Cyclic Olefin Copolymer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

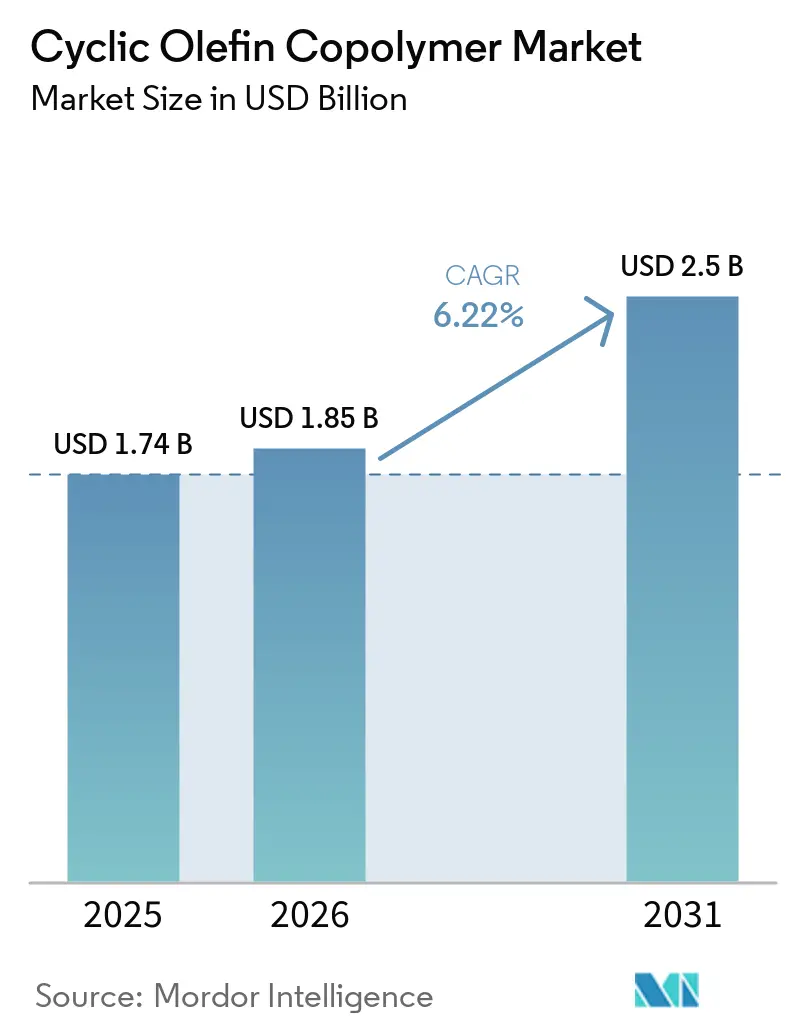

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 2.5 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cyclic Olefin Copolymer Market Analysis by Mordor Intelligence

The Cyclic Olefin Copolymer Market size is expected to increase from USD 1.74 billion in 2025 to USD 1.85 billion in 2026 and reach USD 2.5 billion by 2031, growing at a CAGR of 6.22% over 2026-2031. Demand accelerates as pharmaceutical packaging moves to monomaterial blister formats that satisfy the European Union (EU) Packaging and Packaging Waste Regulation, while semiconductor front-end logistics adopt COC carriers that comply with SEMI organic-outgassing thresholds. Asia-Pacific advances fastest as new Japanese capacity debottlenecks resin supply, whereas North American syringe conversion programs hinge on the polymer’s cryogenic impact strength. Supply remains concentrated among fewer than ten producers, yet strategic differentiation around ultra-low birefringence optics and photocurable grades tempers price-based rivalry. Near-term adoption headwinds stem from resin premiums that average 2.5-3.5 times linear low-density polyethylene and from the absence of large-scale mechanical recycling streams.

Key Report Takeaways

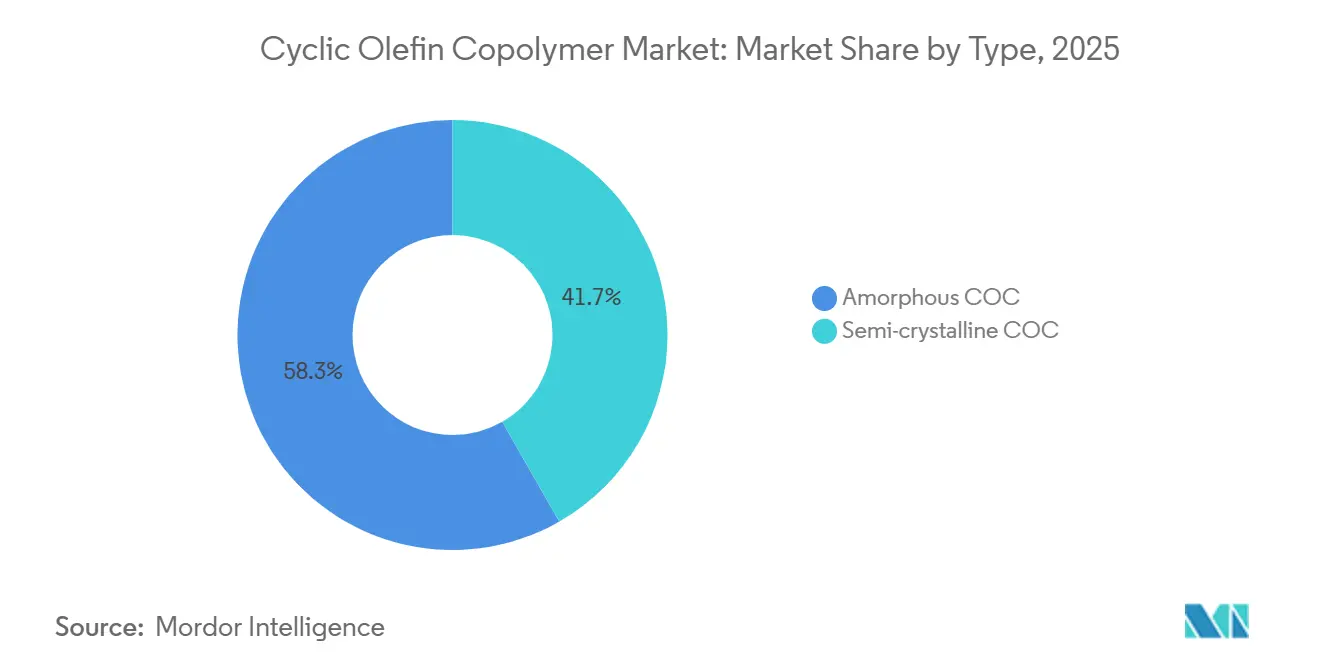

- By type, amorphous captured 58.27% revenue share of the cyclic olefin copolymer market in 2025; semi-crystalline variants are projected to grow at 6.58% CAGR through 2031.

- By grade, injection-molding grade held 41.78% of the cyclic olefin copolymer market share in 2025, while film and sheet grades are expected to post the highest projected CAGR at 6.89% to 2031.

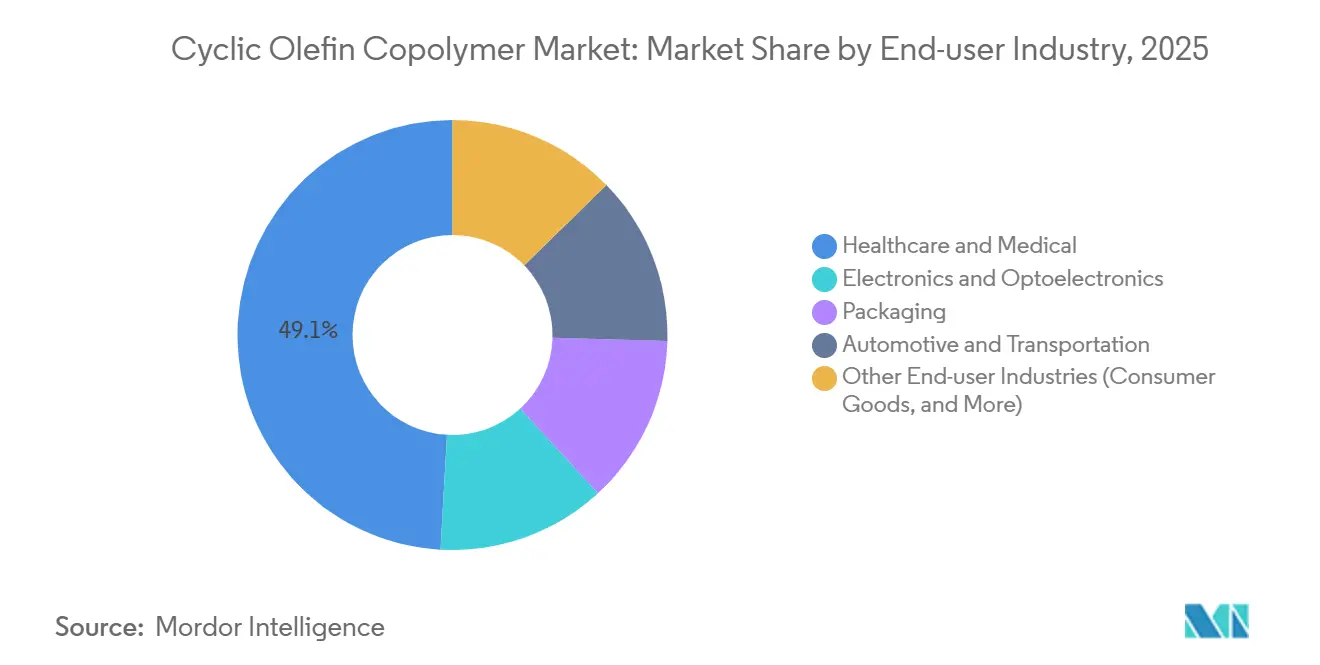

- By end-user industry, healthcare and medical accounted for 49.12% share of the cyclic olefin copolymer market size in 2025 and are expected to advance at a 7.10% CAGR through 2031.

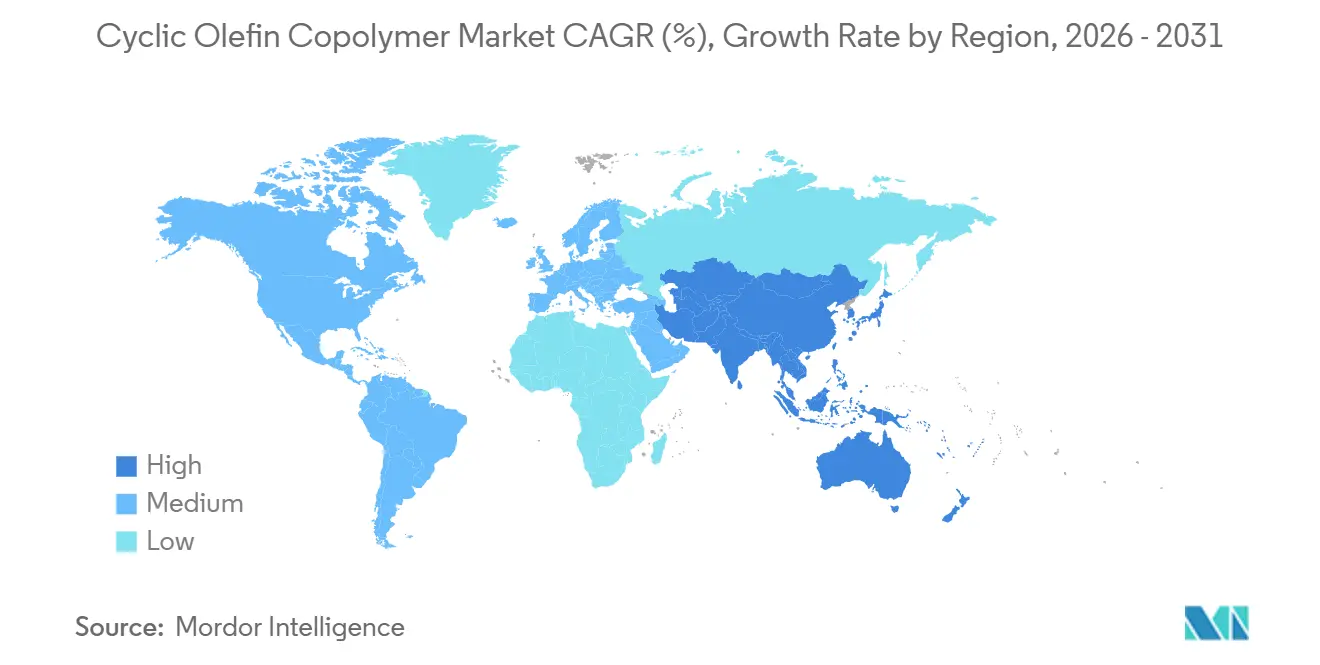

- By geography, North America led with 31.16% share in 2025; Asia-Pacific is expected to register the fastest regional CAGR at 7.02% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cyclic Olefin Copolymer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for pharmaceutical blister packs, pre-filled syringes and vials | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Adoption in microfluidics and point-of-care lab-on-chip devices | +1.2% | North America, EU, Japan | Medium term (2-4 years) |

| Growth of high-resolution display and LED optical films | +1.0% | APAC core (South Korea, Japan, China), spill-over to North America | Short term (≤ 2 years) |

| EU-PPWR push for monomaterial recyclable pharma blister based on COC | +0.9% | EU, with early adoption in Germany, France, Nordic countries | Long term (≥ 4 years) |

| COC backplane substrates enabling ultra-thin foldable micro-LED panels | +0.7% | South Korea, China, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Pharmaceutical Blister Packs, Pre-filled Syringes and Vials

Glass surfaces promote protein adsorption that degrades biologics, whereas COC’s 26 mN/m surface energy curbs binding and maintains drug potency[1]Zeon Corporation, “ZEONEX Medical Grade Data Sheet,” zeon.co.jp. ZEONEX medical-grade syringes retain impact strength at -194°C, enabling mRNA and cell-therapy distribution in ultra-cold chains. Monomaterial COC blisters reach moisture-vapor transmission rates below 0.1 g/m²/day, rivaling foil laminates and aligning with EU recyclability rules. Zeon’s vertically integrated C5 chain secures residual-unsaturation levels under 0.02 wt%, a prerequisite for FDA Drug Master File acceptance. Yet Daicel shifted its German start-up to Q1 2027 after 2026 order volumes fell 4%, exposing reliance on a few pharmaceutical accounts.

Adoption in Microfluidics and Point-of-Care Lab-on-Chip Devices

Polydimethylsiloxane absorbs hydrophobic reagents, whereas cyclic olefin copolymer market solutions show negligible small-molecule partitioning, sharpening assay accuracy[2]Royal Society of Chemistry, “Microfluidic Devices Using COC,” rsc.org. Fraunhofer trials achieved 10,000 pneumatic-valve cycles in elastomeric COC chips, extending device lifetimes versus rigid thermoplastics. COVID-19 fluorescence tests lowered autofluorescence noise to under 5% of signal when switching from polystyrene to COC substrates. Hybrid COC-PLGA microchannels are enabling wearable insulin pumps with integrated drug-delivery reservoirs. Divergent ISO 10993 test regimes between the EU and the USA create regulatory arbitrage that favors North American contract molders.

Growth of High-Resolution Display and LED Optical Films

ZEONEX 360R lowers birefringence to one-third of earlier grades, sustaining true color in foldable screens. Zeonor Film sheets transmit more than 92% of light from UV to NIR, supporting transparent 5G antenna windows with a dielectric constant near 2.4. Konica Minolta’s COC films tolerate 130°C lamination without creep, displacing triacetyl cellulose that yellows under UV. Korean research extended tensile elongation from 4% to 245% through novel copolymerization, solving brittleness in rollable OLED backplanes. APEL optics from Mitsui replicate glass-level refractive indices in smartphone lens stacks, shaving 15-20 % of thickness.

EU PPWR Push for Monomaterial Recyclable Pharma Blister Formats

The regulation obliges 65% of pharma packaging to be practically recyclable by 2030, incentivizing a switch from aluminum-PVC laminates to COC monolayers. Near-infrared sorters can distinguish COC from mainstream polyolefins, easing material recovery at scale. Germany’s 2025 VerpackG amendment lifted producer fees by 40% for non-recyclables, hastening validation trials among generics fillers. Polyplastics postponed its Leuna line to 2027 after converters questioned single-site supply resilience. Lack of ISCC PLUS mass-balance certification prevents eco-label claims that competitors achieve with circular polypropylene.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High resin cost versus polyolefin commodity plastics | -0.8% | Global | Short term (≤ 2 years) |

| Limited large-scale mechanical recycling infrastructure | -0.5% | EU, North America | Long term (≥ 4 years) |

| Supply-chain concentration with lesser global resin producers | -0.4% | Global, acute in ASEAN and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Resin Cost Versus Polyolefin Commodity Plastics

Cyclic olefin copolymer market resin sells at 2.5-3.5 times linear low-density polyethylene because norbornene synthesis and metathesis polymerization require capital-heavy C5 crackers and multi-stage hydrogenation. Generic blister applications in emerging regions stay with polypropylene that meets 1-2 g/m²/day moisture targets at half the cost. Chinese suppliers undercut Japanese benchmarks by 15-20%, but pellet-drying lapses yield hydrolysis defects that rule them out of pharma and semiconductor supply chains. Cyclopentadiene feedstock prices spiked 18% in Q1 2025 after Asian crackers shut unexpectedly, squeezing converter margins locked into fixed drug-contract pricing. Customer reticence forced Daicel to delay its German plant commissioning, highlighting how price volatility suppresses long-term offtake deals.

Limited Large-Scale Mechanical Recycling Infrastructure

Municipal sorters calibrate near-infrared scanners for PET, PE, and PP, not cyclic olefin signatures, so post-consumer blister packs still head to incineration. Borealis’ Borcycle C scheme will upscale polyolefin pyrolysis by 2029, yet no COC test runs have been disclosed. Inert-atmosphere extrusion that avoids COC yellowing costs USD 2-3 million per line, deterring small recyclers. Without ISCC PLUS approval, brand owners cannot book recycled content against Scope 3 goals, driving procurement toward circular polypropylene that earns 10-15 % price premiums. EU extended-producer-responsibility surcharges introduced in 2025 increased fees by 40%, but with no collection network, converters absorb the cost burden themselves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Amorphous Grades Lead, Crystalline Variants Gain in Heat-Loaded Optics

Amorphous COC controlled 58.27% cyclic olefin copolymer market share in 2025, owing to glass-like clarity and tight-tolerance injection molding for vials and microfluidics. These grades deliver glass-transition points of 101-154°C and modulus near 2,900 MPa, sustaining smartphone lenses where alignment tolerances stay within 5 µm. Semi-crystalline variants are pacing a 6.58% CAGR for the forecast period (2026-2031) as automotive head-up displays and ADAS (Advanced Driver Assistance Systems) cameras need higher heat-deflection ceilings above 120°C without haze growth.

Semi-crystalline resins, strengthened through novel copolymer chains, extend elongation from 4% to 245%, permitting foldable display backplanes that endure 10,000 flex cycles. ZEONEX 360R’s ultralow birefringence supports augmented-reality optics because color shift remains under 5 nm retardation. Sumitomo’s photocurable COC hybridizes thermoplastic processing with thermoset dimensional stability, responding to semiconductor lithography’s need for solvent-resistant photoresists. Tight ISO 9001 controls cap refractive-index variance at ±0.001, a threshold demanded by phone-camera OEMs.

By Grade: Injection-Molding Dominates, Film-and-Sheet Surges on Foldable Displays

Injection resin held 41.78% of the cyclic olefin copolymer market size in 2025, underpinned by high-flow ZEONEX grades clocking 16-52 g/10 min at 280°C that cut vial wall thickness below 0.5 mm and save up to 25% material. Medical variants certified to USP Class VI guarantee leachables under 0.04 µg/cm², commanding 25-30% price premiums. Film-and-sheet capacity, however, is advancing at a 6.89% CAGR through 2031 as ZeonorFilm and Konica Minolta substrates underpin micro-LED modules that specify sub-5 nm birefringence.

Coextrusion pilots merge COC clarity with polyethylene heat-seal layers to deliver blister webs that meet monomaterial recycling rules while retaining less than 0.1 g/m²/day moisture permeability. Sumitomo’s room-temperature photocurable sheets enable direct patterning on PET circuits, shaving capital outlays for thermal curing ovens. Chinese molders that skip nitrogen drying witness hydrolytic degradation during high-shear processing, dampening their bid to grab healthcare share despite 20% price discounts.

By End-user Industry: Healthcare Leads, Electronics Accelerates

Healthcare and Medical absorbed 49.12% of 2025 revenue and is set to advance at 7.10% CAGR to 2031, anchored by cryogenic-storage syringes, sterile vials, and point-of-care microplates that curb autofluorescence. USP 661.1 compliance and FDA (Food and Drug Administration) master files streamline device clearances, anchoring healthcare buyers despite resin premiums. Electronics and optoelectronics are the next growth pillar as cyclic olefin copolymer market lenses shave 15-20 % height off smartphone camera stacks and foldable screens migrate to ultralow-birefringence substrates.

Pharmaceutical blister demand widens under EU recyclability mandates, though converters delay investment until redundant European capacity arrives in 2027. Automotive optics expand as ADAS modules need 85°C continuous-use lenses with moisture uptake below 0.01%, parameters that amorphous grades deliver. Semiconductor wafer carriers depend on COC’s sub-30 ppb moisture release, though volume lags due to entrenched polycarbonate tooling.

Geography Analysis

North America accounted for 31.16% of 2025 sales. U.S. drug-delivery firms value COC syringes that survive -194°C transport without cracks. Zeon’s domestic depots shorten lead times to one week, a clear edge over ocean freight from Europe. Canadian microfluidic start-ups pivot from Polydimethylsiloxane (PDMS) to COC for low dye absorption, while Mexican lens molders adopt APEL for ADAS cameras that function at 120°C.

Asia-Pacific is the fastest-growing geography with a 7.02% CAGR to 2031. Zeon’s JPY 70 billion (USD 470 million) Tokuyama East complex will lift Japanese output 30% to 54 kilotons/year by 2028, easing resin allocations for South Korean display fabs. Korean research that multiplies tensile elongation fivefold positions regional suppliers at the forefront of rollable OLED substrates. China added 10 kilotons/year of low-cost injection resin in 2024, yet still captures a very low share of the pharmaceutical business because pellets exceed moisture specs. India explores COC blister webs for high-humidity APIs but remains price sensitive.

Europe accelerates blister-format validation following the 2025 VerpackG fee hike. Still, Polyplastics deferred its Leuna start-up to 2027 amid weak early-stage PPWR spending. Nordic insulin-vial pilots showcase COC’s less than 0.1 g/m²/day moisture rate, protecting 24-month shelf lives. South America and MEA lag because freight costs and import duties add 10-15% to already premium resin, restricting use to top-tier biologics.

Competitive Landscape

The Cyclic Olefin Copolymer market is concentrated. White-space lies in bio-attributed or chemically recycled grades. No supplier holds ISCC PLUS mass-balance accreditation, a gap that competitors in polypropylene already monetize with 10-15% premiums. Intellectual-property moats include Zeon’s outgassing-controlled wafer pods that keep organic release below 150 nanograms/gram, critical for 450 millimeter fabs. Clean compounding under ISO 9001 guards optical batch consistency demanded by phone OEMs.

Cyclic Olefin Copolymer Industry Leaders

TOPAS Advanced Polymers/Polyplastics

ZEON CORPORATION

Mitsui Chemicals, Inc.

JSR Corporation

Celanese Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Zeon Corporation initiated the construction of a new cyclo-olefin polymers production plant in Yuka Town, Shunan City, China, with plans to wrap up by the first half of fiscal 2028.

- February 2026: Daicel Corporation adjusted its investment strategy in Germany concerning its Topas-branded cyclic olefin copolymers (COC). While the new plant in Leuna, Germany, has been completed, it will not commence operations in the second quarter of 2026 as previously stated. Instead, the startup is now slated for the early months of 2027.

Global Cyclic Olefin Copolymer Market Report Scope

Cyclic Olefin Copolymer (COC) is an amorphous, transparent thermoplastic characterized by high purity, excellent optical clarity, low birefringence, and high moisture barrier properties.

The Cyclic Olefin Copolymer market is segmented by type, grade, end-user industry, and geography. By type, the market is segmented into amorphous COC and semi-crystalline COC. By grade, the market is segmented into injection-molding grade, blow-molding grade, film and sheet grade, and medical and pharmaceutical grade. By end-user industry, the market is segmented into healthcare and medical, electronics and optoelectronics, packaging, automotive and transportation, and other end-user industries (consumer goods, and more). The report also covers the market size and forecasts for cyclic olefin copolymer in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Amorphous COC |

| Semi-crystalline COC |

| Injection-Molding Grade |

| Blow-Molding Grade |

| Film and Sheet Grade |

| Medical and Pharmaceutical Grade |

| Healthcare and Medical |

| Electronics and Optoelectronics |

| Packaging |

| Automotive and Transportation |

| Other End-user Industries (Consumer Goods, and More) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Amorphous COC | |

| Semi-crystalline COC | ||

| By Grade | Injection-Molding Grade | |

| Blow-Molding Grade | ||

| Film and Sheet Grade | ||

| Medical and Pharmaceutical Grade | ||

| By End-user Industry | Healthcare and Medical | |

| Electronics and Optoelectronics | ||

| Packaging | ||

| Automotive and Transportation | ||

| Other End-user Industries (Consumer Goods, and More) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast will global demand for cyclic olefin copolymer grow through 2031?

The Cyclic Olefin Copolymer Market size is expected to increase from USD 1.74 billion in 2025 to USD 1.85 billion in 2026 and reach USD 2.5 billion by 2031, growing at a CAGR of 6.22% over 2026-2031.

Which region shows the highest growth trajectory?

Asia-Pacific leads with a projected 7.02% CAGR for the forecast period (2026-2031) because new Japanese capacity shortens lead times for Korean and Chinese display fabs.

Why are pharmaceutical companies shifting from glass to COC syringes?

COC avoids protein adsorption, withstands -194°C cryogenic storage, and meets FDA leachables limits below 0.04 µg/cm².

What limits broader adoption of COC in commodity packaging?

Resin costs average 2.5-3.5 times polyethylene and large-scale recycling systems are not yet in place.

Page last updated on: