Market Overview

| Study Period | 2021 - 2031 |

|---|---|

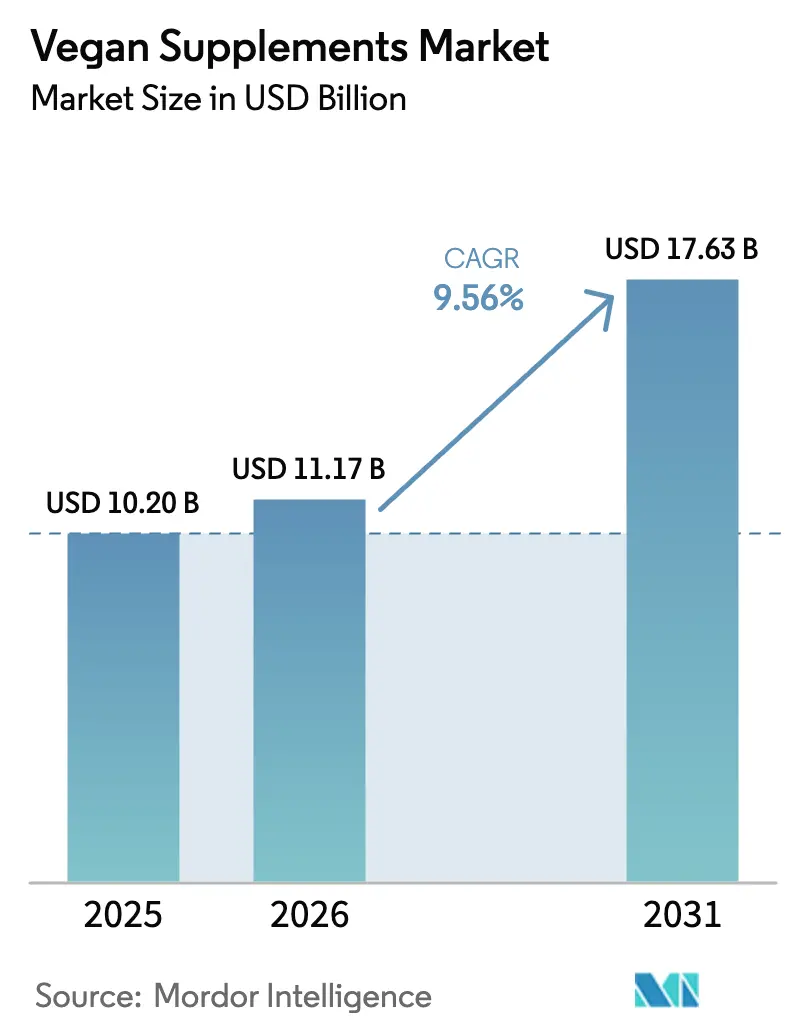

| Market Size (2026) | USD 11.17 Billion |

| Market Size (2031) | USD 17.63 Billion |

| Growth Rate (2026 - 2031) | 9.56% CAGR |

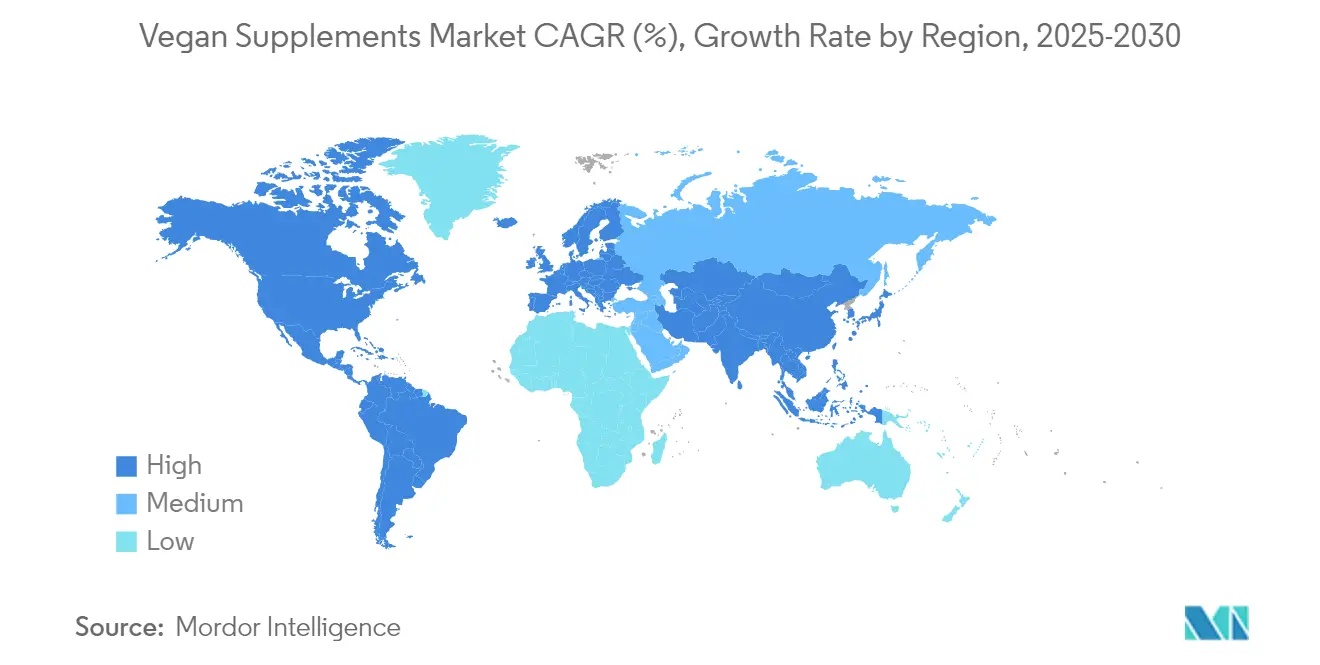

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vegan Supplements Market Analysis by Mordor Intelligence

The vegan supplements market size was valued at USD 10.20 billion in 2025 and estimated to grow from USD 11.17 billion in 2026 to reach USD 17.63 billion by 2031, at a CAGR of 9.56% during the forecast period (2026-2031). This growth reflects a compound annual growth rate (CAGR) of 9.68% during the forecast period of 2025-2030. The market is being driven by several factors, including increasing health awareness among millennials, stricter regulations promoting the fortification of food products, and innovations in sustainable ingredients. Large food and pharmaceutical companies are using vertical integration strategies to streamline their operations and scale up production to meet the rising demand. Currently, North America leads the market in terms of revenue, but the Asia-Pacific region, particularly India, is growing at the fastest rate due to increasing consumer awareness and demand for plant-based products. Among the various product types, vitamins hold the largest share of the market, while prebiotics are emerging as the fastest-growing segment due to their benefits for gut health. In terms of product formats, gummies are becoming increasingly popular and are growing faster than traditional capsules, as they are more convenient and appealing to consumers. Algae-based omega-3 supplements are gaining traction among premium consumers who are willing to pay more for high-quality, plant-based alternatives. Children’s formulas are becoming a significant growth area, as parents are increasingly looking for vegan and healthier options for their kids. The market is highly fragmented, with many small and niche players competing for market share.

Key Report Takeaways

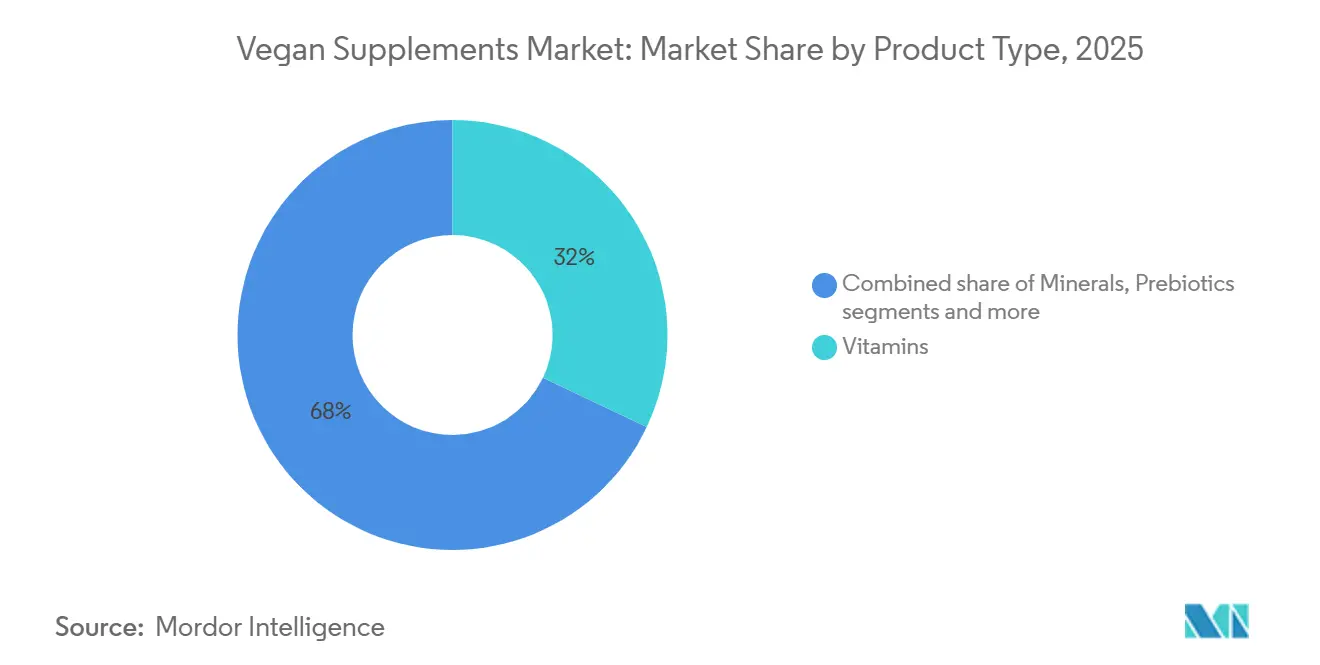

- By product type, vitamins held 32.03% of the vegan supplements market share in 2025, while prebiotics are set to advance at 11.44% CAGR through 2031.

- By form, capsules and softgels captured 45.58% of the vegan supplements market size in 2025; gummies are projected to rise at a 11.84% CAGR to 2031.

- By function, general wellness led with 37.96% revenue share in 2025; immune support is forecast to grow at 11.02% CAGR to 2031.

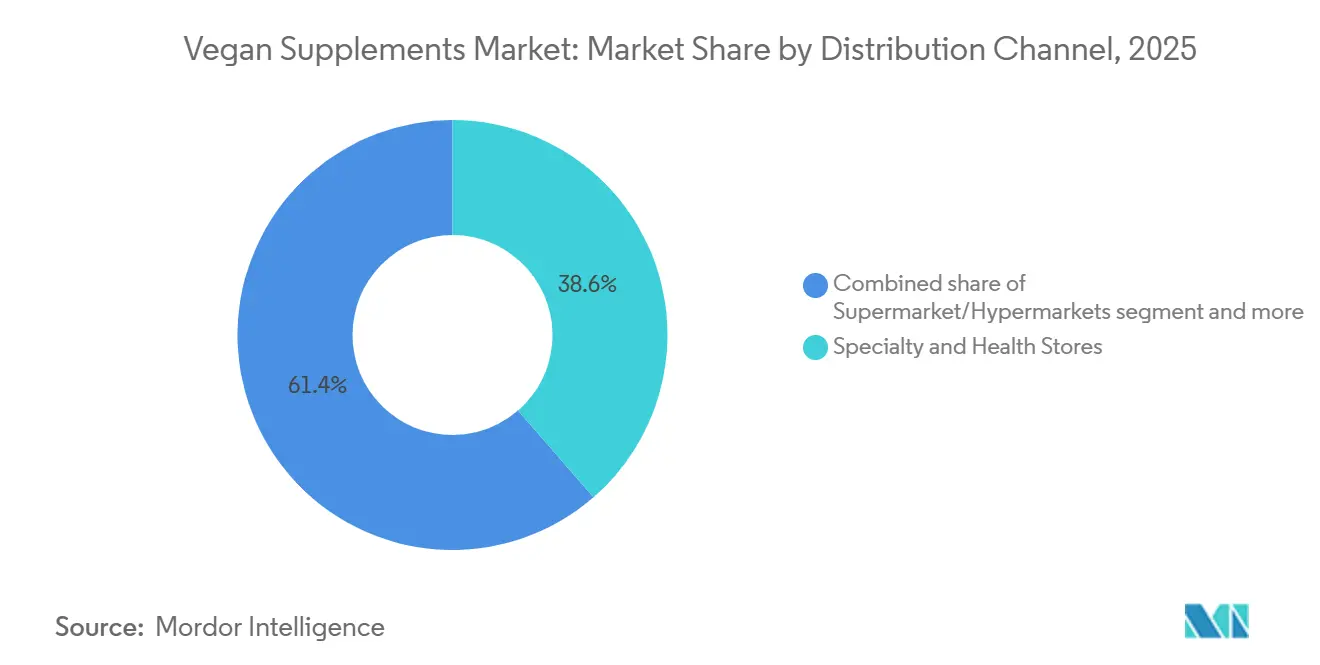

- By distribution channel, specialty stores accounted for 38.62% of sales in 2025, yet online retail is expected to expand at a 10.27% CAGR through 2031.

- By end user, adults dominated the vegan supplements market, holding a 44.73% share. Meanwhile, children's surged ahead as the fastest-growing segment, boasting a 9.88% CAGR through 2031.

- By geography, North America commanded 37.74% of 2025 revenue; Asia-Pacific is set to climb at 9.75% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Vegan Supplements Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing consumer preference for vegan diets | +2.1% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Growing demand for vegan prenatal supplements among millennial parents | +1.8% | North America and Europe core, spill-over to Asia-Pacific urban centers | Short term (≤ 2 years) |

| Government fortification regulations increasing demand for iron-rich vegan supplements | +1.5% | Europe, North America, with emerging adoption in India and Southeast Asia | Long term (≥ 4 years) |

| Rising adoption of algae-based omega-3 as a sustainable alternative | +1.3% | Global, with premium markets in North America and Northern Europe | Medium term (2-4 years) |

| Increasing integration of ayurvedic and botanical ingredients | +1.0% | Global, with strongest demand in North America and India | Medium term (2-4 years) |

| Innovation in formulations and delivery formats | +0.9% | Global, with technology hubs in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing consumer preference for vegan diets increases market demand

The global vegan supplements market is expanding quickly as more people embrace plant-based diets due to concerns about sustainability, environmental impact, and health benefits. Millennials, flexitarians, and health-conscious individuals are at the forefront of this shift, opting for alternatives to animal-based products. According to the World Population Review, as of 2025, countries with the highest percentage of vegans include India (9%), Mexico (9%), Israel (5%), Canada (4.6%), and Ireland (4.1%) [1]Source: World Population Review, "Veganism by Country 2025," worldpopulationreview.com. This growing trend is also evident in the sports nutrition industry, where athletes like Venus Williams advocate for vegan supplements, highlighting their advantages in improving performance and aiding recovery. The popularity of plant-based diets has led to significant growth in the food sector. For instance, the Plant Based Foods Association of the United States reported that sales of plant-based foods reached USD 8.1 billion in 2024 [2]Source: Plant Based Foods Association, “PBFA Marketplace,” plantbasedfoods.org. This surge in demand reflects the increasing acceptance of vegan products across various consumer groups.

Growing demand for vegan prenatal supplements among millennial parents

Millennial parents are increasingly choosing vegan prenatal supplements due to their preference for clean-label, ethically sourced, and environmentally friendly products during pregnancy. This generation is actively looking for alternatives to traditional fish-oil-based DHA, opting instead for plant-based options like algae-derived omega-3s and naturally sourced folate. These choices help avoid concerns about toxins, allergens, and synthetic additives, ensuring safer and healthier options for both the mother and baby. Organizations such as the American Pregnancy Association recommend plant-based DHA for expectant mothers, while certifications from groups like The Vegan Society ensure that vegan prenatal products meet strict ethical and nutritional standards[3]Source: American Pregnancy Association, “Omega‑3 Fish Oil and Pregnancy,” americanpregnancy.org. Millennial parents often plan pregnancies well in advance, leading to longer periods of supplement use. This trend increases the lifetime value of customers, as many begin taking supplements before conception and continue through the postpartum phase.

Government fortification regulations increasing demand for iron-rich vegan supplements

Government-mandated fortification policies are playing a significant role in increasing the demand for iron-rich vegan supplements. Public health authorities are focusing on addressing micronutrient deficiencies by implementing standardized nutrition guidelines. In regions like the U.S. and the European Union, regulations are encouraging the use of plant-based, bioavailable forms of iron and vitamin D2 in fortified foods and supplements. This has led brands to prioritize higher-quality vegan ingredients to meet these requirements. For instance, in June 2024, the Government of Canada approved vitamin D fortification in yogurt, including plant-based options, highlighting growing regulatory support for vegan-friendly fortification strategies [4]Source: Health Canada, “Fortified Foods: Canada’s Approach to Fortification,” Canada.ca. These developments are driving the demand for specialized vegan iron compounds, such as ferrous bisglycinate and encapsulated plant-based iron, which are known for their effectiveness and compatibility with vegan diets.

Rising adoption of algae-based omega-3 as a sustainable alternative

Algae-based omega-3 supplements are becoming increasingly popular as a sustainable and ethical alternative to traditional fish oil. These supplements address both environmental and health concerns effectively. Unlike fish oil, algae-based omega-3 provides the same essential fatty acids, EPA and DHA, without the risk of contaminants such as mercury or microplastics. Additionally, they help reduce the strain on overfished marine ecosystems, making them an eco-friendly choice. In 2024, the launch of Life’s DHAA B54-0100, which delivers 620 mg of omega-3 per dose in a compact capsule format, opened up new possibilities for use in gummies and chewable supplements. This innovation caters to consumers who prioritize convenience and taste. Advancements in photobioreactor technology have made algae cultivation more efficient, requiring less land, water, and energy compared to fish-based sources. With the growing focus on sustainability and health-conscious choices, algae-based omega-3 supplements are expected to see significant demand.

Restraints Impact Analysis of Vegan Supplements Market*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High production costs and premium pricing restrict the growth of vegan supplements | -1.7% | Global, with acute impact in price-sensitive emerging markets | Medium term (2-4 years) |

| Supply chain disruptions impede vegan supplements market expansion | -1.2% | Global, with China dependency creating vulnerability | Short term (≤ 2 years) |

| Limited consumer awareness and misconceptions hinder vegan supplements adoption | -0.9% | Emerging markets in Asia-Pacific and Latin America, rural regions globally | Long term (≥ 4 years) |

| Stringent regulatory and certification processes | -0.6% | Europe, North America, with emerging complexity in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production costs and premium pricing restrict the growth of vegan supplements

The vegan supplements market is experiencing challenges due to higher production costs, which make these products less affordable for many consumers. Plant-based supplements are often 24–115% more expensive than traditional options. This is because their production involves advanced processes like precision fermentation, clean extraction methods, and obtaining multiple certifications such as vegan, non-GMO, and organic. Since 2024, global price fluctuations in raw materials, particularly for essential components like vitamins A and D, have further increased costs. Supply chain disruptions in key regions like China and Europe have also contributed to these price hikes. This price gap is especially noticeable in emerging markets, where consumers are more sensitive to costs and may find it harder to afford premium-priced products. As a result, vegan supplements are primarily adopted in wealthier urban areas. However, advancements in technology, such as microbial production of vitamins through synthetic biology and fermentation, are gradually improving production efficiency.

Supply chain disruptions impede vegan supplements market expansion

The vegan supplements market faces challenges due to its dependence on specific regions, particularly China, for raw materials like vitamins, amino acids, and botanical extracts. This reliance makes the market vulnerable to disruptions such as rising freight costs, regulatory changes, and geopolitical tensions. For example, proposed tariffs in the United States on Chinese-made vitamins could significantly increase production costs for vegan supplements. Climate-related issues are impacting the supply of key ingredients. Droughts in India have reduced the availability of adaptogens like ashwagandha, while anchovy shortages in Peru, which are crucial for some algal omega-3 production processes, highlight the fragility of marine-linked supply chains. To address these challenges, companies are exploring alternative sourcing options in regions like Southeast Asia, Latin America, and Europe. However, ensuring consistent quality and traceability with new suppliers remains a hurdle. These ongoing issues are causing delays, increasing costs, and slowing the global expansion of vegan supplement production.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Vegan Supplements Market Segment Analysis

By Product Type:

Vitamins Lead While Prebiotics SurgeIn 2025, vitamins contributed to 32.03% of the total revenue in the vegan supplements market, driven by the essential need for nutrients like B12, D3, and others among plant-based consumers. These vitamins are vital for addressing common deficiencies in vegan diets, ensuring proper health and nutrition. Prebiotics, although currently a smaller segment, are gaining significant traction with an expected annual growth rate of 11.44%. This growth is fueled by increasing awareness of gut health and its critical role in boosting immunity. Minerals such as iron and zinc, along with algae-based omega-3 supplements, are also experiencing steady double-digit growth. A notable development in 2024 was the introduction of spirulina-grown bioactive B12, which offers a sustainable and innovative solution for vitamin production, further strengthening the market's potential.

The vegan supplements market has also benefited from regulatory approvals, such as the European Food Safety Authority (EFSA) clearances for mushroom-derived vitamin D2 and magnesium L-threonate. These approvals have encouraged the entry of new brands and products into the market, expanding consumer choices. However, the industry still faces challenges, particularly in improving the absorption rates of supplements and addressing taste-related issues to make products more appealing. Formulation laboratories are actively working on these areas to enhance product quality and consumer satisfaction. With growing consumer demand, scientific advancements, and regulatory support, the vegan supplements market is poised for continued growth and innovation in the coming years.

By Form:

Capsules Dominate as Gummies AccelerateCapsules and softgels made up 45.58% of the vegan supplements market share in 2025, primarily because they offer accurate dosing and are cost-effective. These formats are popular among consumers who prioritize convenience and affordability. However, gummies are quickly gaining traction, growing at a remarkable compound annual growth rate (CAGR) of 11.84%. This growth is driven by their appealing taste and ease of use, making them a preferred choice for many consumers. Innovations such as replacing gelatin with pectin and introducing starch-free production lines are helping reduce waste and energy consumption, making gummies more sustainable.

Tablets continue to attract budget-conscious consumers due to their affordability, while powders remain a favorite among athletes and individuals who prefer adding supplements to smoothies or other beverages. Each format caters to different consumer preferences, ensuring a diverse range of options in the vegan supplements market. As the demand for vegan supplements grows, manufacturers are focusing on improving the quality and functionality of these products to meet the evolving needs of consumers. This includes addressing challenges like ingredient stability and enhancing the overall consumer experience, which will likely drive further innovation and growth in the market.

By Function/Health Benefit:

General Wellness Leads; Immune Support GainsIn 2025, general wellness made up 37.96% of the market's sales, reflecting a growing trend of people prioritizing preventive health to stay healthy and avoid future health issues. Consumers are increasingly choosing vegan supplements as a natural way to support their overall health. Immune support products are leading the growth in this market, with a compound annual growth rate (CAGR) of 11.02%. Ingredients like ashwagandha, elderberry, and high-polyphenol adaptogens are driving this demand. Weight management products are gaining traction, especially as they align with the growing use of GLP-1 therapies. Plant-based protein mixes are particularly popular for helping people maintain lean muscle mass while managing their weight effectively, making them a preferred choice for health-conscious consumers.

Other segments, such as digestive health and beauty-from-within products, are also becoming important growth areas in the vegan supplements market. These products often combine natural plant-based ingredients with clinically proven formulations, offering consumers effective solutions for their health needs. For instance, digestive health products frequently include botanicals and probiotics to improve gut health, while beauty-from-within products focus on enhancing skin, hair, and nail health through vegan-friendly nutrients. This mix of natural and science-backed benefits is reshaping consumer preferences, as more people seek functional products that deliver visible results.

By Distribution Channel:

Specialty Stores Lead; E-commerce AcceleratesSpecialty nutrition stores contributed to 38.62% of the market's revenue in 2025, as they provide tailored advice and a carefully curated selection of products that appeal to health-conscious buyers. These stores offer a personalized shopping experience, helping customers make informed decisions about their health needs. This approach builds trust and loyalty, making specialty stores a preferred choice for many consumers. However, online sales are rapidly gaining traction, with an annual growth rate of 10.27%, which is expected to significantly increase the digital presence of vegan supplements. Direct-to-consumer platforms like Billion Vegans are thriving, achieving high conversion rates while maintaining low customer acquisition costs of under USD 20.

Supermarkets are increasingly dedicating specific sections to plant-based products, making vegan supplements more visible and accessible to a broader audience. This strategy encourages more consumers to explore and purchase these items during their regular shopping trips. At the same time, innovative distribution methods, such as vending machines placed in gyms, are being tested to provide convenient, on-the-go options for fitness enthusiasts. These developments are making vegan supplements more accessible across various retail channels, catering to the changing preferences of consumers.

By End User:

Adults Dominate; Children’s Segment EmergesIn 2025, adults made up 44.73% of the market revenue, driven by the increasing adoption of vegan supplements for lifestyle nutrition and chronic disease prevention. Many adults are incorporating these supplements into their daily routines to maintain overall health and address specific wellness goals. The growing awareness of plant-based nutrition and its benefits has encouraged this shift, as more people look for natural and sustainable ways to support their health. On the other hand, children’s formulas, though currently a smaller segment, are growing at the fastest rate, with a compound annual growth rate (CAGR) of 9.88%. This growth is supported by the rising use of wellness apps among Generation Alpha and parents’ focus on preventive healthcare for their children, ensuring they receive essential nutrients early on.

Gummy supplements for children are becoming increasingly popular because they are easy to consume and appealing to kids. These products make it simpler for parents to ensure their children get the necessary nutrients, but manufacturers must pay extra attention to dosage and safety standards to meet the specific needs of this age group. Meanwhile, senior consumers continue to drive steady demand for vegan supplements that support bone health, joint mobility, and cognitive function. These products are often designed to complement existing medications while minimizing the risk of side effects or interactions.

Geography Analysis

North America Vegan Supplements Market

North America accounted for 37.74% of the market share in 2025, driven by strong support from the FDA’s fortification guidelines and a growing preference for premium, clean-label products. Consumers in this region are increasingly willing to pay more for high-quality vegan supplements, which has encouraged companies to invest heavily in the market. For example, Nestlé’s USD 2.3 billion acquisition of Garden of Life has expanded the availability of plant-based supplements in the region. However, the market faces challenges such as tariff risks and a heavy reliance on East Asia for raw materials. These issues particularly affect price-sensitive consumers, who often prioritize affordability over premium offerings, creating a mixed growth environment in North America.

APAC Vegan Supplements Market

Asia is emerging as a key growth region, with the market expanding at a compound annual growth rate (CAGR) of 9.75%. India’s dietary supplement market is promising, supported by the increasing popularity of Ayurveda and government policies that encourage the use of natural products. Regulatory changes in China and Japan have made it easier for companies to introduce innovative products, such as probiotics and supplements for joint health. Additionally, the rise of mobile commerce and influencer-driven marketing has fueled growth in Southeast Asia, which is growing at 7.1%. However, companies must address challenges like price sensitivity and varying regulatory standards to succeed in this diverse and competitive market.

EMEA and LATAM Vegan Supplements Market

Europe remains a mature yet innovative market, with the European Food Safety Authority (EFSA) setting global benchmarks through its novel food approvals. Over 40% of European consumers prioritize eco-friendly products, and 70% actively seek brands with strong sustainability commitments. Countries like Germany and the Netherlands are leading the way with initiatives such as nutrient guidelines and campaigns promoting plant-based proteins. Despite these advancements, the region faces challenges like post-Brexit regulatory complexities, which have created administrative hurdles for businesses. Meanwhile, regions like Latin America, the Middle East, and Africa are experiencing moderate growth in the mid-single digits.

Competitive Landscape

The vegan supplements market is moderately fragmented, with niche brands gaining popularity in areas like collagen-free sports nutrition, personalized DNA-based supplement packs, and mushroom-based nootropics. Larger companies are responding to this competition through mergers and acquisitions. For example, Nestlé Health Science integrated Nature’s Bounty and Solgar in 2025, while Glanbia acquired Flavor Producers in 2024 for USD 300 million to improve botanical flavor profiles. Technological advancements are also driving innovation, with precision fermentation enabling the production of bio-identical collagen, algae-based EPA/DHA, and vitamin D2 with a lower environmental impact.

Start-ups are leveraging direct-to-consumer channels and content marketing to overcome their limited presence in physical retail stores. Many of these companies are focusing on intellectual property, with an increasing number of patents being filed for innovations like microencapsulation and chelated minerals. Co-manufacturers are scaling up clean-room facilities to produce gummy supplements, which are growing in popularity. To address supply chain challenges, companies are diversifying their sourcing to regions like India, Brazil, and Europe. However, maintaining consistent quality through audits adds to operational costs.

The vegan supplements market is evolving rapidly, driven by innovation and changing consumer preferences. Companies are investing in advanced technologies and sustainable practices to differentiate themselves in a competitive landscape. While larger players are expanding through acquisitions, smaller brands are finding success by focusing on niche segments and leveraging digital marketing strategies. Supply chain diversification and advancements in manufacturing processes are helping to address some challenges, but issues like cost pressures and quality control remain. As the market grows, the ability to adapt quickly and offer science-backed, high-quality products will be key to success.

Vegan Supplements Industry Leaders

-

NOW Foods

-

Glanbia plc

-

Nordic Naturals, Inc.

-

Herbalife Nutrition Ltd.

-

Nestle S.A.

- *Disclaimer: Major Players sorted in no particular order

Vegan Supplements Market Companies Covered in this Report

- NOW Foods

- Glanbia plc

- Nordic Naturals, Inc.

- Herbalife Nutrition Ltd.

- Nestle S.A.

- Deva Nutrition

- Solgar Inc.

- Naturaltein LNG Pvt. Ltd.

- H&H Group

- PlantFusion

- Complement

- The Hut.com Ltd.

- MRO MaryRuth, LLC

- Jarrow Formulas, Inc.

- Sunwarrior LLC

- Nuzest Natural Products Pty Ltd

- Plantigo Nutrition Private Limited

- Ora Organic

- Unived

- Fermentis Life Sciences

Recent Industry Developments in Vegan Supplements Market

- February 2025: ACG Capsules Introduces Full Vegan Printed Capsules. Every aspect of the capsules, from shell to print, meets stringent vegan standards and supports the growing demand for transparency, sustainability, and cruelty-free options in medications and dietary supplements.

- April 2024: Rasayanam, a trusted name in natural wellness products, has officially launched its 100% Plant-Based Omega-3 Supplement, offering a reliable and vegan-friendly way to get essential nutrients that are often missing from vegetarian diets.

- April 2024: OpenStore acquired Future Kind, which is a 100% vegan, sustainability-focused supplement company founded by brothers Shaun and Eliot, to its brand portfolio through an acquisition.

Global Vegan Supplements Market Report Scope

Vegan Supplements are plant-sourced supplements that are consumed to reach the required dietary allowance. The global vegan supplements market (henceforth referred to as the market studied) is segmented by product type, form, distribution channel, and geography. By product type, the market is segmented into Vitamins, Minerals, proteins, Omega Supplements, and Other Vegan Supplements. Based on form, the market is segmented into Powder, Capsules, and Others. Based on the distribution channel, the market studied is segmented into Supermarkets/Hypermarkets, Pharmacies & Drug Stores, Online Retail Stores, and Other Distribution channels. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD billion).

Segmentation Overview

By Product Type

| Vitamins |

| Minerals |

| Prebiotics |

| Omega Fatty Acids |

| Other Vegan Supplements |

By Form

| Capsules and Softgels |

| Tablets |

| Gummies |

| Other Forms |

By Function/Health Benefit

| General Wellness |

| Immune Support |

| Weight Management |

| Digestive and Gut Health |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty and Health Stores |

| Online Retailers |

| Other Distribution Channels |

By End User

| Adult |

| Children |

| Elderly Population |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Sweden | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Thailand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America |

| By Product Type | Vitamins | |

| Minerals | ||

| Prebiotics | ||

| Omega Fatty Acids | ||

| Other Vegan Supplements | ||

| By Form | Capsules and Softgels | |

| Tablets | ||

| Gummies | ||

| Other Forms | ||

| By Function/Health Benefit | General Wellness | |

| Immune Support | ||

| Weight Management | ||

| Digestive and Gut Health | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty and Health Stores | ||

| Online Retailers | ||

| Other Distribution Channels | ||

| By End User | Adult | |

| Children | ||

| Elderly Population | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Sweden | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the vegan supplements market?

The vegan supplements market stands at USD 11.17 billion in 2026 and is on track to reach USD 17.63 billion by 2031 at a 9.56% CAGR.

Which product segment leads the vegan supplements market?

Vitamins hold the largest share at 32.03% of 2025 revenue, followed by minerals and omega-3 oils.

Which region is expanding the fastest?

Asia-Pacific, driven by India and Southeast Asian e-commerce, is expected to grow at 9.75% CAGR from 2026 to 2031.

What portion of the vegan supplements market is generated by adult consumers?

Adults contribute 44.73% of total demand, making them the single largest end-user group.

Page last updated on: