Enterprise Information Archiving Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

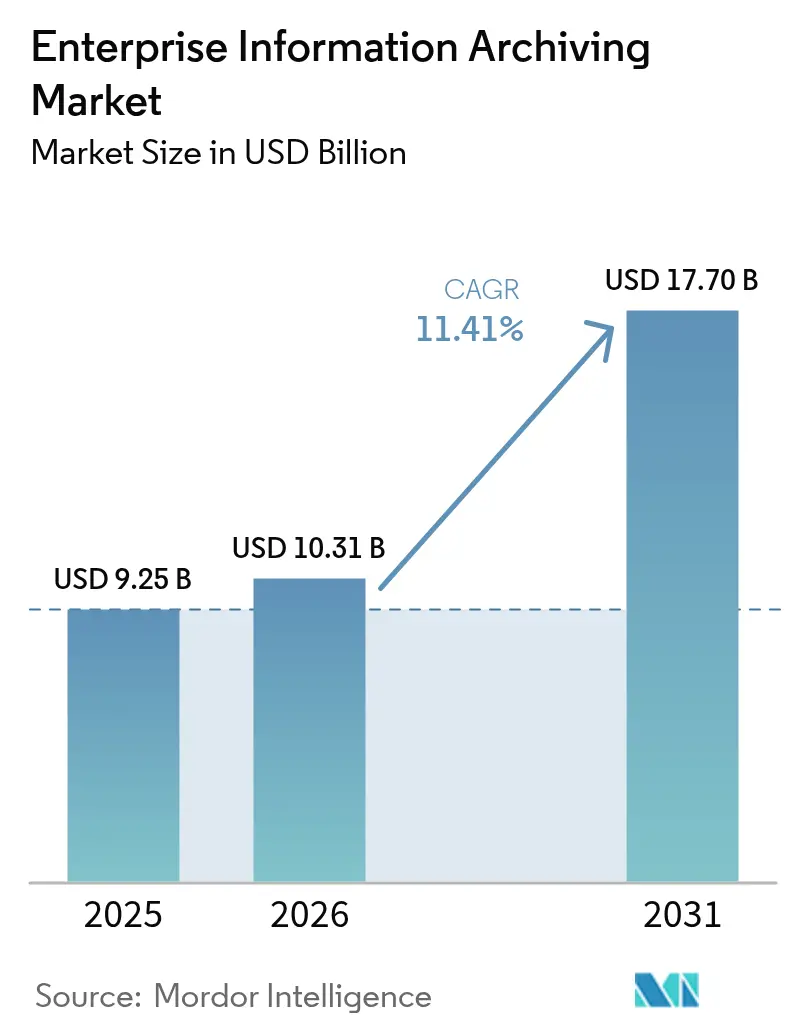

| Market Size (2026) | USD 10.31 Billion |

| Market Size (2031) | USD 17.7 Billion |

| Growth Rate (2026 - 2031) | 11.41% CAGR |

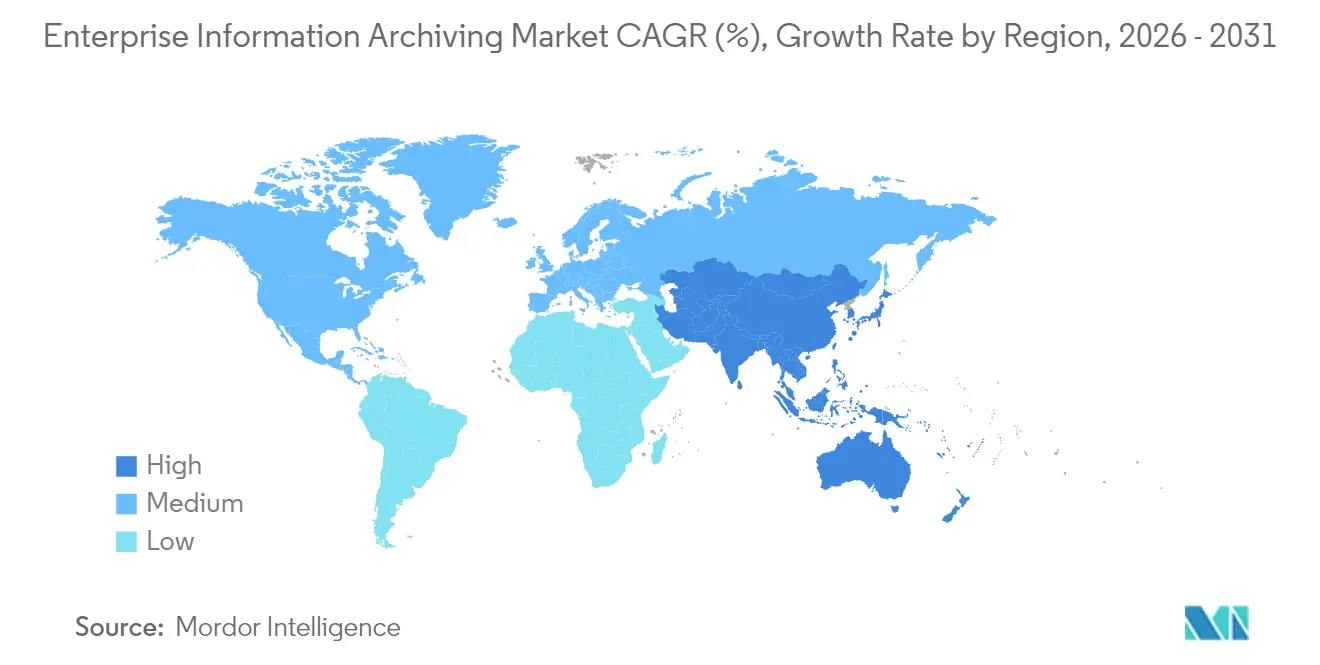

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Information Archiving Market Analysis by Mordor Intelligence

The enterprise information archiving market size is expected to grow from USD 9.25 billion in 2025 to USD 10.31 billion in 2026 and is forecast to reach USD 17.7 billion by 2031 at 11.41% CAGR over 2026-2031. This expansion stems from stricter global record-keeping mandates, escalating e-discovery exposure, and a decisive shift toward cloud-native retention platforms. Vendors are weaving artificial intelligence into core capture, classification, and search functions to lower compliance costs and turn archives into insight engines. Intensifying demand for immutable object storage, mounting litigation penalties tied to disappearing messages, and the need to train generative-AI models on well-governed historical data further accelerate adoption. Competitive dynamics favor suppliers that can integrate multichannel capture at scale while satisfying divergent sovereignty rules across regions.

Key Report Takeaways

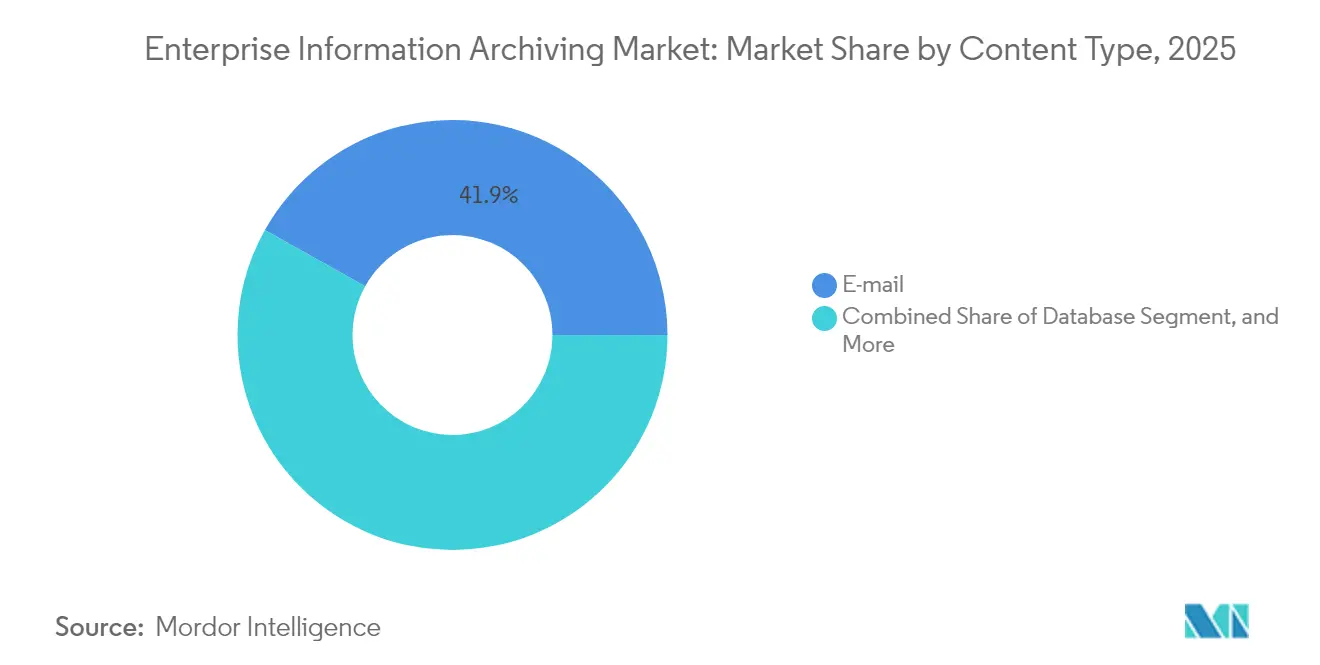

- By content type, email preserved 41.88% of the Application Performance Management market share in 2025, whereas database archiving is advancing at a 14.92% CAGR through 2031.

- By services, system integration accounted for 36.10% of the Enterprise Information Archiving Market market share in 2025, while consulting services recorded the sharpest growth at 12.23% CAGR to 2031.

- By deployment mode, cloud implementations commanded 70.56% of the enterprise information archiving market size in 2025, and on-premise deployments are expanding at a 14.38% CAGR through 2031.

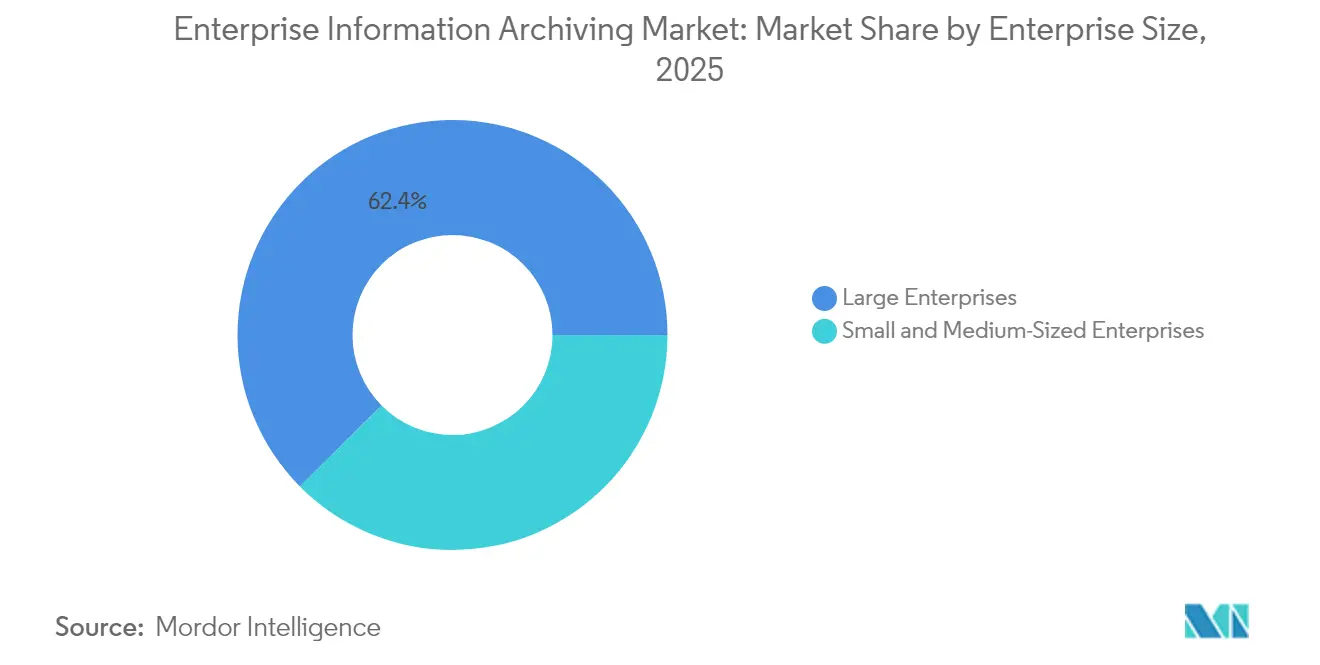

- By enterprise size, large enterprises controlled 62.44% of the Enterprise Information Archiving Market market share in 2025, yet small and medium enterprises are on track for a 13.31% CAGR to 2031.

- By end-user industry, banking, financial services, and insurance contributed 28.74% of the Enterprise Information Archiving Market market share in 2025, whereas government and defense registered the fastest 13.72% CAGR between 2026 and 2031.

- By geography, North America led with 38.15% of the Enterprise Information Archiving Market market share in 2025; Asia-Pacific is poised for a 13.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Information Archiving Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing volume of compliance-mandated data | +2.8% | North America, European Union, global spillover | Medium term (2-4 years) |

| Shift from CAPEX to OPEX via cloud archiving | +2.1% | North America, Asia-Pacific, worldwide adoption | Short term (≤ 2 years) |

| Surge in e-discovery litigation costs | +1.9% | North America, European Union, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rise of collaboration apps | +1.7% | Developed markets globally | Short term (≤ 2 years) |

| Generative-AI-ready archives | +1.4% | North America, European Union, Asia-Pacific spillover | Long term (≥ 4 years) |

| Demand for immutable WORM storage | +1.1% | Financial hubs worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Volume of Compliance-Mandated Data

Financial, healthcare, and public-sector regulators are broadening retention rules to cover chat, social, and ephemeral messages. The U.S. SEC, FTC, and DOJ now require preservation of Slack, Teams, and WhatsApp messages, heightening urgency for unified capture platforms.[1]Weberman, Melissa, “Federal Authorities Continue to Focus on Preserving Collaboration Tools and Ephemeral Messages,” Arnold and Porter, arnoldporter.com Hospitals must treat all patient communications as protected health information under HIPAA, demanding tamper-evident storage across portals, text, and video. In Europe, GDPR’s data minimization clause pushes firms to combine granular classification with automated disposal. Collectively, these mandates enlarge archive footprints and force investment in scalable, policy-driven repositories able to span structured and unstructured sources.

Shift From CAPEX to OPEX via Cloud Archiving

Cloud-native platforms replace hardware refresh cycles with elastic, pay-as-you-go models. Case studies show enterprises cutting USD 40 million in five-year costs after retiring legacy tape libraries and migrating to Archive360 on Azure Blob tiers. Smaller firms gain enterprise-grade retention without capital budgets, fostering democratization of compliance tooling. Hyperscaler marketplaces bundle archive licenses with productivity suites, Microsoft 365 retention labels, and Purview e-discovery, for example, further simplifying procurement. Low-cost cold tiers such as AWS Glacier Deep Archive push storage prices under USD 1 per terabyte monthly, sustaining OPEX momentum.

Surge in E-Discovery Litigation Costs

Legal departments spend more as discovery demands encompass chat threads, voice recordings, reactions, and emojis. Real-time capture prevents spoliation of disappearing content and enables early case assessment at scale. North American courts increasingly penalize incomplete chat preservation, prompting investments in AI-driven culling and smart sampling to shrink review volumes. Vendors respond with integrated legal-hold automation that can suspend deletion instantly across Teams and Slack through APIs, reducing risk while controlling attorney hours.

Rise of Collaboration Apps (Teams, Slack, Zoom)

Billions of daily Teams and Slack messages scatter regulated data outside email silos. Financial dealers must archive emoticons, edits, and GIFs under FINRA rules. Government-grade solutions stitch together chat, file shares, and meeting transcripts into a single timeline, supplying context for audits. Enterprises favor vendors that normalize metadata across channels and provide federated search, ensuring consistent retention schedules despite platform proliferation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reliance on legacy on-premises email archives | -1.8% | Global, especially mature markets | Medium term (2-4 years) |

| Budget constraints for SMEs | -1.2% | Emerging markets worldwide | Short term (≤ 2 years) |

| Complex data-sovereignty regulations | -0.9% | European Union, Asia-Pacific, global influence | Long term (≥ 4 years) |

| Shadow-IT and “chat-ops” sprawl | -0.7% | Technology-centric organizations globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reliance on Legacy On-Premises Email Archives

Many enterprises still run Veritas Enterprise Vault or Dell SourceOne, accumulating sunk costs and petabytes of stubbed messages. Migrating holdings to cloud buckets without breaching chain-of-custody requirements is complex, often leading to prolonged hybrid estates. Older systems lack APIs for modern analytics, forcing expensive workarounds for e-discovery. Scarcity of technicians skilled in vintage platforms inflates project timelines and keeps capital locked in outdated hardware.

Budget Constraints for SMEs

Regulatory obligations apply to small businesses, yet compliance talent and tooling remain expensive. Subscription plans help, but usage-based search, export, and legal-hold fees can still outstrip tight budgets. SMEs often rely on managed service providers, adding margin layers that dilute savings. These cost pressures delay full-spectrum archiving, leaving gaps in chat or social media capture that heighten litigation exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Content Type: Email Continues to Lead While Databases Surge

Email retained 41.88% of 2025 revenue, anchoring the enterprise information archiving market through well-established capture policies and regulator familiarity. The enterprise information archiving market size for databases, however, is expected to expand at a 14.92% CAGR as firms recognize that structured records feed analytics and AI pipelines. In parallel, instant-messaging archives benefit from collaboration app ubiquity, while web and social media collections meet public-sector transparency mandates.

Structured data preservation attracts investment in tiered storage, query acceleration, and policy-driven masking that secures personal identifiers. Integrated platforms now route tables, logs, and time-series streams into the same governance fabric as chat or voice files. Advanced classification detects sensitive columns on ingestion and assigns retention codes automatically, shrinking manual oversight burdens.

By Services: Integration Dominates, Consulting Climbs

System integration captured 36.10% of 2025 spending as enterprises knit together multichannel capture, identity management, and legal-hold orchestration. Implementers map retention rules across dozens of jurisdictions and embed journaling connectors into Teams, Slack, and Zoom. The enterprise information archiving market size tied to consulting is projected to grow 12.23% annually as firms seek specialized guidance on privacy-by-design architectures and AI-driven classification.

Service providers extend beyond lift-and-shift migrations to deliver automation scripts, policy blueprints, and analytics dashboards. Training and support remain necessary for change management, but vendors increasingly automate routine tuning through machine-learning models that optimize archive tier selection and deduplication schedules.

By Deployment Mode: Cloud Rules, On-Premises Persists

Cloud archives owned 70.56% of 2025 revenue thanks to elastic economics and turnkey compliance certifications. Yet on-premise deployments will outpace overall growth at 14.38% CAGR, reflecting defense agencies and capital-markets desks that cannot export data because of sovereignty or latency constraints. Hybrid designs emerge, allowing sensitive datasets to stay local while bulk analytics run in the cloud.

Providers answer with region-locked storage nodes and customer-managed encryption keys. Some offer software-defined appliances mirroring cloud APIs so firms can shift workloads without rewriting applications. This flexibility sustains investment in both models, preventing a one-directional migration narrative.

By Enterprise Size: SME Adoption Accelerates

Large corporations controlled 62.44% of 2025 spend through sprawling global footprints and multichannel compliance needs. The enterprise information archiving market share among SMEs is smaller but expanding rapidly at a 13.31% CAGR. Consumption-based pricing lowers entry barriers while pre-built regulatory templates minimize configuration. Vendors target this cohort with wizard-driven deployments and managed discovery add-ons, letting lean IT teams outsource complexity.

SMEs increasingly view archives as data lakes for customer insight, not just compliance vaults. AI modules surface sentiment trends and product feedback embedded in chat logs, providing commercial value that offsets ongoing subscription fees.

By End-User Industry: Financial Services Lead; Government Rises

Banks, insurers, and broker-dealers contributed 28.74% of 2025 revenue owing to Rule 17a-4 and MiFID II mandates that prescribe precise retention windows and write-once storage. Government and defense are projected to grow 13.72% annually as agencies modernize electronic records programs and pursue cloud-smart directives. Healthcare organizations adopt chat capture to safeguard telehealth transcripts under HIPAA, while manufacturing firms archive IoT telemetry for warranty analytics and quality audits.

Sector-specific solutions embed regulatory taxonomies such as NIST controls for defense or CFR Title 21 requirements for life sciences, reducing customization time. Horizontal vendors partner with domain experts to pre-load rule packs and automate submission workflows, broadening vertical reach without building bespoke codebases.

Geography Analysis

North America accounted for 38.15% of the enterprise information archiving market in 2025, sustained by SEC and FINRA record-keeping enforcement, plus HIPAA and DOJ preservation directives. Financial institutions invest heavily in chat journaling and predictive analytics to avoid multi-million-dollar fines. Federal cloud-first policies spur agencies to migrate electronic records into FedRAMP-authorized repositories, keeping public-sector demand robust. Canada follows with provincial privacy statutes aligning with GDPR principles, reinforcing pan-regional compliance spending.

Europe maintains a substantial share thanks to GDPR, eIDAS, and industry-specific obligations. Multinational firms deploy localized clusters to honor data-residency rules while centralizing search across jurisdictions. Germany spearheads manufacturing use cases that combine IoT telemetry with process-control logs, whereas the United Kingdom emphasizes financial conduct oversight post-Brexit. Vendors that certify against both EU and U.K. frameworks secure a competitive advantage.

Asia-Pacific represents the fastest-growing territory at 13.61% CAGR. China enforces data-localization laws that favor domestic cloud regions, while India’s Digital Personal Data Protection Act accelerates adoption among multinationals needing regional segregation. Japan and South Korea champion AI-enabled classification, and Singapore positions itself as a compliance hub for Southeast Asian financial flows. Local channel partners and sovereign cloud options are becoming decisive differentiators.

Mordor Intelligence provides coverage of the enterprise information archiving market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Competitive intensity is rising as traditional archive vendors, cloud hyperscalers, and niche compliance specialists converge. Microsoft integrates Purview retention with Teams capture, while Veritas, now under Cohesity ownership following the USD 7 billion deal, broadens multicloud analytics, jointly servicing more than 12,000 customers. Archive360 leverages Azure infrastructure to migrate legacy stubs at a petabyte scale, claiming USD 40 million in customer savings over five years. Smarsh and SteelEye tailor FINRA-centric surveillance modules, embedding voice transcription and lexicon-based alerting.

Emerging disruptors emphasize open APIs and microservices that connect to new channels within days rather than months. Providers differentiate through AI modules that automate sensitivity labeling, PII redaction, and predictive legal-hold scopes. Certification depth—FedRAMP High, SOC 2 Type II, and ISO 27001 remains a key buying criterion, especially for public-sector and healthcare deals. Partnerships with global systems integrators expand reach into regulated verticals, while regional resellers address sovereign-cloud mandates.

Strategic moves in 2024–2025 include Preservica’s launch of an AI-enabled digital-preservation service, Sharp Archive’s Asian distribution tie-up, and Datasite’s acquisition of Sealk to infuse M&A search capabilities into its platform. These transactions demonstrate a pivot from pure storage toward value-added analytics and workflow automation, underscoring the market’s evolution from compliance repository to intelligence layer.

Enterprise Information Archiving Industry Leaders

Barracuda Networks, Inc

Google LLC

Microsoft Corporation

ZL Tech

Veritas Technologies LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Preservica launched its new Enterprise Digital Preservation platform featuring enhanced security, automated preservation, and AI/ML integration.

- October 2025: Sharp Archive partnered with Trinax Pte Ltd to broaden distribution of its communication-archiving suite across Asia-Pacific.

- September 2024: Datasite acquired Paris-based Sealk, adding AI-powered M&A search to its portfolio.

- June 2024: SOLIX Technologies upgraded its SOLIXCloud archiving platform with enhanced analytics.

Global Enterprise Information Archiving Market Report Scope

Enterprise information archive solutions capture, index, and archive the data. Also, they make large volumes of archived information searchable and retrievable in seconds.

Enterprises use these solutions to optimize information resources, improve efficiency, and maintain transparency. The estimation is for the license and subscription-based software offerings for different content types from the vendors and services-related revenues in the market studied.

The Enterprise Information Archiving Market is segmented by type (content types (database, email, social media, instant messaging, web, mobile communication, file, and enterprise file synchronization and sharing), by services (consulting, system integration, training, support, and maintenance)), by deployment mode (on-premise, cloud), by enterprise size (small and medium-sized enterprises, large enterprises), end-user (government and defense, banking, financial services, and insurance, healthcare and pharmaceutical, retail and e-commerce, manufacturing, and other end-user types), and by geography(North America, Europe, Asia Pacific, and rest of the world).

The report also covers the COVID-19 impact analysis on the market studied and the stakeholders, and the same is considered for the current market estimation and future projections.

The report offers the market size and forecasts in USD billion for all the above segments.

| Database |

| Social Media |

| Instant Messaging |

| Web |

| Mobile Communication |

| File and EFSS |

| Consulting |

| System Integration |

| Training, Support and Maintenance |

| On-Premise |

| Cloud |

| Small and Medium-Sized Enterprises |

| Large Enterprises |

| Government and Defense |

| Banking, Financial Services and Insurance |

| Healthcare and Pharmaceutical |

| Retail and E-commerce |

| Manufacturing |

| Telecommunications |

| Education |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Content Type | Database | ||

| Social Media | |||

| Instant Messaging | |||

| Web | |||

| Mobile Communication | |||

| File and EFSS | |||

| By Services | Consulting | ||

| System Integration | |||

| Training, Support and Maintenance | |||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| By Enterprise Size | Small and Medium-Sized Enterprises | ||

| Large Enterprises | |||

| By End-User Industry | Government and Defense | ||

| Banking, Financial Services and Insurance | |||

| Healthcare and Pharmaceutical | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Telecommunications | |||

| Education | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the enterprise information archiving market in 2026?

It is valued at USD 10.31 billion, with a forecast to reach USD 17.7 billion by 2031 on an 11.41% CAGR.

Which region leads adoption of archiving solutions?

North America holds 38.15% share thanks to mature financial and healthcare regulations.

What content type dominates archived volumes today?

Email remains dominant with 41.88% of 2025 revenue, although database archiving is growing fastest at a 14.92% CAGR.

Why are SMEs accelerating their use of archiving platforms?

Subscription-based, cloud-native tools remove upfront hardware costs and simplify compliance, driving a 13.31% CAGR among SMEs.

Page last updated on: