Data Catalog Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

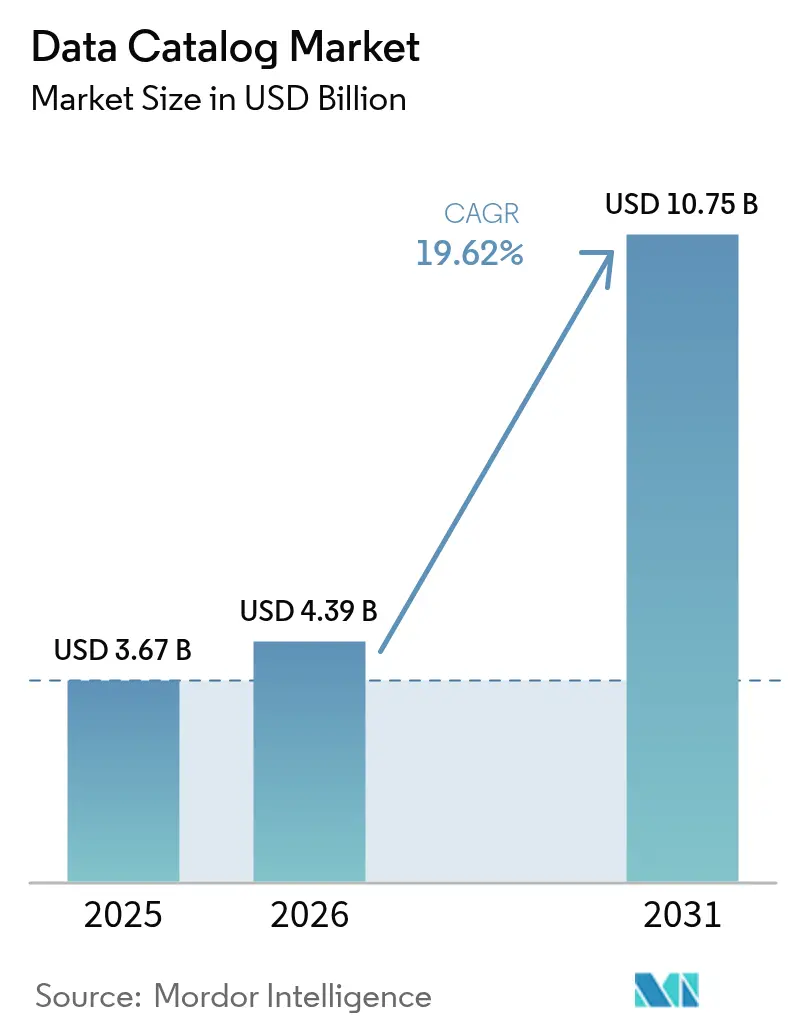

| Market Size (2026) | USD 4.39 Billion |

| Market Size (2031) | USD 10.75 Billion |

| Growth Rate (2026 - 2031) | 19.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Catalog Market Analysis by Mordor Intelligence

The Data Catalog Market size is expected to grow from USD 3.67 billion in 2025 to USD 4.39 billion in 2026 and is forecast to reach USD 10.75 billion by 2031 at 19.62% CAGR over 2026-2031.

Demand is propelled by cloud deployment, tighter regulatory oversight, and the need to support enterprise AI workloads with trusted, well-governed data. Vendors now deliver automated discovery, lineage, and quality checks that shorten implementation cycles, while the rapid pivot to cloud-native catalogs allows value realization in weeks instead of months. Generative AI is reshaping catalog functionality, shifting platforms from passive metadata stores to intelligent systems that enrich, classify, and secure information with limited manual effort. Competitive intensity is rising as large platform vendors integrate catalog features directly into broader data and analytics suites, forcing niche providers to innovate around time-to-value, industry depth, and AI enablement.

Key Report Takeaways

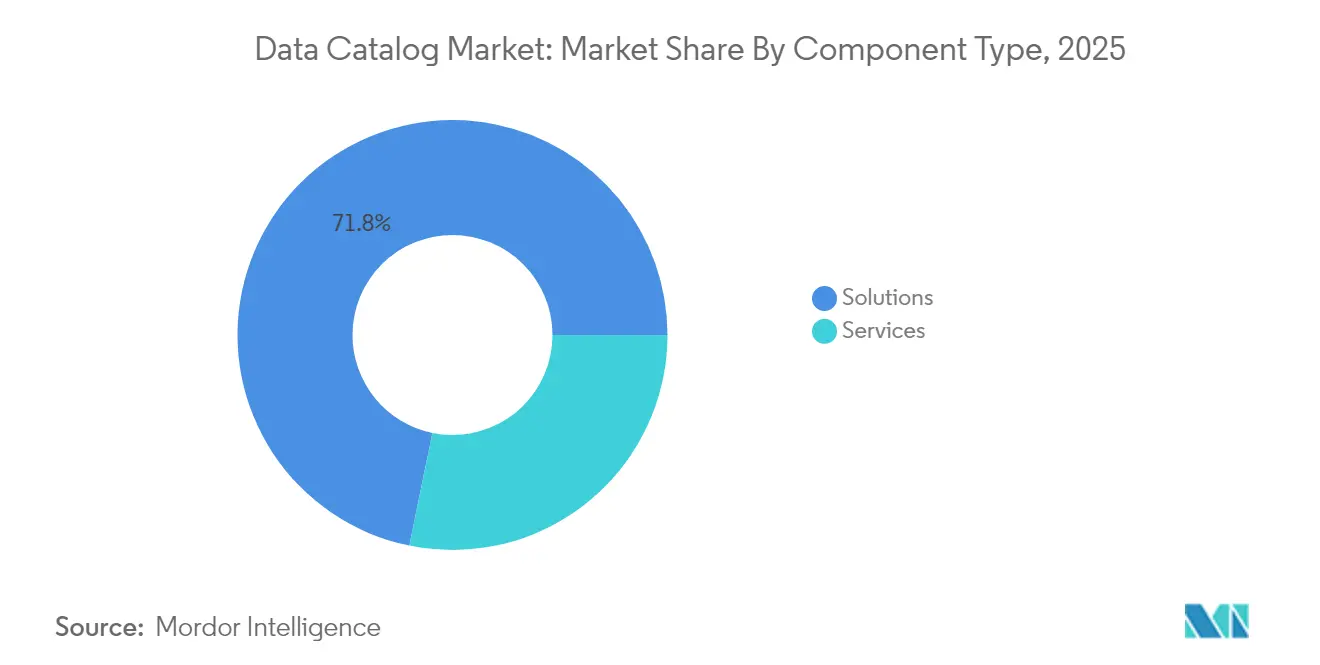

- By component, solutions led with 71.78% revenue share in 2025; services are projected to expand at a 24.96% CAGR through 2031.

- By deployment mode, the cloud segment held 80.55% of the data catalog market share in 2025, while the on-premise segment is set to post a 21.9% CAGR as hybrid demand persists.

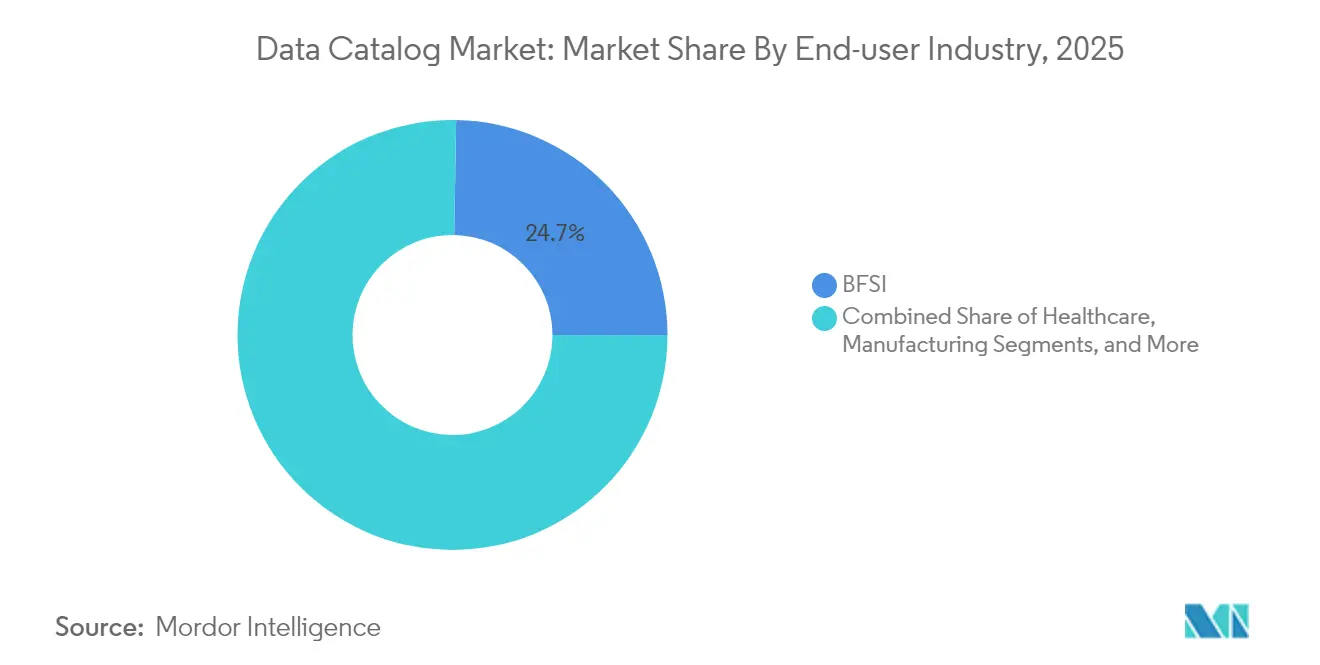

- By end-user industry, BFSI captured 24.73% of the data catalog market size in 2025; healthcare is expected to grow at 22.46% CAGR to 2031.

- By organization size, large enterprises accounted for 62.35% share of the data catalog market in 2025, whereas SMEs are forecast to rise at a 25.58% CAGR through 2031.

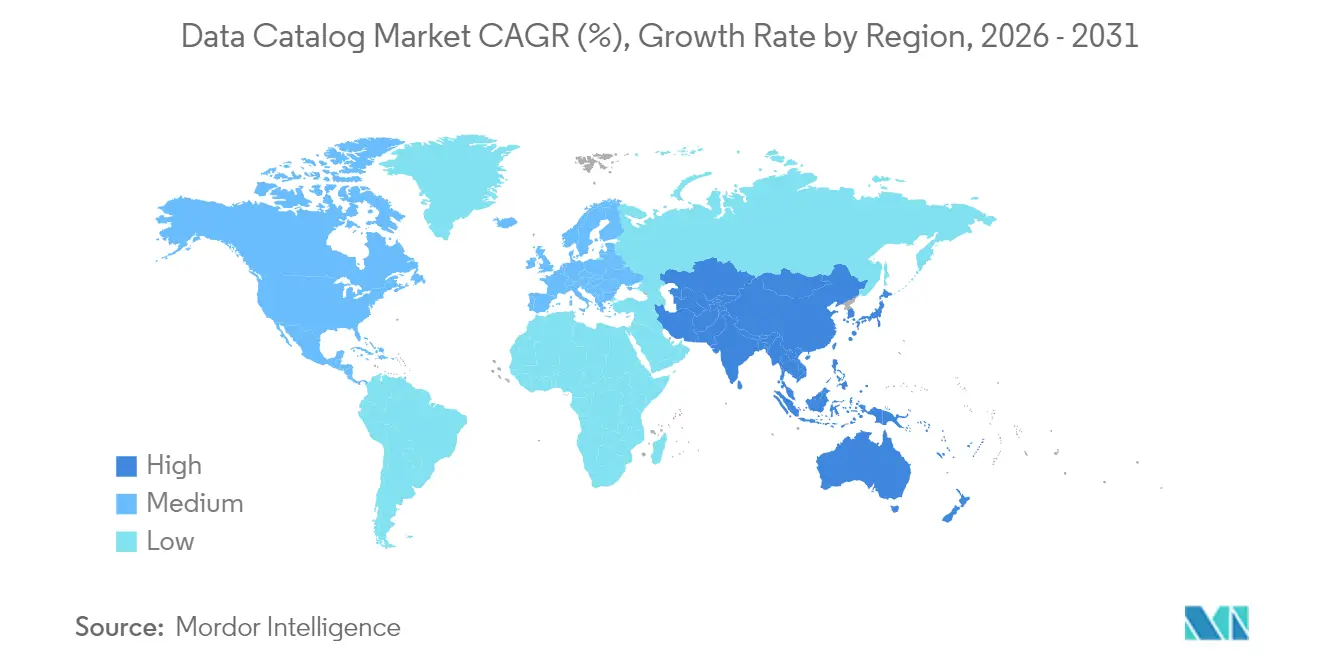

- By geography, North America held 41.62% of the data catalog market share in 2025; Asia-Pacific is advancing at a 23.62% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Catalog Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-based catalog adoption surge | +5.8% | Global; higher impact in North America and Europe | Short term (≤ 2 years) |

| Data-volume explosion and complexity | +4.3% | Global | Medium term (2-4 years) |

| Regulatory compliance mandates | +3.5% | North America, Europe, rising in Asia-Pacific | Medium term (2-4 years) |

| Generative-AI metadata enrichment | +2.7% | North America, Europe, advanced Asian markets | Medium term (2-4 years) |

| Data-mesh architecture proliferation | +2.0% | Global; higher in technology and financial sectors | Long term (≥ 4 years) |

| Open-source metadata standards | +1.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-based catalog adoption surge

Cloud deployment now underpins 81.2% of implementations, reducing infrastructure overhead and speeding roll-outs to days instead of months. Distributed workforces rely on cloud catalogs for consistent access to governed data, and usage-based pricing introduced by Microsoft Purview in January 2025 aligns costs to asset volume. [1]Microsoft Corporation, “Billing in Microsoft Purview Data Governance,” microsoft.com Cloud ecosystems also simplify integrations, allowing enterprises to connect diverse data stores while applying uniform policies. As analytics workloads migrate to public clouds at scale, demand for cloud-native catalogs will keep rising, fueling vendor innovation around elasticity, security, and cross-platform lineage.

Data-volume explosion and complexity

By 2025, unstructured information is projected to account for 80% of global data, forcing organizations to move beyond manual tagging toward automated discovery. [2]IBM Corporation, “Extracting insights from complex, unstructured big data,” ibm.com Data lakes capture varied content, yet without a catalog, users struggle to locate reliable assets. Effective discovery cuts time-to-insight by up to 40% and improves conversion in customer applications. Healthcare providers deploy solutions such as IQVIA Health Data Catalog to profile more than 3,700 assets through a single portal. [3]IQVIA, “Analytics Research Accelerator: Health Data Catalog,” iqvia.com As variety and velocity accelerate, catalogs able to span structured and unstructured sources become strategic differentiators.

Regulatory compliance mandates

Financial institutions comply with BCBS 239 by standardizing risk taxonomies and tracking lineage through catalogs. [4]OvalEdge, “BCBS 239 Compliance Through Practical Data Governance,” ovaledge.com Beyond banking, data privacy rules in Europe and emerging Asia-Pacific markets compel automated classification of sensitive fields. Catalog platforms now embed policy workflows, cutting manual compliance tasks and raising data quality. With AI governance frameworks on the horizon, catalogs increasingly serve as evidence of responsible data stewardship.

Generative-AI metadata enrichment

Large language models generate column descriptions, detect semantic similarities, and recommend quality rules, trimming curation workloads that once consumed scarce expert time. Microsoft embeds Copilot into Purview, guiding users through policy application while enriching metadata in the background. As models advance, the loop tightens: catalogs provide trusted inputs to AI, and AI returns enriched context that deepens catalog value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Standardization and security gaps | -2.8% | Global | Medium term (2-4 years) |

| Talent shortage in metadata mgmt | -1.9% | Global; higher in emerging markets | Medium term (2-4 years) |

| Catalog curation cost burden | -1.6% | Global; higher impact on SMEs | Short term (≤ 2 years) |

| Vendor lock-in via proprietary models | -1.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Standardization and security gaps

Inconsistent metadata models hamper interoperability, especially in healthcare, where differing clinical vocabularies lead to misinterpretation. Biomedical projects adopt frameworks such as DATS to encode diverse datasets, yet fragmentation persists. Security layers also vary across data sources, making it hard to enforce unified access through the catalog. Regional divergence in Asia-Pacific regulations risks data balkanization that could slow cross-border analytics.

Talent shortage in metadata management

Sixty percent of data professionals cite limited skills as the leading barrier to AI success, and 42% see it as their top data quality challenge. Healthcare providers report pronounced gaps that delay governance programs. Automation helps, but human expertise still defines business context and ownership. Enterprises respond with managed services and internal training, yet supply lags demand, restraining near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Drive Strategic Investments

Solutions accounted for 71.78% of 2025 revenue, confirming their role as the backbone of enterprise discovery and governance. Vendors now deliver automated lineage, AI-assisted enrichment, and granular policy enforcement through single interfaces that scan heterogeneous stores. This functionality positions solutions as the first stop in modernization programs, anchoring broader data intelligence strategies. At the same time, the services segment is expanding at 24.96% CAGR as enterprises seek guidance on operating models, policy design, and change management. Many engagements develop federated governance structures that distribute accountability while retaining global standards.

Across both segments, enterprises prioritize tight integration. Microsoft Purview’s reference architecture encourages the definition of governance domains before scan configuration, highlighting the process maturity required for success. Service providers craft accelerators that codify best practices, reducing risk for first-time deployments. As solutions evolve into platforms and vendors wrap advisory and managed services around them, the traditional boundary between product and service blurs. This blend supports rapid adoption while ensuring organizations extract measurable value, sustaining long-term momentum for the data catalog market.

By Deployment Mode: Cloud Dominance Accelerates Innovation

Cloud captured 80.55% share in 2025 and is forecast to rise at 23.85% CAGR, reflecting advantages in elastic scale and rapid provisioning. Consumption models let teams start small and expand as asset counts grow, aligning spend to value delivered. Microsoft’s pay-as-you-go tariff, adopted in 2025, exemplifies this shift, charging only for unique governed assets and quality metrics. Cloud deployment also delivers automatic feature updates, shortening innovation cycles and ensuring immediate access to AI-driven enhancements.

Despite cloud momentum, on-premise catalogs remain important in sectors with strict data residency or legacy mainframe workloads. These organizations increasingly favor hybrid patterns, scanning sensitive stores in place while centralizing metadata in a secure cloud hub. Vendors respond with private-link connectivity and role-based access controls that enforce consistent policy regardless of location. This balance between agility and sovereignty sustains a diversified deployment landscape and broadens addressable demand for the data catalog market.

By End-user Industry: BFSI Leads While Healthcare Accelerates

BFSI led with a 24.73% share in 2025, leveraging catalogs to align with BCBS 239 and other capital adequacy mandates. A Swiss bank trimmed search time to under one second after rolling out a cross-domain catalog that links documents and data assets, boosting end-user satisfaction to 97%. Financial firms also harness lineage to support model risk management, tracing outputs back to approved data sources and reducing audit effort. These use cases keep BFSI investment high, anchoring revenue for the data catalog market.

Healthcare, growing at 22.46% CAGR, uses catalogs to apply FAIR principles and enhance research reproducibility. The Translational Data Catalog surfaces biomedical datasets for secondary analysis, expanding the value of funded studies. Providers integrate clinical, imaging, and genomic data to personalize treatment while safeguarding patient privacy. Similar gains appear in retail, manufacturing, and telecom, where catalogs unify customer journeys, trace supply chains, and manage network telemetry. This sectoral diversity underlines the universal relevance of trusted, findable data.

By Organization Size: Large Enterprises Dominate While SMEs Accelerate

Large enterprises held a 62.35% share in 2025 as sprawling data estates mandate robust governance. These firms adopt federated models that assign stewardship to domains while enforcing global standards through centralized workflow engines, mirroring guidelines published for Microsoft Purview deployments. Scale drives investment not only in software but also in operating processes, making large enterprises the core revenue base for vendors.

SMEs represent the fastest-growing cohort at 25.58% CAGR, empowered by cloud catalogs that remove upfront infrastructure cost. Pay-as-you-go pricing lowers entry barriers, while managed services fill skill gaps. SMEs typically target high-impact use cases such as privacy compliance or customer segmentation before expanding scope. As offerings mature and automation intensifies, catalog adoption within mid-market firms will further broaden the data catalog market size across all regions.

Geography Analysis

North America retained leadership with a 41.62% share in 2025, supported by mature cloud infrastructure, advanced AI adoption, and stringent industry regulations. Enterprises in the United States integrate generative models into catalogs to automate profiling and improve lineage, addressing quality concerns reported by 46% of data practitioners. Canada follows similar trajectories in financial services and healthcare, while Mexico’s fast-growing fintech sector spurs new deployments. Regional buyers favor solutions that pair deep compliance tooling with open connectivity, a profile that continues to shape vendor roadmaps.

Asia-Pacific is the fastest-expanding arena, growing at 23.62% CAGR through 2031. China, India, and Japan top AI investment rankings, prompting higher spending on robust data foundations. Governments tighten privacy and sovereignty rules, driving demand for tools that locate, classify, and tokenize personal data at rest and in motion. Challenges arise from fragmented policy landscapes and uneven skill availability, yet flexible architectures and managed services help enterprises keep pace. Local deployments increasingly blend global best practices with country-specific encryption and residency controls.

Europe advances on the back of GDPR-aligned governance. Data catalogs automate the detection of sensitive fields and record data lineage, letting firms demonstrate accountability under evolving AI rules. Industries in Germany and France extend catalog scope to supply-chain data for sustainability reporting. The Middle East and Africa see accelerated uptake from a small base, leveraging cloud to bypass legacy constraints. South America’s digital initiatives, particularly in Brazil, extend catalog coverage to e-commerce and energy assets. Across regions, the common thread remains a need for transparent, policy-driven access that underpins both operational reporting and AI innovation, widening the data catalog market size globally.

Competitive Landscape

The market shows moderate concentration as platform giants and focused specialists vie for influence. Microsoft integrates Purview tightly with Azure and Fabric, offering unified asset discovery across databases, storage, and analytics services. IBM enriches Watsonx with an Agent Catalog comprising more than 150 tools that connect hybrid environments, strengthening its position in AI-driven governance. Salesforce’s USD 8 billion purchase of Informatica in 2025 bundles catalog, integration, and Data Cloud, signaling convergence between operational applications and governance backbones.

Pure-play vendors such as Alation and Collibra compete on agility and user experience, delivering rapid deployment and domain-specific accelerators that appeal to business stewards. They differentiate through open connectors and partnership ecosystems, addressing concerns about vendor lock-in. Open-source initiatives gain visibility but face hurdles in enterprise support and compliance certifications. Vertical specialists carve niches in healthcare and financial services, embedding regulatory logic out of the box.

Strategic themes include embedding generative AI, widening API coverage, and simplifying role-based policy management. Buyers increasingly ask for catalog services that integrate quality monitoring, observability, and cost tracking across multi-cloud estates. Vendors able to span these requirements without compromising performance or governance rigor are positioned to outpace slower competitors and expand their share of the data catalog market.

Data Catalog Industry Leaders

Collibra NV

IBM Corporation

Microsoft Corporation

Informatica Inc.

Alation Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Salesforce agreed to acquire Informatica for USD 8 billion to build an end-to-end AI data platform that unites Data Cloud, MuleSoft, and Tableau with Informatica’s governance suite.

- April 2025: IBM announced its intent to acquire DataStax, adding NoSQL and unstructured data expertise to Watsonx for enhanced hybrid data discovery.

- April 2025: Microsoft Fabric updates enhanced OneLake catalog governance, adding detailed metadata capture and role-based access control.

- February 2025: Microsoft launched the Purview Unified Catalog with AI-powered search and automated quality checks, extending reach to non-Microsoft data stores.

- January 2025: Collibra expanded its platform with AI governance features that align catalog workflows to model lifecycle management.

- January 2025: Microsoft introduced a pay-as-you-go billing model for Purview Data Governance, tying charges to unique governed assets and data health metrics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global data catalog market as all commercial software licenses, plus related implementation or managed services, that harvest, enrich, and serve enterprise metadata so users can quickly find, trust, and govern structured, semi-structured, and unstructured data across on-premise and multi-cloud estates. Any counted tool must offer federated search, lineage visualization, and policy-based tagging.

Scope exclusion: Stand-alone desktop tagging utilities or simple media libraries that lack enterprise governance are not covered.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud

- On-Premise

- By End-user Industry

- BFSI

- Retail and E-commerce

- Healthcare

- Manufacturing

- Telecommunications

- Other End-user Industries

- By Organization Size

- Large Enterprises

- Small and Mid-size Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed chief data officers, solution architects, compliance leads, and system-integrator partners in North America, Europe, and fast-growing Asia-Pacific to validate usage depth, price dispersion, and budget shifts that documents alone could not reveal.

Desk Research

We began by mapping open indicators from the US National Institute of Standards and Technology, the European Data Protection Board, Singapore IMDA, and OECD ICT datasets, which anchor regulation timelines, cloud uptake, and firm counts. Trade bodies such as the Cloud Native Computing Foundation and DAMA International supplied adoption ratios, while Volza customs logs flagged regional software inflows.

Our team then compared vendor revenue splits and average selling prices using company 10-Ks, price lists, and news pulled through D&B Hoovers and Dow Jones Factiva. The sources named here illustrate our desk effort and are not exhaustive.

Market-Sizing & Forecasting

A hybrid top-down and bottom-up model starts with the global pool of mid- and large-size enterprises, applies region-specific penetration rates, and multiplies by blended cloud and on-premise ASPs. Sampled vendor bookings and channel checks validate totals. Key drivers include public-cloud spend, regulation-linked governance budgets, dataset growth per employee, metadata-automation rates, and renewal cycles. Multivariate regression with ARIMA smoothing projects each driver to 2030.

Data Validation & Update Cycle

Outputs clear two analyst reviews; variances beyond preset bands trigger fresh calls. Models refresh annually, with interim tweaks for major M&A or policy shocks.

Why Our Data Catalog Baseline Commands Reliability

Published figures often diverge because firms select dissimilar scopes, price ladders, and refresh cadences. Gaps widen when services are ignored or only on-premise licenses are counted.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.67 B (2025) | Mordor Intelligence | - |

| USD 1.06 B (2024) | Global Consultancy A | Excludes services, short vendor set |

| USD 0.90 B (2023) | Industry Association B | Historic base year, no cloud uplift factor |

| USD 0.97 B (2024) | Trade Journal C | Relies on supplier press notes only |

These contrasts show that, by coupling complete scope with our annually refreshed mixed-method evidence, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers trust.

Key Questions Answered in the Report

What is driving the rapid growth of the data catalog market in 2026?

Growth is fueled by cloud deployment, tighter regulatory mandates and the need to supply AI models with trusted data, resulting in a 19.62% CAGR outlook.

How large is the data catalog market size today?

The data catalog market size stands at USD 4.39 billion in 2026 and is projected to reach USD 10.75 billion by 2031.

Which region leads the data catalog market share?

North America holds the largest data catalog market share at 41.62% in 2025, supported by mature cloud infrastructure and strict compliance requirements.

Which deployment mode dominates current implementations?

Cloud deployment commands 80.55% of live catalogs, with pay-as-you-go pricing accelerating adoption among organizations of all sizes.

Why are data catalogs important for AI initiatives?

Catalogs supply AI teams with governed, high-quality data, while generative capabilities within catalogs automate enrichment and cut manual curation effort.

What are the main challenges limiting adoption?

Metadata skill shortages, inconsistent security standards and concerns over vendor lock-in are the leading restraints, collectively shaving around 5.6% from forecast CAGR.

Page last updated on: