Enterprise Metadata Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

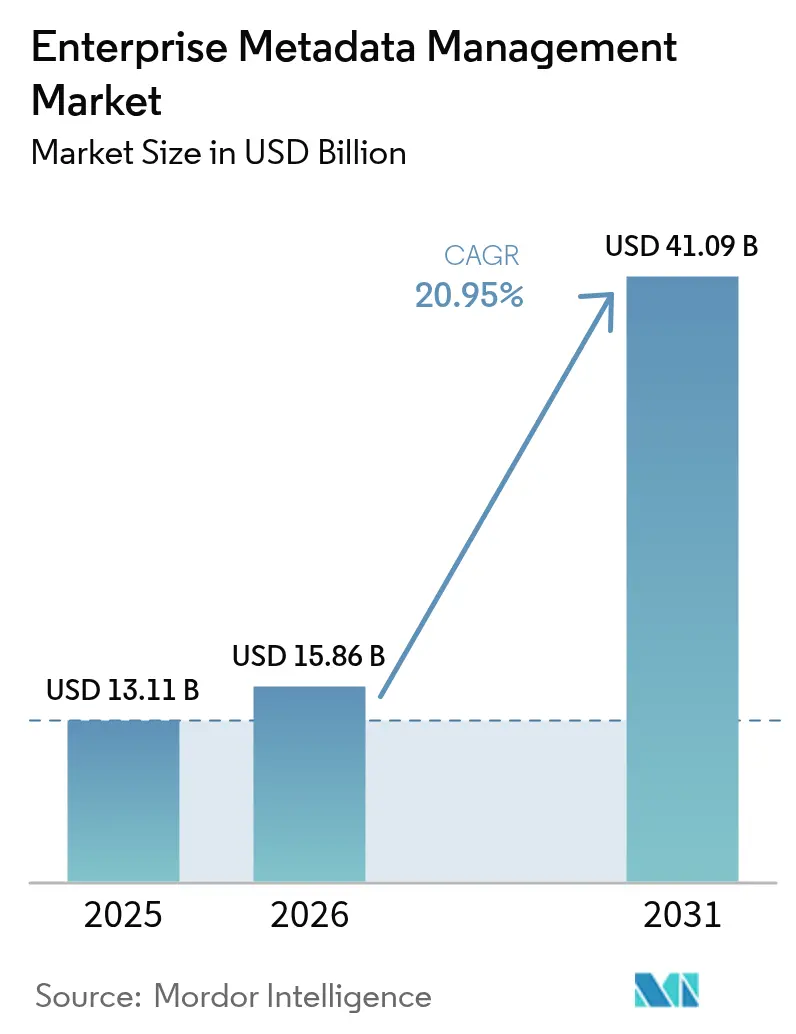

| Market Size (2026) | USD 15.86 Billion |

| Market Size (2031) | USD 41.09 Billion |

| Growth Rate (2026 - 2031) | 20.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Metadata Management Market Analysis by Mordor Intelligence

Enterprise Metadata Management market size in 2026 is estimated at USD 15.86 billion, growing from 2025 value of USD 13.11 billion with 2031 projections showing USD 41.09 billion, growing at 20.95% CAGR over 2026-2031. Strong investment momentum stems from converging regulatory mandates, intensified cloud and hybrid migrations, and AI-driven demand for unified, actionable data. North America remains the largest regional contributor, supported by mature governance frameworks and high cloud uptake, while Asia-Pacific is on a steeper trajectory as new privacy statutes and rapid digitalization expand the addressable base. Solution licenses still deliver the bulk of revenue, yet service engagement is accelerating as enterprises seek integration and change-management expertise to scale metadata programs. Competitive activity is heating up: leading vendors continue to embed AI agents for automated lineage, and newer entrants focus on decentralized architectures that keep pace with data-mesh adoption.

Key Report Takeaways

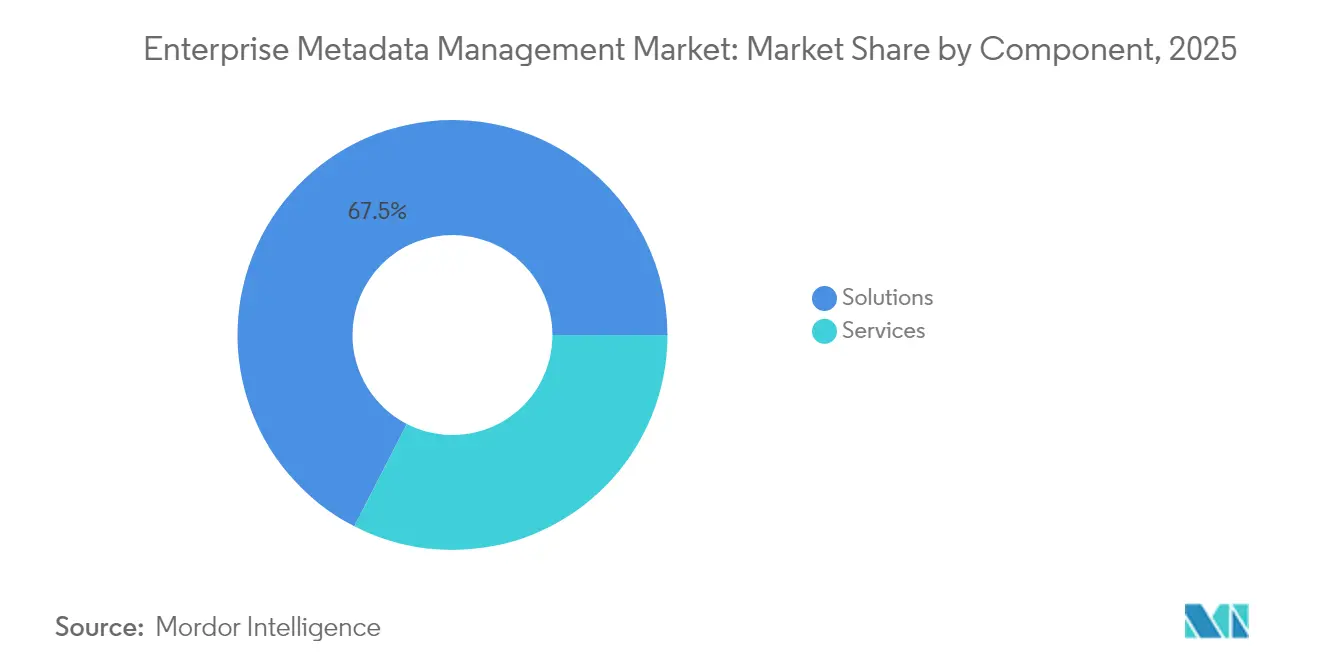

- By component, solutions captured 67.45% of revenue in 2025, while services are on course for a 23.52% CAGR through 2031.

- By deployment mode, cloud deployments held 58.10% of the enterprise metadata management market share in 2025; hybrid models are projected to grow at a 22.55% CAGR to 2031.

- By metadata type, business metadata led with a 50.65% share in 2025, whereas operational/process metadata is forecast to post a 23.05% CAGR through 2031.

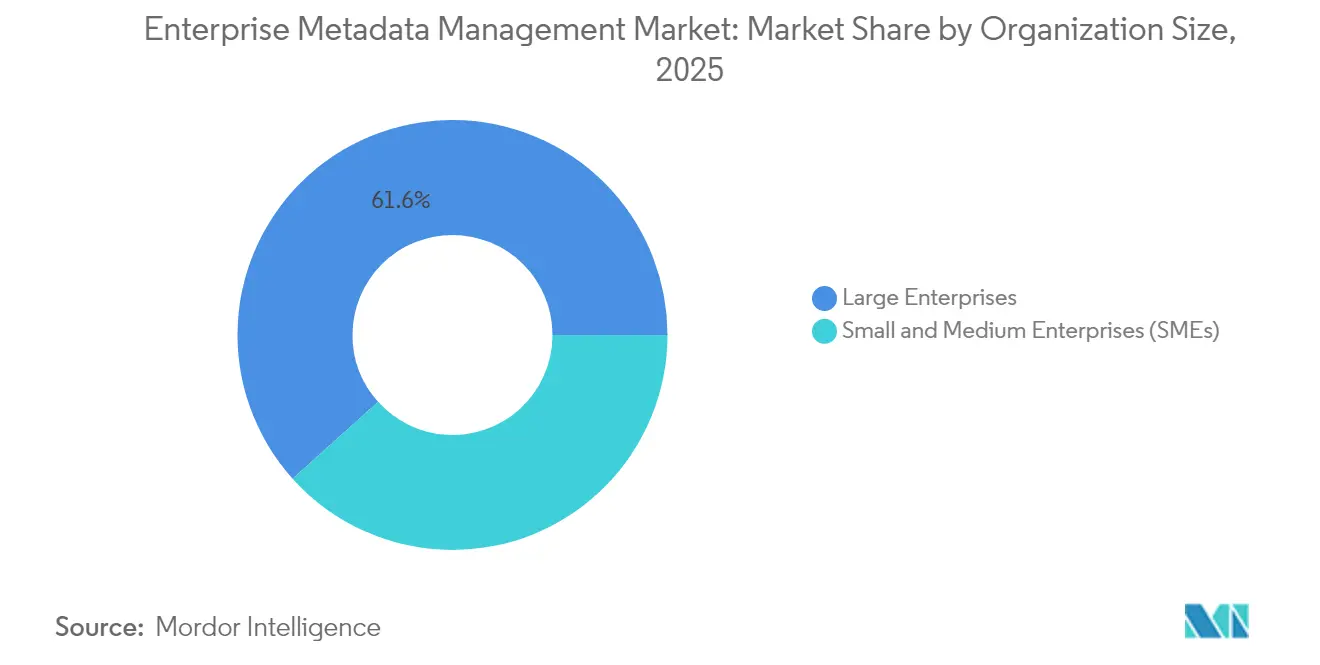

- By organization size, large enterprises accounted for 61.65% of the enterprise metadata management market size in 2025, yet SMEs are expected to advance at a 24.10% CAGR by 2031.

- By end-user industry, IT and telecom contributed 25.10% of revenue in 2025; retail and e-commerce are anticipated to expand at a 22.70% CAGR to 2031.

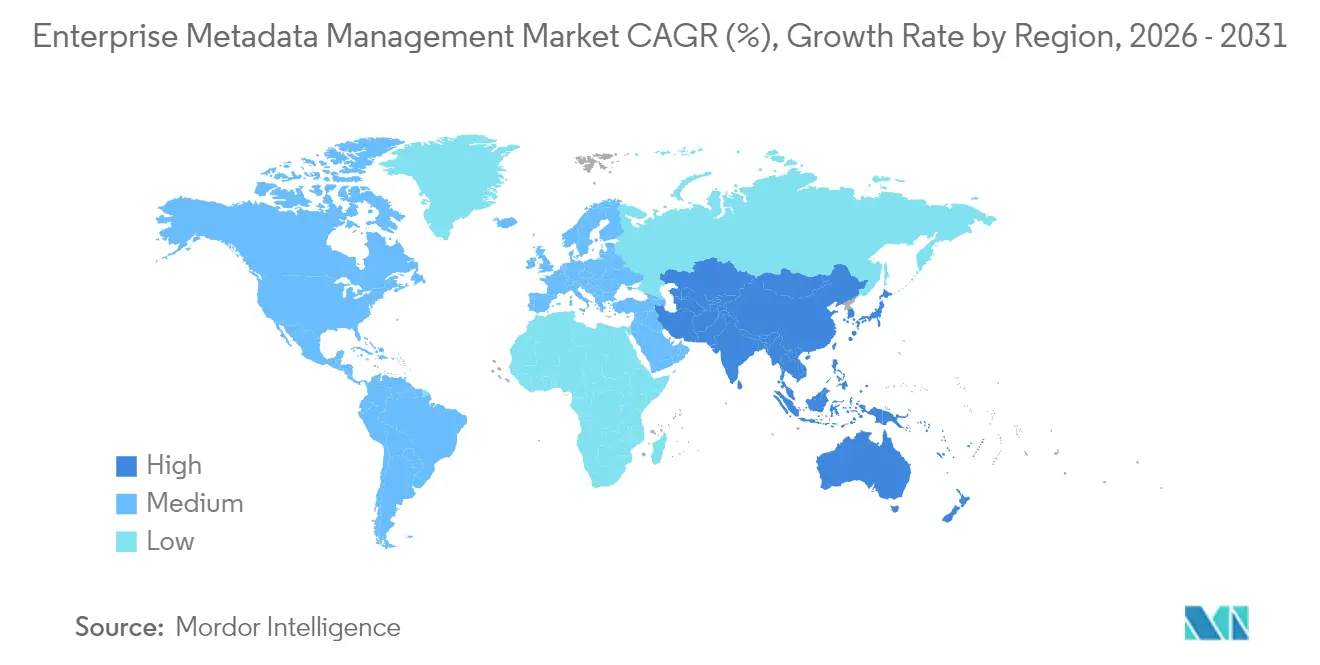

- By geography, North America led with 35.72% enterprise metadata management market share in 2025, while Asia-Pacific is set to record a 24.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Metadata Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of enterprise data volumes | +3.5% | Global | Medium term (2-4 years) |

| Regulatory compliance and data-governance mandates | +2.8% | North America, EU, APAC core | Short term (≤ 2 years) |

| Cloud and hybrid migration requires unified metadata | +2.6% | Global, APAC, Europe | Medium term (2-4 years) |

| Self-service analytics adoption spurs data-catalog demand | +2.1% | North America, Europe, APAC | Medium term (2-4 years) |

| Generative-AI-driven auto-classification unlocks ROI | +1.7% | Global | Long term (≥ 4 years) |

| Data-mesh architectures need federated metadata services | +1.2% | Europe, North America, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of enterprise data volumes

IoT rollouts, 5G connectivity, and omnichannel commerce are swelling corporate data troves, pushing metadata management to board agendas. AT&T used Snowflake to consolidate metadata across legacy and cloud assets, accelerating analytics while cutting infrastructure costs. [1]Snowflake, “AT&T Provides Faster Insights at Lower Costs with Snowflake,” snowflake.com Similar initiatives are multiplying in telecom and e-commerce, where high-velocity data flows demand automated lineage and cataloging to sustain agility and compliance.

Regulatory compliance and data-governance mandates

Fresh regulations are tightening oversight. Malaysia now obliges firms with more than 20,000 data subjects to nominate Data Protection Officers and notify breaches, a step that is enlarging the enterprise metadata management market. [2]ASEAN Briefing, “Malaysia Tightens Data Protection from June 2025,” aseanbriefing.com India’s Digital Personal Data Protection Act and China’s Interim AI Measures act likewise raise expectations for granular lineage and consent tracking. Singapore’s banking regulator mandates AI model risk governance, reinforcing the need for transparent metadata.

Cloud and hybrid migration requires unified metadata

Organizations migrate analytic workloads to hyperscale clouds yet keep sensitive datasets on-premises. TELUS migrated to Google Cloud, retiring obsolete data and optimizing 200+ pipelines, demonstrating the integration complexity enterprises face. Hybrid patterns prevail in regulated sectors that must balance residency rules with cloud scalability, pushing demand for federated metadata services.

Self-service analytics adoption spurs data-catalog demand

Line-of-business analysts now expect intuitive catalogs that supply context and trust signals. NTT DOCOMO adopted Alation to democratize data discovery, equipping non-technical users with governed access. In retail, a new patent for hyper-localized assortment optimization shows how rich metadata feeds agile merchandising models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation cost and integration complexity | -2.5% | Global, especially SMEs | Short term (≤ 2 years) |

| ROI uncertainty and skills shortage | -2.1% | Global | Medium term (2-4 years) |

| Multi-cloud metadata silos limit lineage completeness | -1.6% | Multinational, regulated sectors | Medium term (2-4 years) |

| Data-sovereignty limits cross-border metadata hosting | -1.2% | APAC, Europe, MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High implementation cost and integration complexity

Legacy sprawl inflates deployment timelines and budgets. Citigroup’s fragmented data stack incurred USD 1.5 billion in fines, illustrating the risk of retrofitting modern metadata onto heritage systems. SMEs, with leaner resources, hesitate to invest without near-term returns, dampening uptake.

ROI uncertainty and skills shortage

Quantifying value is difficult when benefits span risk, efficiency, and decision quality. Scarce data stewards and engineers further slow progress. Firms counter by choosing SaaS catalogs that bootstrap automation; telecom operators used UltiHash tools to trim storage costs while improving observability. [3]UltiHash, “Intelligent Network Management in Telecoms,” ultihash.io

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace as Integration Complexity Rises

Solutions produced 67.45% of revenue in 2025. The enterprise metadata management market expects services to grow at a 23.52% CAGR to 2031 as firms need consulting for hybrid integration, AI enablement, and regulatory readiness. Deutsche Telekom partnered with Capgemini for a TMForum-aligned model that shortened product-launch cycles, highlighting service value.

Enterprises also outsource managed metadata operations to navigate ever-changing privacy laws and cloud tooling, fueling annuity revenues for system integrators and MSPs. As cloud estates scale, outcome-based service contracts expand, reinforcing a healthy pipeline for advisory, implementation, and support.

By Deployment Mode: Hybrid Models Bridge Compliance and Agility

Cloud remains the default, holding 58.10% market share in 2025. However, hybrid configurations are projected to post a 22.55% CAGR because regulated entities must localize sensitive data while exploiting cloud analytics. Malaysia’s new privacy guidelines and Singapore’s sovereign cloud framework intensify this pattern.

Hybrid tooling unites on-prem and cloud catalogs into a single control plane. TELUS proved the model by maintaining critical data hubs on-site while orchestrating analytics in Google Cloud, safeguarding residency obligations without impeding AI development.

By Metadata Type: Operational Metadata Powers Supply-Chain Resilience

Business metadata occupies 50.65% of 2025 spend, yet operational/process metadata is forecast to climb at 23.05% CAGR. Manufacturers apply operational lineage to assure provenance and adapt supply networks to shocks. Alpha, a German firm, used a data mesh to gain real-time visibility, improving agility and performance.

Financial regulators also demand auditable process metadata that traces data movement across multi-cloud estates. The enterprise metadata management market size for operational/process metadata is set to expand from its current base as digital twin initiatives multiply in discrete and process industries.

By Organization Size: SMEs Leverage SaaS for Governance Parity

Large enterprises delivered 61.65% of revenue in 2025, but SMEs will advance faster at 24.10% CAGR. Lightweight SaaS catalogs such as Atlan or OpenMetadata allow smaller firms to embed governance without heavy capital outlays.

Regional SMEs in Asia-Pacific adopt these offerings to satisfy emerging privacy statutes and compete with larger incumbents on data quality. The enterprise metadata management market share held by SMEs is likely to widen as subscription pricing and no-code integrations lower entry barriers.

By End-user Industry: Telecom and Retail Lead Adoption, E-commerce Surges

IT and Telecom captured 25.10% of the 2025 demand, propelled by network optimization and stringent compliance. AT&T and Deutsche Telekom rely on rich metadata to fast-track product innovation and manage spectrum assets. Retail and e-commerce are the quickest movers, tracking a 22.70% CAGR as omnichannel merchants need metadata for hyper-localized assortment and dynamic pricing.

A patent granted in 2024 shows how retailers exploit metadata to calibrate store-level variety, lifting sales and satisfaction. Fraud detection and personalized promotions further stimulate adoption across digital commerce ecosystems.

Geography Analysis

North America commands 35.72% of revenue, underpinned by the CCPA, sector-specific mandates, and a deep ecosystem of vendors and integrators. Enterprises capitalize on mature cloud infrastructure and robust venture funding, driving early experiments with AI-guided stewardship. Patent activity from Snowflake and Palantir reinforces the region’s innovation edge.

Asia-Pacific is the fastest-growing theater, rising at 24.05% CAGR. Malaysia’s mandatory DPO policy, India’s DPDPA, and China’s AI rules oblige enterprises to implement granular lineage, swelling demand. Telecommunications, retail, and manufacturing players in Indonesia and Vietnam adopt catalogs to meet new fintech and personal-data laws. The enterprise metadata management market size in Asia-Pacific is projected to more than triple by 2031.

Europe retains momentum through GDPR enforcement and the forthcoming AI Act, which emphasizes consent management and cross-border processing safeguards. Manufacturers embrace data mesh to coordinate multi-plant supply chains, while financial institutions strengthen lineage to satisfy supervisory reviews.

Smaller Latin American, Middle Eastern, and African markets are nascent but observe global precedents, gradually instituting metadata programs to shore up resilience.

Regulatory Landscape

Enterprise metadata management is increasingly shaped by regulator-driven requirements for traceable, standardized, and machine-readable data inventories. In the United States, a final joint rule published June 25, 2026 under the Financial Data Transparency Act of 2022 advances interoperability-focused data standards for regulatory reporting, reinforcing demand for consistent definitions, lineage, and governance metadata across institutions. The United Kingdom's Cabinet Office also issued a Data Asset Management Policy in May 2026 that requires government departments to identify, record, and maintain metadata in central data catalogues, formalizing catalog-centric operating practices that mirror enterprise deployments.

In Europe, the EU Artificial Intelligence Act (Regulation (EU) 2024/1689) intensifies metadata-driven governance for high-risk AI through data governance and documentation obligations, with full application noted for August 2, 2026 in the evidence pack. Standards activity also reinforces common approaches to metadata registries and exchange, including ISO/IEC 11179-34:2024 for computable data and ISO/IEC TR 19583 parts published in 2025 for metadata registry data models and mappings, supporting cross-platform metadata portability and auditability.

Value Chain Analysis

The enterprise metadata management value chain runs from data producers (business applications, data platforms, and operational systems) through metadata capture and harvesting (connectors into cloud data warehouses, lakes, ETL/ELT, BI, and ML toolchains), to core governance and catalog platforms (active metadata, lineage, policy, and semantic layers). Downstream consumers include analytics teams, data stewards, risk and compliance functions, and AI engineering. System integrators and managed service providers are central in implementation, change management, and operating-model design as enterprises connect hybrid estates and reconcile legacy definitions into governed glossaries.

Industry-specific supply chains show where value concentrates when metadata affects monetization and control. In media and entertainment, fragmented workflows and manual metadata handling can create release delays and revenue leakage; vendors and service providers respond by consolidating rights, avails, and title metadata into unified sources of truth (for example, Vubiquity updates to MetaVU and AssetVU during 2025), and by adding AI-driven readiness tooling (such as Vubiquity's Catalog Intelligence becoming commercially available in July 2025). Across sectors, standards such as Dublin Core and MPEG-7, along with media-specific identifiers and formats (including EIDR, SMPTE, DDEX, and IMF), coexist with enterprise governance frameworks, making interoperability, connector breadth, and policy enforcement key differentiators across the chain.

Competitive Landscape

Incumbent vendors—Informatica, Collibra, Alation, IBM—consolidate their lead by integrating agentic AI, active governance, and cloud-native deployment options. Informatica launched CLAIRE Agents that automate data-quality fixes and push lineage insights into service-management tools. Collibra pilots a unified governance layer that spans structured data and ML models.

Patent filings from Snowflake and Palantir reveal multi-level metadata storage and decentralized protection for multi-cloud footprints, signaling ongoing differentiation in scale and security. Disruptors such as Zeenea, Select Star, Atlan, and OpenMetadata pursue open, composable stacks that dovetail with data-mesh principles. HCLSoftware’s planned acquisition of Zeenea underlines the strategic value of nimble discovery engines.

Partnerships flourish as system integrators package metadata solutions with broader modernization programs. Capgemini’s work with Deutsche Telekom highlights co-innovation to accelerate B2B launches. Futurum Group spotlights agentic AI as a catalyst that reduces stewardship overhead and democratizes governance. [4]Futurum Group, “The Rise of Agentic AI,” futurumgroup.com White-space remains in harmonizing cross-cloud lineage, enforcing active policy, and supporting the next wave of APAC and European regulations.

Enterprise Metadata Management Industry Leaders

Informatica LLC

Collibra NV

Alation Inc.

IBM Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulated data spaces and AI governance programs create concrete whitespace for metadata platforms that can enforce standardized, machine-readable context across organizations and clouds. A cited example is the European Health Data Space, where an April 2026 draft implementing regulation referenced in the evidence pack specifies mandatory metadata elements for secondary use of health data and establishes HealthDCAT-AP as a mandatory metadata framework. This increases requirements for catalog completeness, controlled vocabularies, and lineage in healthcare and life sciences. Regulatory pull also comes through AI-focused controls, with the EU Artificial Intelligence Act (Regulation (EU) 2024/1689) elevating the operational need for documented provenance and data governance for high-risk AI systems.

Technology opportunities also center on operationalizing active metadata for AI agents and self-service analytics, particularly in hybrid and multi-cloud estates where lineage completeness and policy consistency remain difficult. Vendor roadmaps point to bi-directional synchronization between governance platforms and cloud-native catalogs (for example, integrations spanning Snowflake, Google Cloud, AWS, and Databricks) and to automated tag extraction and classification to reduce stewardship workload. Buyers are also showing demand for outcome-oriented services, evidenced in telecom modernization and large-scale migrations, including TELUS optimizing 200+ pipelines during its Google Cloud migration, which expands the addressable scope for integration accelerators, governance operating models, and managed metadata operations.

Recent Industry Developments

- June 2026: Collibra expanded its integration with Snowflake, focusing on bi-directional synchronization of governance context such as metadata, tags, and policies across the Snowflake AI Data Cloud. The update targets faster alignment between governance controls and cloud-native data consumption, reducing gaps between centralized catalogs and in-platform AI and analytics workflows.

- May 2026: Informatica introduced Headless Data Management capabilities and expanded Databricks-aligned governance features, including support for extracting governance tags from Databricks Unity Catalog. These updates strengthen interoperability between enterprise governance layers and modern lakehouse platforms, helping organizations operationalize trusted context for AI agents across hybrid environments.

- March 2025: HCLSoftware announced its intent to acquire Zeenea, adding a specialist data catalog and discovery capability to broaden its governance coverage for regulated industries. The planned deal points to continued consolidation as enterprise buyers prefer integrated metadata, catalog, and governance stacks rather than point solutions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the enterprise metadata management market counts the revenues earned from tools and related services that help enterprises capture, organize, govern, and share metadata (technical, business, and operational) across on-premises, cloud, and hybrid data environments.

Scope exclusions: We exclude open-source utilities with no paid license, one-off consulting-only projects, and data catalog modules that are bundled but do not provide a stand-alone metadata management layer.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Metadata Type

- Technical Metadata

- Business Metadata

- Operational/Process Metadata

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Retail and E-commerce

- IT and Telecom

- Government and Public Sector

- Manufacturing

- Media and Entertainment

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the initial market boundaries, terminology, and demand signals before any calculations were finalized. Public sources such as the US Bureau of Labor Statistics, US Census Bureau economic datasets, the OECD digital economy indicators, the National Institute of Standards and Technology (NIST) guidance, and ISO and IEC standards documents helped align on which metadata management capabilities are typically counted in enterprise settings.

We then reviewed annual reports, 10-K filings, investor presentations, product documentation, and credible press coverage to understand how vendors describe revenue streams and packaging. When needed, paid subscriptions focused on company financials and intelligence, news and financials, and patent databases were used to validate timelines, acquisitions, and product scope shifts that can affect revenue mapping. These examples are not exhaustive, and other public sources were also used to support data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test assumptions that desk research cannot fully confirm, especially packaging, pricing logic, and adoption pace across industries. We spoke with solution leaders, service providers, system integrators, and enterprise buyers across APAC, EMEA, and the Americas, then used their feedback to refine scope boundaries and normalize regional demand patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | APAC: 46% |

| Mid tier: 55% | Functional/Unit leaders: 39% | EMEA: 34% |

| Smaller Players: 19% | Managers: 46% | Americas: 20% |

Market-Sizing & Forecasting

The core sizing starts with a top-down build where enterprise software and data management spending pools are reconstructed by region, then filtered using metadata management adoption and spend-share indicators. To keep the numbers realistic, we corroborate outputs with selective bottom-up approximations, including sampled vendor revenue mapping, partner channel checks, and a price-times-volume sanity check for common subscription bundles.

Key inputs used in the model include cloud and hybrid data platform adoption, growth in governed data assets and data domains per enterprise, regulatory pressure for lineage and auditability, average subscription pricing progression for metadata capabilities, implementation and support attachment rates, and the share of projects moving from pilot to enterprise rollout. Where direct bottom-up roll-ups are incomplete, we handle gaps through peer group benchmarking by region and by enterprise size, then adjust using interview feedback.

For forecasting, scenario analysis is used to reflect different adoption speeds of governed data programs, followed by a multivariate regression that connects spending outcomes with a small set of demand indicators. Assumptions are reviewed with practitioners so the forward view aligns with what is budgeted and deployed, not only what is technically possible.

Data Validation & Update Cycle

Validation is done through step-by-step checks so the market totals stay consistent with real-world signals. We compare results against independent indicators like enterprise software spending direction, cloud migration pace, and the observed mix of subscription versus services revenues, and then investigate any sharp regional spikes or unusual year-over-year shifts.

Before sign-off, the model is reviewed by another analyst who rechecks key assumptions, unit logic, and currency conversions, then a final consistency pass is completed to ensure the story matches the numbers. Reports are refreshed annually, and interim updates are triggered when major events occur, such as a large acquisition, a major product packaging change, or a macro shift that alters IT spending behavior. Right before delivery, we do a fresh review so clients receive the latest updated view.

Mordor Intelligence's Enterprise Metadata Management Market Sizing Compared With Other Published Estimates

It is common to see different market sizes for enterprise metadata management because publishers do not always count the same revenue streams, and they also pick different base years and forecast windows. The spread usually comes from scope boundaries, how services are treated, and how pricing and adoption are carried forward year by year.

By checking revenue inclusion rules and refresh cadence, Mordor Intelligence separates stand-alone enterprise metadata management subscriptions and recurring support from adjacent modules and consulting-only activity, which can move totals up or down depending on how broadly the market is defined.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.11 B (2025) | |

| Global Market Publisher A | USD 10.65 B (2025) | This estimate applies a broader value definition that blends goods and services but can undercount software-first subscriptions when revenue is reported inside wider data management lines, and it may use different regional weighting for early adoption markets. |

| Industry Research House B | USD 3.50 B (2025) | This estimate appears to use a narrower software-only boundary and may exclude recurring support and certain enterprise-grade deployment patterns, which reduces the addressable revenue pool even when adoption is rising. |

The benchmark differences mainly come from what is counted as in-scope revenue and how consistently that scope is applied across regions and years. When the scope is documented clearly and cross-checked with adoption, pricing, and support attachment logic, the final number becomes easier to trace and repeat for planning use cases.

Key Questions Answered in the Report

What is the current value of the enterprise metadata management market?

The enterprise metadata management market size stands at USD 15.86 billion in 2026 and is forecast to climb to USD 41.09 billion by 2031, registering a 20.95% CAGR.

Which region is growing fastest?

Asia-Pacific leads growth with a 24.05% CAGR, propelled by new privacy laws in Malaysia, India, and China plus rapid digital transformation across telecom, retail, and manufacturing.

What segment will expand most quickly?

Services are projected to advance at a 23.52% CAGR as enterprises seek consulting, integration, and managed operations to scale metadata programs.

Why are hybrid deployments gaining momentum?

Hybrid architectures help regulated organizations satisfy data-residency rules while accessing cloud analytics, making hybrid the fastest deployment mode at a 22.55% CAGR.

How are vendors differentiating in this market?

Incumbents integrate agentic AI for automated lineage, while disruptors offer open, composable stacks optimized for data mesh and decentralized governance.

What is the chief barrier to adoption?

High integration cost and skills shortages deter many firms, especially SMEs, though SaaS platforms and automation are beginning to lower entry hurdles.

Page last updated on: