Ethyleneamines Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

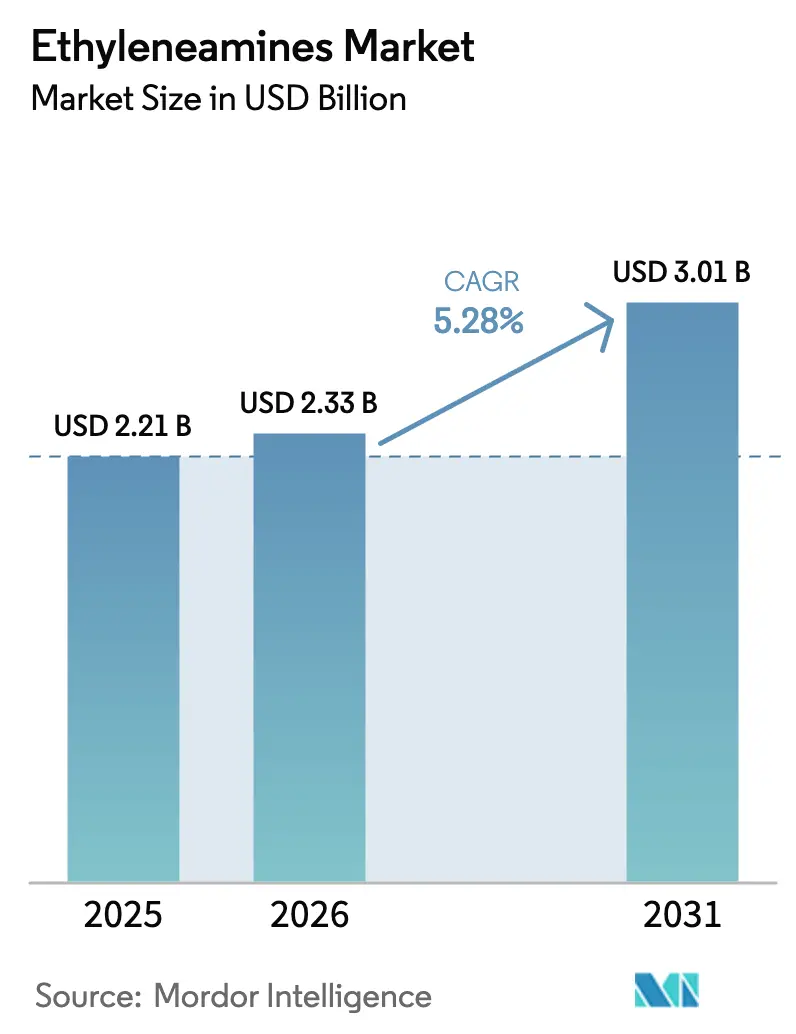

| Market Size (2026) | USD 2.33 Billion |

| Market Size (2031) | USD 3.01 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

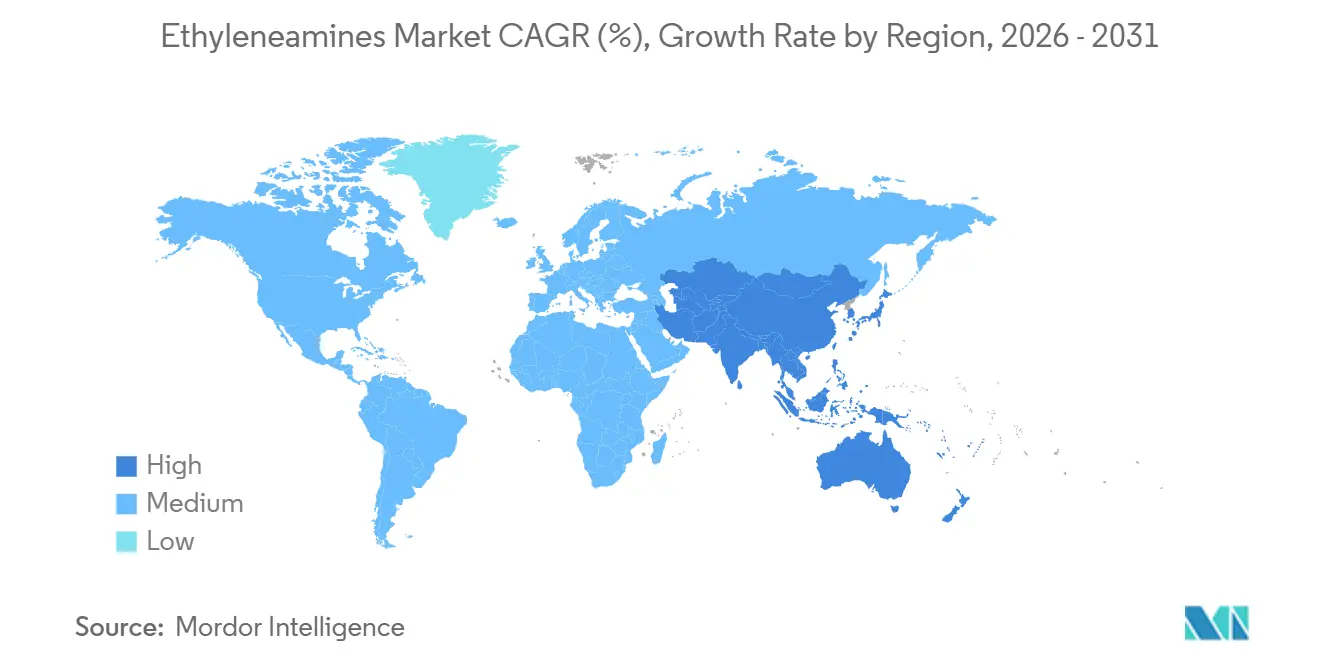

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethyleneamines Market Analysis by Mordor Intelligence

The Ethyleneamines Market size was valued at USD 2.21 billion in 2025 and is estimated to grow from USD 2.33 billion in 2026 to reach USD 3.01 billion by 2031, at a CAGR of 5.28% during the forecast period (2026-2031). Growth is anchored by epoxy-resin demand in wind-energy blades, accelerating adoption of amine-blend solvents for carbon capture, and steady pull-through from agrochemicals, surfactants, and waterborne coatings. Producers with integrated ethylene oxide and ammonia enjoy margin advantages when feedstock prices swing, while the shift toward low-carbon and biomass-balanced pathways is opening premium niches for mass-balance certified grades. Capacity rationalization in Europe contrasts with new builds in China and Saudi Arabia, reshaping regional trade flows within the ethyleneamines market. At the same time, tightening occupational-exposure limits and volatile feedstocks continue to temper short-term operating rates yet have not derailed the sector’s medium-term expansion.

Key Report Takeaways

- By type, ethylenediamine held 62.94% of the ethyleneamines market share in 2025 and is forecast to witness a 5.36% CAGR through 2031.

- By end-user industry, agrochemicals accounted for a 16.02% share of the ethyleneamines market size in 2025. Personal care is projected to post the fastest 5.48% CAGR through 2031 within the ethyleneamines market.

- By geography, Asia-Pacific commanded 53.32% of the 2025 volume and is set to increase at a 5.43% CAGR, the quickest among all regions, highlighting its pivotal role in the ethyleneamines market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ethyleneamines Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming epoxy-resin demand from wind-energy blade production | +0.9% | Global, with concentrated capacity in China, Europe, and North America | Medium term (2–4 years) |

| Rising agrochemical consumption in Asia and South America | +1.1% | Asia-Pacific (China, India), South America (Brazil, Argentina) | Short term (≤ 2 years) |

| Surfactant and detergent capacity additions in Asia-Pacific | +0.7% | Asia-Pacific core, spill-over to Middle-East and Africa | Medium term (2–4 years) |

| Shift to low-VOC coatings using polyamine curing agents | +0.6% | North America and EU, early adoption in China | Long term (≥ 4 years) |

| CO₂-capture solvent research and development using ethyleneamines blends | +0.4% | Global, pilot, and early commercial projects in North America, the EU, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming Epoxy-Resin Demand from Wind-Energy Blade Production

Multi-year epoxy supply agreements are being inked by wind-turbine manufacturers, leading to a surge in the consumption of polyamine curing agents and, consequently, boosting volumes in the ethyleneamines market. Huntsman provides ethyleneamine-based systems that cure at room temperature, ensuring the necessary fatigue resistance for blades longer than 80 meters in length[1]Huntsman Corporation, “Form 10-K 2024,” huntsman.com. In 2024, China bolstered its wind capacity significantly, with each gigawatt requiring substantial amounts of epoxy resin, thereby amplifying the demand for heavy ethyleneamines. European manufacturers of wind turbine blades are transitioning to vacuum-infusion resins, which necessitate customized DETA and TETA blends to manage gel time. With the expansion of rotor diameters, there's a need for thicker laminates to achieve a quicker through-cure, resulting in an amine-to-resin ratio that escalates at a pace outstripping the increase in turbine unit counts.

Rising Agrochemical Consumption in Asia and South America

As growers combat glyphosate resistance, Brazil and Argentina see a resurgence in herbicide formulations utilizing ethylenediamine salts. In 2024, India greenlit several new crop-protection formulations, many incorporating ethylenediamine-based adjuvants to boost foliar uptake. China, the globe's leading glyphosate producer, highlights high-value agrochemical intermediates as strategic in its 14th Five-Year Plan, bolstering local demand for ethyleneamines. With South American soybean acreage expanding significantly in 2024, herbicide application intensity surged, driving up the use of ethyleneamine derivatives. Swift regulatory approvals and bolstered domestic capacities fuel the short-term growth of the ethyleneamines market within the agrochemical sector.

Surfactant and Detergent Capacity Additions in Asia-Pacific

Between 2024 and 2025, China and India added new surfactant capacity, with a significant focus on betaine and amine-oxide lines. Ethylenediamine, a key ingredient for cocamidopropyl betaine, is increasingly sought after in sulfate-free shampoos and body washes throughout Asia. India's chemical roadmap highlights surfactants as a key priority. Meanwhile, China aims for growth in petrochemicals for 2025–2026, with a spotlight on specialty surfactants for electronics cleaning and oilfield services. As disposable incomes rise, consumers are gravitating towards premium formulations, propelling personal care to the forefront of demand growth in the ethyleneamines market.

Shift to Low-VOC Coatings Using Polyamine Curing Agents

North American and European VOC limits push coatings formulators toward waterborne or high-solids systems that rely on polyamine curing agents[2]U.S. Environmental Protection Agency, “NESHAP,” epa.gov. Evonik is expanding specialty-amine capacity in Nanjing to supply low-VOC epoxy curatives, with start-up slated for 2026. Polyaspartic coatings cure quickly and emit little odor, reducing downtime for commercial spaces. Europe’s Industrial Emissions Directive tightens allowable solvent emissions in metal and plastic finishing, accelerating demand for amine-cured systems. Coatings producers now request mass-balance certified ethyleneamines to meet Scope 3 targets, opening premium segments within the ethyleneamines market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity-driven workplace exposure limits tightening | -0.8% | Global, with stricter enforcement in North America and EU | Short term (≤ 2 years) |

| Volatile ethylene oxide and ammonia feedstock pricing | -1.2% | Global, acute in regions dependent on imported feedstocks | Short term (≤ 2 years) |

| Emerging bio-based polyamines cannibalising petro routes | -0.6% | North America and EU early adoption, spreading to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Toxicity-Driven Workplace Exposure Limits Tightening

Producers are investing in containment upgrades as occupational agencies lower exposure limits for several ethyleneamines to 1 ppm. Authorization fees from European Chemicals Agency reviews under REACH could raise production costs. Before idling its Moers plant, Huntsman incurred restructuring charges in 2025, which included spending on environmental and safety measures. While formulators are testing polyetheramines as partial substitutes, trade-offs in cure speed and durability hinder widespread replacement. With tightening enforcement, capacity additions are moving toward regions with clearer regulatory pathways, reshaping the global footprint of the ethyleneamines market.

Volatile Ethylene Oxide and Ammonia Feedstock Pricing

In 2024–2025, ethylene oxide spot prices fluctuated, influenced by outages along the Gulf Coast. Concurrently, ammonia prices surged to a peak, driven by curbs on fertilizer exports. While integrated producers like BASF and Dow manage to stabilize their operations through internal sourcing, merchant producers find themselves grappling with margin reductions. SABIC, in 2024, cited feedstock volatility as a contributing factor to its diminished petrochemical volumes. While buyers are leaning towards formula-based contracts, they still contend with lag risks. The ethyleneamines market sees a hesitance towards forward contracting, and capital-budget planning becomes a challenge, all due to the consistently broad price ranges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: EDA Dominates While Heavy Amines Target Specialty Niches

Ethylenediamine captured 62.94% of the ethyleneamines market share in 2025 and is projected to grow at a 5.36% CAGR through 2031, underpinned by its dual role in polyetheramine production and water-treatment chelation. Heavy ethyleneamines such as DETA, TETA, TEPA, and AEP supply epoxy curing, asphalt modification, and oilfield chemicals where higher amine functionality drives adhesion and film build. Bio-attributed feedstocks are gaining momentum; BASF and Evonik signed a biomass-balanced ammonia agreement in 2024, allowing ISCC PLUS certification that carries a price premium.

Piperazine, though smaller in volume, enjoys steady pharmaceutical demand as an intermediate for antihistamines and anthelmintics. Aminoethylpiperazine bridges cyclic and linear chemistries, offering fast cure in polyurea coatings and robust corrosion inhibition in pipelines. As rotor blades lengthen and low-VOC regulations tighten, formulations often specify narrow amine functionality windows, favoring suppliers with broad heavy-amine slats. These needs reinforce the dominance of integrated producers within the ethyleneamines market. Over the forecast, the ethyleneamines market size for heavy amines is expected to expand steadily, supported by composite, oilfield, and specialty-adhesive applications.

By End-User Industry: Agrochemicals Lead Share While Personal Care Accelerates

Agrochemicals held 16.02% of the ethyleneamines market size in 2025, driven by glyphosate, triazine herbicides, and micronutrient fertilizers across Brazil, India, and China. Personal care, however, is set to grow the fastest at 5.48% CAGR as sulfate-free shampoos and body washes boost demand for betaine and amine oxides derived from ethylenediamine. India’s expanding middle class and Southeast Asia’s contract manufacturing hub status spur surfactant build-outs that vertically integrate into ethyleneamines. Adhesives, paints, and resins remain significant, employing DETA, TETA, and TEPA in epoxy curatives and polyamide backbones, especially for wind-blade and flooring markets.

Automotive uses ethyleneamines in fuel additives and cooling-system inhibitors, yet electric-vehicle uptake is capping long-term growth. Oil and gas services deploy heavy amines in corrosion inhibitors and demulsifiers, with Middle Eastern producers supplying much of this demand. Pharmaceuticals and textiles consume piperazine and ethylenediamine in API synthesis and softeners, respectively, with moderate expansion tied to generics and synthetic-fiber blends. Across segments, premium pricing for biomass-balanced or low-carbon variants supports margin resilience, reinforcing the positive trajectory of the ethyleneamines market.

Geography Analysis

Asia-Pacific accounted for 53.32% of global volume in 2025 and is forecast to post a 5.43% CAGR to 2031. China is ramping up its integrated complexes, with Hengli Petrochemical spearheading a specialty-materials unit. This unit, which includes ethyleneamines, strategically pairs captive ethylene oxide with downstream derivatives, ensuring a cost edge. Meanwhile, India is making waves with a substantial capital investment in downstream chemicals, particularly emphasizing backward integration in agrochemicals and surfactants. While Japan and South Korea play pivotal roles in electronics and auto manufacturing, their growth lags behind the regional average. In Southeast Asia, rising disposable incomes are luring multinational personal-care firms, leading to localized surfactant production and a surge in ethyleneamine imports.

North America, despite its robust production capabilities, grapples with competitive pressures. Dow’s Sadara joint venture in Saudi Arabia is making global waves by shipping cost-advantaged amines, thereby nibbling away at the Gulf Coast's export share. Following the closure of its Moers facility, Huntsman has pivoted its Chocolate Bayou plant's focus towards epoxy and oilfield clientele. In a move towards sustainability, Canada’s Path2Zero ethylene complex is rolling out low-carbon ethylene oxide, positioning Alberta as a prime supply hub for environmentally-conscious buyers. Capitalizing on its proximity to Gulf-Coast feedstocks, Mexico is ramping up its surfactant lines to cater to U.S. personal-care brands.

Europe grapples with soaring energy costs and stringent REACH regulations. This has led to selective investments, such as BASF’s expansion of alkyl-ethanolamines in Antwerp and Evonik’s specialty-amine facility in Nanjing, strategically catering to European demand. In South America, the focus remains on agrochemical consumption, albeit with a heavy reliance on imports. The Middle East, bolstered by SABIC’s ethyleneamine unit and Huntsman’s Arabian Amines venture, is exporting to both Asia and Europe. They're also exploring carbon-capture projects to bolster their sustainability image. Africa, still in its infancy in this market, sees demand primarily driven by imported agrochemicals and coatings.

Competitive Landscape

The ethyleneamines market is moderately consolidated. Strategic themes center on low-carbon credentials and regional diversification. BASF and Evonik now market ISCC PLUS-certified ethyleneamines using biomass-balanced ammonia, aligning with downstream Scope 3 targets. Hengli Petrochemical’s planned complex in China could shift global supply if its integrated economics prove competitive. Technology innovation also matters; continuous reactive distillation trims production costs, giving operators of modern plants a pricing edge. In application development, Pacific Northwest National Laboratory’s work on energy-lean CO₂ solvents highlights new pull-through opportunities for tailored ethyleneamine blends.

Ethyleneamines Industry Leaders

Huntsman International LLC

Dow

BASF SE

Nouryon

Tosoh Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: BASF will convert its Geismar amines portfolio, including ethyleneamines, to 100% renewable electricity from Q4 2025, cutting 25,000 t CO₂e and lowering product carbon footprint by 4.5%.

- November 2023: BASF and SINOPEC inaugurated expanded downstream plants at BASF-YPC, Nanjing, adding purified ethylene oxide and ethyleneamines capacity.

Global Ethyleneamines Market Report Scope

Ethyleneamines are amine compounds having ethylene linkages between amine groups. These compounds are colorless, low-viscosity liquids with a fishy amine odor.

The Ethyleneamines market is segmented by type, end-user industry, and geography. By type, the market is segmented into Ethylenediamine (EDA) and Heavy Ethyleneamines (DETA, TETA, TEPA, AEP, etc.). By end-user industry, the market is segmented into Personal Care, Pulp and Paper, Adhesives, Paints, and Resins, Agro Chemicals, Automotive, Pharmaceuticals, Oil and Gas, Textiles, Metals, and Other Industries. The report also covers the market size and forecasts in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Ethylenediamine (EDA) |

| Heavy Ethyleneamines (DETA, TETA, TEPA, AEP, etc.) |

| Personal Care Industry |

| Pulp and Paper Industry |

| Adhesives, Paints, and Resins |

| Agro Chemicals Industry |

| Automotive Industry |

| Pharmaceutical Industry |

| Oil and Gas Industry |

| Textile Industry |

| Metal Industry |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Ethylenediamine (EDA) | |

| Heavy Ethyleneamines (DETA, TETA, TEPA, AEP, etc.) | ||

| By End-user Industry | Personal Care Industry | |

| Pulp and Paper Industry | ||

| Adhesives, Paints, and Resins | ||

| Agro Chemicals Industry | ||

| Automotive Industry | ||

| Pharmaceutical Industry | ||

| Oil and Gas Industry | ||

| Textile Industry | ||

| Metal Industry | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What was the global size of the ethyleneamines market in 2026, and how fast is it forecast to grow?

It reached USD 2.33 billion in 2026 and is projected to advance to USD 3.01 billion by 2031, implying a 5.28% CAGR.

Which ethyleneamine grade currently dominates demand?

Ethylenediamine leads with a 62.94% share in 2025, supported by its roles in water treatment, chelation, and polyetheramine production.

Why is Asia-Pacific expected to post the fastest growth?

China’s integrated petrochemical expansions and India’s downstream-chemicals pipeline together underpin a 5.43% CAGR to 2031 for the region.

How are wind-energy installations influencing ethyleneamine consumption?

Larger turbine blades require more epoxy resin cured with heavy ethyleneamines, directly lifting volumes for DETA and TETA.

What regulatory factors could restrain near-term production?

Stricter 1 ppm workplace exposure limits and volatile ethylene oxide plus ammonia pricing are raising compliance costs and squeezing margins.

Page last updated on: