Lactase Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

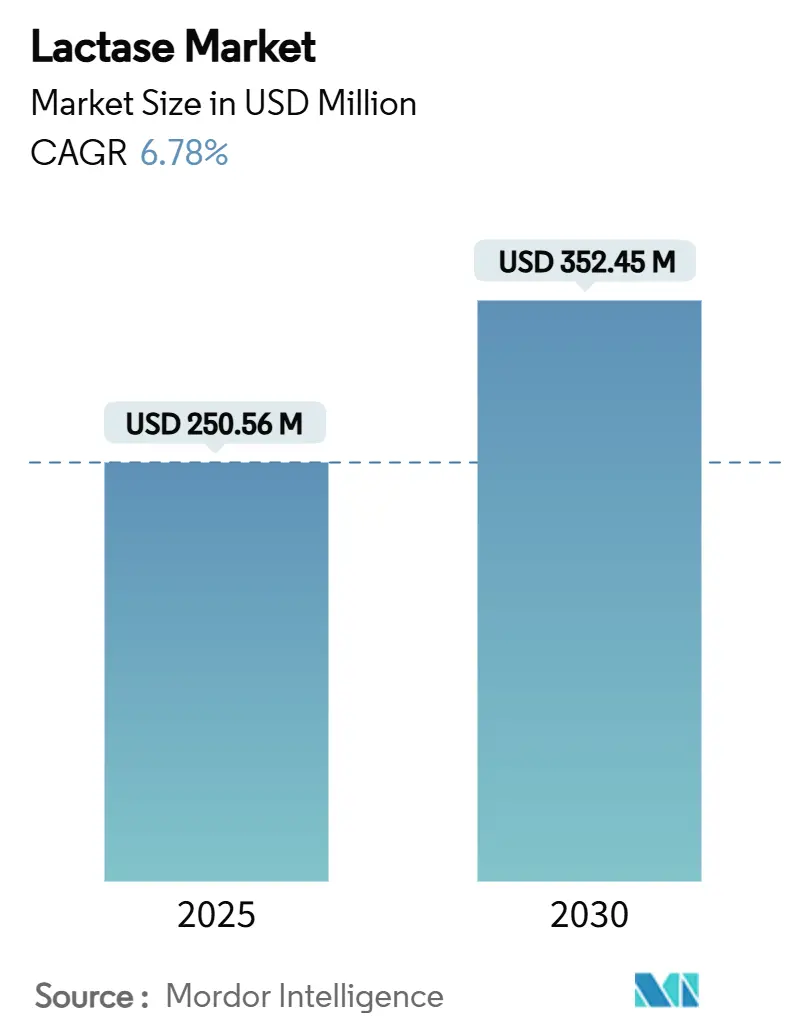

| Market Size (2025) | USD 250.56 Million |

| Market Size (2030) | USD 352.45 Million |

| Growth Rate (2025 - 2030) | 6.78% CAGR |

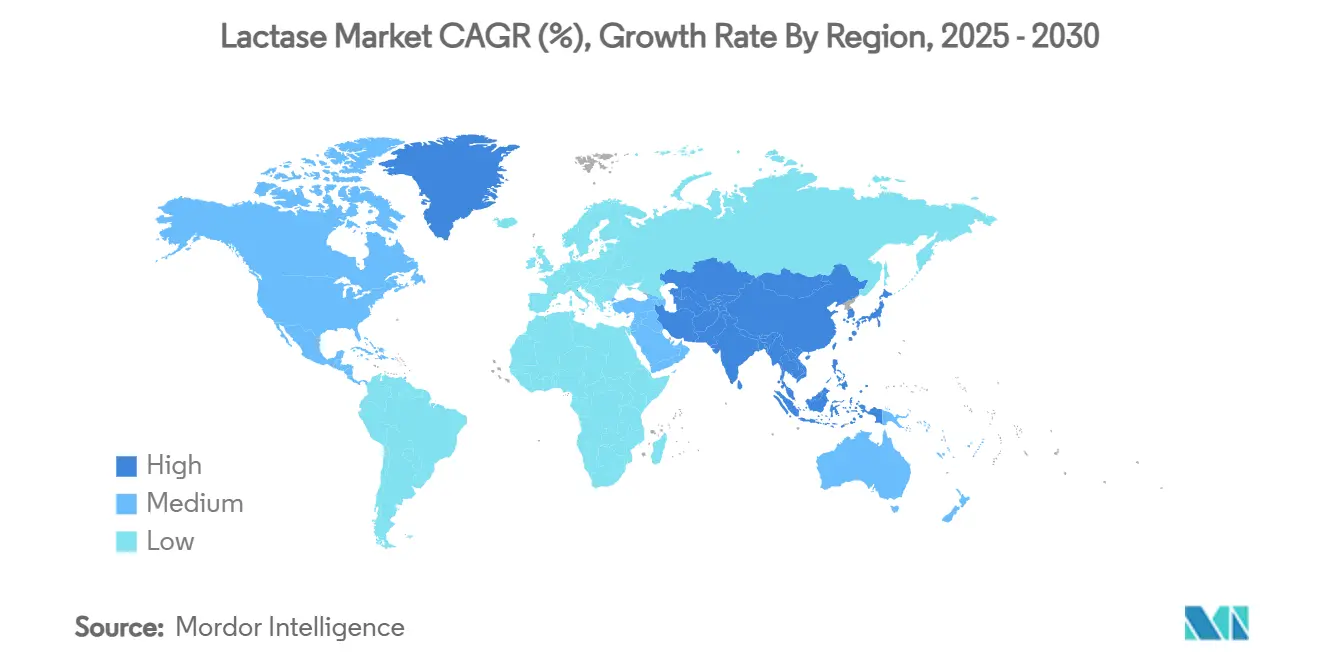

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lactase Market Analysis by Mordor Intelligence

The global lactase market size stands at USD 250.56 million in 2025 and is forecast to climb to USD 352.45 million by 2030, translating to a 6.78% CAGR over the period. Accelerating diagnosis of lactose malabsorption, rapid adoption of lactose-free product ranges, and regulatory clearance for multiple genetically modified and non-modified enzyme strains are the principal engines of expansion for the lactase enzyme market. Competitive differentiation is increasingly driven by high-purity formulations and cost-efficient enzyme immobilization technologies, while clean-label purchasing preferences are nudging processors toward non-GMO sources. Regional adoption patterns remain uneven: North America’s mature consumer base supports premium applications, Europe’s regulatory stringency guides sourcing strategies, and Asia Pacific’s growing lactose-intolerant population underpins outsized volume growth. Together, these factors sustain technology investment, price discipline, and multi-year pipeline visibility across the lactase enzyme industry.

Key Report Takeaways

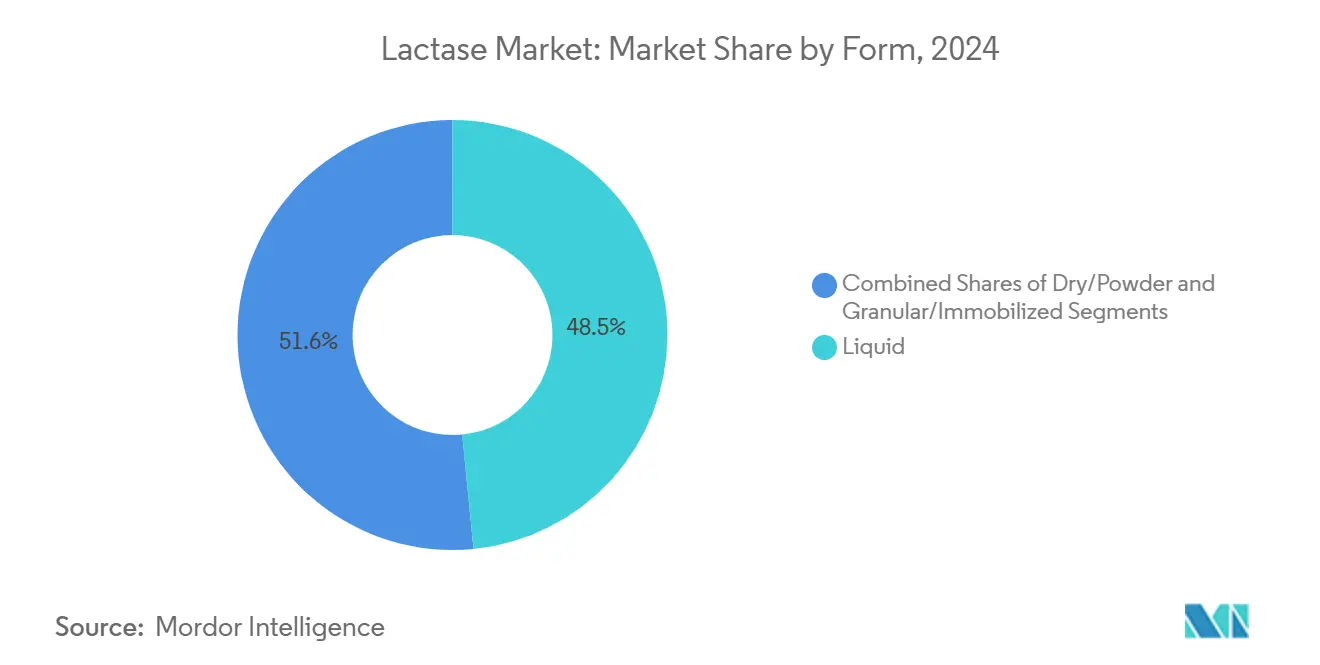

- By form, liquid formats held 48.45% of the lactase market share in 2024, while powder forms are set to grow at a 7.12% CAGR between 2025 and 2030.

- By source, yeast-derived lactase captured 55.67% of the lactase enzyme market size for source-based categories in 2024; fungal lactase is forecast to register the fastest 7.45% CAGR to 2030.

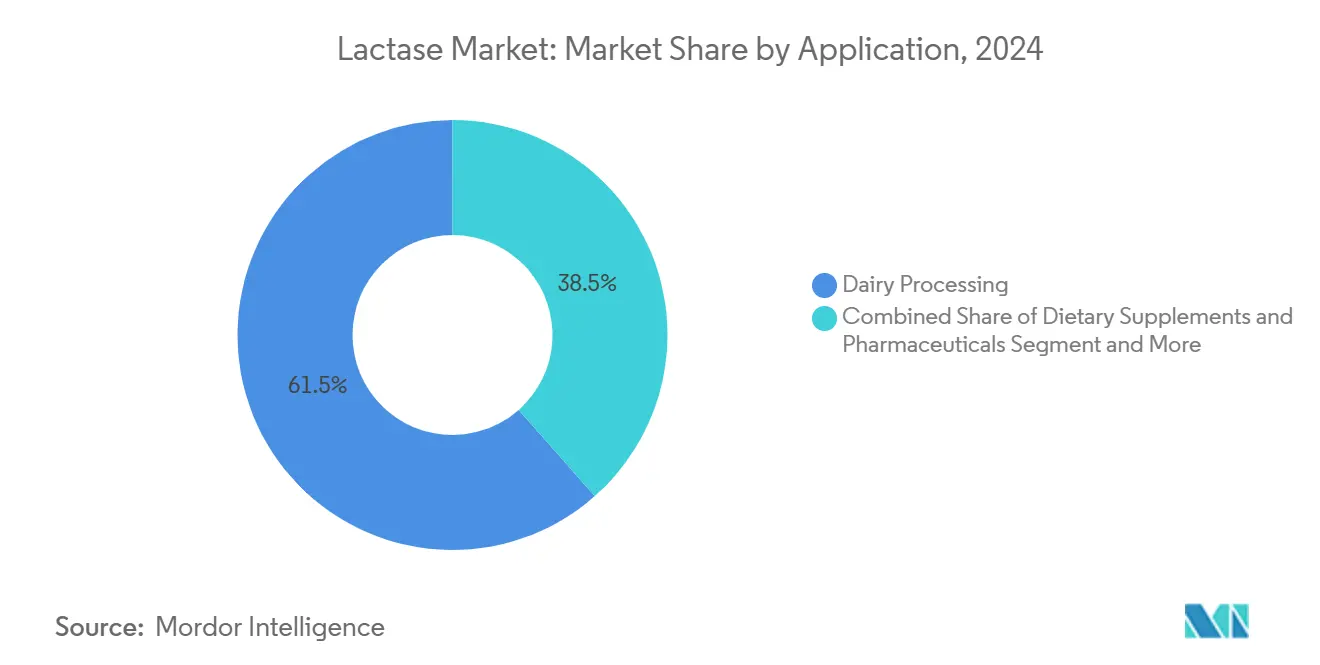

- By application, dairy processing accounted for 61.45% of the lactase market share in 2024 and is projected to expand at an 8.23% CAGR through 2030.

- By geography, North America commanded 33.67% of global revenue in 2024, whereas the Asia Pacific is projected to reach a 7.44% CAGR through 2030.

Global Lactase Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of lactose intolerance | +1.0% | Global; strongest in Asia Pacific and Latin America | Long term (≥ 4 years) |

| Surge in lactose-free product launches | +0.8% | North America and Europe; spreading to Asia Pacific | Medium term (2–4 years) |

| Demand for clean-label enzymes | +0.7% | Global; led by North America and Western Europe | Medium term (2–4 years) |

| Low-sugar positioning enabled by lactase | +0.5% | North America and Europe; emerging in Asia andPacific | Short term (≤ 2 years) |

| Cost-cutting enzyme immobilization tech | +0.5% | Global; early adoption in developed markets | Long term (≥ 4 years) |

| Micro-channel bioreactors for on-site use | +0.4% | Industrial hubs in North America, Europe, East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Lactose Intolerance Worldwide

Nearly 70% of adults globally have genetic lactase non-persistence, particularly in Asia, Africa, and Latin America, making them unable to digest conventional dairy products without discomfort, according to the Medline Plus data[1]Source: Medline Plus, "Lactose Intolerance", medlineplus.gov.. Medical professionals increasingly recommend lactase supplementation rather than dairy avoidance, which strengthens the demand for lactase enzymes. Clinical studies conducted on Korean adults demonstrated reduced hydrogen-breath-test levels after consuming low-lactose milk for one month, validating the enzyme's effectiveness. The increasing disposable income in developing economies has led to higher dairy consumption, driving the demand for lactase enzymes. Research shows that galacto-oligosaccharides, produced through enzymatic hydrolysis, promote beneficial gut bacteria, adding digestive health benefits to these products.

Surge in Lactose-Free Dairy Product Launches in Retail Chains

The retail market for lactose-free products has expanded beyond traditional milk into premium categories, including artisanal cheese, Greek yogurt, and specialty ice cream. This expansion creates new opportunities for enzyme applications across products with different pH and temperature requirements. As plant-based alternatives grow, dairy processors are developing lactose-free versions of traditional products to maintain market share, which increases the demand for lactase enzymes. The market emphasis on clean-label products has led to the adoption of lactic acid bacteria fermentation instead of synthetic preservatives in yogurt production. This shift requires specialized enzyme formulations that remain effective in fermented environments. Retailers now require enzyme solutions that extend product shelf life while maintaining taste quality. The combination of lactase enzymes with protective cultures and postbiotics addresses both lactose intolerance and clean-label requirements in dairy products.

Rising Demand for Clean-Label Enzymes from Dairy Processors

Recent regulations on clean-label ingredients are influencing enzyme sourcing in food processing, as manufacturers seek non-genetically modified alternatives that maintain efficiency and performance. The European Food Safety Authority's 2024 safety assessments of non-GMO lactase sources, including Kluyveromyces lactis strain GD-YNL and Aspergillus sp. strain GD-FAL, establish regulatory frameworks for clean-label enzyme implementation. Dairy processors are adopting enzyme immobilization technologies to improve stability and reuse capabilities, addressing both economic and environmental considerations. The industry faces the task of meeting clean-label standards while ensuring functional effectiveness, as natural enzymes typically show different performance characteristics than their engineered counterparts. New developments in purification methods and immobilization materials help processors achieve clean-label compliance while maintaining production efficiency and product standards.

Health-Positioning of Low-Sugar Claims Enabled by Lactase

Lactase hydrolysis converts lactose into glucose and galactose, allowing dairy products to maintain natural sweetness while qualifying for low-sugar claims. This enzymatic process provides significant benefits over artificial sweeteners, as the resulting simple sugars enhance calcium absorption and act as prebiotics in the digestive system. The FDA's allergen labeling guidelines require comprehensive disclosure of enzymatic modifications in dairy products to ensure consumer safety and transparency. The emergence of precision fermentation technology enables the production of dairy proteins without traditional dairy processing methods, expanding lactase enzyme applications across various alternative protein manufacturing processes. These combined factors increase the market demand for specialized lactase formulations that maintain stability during diverse processing conditions while meeting strict clean-label standards and consumer preferences.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in dairy supply impacting enzyme off-take | -0.3% | Global, with acute impact in regions with concentrated dairy production | Short term (≤ 2 years) |

| Regulatory hurdles on GMO-derived recombinant lactase | -0.3% | Europe and select Asia-Pacific markets | Medium term (2-4 years) |

| Allergen-labeling complexities in multi-enzyme blends | -0.2% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Price pressure from Chinese low-cost enzyme producers | -0.5% | Global, with highest impact in price-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Dairy Supply Impacting Enzyme Off-Take

Dairy supply chain disruptions create irregular demand patterns for lactase enzymes, as processors modify their production based on raw milk availability and price fluctuations rather than market demand. The integrated nature of global dairy markets means regional supply disruptions affect enzyme demand across multiple markets, creating inventory management challenges for manufacturers. Climate-related impacts on feed supplies and dairy herd productivity occur more frequently, requiring enzyme suppliers to implement flexible production and distribution models. The geographic concentration of dairy processing facilities intensifies this volatility, as regional disruptions significantly affect enzyme usage patterns. Enzyme manufacturers now require advanced forecasting systems and strategic inventory placement to maintain their market position during supply chain uncertainties.

Regulatory Hurdles on GMO-Derived Recombinant Lactase

The European Union's stringent evaluation process for genetically modified enzyme sources creates market access barriers that favor established players with regulatory expertise while limiting innovation from smaller biotechnology companies. The EFSA's 2024 evaluation framework for novel foods and food enzymes emphasizes comprehensive safety assessments that can extend approval timelines by 18-24 months compared to non-GMO alternatives. Regulatory complexity increases when enzymes are used in multi-enzyme blends, as each component requires individual assessment, and the interaction effects must be evaluated separately. The cost of regulatory compliance disproportionately impacts smaller enzyme manufacturers, potentially leading to market consolidation as companies seek scale advantages in regulatory affairs capabilities. Emerging markets are increasingly adopting European regulatory standards, expanding the geographic scope of these compliance challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Dominance Drives Processing Efficiency

Liquid lactase enzymes hold 48.45% market share in 2024, due to their effective integration in continuous dairy processing systems where precise dosing and rapid mixing are essential for product quality. The powder segment shows the highest growth rate at 7.12% CAGR during 2025-2030, benefiting from reduced transportation and storage costs, particularly among smaller dairy processors in emerging markets. Granular and immobilized enzyme forms serve specialized applications where extended activity and reusability offset higher initial costs, specifically in batch processing and specialty dairy products. The liquid segment maintains its market leadership through compatibility with automated dosing systems and immediate bioavailability, ensuring consistent lactose hydrolysis across production runs.

Immobilization technologies are changing the market dynamics between liquid and solid enzyme forms. Magnetic nanoparticle immobilization allows powder and granular enzymes to match liquid performance while retaining solid-form benefits. Electrospun fiber matrices provide enhanced mechanical stability and reusability compared to conventional methods, increasing the appeal of immobilized forms for industrial use. Cross-linked enzyme aggregates (CLEAs) technology enables efficient production of specialized enzyme forms, with magnetic CLEAs maintaining over 80% activity after thermal treatment.

By Source: Yeast-Derived Enzymes Lead Market Penetration

Yeast-derived lactase enzymes hold 55.67% of the market share in 2024, supported by well-established production infrastructure and widespread regulatory acceptance in major dairy markets. The fungal enzyme segment projects a 7.45% CAGR through 2030, driven by its enhanced thermal stability and pH tolerance, enabling use in demanding processing conditions. Recombinant and engineered lactase variants represent emerging technologies, with genetic modifications improving specific attributes like cold-active properties for refrigerated dairy processing. The regulatory approval of β-galactosidase from conventional sources, including Hamamotoa singularis strain YIT 10047, creates pathways for new enzyme variants while meeting clean-label requirements.

The market competition between yeast and fungal sources continues to evolve as processors require application-specific enzymes. Fungal enzymes gain market share in high-temperature processing applications, while yeast enzymes retain their position in conventional dairy processing. New β-galactosidase variants from Kluyvera intermedia show enhanced cold-temperature performance, reducing lactose to below 0.1 g/L within 72 hours at 8°C, compared to 192 hours for standard enzymes. Robot-assisted enzyme discovery systems accelerate the identification and analysis of new enzyme variants, potentially shifting established market preferences.

By Application: Dairy Processing Maintains Dual Leadership

Dairy processing applications hold a dominant 61.45% market share in 2024 and are projected to grow at 8.23% CAGR during 2025-2030, demonstrating both market leadership and growth potential. Cheese production represents the largest sub-segment, where lactase applications enhance texture and reduce processing time. Yogurt manufacturing shows significant growth driven by probiotic compatibility requirements. Ice cream production requires specialized enzyme formulations that maintain effectiveness at low temperatures while preventing crystallization issues. Specialty products, including lactose-free condensed milk and dairy-based infant formulas, comprise high-value niche applications subject to specific regulations.

The dietary supplements and pharmaceuticals segment maintains higher pricing despite lower volumes, due to strict purity standards and specialized therapeutic formulations. Pharmaceutical applications have expanded from basic lactase supplements to include enzyme-based treatments for digestive disorders and specialized medical foods. Multi-enzyme blends incorporating lactase create regulatory complexities while providing enhanced benefits for patients with multiple digestive sensitivities. Advanced fermentation technologies enable the production of pharmaceutical-grade lactase enzymes with consistent activity levels and lower immunogenic potential.

Geography Analysis

North America holds 33.67% market share in 2024, driven by well-established lactose-free product segments and regulatory frameworks that support enzyme use across dairy applications. The region's mature market enables premium pricing for specialized enzyme formulations, supported by robust distribution networks. The established market infrastructure facilitates efficient product development and commercialization processes. Strong consumer awareness and acceptance of lactose-free products further reinforce North America's market leadership.

Europe maintains its position as the second-largest market, with strict regulatory requirements favoring established enzyme suppliers who possess comprehensive safety documentation and clean-label capabilities. The European market's focus on sustainability drives demand for non-GMO enzymes and eco-friendly production methods. Regional preferences for natural and clean-label products influence enzyme formulation strategies. The presence of major dairy processors and enzyme manufacturers strengthens Europe's market position.

Asia Pacific shows the highest growth rate at 7.44% CAGR during 2025-2030, fueled by increased dairy consumption, growing lactose intolerance awareness, and improved retail infrastructure for lactose-free products. Japan's food processing industry, which saw production value decrease to USD 182 billion in 2023, maintains strength in dairy innovation and functional foods development, according to the United States Foreign Agriculture Services data[2]Source: United States Foreign Agriculture Services, "Food Processing Ingredients Annual", fas.usda.gov. China and India demonstrate significant growth potential due to urbanization and higher disposable incomes driving dairy consumption, combined with prevalent lactose intolerance patterns. South America and Middle East & Africa show growth opportunities as dairy processing infrastructure expands and lactose intolerance awareness increases.

Competitive Landscape

The lactase enzyme market maintains moderate consolidation, with established companies competing through technological differentiation and regulatory compliance. Market leaders implement innovation-focused strategies, as demonstrated by DSM-Firmenich's Maxilact®Next, the market's fastest pure lactase enzyme. This development illustrates how established companies address competition through enhanced product performance rather than price-based competition.

The market's competitive dynamics are influenced by new cost-reduction technologies, including enzyme immobilization on magnetic nanomaterials and improved bioreactor designs, which allow smaller manufacturers to achieve efficient production costs. The market shows two distinct strategic approaches: premium positioning through clean-label and specialty applications, and cost leadership through production efficiency and economies of scale. Growth opportunities exist in cold-active enzyme formulations for refrigerated dairy processing and multi-enzyme combinations that address complex digestive needs while meeting allergen labeling requirements.

The FDA's GRAS[3]Source: U.S. FDA, “GRAS Notice 1039 – Lactase from Aspergillus oryzae,” fda.gov approval of lactase enzyme from Aspergillus oryzae, with a no observed adverse effect level of 2000 mg/kg/day, provides a regulatory framework for new enzyme formulations. New market entrants utilize precision fermentation and synthetic biology to develop enhanced enzyme variants, while established companies maintain their position through regulatory knowledge and strong customer relationships.

Lactase Industry Leaders

-

Novozymes A/S

-

DSM-Firmenich

-

Kerry Group

-

International Flavors and Fragrances Inc.

-

Advanced Enzyme Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2023: Kerry Group plc acquired a portion of the global lactase enzyme business from Chr. Hansen Holding A/S and Novozymes A/S. The acquisition, which includes NOLA Products, strengthens Kerry's biotechnology solutions portfolio, building upon its previous acquisitions of c-LEcta and Enmex.

- June 2023: DSM-Firmenich, a Swiss-Dutch company, introduced Maxilact Next, expanding its Maxilact lactase enzyme product line. The new enzyme offers enhanced efficiency and purity compared to existing lactase products in the market.

Global Lactase Market Report Scope

| Liquid |

| Dry/Powder |

| Granular/Immobilise |

| Yeast |

| Fungi |

| Bacteria |

| Dairy Processing | Cheese |

| Yogurt | |

| Ice-Creams | |

| Other Dairy Products | |

| Dietary Supplements and Pharmaceuticals | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Rest of Asia Pacific | |

| South America | |

| Middle East and Africa |

| Form | Liquid | |

| Dry/Powder | ||

| Granular/Immobilise | ||

| Source | Yeast | |

| Fungi | ||

| Bacteria | ||

| Application | Dairy Processing | Cheese |

| Yogurt | ||

| Ice-Creams | ||

| Other Dairy Products | ||

| Dietary Supplements and Pharmaceuticals | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the lactase enzyme market?

The lactase enzyme market size is valued at USD 250.56 million in 2025, with strong growth projected through 2030.

Which application accounts for the largest share of the lactase enzyme market?

Dairy processing dominates, holding 61.45% of 2024 revenue and posting the fastest 8.23% CAGR forecast to 2030.

Why is Asia-Pacific considered the fastest-growing region?

The region combines rising per-capita dairy intake with a high prevalence of lactose intolerance, driving a 7.44% CAGR from 2025 to 2030.

How consolidated is the market?

A concentration score of 7 indicates that while leading firms dominate, emerging players still find room to compete through niche specialisation and innovation.

Page last updated on: