Enterprise Backup And Recovery Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 10.63 Billion |

| Market Size (2030) | USD 16.86 Billion |

| Growth Rate (2025 - 2030) | 9.67% CAGR |

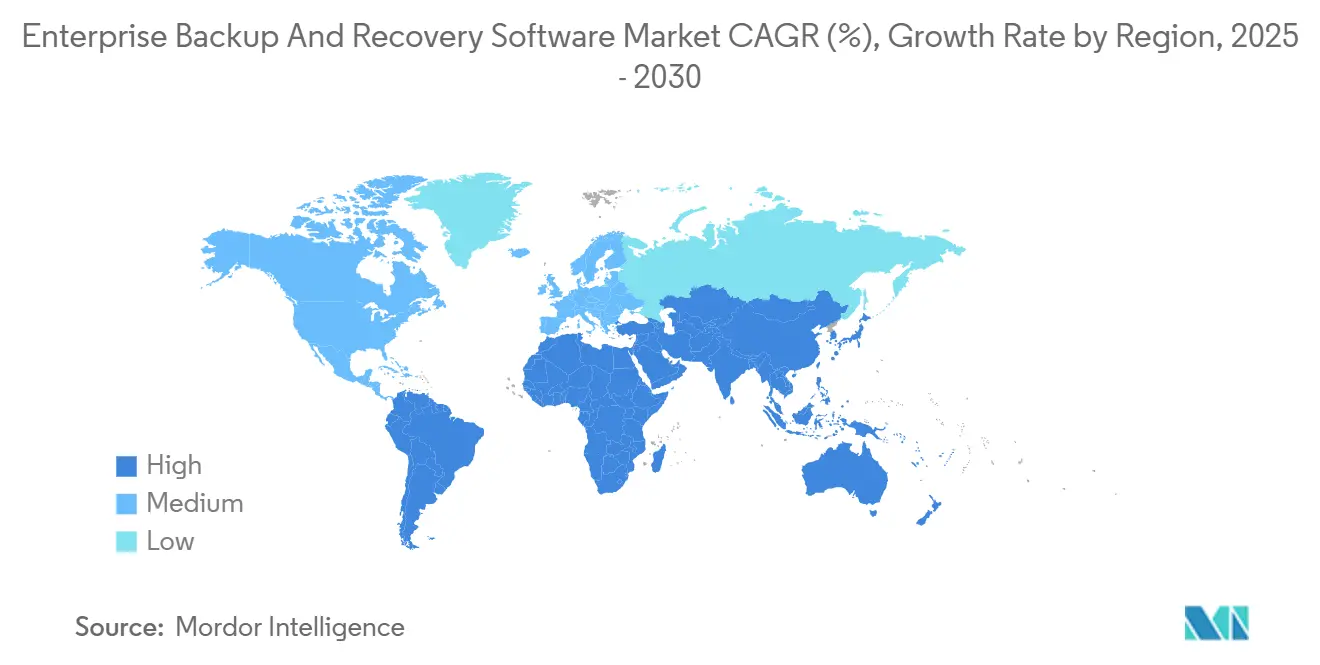

| Fastest Growing Market | South America |

| Largest Market | North America |

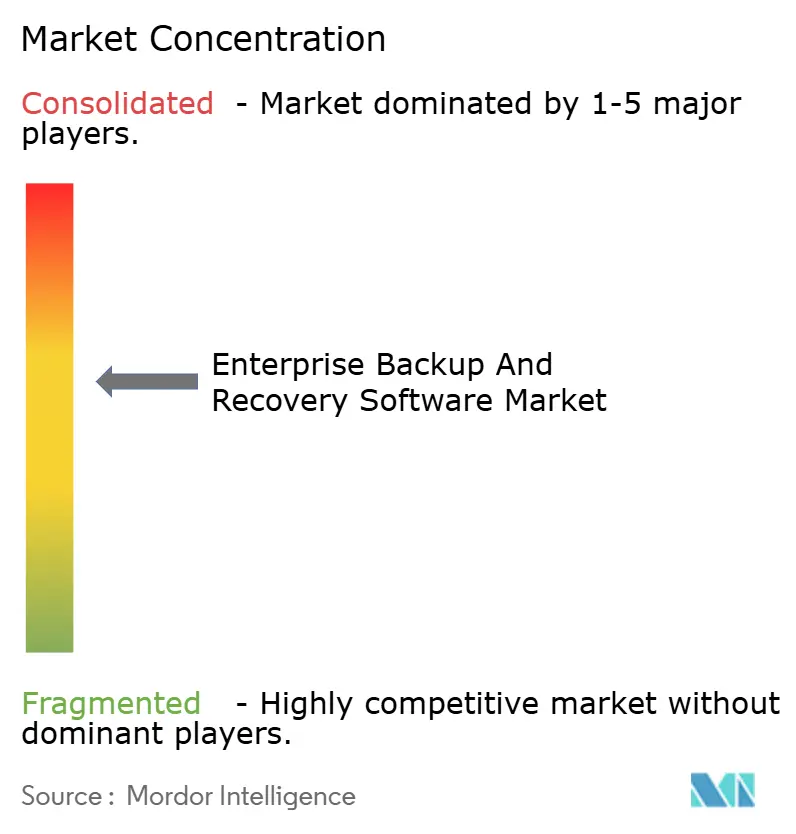

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Backup And Recovery Software Market Analysis by Mordor Intelligence

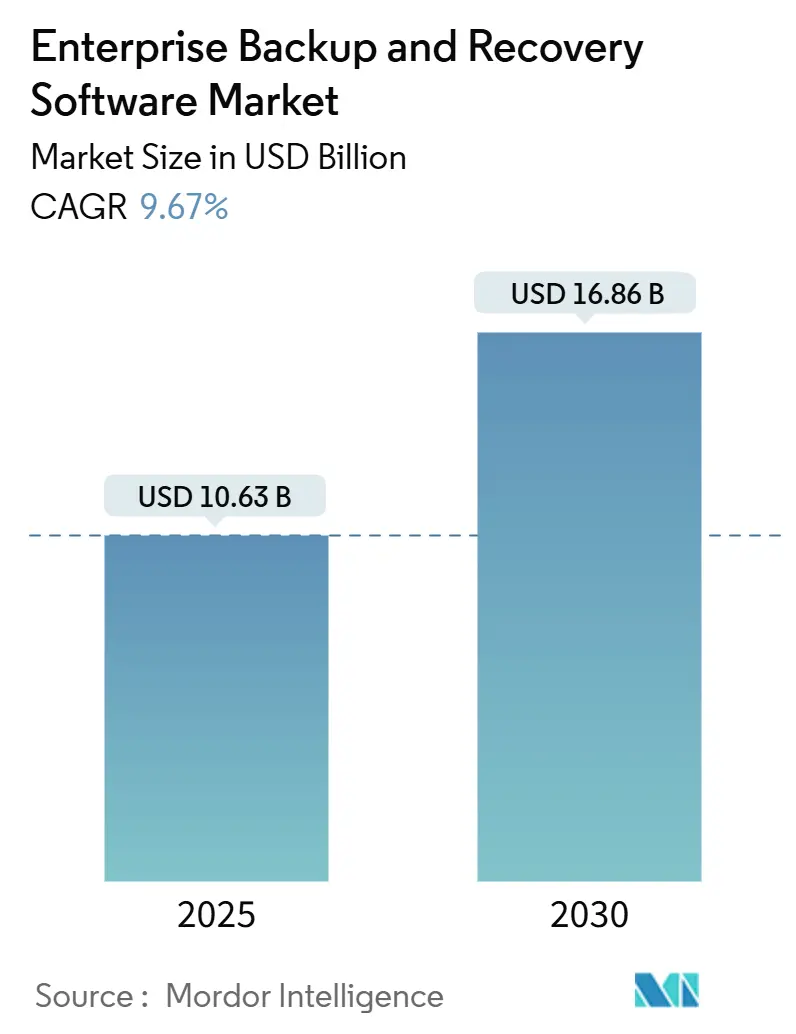

The enterprise backup and recovery software market size is valued at USD 10.63 billion in 2025 and is forecast to reach USD 16.86 billion by 2030, expanding at a 9.67% CAGR. Heightened ransomware-as-a-service activity that inflicted USD 57 billion damage across enterprises in 2024 is compelling organizations to harden backup architectures with immutable, air-gapped copies. Convergence of SecOps and DevOps is normalizing policy-as-code deployments that blend backup workflows into CI/CD pipelines, accelerating hybrid and multi-cloud adoption. Regulatory actions such as Europe’s Digital Operational Resilience Act (DORA) and India’s DPDP Act mandate tamper-proof recovery copies, redirecting capital toward write-once-read-many storage. Competitive intensity is rising as cloud-native disruptors tap public markets, while established vendors bolster portfolios with AI-driven cyber-resilience. Together, these trends amplify spending on the enterprise backup and recovery software market for both large enterprises and agile small and medium enterprises.

Key Report Takeaways

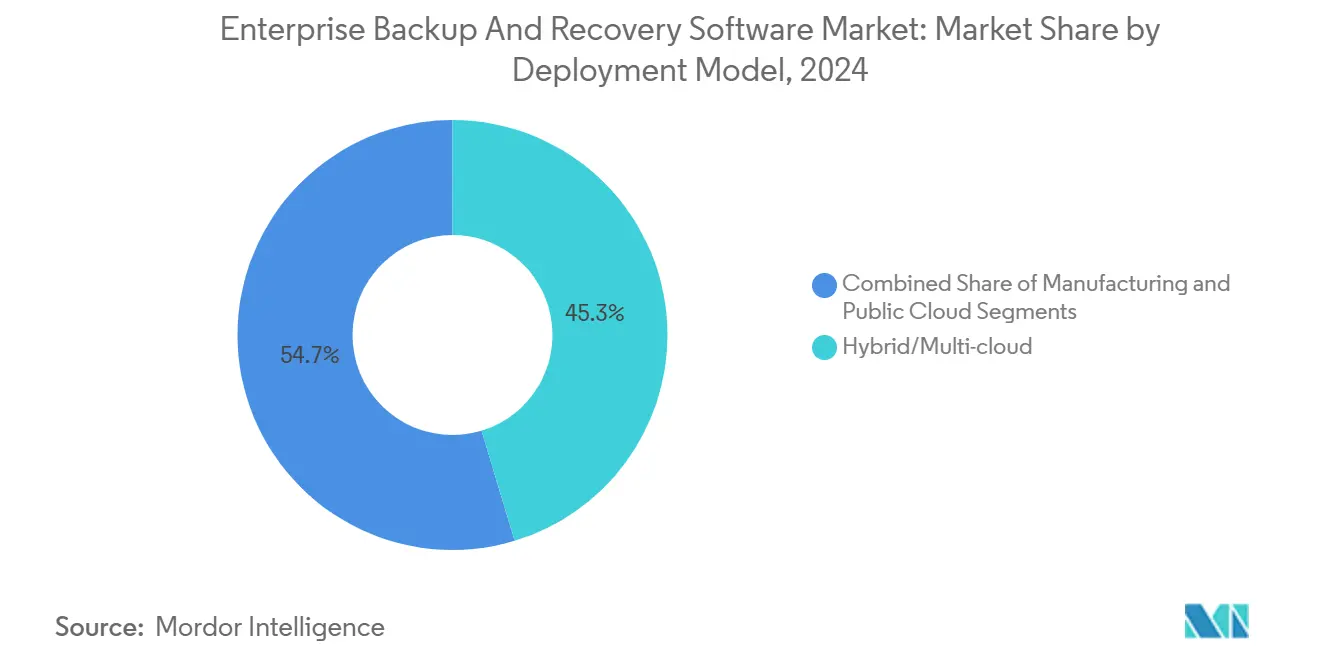

- By deployment model, hybrid and multi-cloud configurations held 45.32% of the enterprise backup and recovery software market share in 2024; public-cloud deployments are projected to expand at a 10.76% CAGR through 2030.

- By organization size, large enterprises accounted for 63.39% revenue share in 2024, while small and medium enterprises are advancing at an 11.24% CAGR to 2030.

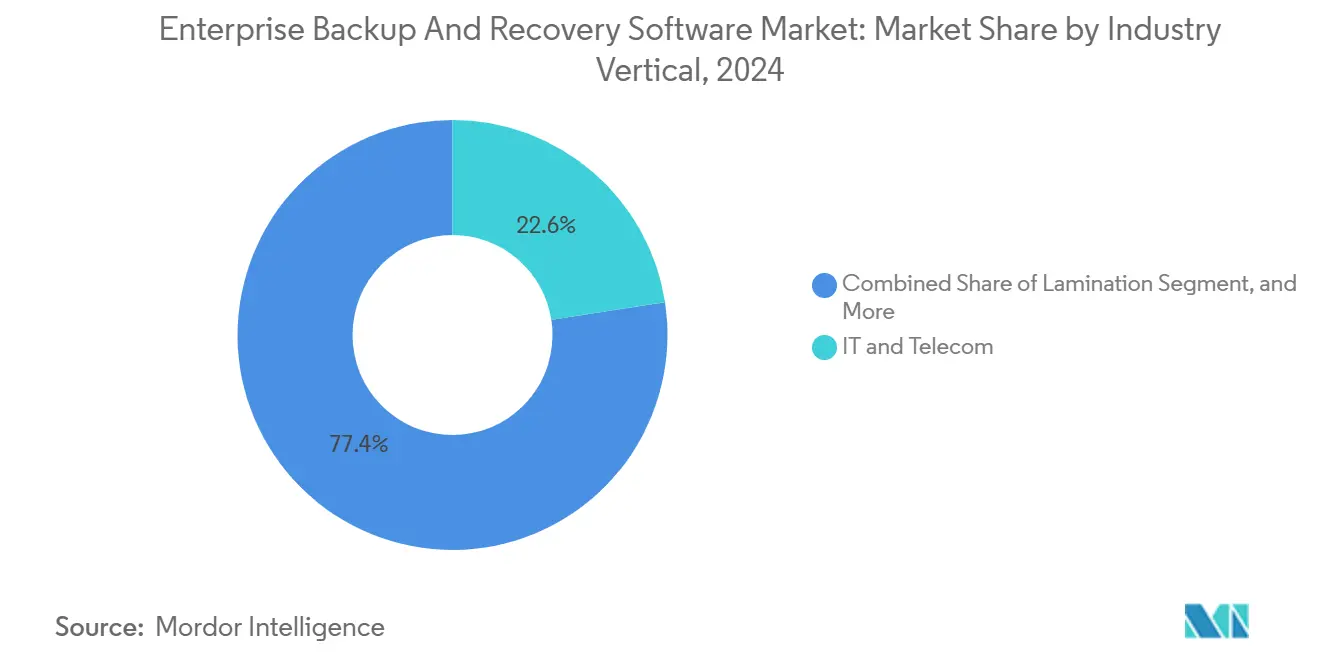

- By industry vertical, IT and telecommunications captured 22.57% of the enterprise backup and recovery software market size in 2024; banking, financial services, and insurance is registering the fastest 9.89% CAGR through 2030.

- By backup type, incremental methods led with a 38.46% share of the enterprise backup and recovery software market size in 2024, whereas continuous data protection is growing at a 10.14% CAGR over the same period.

- By geography, North America dominated with 37.71% market share in 2024, and South America is forecast to record the highest 9.97% CAGR through 2030.

Global Enterprise Backup And Recovery Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ransomware-as-a-Service escalates frequency and cost of attacks | +2.8% | Global, highest in North America and Europe | Short term (≤ 2 years) |

| SecOps/DevOps convergence drives automated backup workflows | +1.9% | North America and Asia-Pacific core, spill-over to Europe | Medium term (2-4 years) |

| Cloud-first strategies accelerate Backup-as-a-Service adoption | +2.1% | Global, early gains in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Regulatory surge (DORA, DPDP Act, NIS2) mandates immutable copies | +1.6% | Europe and Asia-Pacific primarily | Long term (≥ 4 years) |

| AI-generated data volumes strain legacy backup windows | +1.4% | Global, concentrated in tech-forward markets | Long term (≥ 4 years) |

| Low-cost object storage tiers enable near-instant recovery copies | +1.2% | Global, cloud-mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ransomware-as-a-Service Escalates Frequency and Cost of Attacks

The industrialization of ransomware, delivered as turnkey subscription kits, elevated enterprise attack frequency by 41% during 2024. Adversaries increasingly target backup infrastructure to extend downtime leverage, as witnessed in Ascension’s 140-hospital disruption that exposed gaps in traditional vaulting. [1]TechCrunch Staff, “Ascension Health Cyberattack Hospitals,” TechCrunch, techcrunch.com Boards now mandate 3-2-1-1 frameworks that include an immutable offline copy, enabling recovery paths even when primary repositories are encrypted. Incidents where backups stay intact record USD 1.76 million average recovery cost versus USD 4.88 million when compromised, sharpening ROI visibility for upgraded resilience. Consequently, IT budgets earmarked for air-gapped appliances and zero-trust backup networks are expanding, elevating spend across the enterprise backup and recovery software market.

SecOps/DevOps Convergence Drives Automated Backup Workflows

Tight coupling of security operations and development pipelines is reshaping how policies are authored, versioned, and enforced. [2]Shivank Gupta, “The Future of Data Protection: How AI and Automation Are Transforming Backup and Recovery,” Commvault Blog, commvault.com Policy-as-code constructs embed backup definitions alongside infrastructure-as-code, letting new microservices inherit protection automatically during GitOps deployments. Financial institutions now halt releases if automated restore tests fail in CI/CD gates, shortening mean time to recovery by 67% and cutting backup-related incidents by 43%. Vendors respond with APIs and Terraform modules that align with DevSecOps toolchains, fueling demand for event-driven orchestration embedded in the enterprise backup and recovery software market.

Cloud-first Strategies Accelerate Backup-as-a-Service Adoption

Consumption-based pricing and elastic capacity are persuading cost-sensitive buyers to retire on-premises tape libraries. Case in point, SoFi trimmed total cost of ownership 40% after migrating to Druva’s cloud-native platform. Small and medium enterprises, previously constrained by CapEx hurdles, now represent the fastest-growing cohort at 11.24% CAGR, outpacing large enterprise spend. Hyperscale ecosystems embed cross-region replication and SLA-based restore targets that deliver 99.9% availability. These economics underpin continued expansion of the enterprise backup and recovery software market as organizations modernize data-protection stacks.

Regulatory Surge Mandates Immutable Copies

Legislators increasingly stipulate technical controls rather than procedural checklists. Europe’s DORA compels financial entities to maintain tamper-proof backups with specified retention windows. [3]European Banking Authority, “Digital Operational Resilience Act,” eba.europa.eu Banks invested EUR 2.3 billion (USD 2.6 billion) in 2024 alone to deploy WORM storage and cryptographic integrity verification layers. Similar mandates in India and Singapore expand the regulatory envelope, pressuring enterprises to adopt immutable architectures across all jurisdictions. Compliance-driven refresh cycles notably uplift revenue trajectories for the enterprise backup and recovery software market over the long term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising egress fees inflate multi-cloud recovery TCO | −1.4% | Global, multi-cloud environments | Short term (≤ 2 years) |

| Backup data sprawl complicates compliance auditability | −0.9% | Global, regulated industries | Medium term (2-4 years) |

| Skilled-talent shortage delays cyber-resilient architecture rollout | −1.1% | Global, acute in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Legacy tape/system inertia in highly regulated on-prem industries | −0.8% | North America and Europe, some Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Egress Fees Inflate Multi-cloud Recovery TCO

Hyperscale providers levy USD 0.09–0.12 per GB outbound, translating to monthly bills above USD 100,000 for petabyte-scale repositories exercising cross-cloud restores. Enterprises report 30–40% of total backup costs tied to egress during disaster events, forcing reevaluation of multi-cloud resilience. Some consolidate around a single cloud, while others deploy on-premises caches to curtail large data pulls. New entrants offering zero-egress tiers try to disrupt this dynamic but often lack integrated ecosystems, widening the gap between cost optimization and functional robustness.

Backup Data Sprawl Complicates Compliance Auditability

Organizations juggle an average of 7.3 backup platforms spanning SaaS, on-premises, and edge footprints. Fragmented repositories impede evidence gathering for audits such as HIPAA or GDPR, consuming up to 40% compliance team bandwidth. Locating data for right-to-be-forgotten requests stretches weeks, risking fines and customer dissatisfaction. Vendors now ship centralized metadata catalogs and AI-assisted discovery to tame heterogeneity, but integration complexity persists as a drag on the enterprise backup and recovery software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Dominance Balances Control and Scale

Hybrid and multi-cloud configurations accounted for 45.32% of the enterprise backup and recovery software market in 2024, reflecting the preference to blend on-premises sovereignty with cloud elasticity. Public-cloud deployments, while smaller today, are projected to log a 10.76% CAGR through 2030, driven by subscription economics and global reach. On-premises models persist in regulated arenas yet increasingly interlink with cloud tiers for cold retention. This orchestration raises the enterprise backup and recovery software market size allocated to intelligent data-placement software that triggers restores from the most proximate source. Institutions such as Nasdaq report 23% faster recovery after adopting cohesive hybrid designs. Enlarging AI-powered placement logic further optimizes cost and compliance, widening competitive gaps.

Advancements in SaaS connectors, Kubernetes hooks, and object-storage tiers strengthen hybrid stickiness. Vendors emphasize low-latency snapshot shipping, immutable cloud vaults, and policy inheritance across environments. As data-sovereignty rules tighten, enterprises shift from binary deployment choices to fine-grained workload placement, cementing hybrid architectures as the strategic default. Consequently, the enterprise backup and recovery software market continues pivoting toward platforms fluent in orchestration rather than static repositories.

By Organization Size: SME Velocity Outstrips Enterprise Volume

Large enterprises commanded 63.39% revenue share in 2024 owing to complex estates and sizable budgets. Yet SMEs clocked an 11.24% CAGR, fueled by SaaS backup platforms that mask infrastructure complexity. Because subscription tiers scale down well, advanced features such as global deduplication and immutable snapshots now reach smaller IT teams. This democratization pushes vendors to craft pricing granularity and automated onboarding, enlarging the enterprise backup and recovery software market reach among resource-constrained buyers.

Large enterprises remain innovation incubators, steering demand for cross-cloud orchestration and compliance automation. Their requirements drive feature roadmaps in areas like unified policy engines and ML-driven anomaly detection. Meanwhile, SMEs value out-of-the-box integrations with Microsoft 365 and Google Workspace. As portfolios converge, multi-tenant architectures capable of stretching from a handful of virtual machines to exabyte-scale domains will dominate the enterprise backup and recovery software market.

By Industry Vertical: Finance Accelerates Under Regulatory Spotlight

IT and telecom led revenue at 22.57% in 2024, mirroring early adoption of cloud workloads. Banking, financial services, and insurance exhibit the fastest 9.89% CAGR as institutions embed cyber-resilience into operational-risk models. Financial regulators demand immutable, periodically tested backups, catalyzing deep investment. Healthcare trails with heightened urgency around patient-safety imperatives and HIPAA penalties. Manufacturing revisits cyber-physical resilience after high-profile supply-chain attacks; Norsk Hydro’s disruption amplified awareness of operational-technology backups.

Retail and e-commerce deploy continuous data protection to safeguard transaction pipelines during seasonal surges. Government agencies opt for hybrid retention that rings secure on-premises nodes with cloud-based cold data lakes. Each vertical’s nuanced needs diversify the enterprise backup and recovery software market, compelling vendors to ship verticalized templates for policy and reporting.

By Backup Type: Continuous Protection Gains Traction

Incremental backups held 38.46% share in 2024 due to storage efficiency balanced with point-in-time recovery. Continuous data protection grows fastest at 10.14% CAGR as tolerance for data loss narrows in financial and healthcare scenarios. Full backups remain mandated for quarterly compliance images but leverage deduplication to mute capacity spikes. Differential strategies serve environments with predictable change rates but face displacement by smarter AI-driven scheduling.

Modern platforms blur legacy categories, dynamically selecting incremental, differential, or near-real-time replication according to workload behavior. AI engines profile data-change velocity and align protection levels with criticality, lifting operational agility. Accordingly, continuous protection’s share of the enterprise backup and recovery software market is poised for steady gains as organizations chase sub-minute recovery points without penalizing storage budgets.

Geography Analysis

North America led with 37.71% of enterprise backup and recovery software market revenue in 2024, underpinned by stringent cyber-insurance requirements and a robust vendor ecosystem. Investments spiked after the Colonial Pipeline incident, prompting energy and utilities to embed immutable vaulting in resilience plans. Venture-capital inflows continue to feed innovation clusters around Silicon Valley and Austin, ensuring rapid commercialization of AI-driven backup analytics.

Europe shows accelerated uptake as GDPR, NIS2, and DORA synchronize regional resilience standards. Financial institutions lead spending, often building multi-site clusters within EU borders to fulfill data-sovereignty clauses. Vendors tailor offerings with sovereign-cloud options and audit-ready reporting templates, increasing the enterprise backup and recovery software market size allocated to compliance automation tools.

Asia-Pacific advances on the back of India’s 950 MW data-center build-out and Japan’s appetite for integrated appliances. Regulators in Singapore and Australia release updated cyber-resilience advisories that reference immutable backups, stimulating procurement cycles. South America registers the fastest 9.97% CAGR, catalyzed by Microsoft’s USD 2.7 billion Brazilian cloud expansion and Google’s USD 1.8 billion commitment. Middle East and Africa see emerging demand, especially among Gulf banking groups modernizing disaster-recovery regimes.

Competitive Landscape

The enterprise backup and recovery software market reflects moderate fragmentation with a tilt toward consolidation. Veeam retained leadership while reaching a USD 15 billion valuation, illustrating investor confidence in platform breadth. Rubrik’s USD 5.6 billion IPO and Cohesity’s USD 7 billion private valuation spotlight appetite for cloud-native disruptors. Traditional suppliers such as Veritas and Commvault pursue AI-infused optimization, using anomaly detection to cut storage costs by 30% and speed ransomware recovery.

Strategic tie-ups with hyperscale providers shape product roadmaps. Cohesity deepened Google Cloud integration to protect Workspace and GCP instances, widening hybrid coverage. Veeam acquired Alcion to strengthen Microsoft 365 protection, acknowledging the SaaS workload surge. Start-ups emphasizing zero-egress object storage lure cost-sensitive buyers, although limited ecosystems temper uptake.

AI and data-management convergence emerge as principal differentiators. Platforms now classify sensitive data, orchestrate lifecycle retention, and visualize recovery readiness in unified consoles. Edge and operational-technology backups constitute a white-space opportunity as manufacturing and energy groups require bandwidth-optimized inbound vaulting. Vendors capable of collapsing backup, disaster recovery, and governance into a single control plane are likely to capture incremental enterprise backup and recovery software market share.

Enterprise Backup And Recovery Software Industry Leaders

Veeam Software AG

Commvault Systems, Inc.

Veritas Technologies LLC

Rubrik, Inc.

Cohesity, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cohesity expanded its Google Cloud partnership to offer native protection for Google Workspace and GCP workloads.

- December 2024: Rubrik completed an IPO, raising USD 752 million at a USD 5.6 billion valuation.

- November 2024: Veeam acquired Alcion, adding advanced Microsoft 365 backup features.

- October 2024: Commvault launched AI-powered Cloud Rewind for automated ransomware detection and recovery.

Global Enterprise Backup And Recovery Software Market Report Scope

| On-premises |

| Public Cloud |

| Hybrid / Multi-cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Manufacturing |

| Retail and e-Commerce |

| Full |

| Incremental |

| Differential |

| Continuous Data Protection (CDP) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment Model | On-premises | ||

| Public Cloud | |||

| Hybrid / Multi-cloud | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Industry Vertical | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Government and Public Sector | |||

| Manufacturing | |||

| Retail and e-Commerce | |||

| By Backup Type | Full | ||

| Incremental | |||

| Differential | |||

| Continuous Data Protection (CDP) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the enterprise backup and recovery software market in 2025?

The enterprise backup and recovery software market size stands at USD 10.63 billion in 2025 with a 9.67% CAGR outlook through 2030.

Which deployment model is gaining fastest traction?

Public-cloud backup-as-a-service shows the highest growth, expanding at a 10.76% CAGR as organizations shed on-premises infrastructure.

What is driving adoption in the financial sector?

Stringent regulations such as DORA and escalating ransomware threats push banks to deploy immutable, frequently tested backup architectures.

Why are egress fees a concern for multi-cloud strategies?

Cross-cloud restore events can trigger data-transfer costs of USD 0.09–0.12 per GB, inflating recovery TCO by 30–40% during major incidents.

Which backup type is projected to grow quickest?

Continuous data protection is forecast to grow at a 10.14% CAGR owing to demand for near-zero recovery points in critical workloads.

How fragmented is vendor competition?

Market concentration is moderate; the top five suppliers hold around 60% share, and recent IPOs are intensifying rivalry.

Page last updated on: