Backup-as-a-Service (BaaS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

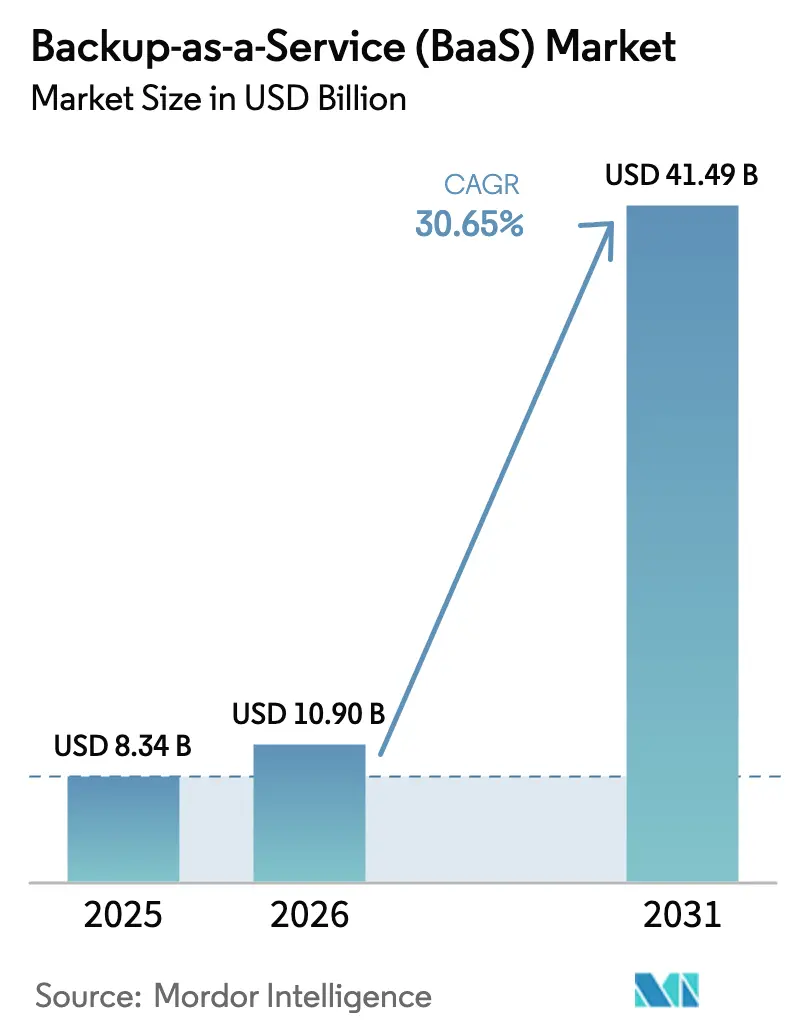

| Market Size (2026) | USD 10.9 Billion |

| Market Size (2031) | USD 41.49 Billion |

| Growth Rate (2026 - 2031) | 30.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Backup-as-a-Service (BaaS) Market Analysis by Mordor Intelligence

The Backup-as-a-Service market size is expected to grow from USD 8.34 billion in 2025 to USD 10.9 billion in 2026 and is forecast to reach USD 41.49 billion by 2031 at 30.65% CAGR over 2026-2031. Demand accelerates as ransomware attempts now probe the integrity of 94% of corporate backup environments, leading enterprises to mandate cloud-native, immutable protection architectures. Convergence of backup and disaster-recovery functions is reshaping buying criteria, with 88% of organizations planning DRaaS adoption inside 24 months. Public-cloud deployments still dominate, yet sovereignty requirements and rising egress fees are pushing more workloads toward private-cloud BaaS platforms. Financial-services, retail, and manufacturing firms are scaling edge-to-core protection to cover operational data sets, while AI-driven optimization increasingly differentiates vendors that can cut storage footprint and speed up recovery analytics. Competitive intensity has risen sharply after Cohesity closed its Veritas data-protection acquisition, creating a USD 1.7 billion-revenue leader ready to challenge incumbents.

Key Report Takeaways

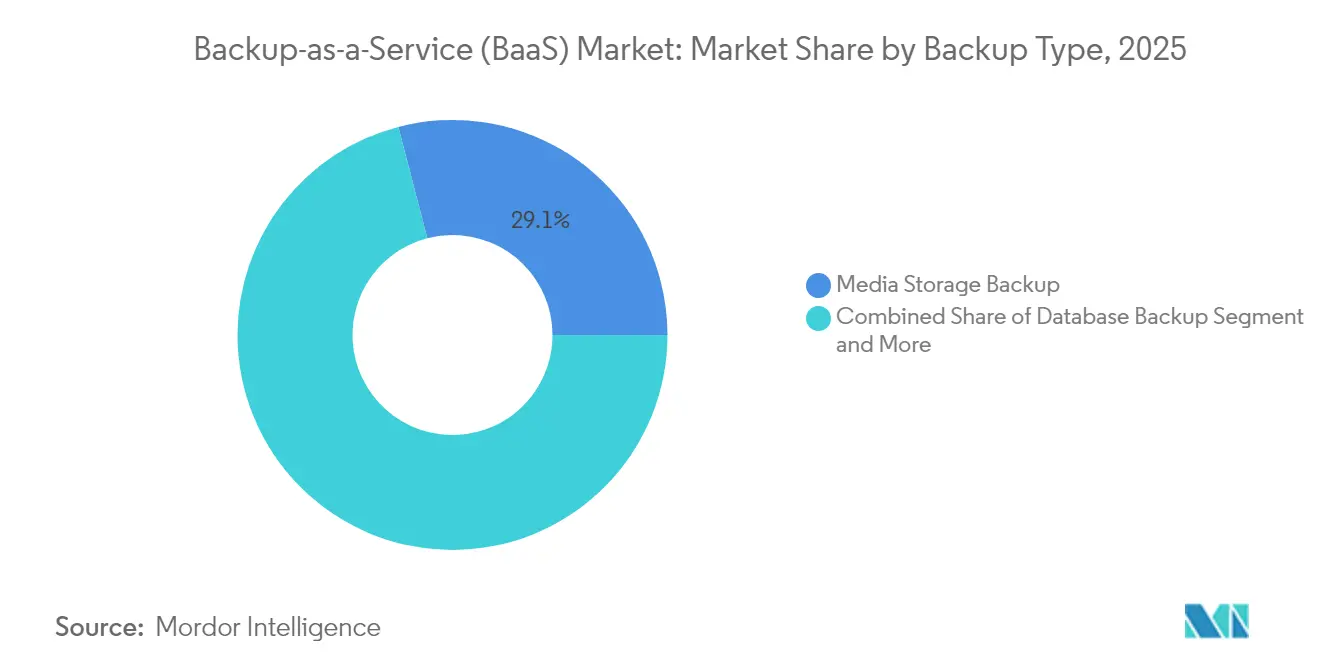

- By backup type, Media Storage Backup led with 29.05% revenue share in 2025; SaaS Application Backup is projected to expand at a 34.15% CAGR through 2031.

- By delivery model, Public Cloud held 52.90% of the Backup-as-a-Service market share in 2025, while Private Cloud is forecast to grow at 32.40% CAGR to 2031.

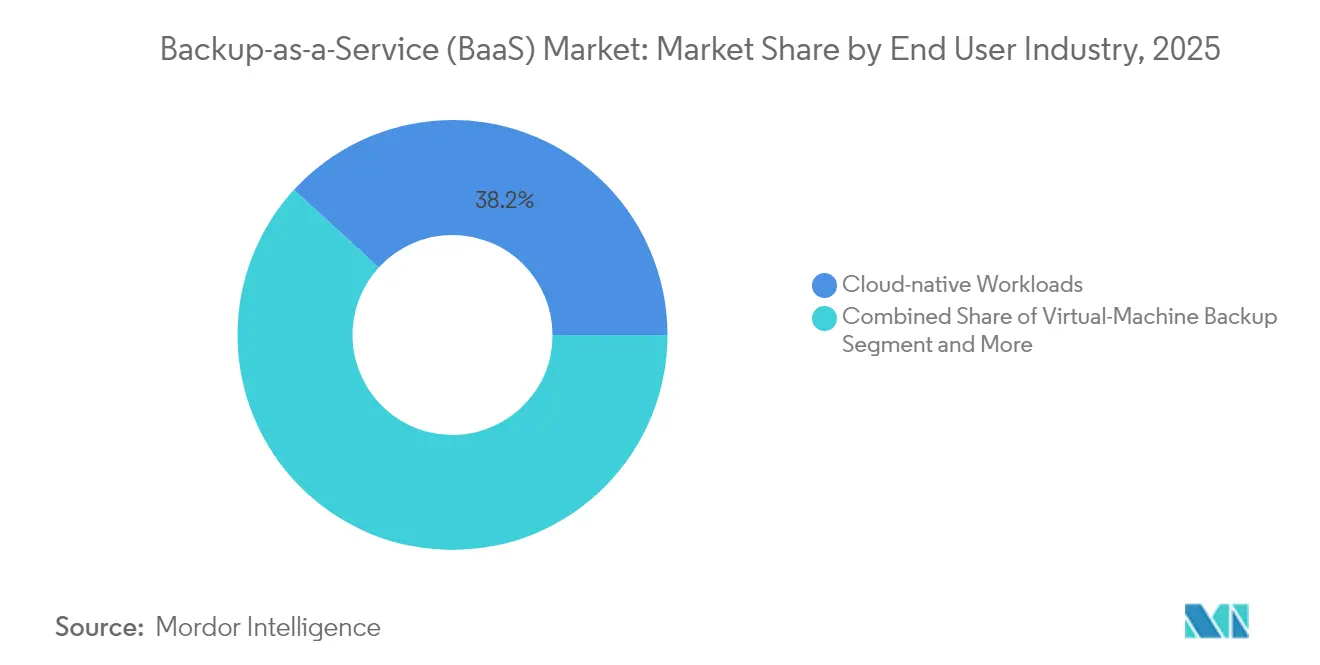

- By application workload, Cloud-native Workloads accounted for 38.20% of the Backup-as-a-Service market size in 2025; Container and Kubernetes Backup shows the fastest momentum at 35.00% CAGR.

- By end-user industry, BFSI dominated with 28.05% share in 2025; Retail and E-commerce is on course for a 37.10% CAGR to 2031.

- By organization size, Large Enterprises controlled 62.60% share in 2025, yet SMEs are poised for the strongest 33.05% CAGR through 2031.

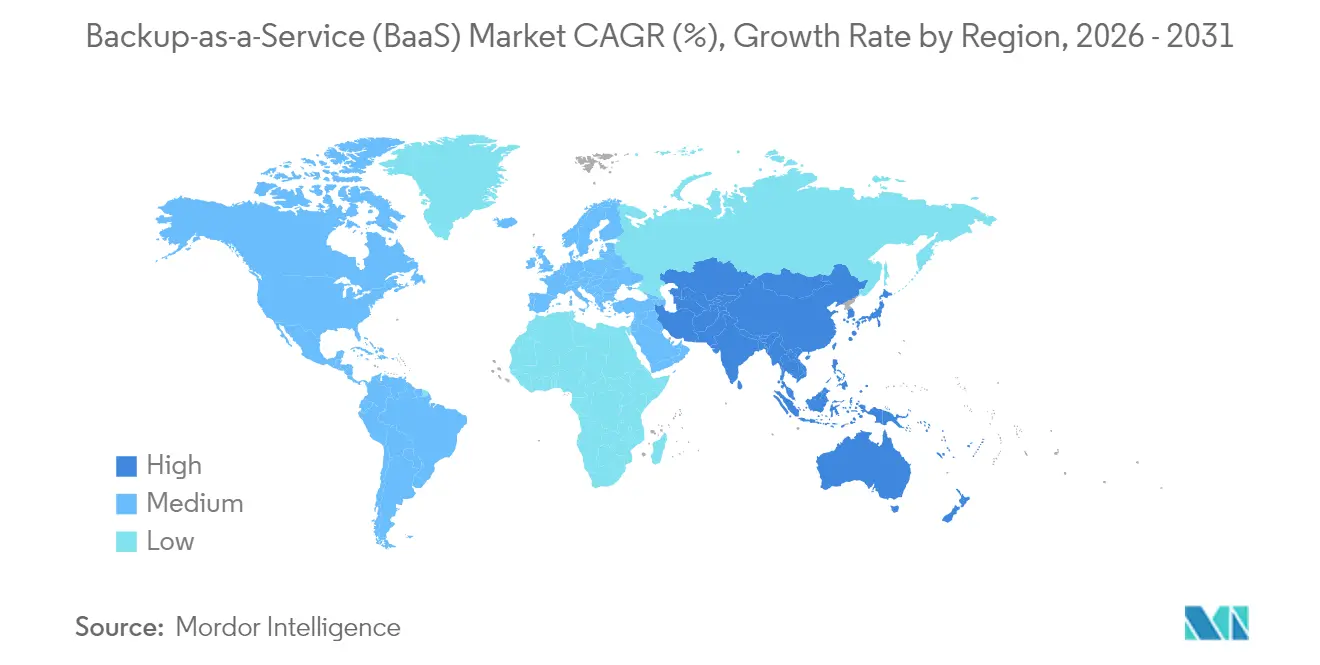

- Geographically, North America led with 37.10% share in 2025, while Asia-Pacific is expected to grow at 36.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Backup-as-a-Service (BaaS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated cloud adoption and multicloud strategies | +8.5% | Global, with strongest impact in North America and Asia-Pacific | Medium term (2-4 years) |

| Escalating ransomware and cyber-threat landscape | +7.2% | Global, particularly acute in North America and Europe | Short term (≤ 2 years) |

| Stricter data-retention / sovereignty regulations | +5.8% | Europe and Asia-Pacific core, expanding to MEA | Long term (≥ 4 years) |

| BaaS-DRaaS convergence for seamless resiliency | +4.3% | Global, led by North America and Europe | Medium term (2-4 years) |

| AI-driven backup optimization and egress-cost control | +3.7% | Global, early adoption in North America | Medium term (2-4 years) |

| Edge-to-core micro-backup demand (IoT/OT datasets) | +2.1% | Asia-Pacific and North America manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Cloud Adoption and Multicloud Strategies

More than four in five enterprises now operate workloads across two or more hyperscale clouds, demanding unified backup that moves data seamlessly among AWS, Azure, and Google Cloud. These multicloud footprints reduce vendor lock-in, improve latency management, and enable jurisdiction-specific data placement. Organizations increasingly standardize on policy-driven orchestration layers that automate snapshot scheduling, retention enforcement, and cross-cloud replication. As a result, the Backup-as-a-Service market gains strategic relevance as the de-facto control plane for multicloud data protection. The shift is especially visible in regulated industries where board-level risk committees seek resilience that transcends a single cloud provider.

Escalating Ransomware and Cyber-Threat Landscape

Attackers now engineer malware to corrupt or delete backups before detonating payloads, elevating immutable storage and air-gapped tiers from best practice to baseline requirement. Sophos reports that ransom demands more than double when attackers compromise backup environments, with median recovery costs reaching USD 3 million for affected firms.[1]Sophos, “The State of Ransomware 2024,” sophos.com Vendors have responded by embedding AI models that detect anomalous I/O patterns, halt suspicious deletions, and isolate clean restore points within seconds. These capabilities accelerate Backup-as-a-Service market adoption among firms lacking in-house cyber-resilience expertise yet facing insurance mandates that specify provable backup integrity.

Stricter Data-Retention and Sovereignty Regulations

The United States Securities and Exchange Commission amended Regulation S-P in 2024, obligating financial institutions to notify affected individuals within 30 days of data-security incidents.[2]United States Federal Register, “Regulation S-P: Privacy of Consumer Financial Information and Safeguarding Personal Information,” federalregister.gov Parallel developments such as evolving GDPR interpretations and sector-specific health-data mandates push enterprises toward providers that guarantee in-region storage and jurisdictional control. Modern BaaS platforms respond through selectable data-residency zones, audit-ready compliance reports, and automated retention enforcement. These features position the Backup-as-a-Service market as a compliance accelerator rather than purely a cost center.

BaaS-DRaaS Convergence for Seamless Resiliency

Separation between daily backup and disaster-recovery tooling creates coverage gaps: 79% of enterprises still cite inadequate backup frequency and 82% report insufficient restoration speed against recovery-time objectives.[3]Veeam Software, “Data Protection Trends Report 2025,” veeam.co To close this gap, leading vendors now deliver single-console offerings where backups, replicas, and orchestrated failover scripts coexist. AI-driven run-books test recovery paths continuously, predict capacity bottlenecks, and trigger multi-cloud failover without manual intervention. This unified model reinforces subscription economics and propels the Backup-as-a-Service market toward holistic resiliency platforms.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy and sovereignty hurdles | -4.2% | Europe and Asia-Pacific, with spillover to MEA | Long term (≥ 4 years) |

| Legacy-system migration complexity | -3.8% | Global, particularly acute in manufacturing and healthcare | Medium term (2-4 years) |

| Rising cloud egress fees and vendor lock-in risks | -2.9% | Global, most severe in North America and Europe | Short term (≤ 2 years) |

| Shortage of data-resilience engineering talent | -2.1% | Global, critical in Asia-Pacific and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Sovereignty Hurdles

Tighter rules in the European Union and several Asia-Pacific jurisdictions restrict cross-border transfer of “important data,” forcing multinationals to deploy multiple sovereign-cloud vaults. Maintaining parallel repositories inflates operational cost and complicates centralized management. Although most BaaS providers have launched regional, logically-isolated instances, customers still wrestle with divergent encryption-key handling and conflicting retention mandates. For smaller entities, the legal burden can delay Backup-as-a-Service market onboarding until guidance clarifies or a full turnkey compliance offering emerges.

Legacy-System Migration Complexity

Many factories and hospitals still run mission-critical workloads on proprietary operating systems or hardware lacking modern APIs. Moving decades of tape or disk archives into cloud repositories risks downtime that OT environments cannot tolerate. The skill set required to map dependencies, deduplicate data at petabyte scale, and re-platform backup jobs remains scarce. Consequently, conservative industries stage migrations over multi-year cycles, slowing the overall Backup-as-a-Service market growth trajectory even as new workloads default to cloud-native models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Backup Type: SaaS Applications Drive Next-Generation Protection

Media Storage Backup retained the largest 29.05% share of the Backup-as-a-Service market in 2025, supported by steady requirements to protect unstructured file repositories and rich-media archives across enterprise NAS arrays. Yet the SaaS Application Backup segment, buoyed by rapid Microsoft 365 and Salesforce adoption, is projected to post the fastest 34.15% CAGR through 2031. The granular restore of individual mails, SharePoint items, or CRM records has become a governance mandate for regulated sectors. Vendors are embedding AI models that scan snapshots for ransomware indicators before commit, ensuring downstream copies stay uncompromised. At the same time, Database Backup maintains healthy momentum because cloud-native relational services now often lack built-in point-in-time retention beyond seven days, prompting customers to offload protection to external BaaS vaults.

The shift toward SaaS-first architectures underscores a reality: software-as-a-service providers operate under a “shared responsibility” model that excludes customer-centric backup. High-profile incidents where administrative errors purged production data have sharpened board oversight, accelerating deals for SaaS-specific protection. The Backup-as-a-Service market size for SaaS Backup is expected to expand even faster where compliance audits require item-level retrieval proof. Meanwhile, System-State Backup gains traction in sectors migrating legacy on-premises workloads to virtual machines because full-server images reduce mean-time-to-recover after ransomware encryption events.

By Delivery Model: Private Cloud Gains Momentum Amid Sovereignty Concerns

Public-cloud subscription models commanded 52.90% of the Backup-as-a-Service market share in 2025 and remain the primary on-ramp for small organizations seeking elastic capacity. However, geopolitical data-residency mandates and increasing egress costs catalyze a pronounced shift toward provider-managed private-cloud vaults, forecast to rise at 32.40% CAGR. Enterprises relying on single-tenant private BaaS benefit from dedicated cryptographic key isolation, custom network segmentation, and predictable bandwidth budgeting. Furthermore, hybrid architectures combining on-premises cache nodes with cloud object storage deliver near-instant local restores and long-term archive economics, a balance that resonates with risk-averse verticals such as healthcare.

Managed-service-provider-hosted models occupy a valuable middle ground by pairing certified personnel with pre-built, multi-tenant infrastructure. Many MSPs now bundle advisory services that optimize snapshot cadences and automate policy compliance, essential for mid-market customers without full-time data-protection staff. As hyperscalers broaden region count and introduce lower-cost “archival infrequent access” tiers, public-cloud BaaS still holds a cost advantage for bulk storage. Nonetheless, concerns around cross-border subpoenas spur multinationals to diversify repositories, reinforcing multi-model orchestration capabilities within the Backup-as-a-Service market.

By Application Workload: Container Backup Emerges as Critical Capability

Cloud-native workloads represented 38.20% of protection spend in 2025, powered by widespread microservices adoption. Conventional image-level backup cannot capture distributed pod configurations, secrets, and persistent volumes, prompting specialized Kubernetes-aware engines. Container and Kubernetes Backup is expected to grow at 35.00% CAGR as DevOps pipelines integrate automated snapshot triggers in Helm charts and GitOps workflows. Vendors now enable namespace-level restores so developers can roll back only impacted microservices rather than entire clusters, saving time during incident response.

Virtual-machine Backup remains foundational because hybrid IT stacks retain core business apps on VMware and Hyper-V even while new services launch in containers. Endpoint and Mobile Backup growth aligns with continued remote-work models, extending enterprise policy control to employee devices and mitigating data loss when laptops succumb to theft or malware. Online File/Folder Backup persists as the entry-level gateway product for the Backup-as-a-Service market, providing rapid onboarding of departmental shares before organizations advance toward full-stack workload coverage.

By End-user Industry: Financial Services Lead While Retail Accelerates

The banking, financial-services, and insurance sector accounted for 28.05% of the 2025 Backup-as-a-Service market size, reflecting stringent audit requirements, daily transactional volumes, and board-level cyber-risk oversight. Institutions demand immutable vaults, continuous-data-protection journaling, and automated reporting that aligns with FFIEC and Basel guidelines. Conversely, retail and e-commerce operators are forecast to expand backup spending at a 37.10% CAGR as omnichannel platforms drive customer data into distributed microservices. Flash-sale traffic spikes require restore performance that supports sub-minute recovery of shopping-cart databases, pushing vendors to optimize snapshot granularity and deduplication for highly transactional NoSQL stores.

Healthcare and life-sciences organizations continue steady adoption as electronic health-record mandates and HIPAA obligations intersect with rising ransomware attacks against hospital networks. Manufacturing firms prioritize protection of operational-technology data from PLCs and SCADA systems; downtime directly halts production, granting OT-aware BaaS propositions strategic value. Finally, government agencies accelerate sovereign-cloud procurement to comply with national cyber-security frameworks, thereby channeling incremental demand into region-specific Backup-as-a-Service market offerings.

By Organization Size: SMEs Embrace Cloud-First Backup Strategies

Large enterprises retained 62.60% share in 2025 by virtue of expansive data estates spanning on-premises, multi-cloud, and edge scenarios. These firms often pursue vendor diversification, leveraging two or more BaaS platforms to avoid concentrated supplier risk. They are early adopters of AI-assisted policy tuning, predictive capacity planning, and cross-platform analytics pipelines that surface dark-data value from backup sets.

Small and medium enterprises continue to post the fastest 33.05% CAGR through 2031 as subscription pricing, zero-hardware deployment, and wizard-driven policy templates remove historical entry barriers. Incidents in which SMEs paid high ransoms because backups were either absent or corrupted have heightened executive awareness. Cloud marketplaces now bundle Backup-as-a-Service plans with SaaS bundles, enabling “click-to-protect” provisioning. As a result, the Backup-as-a-Service industry sees broader geographic dispersion, with channel partners localizing service-level agreements and compliance reporting to meet regional norms.

Geography Analysis

North America generated 37.10% of 2025 revenue, underpinned by mature cloud infrastructure and aggressive cyber-insurance requirements that prescribe immutable backups. AWS posted USD 29.3 billion in Q1 2025 cloud revenue, while Microsoft’s Intelligent Cloud segment delivered USD 26.8 billion, providing a robust base for integrated BaaS marketplaces. Heightened ransomware frequency drives enterprises to implement air-gapped object storage across multiple availability zones, stimulating cross-region backup replication services inside the Backup-as-a-Service market.

Asia-Pacific is projected to be the fastest-growing region, set for 36.60% CAGR through 2031 as governments champion digital-hospital, fintech, and smart-manufacturing initiatives. Hyperscalers continue multi-billion-dollar capital programs across India, Indonesia, and Thailand that include sovereign-cloud partitions designed for local data residency. The region’s manufacturing base fuels demand for edge-aware BaaS that can snapshot industrial IoT feeds without disrupting deterministic control-loop traffic. Regional service providers bundle connectivity, managed security, and BaaS into single contracts, appealing to mid-market firms that prefer one-stop procurement.

Europe advances steadily as GDPR enforcement actions underscore the financial risk of non-compliance. Local providers differentiate through in-country data centers and Schrems-II-compliant contractual clauses that keep encryption keys domiciled within the EU. Adoption also rises in South America and the Middle East and Africa, where improved undersea and terrestrial fiber links reduce latency penalties for cross-border replication. Governments there often launch national cyber-resilience frameworks that budget for off-site backups of critical public-sector databases, injecting new volume into the global Backup-as-a-Service market.

Competitive Landscape

The market’s structure shifted decisively when Cohesity finalized its Veritas data-protection business acquisition in December 2024, forming the largest pure-play vendor with USD 1.7 billion revenue and more than 12,000 customers. Veeam remains the individual market-share leader at 15.1%, buoyed by USD 1.5 billion revenue and a USD 15 billion valuation after a strategic secondary round. Both companies leverage AI engines—Cohesity’s DataHawk and Veeam’s Autonomics—to profile anomalous backup behavior, rank restore candidates, and cut egress costs via intelligent tiering.

Hyperscale clouds intensify competition by expanding native protection features: AWS Backup now supports cross-account vault locking, while Microsoft restores automatically validate integrity in Azure Backup Safe-Vault. Specialized challengers carve niches: Rubrik emphasizes cyber-recovery dashboards that integrate with Palo Alto Networks firewalls; Commvault’s acquisition of Clumio augments its Metallic SaaS line with cloud-native snapshot orchestration; Druva offers a fully managed, agentless model that resonates with resource-constrained mid-market firms.

Backup-as-a-Service (BaaS) Industry Leaders

Amazon Web Services (AWS)

Microsoft Corporation

Google LLC

IBM Corporation

Dell Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: OVHcloud, a global and European cloud provider, and HYCU, Inc., a rapidly growing player specializing in modern data protection across on-premises, cloud services, and SaaS, unveiled a strategic partnership. This collaboration empowers channel partners to resell HYCU's R-Cloud Hybrid Cloud Edition licenses, now hosted on OVHcloud's robust infrastructure.

- February 2025: In a recent announcement, Rewind revealed its collaboration with Monday.com to create a robust backup solution. This tool aims to assist enterprise teams in securely backing up and recovering their business data, safeguarding against accidental deletions, cyber threats, and data corruption. Furthermore, the solution adheres to stringent security compliance standards, including SOC 2 and ISO 27001. Rewind also mentioned that this integrated backup solution is set to debut on the Monday.com marketplace in Q2 2025, with an associated fee for customers opting for installation.

- February 2025: Veeam expanded its partnership with Microsoft to co-develop AI-powered resiliency features that shorten Microsoft 365 and Azure recovery time.

- December 2024: Cohesity completed its combination with Veritas’ Enterprise Data Protection business, creating a USD 1.7 billion revenue leader focused on AI-driven data security.

Global Backup-as-a-Service (BaaS) Market Report Scope

Backup-as-a-Service (BaaS) offers a cloud-based solution, enabling businesses and individuals to securely store their data in the cloud for backup, protection, and recovery. With BaaS, organizations can efficiently back up their critical data in a scalable and cost-effective manner, eliminating the need for on-premises hardware or intricate infrastructure.

The study tracks the revenue accrued through the sale of backup-as-a-service (BaaS) by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The backup-as-a-service (BaaS) market is segmented by type (email backup, media storage backup, and others), application (online backup and cloud backup), end-use industry (BFSI, government and public sectors, healthcare, manufacturing, media, and entertainment, it and telecommunication, and others), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Email Backup |

| Media Storage Backup |

| Database Backup |

| SaaS Application Backup |

| System-State Backup |

| Public Cloud (SaaS) |

| Managed-Service-Provider Hosted |

| Private Cloud |

| Online File/Folder Backup |

| Cloud-native Workloads |

| Virtual-Machine Backup |

| Container and Kubernetes Backup |

| Endpoint and Mobile Backup |

| BFSI |

| Government and Public Sector |

| Healthcare and Life Sciences |

| Manufacturing |

| Media and Entertainment |

| IT and Telecommunications |

| Retail and E-commerce |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Backup Type | Email Backup | ||

| Media Storage Backup | |||

| Database Backup | |||

| SaaS Application Backup | |||

| System-State Backup | |||

| By Delivery Model | Public Cloud (SaaS) | ||

| Managed-Service-Provider Hosted | |||

| Private Cloud | |||

| By Application Workload | Online File/Folder Backup | ||

| Cloud-native Workloads | |||

| Virtual-Machine Backup | |||

| Container and Kubernetes Backup | |||

| Endpoint and Mobile Backup | |||

| By End-user Industry | BFSI | ||

| Government and Public Sector | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Media and Entertainment | |||

| IT and Telecommunications | |||

| Retail and E-commerce | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Backup-as-a-Service market?

The market is valued at USD 10.9 billion in 2026 and is projected to hit USD 41.49 billion by 2031.

Which segment of the Backup-as-a-Service market is growing the fastest?

SaaS Application Backup shows the highest forecast growth at a 34.15% CAGR through 2031.

Why are immutable backups important for ransomware defense?

Immutable storage prevents attackers from altering or deleting backup copies, ensuring clean restore points even if production systems are encrypted.

How does data-sovereignty regulation influence Backup-as-a-Service adoption?

Laws requiring in-country data storage push organizations toward providers offering region-specific vaults and jurisdictional control features.

Page last updated on: