Cloud Backup Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.13 Billion |

| Market Size (2031) | USD 21.62 Billion |

| Growth Rate (2026 - 2031) | 24.84% CAGR |

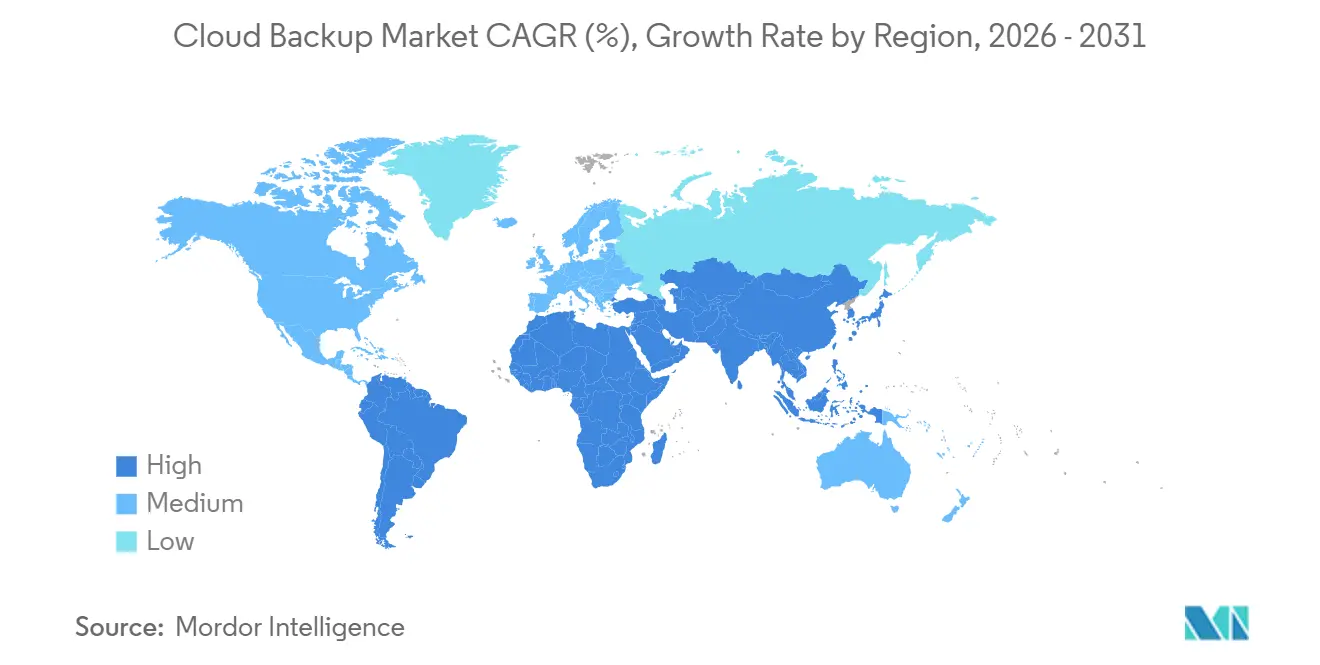

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

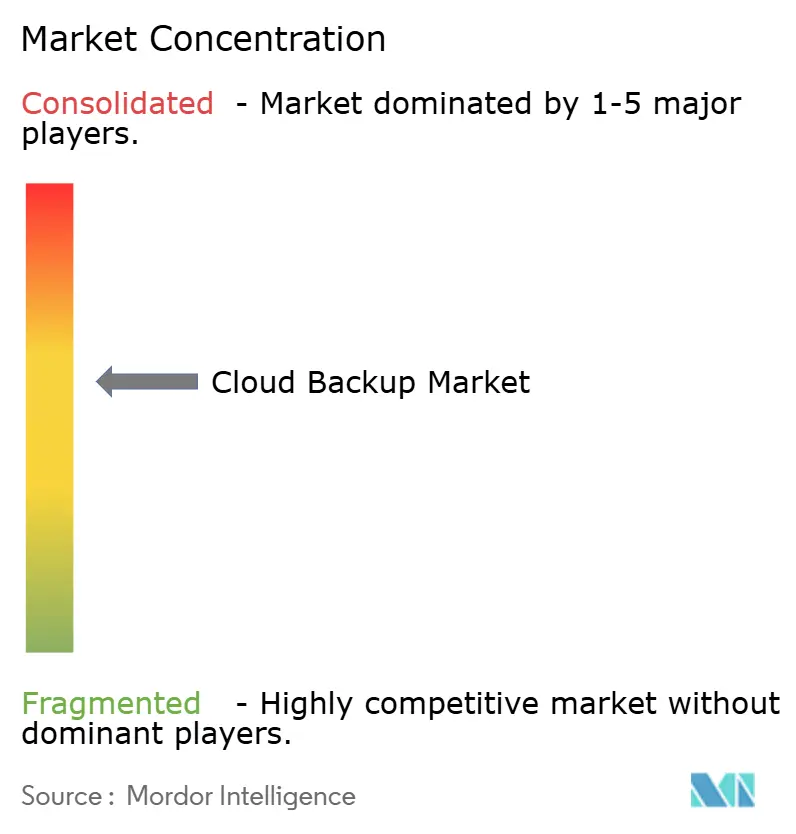

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Backup Market Analysis by Mordor Intelligence

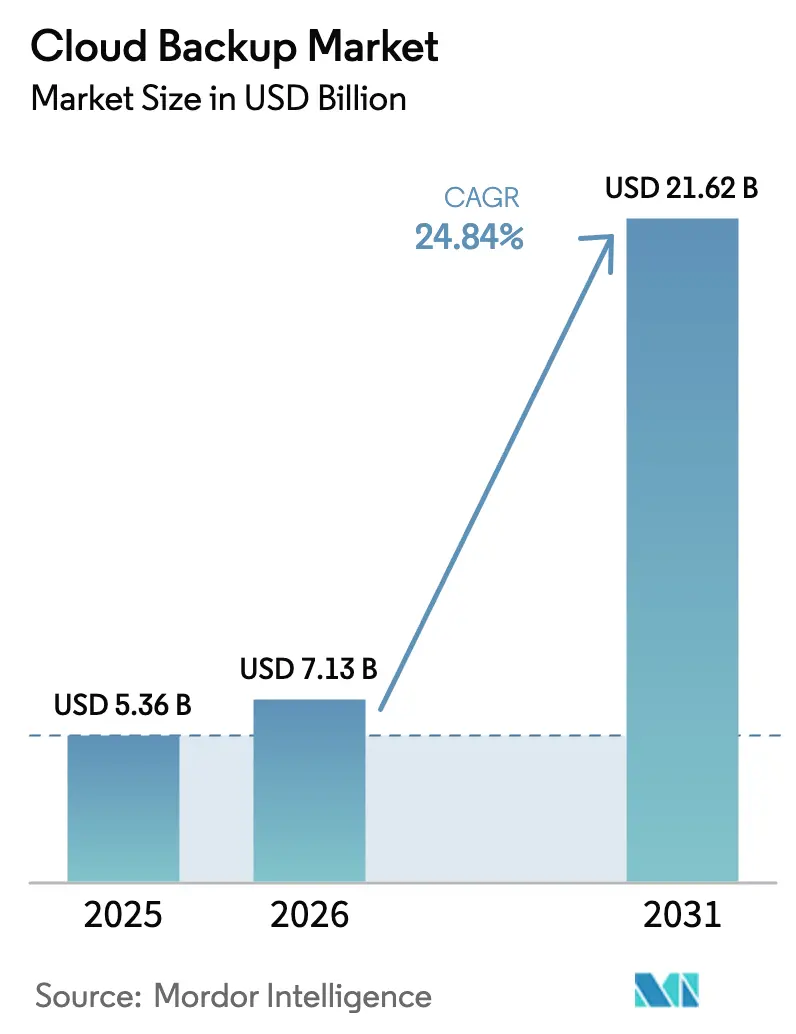

The Cloud Backup Market size was valued at USD 5.36 billion in 2025 and is estimated to grow from USD 7.13 billion in 2026 to reach USD 21.62 billion by 2031, at a CAGR of 24.84% during the forecast period (2026-2031).

Escalating cyber-extortion, rapid SaaS proliferation, and strict data-resiliency rules are accelerating the pivot from tape libraries to elastic cloud repositories. Consolidation is gathering pace as vendors seek scale to counter hyperscaler bundles, while consumption-based pricing realigns outlays with data growth. Localization mandates are fragmenting architectures into in-country vaults, immutable storage is now table-stakes for ransomware insurance, and managed service specialists are capitalizing on operational complexity, especially among small and medium-sized enterprises. These dynamics reinforce long-run adoption momentum across every major industry vertical.

Key Report Takeaways

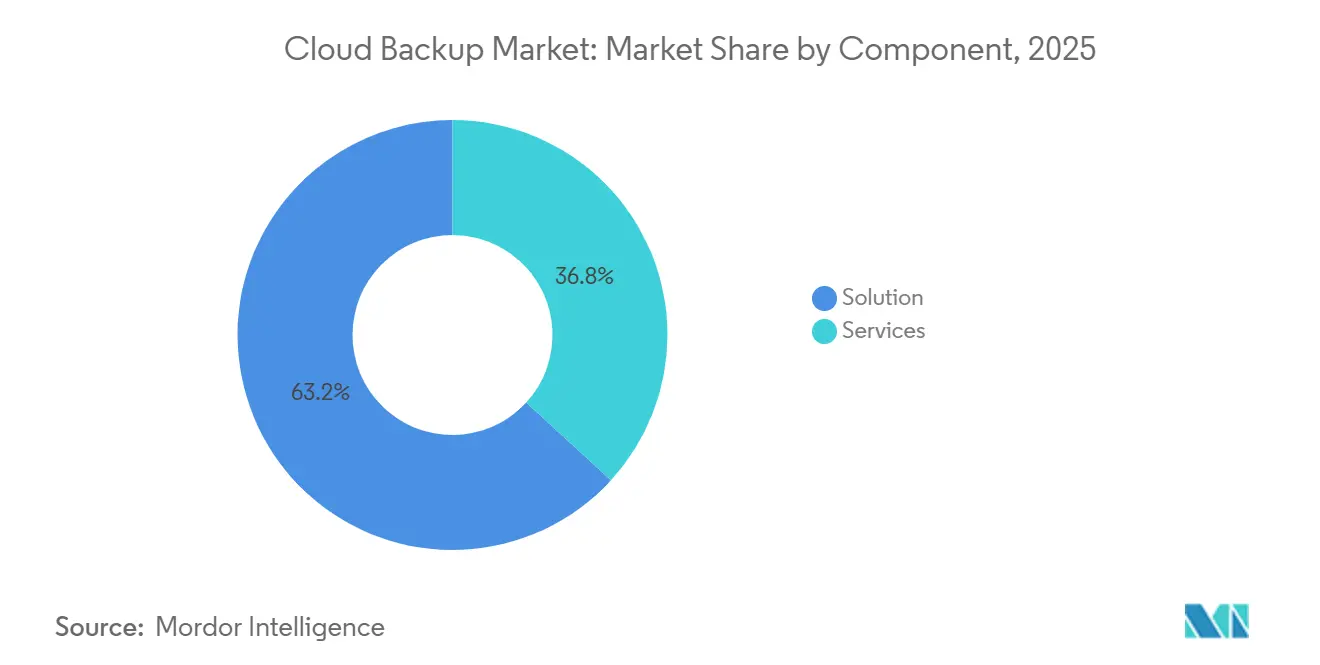

- By component, solution licenses and storage subscriptions held 63.19% of the cloud backup market in 2025, whereas services are expanding faster at a 25.99% CAGR to 2031.

- By deployment model, public cloud led with 48.41% of 2025 revenue, while hybrid cloud shows the highest projected growth at 25.59% CAGR through 2031.

- By end-user industry, banking, financial services and insurance delivered 26.06% of 2025 demand; healthcare is forecast to advance at a 26.71% CAGR to 2031.

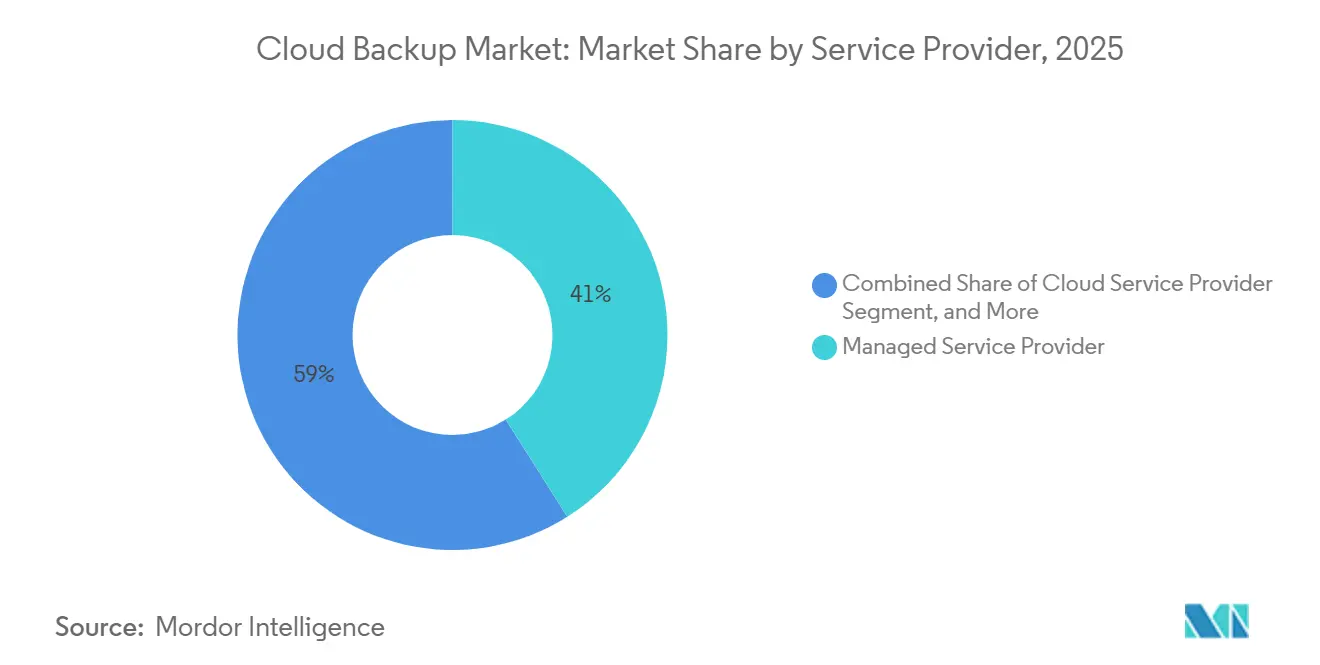

- By service provider, managed service providers captured 41.04% share in 2025 and are projected to expand at a 26.32% CAGR, outpacing cloud and telecom providers.

- By organization size, large enterprises represented 57.22% of revenue in 2025, whereas small and medium-sized enterprises are projected to grow at 26.19% CAGR through 2031.

- By geography, North America accounted for 35.06% of 2025 revenue; Asia Pacific is the fastest-growing region at 26.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cloud Backup Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Massive Growth in Data Generation Requiring Affordable, Scalable Storage | +5.20% | Global, with peak intensity in North America and Asia Pacific | Long term (≥ 4 years) |

| Accelerated Enterprise Adoption of SaaS Platforms Driving Integrated Backup Demand | +4.80% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising Enterprise-wide Cloud Computing Maturity Levels | +4.10% | North America and Europe core, spillover to Asia Pacific | Medium term (2-4 years) |

| Heightened Regulatory Focus on Data-Protection and Resiliency Mandates | +3.90% | Europe (GDPR), North America (CCPA, HIPAA), Asia Pacific (PIPL, DPDP) | Short term (≤ 2 years) |

| Surge in Adoption of Immutable Storage for Ransomware Insurance Compliance | +3.60% | North America and Europe, expanding to Asia Pacific | Short term (≤ 2 years) |

| Growing Use of AI-Based Data Classification to Optimize Backup Footprints | +2.80% | North America and Europe early adopters, gradual Asia Pacific uptake | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Massive Growth in Data Generation Requiring Affordable, Scalable Storage

Enterprises created 120 zettabytes of data in 2024, straining fixed-capacity arrays. Consumption-based cloud backup aligns cost with active datasets and removes three-year hardware refresh cycles. Hyperscalers’ cold object tiers such as Amazon S3 Glacier Instant Retrieval deliver sub-cent-per-gigabyte pricing, enabling decade-long retention without disproportionate spend.[1]AMAZON, “Amazon S3 Pricing,” aws.amazon.com Edge caching that transmits only changed blocks mitigates bandwidth limitations, while analytics on backup telemetry support proactive capacity planning. These factors collectively underpin sustained demand for the cloud backup market.

Accelerated Enterprise Adoption of SaaS Platforms Driving Integrated Backup Demand

Microsoft 365 surpassed 400 million paid seats in 2024, yet Microsoft’s shared-responsibility model excludes application-layer protection.[2]MICROSOFT, “Microsoft 365 Shared Responsibility Model,” learn.microsoft.com Enterprises therefore deploy workload-aware tools that snapshot Exchange, SharePoint, and OneDrive data outside the 93-day recycle-bin window. Similar gaps exist for Salesforce and Google Workspace, and the average company now uses 130 SaaS tools. Unified policy engines that orchestrate granular snapshots across disparate APIs have become critical, elevating the cloud backup market as a core pillar of SaaS governance.

Rising Enterprise-Wide Cloud Computing Maturity Levels

Hybrid and multi-cloud backups underpin 78% of 2025 deployments, demanding coverage for on-premises clusters, hyperscaler instances, and Kubernetes workloads under a single control plane. SaaS-delivered management eliminates site-specific agents, reducing mean time-to-recover. Container environments require snapshots that include persistent volumes plus configuration metadata, while policy portability helps enterprises avoid lock-in amid expanding provider portfolios. This maturity accelerates recurring demand for the cloud backup market.

Heightened Regulatory Focus on Data-Protection and Resiliency Mandates

GDPR Article 32 mandates rapid restoration, U.S. Regulation S-P sets 30-day breach-notification clocks, and CISA directive 23-01 requires immutable copies for federal systems.[3]UNITED STATES SECURITIES AND EXCHANGE COMMISSION, “Regulation S-P Amendments,” sec.gov China’s PIPL and India’s DPDP impose in-country storage, splintering architectures into national vaults. Healthcare entities must also satisfy HIPAA encryption and audit requirements. Compliance complexity elevates backup from an insurance policy to a board-level priority, reinforcing expansion of the cloud backup market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Data-Sovereignty and Cross-Border Transfer Restrictions | -2.40% | Europe (GDPR), China (PIPL), India (DPDP), Brazil (LGPD) | Short term (≤ 2 years) |

| Persistent Privacy and Security Concerns Around Multi-Tenant Clouds | -1.80% | Global, with heightened scrutiny in Europe and North America | Medium term (2-4 years) |

| Escalating Hyperscaler Data-Egress Charges Hindering Recovery Economics | -2.10% | Global, particularly impacting multi-cloud and hybrid deployments | Medium term (2-4 years) |

| Scarcity of Edge-Grade Backup Solutions for Operational-Technology Workloads | -1.30% | Manufacturing hubs in Asia Pacific, Europe, and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Data-Sovereignty and Cross-Border Transfer Restrictions

China’s PIPL forces personal data to remain onshore, while India’s DPDP empowers the government to designate restricted categories. European exporters must verify third-country surveillance laws before transfer, inflating due-diligence overhead. These rules drive multinationals to duplicate repositories across jurisdictions, raising infrastructure costs yet stimulating regional spending within the cloud backup market.

Escalating Hyperscaler Data-Egress Charges Hindering Recovery Economics

AWS, Azure, and Google levy USD 0.08-0.12 per gigabyte for outbound traffic. A single 100-terabyte restore therefore incurs up to USD 12,000, discouraging routine test drills. Although Amazon removed exit fees for permanent migrations in 2024, standard recovery operations remain chargeable, nudging enterprises toward hybrid topologies where primary copies sit on-premises. Pending antitrust probes may soften the restraint, yet fees currently temper cloud backup market adoption curves in egress-heavy industries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Expand on Integration Complexity

Solution contracts commanded 63.19% revenue in 2025, yet services are forecast to grow faster at 25.99% CAGR. The cloud backup market size for services reflects rising demand for architecture design, policy scripting, and managed testing. Enterprises that juggle multi-tenant SaaS, container clusters, and legacy mainframes outsource integration to specialists, lifting deal values. Vendors embed AI to classify data and assign retention tiers automatically, tightening compliance posture while lowering storage overhead.

Services growth is reinforced by consumption subscriptions that bundle storage, software, and support. Metallic charges per protected workload, which simplifies procurement for finance teams. Independent validation of backup integrity has become a regulatory staple, boosting third-party audit services. Managed Service Providers with ISO 27001 or SOC 2 certifications capture premium contracts, supporting long-run expansion of the cloud backup market.

By Deployment Model: Hybrid Configurations Balance Sovereignty and Elasticity

Public cloud led 2025 demand at 48.41%, yet hybrid cloud is projected to advance at 25.59% CAGR as firms reconcile in-country mandates with hyperscaler economics. The cloud backup market share for hybrid designs rises when regulators prescribe data localization while boards insist on offsite redundancy. Hybrid topology also supports tiered recovery: mission-critical workloads restore from on-premises copies within minutes, whereas archival data recovers from cloud repositories over hours.

Edge computing widens hybrid relevance. Stores, plants, and towers replicate local snapshots to central clouds during off-peak windows, preserving bandwidth headroom. The EU Data Act, effective in 2024, obliges providers to enable portability, trimming migration risk and further bolstering hybrid adoption. Overall, flexible deployment choice remains a leading purchase criterion in the cloud backup market.

By End-User Industry: Healthcare Accelerates Amid Ransomware Surge

Banking, financial services and insurance supplied 26.06% of 2025 revenue, propelled by Basel III recovery objectives and PCI DSS encryption rules. Healthcare is poised for the fastest 26.71% CAGR through 2031 as ransomware attacks multiply and insurers require immutable copies before underwriting policies. The cloud backup market size for healthcare therefore widens materially, aided by vault features that isolate recovery points from operational credentials.

Manufacturing, media, retail, and government buyers add tailwinds. Media firms protect petabyte-scale video, retailers secure distributed point-of-sale data, and agencies comply with NIST SP 800-53 benchmarks. Each vertical exhibits nuanced workload mixes, but all converge on immutable, API-integrated recovery workflows that sustain total demand for the cloud backup market.

By Service Provider: MSPs Dominate Channel Distribution

Managed Service Providers held 41.04% share in 2025 and are forecast to grow at 26.32% CAGR. Aggregated purchasing power lets MSPs negotiate storage discounts and deliver white-label backup-as-a-service platforms. Veeam’s program enrolled over 35,000 partners, exemplifying scale leverage. Telecom carriers and hyperscalers supply native options, yet their feature velocity trails best-of-breed specialists, maintaining healthy MSP differentiation.

Cyber-recovery add-ons boost margins: vault hosting, incident response, and quarterly drills underscore value beyond commodity storage. As enterprises pursue OpEx predictability, subscription bundles are displacing break-fix billing, sustaining long-run revenue for MSPs and enlarging their position inside the cloud backup market.

By Organization Size: SMEs Embrace Cloud-Native Simplicity

Large enterprises accounted for 57.22% revenue in 2025, but SMEs are projected to outpace them at 26.19% CAGR through 2031. Flat-rate bundles with no egress fees resonate with budget-constrained firms. Backblaze’s 25% year-on-year growth underscores this momentum. Automated policy templates, pre-built SaaS connectors, and browser-based dashboards replace specialist staff, letting SMEs achieve enterprise-grade resilience.

Conversely, complex environments keep large enterprises invested in high-end platforms. Database-consistent snapshots for Oracle and SAP, plus detailed audit exports for Sarbanes-Oxley, drive premium license renewals. Both cohorts therefore sustain layered demand, broadening the user base for the cloud backup market.

Geography Analysis

North America held 35.06% of 2025 revenue thanks to early cloud adoption and mature continuity planning. HIPAA, Sarbanes-Oxley, and state breach laws create compliance urgency, while dense hyperscaler footprints cut latency and enable in-region restores. Asia Pacific is projected to expand at 26.89% CAGR to 2031, the quickest worldwide. China’s PIPL and India’s DPDP enforce in-country storage, fragmenting architectures yet spurring localized spending that lifts the cloud backup market in both nations.

Europe’s landscape is defined by GDPR plus Standard Contractual Clauses that demand granular export controls. Providers hosting data inside EU availability zones enjoy procurement preference, and immutable archives help satisfy Article 17 “right to erasure” requests without compromising record integrity. South America, the Middle East and Africa remain nascent but attractive. Brazil’s LGPD mirrors GDPR, driving encryption and reporting requirements; Gulf states are building sovereign clouds to attract foreign direct investment.[4]AMAZON, “Global Infrastructure,” aws.amazon.com

Latency-sensitive workloads lead firms to replicate across multiple regions. AWS counts 33 global regions and Azure runs over 60, permitting fine-grained vault placement. Edge micro-data centers in stores, factories, or cell towers add another layer, requiring local snapshots before synchronizing to central repositories. These geographic nuances collectively reinforce robust regional pipelines for the cloud backup market.

Competitive Landscape

The cloud backup market shows moderate concentration. Hyperscalers Amazon Web Services, Microsoft, Google, IBM, and Oracle exploit integrated stacks, yet specialists Veeam, Veritas, Commvault, Cohesity, Rubrik, Acronis, Druva, and Arcserve remain competitive through immutable storage, ransomware orchestration, and application-aware snapshots. Rubrik’s April 2024 IPO raised USD 752 million at a USD 5.6 billion valuation, funding cyber-recovery vault expansion. The Cohesity-Veritas merger in December 2024 produced a USD 7 billion entity with 12,000 customers.

Strategic themes include a shift from perpetual licenses to subscriptions, AI-driven data classification, and predictive capacity planning. Veeam’s December 2025 completion of its USD 1.73 billion Securiti purchase embeds automated sensitivity labelling that tiers low-priority data into cold storage. White-space opportunities persist in edge and operational-technology protection for manufacturing and energy networks and in coverage for emerging SaaS platforms such as Workday and ServiceNow.

Startups emphasize zero-trust architectures, requiring multi-factor authentication for deletions and write-once logs that flag unauthorized actions. As hyperscalers bundle elementary backup into broader IaaS contracts, specialists differentiate through faster restore times, policy granularity, and cross-platform intelligence. The interplay sustains healthy competition and continued innovation across the cloud backup market.

Cloud Backup Industry Leaders

IBM Corporation

Backblaze Inc.

Barracuda Networks, Inc.

Microsoft Corporation

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Veeam completed its USD 1.73 billion acquisition of Securiti, integrating AI-driven data classification to automate policy assignment and storage tiering.

- October 2025: Veeam announced plans to acquire Securiti for USD 1.73 billion to enhance compliance reporting capabilities.

- February 2025: Microsoft made a strategic investment in Veeam to deepen Azure integration for Microsoft 365 protection.

- December 2024: Cohesity finalized its merger with Veritas, creating a USD 7 billion data-management vendor with USD 1.5 billion annual recurring revenue.

Global Cloud Backup Market Report Scope

The Cloud Backup Market Report is Segmented by Component (Solution, Services), Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), End-User Industry (Banking Financial Services and Insurance, IT and Telecom, Media and Entertainment, Retail, Healthcare, Manufacturing, Government and Public Sector, Education, Other End-User Industries), Service Provider (Managed Service Provider, Cloud Service Provider, Telecom and Communication Provider, Other Service Providers), Organization Size (Large Enterprises, Small and Medium-Sized Enterprises), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solution |

| Services |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Banking, Financial Services and Insurance |

| IT and Telecom |

| Media and Entertainment |

| Retail |

| Healthcare |

| Manufacturing |

| Government and Public Sector |

| Education |

| Other End-User Industries |

| Managed Service Provider |

| Cloud Service Provider |

| Telecom and Communication Provider |

| Other Service Providers |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| ASEAN | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Solution | |

| Services | ||

| By Deployment Model | Public Cloud | |

| Private Cloud | ||

| Hybrid Cloud | ||

| By End-User Industry | Banking, Financial Services and Insurance | |

| IT and Telecom | ||

| Media and Entertainment | ||

| Retail | ||

| Healthcare | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Education | ||

| Other End-User Industries | ||

| By Service Provider | Managed Service Provider | |

| Cloud Service Provider | ||

| Telecom and Communication Provider | ||

| Other Service Providers | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the cloud backup market today?

The cloud backup market size reached USD 7.13 billion in 2026 and is forecast to climb to USD 21.62 billion by 2031.

What CAGR is expected for cloud backup spending through 2031?

Global revenue is projected to grow at a 24.84% CAGR between 2026 and 2031, reflecting sustained demand for cyber-resilient storage.

Which deployment model is expanding the fastest?

Hybrid cloud backup is projected to register the highest 25.59% CAGR as organizations balance sovereignty mandates with hyperscaler elasticity.

Why is healthcare seeing rapid backup adoption?

Healthcare providers face intensified ransomware attacks and stricter insurance prerequisites that mandate immutable, regularly tested backups, driving a 26.71% CAGR.

How are data-egress charges influencing architecture?

Ongoing egress fees of USD 0.08-0.12 per gigabyte make large-scale restores expensive, pushing many enterprises toward hybrid designs that keep primary copies on-premises.

Who dominates channel distribution in backup services?

Managed Service Providers hold the largest 41.04% share thanks to aggregated buying power and value-added cyber-recovery offerings.

Page last updated on: