Document Capture Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

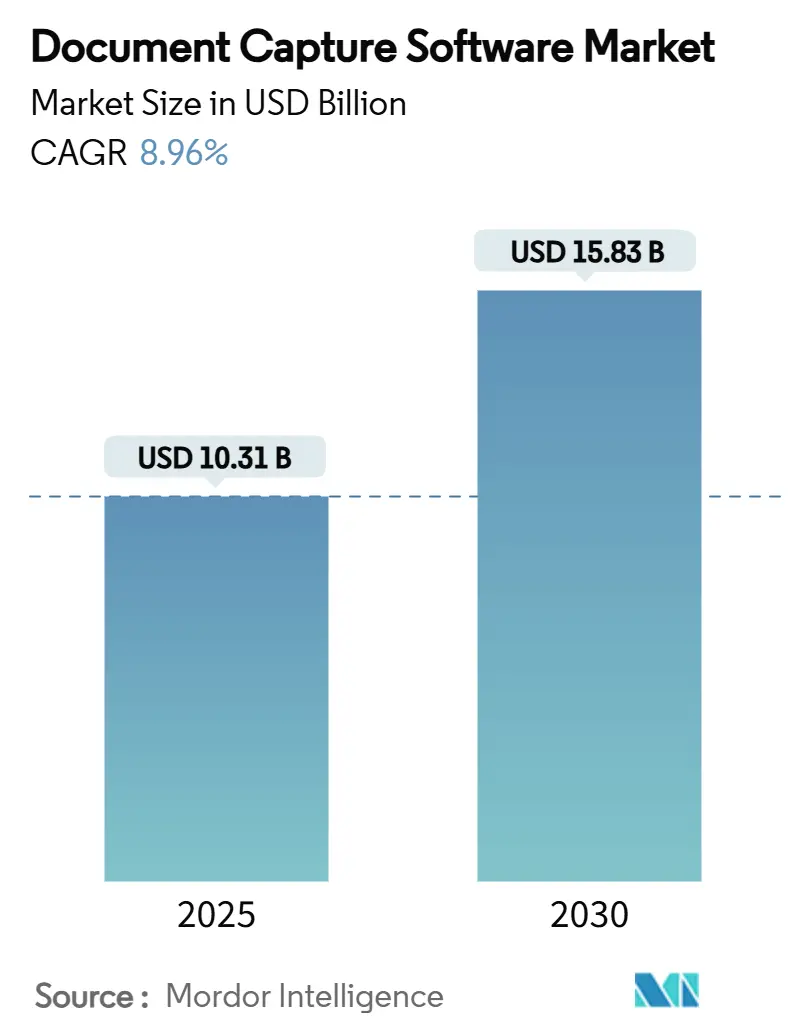

| Market Size (2025) | USD 10.31 Billion |

| Market Size (2030) | USD 15.83 Billion |

| Growth Rate (2025 - 2030) | 8.96% CAGR |

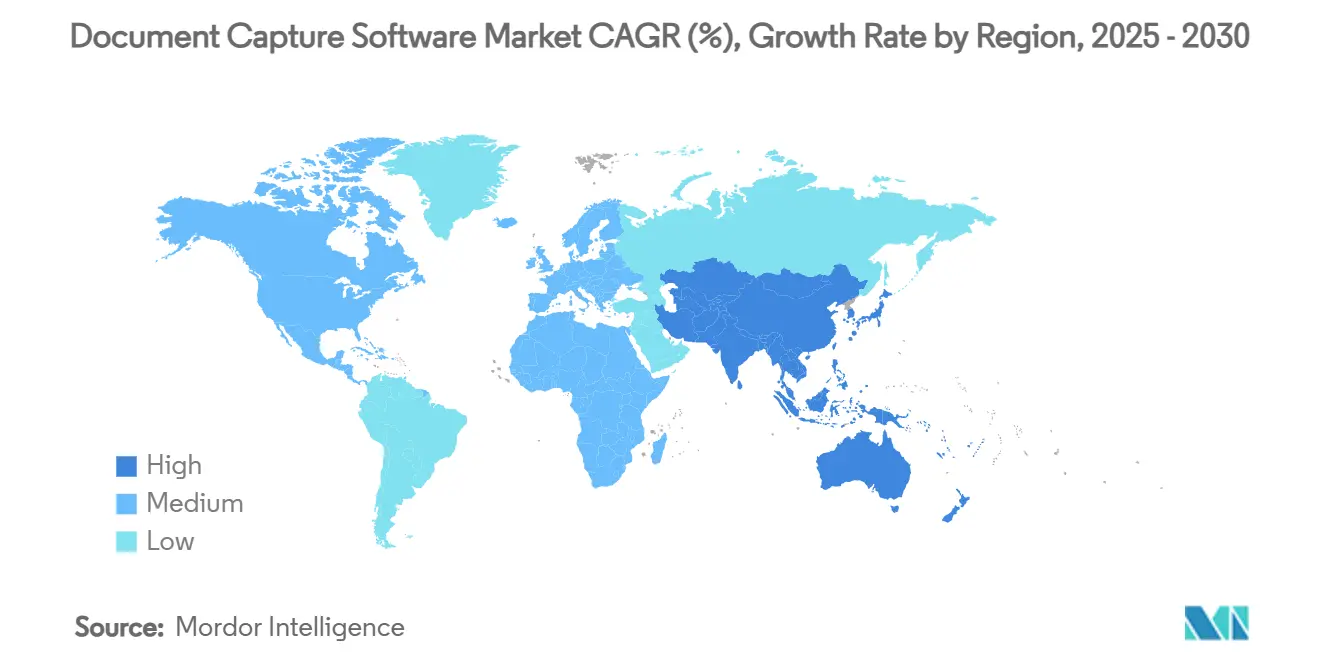

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

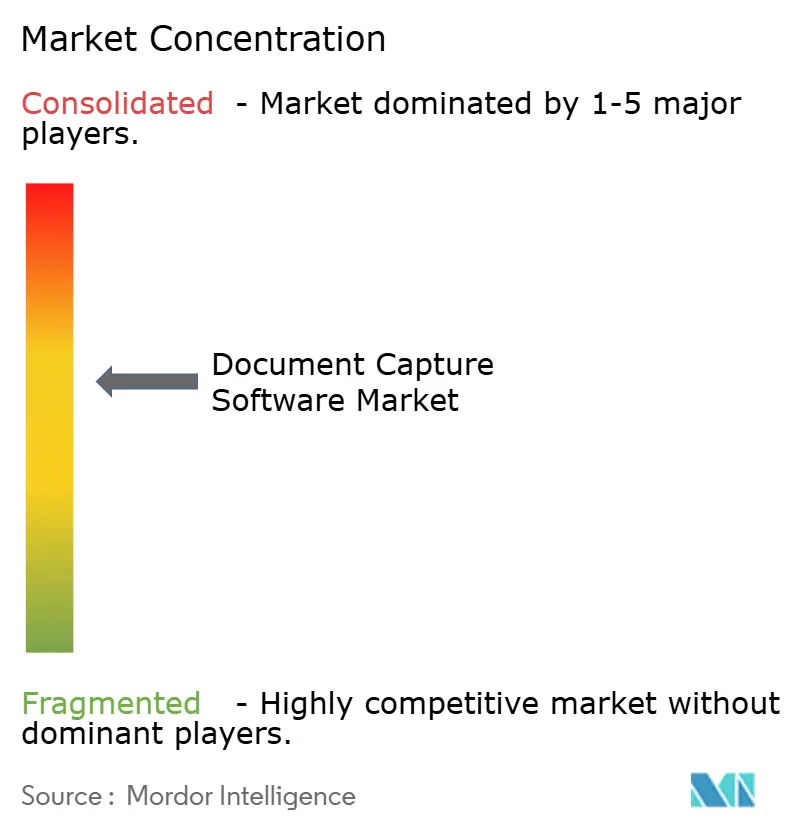

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Document Capture Software Market Analysis by Mordor Intelligence

The document capture software market size stands at USD 10.31 billion in 2025 and is projected to reach USD 15.83 billion by 2030, reflecting an 8.96% CAGR over the forecast period. Cloud deployment models now dominate adoption, intelligent document processing (IDP) capabilities are eclipsing rule-based optical character recognition (OCR), and vendors are embedding generative AI to achieve straight-through processing. Growth is sustained by global digitization mandates, hybrid-work requirements, and heightened compliance pressures, while cost-efficiency goals in shared-service centers spur rapid return-on-investment conversations. Competitive intensity is moderate as established providers defend share through continuous platform upgrades and acquisitions, and challengers focus on large-language-model (LLM) innovation to close accuracy gaps. The document capture software market is therefore transitioning from tactical digitization to strategic revenue enablement.

Key Report Takeaways

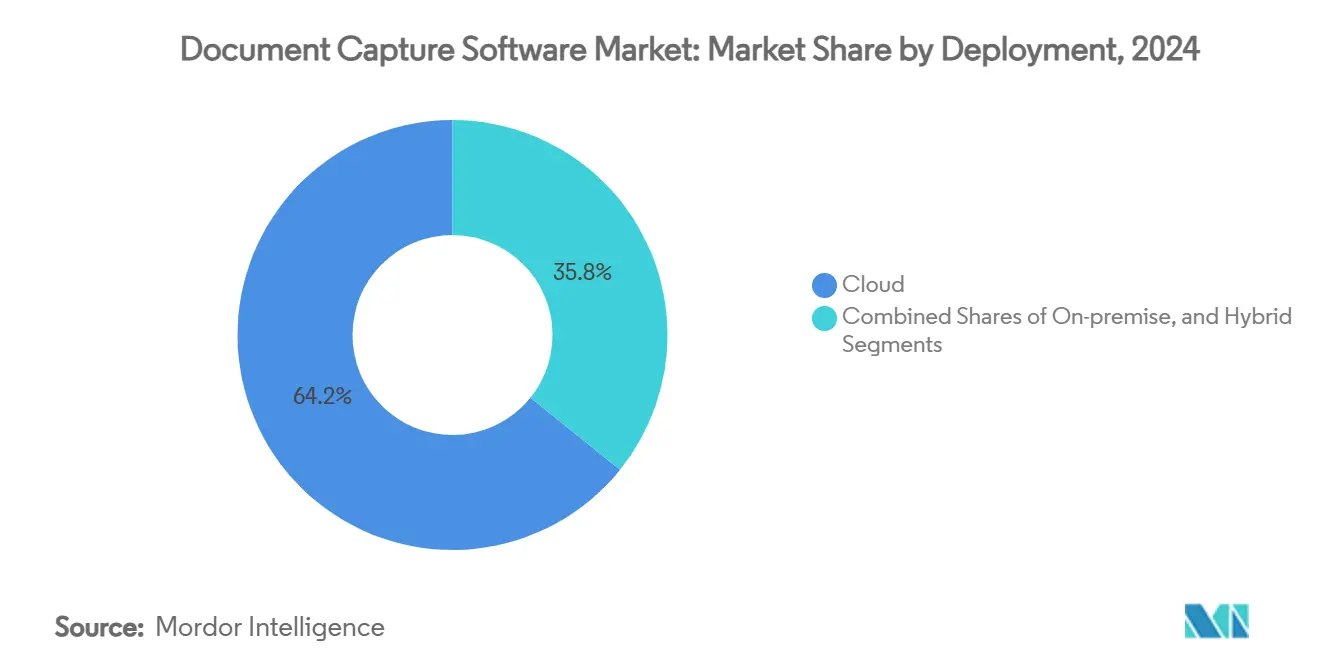

- By deployment, cloud captured 64.21% of document capture software market share in 2024, while the same deployment method is advancing at 12.67% CAGR through 2030.

- By organization size, large enterprises held 54.06% of the document capture software market size in 2024; small and medium enterprises are expanding at 13.71% CAGR.

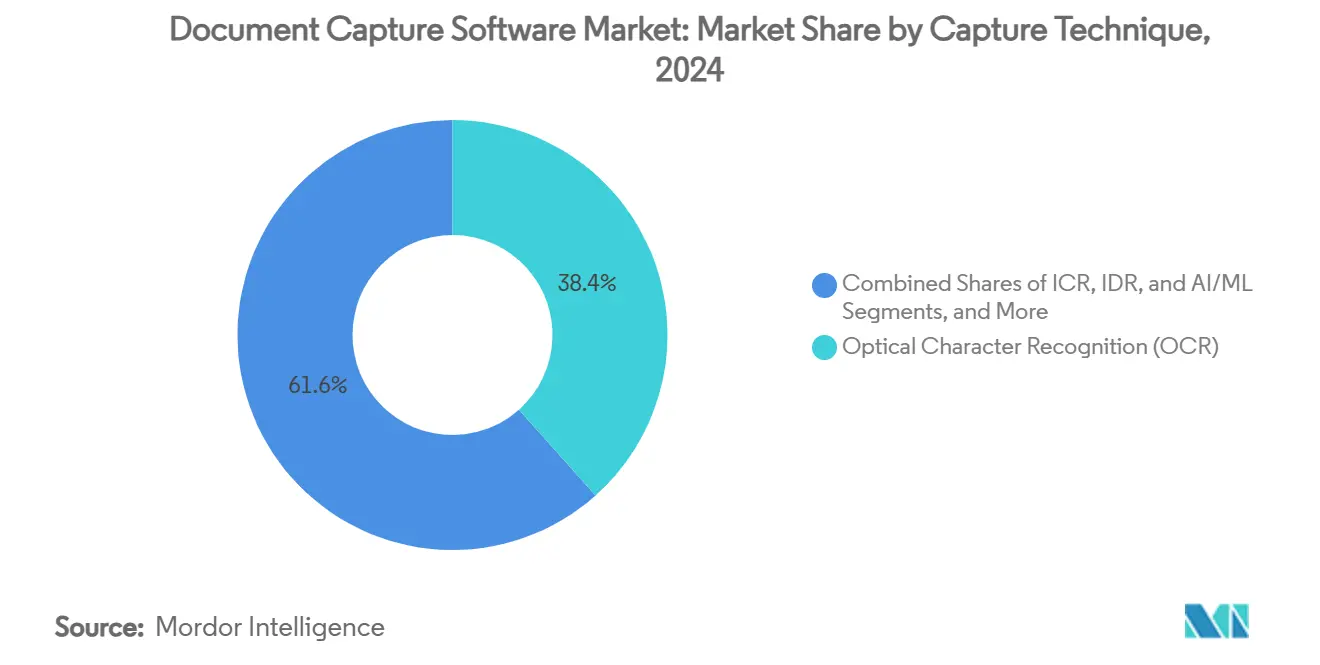

- By capture technique, OCR led with 38.42% revenue share in 2024, whereas intelligent document processing is growing at 11.85% CAGR.

- By end-user industry, BFSI accounted for 22.61% share of the document capture software market in 2024, while healthcare is expanding at 12.04% CAGR.

- By geography, North America commanded 37.91% share in 2024; Asia-Pacific is forecast to grow at 11.34% CAGR through 2030.

Global Document Capture Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large-scale enterprise digitization programs | +2.1% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Stringent data-retention and compliance mandates | +1.8% | Global, particularly EU and North America | Long term (≥ 4 years) |

| Remote and hybrid workforce expansion | +1.4% | Global, accelerated in developed markets | Short term (≤ 2 years) |

| Cost-efficiency pressure on shared-service centers | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Hyper-automation road-maps in mid-market firms | +0.9% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Edge-capture for near-real-time analytics | +0.7% | Global, early adoption in manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Large-scale Enterprise Digitization Programs

Organizations link capture investments directly to enterprise-resource-planning workflows, treating intelligent automation as a revenue generator rather than an overhead function. Tungsten Automation’s TotalAgility 8.1 reduces development cycles by 80%, enabling fast rollout of AI agents that manage high-volume content.[1]Tungsten Automation, “Tungsten Automation Unveils TotalAgility 8.1: Powering Rapid AI Agent Development and Smarter Automation,” tungstenautomation.com Denmark’s electronic-invoicing framework yields annual savings of EUR 150 million (USD 163 million).[2]European Commission, “eGovernment Action Plan,” europa.eu Italy’s procurement automation trims EUR 3 billion (USD 3.3 billion) in spending, underscoring scale benefits. Generative AI lets firms process unstructured formats with contextual reasoning, eliminating reliance on fixed templates. Consequently, the document capture software market benefits from sustained executive sponsorship and multi-year budget allocations.

Stringent Data-retention and Compliance Mandates

European Union objectives for universal online public services by 2030 force private-sector partners to demonstrate audit-grade capture capabilities. Financial institutions deploy solutions such as CambioML’s AnyParser API, which raises KYC precision while accelerating screening workloads.[3]CambioML, “AnyParser API: The First LLM for Document Parsing,” cambioml.com Vendors embed automatic classification and retention features to turn compliance into a strategic differentiator. Cross-border processing rules favor cloud platforms that guarantee jurisdiction-specific data residency without latency penalties. As regulators tighten oversight, enterprises expand adoption to mitigate potential fines, lifting the document capture software market.

Remote and Hybrid Workforce Expansion

Distributed work patterns demand secure, device-agnostic capture. Laserfiche Smart Fields extracts handwritten content through on-device AI, protecting data in transit. Edge computing supports near-real-time processing at branch locations, minimizing bandwidth use without relaxing governance. LINE WORKS’ AI-OCR trims order-entry time from 200 hours to 45 hours, showing the productivity upside. Zero-trust architectures and encryption are now baseline requirements, and capture is recognized as core digital-workspace infrastructure. These factors enlarge the document capture software market by embedding capture into everyday collaboration.

Cost-efficiency Pressure on Shared-service Centers

E-invoicing reduces processing expenses by up to 90% relative to paper flows. Advanced OCR reaches 99% accuracy on standard forms, and LLM extensions improve poor-image performance by 20–30%. Natural-language configuration lowers barriers for business users, shrinking IT queues. Redeployment of staff to analytics roles elevates perceived value, driving continued funding. Therefore, cost rationalization imperatives tangibly expand the document capture software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High switching costs of legacy content platforms | -1.6% | Global, particularly established enterprises | Medium term (2-4 years) |

| Persistent data-privacy and sovereignty concerns | -1.1% | EU and regulated industries globally | Long term (≥ 4 years) |

| Shortage of skilled IDP configuration talent | -0.8% | Global, acute in APAC and emerging markets | Short term (≤ 2 years) |

| Rising open-source alternatives eroding license fees | -0.5% | Global, concentrated in price-sensitive SME segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Switching Costs of Legacy Content Platforms

Complex integrations and entrenched user practices extend migration projects beyond the two-year horizon. The UK government notes that 47% of central services still lack digital pathways despite potential GBP 45 billion (USD 58 billion) savings. Vendors counter with API-first connectors; Tungsten Automation lists more than 200 integrations that allow phased adoption. Nonetheless, multi-system coexistence elevates operational overhead, temporarily slowing document capture software market expansion.

Persistent Data-privacy and Sovereignty Concerns

GDPR and sector-specific regulations often necessitate on-premise or hybrid capture, tempering pure-cloud enthusiasm. OECD research shows only 18% of SMEs are aware of government support for compliant digitalization, prolonging uncertainty. Providers respond with encryption, federated learning, and sovereign-cloud offerings, but architectural compromises can limit scalability benefits. These factors curtail near-term growth within the document capture software market, though technology advances may ease constraints over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Accelerates

Cloud models held 64.21% share of the document capture software market in 2024 and are projected to grow at 12.67% CAGR. Hyland’s hosted content services deliver 99.99% uptime and cut rollout times by 75%. OpenText Core Capture scales across public, private, and managed clouds, using machine learning for automated classification. Hybrid arrangements persist where data-residency mandates prevail, yet even regulated entities adopt cloud-adjacent architectures for surge capacity. The convergence of LLMs and elastic infrastructure positions cloud as the default for new deployments, strengthening vendor recurring-revenue streams and deepening customer engagement across the document capture software market.

Cloud subscription models reshape total cost of ownership, shifting budgets from capital to operating expenditure and enabling SMEs to access enterprise-grade capabilities. Continuous delivery of AI upgrades shortens innovation cycles, ensuring users gain incremental accuracy gains without disruptive platform migrations. Consequently, the document capture software industry sees accelerated feature parity across geographies, reinforcing cloud’s leadership.

By Organization Size: SME Acceleration Challenges Enterprise Dominance

Large enterprises account for 54.06% of the document capture software market size, but SMEs are expanding at 13.71% CAGR. The UK’s SME Digital Adoption Taskforce underlines policy support designed to spur productivity improvements. GenX AI-OCR targets SME pain points with 96% accuracy and wizard-based configuration. No-code platforms lower technical hurdles, allowing line-of-business teams to automate previously manual workflows. Vendors now adapt pricing tiers, training assets, and partner ecosystems to court the mid-market segment.

Enterprise-class buyers continue to drive volume but emphasize deep ERP integrations and advanced compliance modules. SMEs prize speed, affordability, and turnkey templates. This bifurcation compels suppliers to maintain dual roadmaps, ensuring the document capture software market captures expansion on both fronts.

By Capture Technique: AI/ML Disrupts OCR Leadership

OCR retains the largest share at 38.42%, yet intelligent document processing is rising at 11.85% CAGR. super.AI’s LLM intelligence provisions zero-shot learning for unseen layouts. Q1 2025 improvements push OCR accuracy to 99.56%, while LLM post-processing elevates low-quality image results. IDP blends text extraction with contextual reasoning, delivering substantial error-reduction in loan-application and claims-processing workflows.

Intelligent character recognition and intelligent document recognition bridge legacy and next-generation techniques, whereas mobile capture satisfies distributed-workforce demand. Financial institutions report 80% processing-speed gains and 95% error reductions after adopting IDP. This trajectory signals a long-term transition toward AI-native architectures within the document capture software market.

By End-user Industry: Healthcare Disrupts BFSI Dominance

BFSI segments led with 22.61% share of the document capture software market in 2024, deploying high-precision parsing for KYC and fraud checks. Healthcare, however, shows 12.04% CAGR driven by mandates to digitize patient records and achieve interoperability benchmarks. Japanese hospitals pilot GenOCR to extract handwritten physician notes, cutting chart-coding time by 60%. Government agencies follow suit as e-government programs mature, while retail applies automation to supply-chain documentation. Manufacturing harnesses IDP for quality-control certificates, and legal practices automate contract analysis, demonstrating sectoral breadth.

Vertical-specific features-such as HIPAA compliance for healthcare or Basel III reporting for banking-shape product roadmaps. Providers increasingly bundle pre-trained models tuned for domain jargon, cementing their role in widening adoption across the document capture software market.

Geography Analysis

North America commands 37.91% of revenue, benefiting from early cloud adoption, robust venture funding, and a dense ecosystem of technology vendors. US enterprises prioritize end-to-end automation, often standardizing on platforms that couple IDP with robotic process automation and analytics. Canadian and Mexican firms adopt capture to navigate cross-border trade documentation, reinforcing regional cohesion. Government incentives and stringent financial-sector regulation reinforce demand.

Asia-Pacific is the fastest-growing territory at 11.34% CAGR. Japan leads innovation, where Jinbay’s GenOCR processes complex forms at 99% accuracy for construction and manufacturing. China and India propel volume through public-sector digitization, while South Korea and Singapore emerge as AI research hubs. Subsidies and cloud-first directives accelerate enterprise adoption, allowing the document capture software market to scale rapidly across diverse economic profiles.

Europe balances sophistication with regulatory rigor. GDPR and sovereign-cloud policies condition deployment models, but EU targets for 100% online public services energize investment. Germany, France, and the UK spearhead enterprise rollouts, whereas Denmark showcases measurable savings from electronic invoicing. Open-banking and e-invoice mandates harmonize standards across member states, extending addressable demand. Elsewhere, South America, the Middle East, and Africa register steady uptake as infrastructure improves and governments digitize procurement. Though their combined share is modest, local partners and affordable SaaS tiers broaden the document capture software market footprint.

Competitive Landscape

The document capture software market shows moderate concentration. ABBYY, Hyland, and Tungsten Automation fortify portfolios with generative-AI services and ready-made connectors. ABBYY’s 2024 R&D expansion in India augments engineering capacity and localizes language models. Hyland’s Content Innovation Cloud vision pivots from content management to intelligent automation, positioning the firm for upsell into legacy accounts.

Tungsten Automation integrates AI agent builders that slash configuration time, elevating total-agility retention rates. OpenText reports USD 5.8 billion fiscal-2024 revenue with cloud sales at USD 1.8 billion, highlighting commercial momentum. Hyperscience advances its Hypercell platform with deeper enterprise connectors, aiming to displace manual keying in highly regulated workflows.

Disruptors employ large language models to approach human-level comprehension. DeepOpinion gained IDC Innovator status by demonstrating straight-through processing for semi-structured forms. CAPSYS introduces IoT-connected scanners for point-of-origin capture, minimizing latency in logistics environments. SMA Technologies acquired Encapture to weave IDP into broader automation suites, illustrating convergence between capture and orchestration. Patent filings emphasize annotation-based review and AI-generated document synthesis, indicating expansion into adjacent lifecycle phases.

Platform consolidation and full-stack strategies raise switching costs, but open-source pressure restrains license inflation in the SME segment. Edge analytics and privacy-preserving AI remain white-space arenas where no clear leader yet dominates, setting the stage for next-wave differentiation in the document capture software market.

Document Capture Software Industry Leaders

Kofax Inc.

Hyland Software, Inc.

ABBYY Solutions Ltd.

OpenText Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Laserfiche launched Smart Fields with handwriting recognition and Smart Chat, enabling conversational access to repositories while automating data extraction

- June 2025: Jinbay Corporation upgraded GenOCR to capture handwritten text, formulas, and diagrams at 99% accuracy, targeting engineering processes

- March 2025: Hyperscience released a new Hypercell version focusing on deeper system integration and advanced document processing

- February 2025: CAPSYS Technologies introduced IoT Smart Connected Scanning powered by CAPSYS CAPTURE ONLINE, delivering encrypted, PC-free point-of-origin capture

Global Document Capture Software Market Report Scope

| Cloud |

| On-premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Optical Character Recognition (OCR) |

| Intelligent Character Recognition (ICR) |

| Intelligent Document Recognition (IDR) |

| Intelligent Document Processing (AI/ML) |

| Mobile / Smart Capture |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Retail and eCommerce |

| Manufacturing |

| Legal and Professional Services |

| Education |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Turkey | ||

| Saudi Arabia | ||

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Deployment | Cloud | ||

| On-premise | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Capture Technique | Optical Character Recognition (OCR) | ||

| Intelligent Character Recognition (ICR) | |||

| Intelligent Document Recognition (IDR) | |||

| Intelligent Document Processing (AI/ML) | |||

| Mobile / Smart Capture | |||

| By End-user Industry | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| Government and Public Sector | |||

| Retail and eCommerce | |||

| Manufacturing | |||

| Legal and Professional Services | |||

| Education | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Turkey | |||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is demand growing for intelligent document processing solutions?

IDP is forecast to expand at 11.85% CAGR through 2030 as enterprises shift from rule-based OCR to contextual AI extraction.

Which deployment option will dominate spending by 2030?

Cloud already captures 64.21% of spending and is projected to outpace all other models at 12.67% CAGR.

What vertical shows the highest future growth potential?

Healthcare is advancing at 12.04% CAGR, driven by patient-data digitization mandates and interoperability goals.

Why are SMEs adopting capture platforms more quickly than large enterprises?

Cloud subscriptions, no-code configuration, and government productivity programs reduce cost and skill barriers, enabling 13.71% CAGR in the SME segment.

What region leads innovation in AI-OCR accuracy?

Asia-Pacific, especially Japan, where solutions such as GenOCR achieve 99% accuracy on complex handwritten documents.

How does generative AI change the competitive landscape?

Vendors integrate LLMs to achieve straight-through processing, raising switching costs and creating new service-revenue streams.

Page last updated on: