Purpose-Built Backup Appliance (PBBA) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.23 Billion |

| Market Size (2031) | USD 16.23 Billion |

| Growth Rate (2026 - 2031) | 9.67% CAGR |

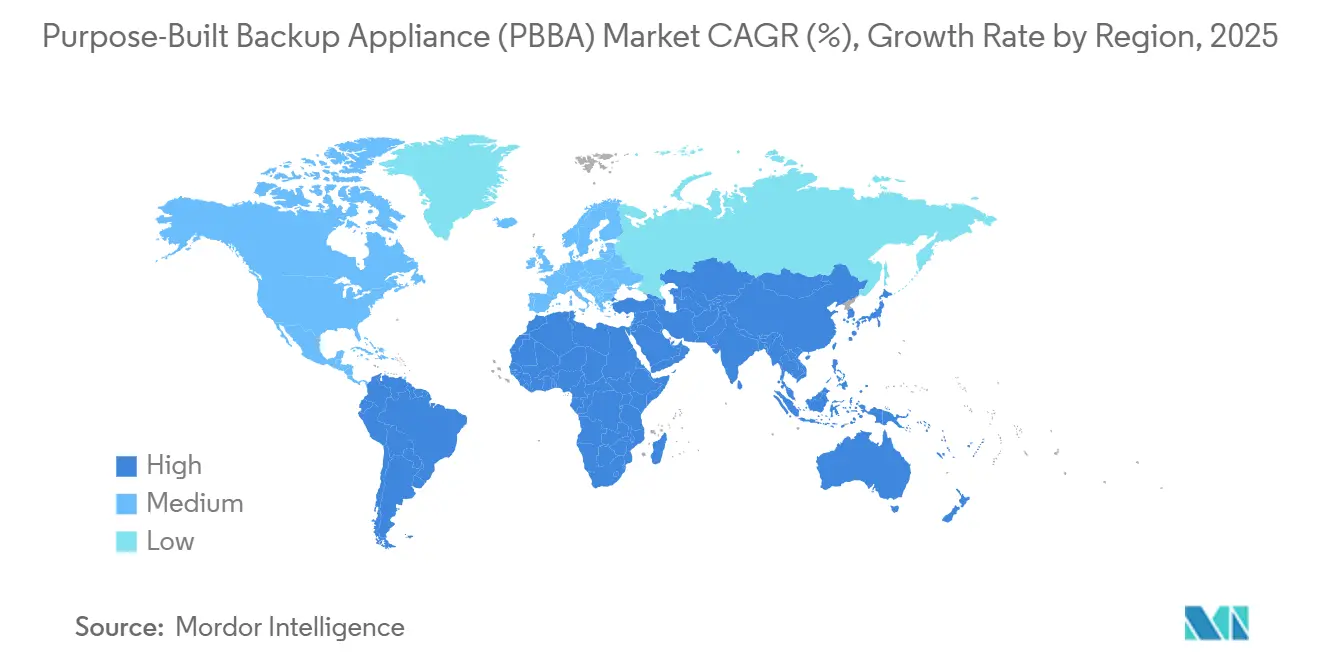

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

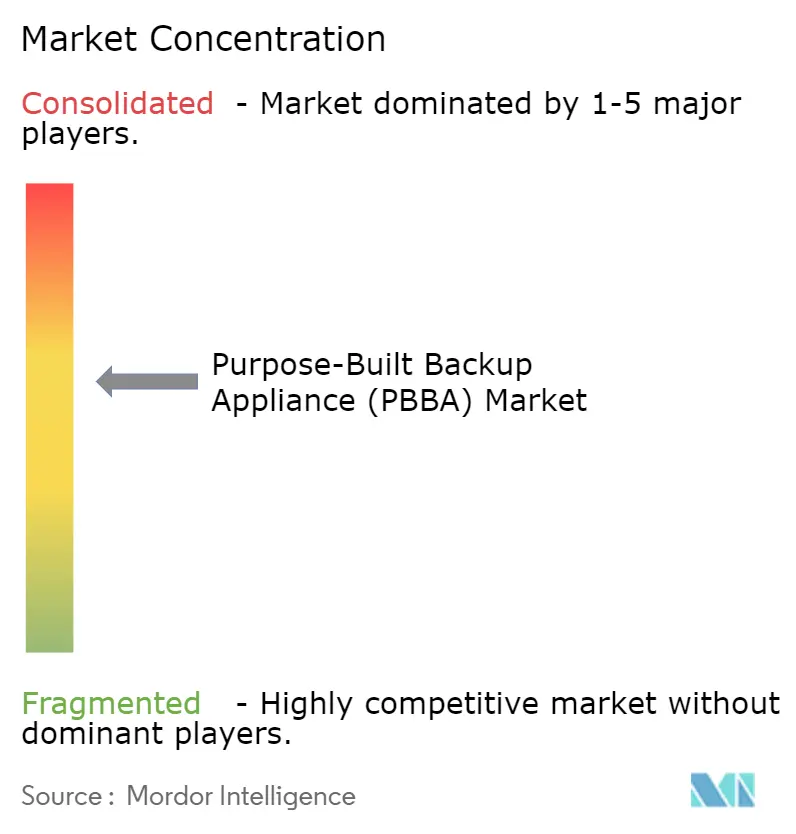

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Purpose-Built Backup Appliance (PBBA) Market Analysis by Mordor Intelligence

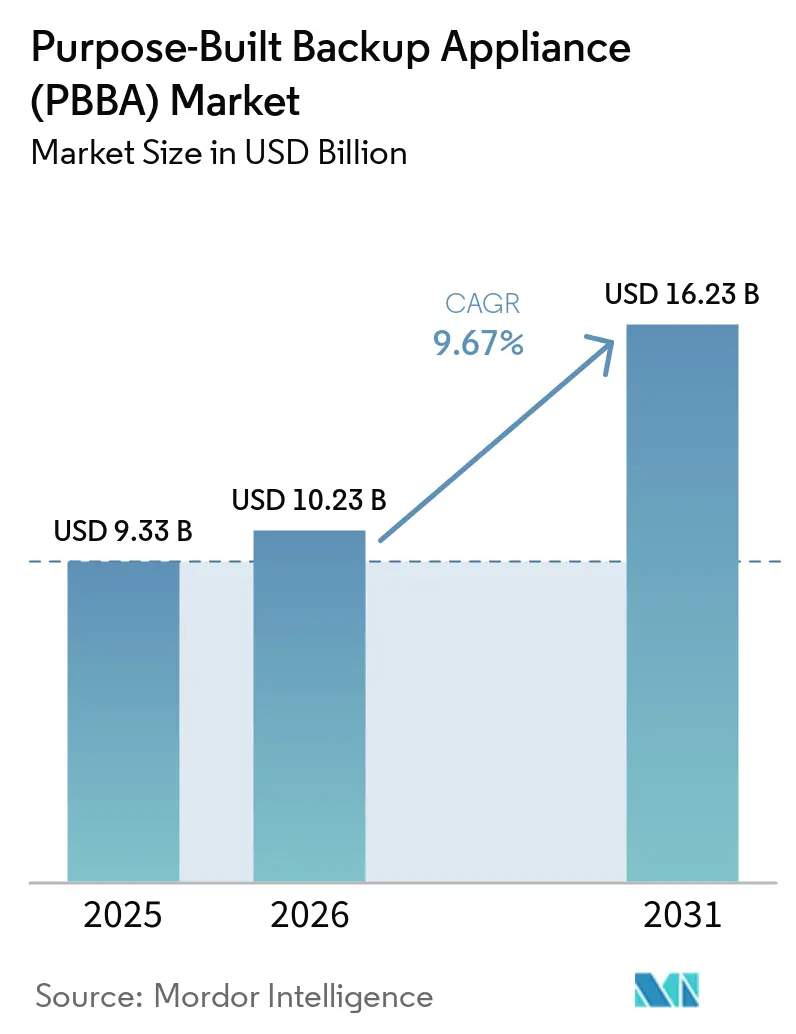

The market size of the Purpose-Built Backup Appliance (PBBA) market was valued at USD 9.33 billion in 2025 and is expected to increase to USD 10.23 billion in 2026. By 2031, the market is projected to surge to USD 16.23 billion, marking a robust CAGR of 9.67% from 2026 to 2031. Elevated ransomware frequency, the flash-storage supply shock that began in 2025, and board-level mandates for immutable data copies have shifted backup infrastructure from a capacity add-on to a frontline risk-mitigation asset. Buyers now treat cyber-recovery capability as a decisive specification, and vendors are responding with appliance portfolios that embed anomaly detection engines, cyber-vault orchestration, and consumption-based pricing. Equipment lead-times lengthened in 2025 as triple-level-cell SSD prices spiked, so enterprises adopted hybrid systems that layer high-speed flash on dense nearline disks to balance recovery performance with cost. Taken together, these forces underpin robust demand and reinforce the long-run growth profile of the purpose-built backup appliance market.

Key Report Takeaways

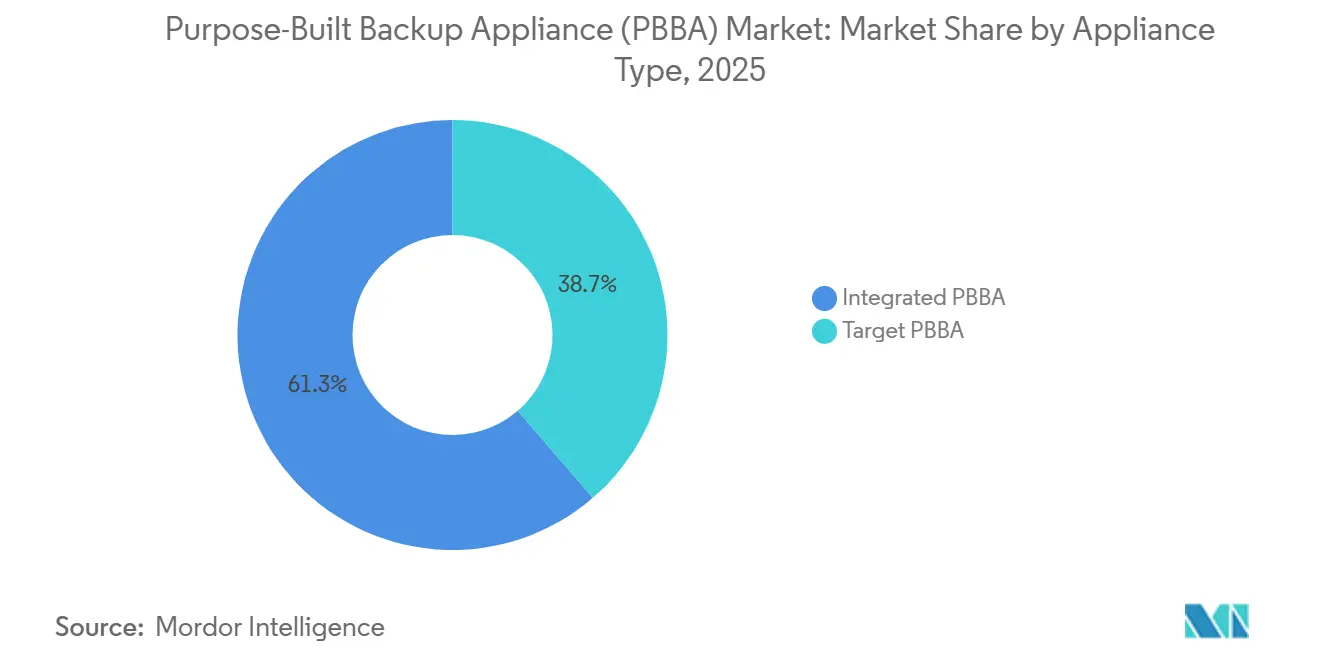

- By appliance type, integrated systems led with 61.32% revenue share in 2025, while target appliances posted the fastest projected 11.34% CAGR through 2031.

- By deployment mode, on-premises configurations held 49.82% of 2025 revenue, whereas hybrid models are advancing at a 10.46% CAGR as firms combine local flash restores with cloud object retention.

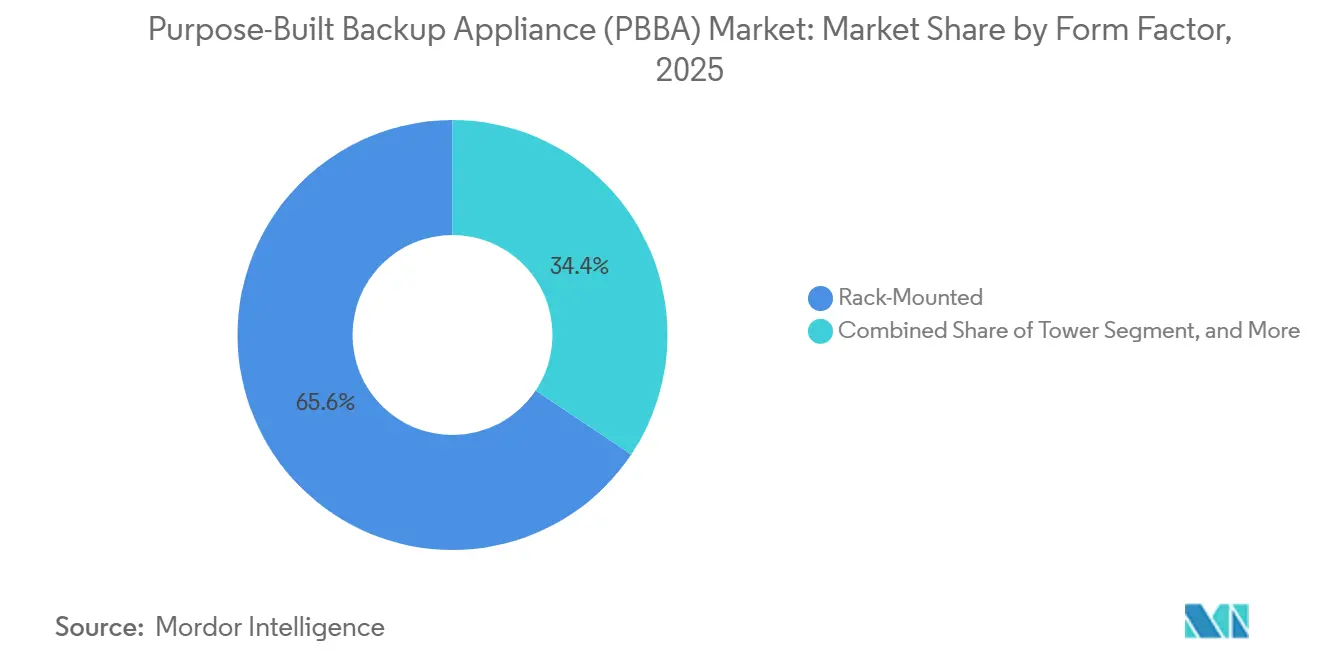

- By form factor, rack-mounted models accounted for 65.63% of 2025 sales, yet modular scale-out nodes are expanding at 10.69% CAGR thanks to their sub-100 TB incremental expansion capability.

- By end-user industry, banking and financial services accounted for 27.89% of 2025 demand, while telecom and media are projected to grow at a 9.78% CAGR due to rising 5G core data volumes.

- By geography, North America contributed 37.78% of 2025 revenue, whereas Asia-Pacific is forecast to rise at 9.96% CAGR on the back of USD 772 billion in data-center capital spending.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Purpose-Built Backup Appliance (PBBA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding ransomware incidents elevating demand for immutable backup targets | +2.8% | North America, Europe | Short term (≤ 2 years) |

| Mandatory data-sovereignty and cyber-resiliency regulations in OECD and BRICS | +2.1% | Asia-pacific, Europe | Medium term (2-4 years) |

| Cloud-connected PBBA integrated into hybrid-IT architectures | +1.9% | North America, Europe, Asia-pacific | Medium term (2-4 years) |

| Hardware-level support for object-lock and WORM enabling cyber-insurance discounts | +1.4% | Global | Short term (≤ 2 years) |

| Edge-ready micro-PBBA for OT / IIoT environments | +0.9% | Manufacturing hubs | Long term (≥ 4 years) |

| Purpose-built backup for AI model checkpoints and unstructured data lakes | +0.6% | North America, China, select Asia-pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding Ransomware Incidents Elevating Demand for Immutable Backup Targets

Ransomware attackers compromise backup repositories in 96% of successful breaches, making immutable storage a frontline defense. Tiered architectures such as ExaGrid’s non-network-facing repository layer now isolate data from production networks. [1]VMblog Staff, “ExaGrid CEO on Tiered Backup Storage,” VMblog, VMBLOG.COM AI-driven anomaly detection flags suspicious deletions and triggers automated safeguards. Cyber-insurance providers grant 10-15% premium reductions to clients deploying certified immutable targets. Object First’s Ootbi appliance achieves eleven-nines durability while maintaining a complete air gap. These economic and security incentives accelerate Purpose-Built Backup Appliance market adoption across regulated industries.

Mandatory Data-Sovereignty and Cyber-Resiliency Regulations in OECD and BRICS

India’s Digital Personal Data Protection Act requires in-country storage for payment data, pushing local appliance deployments. GDPR enforcement in Europe has levied EUR 1.32 billion in fines, reinforcing the need for verifiable backup controls. [2]U.S. ITC Analysts, “Changing Tides of GDPR Enforcement,” USITC, USITC.GOV Brazil’s AI strategy revived the debate on digital sovereignty, highlighting the role of localized infrastructure. Appliances with object-lock and geo-fencing enable enterprises to satisfy residency rules without ceding operational flexibility. Data-Residency-as-a-Service platforms such as InCountry underscore emerging demand for compliant regional backup nodes. NIST’s revised framework now embeds backup integrity as a mandatory resilience control.

Cloud-Connected PBBA Integrated into Hybrid-IT Architectures

Hybrid deployments blend low-latency local recovery with cloud scalability, reducing total cost of ownership by 30-40%. Appliances such as Azure Stack Edge deliver compute and storage at branch sites while replicating to Azure for disaster recovery. AI workloads spur demand for protection of model checkpoints, with sparse checkpointing cutting backup overhead by 60%. Cohesity’s joint solution with Lenovo centralizes backup across core, cloud, and edge, supporting up to 64 TB per node. Consumption-based subscriptions such as HPE GreenLake align expenditures with usage, further propelling hybrid Purpose-Built Backup Appliance market demand.

Hardware-Level Support for Object-Lock and WORM Enabling Cyber-Insurance Discounts

Quantum’s DXi all-flash systems enforce WORM at the controller layer, delivering cryptographic authentication of every write. Dell’s PowerProtect portfolio integrates hardware-based immutability that meets federal security criteria while retaining multi-cloud mobility. Some insurers now require such capabilities for policy renewal in high-risk verticals, offering 10-20% premium cuts when verified. Blockchain audit trails add further assurance, enabling tamper-proof evidence for compliance reviews. These incentives strengthen the Purpose-Built Backup Appliance market as enterprises weigh cyber-risk transfer against capital investments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of agentless cloud backup-as-a-service reducing on-prem PBBA spend | -1.8% | North America, Europe | Short term (≤ 2 years) |

| Budget squeeze amid macro IT cap-ex re-prioritization | -1.2% | Global mid-market | Medium term (2-4 years) |

| Supply-chain volatility in high-density HDD and LTO media | -0.9% | Asia manufacturing hubs | Short term (≤ 2 years) |

| Perceived vendor lock-in due to proprietary file systems | -0.7% | Global enterprise | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Agentless Cloud Backup-as-a-Service Reducing On-Prem PBBA Spend

Cloud-native offerings deliver agentless protection with 40-60% lower total cost of ownership compared with appliance ownership. Veeam’s Microsoft partnership channels AI analytics into policy management, attracting SaaS-first buyers. Even so, data-localization rules and recovery-time guarantees keep hybrid models relevant, prompting Commvault’s acquisition of Clumio to widen cloud coverage.[3]Ron Miller, “Commvault Buys Clumio,” TechCrunch, TECHCRUNCH.COM Vendors thus hedge with subscription services layered on existing hardware portfolios. The restraint lies in diverted cap-ex, not the elimination of the Purpose-Built Backup Appliance market.

Budget Squeeze Amid Macro IT Cap-ex Re-Prioritization

AI infrastructure soaks up 35% annual budget growth, leaving limited headroom for storage refreshes. Enterprises prolong appliance lifecycles and insist on pay-per-use models. Arcserve’s OneXafe Solo bundles backup-as-a-service to sidestep up-front capital. Rising HDD and LTO costs compound spending hesitancy, with suppliers imposing 10-20% price hikes amid demand spikes. Vendors answer by integrating deduplication ratios exceeding 30:1 to stretch available capacity, preserving the Purpose-Built Backup Appliance industry through efficiency gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Appliance Type: Integrated Dominance Meets Target Flexibility

Integrated systems generated 61.32% of 2025 revenue, anchoring the purpose-built backup appliance market share by combining storage media, software, and deduplication in a single SKU. Banking and healthcare buyers appreciate the unified support path and predictable maintenance windows. Target appliances are projected to log an 11.34% CAGR through 2031 as enterprises that standardize on Commvault or Veeam favor protocol-flexible storage pools that avoid software lock-in. The purpose-built backup appliance market size attached to target platforms is expected to outpace integrated models in the second half of the forecast horizon, driven by container-native data flows and multi-cloud workload mobility.

Modular licensing blurs the integrated-versus-target distinction. Quantum’s DXi-series firmware now lets administrators flip between modes without swapping hardware. This elasticity extends asset life by up to three budget cycles and supports phased migrations when application portfolios shift. Vendors updating appliances over-the-air rather than through forklift replacements also reduce customer churn and seed recurring revenue.

By Deployment Mode: Hybrid Becomes the Norm

On-premises installations retained 49.82% of 2025 spending as latency-sensitive workloads and sovereignty laws restrict off-site replication. Hybrid deployments are scaling at a 10.46% CAGR to 2031 because firms keep hot restores on local flash while pushing long-term copies to low-cost object stores, cutting storage expense by more than half for cold data sets. The purpose-built backup appliance market size tied to hybrid architectures should climb steadily as WAN optimization algorithms mature and cloud egress fees remain punitive for bulk restores.

Nevertheless, network bandwidth often caps cloud replication volume, and a 100 TB recovery from a hyperscaler can incur USD 9,000 in transfer fees. Suppliers now bundle layered deduplication, adaptive tiering, and bandwidth throttling. ExaGrid’s January 2026 release prioritizes datasets most likely to be restored, freeing bandwidth for mission-critical objects. These enhancements widen the hybrid appeal without compromising recovery-time objectives.

By Form Factor: Scale-Out Nodes Challenge Rack Staples

Rack-mounted chassis contributed 65.63% of 2025 revenue, fitting neatly into raised-floor footprints and colocation power envelopes. Yet modular scale-out nodes, forecast to add 10.69% CAGR, let data-intensive users expand in bite-size units when flash lead-times exceed 16 weeks. Cohesity’s C6800 platform supports 60 TB node increments that slot into existing clusters with zero downtime. Healthcare providers processing ever-larger CT and MRI images embraced this flexibility, turning modular clusters into the fastest-growing slice of the purpose-built backup appliance market.

Scale-out topologies also simplify phased refresh cycles, enabling customers to retire the oldest nodes and bleed in new ones without wholesale migrations. Power-and-cooling stress declines because smaller nodes spread heat load, a benefit in colocation halls where wholesale pricing has topped USD 196 per kW per month. That cost efficiency sharpens the competitive edge of modular appliances versus monolithic racks.

By End-User Industry: Regulation Drives Banking, Data Explodes in Telecom

Banking and financial services captured 27.89% of 2025 revenue after DORA imposed two-hour recovery objectives and quarterly test mandates. Appliances able to auto-generate immutable test logs have become de facto purchase prerequisites. Telecom and media are forecast to grow at a 9.78% CAGR as 5G standalone cores crank out petabytes of call-detail records requiring multi-year retention. The purpose-built backup appliance market share held by telecom carriers should climb steadily because lawful-intercept, fraud analytics, and edge-cloud architectures converge on the need for rapid recovery.

Healthcare purchasing momentum accelerated after U.S. regulators proposed a 72-hour ePHI restore window, a bar that tape libraries cannot meet. Defense and government demand is pent-up but hampered by budget holds and security certifications. Manufacturing and retail show mid-single-digit growth; both rely on on-premises appliances to safeguard IoT telemetry and point-of-sale data where WAN links prove insufficient for nightly cloud replication.

Geography Analysis

North America generated 37.78% of 2025 revenue, its cyber-insurance underwriters compelling policyholders to operate immutable backups and quarterly restore tests. Vacancy in the region’s data-center market fell to 1.4% during 2025, and Northern Virginia alone absorbed 1,102 MW of additional capacity, a scenario that amplified appetite for high-density backup gear placed inside colocation suites. Power pricing above USD 190 per kW tipped procurement toward liquid-cooled appliance lines such as Dell’s PowerProtect DP5500, which boosts deduplication throughput per rack unit while cutting thermal load.

Asia-Pacific is on track for a 9.96% CAGR through 2031, undergirded by USD 772 billion in data-center pipelines that add 24 GW of capacity between 2025 and 2030. India’s installed base could multiply sixfold by 2032, and Johor, Malaysia, already hosts 897 MW with a sub-1% vacancy rate. Sovereignty laws barring cross-border replication obligate enterprises to deploy local backup appliances, bolstering the purpose-built backup appliance market in jurisdictions where hyperscale cloud coverage lags. KPMG projects the region’s data-center power demand will climb to 37,580 MW by 2030, a 165% jump from 2024 levels, indicating corresponding acceleration for associated data-protection infrastructure.

Europe’s growth leans on DORA compliance across financial services, while Middle East and Africa momentum stems from sovereign AI infrastructure such as Saudi Arabia’s HUMAIN project that earmarks 6 GW for GPU-rich data halls. These new facilities require flash-heavy backup appliances able to restore 10 TB model checkpoints within minutes, driving niche demand for GPU-tuned platforms. South America remains modest in scale, with Brazil’s financial regulators and Argentina’s telecom operators forming the primary purchase base.

Competitive Landscape

The purpose-built backup appliance market displays moderate concentration: the top five suppliers account for roughly 55-60% of revenue. Legacy system vendors defend rack platforms with bundled financing and support. Software-defined challengers court container workloads using Kubernetes-native agents and metered billing. The March 2025 Cohesity-Veritas merger formed a 10,000-account giant, underscoring that channel depth now outranks feature velocity in saturated markets. Rubrik’s 2024 IPO bankrolled global expansion and acquisitions like Laminar, bringing continuous data classification into its stack.

White-space persists in edge-to-cloud tiering, GPU-training data checkpoints, and cost-optimized SMB appliances that bundle S3-compatible object stores. Object First, for example, shaves 30-40% from total cost by collapsing compute and disk into a single enclosure, resonating with price-sensitive midsize firms. Vendors unable to document DORA-compliant orchestration or HIPAA-grade audit trails face disqualification in highly regulated tenders, pushing the competitive bar toward integrated compliance tooling.

High-density liquid-cooled chassis gained traction when colocation power tariffs exceeded USD 190 per kW. Dell’s DP5500 series upped deduplication throughput by 40% per rack unit, addressing both performance and energy constraints. Hewlett Packard Enterprise’s GreenLake backup-as-a-service, launched March 2026, places vendor-owned hardware on customer premises yet bills by protected terabyte, an option that resonates with organizations hesitant to commit up-front capital but unwilling to relinquish on-site data residency.

Purpose-Built Backup Appliance (PBBA) Industry Leaders

Dell Technologies Inc.

International Business Machines Corporation

Veritas Technologies LLC

Hewlett Packard Enterprise Company

Quantum Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cohesity released Gaia, an AI-powered data-management platform that cuts false-positive ransomware alerts by 85%.

- March 2026: Hewlett Packard Enterprise added backup-as-a-service to GreenLake, delivering on-premises capacity with monthly usage billing.

- February 2026: Dell Technologies debuted the liquid-cooled PowerProtect DP5500 modular line, boosting deduplication throughput per rack unit by 40%.

- January 2026: Veeam partnered with Nvidia to accelerate AI-training checkpoint snapshots, trimming overhead from 12 minutes to 90 seconds.

Global Purpose-Built Backup Appliance (PBBA) Market Report Scope

The Purpose-Built Backup Appliance Market Report is Segmented by Appliance Type (Integrated PBBA, Target PBBA), Deployment Mode (On-Premises, Cloud-Connected, Hybrid), Form Factor (Rack-Mounted, Tower, Modular/Scale-Out Nodes), End-User Industry (Banking and Financial Services, Healthcare and Life Sciences, Government and Defense, Telecom and Media, Manufacturing, Retail and e-Commerce), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Integrated PBBA |

| Target PBBA |

| On-Premises |

| Cloud-Connected |

| Hybrid |

| Rack-Mounted |

| Tower |

| Modular / Scale-Out Nodes |

| Banking and Financial Services |

| Healthcare and Life Sciences |

| Government and Defense |

| Telecom and Media |

| Manufacturing |

| Retail and e-Commerce |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa |

| Segmentation by Appliance Type | Integrated PBBA | |

| Target PBBA | ||

| Segmentation by Deployment Mode | On-Premises | |

| Cloud-Connected | ||

| Hybrid | ||

| Segmentation by Form Factor | Rack-Mounted | |

| Tower | ||

| Modular / Scale-Out Nodes | ||

| Segmentation by End-User Industry | Banking and Financial Services | |

| Healthcare and Life Sciences | ||

| Government and Defense | ||

| Telecom and Media | ||

| Manufacturing | ||

| Retail and e-Commerce | ||

| Segmentation by Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current purpose-built backup appliance market size and how fast is it growing?

The purpose-built backup appliance market size is USD 10.23 billion in 2026 and is projected to reach USD 16.23 billion by 2031 at a 9.67% CAGR, according to Mordor Intelligence.

Which appliance type holds the largest share?

Integrated systems command 61.32% of 2025 revenue because they bundle storage, software, and deduplication into one turnkey platform.

Which appliance type holds the largest share today?

Integrated systems lead with 61.32% Purpose-Built Backup Appliance market share in 2024.

Which deployment model is growing the fastest?

Hybrid deployments combining local flash restores with cloud object retention are advancing at a 10.46% CAGR as buyers balance performance against storage cost.

How big is the banking segment in this market?

Banking and financial services generated 27.89% of 2025 demand, driven by EU Digital Operational Resilience Act compliance mandates.

Why are modular scale-out nodes gaining popularity?

Scale-out nodes allow sub-100 TB incremental expansion, minimize procurement lead-time risk, and cut stranded capacity, factors that push their growth to a 10.69% CAGR through 2031.

Page last updated on: