Encapsulated Lactic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.45 Billion |

| Market Size (2031) | USD 2.01 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

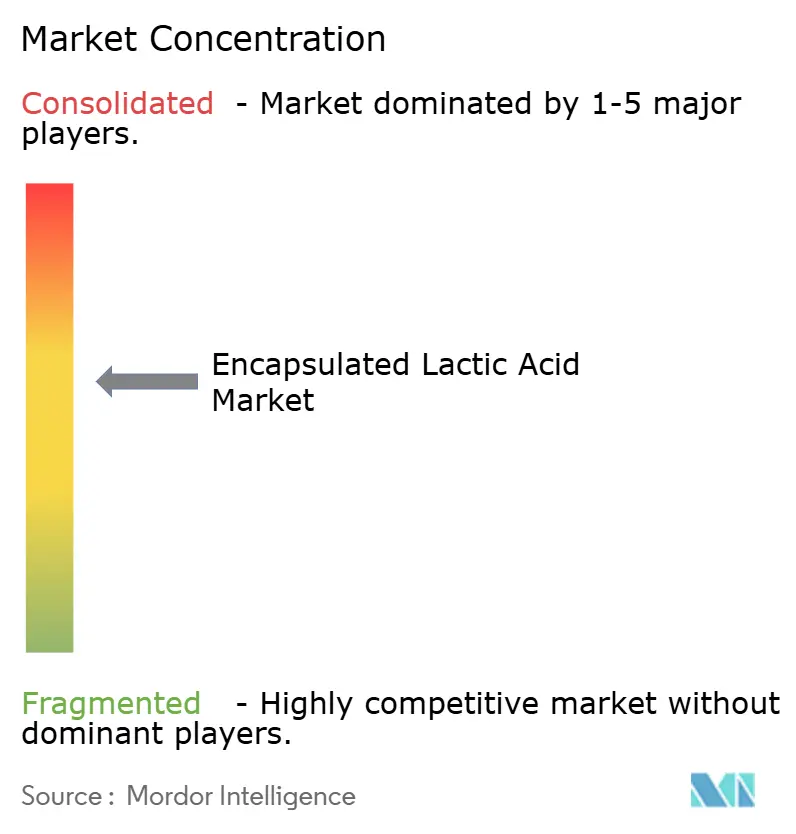

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Encapsulated Lactic Acid Market Analysis by Mordor Intelligence

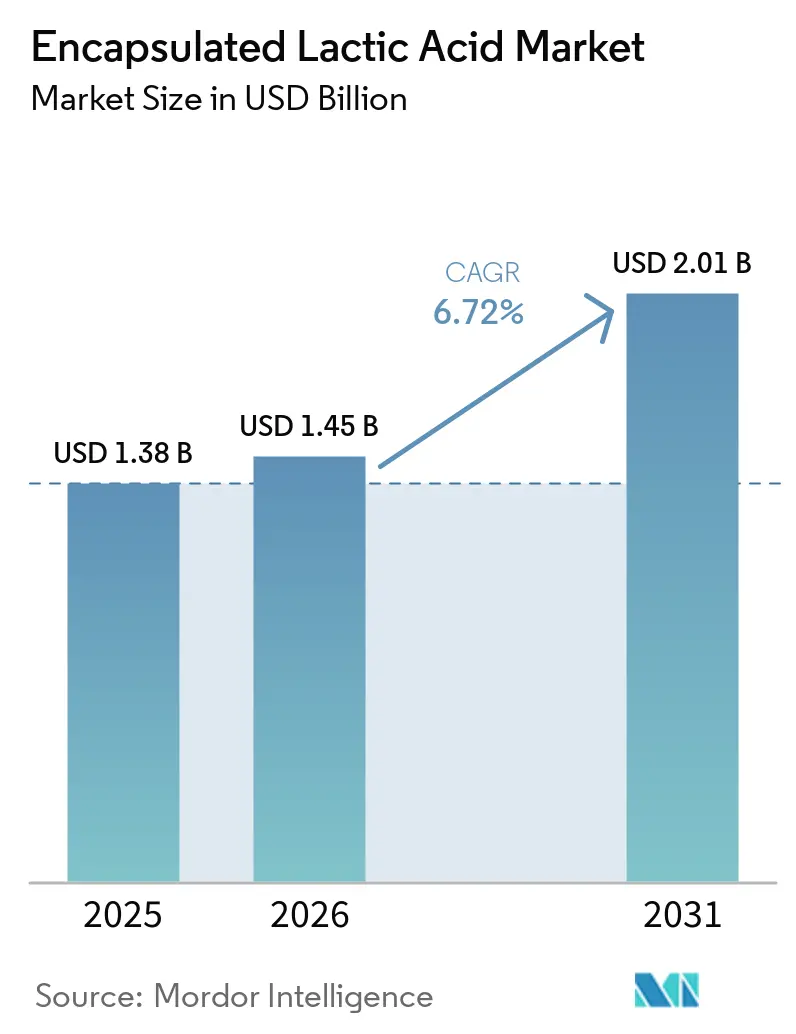

The encapsulated lactic acid market size is projected to be USD 1.38 billion in 2025, USD 1.45 billion in 2026, and reach USD 2.01 billion by 2031, growing at a CAGR of 6.72% from 2026 to 2031. The encapsulated lactic acid market is expanding because encapsulation now works as a functional precision tool, which supports premium pricing across bakery, meat, nutraceutical, and pharmaceutical end uses. Clean-label reformulation in processed food, higher probiotic supplement use, and stronger pharmaceutical demand for biodegradable polymer matrices are lifting demand across the encapsulated lactic acid market. The value proposition in the encapsulated lactic acid market comes from converting a commodity acid into a controlled-release ingredient, which favors producers that own coating systems and fermentation capabilities. Competitive behavior in the encapsulated lactic acid market is increasingly shaped by proprietary encapsulation matrices, feedstock integration, and quality consistency that can support regulated applications. Direct acidification in processed meat and rising quality standards from biomedical polymer applications are also giving the encapsulated lactic acid market a more durable growth base than a standard food-ingredient view would suggest.

Key Report Takeaways

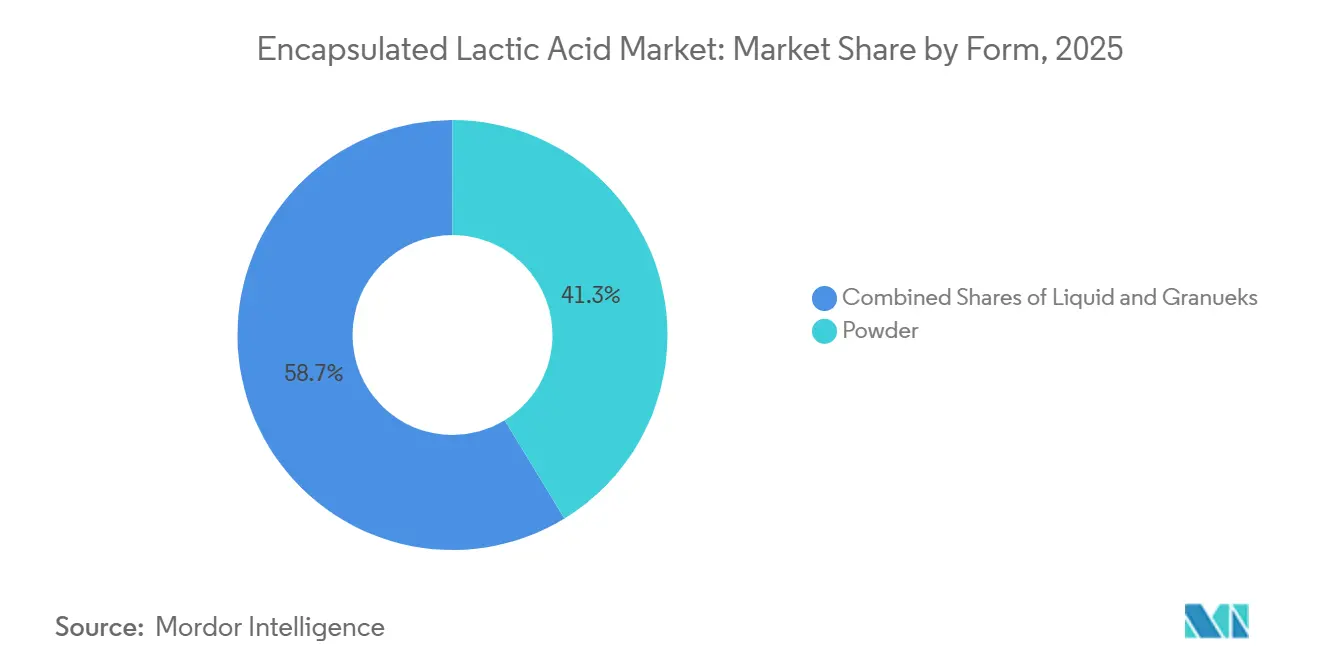

- By form, powder held 41.27% share in 2025, while liquid is forecast to grow at 8.02% CAGR through 2031.

- By source, plant-based sources captured 64.38% of the encapsulated lactic acid market share in 2025, while the same segment is also projected to expand at 7.21% CAGR through 2031.

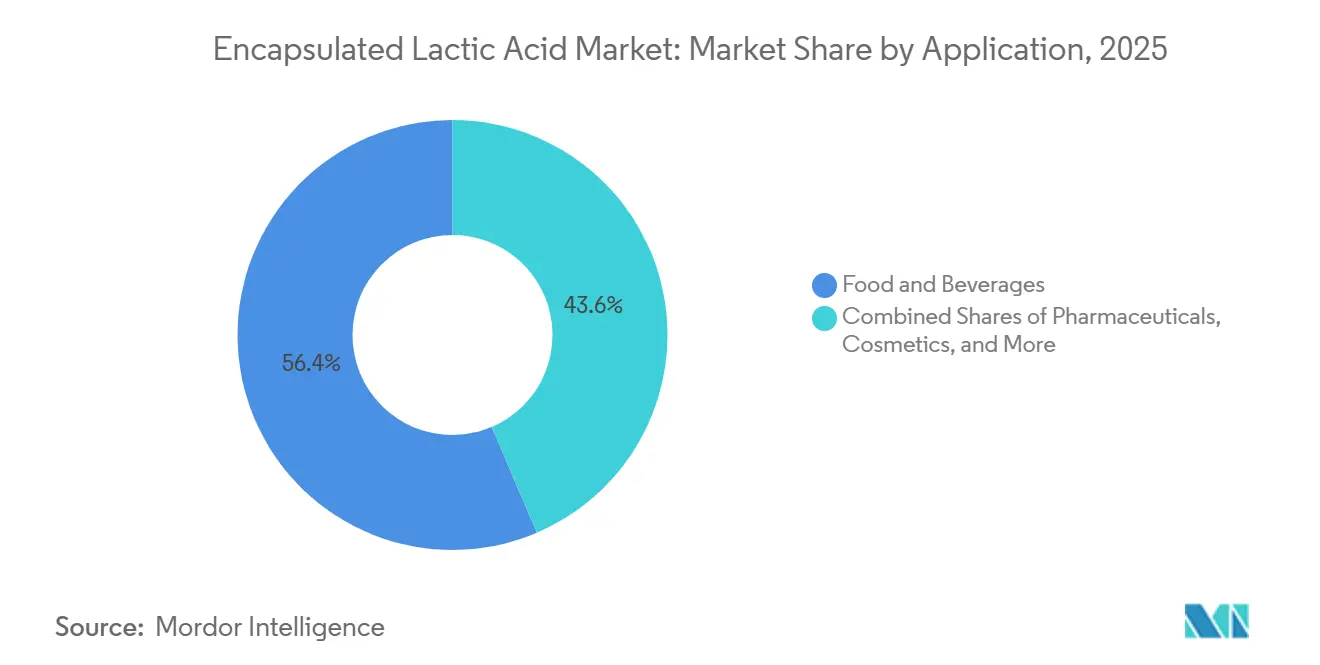

- By application, food and beverages accounted for 56.42% of the encapsulated lactic acid market size in 2025, while pharmaceuticals are advancing at 7.55% CAGR through 2031.

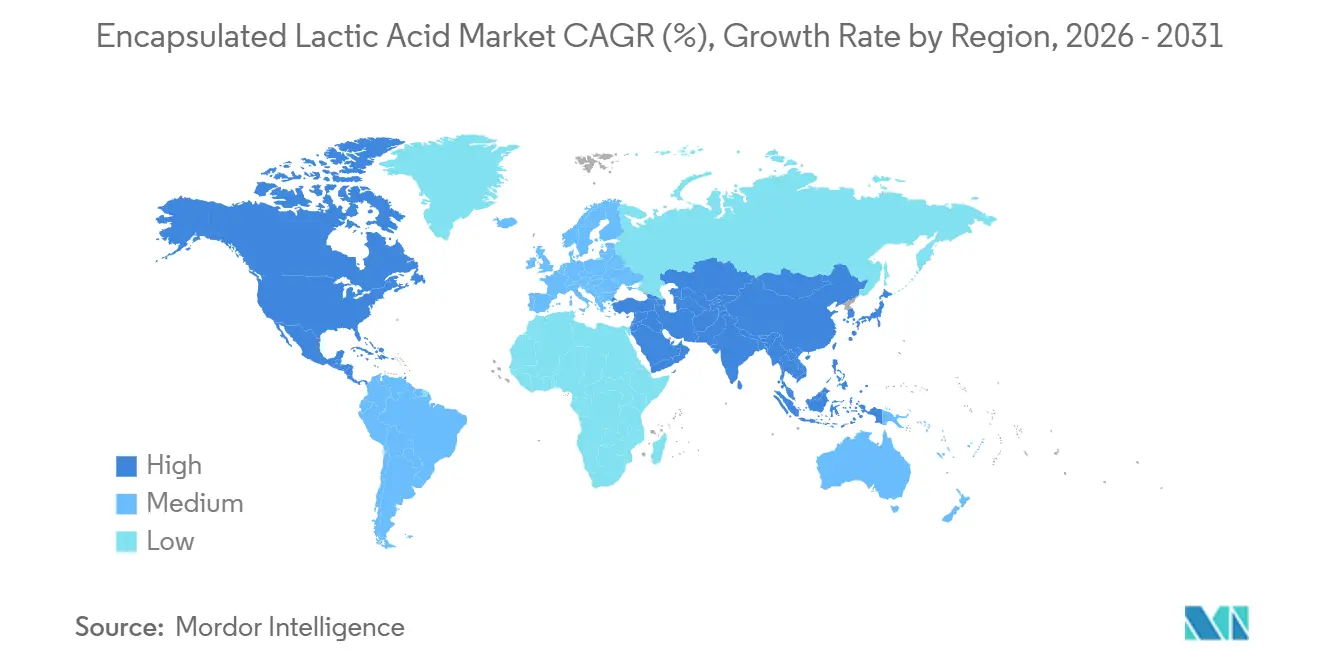

- By geography, North America led with 40.21% share in 2025, while Asia-Pacific is projected to record the fastest CAGR at 7.62% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Encapsulated Lactic Acid Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nutraceutical And Dietary Supplement Application Growth | +1.5% | North America, Europe | Medium term (2-4 years) |

| Dry Mixes And Instant Food Product Expansion | +1.0% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Encapsulation Technology Advancements | +1.2% | Global | Long term (≥ 4 years) |

| Rising Demand For Acid-Sensitive Ingredient Formulations | +0.8% | North America, Europe | Medium term (2-4 years) |

| Functional Food And Probiotic Format Expansion | +1.1% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Sustainable And Bio-Based Formulation Shift | +0.7% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nutraceutical And Dietary Supplement Demand Redefines Encapsulation Economics

The encapsulated lactic acid market is benefiting from stronger nutraceutical demand because supplement brands need delivery systems that protect sensitive actives and improve ingredient performance. Lactic acid already has GRAS recognition in the United States, which gives product developers a clearer regulatory path in food and supplement applications[1]Source: U.S. Food and Drug Administration, “GRAS Notices, Lactic Acid,” U.S. Food and Drug Administration, fda.gov. Probiotic supplement expansion is increasing demand for coatings that can protect ingredients during gastric transit and release them later in the digestive cycle. Corbion stated in 2025 that its pharmaceutical-grade sodium lactate and biomedical polymer capabilities are being extended into nutraceutical delivery systems, which shows tighter overlap between supplement and pharmaceutical supply requirements. This is raising the value of suppliers that can meet pharmaceutical-grade L(+) purity expectations while still serving the broader encapsulated lactic acid market. The result is a margin profile in premium supplements that commodity food-grade suppliers are less able to access.

Encapsulation Technology Advances Lower The Barrier To Specialty Formats

The encapsulated lactic acid market continues to rely on spray drying because it remains the most scalable and cost-effective way to produce stable encapsulated powders. The technology focus is now moving toward dual-coating systems and complex coacervation based on plant proteins and polysaccharides. Research published in 2025 showed that plant protein and polysaccharide coacervates can reach encapsulation performance close to synthetic polymer systems while also supporting vegan-label compatibility. For the encapsulated lactic acid market, that shift matters because it creates a cleaner-label route that also reduces dependence on older coating systems. Balchem’s BakeShure®, ConfecShure®, and MeatShure® lines show how changes in coating chemistry can directly widen addressable applications and support margin defense. Better coating efficiency and lower wall-material cost are also making specialty grades more accessible in applications that once relied on standard powder formats.

Functional Foods And Probiotic Expansion Create A Compounding Demand Effect

The encapsulated lactic acid market is gaining from probiotic expansion because encapsulation can support both ingredient stability and functional delivery in one system. A 2025 study in the Journal of Food Quality found that PLGA-based microencapsulation maintained probiotic viability above the therapeutic threshold under simulated gastrointestinal conditions. That matters because encapsulated lactic acid can work both as a protective matrix and as a functional acidulant in the same formulation. Food companies that use this dual role can simplify formulas and avoid separate carriers and acidulants in finished products. Corbion joined the Ferment4Health consortium in 2026, which shows that suppliers are investing earlier in platform science around fermented food and gut health applications. This is helping the encapsulated lactic acid market move beyond single-product innovation and toward more defensible formulation claims tied to clinical validation and ingredient functionality.

Bio-Based Sourcing Mandates Elevate Feedstock Origin As A Competitive Differentiator

The encapsulated lactic acid market is also being shaped by feedstock origin because bio-based procurement criteria are becoming stricter in Europe and Japan. Corbion reported that it launched a circular lactic acid plant in Thailand in 2024, which strengthens the supply base for bio-derived lactic acid and supports resource efficiency goals. NatureWorks opened a fully integrated Ingeo biopolymer facility in Thailand in April 2026, linking sugarcane-based lactic acid production with lactide and PLA operations in one complex. Research published in 2025 identified lignocellulosic waste streams such as corn stover and sugarcane bagasse as viable alternative substrates for lactic acid fermentation. Those developments support the encapsulated lactic acid market because they widen the long-term feedstock base and strengthen resilience against conventional agricultural input cycles. Companies that lock in bio-based feedstock agreements are better placed to defend margins where sustainability screening has become part of supplier qualification.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Encapsulation Cost And Process Complexity | -1.0% | Global, particularly South America & MEA | Medium term (2-4 years) |

| Limited Scale-Ready Supply Of Specialized Feedstocks | -0.7% | Asia-Pacific, Europe | Short term (≤ 2 years) |

| Substitution By Free Lactic Acid In Low-Sensitivity Uses | -0.5% | Global | Short term (≤ 2 years) |

| Regulatory And Stability Validation Burden | -0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Encapsulation Cost And Process Complexity Limit Mid-Market Penetration

The encapsulated lactic acid market still faces cost pressure because encapsulation adds a premium that many bulk food categories cannot absorb easily. Commodity-oriented manufacturers in standard bakery, dairy, and seasoning applications often compare encapsulated formats directly with free acid alternatives. Controlled-release manufacturing also requires wall-material selection, coating thickness control, moisture testing, and release-rate validation. Those steps raise both capital needs and technical complexity for regional suppliers in South America and the Middle East and Africa. Balchem’s USD 36 million investment in a new microencapsulation facility in Orange County, New York, highlights the scale required to reduce unit cost while maintaining coating quality. The encapsulated lactic acid market therefore remains harder to enter for smaller producers that lack both specialized personnel and the financial capacity to build repeatable controlled-release systems.

Feedstock Supply Concentration Creates A Structural Input Vulnerability

The encapsulated lactic acid market also carries input risk because lactic acid fermentation depends heavily on corn and sugarcane as primary carbohydrate sources. Research published in 2025 noted that conventional lactic acid fermentation competes directly with food and animal feed markets for those same substrate pools[2]Source: Mendez L. et al., “Complex Coacervation of Plant-Based Proteins and Polysaccharides, Sustainable Encapsulation Techniques for Bioactive Compounds,” Food Engineering Reviews, springer.com. Specialty encapsulation-grade material needs high optical purity in the L(+) isomer configuration, which narrows substitution flexibility during supply disruption. The problem extends beyond fermentation substrates because specialized coating materials also have concentrated supply chains across regions. Futerro’s 2025 partnership with Galactic in France showed how producers are responding through tighter integration with local biomass infrastructure and downstream derivatives capacity. This makes feedstock security and local sourcing an increasingly important competitive factor in the encapsulated lactic acid market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Leads As Liquid Format Demand Accelerates

Powder formats retained 41.27% of the encapsulated lactic acid market in 2025, which kept them in the lead across form segments. Their position reflects long-established dry-blend infrastructure in bakery, meat processing, and instant food production. Powder also remains easy to dose, stable under ambient conditions, and compatible with standard blending equipment used in large-volume processing lines. These traits keep the encapsulated lactic acid market anchored in formats that support scale and consistency across routine manufacturing runs. Spray drying remains the main production route for powder and granule formats because it can support high-volume output with controlled particle morphology.

Granules serve a narrower but important role in the encapsulated lactic acid market because they are better suited to slower dissolution and staged acid release. That makes them useful in confectionery applications, especially sour candy, and in probiotic systems that require delayed release behavior. The segment is also seeing interest in combining nanoencapsulation techniques with conventional spray drying to improve coating uniformity without losing industrial throughput. MDPI.COM Liquid is projected to grow at 8.02% CAGR through 2031, which makes it the fastest-growing form in the encapsulated lactic acid market size outlook. That growth is tied to ready-to-drink probiotic beverages, sports nutrition liquids, and liquid nutraceuticals where rapid dispersibility is essential.

By Source: Plant-Based Dominance Signals A Structural Market Preference

Plant-based sources held 64.38% of the encapsulated lactic acid market share in 2025, and they are also projected to grow at 7.21% CAGR through 2031. That dual lead in both size and growth shows that the preference in the encapsulated lactic acid industry is structural rather than temporary. Fermentation-derived lactic acid from sugarcane, corn, and cassava fits clean-label positioning, vegan certification needs, and retailer pressure to remove animal-derived processing aids. Jungbunzlauer states that its L(+)-lactic acid is produced through fermentation of natural carbohydrates and uses the L(+) isomer because of its favorable human metabolization profile. Research published in 2025 also identified agricultural waste streams such as cassava processing wastewater and corn steep water as promising lower-cost fermentation substrates.

Animal-based sources represented 35.62% of the market in 2025 and still matter in pharmaceutical-grade encapsulation, where casein and whey coatings can support stronger gastric protection and controlled release. At the same time, plant protein coacervation research is narrowing that performance gap. A 2025 review in Food Engineering Reviews described dual-coating systems that use pea protein with polysaccharides to achieve stability and release behavior comparable to dairy-based coatings. If validated at commercial scale, those systems would reduce allergen management burdens and simplify supply chain compliance in regulated procurement settings. That would strengthen the long-run position of plant-based materials within the encapsulated lactic acid market.

By Application: Food Anchors Volumes, Pharmaceuticals Drive Premium Growth

Food and beverages held 56.42% of the encapsulated lactic acid market in 2025, which kept this segment as the main volume anchor. Encapsulation solves the problem of premature acid release during processing in meat, bakery, confectionery, and dairy applications. In processed meat, Balchem’s MeatShure® line shows how encapsulated acid systems can replace live starter cultures, remove the fermentation stage, and deliver more precise pH control. Cosmetics and personal care also remain relevant because sustained release can reduce irritation while extending acid contact time in sensitive-skin formulations. Animal feed adds another important use case because encapsulated lactic acid can support intestinal pH control in poultry and swine systems where antibiotic growth promoters face tighter restrictions.

Pharmaceuticals is projected to grow at 7.55% CAGR through 2031, making it the fastest-growing application in the encapsulated lactic acid market. Growth is being driven by wider use of PLGA-based injectable formulations across oncology, endocrinology, and reproductive health. Research published in RSC Pharmaceutics in 2026 confirmed that PLGA microspheres can achieve sustained drug release through diffusion and polymer degradation, with lactic acid metabolites then assimilated safely in the body[3]Source: Desai N. et al., “Advanced Mechanisms of Polymer-Based Drug Delivery Systems for Clinical Applications,” RSC Pharmaceutics, pubs.rsc.org. Work published in Nutrition and Diabetes in 2025 also linked expansion in GLP-1 delivery systems with the need for long-acting injectable formulation approaches that often rely on PLGA matrices. A 2025 review in BioNanoScience further showed that particle size and encapsulation efficiency in PLGA systems are actively tuned through polymer molecular weight and stabilizer selection, which raises the value of high-purity lactic acid in this part of the encapsulated lactic acid market.

Geography Analysis

North America remained the largest regional segment in the encapsulated lactic acid market at 40.21% in 2025. The United States supports that position because lactic acid has GRAS status for food applications, which lowers regulatory friction across food and supplement formulation. The region also benefits from strong processed meat activity and a mature nutraceutical channel, both of which support repeat demand for controlled-release acidulants. Balchem’s USD 36 million investment in Orange County, New York, which is intended to more than double its microencapsulation capacity, reinforces confidence in sustained domestic demand. Europe held the second-largest position in the encapsulated lactic acid market, supported by demand for fermentation-derived acid systems in processed food and clean-label reformulation. Corbion’s BRIGHT 2030 strategy also places clean-label preservation and biomedical polymers at the center of its growth agenda across European and North American channels.

Asia-Pacific is the fastest-growing region in the encapsulated lactic acid market size profile, with a projected CAGR of 7.62% through 2031. Food processing expansion across China, India, Japan, and Southeast Asia is broadening the regional demand base. China remains the largest country market in the region, while India is gaining importance through its expanding nutraceutical and pharmaceutical contract manufacturing base. Japan adds a more specialized demand pattern centered on enzyme-stabilized and pH-sensitive functional food systems. NatureWorks’ fully integrated 75,000-ton facility in Nakhon Sawan, Thailand, opened in April 2026 and signaled deeper regional integration across lactic acid, lactide, and PLA supply.

South America and the Middle East and Africa remain smaller in the encapsulated lactic acid market, but each region has distinct demand patterns. Brazil anchors South America through processed meat preservation needs, while Argentina remains more visible in dairy-related use. Price sensitivity across the region favors cost-competitive powder formats over higher-priced specialty encapsulation systems. In the Middle East and Africa, demand is still at an early stage and remains concentrated in the UAE and South Africa across food service and pharmaceutical cold-chain applications.

Competitive Landscape

The encapsulated lactic acid market is semi-consolidated, with a technology-led group of multinational specialty ingredient companies at the top and a wider set of regional producers competing in standard powder grades. Corbion N.V., Balchem Corporation, and Galactic S.A. remain central names because they combine fermentation capability with differentiated coating know-how or broader preservation platforms. Corbion’s BRIGHT 2030 strategy, announced in 2025, targets natural preservation, nutrition, and biomaterials, which shows how the company is linking food and biomedical growth paths rather than treating them as separate businesses. Balchem’s USD 36 million Orange County expansion is another clear strategic move because it is designed to more than double microencapsulation capacity for its controlled-release ingredient lines. Galactic’s broader portfolio development in fermentation-based preservation also suggests that competitive positioning is widening beyond core lactic acid alone.

The most attractive white space in the encapsulated lactic acid market sits in pharmaceutical-grade PLGA-related applications because those uses require high optical purity and stricter manufacturing controls. Many Asian commodity producers can compete on price in basic powder grades, but they face a much higher barrier in regulated formats that need stronger analytical systems and quality assurance. Competitive differentiation is also moving toward encapsulation matrix design, especially plant protein and polysaccharide systems that can deliver controlled release without synthetic polymer inputs. That matters because customers are asking for cleaner labels while still expecting performance consistency across food, nutraceutical, and pharmaceutical uses. Suppliers that stay tied to older PHO-based coating routes face more pressure as retailer ingredient standards and product reformulation requirements move upstream into processing aids and encapsulants.

Competitive behavior in the encapsulated lactic acid market is therefore becoming more platform-driven than product-driven. Companies that can connect fermentation quality, coating science, and application support are better positioned to defend premiums. Companies that cannot do that are more likely to remain in lower-priced grades where regional competition is stronger. This dynamic keeps the market open enough for regional participation, but it still favors a smaller set of firms in higher-value applications.

Encapsulated Lactic Acid Industry Leaders

BASF SE

Cargill Incorporated

Corbion N.V.

DSM-Firmenich

Kerry Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: NatureWorks announced the grand opening of its fully integrated Ingeo biopolymer manufacturing facility in Nakhon Sawan, Thailand, the first time a PLA producer has established a second global manufacturing site. The complex integrates sugarcane-sourced lactic acid production, lactide monomer synthesis, and PLA polymerization at a single site with 75,000 tons of annual capacity, significantly expanding bio-derived lactic acid supply in Asia-Pacific and globally.

- December 2025: Balchem announced development of a new USD 36 million, high-capacity microencapsulation manufacturing facility in Orange County, New York, scheduled to open in 2027. The site will more than double Balchem's production capacity for its BakeShure, ConfecShure, and MeatShure encapsulated ingredient lines, including encapsulated lactic acid for bakery, confectionery, and meat applications, reinforcing Balchem's market position as a controlled-release acidulant leader.

- May 2025: Futerro S.A. and Galactic S.A. announced a strategic partnership to establish a lactic acid derivatives production facility co-located with Futerro's project site at Port-Jérôme-sur-Seine, France, drawing on Tereos's locally sourced biomass supply.

Global Encapsulated Lactic Acid Market Report Scope

| Powder |

| Liquid |

| Granuels |

| Plant-Based |

| Animal-Based |

| Food and Beverages |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Animal Feed |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Powder | |

| Liquid | ||

| Granuels | ||

| By Source | Plant-Based | |

| Animal-Based | ||

| By Application | Food and Beverages | |

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Animal Feed | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of encapsulated lactic acid demand

The encapsulated lactic acid market stands at USD 1.45 billion in 2026 and is projected to reach USD 2.01 billion by 2031 at a CAGR of 6.72%.

Which application area generates the highest revenue?

Food and beverages led with 56.42% share in 2025 because encapsulation helps control acid release in meat, bakery, confectionery, and dairy uses.

Which application is growing the fastest through 2031?

Pharmaceuticals is the fastest-growing application at 7.55% CAGR, supported by PLGA-based delivery systems and long-acting injectable drug development.

Which region is leading current demand?

North America held the largest regional share at 40.21% in 2025, supported by processed food demand, nutraceutical activity, and strong domestic production capacity.

Page last updated on: