Enterprise Governance, Risk And Compliance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

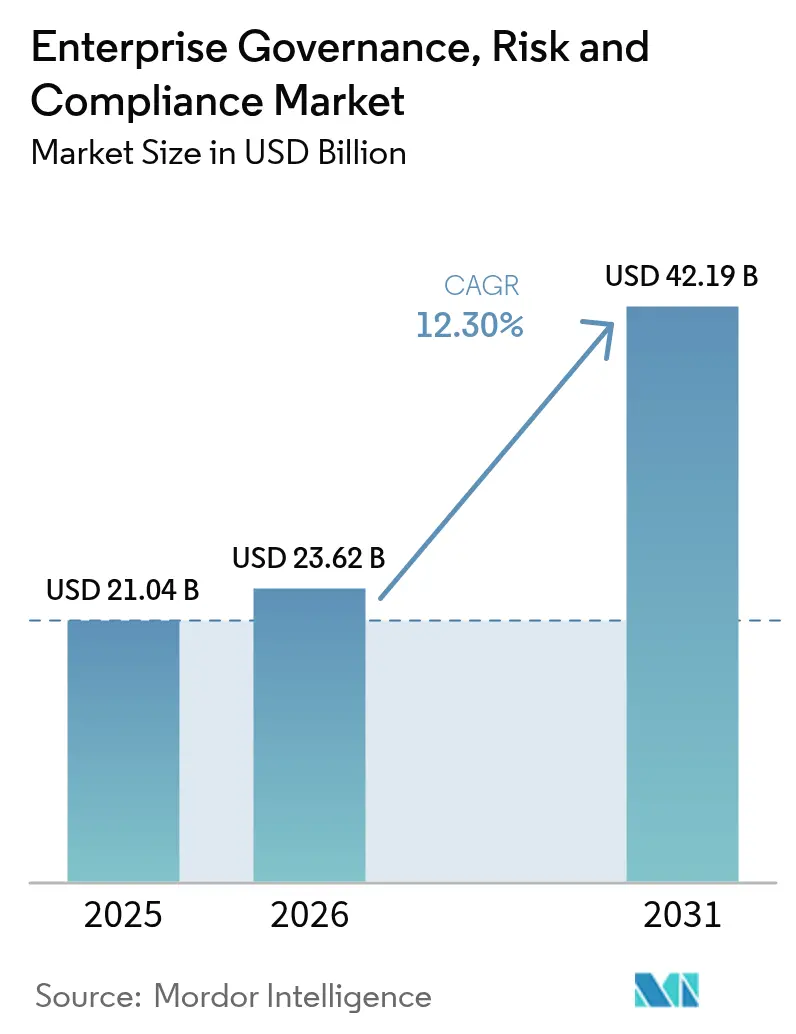

| Market Size (2026) | USD 23.62 Billion |

| Market Size (2031) | USD 42.19 Billion |

| Growth Rate (2026 - 2031) | 12.30% CAGR |

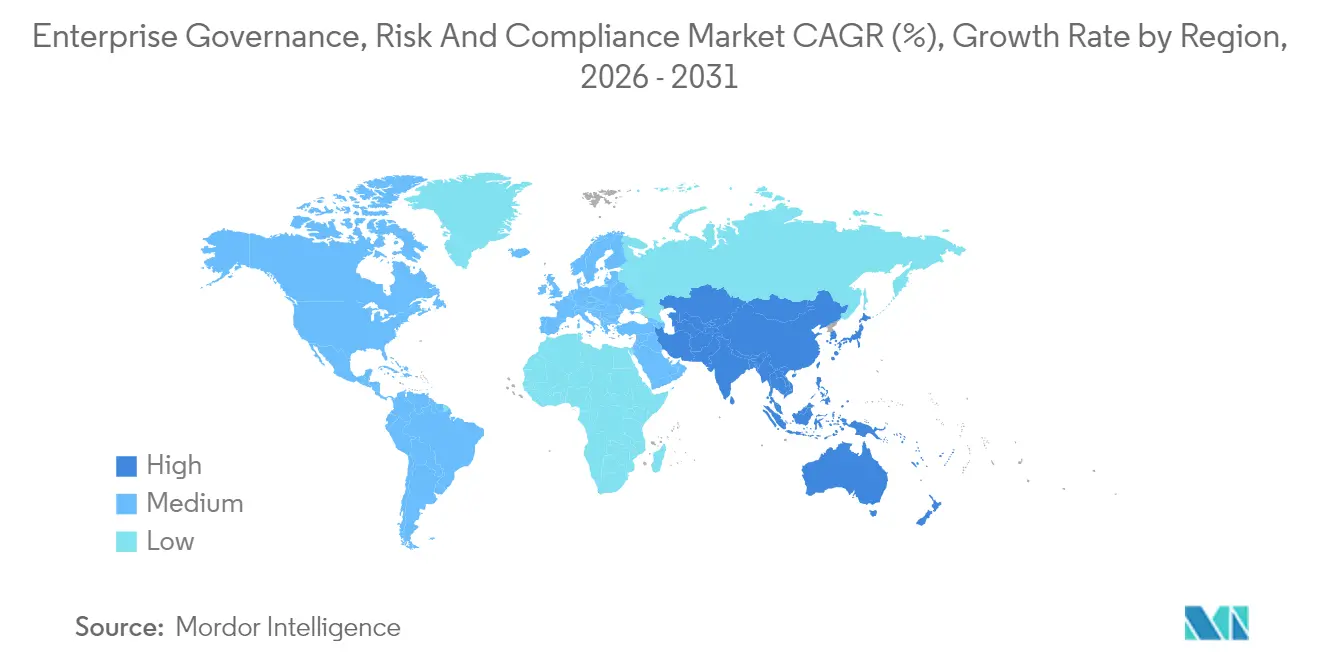

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Governance, Risk And Compliance Market Analysis by Mordor Intelligence

The enterprise governance risk compliance market size is expected to grow from USD 21.04 billion in 2025 to USD 23.62 billion in 2026 and is forecast to reach USD 42.19 billion by 2031 at 12.3% CAGR over 2026-2031. Demand accelerates as organizations confront a surge in regulatory obligations, most notably the Digital Operational Resilience Act (DORA), while adopting AI to automate controls, interpret fast-changing rules, and flag anomalies in real time. Platform uptake intensifies because integrated suites consolidate previously siloed audit, policy, and cybersecurity workflows into a single source of truth, producing measurable cost savings and faster issue resolution. Early adopters report efficiency gains of up to 42% in false-positive reduction after embedding AI-driven compliance analytics alongside security telemetry. Momentum is further reinforced by insurers that now price coverage using real-time GRC metrics, translating strong governance performance into premium discounts and competitive advantage.

Key Report Takeaways

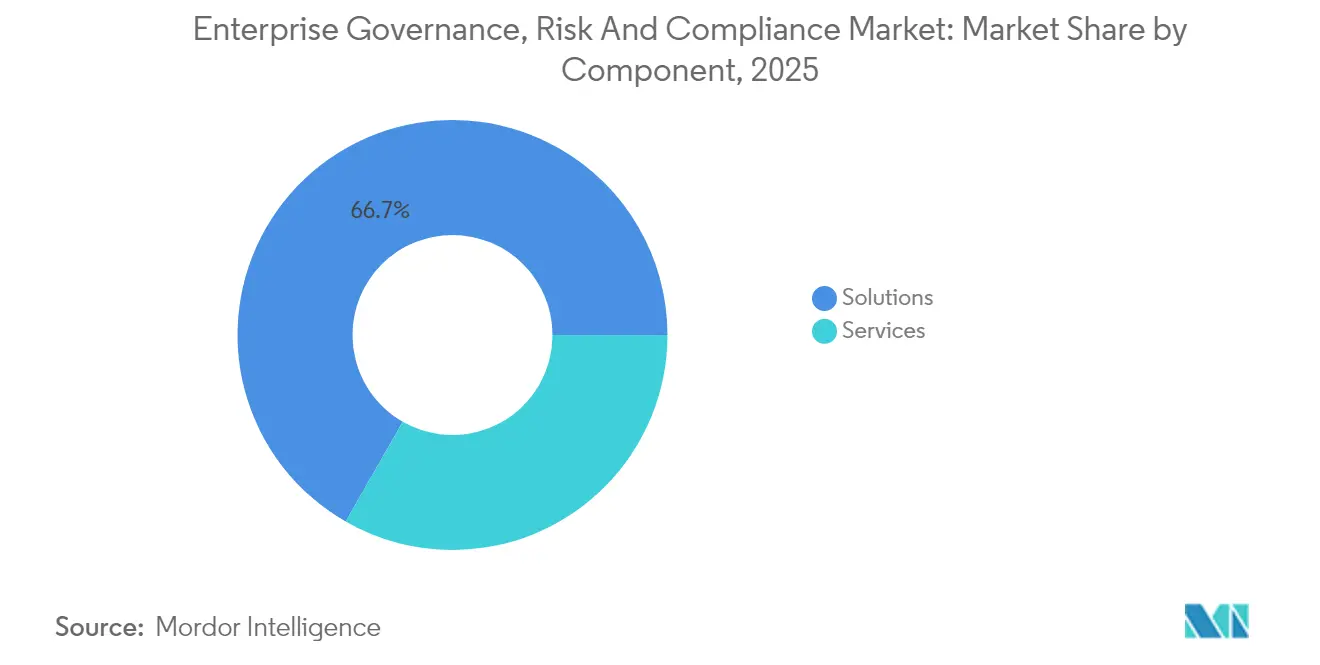

- By component, Solutions held 66.72% of enterprise governance risk compliance market share in 2025, whereas Services are forecast to post the fastest 12.6% CAGR through 2031.

- By deployment model, on-premise installations accounted for 53.40% revenue in 2025, but cloud platforms are projected to grow at 13.3% CAGR to 2031.

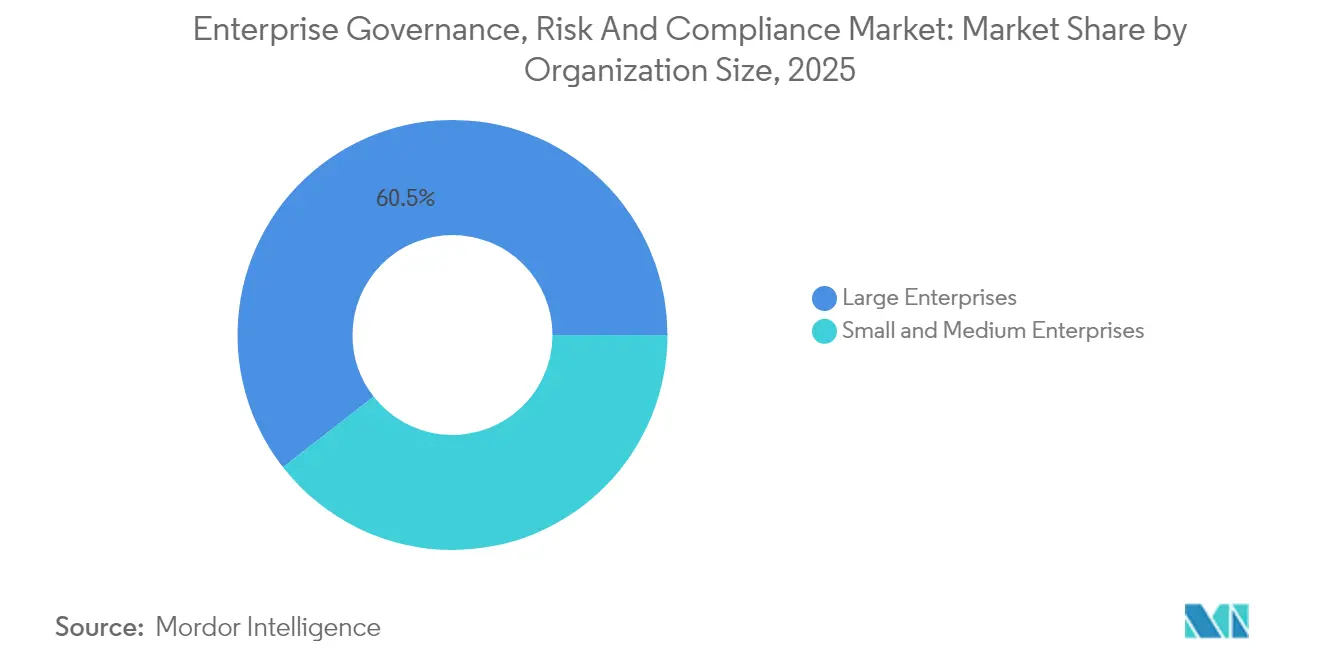

- By organisation size, Large Enterprises captured 60.55% of 2025 revenue, yet SMEs will expand at a 14.1% CAGR on the back of cloud-based offerings.

- By end-user industry, Healthcare and Life Sciences commanded 34.25% revenue in 2025; BFSI is expected to lead growth at 12.7% CAGR through 2031.

- By geography, North America led with 34.80% share in 2025, while Asia-Pacific is anticipated to register the highest 12.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Governance, Risk And Compliance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations and mandates | +2.8% | Global with focus in EU and North America | Medium term (2-4 years) |

| Rising cybersecurity threats with digital transformation | +2.1% | Global, pronounced in APAC and North America | Short term (≤ 2 years) |

| Move toward integrated risk-management platforms | +1.9% | North America and EU leading | Medium term (2-4 years) |

| ESG reporting pressure and non-financial disclosure rules | +1.7% | EU primary driver | Long term (≥ 4 years) |

| AI-powered predictive compliance analytics adoption | +2.3% | North America and EU early adopters | Short term (≤ 2 years) |

| Insurance underwriting dependencies on real-time GRC metrics | +1.5% | Global, mature insurance markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent government regulations and mandates drive platform consolidation

Heightened rulemaking continues to swell the enterprise governance risk compliance market as DORA, effective January 2025, obliges EU financial entities to embed ICT risk frameworks covering incident response, resilience testing, and third-party oversight.[1]Norton Rose Fulbright, “DORA: Key Operational Resilience Obligations,” nortonrosefulbright.com Firms now monitor more than 250 regulatory changes each day, a pace that outstrips manual processes. Machine-learning models parse new statutes, rank their relevance, and route tasks to accountable owners within minutes, enabling compliance teams to redeploy effort toward strategic risk analysis. Vendors offering multijurisdictional mapping and automated update engines have therefore moved to the top of enterprise shortlists. Failure to comply risks both material penalties and reputational damage, whereas early movers secure investor confidence by demonstrating operational resilience.

Rising cybersecurity threats accelerate GRC technology integration

Cyber incidents spiked 75% in 2024, pushing CISOs to embed security posture metrics into core governance dashboards instead of handling them in isolation. A single console that overlays policy checks onto threat telemetry cuts duplication and shrinks time to remediate vulnerabilities across hybrid environments. Healthcare providers adopting AI-enabled GRC suites recorded 37% stronger risk detection rates and 42% fewer false positives, illustrating the value of unifying compliance and security data. Because 70% of organizations label current cloud-risk assignment processes ineffective, appetite for centralised, cloud-agnostic controls has intensified.[2]Cloud Security Alliance, “State of Cloud Security 2024,” cloudsecurityalliance.org Suppliers that deliver actionable dashboards—rather than raw alerts—win traction by easing user fatigue and freeing specialists to focus on high-impact threats.

AI-powered predictive compliance analytics transform risk management

Two-thirds of enterprises intend to fund AI initiatives for risk oversight, yet only 14% have completed integration, signalling broad runway for the enterprise governance risk compliance market. Generative AI engines now interpret draft laws with 95% accuracy and push automatic policy updates, turning compliance from reactive box-ticking into forward-looking advisory. Bespoke small language models let firms retain data residency while reducing compute costs, an attractive proposition for regulated industries. Early adopters have shortened audit cycles, eliminated redundant controls, and produced predictive heat maps that guide board spending on mitigation. Consequently, AI capability is becoming a baseline buyer requirement rather than a premium feature.

ESG reporting pressure creates new compliance categories

European regulations converted ESG disclosures from voluntary to mandatory, compelling firms to track carbon footprints, social-impact metrics, and governance practices alongside financial statements. Integrated platforms now ingest energy data, supplier ethics scores, and diversity statistics, generating investor-ready dashboards that align with frameworks such as CSRD. AI-powered ESG auditors scrape unstructured sources—utility bills, sensor feeds, supplier attestations—and auto-populate reports, cutting manual effort while raising accuracy. Vendors that link ESG scores to risk appetite statements extend their value proposition, positioning the enterprise governance risk compliance market as a central hub for sustainability intelligence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of skilled GRC professionals | -1.8% | Global, acute in Asia-Pacific | Long term (≥ 4 years) |

| High initial integration cost for legacy environments | -2.1% | North America and EU | Medium term (2-4 years) |

| Data-residency and sovereignty complexity in multi-cloud | -1.3% | Worldwide | Short term (≤ 2 years) |

| Organisational GRC-fatigue and alert overload | -1.6% | Mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High initial integration costs challenge legacy system modernization

Annual subscriptions for leading suites range from USD 50,000 to USD 500,000, while implementation often costs two to six times the license fees, straining budgets for firms running ageing ERP backbones.[3]6clicks, “Cost Benchmarks for GRC Implementations,” 6clicks.com SaaS inflation running at 11.3% further heightens price sensitivity as vendors impose 25% hikes despite flat headcount. Integrating modern GRC tools with bespoke finance, HR, and manufacturing systems often demands custom APIs and change-management programmes that extend timelines. Outcome-based licensing and low-code connectors are gaining popularity by shifting capital expenditure to operating expense and demonstrating payback through quantifiable risk-reduction metrics.

Organizational GRC-fatigue impedes platform adoption

Users inundated by non-stop alerts disengage, diminishing system value. In 2024, 60% of firms cited overwhelmed staff as the top barrier to realizing full benefits from their platforms. Over-automation without context delivers data dumps rather than insights, compelling buyers to demand AI filters that rank issues by criticality and present tailored dashboards for each role. Suppliers answering this pain point improve stickiness and reduce churn, positioning themselves strongly as enterprises rationalize overlapping systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominance Drives Service Innovation

Solutions generated 66.72% of 2025 revenue, underscoring buyer preference for end-to-end suites that blend policy libraries, audit trails, risk scoring, and incident response into one stack. This dominance reflects how enterprises value single-vendor accountability and consistent user experience across all functions of the enterprise governance risk compliance market. Consulting, integration, and managed services, though smaller in absolute value, are set to grow 12.6% through 2031 as buyers turn to external experts for regulatory interpretation and complex system rollouts. Risk Management and Audit Management modules experience the fastest take-up because they replace spreadsheet workflows and provide real-time analytics that executives can track on mobile apps. Demand for Business Continuity features surged after supply-chain shocks averaged USD 184 million in losses, prompting firms to link continuity plans directly to supplier scorecards.

By Deployment Model: Cloud Migration Accelerates Despite Security Concerns

On-premise installations retained 53.40% of 2025 revenue because banks and hospitals must store sensitive records locally, but cloud subscriptions will expand 13.3% annually through 2031 as CIOs favor elastic compute for AI workloads. Cloud platforms automate upgrades, shorten implementation cycles, and empower remote teams, making them attractive to SMEs and multinationals alike. Regulatory scrutiny on third-party resilience through DORA pushes firms to demand continuous oversight of external cloud providers-a capability that cloud-native GRC suites embed by design. Hybrid models, which keep critical data on-site while shifting analytics to the cloud, enable risk-averse firms to test the waters without breaching residency rules.

Providers mitigate perceived security gaps by offering customer-managed encryption keys and sovereign-cloud regions certified for local compliance regimes. They also streamline deployment through infrastructure-as-code templates that stand up full environments in hours rather than weeks. As AI algorithms require large training sets and scalable GPUs, cloud deployments become the default choice for predictive compliance analytics-cementing their role in the future landscape of the enterprise governance risk compliance market.

By Organisation Size: SME Adoption Accelerates Through SaaS Models

Large Enterprises contributed 60.55% of 2025 sales, driven by multi-jurisdictional operations that necessitate sophisticated workflow orchestration and advanced analytics. These organizations integrate platforms with ERP and IT-service-management systems to gain cross-functional transparency and automated evidence collection. However, SMEs will outpace them with a 14.1% CAGR because subscription-based offerings strip away hefty capital outlays and deliver pre-configured controls tailored to sector needs. Vendors promote rapid, low-touch deployments that go live in weeks, meeting smaller teams' resource constraints while satisfying auditors' demands.

SaaS inflation does present budgetary pressure, but SMEs balance higher fees against the risk of non-compliance penalties, reputational damage, and lost tenders. Outcome-based pricing-charging only when audit checkpoints pass or incidents close within SLA-encourages adoption by tying cost to value delivered. The playbook resonates in emerging markets where regulators ramp oversight yet local talent pools remain thin, propelling the enterprise governance risk compliance market into new customer segments.

By End-User Industry: Healthcare Leadership Reflects Regulatory Intensity

Healthcare and Life Sciences accounted for 34.25% of 2025 revenue on the back of strict patient-safety norms, HIPAA, and FDA guidelines. AI-enabled platforms that automatically scan electronic medical records flag privacy violations and ensure audit readiness, reducing manual review workload by thousands of hours. Manufacturing and Energy firms increasingly connect shop-floor IoT devices to GRC hubs, monitoring safety compliance in real time and linking findings to maintenance tickets. BFSI lines up as the fastest-growing vertical at 12.7% CAGR because soaring financial crime costs-USD 61 billion annually in North America-make automated surveillance indispensable.

Retailers invest to manage supply-chain transparency mandates, while government agencies deploy platforms to boost accountability and citizen trust. Cross-industry, ESG reporting mandates ensure every sector now needs structured data collection and auditable trails, expanding addressable demand for the enterprise governance risk compliance market.

Geography Analysis

North America generated 34.80% of global revenue in 2025, supported by mature regulatory ecosystems and robust technology budgets. Financial institutions spend USD 61 billion annually on compliance, and 99% expect costs to rise, reinforcing demand for automated solutions that lower expense ratios. Federal guidelines reward self-reporting and resilient operations, so firms treat GRC investment as a competitive edge. Partnerships such as ServiceNow-Visa illustrate how technology vendors co-create AI workflows that enhance dispute management while ensuring regulatory adherence.

Asia-Pacific is projected to log a 12.9% CAGR, the highest globally. Governments in Singapore, Australia, and India introduce corporate liability rules mirroring the UK Bribery Act, compelling companies to invest in modern compliance architecture. APAC banks also confront USD 45 billion in financial-crime compliance costs, with 70% citing higher software spend in 2024, driving cloud-native uptake that aligns with rapid digitalization.

Competitive Landscape

The enterprise governance risk compliance market shows moderate concentration. Technology majors—IBM, SAP, ServiceNow, and Oracle—hold significant share through broad portfolios and deep integration capabilities. IBM’s pending HashiCorp acquisition strengthens hybrid-cloud automation and positions its platform suite to orchestrate multi-cloud compliance. ServiceNow scales AI reach via partnerships with NVIDIA and Google Cloud, embedding generative agents that draft control remediations and summarize audit evidence.

Mid-tier specialists pursue vertical depth. Mitratech’s purchases of Prevalent and Preparis augment third-party risk and business continuity modules. Kroll’s takeover of Resolver fuses risk intelligence with cyber forensics, producing end-to-end visibility for incident teams. Disruptors like Scytale and Drata differentiate on outcome-based pricing, SOC 2 automation, and curated policy libraries for SMEs.

Innovation focuses on AI-guided control testing, low-code policy engines, and UX that filters noise through intelligent prioritization. Patent filings, such as ServiceNow’s automated vulnerability-remediation method, underscore the race to reduce manual toil. As vendors converge on core features, ecosystem strength—integrations, content partnerships, and developer communities—becomes the deciding factor for buyers evaluating long-term platform fit within the enterprise governance risk compliance market.

Enterprise Governance, Risk And Compliance Industry Leaders

Dell Technologies (incl. RSA Security)

SAP SE / GRC Suite

Oracle Corporation

MetricStream Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ServiceNow and NVIDIA unveiled the Apriel Nemotron 15B model to power real-time workflow agents.

- June 2025: Scytale bought AudITech to fold SOX ITGC automation into its compliance suite

- May 2025: Diligent acquired Vault, adding multilingual whistle-blowing and ethics reporting tools.

- April 2025: AQM Technologies purchased TRaiCE to broaden AI-driven risk monitoring for banks.

Global Enterprise Governance, Risk And Compliance Market Report Scope

Enterprise GRC is defined as a company's coordinated strategy for managing the broad issues of corporate governance, enterprise risk management (ERM), and corporate compliance concerning regulatory requirements. The integrated collection of capabilities enables an organization to achieve objectives reliably, address uncertainty, and act with integrity.

The Enterprise Governance, Risk and Compliance Market is segmented by Type (Software, Services), Size of the Enterprise (Small and Medium Enterprise, Large Enterprise), End-user Industry (BFSI, Healthcare, Manufacturing, IT, and Telecom), and Geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The market sizes and forecasts are in terms of value (USD) for all the above segments.

| Solutions | Policy and Compliance Management |

| Audit Management | |

| Risk Management | |

| Incident Management | |

| Business Continuity and Disaster Recovery | |

| Services | Consulting |

| Integration and Implementation | |

| Training and Support |

| On-premises |

| Cloud |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing |

| IT and Telecom |

| Energy and Utilities |

| Retail and Consumer Goods |

| Government and Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Solutions | Policy and Compliance Management |

| Audit Management | ||

| Risk Management | ||

| Incident Management | ||

| Business Continuity and Disaster Recovery | ||

| Services | Consulting | |

| Integration and Implementation | ||

| Training and Support | ||

| By Deployment Model | On-premises | |

| Cloud | ||

| By Organisation Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail and Consumer Goods | ||

| Government and Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the enterprise governance risk compliance market?

The market stands at USD 23.62 billion in 2026 and is projected to reach USD 42.19 billion by 2031.

Which component segment dominates the enterprise governance risk compliance market?

Software solutions lead with 66.72% revenue in 2025, while services are growing fastest at a 12.6% CAGR.

Why is Asia-Pacific the fastest-growing region?

Rapid regulatory evolution and RegTech expansion are driving a 12.9% CAGR through 2031 in the region.

How are AI technologies reshaping GRC platforms?

Generative models now interpret regulations with 95% accuracy, automate policy updates, and cut false positives by 42%.

Page last updated on: