Enterprise Data Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

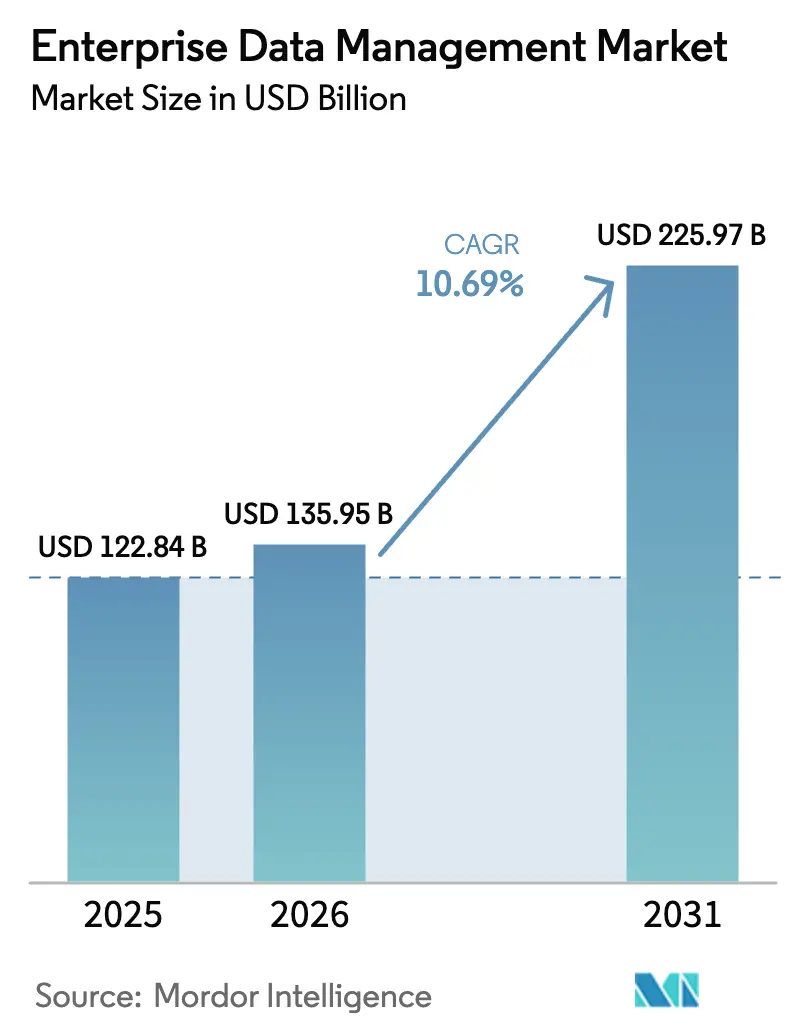

| Market Size (2026) | USD 135.95 Billion |

| Market Size (2031) | USD 225.97 Billion |

| Growth Rate (2026 - 2031) | 10.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Data Management Market Analysis by Mordor Intelligence

The enterprise data management market size was valued at USD 122.84 billion in 2025 and estimated to grow from USD 135.95 billion in 2026 to reach USD 225.97 billion by 2031, at a CAGR of 10.69% during the forecast period (2026-2031). Expansion is propelled by the convergence of AI-enabled data-fabric architectures, the rapid scale-up of cloud-native platforms, and global data-privacy mandates that elevate compliance spending. Explosive IoT and edge deployments are creating unprecedented unstructured-data volumes, forcing enterprises to prioritize modern data fabrics that automate classification, lineage, and governance. Growth also reflects a strategic pivot from reactive governance to data-as-a-product models, where sovereign-cloud requirements fragment traditional hyperscale roll-outs yet reinforce the need for unified control planes. Demand accelerates as enterprises seek to reconcile ESG audit obligations with real-time analytics, while a persistent skills shortage intensifies outsourcing toward managed service providers.

Key Report Takeaways

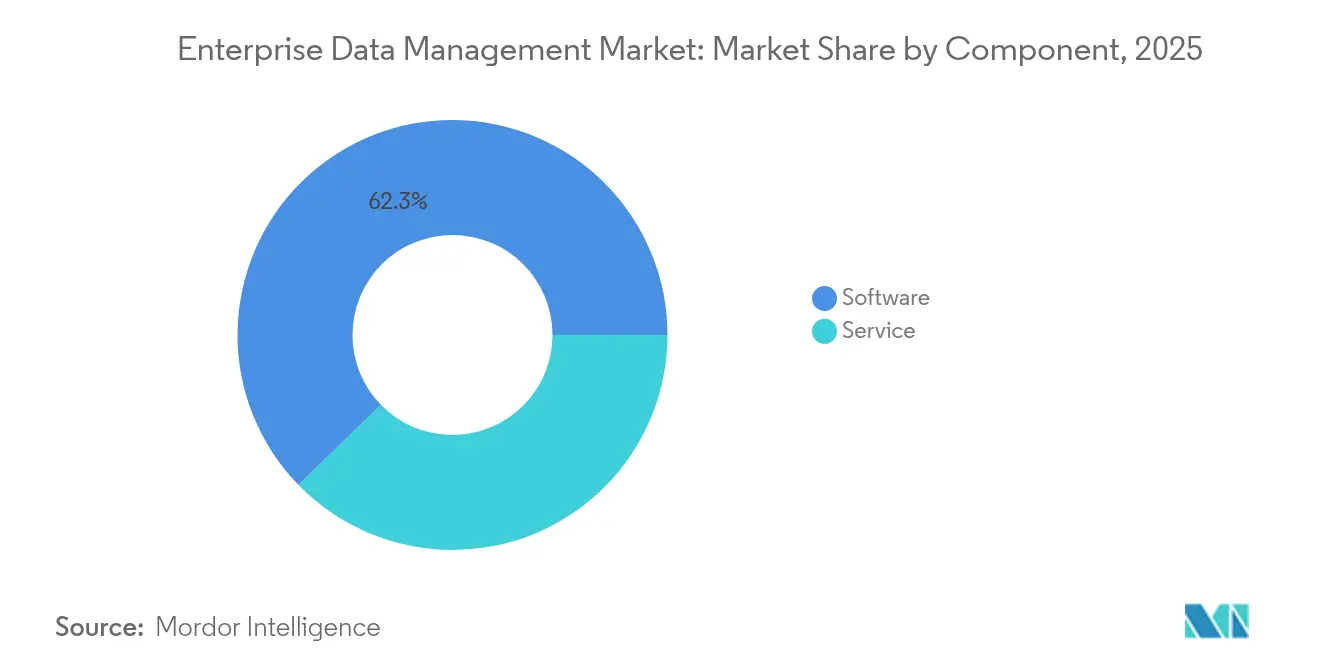

- By component, software retained 62.30% of 2025 revenue, yet services are forecast to expand at a 12.02% CAGR through 2031.

- By deployment model, on-premises installations held 55.00% of 2025 revenue, whereas cloud implementations are projected to rise at a 14.21% CAGR to 2031.

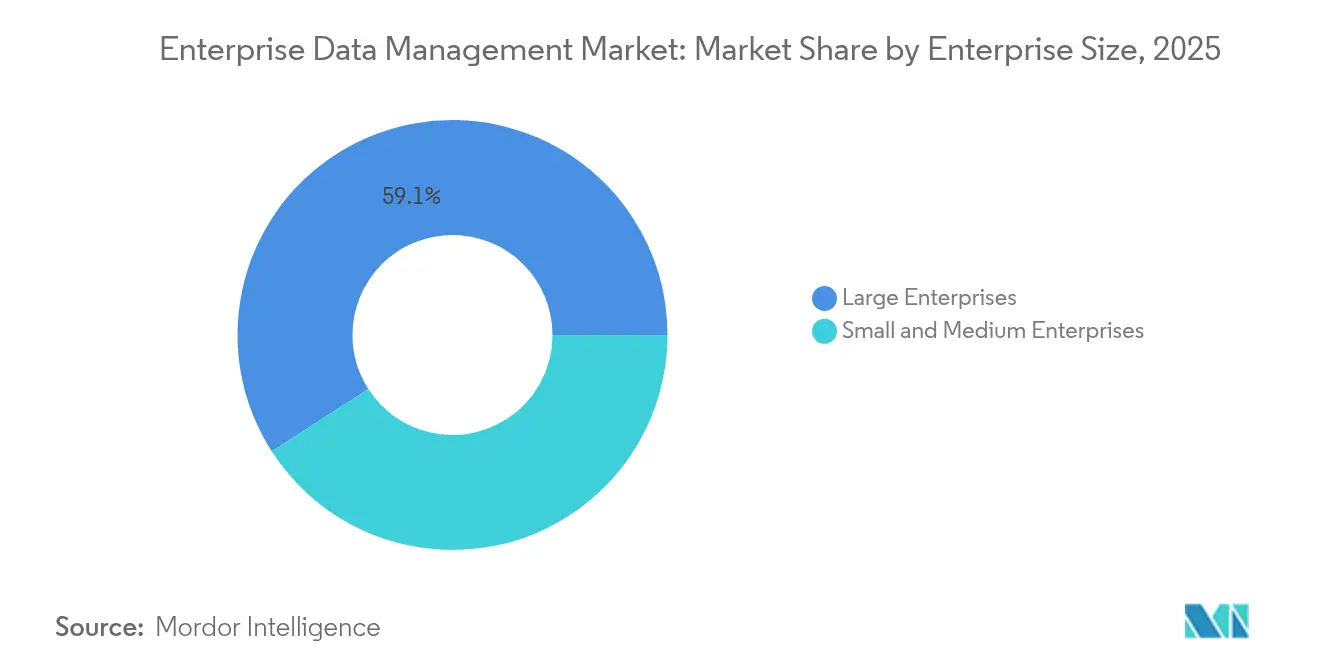

- By enterprise size, large enterprises controlled 59.10% of 2025 revenue; small and midsize firms are poised to grow at a 13.15% CAGR through 2031.

- By end-use industry, BFSI led with 28.60% of 2025 revenue, while healthcare is set to expand at a 13.52% CAGR through 2031.

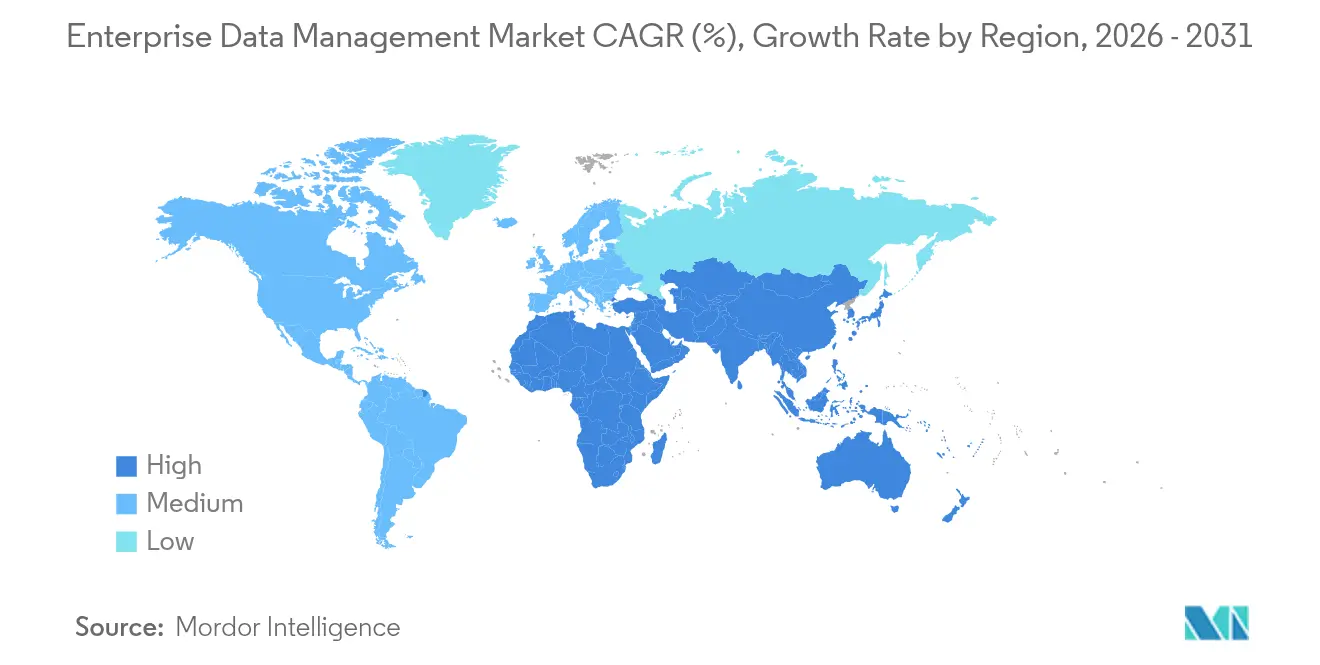

- By geography, North America commanded 33.40% of 2025 revenue; the Asia-Pacific region is projected to pace the market with a 13.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Data Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive data growth from IoT / edge devices | +2.8% | Global, led by Asia-Pacific | Medium term (2-4 years) |

| Tightening global data-privacy regulations | +2.1% | North America and EU; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Cloud-native EDM platforms accelerate time-to-value | +1.9% | Global, strongest in cloud-first regions | Short term (≤ 2 years) |

| AI-enabled data-fabric architectures cut integration cost | +1.7% | North America and EU core markets | Medium term (2-4 years) |

| ESG audit and reporting mandates boost master-data accuracy | +1.2% | EU leading; North America following | Long term (≥ 4 years) |

| Low-code platforms democratize EDM adoption for SMEs | +1.0% | Global, pronounced in emerging digital economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive data growth from IoT / edge devices

Enterprises will manage 180 zettabytes of unstructured data in 2025, with 60% of Asia-Pacific manufacturers already relying on AI models to govern edge data flows.[1]Accenture, “Sovereign Cloud: Catalyzing the Next Digital Wave,” accenture.com Real-time sensor data elevates the need for low-latency processing, prompting a 23% year-over-year rise in cloud-infrastructure spend to USD 94 billion during Q1 2025. Organizations must harmonize edge streams with core systems, accelerating adoption of AI-driven data fabrics that auto-classify and route data in compliance with sector-specific mandates.

Tightening global data-privacy regulations

The EU Corporate Sustainability Reporting Directive compels nearly 50,000 firms to disclose 800 data points beginning 2025, driving large-scale adoption of automated lineage and compliance tools. Simultaneously, SEC climate rules require third-party assurance of emissions data, extending governance complexity. Sovereign-cloud strategies have gained traction, with 37% of European enterprises already investing to maintain jurisdictional control, a figure expected to rise within two years.[2]Expereo, “Digital Silk Road Drives Asia-Pacific Edge Adoption,” expereo.com Enterprises therefore pivot to multi-cloud frameworks combined with granular policy engines that manage disparate residency laws while upholding user-privacy commitments.

Cloud-native EDM platforms accelerate time-to-value

API-first and serverless designs enable enterprises to cut integration cycles by 50%, eliminating most manual migration bottlenecks. Separation of compute and storage lets organizations scale resources on demand, while unified dataspaces such as VAST Data’s model permit real-time analytics without traditional ETL. Oracle’s cloud-infrastructure revenue rose 52% in Q4 2025 as organizations moved mission-critical workloads from on-premises to cloud-native stacks.[3]Oracle, “Q4 2025 Earnings Press Release,” oracle.com Faster deployment is increasingly essential for AI roll-outs that depend on immediate, high-quality data streams.

AI-enabled data-fabric architectures cut integration cost

As 93% of enterprise data remains unstructured, AI-driven fabrics establish a virtualized layer, enabling unified access without necessitating physical data relocation. Automated discovery and quality enforcement can reduce infrastructure cost by 30% while boosting data-quality scores by 98%. IBM’s acquisition of DataStax highlights the strategic priority of aligning unstructured and structured assets within one fabric to support emerging agentic AI workflows. This approach mitigates silo proliferation and improves ROI on multi-cloud deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of data-governance talent inflates service costs | -1.8% | Global; acute in North America and EU | Short term (≤ 2 years) |

| Complex legacy integration raises migration risk | -1.4% | North America and EU legacy-heavy markets | Medium term (2-4 years) |

| Rising sovereign-cloud demands fragment global roll-outs | -1.1% | EU leading; Asia-Pacific following | Long term (≥ 4 years) |

| Vendor lock-in fears on hyperscaler ecosystems | -0.9% | Global enterprise markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of data-governance talent inflates service costs

Sixty percent of data professionals cite skills gaps as the chief barrier to AI initiatives, and 42% report that talent scarcity degrades data quality targets. Premium salaries for AI governance, data ethics, and sovereign-cloud roles elevate consulting fees, extending project timelines. As 67% of mature organizations introduce new generative-AI roles, internal teams must upskill rapidly or cede ground to specialized providers, concentrating successful deployments within well-resourced firms.

Complex legacy integration raises migration risk

Seventy-three percent of enterprises blame incompatible formats for two-thirds of integration failures, while hidden dependencies can inflate project budgets by 40%. Regulated sectors must perform extensive validation, lengthening timelines beyond acceptable thresholds. Cultural resistance also emerges when decades-old business logic embedded in mainframes needs reinterpretation, complicating change-management programs and elevating the probability of disruption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services outpace software as outsourcing accelerates

Software contributed 62.30% of 2025 revenue, underlining its foundational role in data integration, master-data, and security platforms that anchor the enterprise data management market. Yet services will post a 12.02% CAGR through 2031 as enterprises confront rising complexity and use managed expertise to mitigate internal skills gaps. The shift reflects a preference for outcome-based engagements that guarantee regulatory compliance and uptime. Professional services targeting AI integration and sovereign-cloud configuration are in greatest demand, while managed offerings for real-time data quality monitoring gain traction. This pivot from ownership to consumption dovetails with the finding that 60% of data leaders identify skills shortages as a primary obstacle, a gap that service partners readily fill.

Providers now deliver bundled platforms that unite advisory, implementation, and run-time support, reinforcing retention and expanding wallet share. Within software, security and master-data modules show resilient growth as privacy laws tighten, whereas traditional ETL tools morph into AI-enabled constructs that auto-generate integration pipelines. The component mix suggests continued movement toward cloud-delivered, micro-service architectures that can be orchestrated by external specialists, further fueling outsourced-services momentum.

By Deployment Model: Hybrid sovereignty reshapes cloud strategy

On-premises estates still accounted for 55.00% of the enterprise data management market share in 2025, yet the cloud track will grow 14.21% annually to 2031 as organizations seek elasticity and lower time-to-value. Data sovereignty weighs heavily: 88% of large companies rate jurisdictional control as business-critical, spurring interest in sovereign clouds that blend local control with hyperscale economics. As a result, workload placement is becoming dynamic; sensitive records remain on-premises or within sovereign zones, while analytical sandboxes migrate to low-latency public-cloud regions. Hybrid orchestration platforms that enforce common governance policies across locations have become a core purchase criterion.

Vendor lock-in fears further encourage multi-cloud architectures. Eighty-three percent of enterprises planned workload repatriation from public clouds in 2024, up sharply from 43% in 2020. This necessitates flexible data fabrics that span diverse environments without disrupting lineage or security controls, explaining the surge in fabric-centric roadmaps among leading vendors.

By Enterprise Size: Low-code tools unlock SME participation

Large enterprises held 59.10% of 2025 revenue thanks to scale, dedicated data teams, and sizable compliance budgets. However, small and midsize enterprises (SMEs) will outpace with a 13.15% CAGR through 2031. Low-code and no-code platforms abstract data pipelines behind intuitive interfaces, allowing non-specialists to build governance routines. Subscription pricing further eases adoption, eliminating capital barriers that once restricted SME entry. Vendors are packaging simplified editions that preserve core lineage, catalog, and quality functions while reducing configuration overhead, fostering rapid deployment cycles measured in weeks rather than months.

Meanwhile, large enterprises shift focus to optimization, consolidating disparate tools into unified control planes and embedding AI to automate quality checks. They also pilot sovereign-cloud blueprints to satisfy cross-border compliance. The divergent priorities of SMEs and large firms ensure sustained demand across the value chain from streamlined SaaS suites to bespoke advisory engagements.

By End-Use Industry: Healthcare climbs fastest under privacy pressure

Financial services retained 28.60% of 2025 revenue, supported by trade surveillance, risk analytics, and stringent capital-market reporting mandates. Healthcare will chart the highest growth at 13.52% CAGR to 2031, propelled by HIPAA, GDPR, and state-level privacy laws that require auditable lineage for patient data. Telehealth expansion since the pandemic multiplied data volumes, adding impetus for modern master-data systems that unify clinical, operational, and research datasets. Manufacturing maintains steady investment to enable predictive maintenance and quality analytics across Industry 4.0 lines, while retail prioritizes personalization and supply-chain resilience.

Healthcare providers increasingly demand zero-trust architectures that encrypt data in motion and at rest while enabling real-time clinician access. Vendors able to demonstrate certified compliance, automated anonymization, and AI-ready data fabrics stand to capture outsized share of new deployments.

Geography Analysis

North America led with 33.40% of 2025 revenue, leveraging advanced regulatory frameworks and early cloud-native adoption across finance and technology. Enterprises allocate significant budgets to comply with SEC climate disclosures and state privacy laws, spurring demand for integrated governance suites. Europe follows closely, its growth anchored in GDPR enforcement and a rapid pivot to sovereign-cloud constructs; 37% of regional enterprises already run sovereign instances, with more to come as the EU embeds digital-sovereignty objectives in policy planning.

Asia-Pacific, however, will exhibit the strongest expansion at 13.42% CAGR through 2031, underpinned by massive investments in data centers and the Digital Silk Road program that broadens regional connectivity. Manufacturing and telecom spending dominate, striving to harness edge-generated data for AI-enabled applications.

The Middle East and Africa show steady but smaller growth, reflecting nascent regulatory regimes and ongoing infrastructure development. Latin America’s momentum is tied to open-banking regulations and e-commerce growth that escalate real-time data-management requirements. Collectively, these patterns underscore a multipolar landscape where localized regulations, data-residency rules, and infrastructure maturity shape deployment decisions, driving the need for globally consistent yet regionally adaptable platforms.

Competitive Landscape

The market remains moderately concentrated. Oracle, IBM, SAP, and Microsoft continue to leverage end-to-end platforms and active acquisition pipelines. Oracle’s cloud revenue climbed 27% year-on-year to USD 6.7 billion in fiscal 2025, reflecting demand for integrated database-to-application stacks. Salesforce reinforced its positioning through an USD 8 billion Informatica acquisition that folds advanced data-integration and governance functions into its CRM ecosystem. IBM’s USD 6.4 billion purchase of HashiCorp highlights the strategic priority of automating multi-cloud configuration at scale.

Challengers such as Snowflake, Collibra, Alation, and Confluent concentrate on high-growth niches data lakehouses, data catalogs, and streaming platforms offering open architectures that minimize lock-in. Interoperability has become a decisive factor; enterprises routinely evaluate whether a vendor’s AI-governance roadmap aligns with existing security postures and sovereign-cloud requirements.

Competitive differentiation thus hinges on embedding generative-AI assistants that reduce manual stewardship, ecosystem partnerships that certify plug-and-play integrations, and flexible consumption models that adjust to unpredictable data volumes.

Enterprise Data Management Industry Leaders

Oracle Corporation

Amazon Web Services Inc.

Informatica Inc.

SAP SE

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: IBM introduced the Transformation Suite for SAP Applications, automating technical assessment and data migration to shorten S/4HANA projects.

- June 2025: Sema4.ai secured USD 25 million in Series A-extension funding to scale its AI-agent platform integrated with Snowflake Marketplace.

- April 2025: Huawei unveiled its AI Data Lake Solution, uniting storage, governance, and AI toolchains to accelerate analytics workloads.

- January 2025: Prophecy raised USD 47 million in Series B1 to enhance AI-driven data-integration software for cloud migrations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the enterprise data management market as the full stack of software and related managed services that ingest, cleanse, secure, store, integrate, and govern structured, semi-structured, and unstructured data generated inside an organization across on-premise and cloud estates, enabling compliant analytics and operational decision-making. According to Mordor Intelligence, value estimates are presented in USD and track revenues earned by vendors supplying these capabilities to business customers worldwide.

Scope exclusion: consumer-grade file-sync tools and stand-alone business-intelligence applications are not counted.

Segmentation Overview

- By Component

- Software

- Data Security

- Master Data Management

- Data Integration and ETL

- Data Warehousing

- Data Migration

- Metadata Management

- Data Quality and Stewardship

- Services

- Professional Services

- Managed Services

- Software

- By Deployment Model

- On-Premises

- Cloud

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End-Use Industry

- IT and Telecommunication

- Healthcare and Life Sciences

- Retail and E-commerce

- Manufacturing

- Government and Public Sector

- Energy and Utilities

- Education

- Other End-Use Industry

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview chief data officers, cloud-platform partners, and system integrators in North America, Europe, and Asia-Pacific. These conversations validate adoption triggers, average selling prices, and deployment shifts that secondary data alone cannot surface, helping us refine assumptions before numbers are frozen.

Desk Research

We start with authoritative public datasets such as OECD digital-economy indicators, NIST cyber-security guidelines, EU GDPR enforcement statistics, and regional ICT spending tables from the World Bank. Company 10-Ks, investor decks, and trade-association white papers supplement usage metrics, while paid platforms including D&B Hoovers and Dow Jones Factiva give us granular vendor revenue splits and recent deal news. This mosaic lets us map the demand pool and calibrate vendor coverage across regions and industries. The sources cited above are illustrative; many additional references were consulted during data collection and cross-checking.

Market-Sizing & Forecasting

We rebuild the market top-down by reconciling global enterprise IT expenditure with data-management spending ratios, adjusted for cloud penetration and regulated-industry intensity, and then benchmark the totals with selective bottom-up roll-ups from sampled vendor revenues and channel checks. Key variables feeding the model include average data-storage volume per employee, price per terabyte, number of compliance actions, share of workloads on public cloud, and industry GDP outlook. A multivariate-regression forecast projects each driver five years out; scenario analysis tests high-regulation and low-price cases, and gaps in bottom-up inputs are smoothed with median proxy values agreed during expert calls.

Data Validation & Update Cycle

Outputs pass a senior-analyst review, anomaly flags trigger re-contact of sources, and variance versus historical series is capped within predefined bounds. The model refreshes annually, with interim updates if sizable regulatory or technology events shift demand.

Why Our Enterprise Data Management Baseline Commands Reliability

Published values often diverge because firms pick different component mixes, convert currencies on separate dates, or extrapolate older baselines.

Key gap drivers include inclusion of only software revenues, omission of managed services, aggressive cloud-price deflation assumptions, or reliance on pre-pandemic benchmarks that under-represent today's data-governance spend.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 122.84 B (2025) | Mordor Intelligence | |

| USD 110.53 B (2024) | Global Consultancy A | narrower component coverage and earlier base year |

| USD 101.04 B (2024) | Industry Publisher B | excludes managed services and samples top vendors only |

| USD 77.90 B (2020) | Regional Consultancy C | legacy baseline and conservative cloud uptake assumption |

Taken together, the comparison shows that Mordor's disciplined scope, fresh baseline year, and blended top-down-bottom-up modeling deliver a balanced, transparent market view that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

How big is the Enterprise Data Management Market?

The Enterprise Data Management Market size is expected to reach USD 135.95 billion in 2026 and grow at a CAGR of 10.69% to reach USD 225.97 billion by 2031.

What is the current size of the enterprise data management market?

The enterprise data management market is valued at USD 135.95 billion in 2026 and is forecast to reach USD 225.97 billion by 2031.

Which segment is growing fastest within the enterprise data management market?

Services are expanding at a 12.02% CAGR as organizations outsource expertise to manage rising governance complexity.

Why is healthcare adopting enterprise data management platforms rapidly?

Healthcare faces stringent patient-privacy regulations and growing telehealth data volumes, driving a 13.52% CAGR for EDM solutions in the sector. is estimated to grow at the highest CAGR over the forecast period (2026-2031).

How do data-privacy regulations affect deployment models?

Tightening laws encourage hybrid and sovereign-cloud strategies so that sensitive data remains within jurisdictional boundaries while still leveraging cloud scalability.

What technologies most reduce data-integration costs?

AI-enabled data fabrics virtualize access to disparate sources, lowering integration costs by connecting data without physical movement and automating quality checks.

Page last updated on: