Data Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

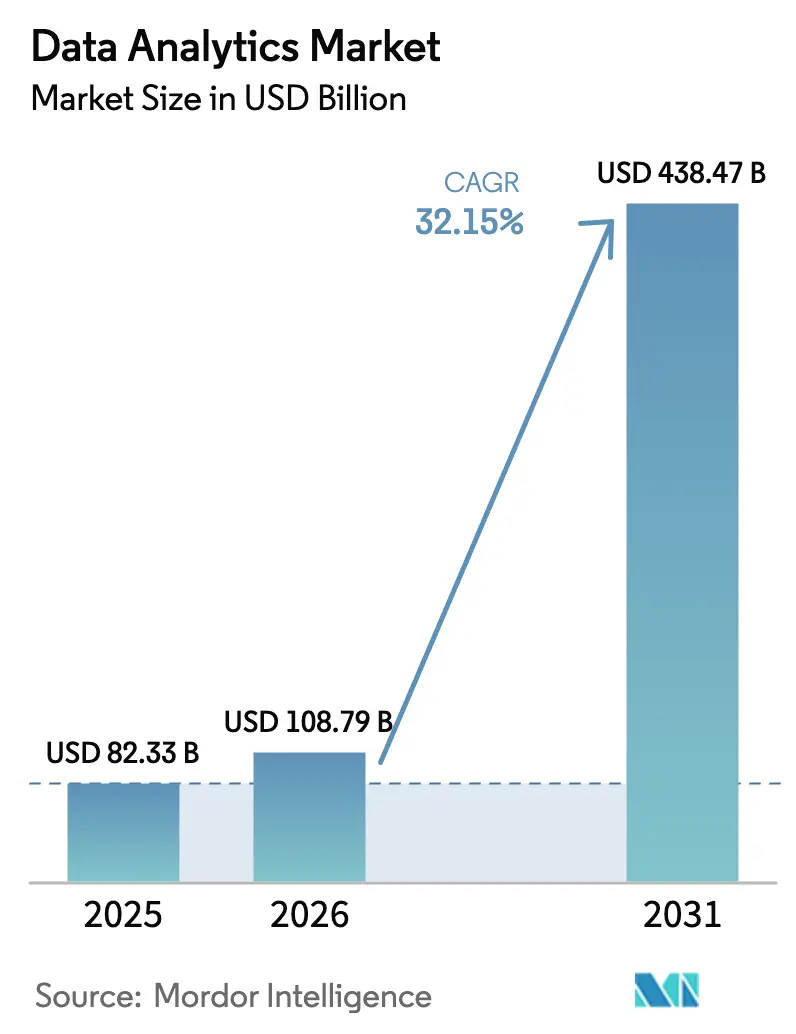

| Market Size (2026) | USD 108.79 Billion |

| Market Size (2031) | USD 438.47 Billion |

| Growth Rate (2026 - 2031) | 32.15% CAGR |

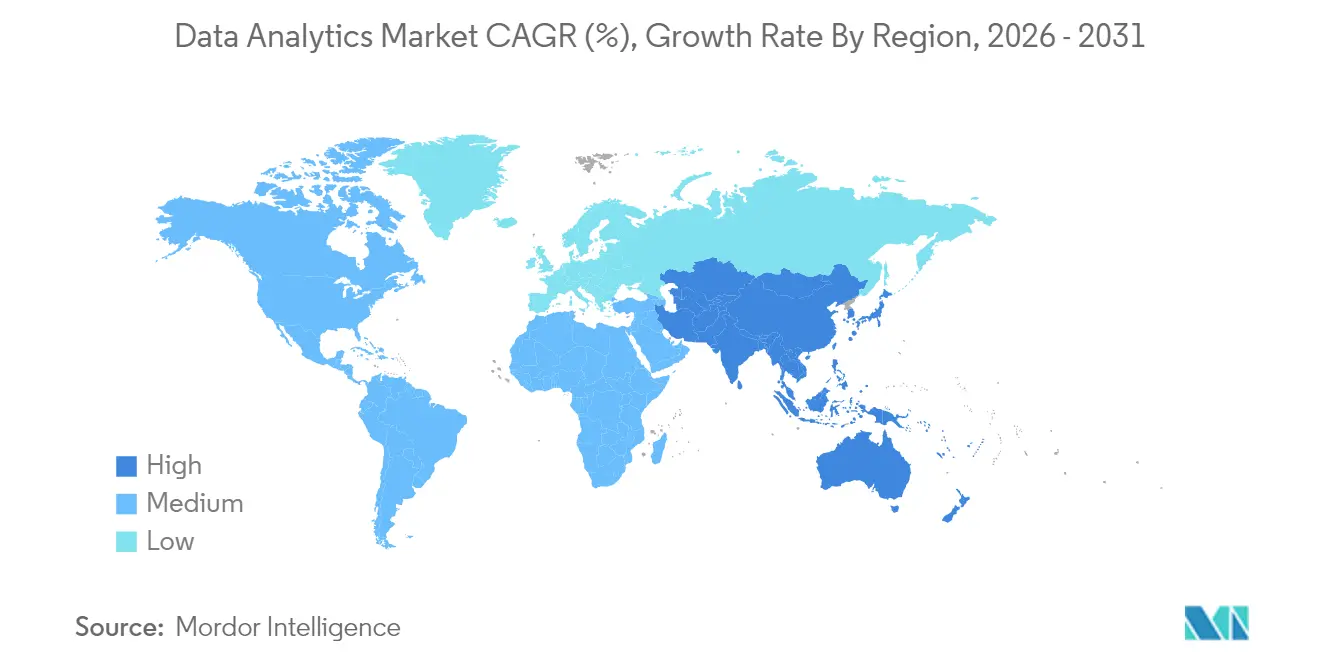

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Analytics Market Analysis by Mordor Intelligence

The data analytics market size in 2026 is estimated at USD 108.79 billion, growing from 2025 value of USD 82.33 billion with 2031 projections showing USD 438.47 billion, growing at 32.15% CAGR over 2026-2031. Cloud-native architectures, AI-driven automation, and surging enterprise data volumes are accelerating adoption across every major vertical. In 2025, 77% of organizations list analytics as the principal lever for operational efficiency, underscoring its shift from support function to strategic core[1]Ataccama, “Data Quality Trends Shaping 2025,” ataccama.com. Heightened regulatory transparency demands, rising cyber-threat complexity, and the need for real-time decision support further amplify solution uptake. Competitive intensity is increasing as platform vendors layer natural-language and agentic AI features on established offerings to boost user productivity and reduce skills-gap friction.

Key Report Takeaways

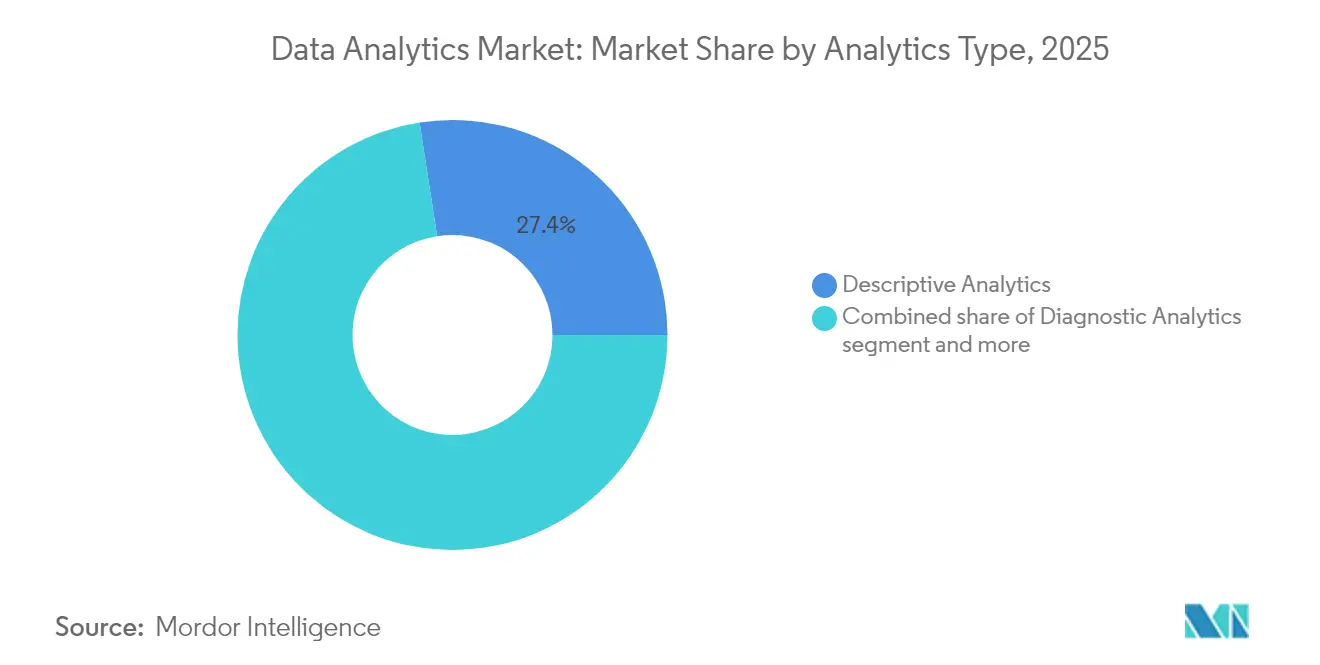

- By analytics type, Descriptive Analytics led with 27.45% of data analytics market share in 2025, while Prescriptive Analytics is set to record a 32.72% CAGR to 2031.

- By solution, Data Management accounted for 24.60% of the data analytics market in 2025; Security Intelligence is projected to advance at a 33.45% CAGR through 2031.

- By application, Customer Relationship Management held a 17.65% share of the data analytics market in 2025, whereas Risk and Fraud Management will grow at a 33.60% CAGR to 2031.

- By deployment model, On-Premises platforms retained 64.25% of the 2025 data analytics market, but Cloud solutions are growing at a 33.05% CAGR.

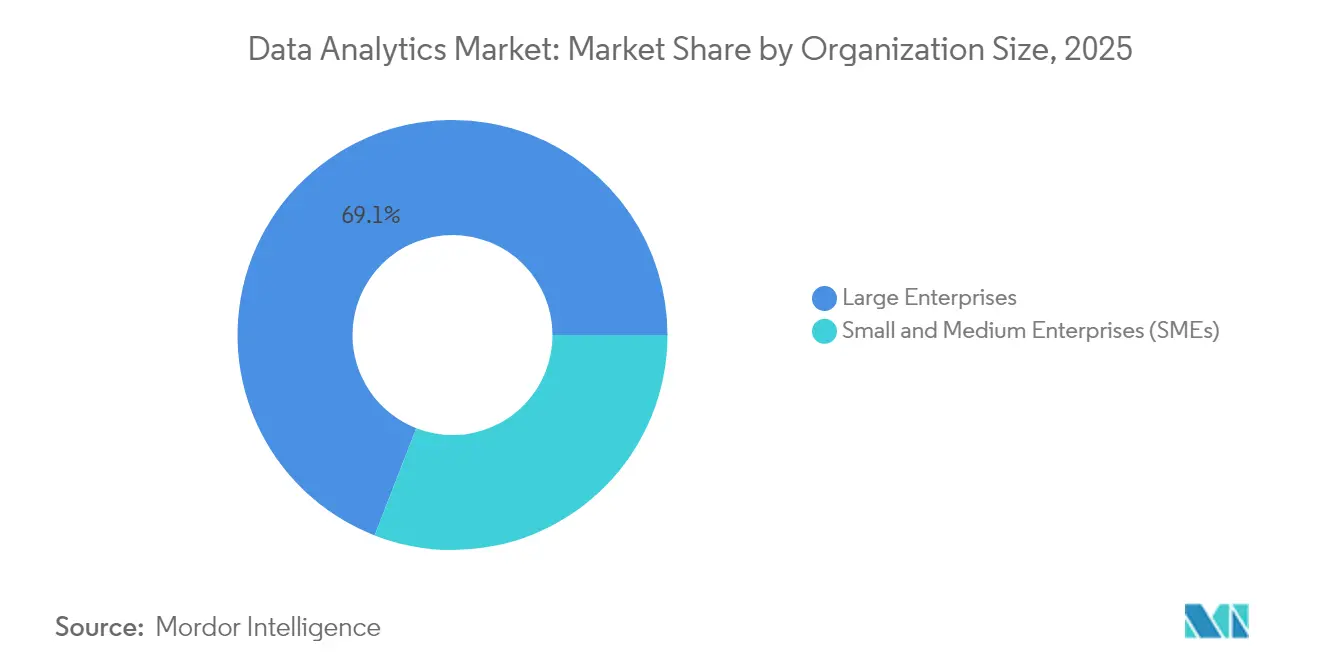

- By organization size, Large Enterprises captured 69.10% revenue in 2025; Small and Medium Enterprises will post a 32.90% CAGR between 2026-2031.

- By end-user industry, Information Technology and Telecom led with 44.20% of data analytics market share in 2025, yet Healthcare will deliver the fastest 33.40% CAGR.

- By geography, North America contributed 32.60% of 2025 revenue, while Asia-Pacific is forecast to grow at a 33.12% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of enterprise data volumes | +5.0% | Global; higher in North America and Europe | Medium term (2–4 years) |

| Rapid adoption of cloud-native analytics | +6.0% | Global; early uptake in North America | Medium term (2–4 years) |

| AI/ML integration elevating analytics value | +6.6% | Global; concentrated in technology hubs | Long term (≥ 4 years) |

| Regulatory push for data transparency | +4.0% | North America, Europe, rising in APAC | Medium term (2–4 years) |

| Privacy-preserving data clean rooms | +2.7% | North America, Europe | Long term (≥ 4 years) |

| Edge analytics for latency-critical IoT | +2.0% | Global; early use in manufacturing and telecom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of enterprise data volumes

Petabyte-scale datasets are now routine, especially in healthcare, which generates 30% of global data and is growing at 36% annually. Only 22% of firms consider their infrastructure adequate for AI workloads, pushing spend toward distributed compute, columnar storage, and GPU-accelerated query engines. Vendors that optimize cost-per-query at scale are gaining advantage in the data analytics market.

Rapid adoption of cloud-native analytics platforms

Elastic consumption pricing, managed services, and ecosystem integrations are making cloud data warehouses the default landing zone for many analytical workloads. The cloud shift democratizes insight creation, with 51% of data leaders prioritizing self-service analytics. Yet integration complexity and egress fees are motivating hybrid architectures within the data analytics market.

AI/ML integration elevating analytics value

Agentic AI unlocks predictive and prescriptive automation, converting static dashboards into decision engines. While McKinsey cites a USD 4.4 trillion productivity upside, only 1% of enterprises judge themselves AI-mature. Snowflake’s Intelligence and Data Science Agent modules exemplify how natural-language interfaces are closing the talent gap[2]Snowflake, “Snowflake Intelligence and Data Science Agent Launch,” snowflake.com. This trend is pivotal for the data analytics market because it lowers entry barriers for nontechnical users.

Regulatory push for data transparency and reporting

With most U.S. states expected to enforce privacy statutes by 2025, firms are upgrading governance, lineage, and consent models. Seventy-two percent of data leaders fear competitive erosion if AI governance lags. Compliance needs accelerate demand for trackable, policy-aware tooling in the data analytics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating data-privacy and cyber-security concerns | -4.6% | Global; acute in regulated industries | Medium term (2–4 years) |

| Shortage of skilled analytics talent | -4.0% | Global; pronounced in emerging markets | Short term (≤ 2 years) |

| ESG scrutiny of high-carbon analytics loads | -1.7% | Europe, North America; rising worldwide | Long term (≥ 4 years) |

| Vendor lock-in risks across analytics stacks | -1.3% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating data-privacy and cyber-security concerns

Cybercrime losses are forecast to hit USD 12 trillion by 2025, intensifying scrutiny on analytics pipelines. IBM’s 2025 Threat Index shows credential harvesting in 28% of incidents and data theft in 18%[3]IBM, “IBM Consulting Expands Microsoft Partnership,” ibm.com. Firms deploy AI-driven anomaly detection and format-preserving encryption, but these controls can slow data access, tempering data analytics market momentum.

Shortage of skilled analytics talent

Forty-two percent of analytics leaders cite skill scarcity as the top hurdle. Demand is acute for specialists in machine learning operations and data engineering. AutoML and low-code tools mitigate the gap, yet supervision by qualified professionals remains essential, adding cost and elongating project timelines in the data analytics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Analytics Type: Prescriptive capabilities unlock action

Prescriptive Analytics will expand at a 32.72% CAGR, signaling a maturity shift from hindsight to foresight. The segment’s growth reflects enterprise appetite for simulation, optimization, and automated orchestration that advise precise next steps. Descriptive Analytics still commands the largest share at 27.45% in 2025, underlining its role as the entry point for a data-driven culture. Diagnostic and Predictive Analytics provide intermediate insights into causality and probability, while Cognitive methods parse unstructured inputs such as images and text. This layered progression positions organizations to traverse the analytics continuum without tool sprawl. As AI augmentation spreads, hybrid platforms are merging descriptive dashboards with prescriptive agents, streamlining workflows inside the data analytics market.

Investment in augmented analytics is lowering the expertise threshold. A survey finds 87.9% of firms prioritizing analytics spend for competitive advantage. Seamless progression from descriptive summaries into predictive scoring, and onward to prescriptive simulation, amplifies decision cadence. Consequently, the data analytics industry is converging on unified platforms where insight chains flow without export-import overhead.

By Solution: Security Intelligence tackles threat evolution

Security Intelligence is poised for a 33.45% CAGR as breach frequency and regulatory pressure converge. Modern solutions embed UEBA, real-time correlation, and playbook automation to curtail mean-time-to-detect. Data Management remains foundational, holding a 24.60% share because data quality, lineage, and cataloging are prerequisites for any downstream analytics. Security Data Pipeline Platforms, such as Cribl, pre-process, enrich, and route telemetry, controlling storage bloat and improving query economics.

Visualization suites like Domo, Tableau, and Power BI are layering AI to auto-suggest visuals and generate narrative summaries. Warehousing and integration stacks adapt to multi-cloud and on-prem intersections, while business intelligence vendors embed analytics into frontline applications. These evolutions boost stickiness and raise switching costs, reinforcing competitive moats inside the data analytics market.

By Application: Risk and Fraud Management advances defense

Risk and Fraud Management will climb at a 33.60% CAGR as financial crime sophistication escalates and regulators impose heavier sanctions. Banking fraud detection spend is forecast to reach USD 63.2 billion by 2029. Customer Relationship Management retains an 17.65% share because personalized engagement is revenue-critical. Analytics-infused CRM uncovers micro-segments, optimizes campaign timing, and boosts customer lifetime value.

Supply chain applications deploy predictive forecasting to balance inventory and avert disruptions. Marketing analytics sharpen media attribution, and human resource analytics monitor attrition risk. Asset-management teams rely on predictive maintenance to cut downtime. Cross-application AI modules, including NLP for sentiment and anomaly detectors for operations, unify analytic capabilities, deepening integration across the data analytics market.

By Deployment Model: Cloud gains velocity, hybrid prevails

Cloud platforms are expanding at a 33.05% CAGR due to elastic compute, subscription economics, and continuous feature delivery. Yet, on-premises workloads hold a 64.25% share in 2025 because of data sovereignty rules and legacy application coupling. Public cloud offers rapid onboarding, private cloud secures sensitive datasets, and hybrid architectures blend both, optimizing for workload fit.

Notably, 33% of organizations repatriated at least one workload in 2023 over cost or latency concerns, signaling a more nuanced deployment calculus. Therefore, the data analytics market is coalescing around platform designs that permit seamless workload portability and policy-based orchestration.

By Organization Size: SMEs accelerate participation

SMEs are forecast to rise at a 32.90% CAGR as SaaS pricing, embedded analytics, and self-service interfaces dismantle historical cost barriers. Meanwhile, Large Enterprises command 69.10% of current spend, leveraging global IT budgets and change-management capacity. Exogenous drivers such as competitive intensity spur adoption, while internal inhibitors like culture and skill deficits slow progress.

Self-service tooling that automates data prep and recommends best-fit visuals is pivotal for SMEs. MDPI research highlights operational gains in SMEs that embed analytics, although financial and talent constraints persist. Embedded analytics inside ERP and CRM systems further softens the learning curve, broadening the reachable audience for vendors in the data analytics market.

By End-User Industry: Healthcare surges on digital health

Healthcare will register a 33.40% CAGR as EHR digitization, outcome-based reimbursement, and clinical AI adoption intersect. Data volume in the sector is projected to outpace every other vertical by 2025. Information Technology and Telecom, with a 44.20% share, continues leveraging analytics for network optimization and customer churn mitigation.

BFSI pursues risk scoring and fraud prevention, retail applies recommerce insights for hyper-personalization, and manufacturing employs predictive quality control to shrink scrap rates. Government agencies adopt analytics for policy impact measurement and fraud detection, while energy utilities rely on demand forecasting. These multifaceted deployments reaffirm that the data analytics market delivers horizontal value across all sectors.

Geography Analysis

North America generated 32.60% of 2025 revenue, underpinned by deep cloud penetration, venture funding, and a dense ecosystem of analytics talent. U.S. firms lead AI patent filings and production deployments, while Canadian banks and hospitals accelerate analytics modernization. Mexico’s manufacturing and retail players invest in analytic supply-chain visibility tools. Privacy regulations are fragmenting; most states will enact bespoke laws by 2025, compelling vendors to embed dynamic compliance controls. The data analytics market, therefore, prioritizes configurable policy engines for U.S. clients.

Asia-Pacific is the fastest mover with a 33.12% CAGR through 2031. China channels sovereign tech funds into AI infrastructure, India’s IT-services majors build global analytics delivery centers, and Japan applies analytics within smart-factory initiatives. South Korea focuses on 5G and edge analytics for telecom optimization. ASEAN economies favor cloud-first deployments to sidestep capital outlay, and regional data-center investment is expected to double Latin America’s capacity from USD 5-6 billion in 2023 to USD 8-10 billion by 2029, supporting globally distributed workloads. This momentum cements Asia-Pacific as the high-growth nucleus of the data analytics market.

Europe maintains robust adoption driven by Industry 4.0, fintech innovation, and national AI programs. Germany and the UK lead manufacturing and financial analytics, respectively, while France emphasizes healthcare AI for personalized medicine. GDPR-linked governance rigor elevates demand for privacy-enhancing technologies. The Middle East and Africa are scaling analytics to support diversification initiatives such as Saudi Vision 2030, with telecom and public-sector projects at the forefront. South America sees analytics uptake in financial inclusion and agritech, tempered by macroeconomic volatility. Overall, regional differences center on pace rather than value, validating the universal applicability of the data analytics market.

Competitive Landscape

The data analytics market is moderately consolidated. Incumbent software giants integrate analytics with cloud, ERP, and security stacks, creating platform lock-in and seeking total-addressable-market expansion. IBM’s dedicated Microsoft practice mobilizes 33,000 certified professionals to deliver joint AI and cloud solutions. Such alliances aim to shorten deployment cycles and de-risk large transformations.

Disruptors differentiate through agentic AI and vertical focus. Snowflake’s new agent frameworks allow natural-language queries and automated model creation, challenging traditional BI value propositions. Acquisition remains a principal growth vector: IBM’s Seek AI purchase strengthens conversational analytics, and 9fin’s Bond Radar deal expands real-time fixed-income intelligence. Vendors also curate marketplaces, offering partner extensions that fill functional gaps without direct research and development expense. These dynamics pressure lagging players to innovate or consolidate, sustaining competitive churn inside the data analytics market.

Third-party ecosystems (consultancies, ISVs, hyperscalers) influence buyer decisions by certifying integrations and recommending reference architectures. The resulting vendor landscape rewards those with open APIs, robust governance capabilities, and AI-ready pipelines. As feature parity rises, pricing transparency, service quality, and data-sovereignty assurances emerge as key differentiators.

Data Analytics Industry Leaders

Accenture plc

IBM Corporation

Oracle Corporation

SAS Institute Inc.

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Snowflake launched Snowflake Intelligence and Data Science Agent, adding agentic AI for natural-language querying and AutoML workflows.

- June 2025: IBM acquired Seek AI to embed conversational data querying into Watsonx AI Labs.

- May 2025: IBM unveiled a Microsoft Practice with 33,000 certified experts to expedite joint AI and cloud projects.

- May 2025: IBM expanded Watsonx with hybrid integration tools, boosting unstructured data accuracy by 40%.

- March 2025: 9fin purchased Bond Radar to reinforce financial analytics capabilities.

- February 2025: Google Cloud showcased AI-driven data analytics innovations at Next’25, including role-specific agents and autonomous data foundations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the data analytics market as the revenues software publishers and cloud-native platform providers earn from tools that ingest, process, and visualize structured or unstructured data to generate descriptive, diagnostic, predictive, prescriptive, or cognitive insights. We count license, subscription, and managed-service fees across on-premises, public, private, and hybrid deployments.

Scope exclusion. Our analysis leaves out pure hardware sales such as servers, storage arrays, and network equipment sold without embedded analytics capabilities.

Segmentation Overview

- By Analytics Type

- Descriptive Analytics

- Diagnostic Analytics

- Predictive Analytics

- Prescriptive Analytics

- Cognitive Analytics

- Other Types

- By Solution

- Data Management

- Data Warehousing and Integration

- Business Intelligence Tools

- Data Mining

- Security Intelligence

- Data Visualization and Dashboarding

- Other Solutions

- By Application

- Supply-Chain Management

- Customer Relationship Management

- Risk and Fraud Management

- Human Resource Management

- Marketing and Sales Optimisation

- Asset and Operations Management

- Other Applications

- By Deployment Model

- On-Premises

- Cloud

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-User Industry

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare and Life Sciences

- Information Technology (IT) and Telecom

- Retail and E-commerce

- Manufacturing

- Government and Public Sector

- Energy and Utilities

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview platform architects, procurement heads, independent data scientists, and regional channel partners across North America, Europe, Asia-Pacific, and the Middle East. The conversations validate price bands, deployment mix shifts, and emerging use cases while filling data blanks that secondary sources leave.

Desk Research

We first assemble a foundational fact-base from freely accessible tier-one sources such as the US Bureau of Labor Statistics, Eurostat, the National Bureau of Statistics of China, and industry associations like the Cloud Native Computing Foundation. Company 10-Ks, investor decks, major press releases, and patent filings provide commercial reality checks. Our analysts also access D&B Hoovers for vendor financials, Dow Jones Factiva for news flow, and Questel for patent intensity signals. These inputs clarify enterprise spending patterns, adoption triggers, and regulatory milestones that shape demand. The sources listed illustrate but do not exhaust the full range consulted during desk work.

Market-Sizing & Forecasting

We start with a top-down reconstruction that aligns national ICT spending, cloud spend ratios, and analytics penetration rates to size the demand pool. We then corroborate totals with selective bottom-up checks such as sampled annual subscription price multiplied by active customer counts shared by vendors. Key variables in the model include average analytics spend per employee, share of workloads moving to cloud each year, data-volume growth per industry, and talent supply tightness which influences service rates. Forecasts rely on multivariate regression combined with scenario analysis so we can stress-test outcomes against shifts in AI regulation or macro slowdowns. Gaps in granular bottom-up data are bridged using weighted regional proxies vetted through expert calls.

Data Validation & Update Cycle

Each draft model passes three internal review gates where anomalies are cross-checked against third-party indicators, news of large deals, and quarterly earnings. Reports refresh annually, with interim updates triggered by material events such as major pricing shifts or landmark regulations. A final analyst sweep ensures clients receive the latest view.

Why Mordor's Data Analytics Baseline Earns Trust

Published estimates often diverge because firms choose different service scopes, price capture points, and refresh cadences.

Our disciplined filter on what counts as true analytics revenue and our dual source triangulation keep the base year grounded.

Key gap drivers include competitors folding in big-data hardware, excluding cloud-only SaaS, or applying long refresh intervals that miss rapid price erosion. Currency conversion timing and undisclosed assumption sets widen the spread further.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 82.33 B | Mordor Intelligence | - |

| USD 85.47 B | Global Consultancy A | Includes stand-alone data-management hardware and limited primary validation |

| USD 64.75 B | Industry Portal B | Omits cloud-native SaaS revenues and restricts coverage to eight core economies |

In short, our tight scope choices, live primary inputs, and annual refresh give decision-makers a balanced, reproducible baseline they can rely on when sizing investments or benchmarking growth.

Key Questions Answered in the Report

What is the current size of the data analytics market?

The data analytics market size stands at USD 108.79 billion in 2026 and is projected to reach USD 438.47 billion by 2031 at a 32.15% CAGR.

Which region grows fastest in the data analytics market through 2031?

Asia-Pacific leads growth with a 33.12% CAGR thanks to aggressive cloud adoption, government AI initiatives, and expanding data-center capacity.

Why are Security Intelligence solutions outpacing other data analytics segments?

Heightened cyber-risk and stricter regulations propel demand for analytics that detect anomalies, automate response, and support compliance, driving a 33.45% CAGR for Security Intelligence.

How are SMEs benefiting from the data analytics market?

Affordable cloud platforms and self-service tools let SMEs deploy analytics without heavy upfront investment, powering a 32.90% CAGR in this segment.

What technology trend most accelerates data analytics adoption?

Integration of agentic AI and machine learning reduces the skills barrier by enabling natural-language querying and automated model creation, speeding enterprise insight generation.

What is the biggest restraint facing the data analytics market?

Escalating privacy and cyber-security concerns, projected to cut CAGR by 4.6 percentage points, force organizations to balance data utility with stringent protection measures.

Page last updated on: