration. Chinese suppliers such as Zhengzhou Chorus Lubricant Additive are scaling 10,000 tpy (tons per year) units and pricing at 15-20% below Western peers, heightening price pressure on incumbents.

Capacity Expansions in Asia-Pacific Improving Price Competitiveness

BASF Petronas Chemicals doubled annual 2-ethylhexanoic acid output at Kuantan to 60,000 tons per year when its second train reached full operation in Q3 2026. Integrated production with regional cracker streams lowers logistics costs and enables volume swings between Europe and Asia as arbitrage dictates. Parallel olefin investments in China, including a 950,000 tons per year polyethylene line at Huajin Aramco, will lift propylene supply for downstream oxo-alcohols once operational in 2026, potentially easing the PDH margin squeeze that dominated 2025.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Phthalate-related regulations restricting traditional plasticizer chain | -1.1% | Europe and North America core, spill-over to Asia-Pacific | Medium term (2–4 years) |

| Volatile propylene feedstock prices squeezing producer margins | -0.8% | Global | Short term (≤ 2 years) |

| EU REACH evaluation may tighten occupational exposure limits | -0.3% | Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Phthalate-Related Regulations Restricting Traditional Plasticizer Chain

California’s AB 2300 outlaws DEHP in IV bags by 2030 and tubing by 2035, while the European Chemicals Agency restricts four major phthalates below 0.1 wt% in most goods. As a result, non-phthalate plasticizers advanced from USD 3.99 billion in 2024 to USD 4.30 billion in 2025 and should attain USD 6.15 billion by 2030 at 7.47% CAGR. Premiums for DOTP and DINCH have narrowed to under 10% thanks to capacity additions in Germany and the United States, but maintaining parallel phthalate and non-phthalate supply chains inflates producer operating costs by roughly 29%.

Volatile Propylene Feedstock Prices Squeezing Producer Margins

Propylene spot values in Northeast Asia slid to USD 830-835 per tonne cfr in April 2025, yet PDH margins stayed at a negative USD 121 per tonne because propane costs remained elevated and multiple PDH units ran below 70%. Naphtha cracker margins also fell below zero as weak polymer demand intersected with tariff uncertainty after the United States imposed new duties up to 46% on certain imports and China retaliated. A brief shutdown of the Strait of Hormuz lifted naphtha prices and prompted force majeure at regional crackers, revealing how feedstock shocks ripple through oxo-alcohol pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Applications: Plasticizers Anchor Volume, Acrylates Drive Growth

Plasticizers maintained 58.65% of the 2-Ethylhexanol market share in 2025 as flexible PVC continued to dominate cable, flooring, and film applications. The 2-Ethylhexanol market size tied to Acrylates is forecast to expand at a 6.31% CAGR through 2031, outpacing every other application because low-VOC coatings and pressure-sensitive adhesives rely on 2-EHA’s long alkyl chain for flexibility and cure balance.

Regulatory migration caps are shifting demand away from DEHP toward terephthalate esters such as DOTP and cyclohexanoates like DINCH, yet these still depend on 2-ethylhexanol as the alcohol component. BASF and Evonik upgraded DINCH capacity in Germany during 2024 and 2025, removing previous supply bottlenecks and narrowing the price gap with legacy phthalates to single-digit percentages.

By End User: Coatings Lead Share, Adhesives Accelerate

Paints and Coatings represented 34.44% of 2025 consumption, and the associated 2-ethylhexanol market size benefits from mandatory VOC caps under EU and U.S. air-quality rules that favor 2-EHA-rich high-solids formulations. Adhesives constitute the fastest-growing end user, projected at 6.22% CAGR through 2031, driven by e-commerce packaging that requires rapid curing and low odor, and by electric-vehicle assembly where structural bonding replaces mechanical fasteners.

Industrial chemicals, largely plasticizers destined for construction and automotive interiors, face mid-single-digit growth in Asia-Pacific but remain flat in Europe, while lubricant additives and specialty solvents provide niche outlets that stabilize demand when construction cycles soften. OQ Chemicals’ restoration of synthesis-gas operations in Germany during 2024 removed a price overhang in these smaller segments and underscored the sensitivity of global 2-EH trade flows to single-site disruptions.

Geography Analysis

Asia-Pacific captured 53.12% of 2025 revenue and should post 5.98% CAGR through 2031 as India’s multi-billion-dollar refinery expansions and China’s ongoing infrastructure build sustain flexible PVC and coatings demand. Beijing’s consolidation of older naphtha crackers and South Korea’s shuttering of a 1.1 million tons per year unit at Daesan in February 2026 will tighten regional olefins and potentially firm 2-EH pricing in the near term. Concurrently, fresh polyethylene and polypropylene projects due online in 2026 promise to ease the propylene deficit that weighed on PDH economics in 2025.

North America leverages shale-advantaged ethane but contends with mature construction markets and tariff volatility. Eastman’s Longview, Texas, integrated Oxo platform secures local propylene and cushions margin swings, while California’s looming DEHP bans accelerate the pivot to DOTP and DINCH in medical devices. Mexico and Canada supply automotive interiors and harnesses under USMCA rules, intensifying demand for low-migration plasticizers and high-solids adhesives.

Europe enforces the tightest phthalate regulations, yet it is leading on renewable content. BASF doubled DINCH output at Ludwigshafen, and Evonik boosted DINCH/DINCD capacity at Marl in 2024, reflecting confidence that non-phthalate volumes will offset shrinking DEHP demand. Perstorp’s ISCC PLUS-certified renewable 2-EH targets scope-3 emission cuts for medical-device firms. However, imports of low-cost Asian plasticizers compress margins, and capacity rationalizations are likely as crackers close across Western Europe.

South America and the Middle East & Africa remain smaller but expanding. Brazil’s flexible-PVC manufacturers and Saudi Arabia’s ethane-based crackers support incremental demand, while South Africa’s diesel generator fleet underpins 5% annual growth in 2-EH nitrate. Regional exposure to feedstock shocks via the Strait of Hormuz continues to set a floor under global 2-ethylhexanol prices when geopolitical tensions escalate.

Competitive Landscape

The 2-Ethylhexanol Market is moderately consolidated. Competitive threats to global major players arise from Chinese newcomers offering discounted 2-EH nitrate and from regional Middle Eastern producers that combine low feedstock costs with greater logistics reach. Meanwhile, OQ Chemicals diversified into heptanoic acid at Oberhausen in 2025 to serve lubricant and aviation fuel additives, highlighting a broader trend of moving up the specialty chain to buffer cyclicality.

2-Ethyl Hexanol Industry Leaders

Eastman Chemical Company

Dow

BASF

LG Chem

OXEA GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Andhra Petrochemicals Limited (APL) halted operations at its main manufacturing plant in Visakhapatnam. APL's decision to suspend the production of oxo-alcohols, including 2-ethylhexanol, is poised to tighten supplies for the automotive sector.

- September 2025: BASF announced that in early 2024, Nan Ya Plastics Corporation (Nan Ya) installed BASF’s SYNSPIRE G1-110 catalyst at its 2-Ethylhexanol (2-EH) Mailiao site. This installation enabled Nan Ya Plastics to cut down the site's annual steam consumption by roughly 40,000 metric tons.

Global 2-Ethyl Hexanol Market Report Scope

2-ethyl hexanol is also known as octanol. It is an 8-carbon higher alcohol species that is usually soluble in organic solvents but poorly soluble in water.

The 2-ethyl hexanol market is segmented by application, end user, and geography. By application, the market is segmented into plasticizers, 2-EH acrylate, 2-EH nitrate, and other applications. By end user, the market is segmented into paint and coatings, adhesives, industrial chemicals, and other end-users. The report also covers the market size and forecasts in 19 countries across major regions. For each segment, market sizing and forecasts have been done based on value (USD).

| Plasticizers |

| 2-EH Acrylate |

| 2-EH Nitrate |

| Other Applications |

| Paint and Coatings |

| Adhesives |

| Industrial Chemicals |

| Other End-Users |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Southeast Asia | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Applications | Plasticizers | |

| 2-EH Acrylate | ||

| 2-EH Nitrate | ||

| Other Applications | ||

| By End User | Paint and Coatings | |

| Adhesives | ||

| Industrial Chemicals | ||

| Other End-Users | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Southeast Asia | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the 2-Ethylhexanol market by 2031?

The projected value of the 2-Ethylhexanol market by 2031 is USD 8.36 billion, reflecting 3.98% CAGR over 2026-2031.

Which application leads 2-ethylhexanol consumption?

Plasticizers application consumed about a 58.65% share in 2025.

Which application segment is expected to grow fastest to 2031?

2-EH Acrylate is expected to grow with the fastest CAGR of 6.31% during the forecast period (2026-2031).

Why is Asia-Pacific the largest regional consumer?

Ongoing infrastructure projects and petrochemical capacity additions in India and China keep regional demand ahead of other geographies.

How are regulations shaping product reformulation?

REACH and California AB 2300 are phasing out key phthalates, pushing converters toward non-phthalate plasticizers that still rely on 2-ethylhexanol.

Page last updated on: