Teeth Whitening Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

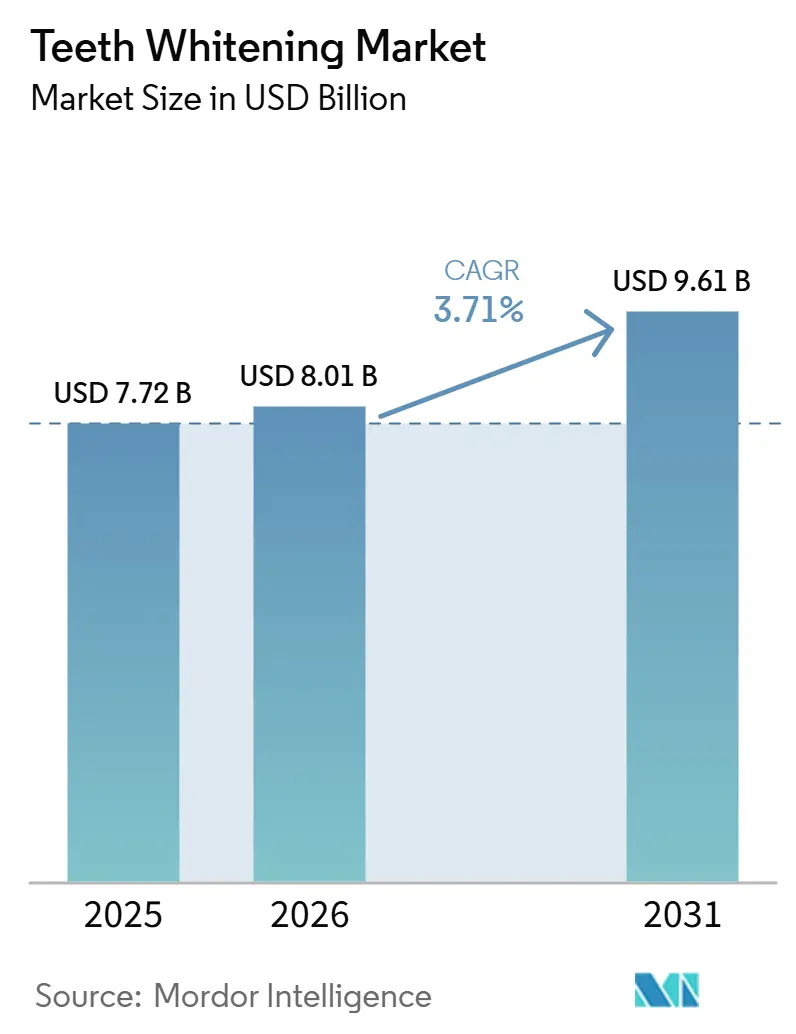

| Market Size (2026) | USD 8.01 Billion |

| Market Size (2031) | USD 9.61 Billion |

| Growth Rate (2026 - 2031) | 3.71% CAGR |

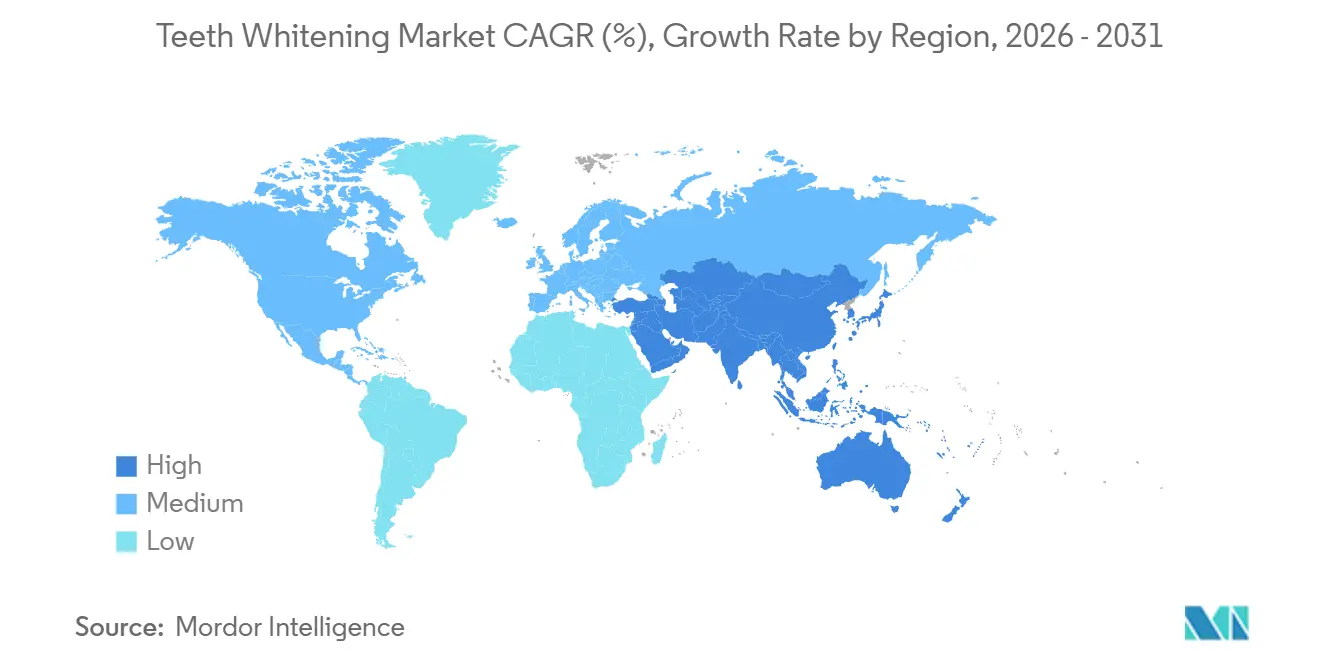

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Teeth Whitening Market Analysis by Mordor Intelligence

The Teeth Whitening Market size is projected to expand from USD 7.72 billion in 2025 and USD 8.01 billion in 2026 to USD 9.61 billion by 2031, registering a CAGR of 3.71% between 2026 to 2031.

Consumer behavior is shifting as at-home kits drive volume sales, while professional in-office procedures sustain higher revenue levels through faster LED-accelerated protocols. Social media has elevated cosmetic standards, attracting new users to entry-level products such as toothpastes, pens, and strips that deliver visible results with minimal effort and cost. In the United States and Europe, regulatory restrictions on peroxide concentrations in over-the-counter formulations have redirected innovation toward enzyme-based systems, nano-hydroxyapatite, PAP chemistry, and light activation methods, focusing on achieving efficacy without causing sensitivity. Leading consumer brands are leveraging retail channels to protect their market share in toothpastes and strips, while direct-to-consumer specialists are expanding through subscriptions, digital marketing, and influencer partnerships to enhance customer acquisition.

Key Report Takeaways

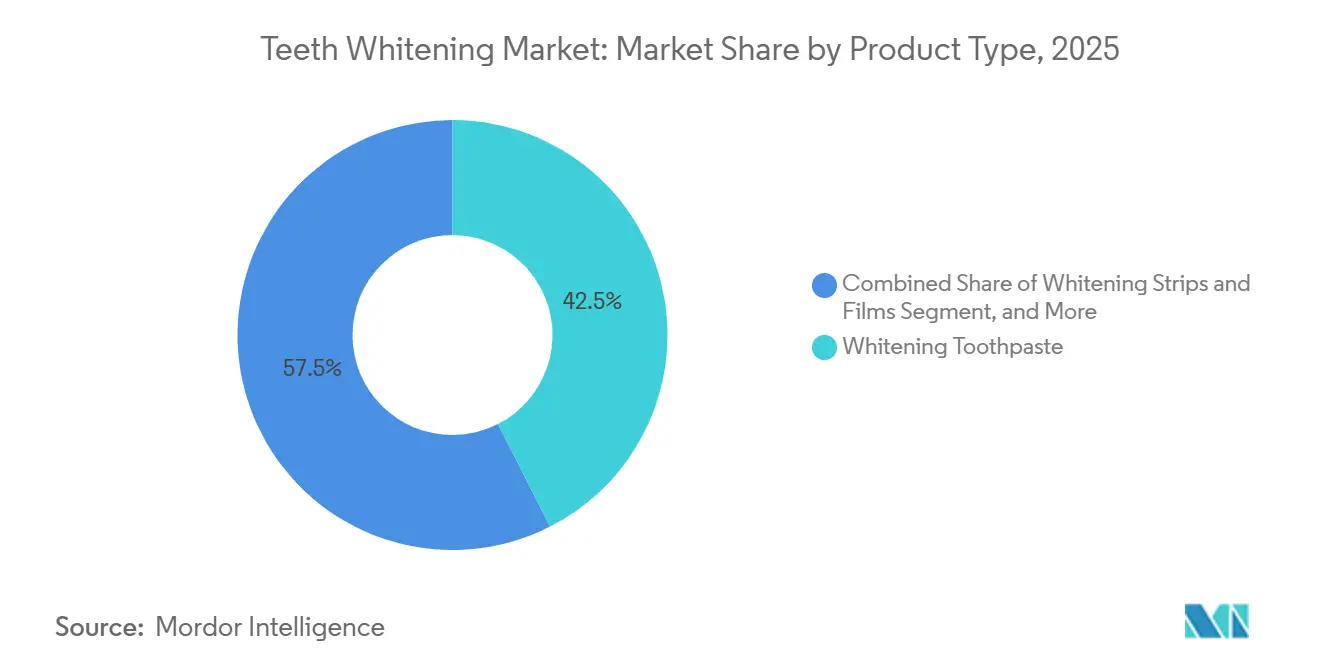

- By product type, whitening toothpaste led with 42.5% of the teeth whitening market share in 2024; whitening strips and films are projected to expand at a 4.12% CAGR through 2030.

- By end user, the individual/at-home segment accounted for 68.67% of the teeth whitening market in 2024, while dental clinics are expected to grow at a 3.94% CAGR through 2030.

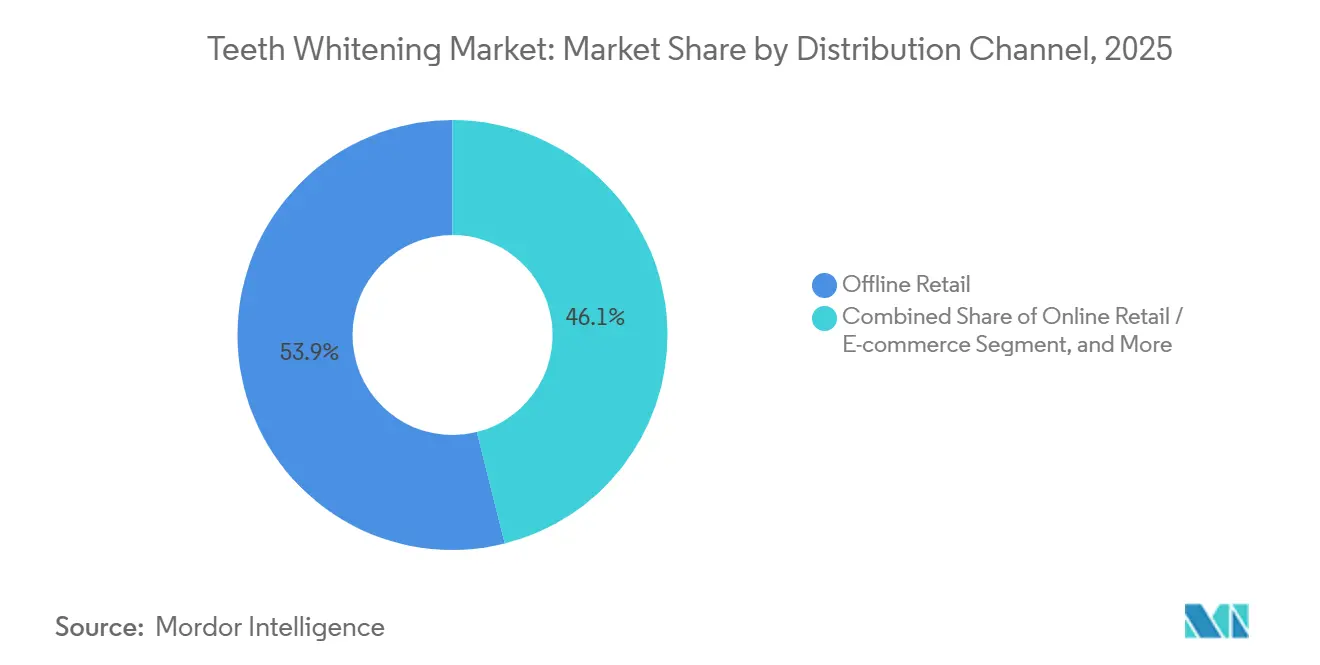

- By distribution channel, offline retail accounted for 53.91% of revenue in 2024; online retail is forecast to post the fastest CAGR of 4.38% through 2030.

- By geography, North America accounted for 32.23% of 2024 revenue, whereas Asia-Pacific is poised to register a 4.63% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Teeth Whitening Market Trends and Insights

Driver Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for cosmetic dental aesthetics | +1.2% | Global, with concentration in North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Growing availability of otc whitening products | +0.80% | Global; strongest in Asia-Pacific | Short term (≤ 2 years) |

| Social-media-driven "smile perfection" culture | +0.9% | Global, led by North America and Europe, with rapid uptake in APAC youth demographics | Short term (≤ 2 years) |

| Technological advances in led & peroxide-free kits | +0.8% | North America and Europe, with APAC adoption following | Medium term (2-4 years) |

| Surge in dental tourism for low-cost whitening | +0.40% | Turkey, Thailand, Mexico | Medium term (2-4 years) |

| AI-enabled shade-matching & personalisation | +0.5% | North America and Europe premium segments with early pilots in China and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Cosmetic Dental Aesthetics

White teeth signal wellness, discipline, and social success, so consumers now view whitening as routine self-care rather than vanity spending. Delta Dental’s 2024 survey confirms that 52% of adults rate tooth brightness as a top oral priority, and 91% equate dental check-ups with annual physicals, embedding whitening into preventive budgets.[1]Source: Delta Dental Plans Association, “2024 State of America’s Oral Health and Wellness Report,” deltadental.com Millennials and Gen Z circulate before-and-after photos that normalise frequent bleaching and create peer pressure to maintain a bright smile. Employers in beauty, hospitality, and customer-facing roles subtly reward candidates with confident smiles, reinforcing commercial value. This combination of personal vanity, social proof, and professional incentives underpins steady market expansion even when discretionary income tightens. A 2025 survey by the American Academy of Cosmetic Dentistry revealed that smile appearance is the leading aesthetic concern among adults aged 25-45, surpassing skin and hair. This trend is driving discretionary spending away from adjacent categories and toward oral aesthetics.

Growing Availability of OTC Whitening Products

Mass retailers have widened shelf space for strips, pens, and blue-filter pastes, moving whitening from pharmacy exclusivity into grocery and convenience channels. Private-label launches lower entry prices, letting first-time users trial simple formats without dentist visits. Harmonised safety standards, such as China’s 2023 toothpaste rules, simplify cross-border roll-outs but require formal efficacy dossiers to weed out weak formulations. UK Trading.[2]Source: UK Office for Product Safety and Standards, “Product Safety Alert: Home Teeth Whitening,” gov.uk Standards, however, still intercept high-peroxide kits online, showing the market’s policing gap. Overall, wider physical and digital reach sparks trial, but enforcement pressure gradually boosts quality and brand trust.

Social-Media-Driven "Smile Perfection" Culture

Social platforms are accelerating the adoption of whitening products by leveraging rapid cycles of before-and-after content that convert visual proof into purchase intent. This approach creates a viral loop for trending formats. This growth highlights the strong influence of social proof in driving first-time trials. Hashtags such as #TeethWhitening and #SmileMakeover generate significant impressions, subtly encouraging viewers to align with the brighter smile standard showcased in curated feeds. Brands are increasingly partnering with micro-influencers who share at-home routines and provide concise demonstrations, reducing dependence on traditional advertising. In March 2025, Colgate’s Optic White Pen campaign, executed through TikTok partnerships, achieved 12 million views in its first week and drove a 34% increase in e-commerce orders, demonstrating the effectiveness of social-first launches in converting awareness into sales.[3]Colgate-Palmolive Company, “Investor Relations: Product Launch Updates,” Colgate-Palmolive, colgatepalmolive.com

Technological Advances in LED & Peroxide-Free Kits

Clinical trials show violet-LED mouthpieces paired with lower peroxide deliver shade gains comparable to high-peroxide gels while cutting sensitivity incidents in half. PAP oxidisers and titanium-dioxide nanogels now mimic hydrogen-peroxide results without enamel dehydration, expanding eligibility to users previously deterred by pain risk. Smartphone-linked mouthpieces manage light cycles and pause when sensors detect gum contact, adding safety assurance. Refillable gel cartridges reduce plastic waste and lock customers into proprietary ecosystems, lifting lifetime value. Collectively, these advances widen the addressable market while boosting perceived product quality.

Restraint Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Tooth-sensitivity concerns & safety warnings | -0.7% | Global, with heightened scrutiny in North America and Europe | Short term (≤ 2 years) |

| Regulatory clamp-down on high-peroxide DIY kits | -0.5% | Europe and North America with selective enforcement in APAC | Medium term (2-4 years) |

| Environmental scrutiny of single-use applicators | -0.3% | EU first, global spread | Long term (≥ 4 years) |

| Rise of natural “whitening” fads diluting clinical demand | -0.4% | Health-conscious markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tooth-Sensitivity Concerns & Safety Warnings

Scientific American warns that frequent high-peroxide bleaching can thin enamel and ignite chronic sensitivity, prompting cautious buyers to delay repeat cycles. Dental associations amplify this message by spotlighting unlicensed kiosks that skip gum protection. Charcoal abrasives, although marketed as natural, have been shown to roughen enamel, adding another cautionary note. Brands respond with PAP creams and potassium-nitrate additives that promise “zero sensitivity” on pack. Even so, lingering fear tempers short-term uptake of aggressive DIY kits.

Regulatory Clamp-Down on High-Peroxide DIY Kits

EU law limits consumer peroxide to 0.1%, forcing brands to reformulate or channel higher strengths through dentists only. UK inspectors recently seized online products exceeding the cap by thirtyfold, signalling vigilant enforcement. The US FDA, while lighter, still mandates device registration, leaving newcomers to navigate ambiguous claim rules. China’s 2023 toothpaste code requires full toxicology dossiers, raising entry costs for foreign labels. Tighter oversight protects consumers but lengthens time-to-market and curbs impulse launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Toothpaste Dominates, Strips Accelerate

Whitening toothpaste accounted for 42.10% of the teeth-whitening market in 2025, representing USD 3.25 billion of the market size. Strips and films, though smaller, post the fastest 3.96% CAGR and are popular among event-driven users needing swift shade lift. Purple-hued micropolishing formulations defend toothpaste shelf share against rapid-action rivals. Sustainability trends catalyse aluminium tubes and biodegradable strip substrates, aligning oral-care routines with broader eco-ethics.

Premium gels and LED kits blur lines between OTC and professional care, allowing consumers to purchase dentist-strength systems for home use. Teeth whitening market growth benefits as refillable gel syringes reduce packaging waste while reinforcing brand loyalty through proprietary cartridge locks. Safety assurances via smart mouthpieces that auto-pause on gum contact strengthen perceived value.

By End User: At-Home Convenience Versus Clinical Precision

In 2025, individual or at-home users accounted for 68.67% of the revenue, as consumers prioritized privacy and flexible treatment schedules over appointment scheduling and higher costs. In-office procedures typically range from USD 500 to 800 per session, while at-home kits are priced between USD 20 and 150. This significant price difference has expanded access to a broader income demographic. The pandemic accelerated the adoption of direct-to-consumer models and digital discovery, and subscription services continue to sustain this trend even as clinics operate at full capacity. Orthodontic e-commerce platforms have introduced bundled whitening kits with aligners, creating cross-selling opportunities that reduce acquisition costs for whitening add-ons. At-home teeth whitening sees repeat purchases as users refresh their results for events or photos, supporting quarterly or semiannual replenishment cycles. Brands offering app-based guidance and shade tracking enhance user adherence, encouraging them to complete full treatment cycles, thereby improving satisfaction and reducing churn.

Dental clinics and hospitals are projected to grow at a compound annual growth rate of 3.94% through 2031, driven by the adoption of LED acceleration technology that reduces treatment sessions to under an hour. Premium chair-side protocols, such as Philips Zoom WhiteSpeed and Ultradent Opalescence Boost, claim to deliver 8 to 10 shades of improvement in a single visit. These advancements support higher price points and strengthen practice economics.

By Distribution Channel: E-Commerce Disrupts Retail Dominance

In 2025, offline retail accounted for 53.91% of sales. This performance was driven by the extensive reach of pharmacies and mass retailers, in-aisle product comparisons, and frequent promotions that encouraged both trials and upgrades. Major chains like CVS, Walgreens, and Walmart offered a wide range of products, catering to both budget-conscious and premium customers with their strips, pens, and LED kits. Shoppers valued the opportunity to read labels, inspect formats, and consult pharmacists, particularly when choosing between peroxide and peroxide-free options. However, foot traffic declined in 2025 as an increasing number of digital-savvy consumers turned to online searches and social media to discover cosmetic products. This shift reduced impulse-driven sales for certain stores.

Forecasts indicate that online retail and direct-to-consumer models will grow at a 4.38% compound annual rate through 2031. Algorithm-driven recommendations, subscription-based auto-ship discounts, and the rapid adoption of product bundles and limited-time drops support this growth. Digital-first brands allocate the majority of their marketing budgets to social media advertising, influencer partnerships, and video reviews, which help reduce customer acquisition costs when content resonates with target audiences.

Geography Analysis

North America contributed 31.95% of 2025 sales, retaining leadership through advanced cosmetic dentistry, insurance coverage, and cultural emphasis on aesthetic norms. The United States pilots most AI-driven whitening technologies, whereas Canada skews toward natural ingredient rosters and fluoride-free claims.

Europe’s growth remains steady yet regulation-driven. Hydrogen-peroxide caps accelerate the adoption of PAP and blue-filter technologies that promise sensitivity-free whitening, protecting enamel, and complying with CE labeling norms. Germany invests in recyclable packaging, while Scandinavia mandates life-cycle disclosures on oral-care plastics.

Asia-Pacific posts the fastest CAGR of 4.52%, propelled by urbanisation and beauty-conscious middle classes embedding whitening into grooming rituals. China’s e-commerce festivals move high-volume LED kits; India’s dental chains bundle whitening with orthodontic aligners; Japan merges vitamin C and collagen into pastes to satisfy synergy-seeking shoppers.

Competitive Landscape

In the teeth whitening market, major consumer goods companies dominate toothpaste and strip portfolios, while numerous challengers emerge with specialized formats and digital-first strategies. Procter & Gamble, Colgate-Palmolive, Unilever, and Church & Dwight leverage decades of brand equity and extensive distribution networks to secure prime shelf space and maintain visibility. Their significant R&D investments validate clinical claims and strengthen patents related to sensitivity reduction, shade enhancement, and enamel care. New product launches are often paired with social campaigns and clinic endorsements, enhancing both credibility and reach. The market favors established players who combine trusted claims with seamless purchasing options across online and offline channels.

Direct-to-consumer brands are expanding by targeting audiences on Instagram and TikTok. They utilize influencer endorsements and offer subscription models that encourage quarterly purchases at discounted rates. Brands like Snow Labs and HiSmile effectively use creator-driven content to promote trials of their pens, strips, and PAP-based kits, reducing reliance on traditional retail launches. This approach has, in some cases, shortened the time-to-market to just a few months, enabling quicker adjustments in flavors, applicators, and packaging. In March 2025, Colgate-Palmolive introduced the Optic White Pen to meet the demand for quick, targeted applications. The product's initial success in the digital space highlights that established brands can effectively adopt a social-first approach when the messaging and use case are clear. As the market evolves, both established and emerging brands are focusing on stronger claims for sensitivity and enamel protection, seeking differentiation that goes beyond peroxide strength.

Teeth Whitening Industry Leaders

Colgate-Palmolive Company

GSK plc

Johnson & Johnson Services, Inc.

Procter & Gamble Co.

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Colgate-Palmolive India launched a new campaign for Colgate Visible White Purple featuring Kriti Sanon and Abhishek Sharma to position teeth whitening as a beauty essential, highlighting a purple toothpaste that uses color theory to offset yellow tones across television, digital, and social channels.

- February 2026: Opalescence whitening expanded its portfolio with an alcohol-free whitening mouthwash formulated with hydrogen peroxide and a cool mint profile, designed to deliver a dentist-fresh sensation after every rinse.

- January 2025: DOWZE introduced a sleek teeth-whitening product designed for busy users aged 18 to 45 that emphasizes simplicity, convenience, and visible results within fast-paced routines.

- March 2025: Colgate-Palmolive launched the Optic White Pen with a 9% hydrogen peroxide gel for targeted application without trays or strips, achieving 12 million TikTok views in the first week and a 34% spike in e-commerce orders.

Global Teeth Whitening Market Report Scope

As per the scope of the report, teeth whitening is the procedure of bleaching teeth to make them whiter and more presentable. Teeth whitening products are simple, non-invasive treatments that effectively change the color of the tooth enamel.

The teeth whitening market is segmented by product, end user, distribution channel, and geography. By product, the market is segmented into whitening toothpaste, whitening gels and strips, white light teeth whitening devices, and other products. By end user, the market is segmented into individual/at-home and dental clinics & hospitals. By distribution channel, the market is segmented into offline sales and online sales. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Whitening Toothpaste |

| Whitening Strips & Films |

| Whitening Gels & Kits |

| Whitening Mouthwash |

| Individual / At-Home |

| Dental Clinics & Hospitals |

| Offline Retail |

| Online Retail / E-commerce |

| Dental Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Whitening Toothpaste | |

| Whitening Strips & Films | ||

| Whitening Gels & Kits | ||

| Whitening Mouthwash | ||

| By End User | Individual / At-Home | |

| Dental Clinics & Hospitals | ||

| By Distribution Channel | Offline Retail | |

| Online Retail / E-commerce | ||

| Dental Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the teeth whitening market in 2026?

It stands at USD 8.01 billion and is forecast to reach USD 9.61 billion by 2031.

Which product segment is currently dominant?

Whitening toothpaste leads with 42.10% of 2025 revenue.

Which region is expanding the fastest?

Asia-Pacific is growing at a 4.52% CAGR through 2031.

Are at-home kits replacing professional treatments?

Home solutions hold 68.10% share, yet clinic whitening still posts 3.88% CAGR as consumers seek guaranteed results.

What regulations affect DIY whitening kits?

The EU caps consumer peroxide at 0.1%, and UK authorities actively seize non-compliant imports while the US FDA mandates device registration.

Which technology is reshaping new launches?

AI-guided shade matching integrated with LED mouthpieces personalises treatment and improves predictability.

Page last updated on: