Data Protection And Recovery Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

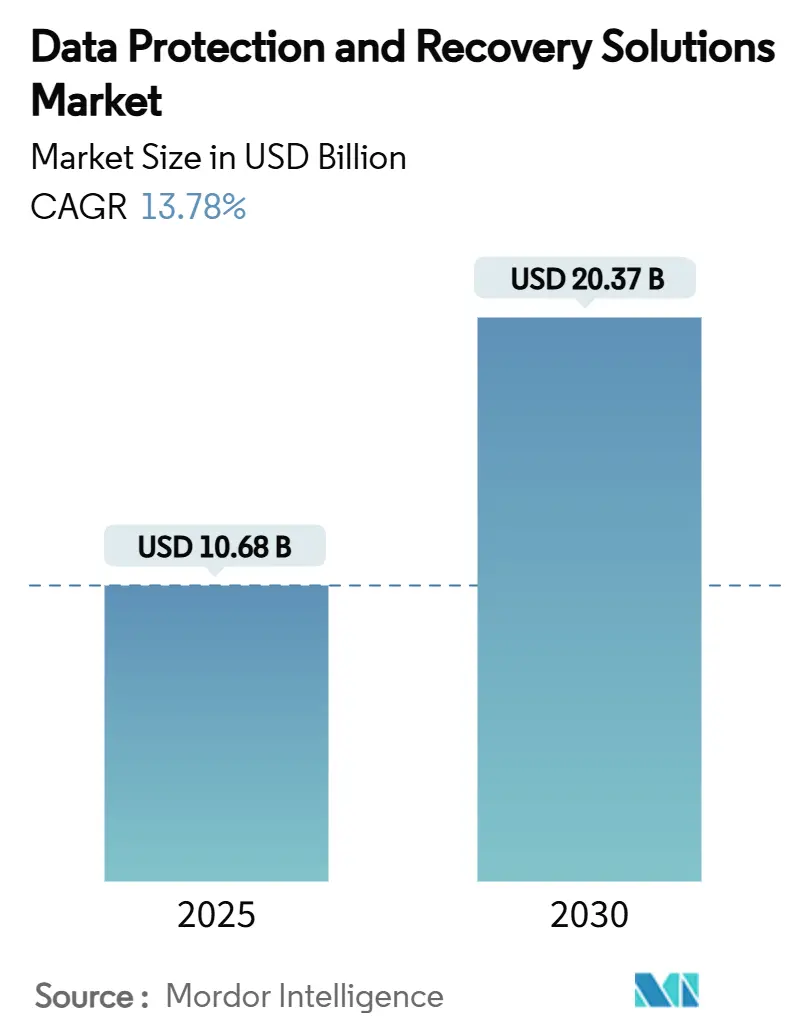

| Market Size (2025) | USD 10.68 Billion |

| Market Size (2030) | USD 20.37 Billion |

| Growth Rate (2025 - 2030) | 13.78% CAGR |

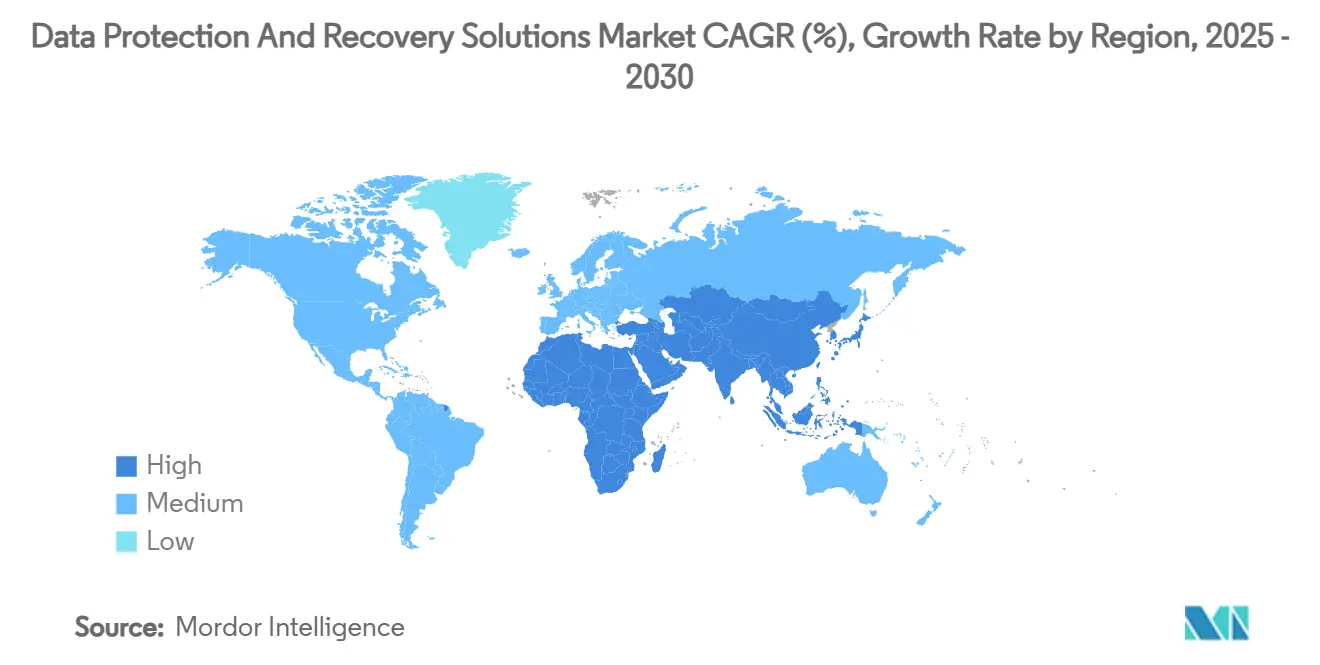

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

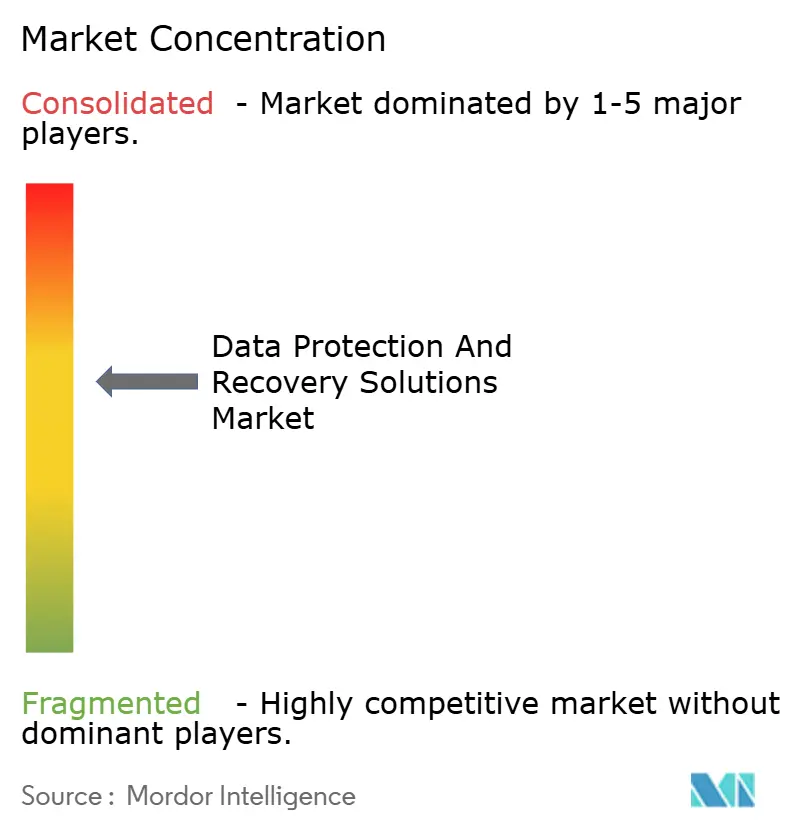

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Protection And Recovery Solutions Market Analysis by Mordor Intelligence

The data protection and recovery solutions market size is valued at USD 10.68 billion in 2025 and is forecast to expand to USD 20.37 billion by 2030, reflecting a 13.78% CAGR. Heightened ransomware sophistication, stricter privacy mandates, and cyber-insurance underwriting rules are turning backup architectures into core business-continuity assets rather than discretionary IT tools. Vendors that combine immutable storage, AI-enabled threat analytics, and zero-trust access controls are winning share as enterprises reposition backups as live defenses that detect, contain, and remediate attacks before production systems collapse. Regulatory fines-such as India’s INR 250 crore penalty ceiling-have also reframed backup investments as risk-mitigation necessities rather than cost centers. Cloud adoption remains the prime catalyst: hybrid workloads require protection that spans SaaS, IaaS, and on-premises estates with uniform policy enforcement, driving rapid uptake of integrated data resilience platforms.

Key Report Takeaways

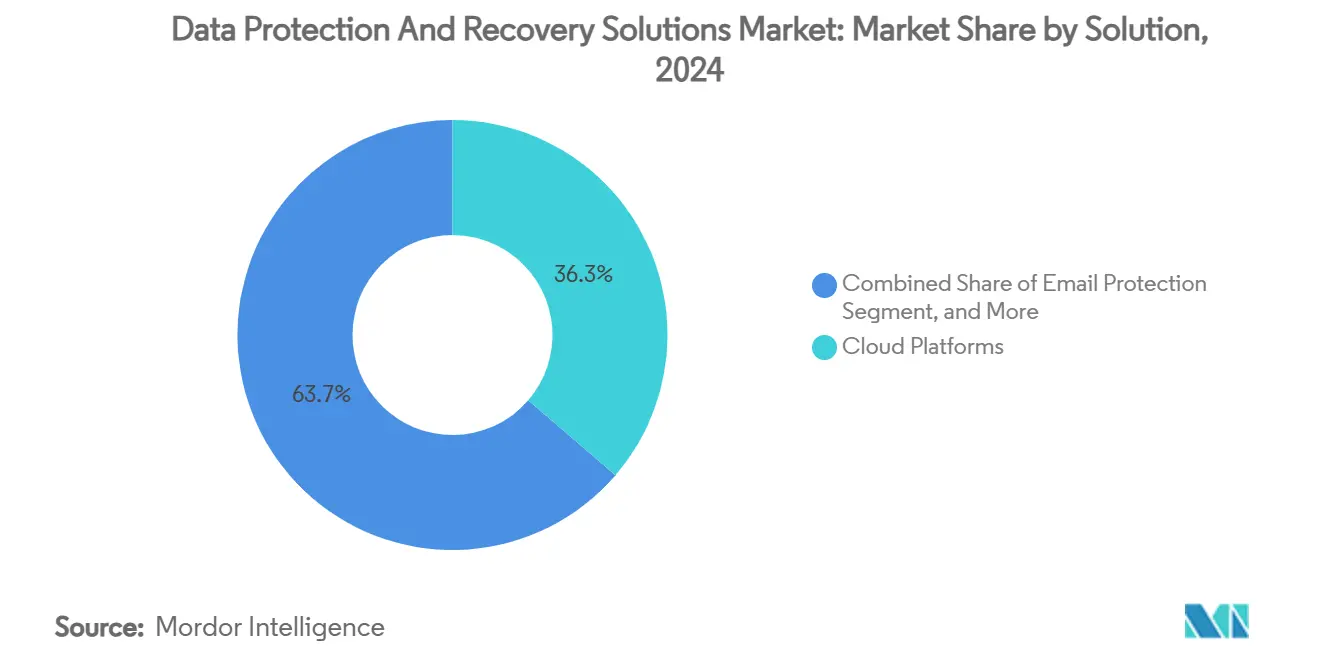

- By solution, Cloud Platforms led with 36.31% revenue share in 2024, while the same segment is projected to record a 13.81% CAGR through 2030.

- By deployment, the Hosted segment is forecast to expand at 13.98% CAGR through 2030; On-Premise retained 58.97% of the data protection and recovery solutions market share in 2024.

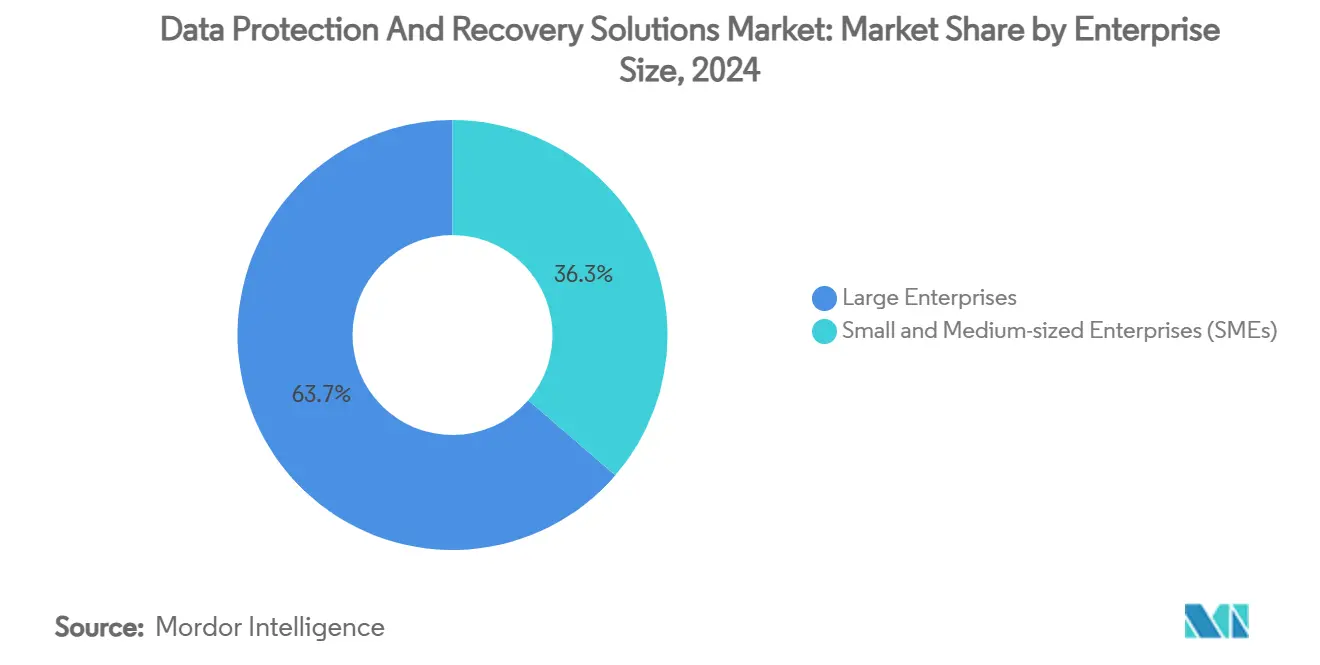

- By enterprise size, Large Enterprises accounted for 63.68% of the data protection and recovery solutions market size in 2024 and Small and Medium-sized Enterprises are advancing at a 13.87% CAGR to 2030.

- By end user, BFSI captured 28.32% share of the data protection and recovery solutions market in 2024, while Healthcare is projected to post the fastest 14.11% CAGR through 2030.

- North America commanded 41.86% of 2024 revenues; Asia-Pacific is poised to grow at 14.28% CAGR up to 2030.

Global Data Protection And Recovery Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reliance on Zero-Trust Architectures | +2.1% | North America, EU | Medium term (2-4 years) |

| Escalating Ransomware Payouts | +3.2% | North America, Europe | Short term (≤ 2 years) |

| Surge in SaaS Workload Protection Needs | +2.8% | Global, led by NA and Asia-Pacific | Short term (≤ 2 years) |

| Stringent Data-Sovereignty Mandates | +1.9% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| AI-Enabled Anomaly Detection | +2.3% | North America, EU | Medium term (2-4 years) |

| Cyber-insurance Requirements for Immutability | +1.5% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reliance on Zero-Trust Architectures

Zero-trust adoption eliminates implicit trust between backup components, reducing lateral threat movement by 60% and accelerating breach detection by 40%. [1]Microsoft, “Secure Data with Zero Trust,” microsoft.com The framework forces continuous identity verification, in-flight encryption, and segmentation of backup repositories, thereby transforming backups from passive data vaults into active security controls. Vendors embedding conditional-access engines inside their platforms benefit as enterprises pivot away from perimeter-centric designs. This shift elevates the data protection and recovery solutions market by rewarding products that natively interlock with identity, endpoint, and network telemetry.

Escalating Ransomware Payouts Driving Backup Modernisation

Median ransom demands now reach USD 2 million when adversaries impair backup copies, versus USD 1 million when backups remain intact, creating clear ROI for modern, immutable architectures. [2]Sophos, “Impact of Compromised Backups on Ransomware Outcomes,” sophos.comAttack groups increasingly leverage ransomware-as-a-service kits that boast 57% success in breaching enterprise backup environments. Financial exposure, particularly in healthcare where outages cost USD 2 million each day, accelerates upgrades from tape systems to cloud-integrated vaults that resist encryption and deletion attempts. This economics-driven urgency directly boosts the data protection and recovery solutions market.

Surge in SaaS Workload Protection Needs

Cloud apps now underpin 55% of enterprise workloads, yet only 14% of IT leaders feel fully confident in their recovery readiness. [3]Atlassian, “How to Create a SaaS Application Resilience Strategy,” atlassian.com Misunderstandings about the shared-responsibility model mean 41% erroneously assume SaaS vendors handle backup duties. High-profile incidents in Microsoft 365-where 87% of administrators reported data loss in 2024-underscore the gap. Specialized SaaS-aware snapshots, granular point-in-time restores, and API-level immutability are therefore hot purchase criteria, widening addressable spend for the data protection and recovery solutions market.

Stringent Data-Sovereignty Mandates

Frameworks such as GDPR and India’s Digital Personal Data Protection Act levy fines up to INR 250 crore (USD 30 million) for mishandled records, forcing firms to store copies in-country and prove tamper-proof retention. Vendors capable of offering location-pinned vaults, sovereign cloud zones, and automated compliance reporting gain traction. Over the long term, these mandates push multinationals to adopt federated architectures that replicate data across regional vaults without violating cross-border controls, amplifying demand for orchestration-heavy platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills Shortage in Cyber-Recovery Engineering | -1.8% | Global | Long term (≥ 4 years) |

| Budget Lock-in from Legacy Tape Infrastructures | -1.2% | North America, Europe | Medium term (2-4 years) |

| Rising Cost of Immutable Storage Tiers | -0.9% | Global | Short term (≤ 2 years) |

| Vendor Overlap Causing Tool Sprawl | -1.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skills Shortage in Cyber-Recovery Engineering

A workforce gap of 4.8 million security professionals leaves 90% of firms understaffed in disciplines such as AI-driven threat hunting and zero-trust backup administration. Cyber-recovery engineers require blended expertise spanning forensics, incident response, and storage operations, yet training pathways take up to 24 months. This human capital crunch slows rollout of sophisticated data resilience architectures and tempers the growth of the data protection and recovery solutions market.

Budget Lock-in from Legacy Tape Infrastructures

Organizations that committed capital to tape libraries struggle to rationalize multi-million-dollar sunk costs even though tape fails to deliver immutable, rapid-recover characteristics. Maintenance alone can exceed USD 1 million annually for large estates, diverting budgets from modern vaults. As a result, decision makers adopt phased refresh timetables, stretching market conversion cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Cloud Platforms Command Dual Leadership

Cloud Platforms dominated with 36.31% 2024 share of the data protection and recovery solutions market and will register the fastest 13.81% CAGR to 2030, underscoring a decisive swing toward hybrid protection models. This leadership stems from unified consoles that secure on-premises systems and SaaS workloads under consistent policy. The email-protection subsegment remains essential because 61% of ransomware breaches originate from messaging channels. Application Recovery Management gains traction as container adoption grows and enterprises demand restoration to application-specific states rather than entire VM images.

Steady interest in Endpoint Data Protection persists as remote work exposes unmanaged devices. Meanwhile, emerging AI-orchestrated orchestration modules and quantum-resistant encryption fall within the Others category, adding innovation headroom. Vendors fusing these capabilities inside cloud-native fabrics continue to capture incremental spend, further solidifying Cloud Platforms’ command over the data protection and recovery solutions market.

By Deployment: Hosted Momentum Outpaces On-Premise Control

On-Premise deployments retained a 58.97% share of the data protection and recovery solutions market in 2024, thanks to direct data custody and compliance needs. Nevertheless, hosted solutions are forecast to grow 13.98% CAGR through 2030, powered by elasticity, geo-redundancy, and consumption-based pricing. Financial institutions cling to self-hosted vaults to meet regulatory mandates while technology firms lean into hosted models to avoid capex.

Hybrid architectures-blending on-premise immutability with cloud-based long-term retention-are now mainstream as executives balance security, cost, and agility. Government bodies mirror this approach by pairing air-gapped local repositories with off-site replicas to satisfy audit criteria, thereby sustaining dual-stack adoption and reinforcing the expansion path of the data protection and recovery solutions market.

By Enterprise Size: SME Uptake Narrows the Gap

Large Enterprises held 63.68% share in 2024 due to complex estates that warrant end-to-end platforms integrating AI analytics and zero-trust controls. Yet Small and Medium-sized Enterprises will post a quicker 13.87% CAGR thanks to ransomware groups intentionally targeting mid-market victims perceived as soft. Cloud-delivered backup-as-a-service dismantles entry barriers by bundling immutability and automated recovery in subscription models.

Scale advantages let large firms negotiate multi-year licenses and deploy layered defense-in-depth tactics, but SMEs increasingly consume those same capabilities through managed offerings. The converging requirements signal that protection is no longer proportional to company size; ransomware risk is universal, driving homogenous expectations across the data protection and recovery solutions market.

By End User: Healthcare Growth Challenges BFSI Supremacy

BFSI retained 28.32% share in 2024 by virtue of stringent audit rules and the high transaction value of compromised data. Healthcare, however, is poised for a 14.11% CAGR to 2030 after headline attacks highlighted life-and-death stakes and USD 2 million-per-day outage costs. Energy and Utilities maintain consistent demand, reinforced by critical-infrastructure directives. Manufacturing adoption rises as plants digitize production lines and require application-aware snapshots to restore machine states quickly without halting throughput.

Retail players pursue granular rollback capabilities that safeguard e-commerce uptime during peak seasons. Government agencies invest in sovereign-cloud backup solutions after attacks disrupted essential public services. These diverse requirements create fertile ground for verticalized modules, sustaining momentum for the data protection and recovery solutions market.

Geography Analysis

North America commanded 41.86% of 2024 revenues as cyber-insurance carriers mandate immutable, air-gapped backups for policy issuance. US enterprises pioneer AI-enabled anomaly detection, while Canadian public-sector bodies roll out sector-wide backup standards. Mexico’s mid-market firms increasingly adopt cloud-hosted resilience platforms, illustrating the region’s trickle-down effect from large-enterprise best practices.

Asia-Pacific will chart the swiftest 14.28% CAGR to 2030 as digital-first expansion coincides with sovereign-data rules. India’s DPDP Act imposes steep penalties and accelerates on-premise vault deployments alongside local-cloud replicas. China enforces data-localization within its borders, reinforcing demand for domestic vault nodes, whereas Japan and South Korea refine cross-border transfer compliance through managed backup exchanges. Australia leads in multi-cloud adoption, using hosted resilience nodes across zones to offset natural-disaster exposure. Southeast Asian SMEs gravitate toward managed services that sidestep capital investments yet meet regulatory tests.

Europe remains stable under GDPR’s mature framework. Germany and the UK advance hybrid models that keep primary repositories on site while aging archives shift to regional clouds. France emphasizes sovereign services operated by domestic providers, and Nordic markets push for energy-efficient storage powered by renewable grids. South America and Middle East and Africa are nascent but rising; constrained budgets push organizations toward pay-as-you-go vaults operated by MSPs, gradually broadening the global footprint of the data protection and recovery solutions market.

Competitive Landscape

The market is moderately fragmented, hosting long-established broad-suite vendors and agile cloud-native entrants. IBM, Veeam, and Microsoft leverage scale, patents, and cloud footprints to anchor end-to-end offerings that bundle backup, AI analytics, and zero-trust integration. The Cohesity-Veritas merger created a behemoth focused on unifying cloud-native management with enterprise-grade resiliency, prompting rivals to accelerate platform consolidation.

Disruptors compete on niche differentiators such as quantum-resistant encryption or fully autonomous recovery orchestration. Strategic alliances grow in importance: Veeam’s equity-infused pact with Microsoft aligns roadmaps around AI-powered threat detection for Microsoft 365 tenants. Hardware innovations such as IBM’s FlashCore Module inject silicon-level intelligence that flags entropy changes during snapshot writes, illustrating hardware-software convergence as a durable moat.

Pricing models also shape rivalry. Vendors now tout predictable vault economics or bundled cyber-insurance discounts to entice budget-constrained buyers. Those able to deliver comprehensive protection without tool sprawl win executive mindshare, sustaining healthy competition that ultimately expands the data protection and recovery solutions market.

Data Protection And Recovery Solutions Industry Leaders

International Business Machines Corporation (IBM)

Dell Technologies Inc.

Microsoft Corporation

Veeam Software AG

Commvault Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Commvault posted USD 275 million fiscal-quarter revenue, up 23% year-on-year, underscoring cloud-backup demand.

- April 2025: Veeam integrated Anthropic’s Model Context Protocol to convert backup telemetry into AI decision intelligence.

- February 2025: Veeam expanded its Microsoft partnership, adding AI-powered detection and equity investment to accelerate joint innovation.

- January 2025: Cohesity and Veritas finalized their merger, creating the largest integrated platform for cyber-resilience.

Global Data Protection And Recovery Solutions Market Report Scope

| Email Protection |

| Endpoint Data Protection |

| Application Recovery Management |

| Cloud Platforms |

| Other Solutions |

| Hosted |

| On-Premise |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| Energy and Utilities |

| Government |

| Healthcare |

| Manufacturing |

| Retail |

| Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Solution | Email Protection | ||

| Endpoint Data Protection | |||

| Application Recovery Management | |||

| Cloud Platforms | |||

| Other Solutions | |||

| By Deployment | Hosted | ||

| On-Premise | |||

| By Enterprise Size | Small and Medium-sized Enterprises (SMEs) | ||

| Large Enterprises | |||

| By End User | Banking, Financial Services and Insurance (BFSI) | ||

| Energy and Utilities | |||

| Government | |||

| Healthcare | |||

| Manufacturing | |||

| Retail | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What CAGR is expected through 2030 for data protection and recovery solutions?

The segment is projected to grow at 13.78% annually, taking revenues from USD 10.68 billion in 2025 to USD 20.37 billion by 2030.

Which solution type currently holds the largest share?

Cloud Platforms account for 36.31% of global 2024 revenues thanks to hybrid workload protection capabilities.

Why is Asia-Pacific the fastest-growing region?

Rapid digitalization and new data-sovereignty laws such as India’s DPDP Act lift Asia-Pacific to a 14.28% CAGR through 2030.

How are zero-trust principles influencing backup architectures?

Zero-trust enforces continuous verification and immutable storage, improving threat detection speed by 40% and curbing lateral movement by 60%.

What main restraint could slow technology upgrades?

A worldwide shortage of cyber-recovery engineers delays advanced deployment because organizations cannot hire or train the required talent quickly.

Page last updated on: