Endodontics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

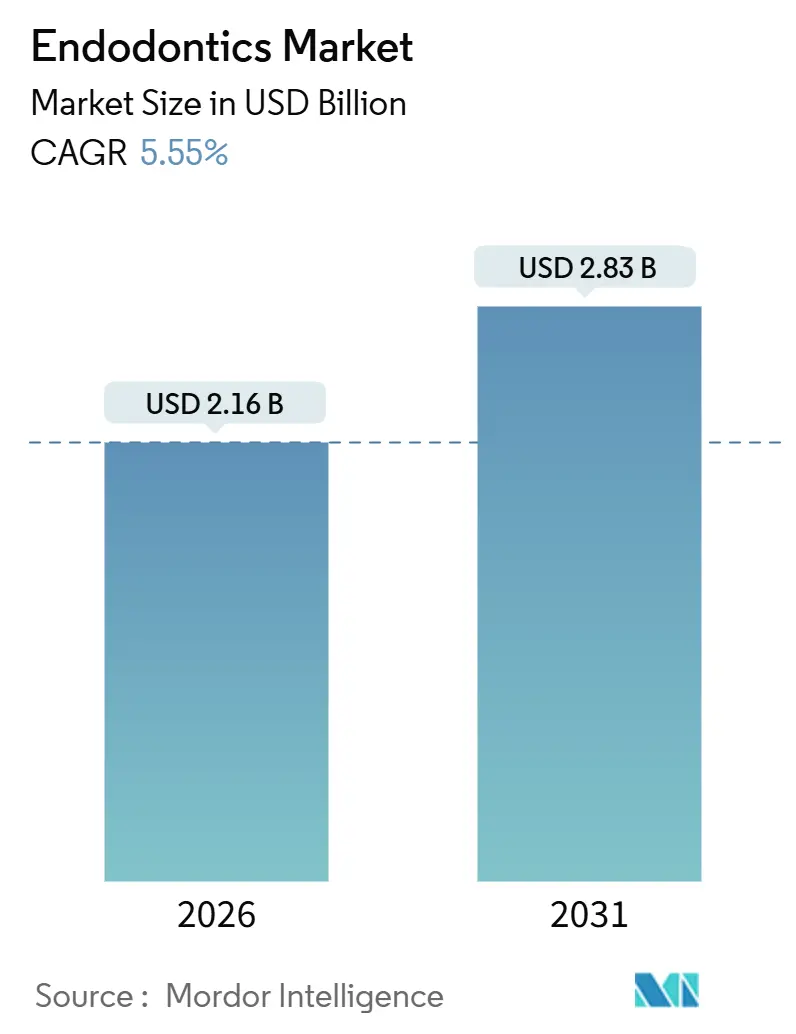

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 2.83 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

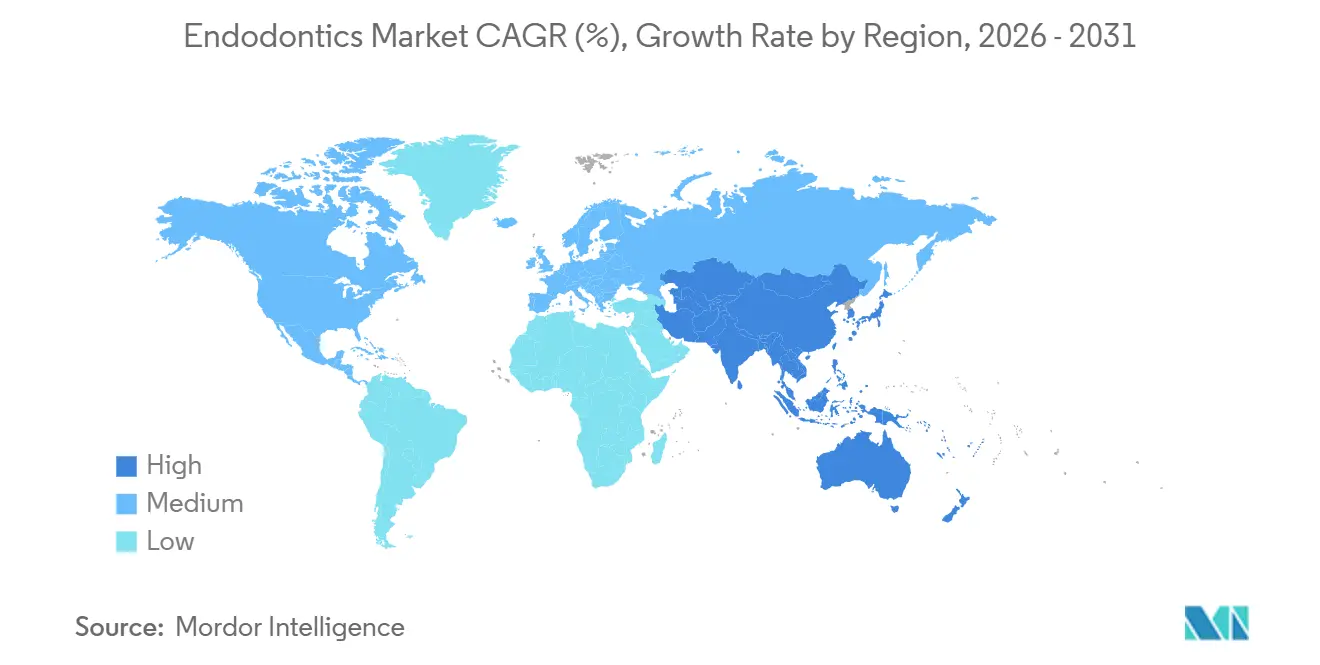

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endodontics Market Analysis by Mordor Intelligence

The Endodontics Market size is estimated at USD 2.16 billion in 2026, and is expected to reach USD 2.83 billion by 2031, at a CAGR of 5.55% during the forecast period (2026-2031).

Steady growth is being fueled by an aging population that retains more natural teeth, procedural upgrades from manual to rotary and AI-guided systems, and greater willingness in emerging economies to pay for tooth-preservation procedures over extraction. Technology spending is shifting toward capital-intensive treatment platforms, such as apex locators with integrated motors, laser units, and AI navigation, that raise first-time success rates and reduce retreatment needs. Recurring consumable sales remain the main revenue pillar, but equipment upgrades generate the fastest incremental gains. Heightened infection-control regulations in Europe, Japan, and Australia are accelerating the move to single-use instrumentation, while subsidies, especially in Germany and France, are blunting price resistance. In parallel, Asia-Pacific is scaling dental-tourism corridors that offer Western-standard technology at attractive prices, pulling demand from North America and Europe. The World Health Organization reported 2.5 billion adults living with untreated caries in 2025, underscoring the persistent clinical need that underpins long-range procedure volumes.

Key Report Takeaways

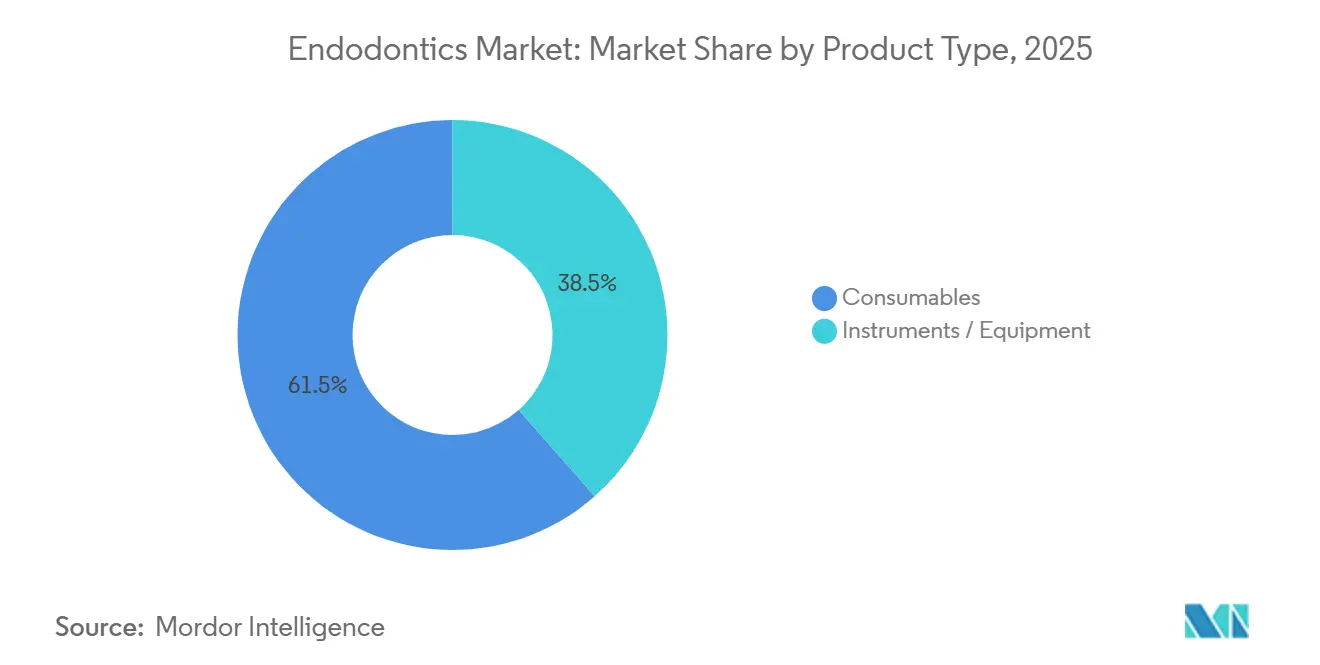

- By product type, consumables led with 61.55% of Endodontics market share in 2025; instruments and equipment are forecast to rise at a 7.25% CAGR through 2031.

- By end user, dental clinics accounted for 58.53% of the Endodontics market size in 2025, while academic and research institutes will expand at an 8.85% CAGR to 2031.

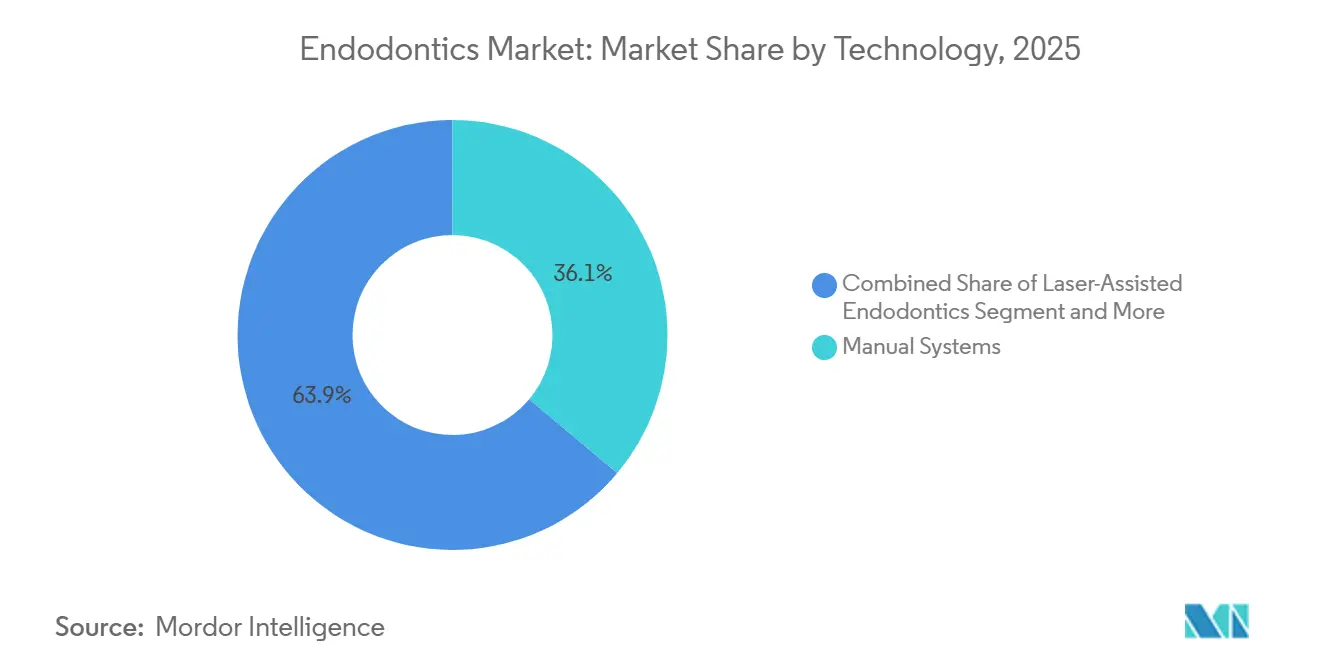

- By technology, manual systems retained 36.13% of Endodontics market share in 2025; AI-guided navigation is poised to climb at a 9.7% CAGR through 2031.

- By geography, North America dominated revenue with a 37.23% share of the Endodontics market size in 2025, whereas Asia-Pacific is projected to advance at an 8.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Endodontics Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of periodontal and dental-caries cases among the aging population | +1.2% | Global, with concentration in North America, Europe, Japan | Long term (≥ 4 years) |

| Rapid advances in NiTi rotary files and adaptive-motion systems | +1.5% | Global, early adoption in North America and Western Europe | Medium term (2-4 years) |

| Expansion of dental-clinic networks and dental-tourism hubs in emerging markets | +1.3% | Asia-Pacific core, spillover to Middle East and South America | Medium term (2-4 years) |

| AI-driven 3D periapical imaging boosting treatment precision | +0.9% | North America and EU, pilot deployments in urban Asia-Pacific | Short term (≤ 2 years) |

| EU subsidies for single-use instrumentation to curb cross-infection | +0.6% | European Union, potential replication in Australia and Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Periodontal and Dental-Caries Cases Among the Aging Population

Adults aged 65 and older will constitute 16% of the global population by 2030, a cohort with 2.8-times higher prevalence of apical periodontitis than younger age groups. Tooth-retention campaigns have lowered edentulism but simultaneously increased the number of teeth susceptible to pulpal necrosis. Japan, the world’s most aged society, recorded an 11% jump in root-canal procedures per 1,000 inhabitants between 2020 and 2024, a surge fully covered by national insurance. Chronic systemic diseases such as diabetes compromise healing and raise retreatment volumes, favoring advanced obturation sealers that release calcium and hydroxyl ions. These demographic tailwinds are weaker in Sub-Saharan Africa and South Asia, where younger populations and lower dental-care utilization delay immediate impact, yet the long-term vector remains upward.

Rapid Advances in NiTi Rotary Files and Adaptive-Motion Systems

Heat-treated nickel–titanium alloys—marketed as Gold Wire, Blue Wire, or CM Wire—deliver 40%–60% higher cyclic-fatigue resistance than conventional superelastic NiTi, enabling confident shaping of complex canal curvatures[1]Dentsply Sirona, “Annual Report 2025,” Dentsply Sirona, dentsplysirona.com. Dentsply Sirona shipped more than 8 million WaveOne Gold files globally by the end of 2025, while FKG Dentaire’s XP-endo Shaper uses shape-memory expansion to minimize pre-flaring. Adaptive-motion algorithms embedded in cordless motors adjust torque and rotation in real time, reducing ledge formation and cutting chair time by 18% according to a 2025 meta-analysis. These advances are particularly impactful in multi-rooted molars where traditional files risk separation, thereby lifting clinical success and patient throughput.

Expansion of Dental-Clinic Networks and Dental-Tourism Hubs in Emerging Markets

Private-equity funded dental chains across India, Thailand, and Brazil are standardizing endodontic workflows, leveraging bulk purchasing to lower per-procedure costs, and marketing ISO 13485–certified care to international patients. Thailand grants tax incentives to clinics achieving Joint Commission International accreditation and serving at least 30% overseas patients, fueling expansion in Bangkok and Phuket. India’s inbound dental-tourism segment grew 22% year-on-year in 2025, with endodontic procedures representing close to one-fifth of cases, as clinics bundle root-canal therapy with CBCT imaging at 40%–50% of U.S. prices. Uniform protocols lift device turnover, accelerate technology diffusion, and compress the payback period on AI-guided systems.

AI-Driven 3D Periapical Imaging Boosting Treatment Precision

Cone-beam computed tomography married to machine-learning algorithms detects accessory canals and periapical lesions with 92% sensitivity compared to 68% for two-dimensional radiography. The FDA cleared Pearl Inc.’s Second Opinion software in 2025, allowing clinicians to overlay color-coded anatomy maps onto live CBCT feeds. Envista’s Apex ID added AI navigation the same year, cutting redundant radiographs and shaving nine minutes off average case time. Uptake is strongest in North America and Western Europe, where reimbursement is favorable, while Southeast Asia and Latin America are running pilot programs in university hospitals to validate cost-to-benefit return.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced endodontic devices and consumables | -0.7% | Global, most acute in low- and middle-income countries across Asia-Pacific, Sub-Saharan Africa, and South America | Long term (≥ 4 years) |

| Stringent global approval pathways for new obturation and laser systems | -0.4% | Global, with longest timelines in North America, EU, and Japan | Medium term (2-4 years) |

| Limited reimbursement for retreatment and CBCT imaging | -0.6% | North America, Europe, Australia; minimal impact in cash-pay markets across Asia and Latin America | Medium term (2-4 years) |

| Eco-regulations on single-use plastics inflating consumable costs | -0.3% | European Union, with spillover to UK and Canada; pilot enforcement in California and Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Endodontic Devices and Consumables

Equipping a treatment room with a cordless motor, apex locator, CBCT scanner, and laser platform can exceed USD 80,000. Rotary NiTi systems cost USD 8–15 per canal under single-use or limited-reuse protocols versus USD 2–3 for stainless-steel hand files, a differential hard to recover where average root-canal fees are USD 50–150. Import tariffs of 10% on dental devices in India and fragmented after-sales support in Indonesia or Nigeria further dampen adoption. Leasing and refurbished pathways help, yet warranty gaps and inconsistent service make many clinicians wary. Out-of-pocket dominant markets shift expenses straight to patients, limiting penetration to large urban clinics.

Stringent Global Approval Pathways for New Obturation and Laser Systems

Novel bioactive sealers without clear predicates often face the FDA’s premarket-approval route, stretching commercialization by up to two years and costing USD 2–4 million in testing. Europe’s MDR demands fuller clinical evaluation and post-market monitoring, adding 12–18 months to launch times[2]European Commission, “Medical Device Regulation Guidance,” European Commission, europa.eu. Japan’s regulator reclassified adaptive-motion motors into a higher risk class in 2025, triggering new biocompatibility tests. These hurdles favor incumbents that can amortize compliance overhead across broader portfolios, sidelining smaller innovators and slowing technology refresh.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Anchor Revenue, Equipment Accelerates

Consumables commanded 61.55% of Endodontics market share in 2025, driven by constant turnover of files, obturation materials, and irrigation solutions. Heat-treated NiTi files, offering 40%–60% greater fatigue resistance, are displacing conventional alloys and are pivotal to repeat purchases. Bioactive sealers that release calcium ions shorten periapical healing by up to 20% versus epoxy-resin alternatives. Instruments and equipment, although smaller, will grow at a 7.25% CAGR, underpinned by cordless motors with Bluetooth connectivity, laser units for minimally invasive pulpotomy, and AI-integrated apex locators. Machine-assisted obturation guns speed three-dimensional fills, appealing to high-volume practices. As the European Union pushes toward disposable files, unit volumes rise even as per-unit margins compress, benefiting firms with vertically integrated packaging lines.

By End User: Clinics Dominate, Academic Institutes Surge

Dental clinics generated 58.53% of Endodontics market size in 2025 and remain the chief revenue channel. Corporate chains in India, Brazil, and the United States negotiate steep volume discounts, driving equipment standardization and widening the technology gap with solo practices. Academic and research institutes, expanding at an 8.85% CAGR, underpin early adoption of CBCT, lasers, and AI systems, aided by government grants in China and India that have grown postgraduate seats by more than one-third since 2024. Dental hospitals, while slower growing, manage complex retreatments and surgical cases that require premium imaging and microscopy, keeping per-case spending elevated. This bifurcation positions clinics as volume engines and universities as technology incubators.

By Technology: Manual Persists, AI Navigation Disrupts

Manual instrumentation still held 36.13% of Endodontics market share in 2025, sustained by low cost and clinician familiarity, especially for simple single-canal teeth. Rotary platforms dominate multi-canal molars, helped by cordless motors that mimic the tactile feedback of hand files. Laser-assisted approaches remain niche due to capital costs above USD 25,000 and specialized training requirements, yet find growing favor in pediatric pulpotomy. AI-guided navigation, cleared as Software as a Medical Device in the United States and Europe, will expand at a 9.7% CAGR through 2031, reducing procedural errors and improving obturation quality by 15% in early trials presented at the American Association of Endodontists. Uptake varies sharply by geography; North American specialty practices lead, while many emerging markets remain in pilot stages.

Geography Analysis

North America captured 37.23% of global revenue in 2025. The United States hosts 15 million procedures annually and leads adoption of AI navigation and laser systems, though reimbursement for retreatment and adjunctive CBCT imaging remains inconsistent. Canada’s mixed public-private model creates a two-tier market, and Mexico’s border cities attract U.S. dental-tourists with FDA-cleared devices at 50% lower fees.

Asia-Pacific will grow at 8.51% CAGR through 2031, powered by rising middle-class incomes and government infrastructure pushes. China subsidizes rotary systems and apex locators for rural townships, narrowing urban-rural quality gaps. India produces over 2,000 new endodontic specialists each year, fueling procedural capacity. Thailand and Malaysia combine ISO-certified supply chains with internationally trained clinicians, underpinning dental-tourism appeal. Australia is evaluating single-use mandates that could speed rotations away from reusable files and lift consumables turnover.

Europe prioritizes infection control, with Germany and France reimbursing 70%–80% of disposable file costs, hastening adoption in both private and hospital settings. The United Kingdom’s NHS budget constraints maintain a divide between basic care and private premium offerings. Southern European cities cater to Northern European patients seeking lower prices yet CE-marked devices. The Middle East invests in dental hubs under healthcare diversification plans, and South Africa’s private sector adopts rotary and CBCT tech at rates similar to Southern Europe.

South America records pockets of rapid growth, mainly in Brazil and Argentina where urban chains standardize protocols. Currency volatility occasionally disrupts imports but fosters local refurbishment markets for CBCT and laser equipment.

Competitive Landscape

Dentsply Sirona and Envista jointly held a significant percentage of global revenue in 2025, leveraging end-to-end portfolios spanning files, motors, obturation devices, and imaging. FKG Dentaire, VDW, and Micro-Mega secure premium rotary-file margins via proprietary heat treatment and adaptive geometry that enhance flexibility and fatigue life. Biolase and Fotona are carving out the laser niche, while AI-navigation startups integrate CBCT data with real-time procedural guidance, fragmenting the equipment tier. ISO 13485 certification and FDA 510(k) clearance remain formidable entry barriers, especially after Europe’s MDR tightened evidence requirements. Contract manufacturers in China and India challenge price points, supplying generic files at up to 50% discounts, pressuring incumbents to differentiate through clinical data, continuous education, and digital service layers.

Patent activity is intense; Dentsply Sirona holds more than 150 live patents on NiTi metallurgy and file geometry[3]United States Patent and Trademark Office, “Patent Database Search,” USPTO, uspto.gov. FKG Dentaire’s XP-endo series uses shape-memory expansion to achieve taper-free shaping, gaining popularity in complex retreatments. Emerging white-space includes bioactive obturation sealers that accelerate healing, single-use file kits tailored to specific anatomies, and cloud-based platforms linking case documentation to inventory and reimbursement coding.

Endodontics Industry Leaders

Dentsply Sirona

Septodont Holding

Brasseler USA

Envista (Kerr)

Coltene Holding

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Septodont launched GenENDO1, a new file system distributed exclusively through Micro-Mega that supports efficient canal shaping.

- June 2025: Swiss start-up Odne raised CHF 4.2 million to accelerate U.S. rollout of its Root Preservation Therapy suite following FDA clearance for OdneClean, OdneCure, and OdneFill.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the endodontics market as all value generated worldwide from instruments, apex locators, endodontic motors, lasers, handpieces, machine-assisted obturation units, and consumables such as NiTi rotary files, irrigants, gutta-percha, and bioceramic sealers that are deployed solely for primary root-canal therapy, retreatment, or surgical endodontic procedures across clinics, hospitals, and teaching institutes.

Scope exclusion: general dental imaging systems, implants, and orthodontic devices are not counted.

Segmentation Overview

- By Product Type

- Consumables

- Endodontic Burs

- Obturation Materials

- Endodontic Files & Shapers

- Irrigation Solutions & Lubricants

- Instruments / Equipment

- Apex Locators

- Lasers

- Machine-Assisted Obturation Systems

- Scalers

- Others

- Consumables

- By End-User

- Dental Clinics

- Dental Hospitals

- Academic & Research Institutes

- By Technology

- Manual Systems

- Rotary Systems

- Laser-Assisted Endodontics

- AI-Guided Navigation Systems

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We then interviewed practicing endodontists, procurement heads at multi-site dental service organizations, and regional distributors across North America, Europe, Asia-Pacific, and the Gulf to validate unit volumes, average selling prices, NiTi adoption rates, and consumable re-use practices that do not surface in secondary sources.

Desk Research

Mordor analysts first compiled trade and patient-care statistics from sources such as the World Health Organization's oral-health data sets, the American Association of Endodontists, Eurostat treatment discharge files, and national customs records tracking HS codes for dental consumables. Regulatory filings from the FDA and CE mark databases helped us map product clearances by type, while company 10-K statements, investor decks, and clinical-trial registries illustrated revenue splits and pipeline traction. Subscription databases, Dow Jones Factiva for deal news, D&B Hoovers for manufacturer financials, and Questel for patent counts, added competitive and innovation signals. Other publicly available academic journals supplied prevalence ratios and success-rate benchmarks. This list is illustrative; numerous additional publications were reviewed to corroborate figures and fill data gaps.

Market-Sizing & Forecasting

A top-down build used procedure volumes and average material spend per root-canal case, which are reconstructed from public treatment statistics and import values, then cross-checked through sampled ASP × volume roll-ups from key suppliers. Variables such as untreated caries prevalence, dentist-to-population ratios, disposable income growth, and NiTi file penetration inform our model. A multivariate regression projects these drivers to 2030, and selective bottom-up channel checks fine-tune regional totals where public data are thin.

Data Validation & Update Cycle

Outputs pass a two-step analyst review against independent signals, quarterly manufacturer sales, shipment anomalies, and currency swings. Reports refresh every twelve months, with interim updates triggered by major product launches or regulatory shifts; a final pre-publication audit ensures clients receive the latest view.

Why Mordor's Endodontics Baseline Commands Reliability

Published estimates often diverge because firms choose different product baskets, base years, and refresh cadences. Our disciplined scope selection, annual updating, and dual-track validation keep Mordor's numbers steady yet responsive.

Key gap drivers include whether consumables are bundled with broader dental equipment, the use of list instead of blended ASPs, and limited primary interviews that miss real-world re-use or price erosion. We also convert all revenues to USD at the average annual rate, reducing currency noise.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.05 B (2025) | Mordor Intelligence | - |

| USD 2.41 B (2024) | Global Consultancy A | Wider basket includes general dental burs and imaging disposables |

| USD 1.86 B (2024) | Research Publisher B | Excludes lasers; relies on list prices without regional discounts |

| USD 1.76 B (2024) | Industry Journal C | Devices only, no consumables; forecast based on historical CAGR extension |

Taken together, the comparison shows that once differing scopes and price assumptions are stripped away, Mordor's baseline offers a balanced midpoint grounded in clear variables, refreshed data, and transparent steps that decision-makers can replicate.

Key Questions Answered in the Report

What is the current value of the Endodontics market?

The Endodontics market size reached USD 2.16 billion in 2026 and is projected to hit USD 2.83 billion by 2031.

How fast is global demand for root-canal equipment growing?

Aggregate revenue is forecast to expand at a 5.55% CAGR through 2031, with instruments and equipment segments rising faster than consumables.

Which region will post the highest growth through 2031?

Asia-Pacific will advance at an 8.51% CAGR thanks to dental-tourism hubs, rising middle-class incomes, and public support for rural clinics.

Which technology segment is the most disruptive?

AI-guided navigation systems, cleared as Software as a Medical Device, are poised to grow 9.7% annually by reducing procedural errors and chair time.

Page last updated on: