Dental Suture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

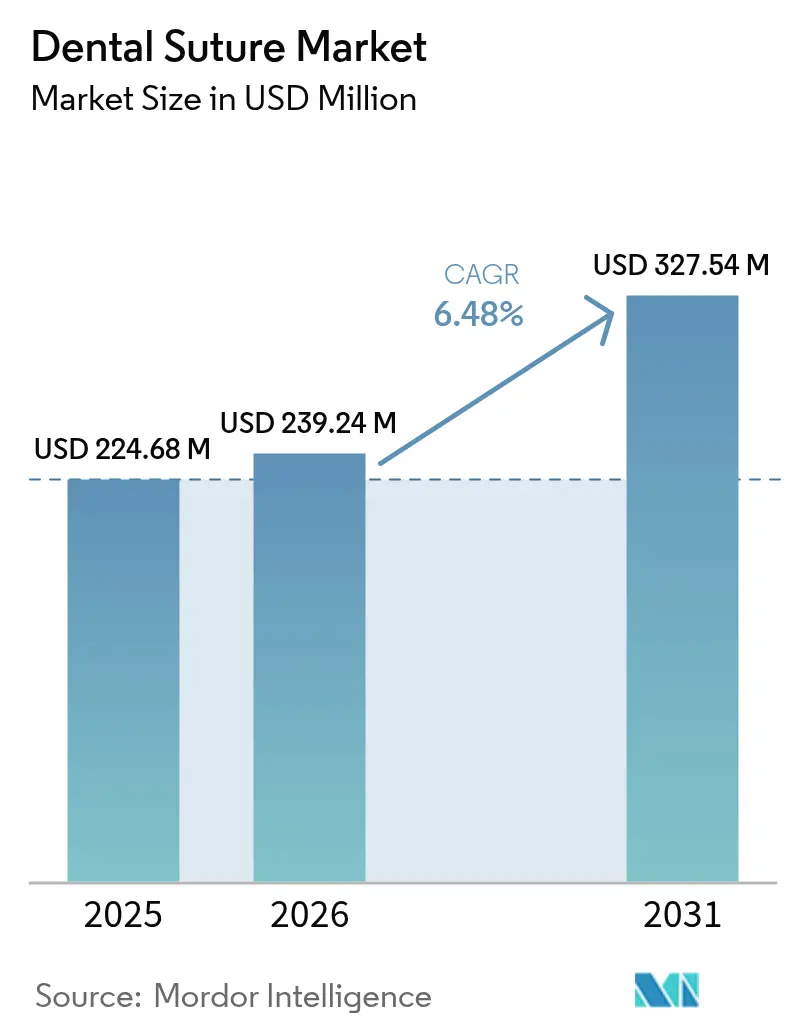

| Market Size (2026) | USD 239.24 Million |

| Market Size (2031) | USD 327.54 Million |

| Growth Rate (2026 - 2031) | 6.48% CAGR |

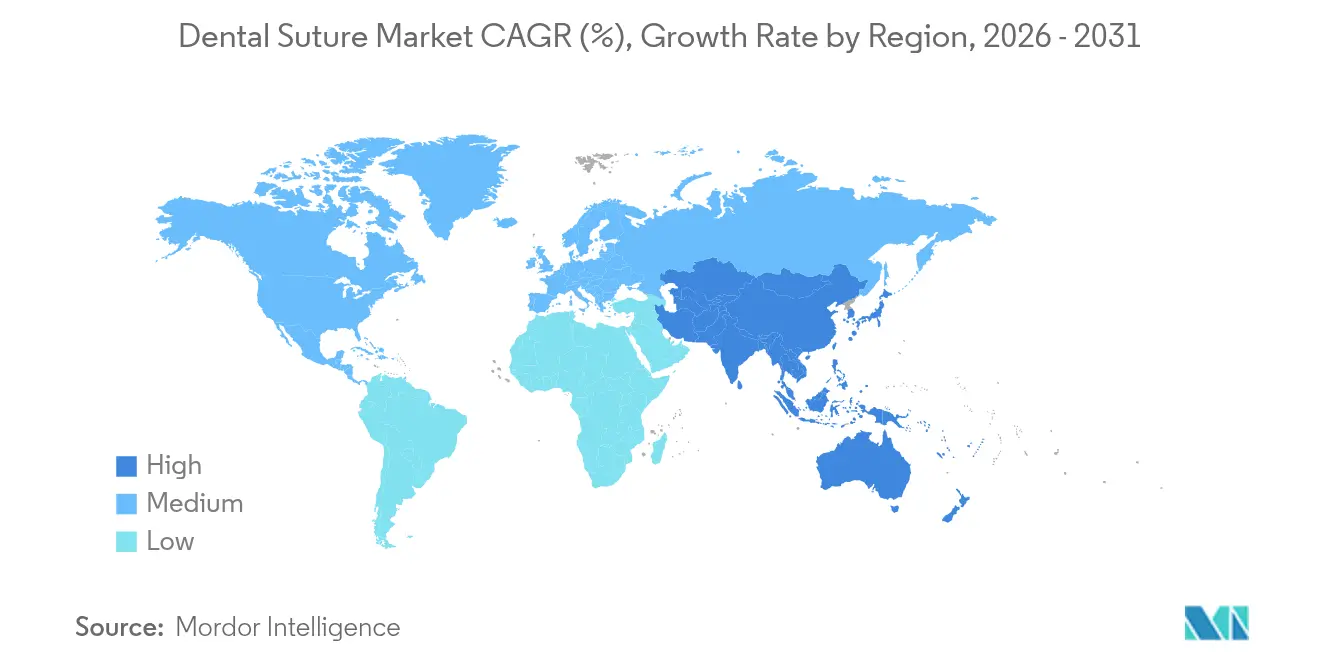

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Suture Market Analysis by Mordor Intelligence

The global dental suture market size in 2026 is estimated at USD 239.24 million, growing from 2025 value of USD 224.68 million with 2031 projections showing USD 327.54 million, growing at 6.48% CAGR over 2026-2031. Market expansion reflects three reinforcing dynamics: an aging population that requires a growing volume of periodontal and extraction procedures, sustained innovation in minimally invasive dentistry, and stricter regulatory momentum favoring biodegradable materials. In 2024, synthetic sutures captured a commanding 60.17% dental suture market share after demonstrating reliable tensile strength and predictable absorption properties. At the same time, the global burden of periodontal disease exceeded 1 billion cases in 2024 and remains on track to reach 1.56 billion by 2050, reinforcing consistent demand for wound-closure products. North America maintained leadership with 37.26% of the dental suture market in 2024, yet Asia-Pacific recorded the fastest growth trajectory at 7.52% CAGR, thanks to expanding middle-class access to dental care. Meanwhile, clinical adoption of resorbable sutures continues to accelerate as randomized trials show lower inflammatory response compared with traditional materials.

Key Report Takeaways

- By suture type, absorbable variants are forecast to post the fastest 6.78% CAGR to 2031, compared with non-absorbable offerings that held 54.10% of the dental suture market size in 2025.

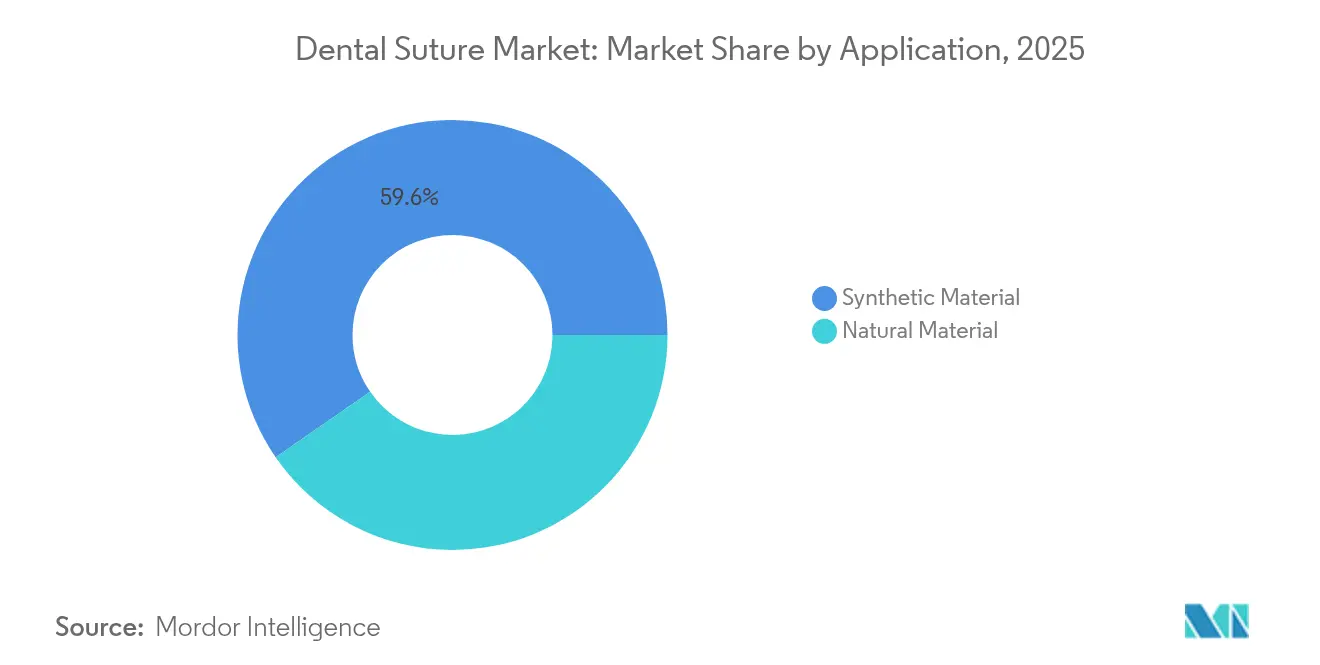

- By material, synthetic products led with 59.62% of the dental suture market share in 2025, while they are projected to expand at a 7.02% CAGR through 2031.

- By patient type, above 17 - Up to 65 segment held 54.00% of the dental suture market size in 2025, whereas up to 17 segment is set to advance at a 7.45% CAGR to 2031.

- By application, tooth-extraction procedures dominated 31.85% of the dental suture market share in 2025, while cosmetic dentistry is set to advance at a 7.40% CAGR to 2031.

- By end-use, dental clinics held a 63.40% share of the dental suture market in 2025 and are growing at a 6.90% CAGR on the back of outpatient care expansion.

- By geography, North America captured 36.90% of 2025 revenue; Asia-Pacific is projected to deliver a 7.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Suture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Periodontal Disease & Tooth-Loss Procedures | +1.8% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Growth in Dental Implant Surgeries Worldwide | +1.5% | North America & Asia-Pacific core, spill-over to Europe | Medium term (2-4 years) |

| Increasing Adoption of Resorbable Sutures in Dentistry | +1.2% | Global, with early gains in North America, Europe, Australia | Short term (≤ 2 years) |

| Growth of Outpatient Dental Microsurgery Enabled by Chairside Microscopes | +0.8% | North America & Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Regulatory Push for Biodegradable Dental Materials | +0.7% | Global, with strongest enforcement in North America & Europe | Medium term (2-4 years) |

| Adoption of 3-D Printed Patient-Specific Graft Membranes Needing Finer Closure | +0.5% | North America & Europe, with selective adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Periodontal Disease and Tooth-Loss Procedures

More than 1 billion people were affected by periodontal disease[1]Liang Xie, “The research progress on periodontitis by the National Natural Science Foundation of China,” International Journal of Oral Science, nature.com in 2024, and epidemiological modeling anticipates 1.56 billion cases by 2050. Disease incidence rises sharply with age and displays pronounced socioeconomic variation, which leads to a diverse set of clinical protocols that rely on precise tissue approximation to curb bacterial infiltration. Surgical guidelines emphasize premium suture selection as a non-negotiable tool for flap stability, especially in patients with comorbid diabetes or cardiovascular conditions that complicate healing.

Growth in Dental-Implant Surgeries Worldwide

U.S. implant prevalence was 5.7% in 2016 and is anticipated to reach as high as 23% by 2026 if accessibility trends continue. Implants usually mandate several suturing episodes—including initial fixture placement, membrane fixation, and soft-tissue reshaping—which multiply suture use per patient. Positioning errors persist in 56.6% of implant cases, leading to revision surgeries[2]Razan Alaqeely, “Cyanoacrylates versus sutures in periodontal surgery,” Journal of Periodontology, mdpi.com that further augment suture demand.

Increasing Adoption of Resorbable Sutures in Dentistry

Randomized comparisons of polyglactin versus polyglycolic-acid filaments report lower postoperative inflammation and reduced plaque adhesion, especially in highly vascular periodontal sites. ASTM F2579-18 gives manufacturers a definitive standard for poly(lactide) and poly(lactide-co-glycolide)[3]U.S. Food and Drug Administration, “ASTM F2579-18 Recognition,” accessdata.fda.gov implants, accelerating product registrations. Patient convenience is another catalyst because absorbable sutures eliminate follow-up removal visits, an attractive advantage for busy clinics operating on lean schedules.

Expansion of Outpatient Dental Microsurgery Enabled by Chairside Microscopes

Magnification devices have migrated from specialty centers to routine practice, enabling broader use of 6-0 to 10-0 sutures that would otherwise be impractical. Observational studies confirm that microscope-assisted flaps present reduced tissue trauma and improved esthetics, which elevates material requirements as clinicians seek ultra-fine filaments with enhanced color visibility under high magnification. Younger dentists and larger urban practices act as first adopters, signaling an impending shift in baseline surgical standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of tissue adhesives and sealants as substitutes | -1.1% | Global, greatest in North America and Europe | Short term (≤ 2 years) |

| Elevated cost of advanced synthetic absorbable sutures | -0.8% | Emerging Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Skill gaps in advanced suturing among general dentists | -0.6% | Global, pronounced in resource-limited regions | Medium term (2-4 years) |

| Stringent waste-disposal regulation for single-use devices | -0.4% | North America, Europe; gradually extending to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Tissue Adhesives and Sealants as Substitutes

Clinical trials show intraoral cyanoacrylate can secure 71.97% root coverage in periodontal surgery compared with 61.36% for sutures, while reducing closure time from 7.31 minutes to 2.16 minutes. Adhesives also eliminate removal appointments, a cost advantage in high-volume practices. Their growing acceptance threatens routine suture volumes, particularly for small incisions.

High Cost of Advanced Synthetic Absorbable Sutures

Price gaps between entry-level catgut and high-end braided polyglactin exceed 300%. In many emerging markets, private dental spending remains out-of-pocket, making high-performance sutures difficult to justify. Research into albumin-based composites demonstrates a credible, low-cost pathway that could narrow the gulf while meeting biocompatibility standards[4]Mohamed A. Naser, “Biodegradable suture development-based albumin composites for tissue engineering applications,” Scientific Reports, nature.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Suture Type: Absorbable Innovation Drives Future Growth

Non-absorbable filaments held 54.10% of the dental suture market in 2025, yet absorbable variants are forecast to deliver the leading 6.78% CAGR to 2031. The absorbable category benefits from synthetic polymers that offer controlled degradation and tensile retention matching tissue-healing kinetics. Dental suture market size for absorbable lines is projected to expand as regulatory frameworks validate their biodegradation profiles. Because removal appointments disappear, clinics gain scheduling flexibility and lower chair-time per patient, reinforcing uptake.

Polyglactin and polyglycolic-acid braids now achieve tensile strengths comparable to silk and nylon while provoking lower tissue reactivity, a critical feature in the oral cavity’s microbe-rich milieu. As product portfolios widen to include monofilament designs for esthetic zones, the adoption curve steepens. Over the forecast horizon, non-absorbable will continue to dominate specific indications that demand permanent tensile support, yet their share is expected to erode gradually in favor of absorbables.

By Material: Synthetic Dominance Reflects Performance Advantages

Synthetic fibers accounted for 59.62% of 2025 revenue and are projected to compound at 7.02% annually through 2031, maintaining clear leadership in the dental suture market. Their low bacterial retention and consistent absorption rates outperform natural alternatives, especially important in procedures where infection control is paramount. Conversely, natural offerings such as silk or cellulose retain niche relevance for patients sensitive to chemical additives.

The regulatory push for eco-friendly materials is catalyzing hybrid R&D that bonds synthetic strength with plant-derived substrates. Early prototypes of cellulose-reinforced polylactide braids suggest a credible bridge between performance and sustainability demands. While not yet commercialized, such products could shift buyer criteria toward environmental credentials.

By Patient Age Group: Pediatric Growth Outpaces Adult Segments

Adults aged 17-65 formed 54.00% of 2025 volume, reflecting peak intervention years. However, pediatric procedures are rising 7.45% yearly, driven by preventive dentistry campaigns and insurance coverage expansions. Child-specific sutures require delicate handling properties and smaller diameters, prompting suppliers to develop size-5-0 monofilaments with brightly colored coatings to aid visibility.

Elderly demand also climbs as life expectancy and edentulous rehabilitation increase. Older patients often present comorbidities that slow healing, so extended-support sutures with antimicrobial coatings gain traction. Tele-dentistry follow-up programs help monitor geriatric recovery, fostering confidence in remote management of postoperative care.

By Application: Cosmetic Procedures Drive Premium Growth

Tooth extraction retained 31.85% dental suture market share in 2025 and will stay volume-heavy. Periodontal therapy follows closely, underpinned by the pervasive incidence of gum disease. Meanwhile, cosmetic dentistry enjoys the fastest 7.40% CAGR to 2031 as social media visibility shapes patient expectations. Suture aesthetics—minimal scarring, color-matched filaments—command price premiums in esthetic zones.

Implant surgery remains a robust contributor because every fixture insertion requires flap management, guided bone regeneration, and often membrane fixation. Orthodontic soft-tissue procedures also increase in line with adult aligner demand, although their share stays modest relative to extractions.

By End-Use: Dental Clinics Maintain Market Leadership

Dental clinics controlled 63.40% of 2025 revenue and are forecast to grow at 6.90% CAGR. Consolidation under multisite Dental Service Organizations (DSOs) boosts volume purchasing power, enabling clinics to negotiate bundling deals on sutures and related consumables. Hospitals continue to manage trauma and medically complex cases, but experience a shrinking share as routine work migrates to the outpatient setting.

Ambulatory surgical centers (ASCs) occupy an intermediate niche. Prospective studies covering 11,680 dental-surgery patients confirm comparable safety to hospital care, encouraging wider insurer acceptance. With ASCs adopting hospital-grade protocols, their demand for specialized absorbable sutures should rise proportionately.

Geography Analysis

North America generated 36.90% of global revenue in 2025, anchored by high procedural volumes, robust insurance coverage, and practitioner familiarity with premium materials. United States-specific initiatives on opioid-sparing analgesia, such as the 2025 approval of suzetrigine, help safeguard patient comfort and promote elective procedures. Recent 10% tariffs on imported dental consumables may shift sourcing toward local suture manufacturers, but the market remains attractive given a 7.05% regional CAGR through 2031. Asia-Pacific represents the fastest 7.25% CAGR trajectory thanks to rising disposable income, urbanization, and large-scale public health investments. While per-capita procedure rates are lower than in North America, the vast population base translates to unparalleled volume potential. Domestic firms in India, China, and South Korea are scaling capacity to meet demand while offering cost-competitive alternatives. Europe recorded a steady 6.80% annual growth, buoyed by single-payer insurance schemes that cover a baseline of restorative care. Strict environmental policy accelerates the shift to biodegradable filaments. Local content regulations in France and Germany stimulate intra-regional production, offering European brands a competitive edge over imports. Latin America and the Middle East & Africa display 6.33% and 5.95% growth rates, respectively. Economic volatility is a recurring challenge, yet targeted government programs—such as Brazil’s Expanded National Oral Health Policy—create pockets of accelerated uptake. GCC countries leverage medical tourism to attract affluent patients seeking advanced aesthetic restoration, supporting premium suture consumption.

Competitive Landscape

Competitive intensity remains moderate, with no single vendor exceeding a one-fifth share across all product categories. Established multinationals leverage polymer science and regulatory experience to maintain quality leadership, whereas regional challengers press price advantages and local regulatory familiarity. Technology portfolios increasingly extend beyond sutures into tissue adhesives, membranes, and sutureless closure systems.

Intellectual-property filings emphasize biodegradable composites and antimicrobial coatings. A recent wave of patents covers polylactide braids embedded with silver nanoparticles that reduce microbial colonization by up to 99% in in-vitro models. Concurrently, several manufacturers have prototyped 3-D-printed suture needles matched to patient anatomy, indicating the convergence of additive manufacturing and dental wound closure.

Distribution strategies pivot on multisite DSOs and e-commerce portals, enabling direct-to-clinic shipment models that shorten replenishment cycles. Customer-experience programs now combine digital education modules, augmented-reality knot-tying tutorials, and remote troubleshooting to lock in brand loyalty among early-career clinicians.

Dental Suture Industry Leaders

Advanced Medical Solutions Group PLC

B. Braun Melsungen AG

DemeTECH Corporation

Johnson & Johnson Services, Inc.

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Henry Schein reported Q1 2025 GAAP diluted EPS growth of 22% on USD 3.168 billion net sales, launching its BOLD+1 plan to streamline dental-sector operations.

- April 2025: MAX has clinched a USD 77 million credit facility, aiming to bolster partnerships in oral and maxillofacial surgery. This move underscores the rising demand for dental surgery consumables, including sutures.

- January 2025: Benco Dental, a major player in distributing oral healthcare technology and supplies, forged a new distribution agreement with A-dec, a prominent provider of dental solutions. This collaboration draws upon the decades of innovation from both firms.

- July 2024: Henry Schein purchased abc dental AG, adding USD 27.5 million Swiss revenue and broadening Central-European reach.

Global Dental Suture Market Report Scope

As per the scope of the report, a suture is commonly used to close wounds following dental extractions, biopsies, or other oral surgical procedures. The rapidly absorbed suture is generally preferred to avoid the need for removal. The dental suture market is segmented by Type (Absorbable and Non-absorbable), Material (Synthetic Material and Natural Material), Technique (Mattress Suture, Crisscross Suture, Interrupted Simple Suture, and Continuous Simple Suture), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The report offers the value (in USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Absorbable |

| Non-Absorbable |

| Synthetic Material |

| Natural Material |

| Up to 17 |

| Above 17 - Up to 65 |

| Above 65 |

| Tooth Extraction |

| Periodontal Procedure |

| Orthodontic Procedure |

| Cosmetic Dentistry |

| Other Applications |

| Dental Clinics |

| Hospitals |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Suture Type | Absorbable | |

| Non-Absorbable | ||

| By Material | Synthetic Material | |

| Natural Material | ||

| By Patient Age Group | Up to 17 | |

| Above 17 - Up to 65 | ||

| Above 65 | ||

| By Application | Tooth Extraction | |

| Periodontal Procedure | ||

| Orthodontic Procedure | ||

| Cosmetic Dentistry | ||

| Other Applications | ||

| By End-Use | Dental Clinics | |

| Hospitals | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which suture material is currently preferred in dental surgeries and why?

Synthetic sutures dominate clinical choice because their engineered polymers deliver consistent tensile strength, low bacterial adherence, and controlled absorption that align well with oral-cavity healing dynamics.

What regulatory trend is shaping future innovation in dental suture products?

Health agencies in North America and Europe are tightening biocompatibility and sustainability standards, prompting manufacturers to prioritize fully biodegradable polymers and recyclable packaging across new product lines.

How does the rise of outpatient microsurgery influence suture design requirements?

Widespread adoption of chairside microscopes encourages use of ultra-fine, high-contrast filaments that enable precise knot placement while minimizing tissue trauma during minimally invasive procedures.

What competitive strategies are suppliers using to stand out in the dental suture landscape?

Leading companies are integrating antimicrobial coatings, developing bioactive resorbable filaments, and bundling sutures with complementary closure solutions such as membranes and tissue adhesives to create full-service portfolios.

Why is Asia-Pacific considered the most dynamic regional market for dental sutures?

Expanding middle-class spending, government-backed healthcare infrastructure projects, and local manufacturing scale-ups are collectively accelerating adoption of advanced wound-closure products throughout the region.

What substitute technologies pose the greatest threat to traditional dental sutures, and how are vendors responding?

Tissue adhesives and sealants offer faster application and eliminate removal visits; in response, suture manufacturers are launching hybrid kits that combine resorbable threads with bio-compatible adhesive patches to preserve procedural versatility.

Page last updated on: